Carrier-Class Infrastructure A Platform Provider’s Perspective

www.drewry.co.uk

Transportation: New challenges and rising costs

RISI Asia Conference - Shenzhen23rd May 2017

Han Ning, Director, Drewry [email protected]

www.drewry.co.uk2

Agenda

• New challenges – Economy and trade

• New challenges – Shipping and supply chain

• Rising cost - Freight rate outlook

• Solutions

www.drewry.co.uk3

New challenges - World Trade FlaggingContainer shipping volumes being disrupted

-9%

-4%

1%

6%

11%

16%

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

Container trade growth

Global GDP growth

Avg GDP multiplier = 1.4 (2008-16)Avg GDP multiplier = 3.2 (1980-07)

Ratio of world merchandised trade volume growth to world real GDP growth, 1981-2016

www.drewry.co.uk4

New challenges - World Trade FlaggingDrivers of trade deceleration

Global Trade

Nearshoring / regionalisation

Product Miniaturisation

Digital Disrupters

3D/4D Printing

Protectionism

Economic Growth

www.drewry.co.uk5

New challenges - World Trade FlaggingIncreasing trade barriers can distort the existing trade flows

• During 2016, a total of 2,336 notifications related to standards and regulations were submitted by79 WTO members, the highest number of notifications submitted in one year in theCommittee's history.

WTO committee on technical barriers to trade, 1995-2016

www.drewry.co.uk6

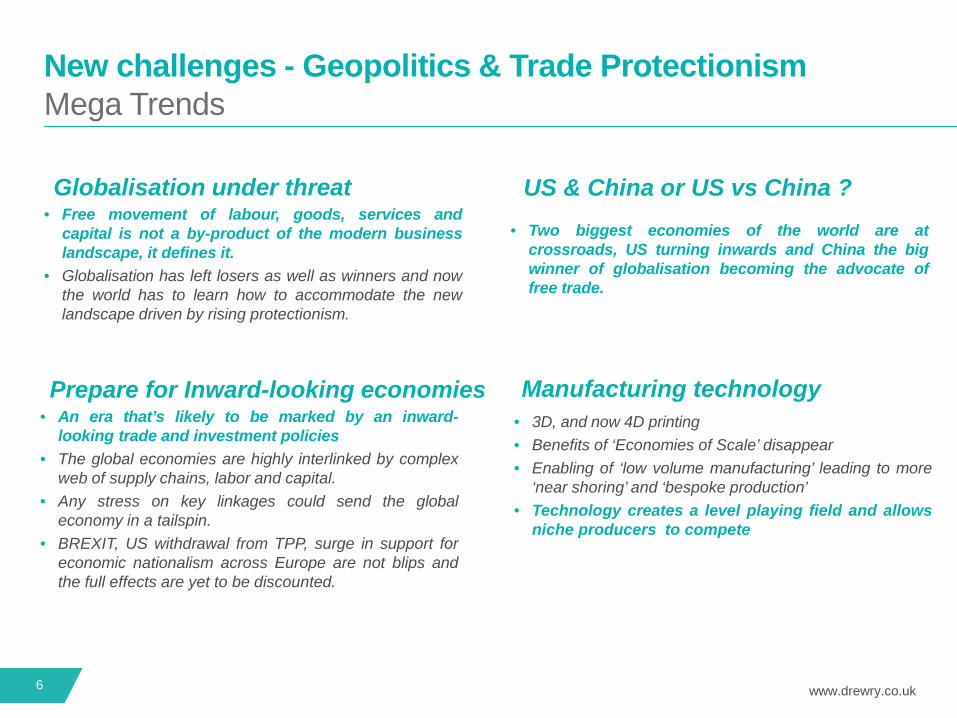

New challenges - Geopolitics & Trade ProtectionismMega Trends

• 3D, and now 4D printing• Benefits of ‘Economies of Scale’ disappear• Enabling of ‘low volume manufacturing’ leading to more

‘near shoring’ and ‘bespoke production’• Technology creates a level playing field and allows

niche producers to compete

Manufacturing technology

Globalisation under threat• Free movement of labour, goods, services and

capital is not a by-product of the modern businesslandscape, it defines it.

• Globalisation has left losers as well as winners and nowthe world has to learn how to accommodate the newlandscape driven by rising protectionism.

Prepare for Inward-looking economies• An era that’s likely to be marked by an inward-

looking trade and investment policies• The global economies are highly interlinked by complex

web of supply chains, labor and capital.• Any stress on key linkages could send the global

economy in a tailspin.• BREXIT, US withdrawal from TPP, surge in support for

economic nationalism across Europe are not blips andthe full effects are yet to be discounted.

US & China or US vs China ?• Two biggest economies of the world are at

crossroads, US turning inwards and China the bigwinner of globalisation becoming the advocate offree trade.

www.drewry.co.uk7

Agenda

• New challenges – Economy and trade

• New challenges – Shipping and supply chain

• Rising cost - Freight rate outlook

• Solutions

www.drewry.co.uk8

To evaluate a logistics provider’s service

Service provider

Market concentration

Product diversifi-

cation

Cost competitive-

ness

Financial robustness

Schedule reliability

Service quality

www.drewry.co.uk9

New challenges - Increasing market concentrationLower return drives liner consolidation

Source: Drewry’s Container Forecaster (www.drewry.co.uk/research)

Operational consolidation through alliances

2MExpiration date: Jan 2025

Ocean 3Expiration date: Sep 2016

G6Expiration date: Mar 2017

CKYHEExpiration date: Feb 2018

HMM joins 2M

Three alliances re-shaping into two

Ocean AllianceStarting date: April 2017

THE AllianceStarting date: April 2017

NewOld

www.drewry.co.uk10

Impact to shippersShippers are left with 3 alliances only. • Less vendor, less bargain power• Less port pairs available• Capacity management / manipulation could be a major threat• There is also concern of product diversification – port calls, routing, network,

frequency, etc.

www.drewry.co.uk11

New challenges – Liner’s financial stress concernLower world trade growth has impacted financial returns

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4Q08 4Q09 4Q10 4Q11 4Q12 4Q13 4Q14 4Q15

Average Z-Scores of Logistics Providers (2008-16)

-4 -2 0 2 4 6 8

Hanjin ShippingZim

Yang MingHyundai Merchant Marine

China Cosco (parent of…CEVA Logistics

Evergreen Marine CorpCMA CGM

MOL groupPacific International Lines

NYK groupRegional Container Lines

K Line groupMatson, Inc.

Hapag-Lloyd HoldingWan Hai

OOIL (parent of OOCL)AP Moller-Maersk

Deutsche Post DHLAgility

UPSKuehne + NagelSeaboard Corp.…

PanalpinaExpeditors International

CH Robinson

Logistics Providers’ Z-Scores

Forwarders have a “safe” Z score (>2.99)Maersk and OOCL have a “grey” Z score (1.8-2.99)All other ocean carriers who report financial results have a “risky” Z scoreHanjin (based on previous data) was by far the riskiest

www.drewry.co.uk12

Impact to shippers – Hanjin caseShippers were facing a chaotic situation.Hanjin was the seventh largest in the world before filing for court receivership. The company’s collapse resulted in hundreds of thousands of shipments around the world being delayed (est. 540k teu) . Shippers were facing a chaotic situation and supply chains seriously disrupted:

‒ Some ships were sized in Asia, Europe and N. America. Uncertain of those ships still en-route.

‒ Some ports immediately refused to handle Hanjin vessels, and charged high release fee.

‒ Depending on contract terms, shipowners terminated ship leases and demanded return of ships.

‒ Some Hanjin agents closed their doors immediately.‒ Hanjin offices were unable to provide update information. Customer service

hotlines jammed.‒ Hanjin’s alliance partners’ containers on Hanjin ships were affected in the same

way.‒ Many cargo missed the Christmas sales. Buyers threatened refusal of goods.‒ A lot of cargoes have been diverted to air freight in the months afterwards.‒ Shippers were responsible for all the costs.

www.drewry.co.uk13

Agenda

• New challenges – Economy and trade

• New challenges – Shipping and supply chain

• Rising cost - Freight rate outlook

• Solutions

www.drewry.co.uk14

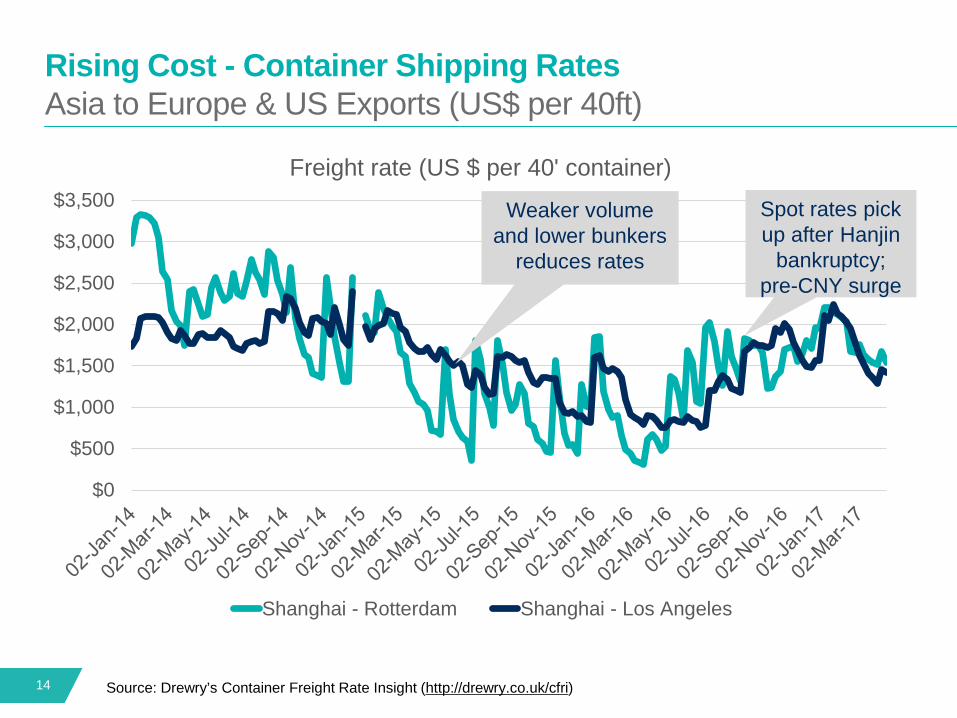

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500Freight rate (US $ per 40' container)

Shanghai - Rotterdam Shanghai - Los Angeles

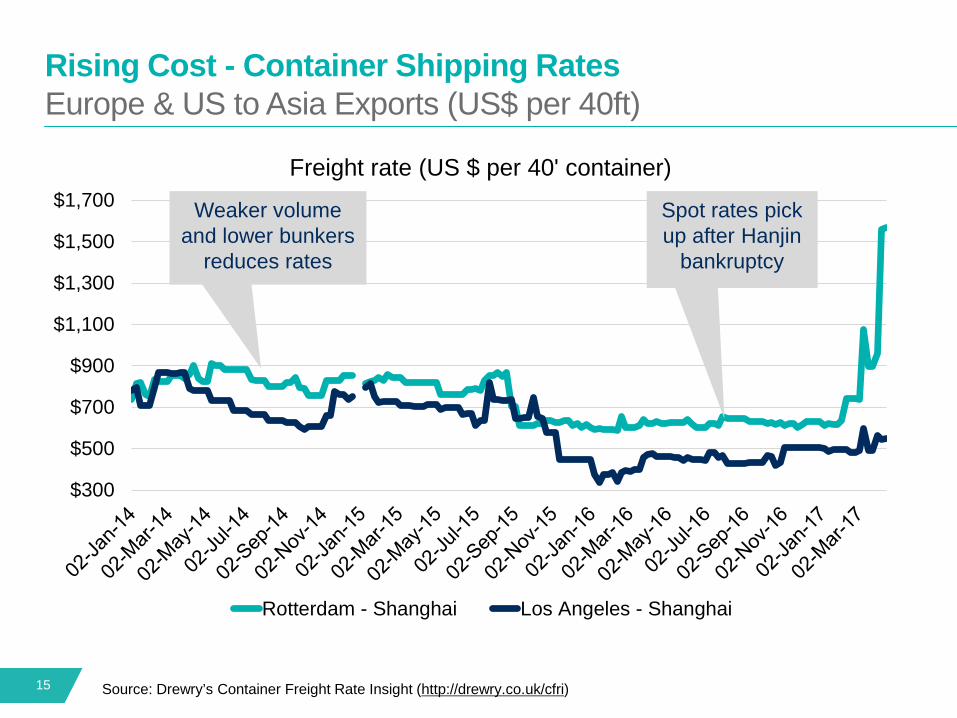

Rising Cost - Container Shipping RatesAsia to Europe & US Exports (US$ per 40ft)

Weaker volume and lower bunkers

reduces rates

Spot rates pick up after Hanjin

bankruptcy; pre-CNY surge

Source: Drewry’s Container Freight Rate Insight (http://drewry.co.uk/cfri)

www.drewry.co.uk15

$300

$500

$700

$900

$1,100

$1,300

$1,500

$1,700Freight rate (US $ per 40' container)

Rotterdam - Shanghai Los Angeles - Shanghai

Rising Cost - Container Shipping RatesEurope & US to Asia Exports (US$ per 40ft)

Weaker volume and lower bunkers

reduces rates

Spot rates pick up after Hanjin

bankruptcy

Source: Drewry’s Container Freight Rate Insight (http://drewry.co.uk/cfri)

www.drewry.co.uk16

Rising Cost - Logistics Costs & RisksPerfect storm of trade & supply-side impacts

Trade & Regulatory

Uncertainties

Tightening Shipping Capacity

Diminishing Economies of

Scale

Provider Consolidation

Oil Prices

Costs & Risks

www.drewry.co.uk17

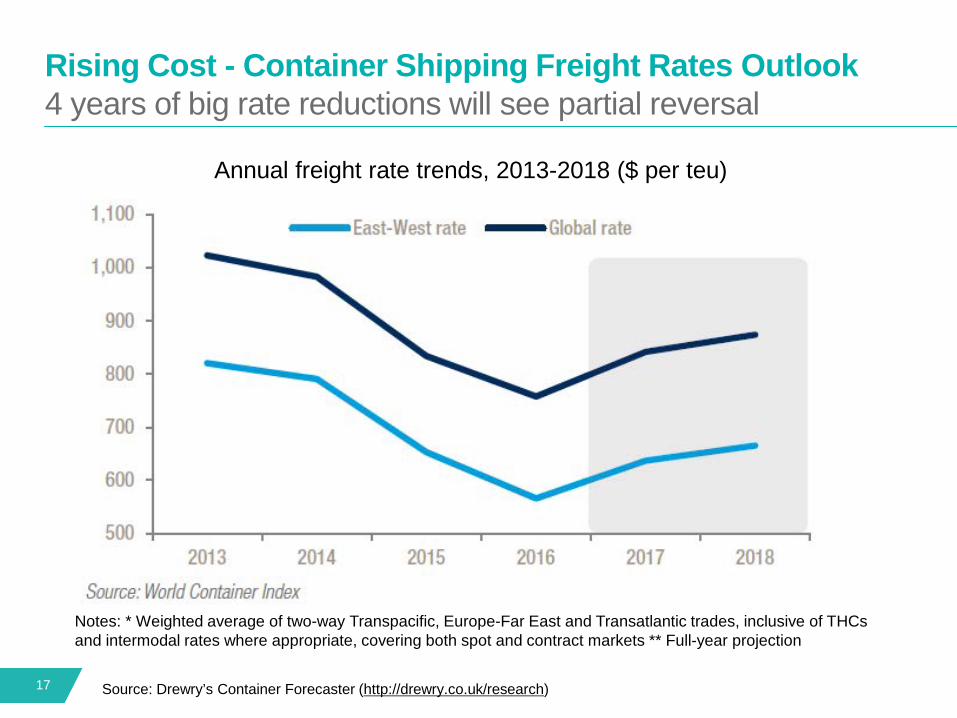

Rising Cost - Container Shipping Freight Rates Outlook4 years of big rate reductions will see partial reversal

Source: Drewry’s Container Forecaster (http://drewry.co.uk/research)

Notes: * Weighted average of two-way Transpacific, Europe-Far East and Transatlantic trades, inclusive of THCs and intermodal rates where appropriate, covering both spot and contract markets ** Full-year projection

Annual freight rate trends, 2013-2018 ($ per teu)

www.drewry.co.uk18

Rising Cost - Break Bulk Vessel TC Rates

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

usd

$ pe

r day

Time charter rate

<4,000 dwt 7,500-9,999 dwt 10,000-14,999 dwt 15,000-19,999 dwt

www.drewry.co.uk19

88

93

98

103

108

113

118

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Supply Demand Balance

Supply Demand Balance

Rising Cost - Break Bulk Shipping Freight Rates Outlook Capacity conditions to tighten (Index: 100 = 2007)

Source: Drewry’s Multipurpose Shipping Forecaster (http://drewry.co.uk/research)

www.drewry.co.uk20

Agenda

• New challenges – Economy and trade

• New challenges – Shipping and supply chain

• Rising cost - Freight rate outlook

• Solutions

www.drewry.co.uk21

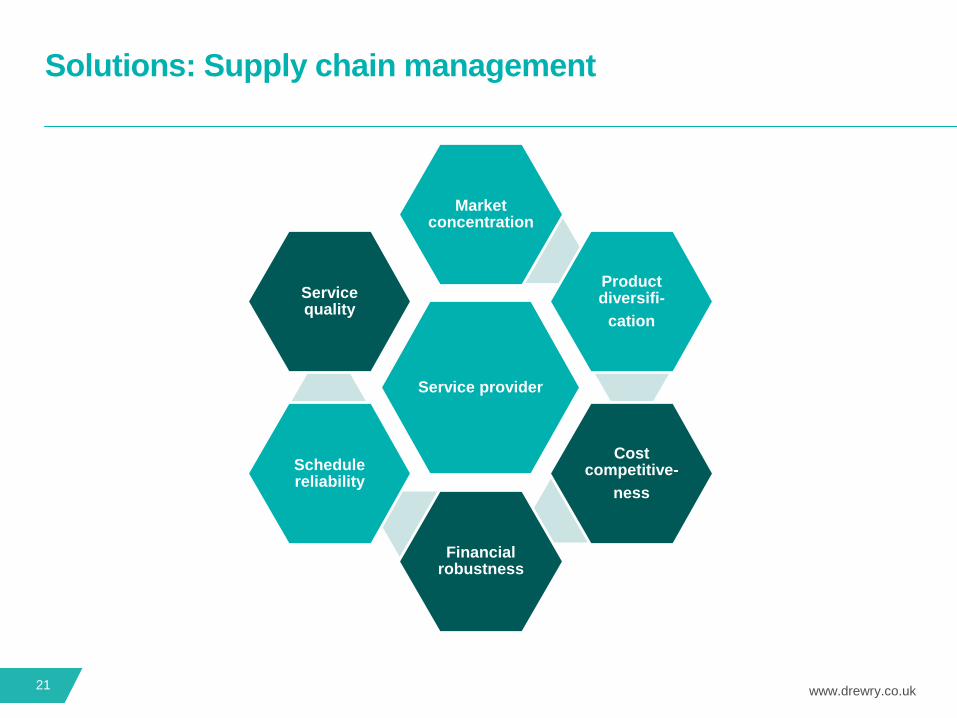

Solutions: Supply chain management

Service provider

Market concentration

Product diversifi-

cation

Cost competitive-

ness

Financial robustness

Schedule reliability

Service quality

www.drewry.co.uk22

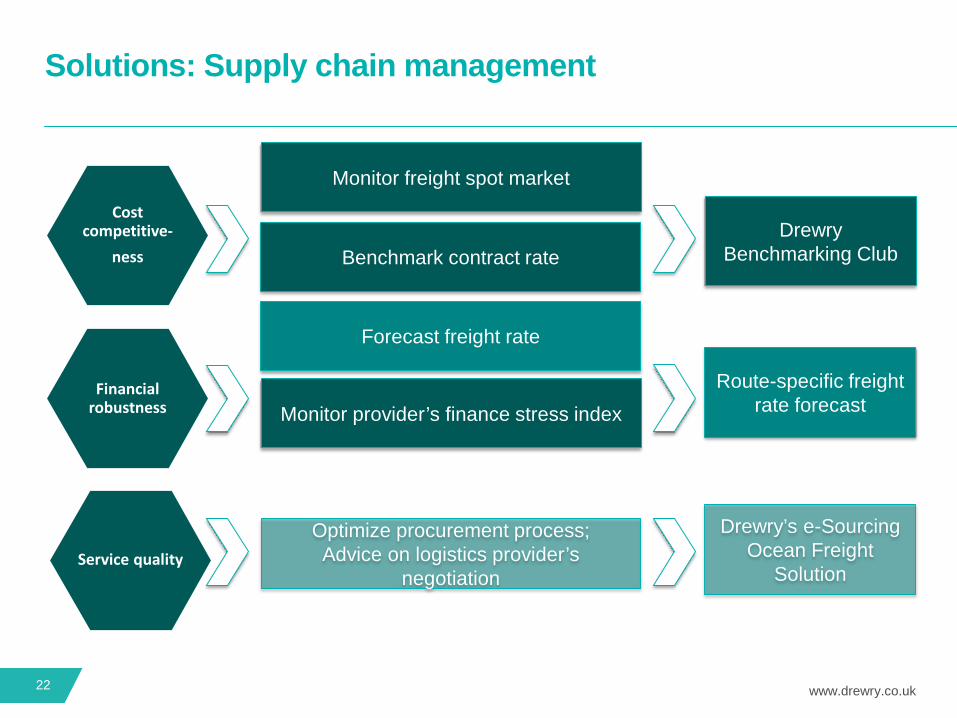

Solutions: Supply chain management

Optimize procurement process; Advice on logistics provider’s

negotiation

Monitor freight spot market

Benchmark contract rate

Forecast freight rate

Monitor provider’s finance stress index

DrewryBenchmarking Club

Route-specific freight rate forecast

Drewry’s e-Sourcing Ocean Freight

SolutionService quality

Financial robustness

Cost competitive-

ness

www.drewry.co.uk23

Remedies: Benchmark CostsConfidentially benchmark contract shipping costs against peers

www.drewry.co.uk24

Solutions: Seek Advice With Logistics Provider NegotiationsDrewry’s e-Sourcing Ocean Freight Solution

ExecutionTools, Resources, EventsAdvisory services

Design & Manage e-Sourcing

Optimization Event

Analyse historical Costs & Service vs spot, contracts and

future trends

Conduct Competitive

e-Sourcing event

Perform real-time analysis

Design go forward plan

Audit & Review

Map & Measure CurrentServices

Compare vs Market actuals

Obtain global Agreement &

Implement decisions

Monitor contracts

Design & Measure carrier

performance KPIs

Jointly Manage QBR’s

Measuresavings &

performance

Train for next event

Implement Audit Optimize

Provide advice on e-Sourcing Optimization

Evaluate Current &

Future MarketplaceDynamics

www.drewry.co.uk25

Conclusions

• Globalisation under threat, get prepared for Inward-looking economies

• Slowing world trade & excess capacity are diminishing logistics provider returns

• Lower return drives liner consolidation, and shippers are left with less choice

• Increasing risk of failure amongst top shipping providers

• Shipping freight rate is rising. Latest global container spot rate forecasts for 2017 is a rise of 12.3% on average

• Cost effective freight rate procurement and making the right carrier selections are critical to mitigate these risks

www.drewry.co.uk

UK

15-17 Christopher StreetLondonEC2A 2BSUnited Kingdom

INDIA

209 Vipul SquareSushant Lok - 1Gurgaon 122002India

SINGAPORE

#13-02 Tower Fifteen15 Hoe Chiang RoadSingapore 089316

CHINA

Unit D01, Level 10,Shinmay Union Square Tower 2, 506 Shang Cheng RoadPudong, Shanghai 200120

T +44 20 7538 0191 T +91 124 497 4979 T +65 6220 9890 T +86 21 5081 0508