Transforming the Payment Landscape in Malaysia - FST...

18

1 Transforming the Payment Landscape in Malaysia 4th Annual Technology and Innovation – the Future of Banking and Financial Services Tan Nyat Chuan Bank Negara Malaysia 10 May 2016

Transcript of Transforming the Payment Landscape in Malaysia - FST...

1

Transforming the Payment Landscape in Malaysia

4th Annual Technology and Innovation – the Future of Banking and

Financial Services

Tan Nyat Chuan

Bank Negara Malaysia

10 May 2016

2

Presentation Outline

1

2

3

Role of Bank Negara Malaysia (BNM) in payment systems

Roadmap to transform Malaysia’s payment landscape in the Financial Sector

Blueprint (2011-2020)

Strategy to accelerate migration to e-payments

• Electronic fund transfer to displace cheque

• Debit card to displace cash

3

To ensure safety, reliability and

efficiency of payment systems and

payment instruments

1 Operator

of large-value

payment system

(LVPS)*

*through BNM’s wholly

owned subsidiary, MyClear

To exercise oversight over payment

system Central Bank Act of Malaysia 2009

Financial Services Act 2013

Islamic Financial Services Act 2013

To promote monetary and financial stability by assuming the following roles:

BNM’s role as overseer of payment systems

2 Overseer

• Ensure payment

system is safe,

efficient and reliable

• Identify and manage

potential risks

3 Facilitator

• Accelerate migration

to e-payments

• Initiate

improvements in

payment services

4

Proportionate regulatory approach to foster innovation whilst

managing risk in payment systems

Evolution of payment system legal framework

• Existing legal framework supported the involvement of banks and non-banks in providing

value-adding payment services.

• Proportionate risk management measures to commensurate with the risk posed by the

players to users and the financial system.

• Promoting standardization and collaboration to foster interoperability and innovation.

1989

Banking and Financial

Institution Act (BAFIA)

Payment system provision in

the banking law

2003

Payment System Act (PSA)

Single dedicated law to

govern payment systems

and instruments

2013

Financial Services Act (FSA)

Islamic Financial Services

Act (IFSA)

)

Omnibus legislation on

financial services regulation

including the area of payment

system

5

Unit cost to the banking industry

Cash withdrawal

• ATM: RM1.20

(up to RM2.50)

• OTC: RM5.30

(up to RM6.80)

Cash deposit

• CDM: RM1.60

(up to RM3.77)

• OTC: RM5.50

(up to RM8.80)

Wholesale cash

handling1

• RM5.60

(up to RM7.60)

Cheque

processing

• RM3.10

(up to RM6.00)

1 Cost of wholesale cash handling comprises the cost of armoured truck services (excluding ATMs), cash storage and rental, float, cash

processing and sorting, insurance and fraud, theft and counterfeit losses. 2 Management Information System

• Focusing on ROI and fee income in the short-term may stifle the growth of e-payments,

while banks continue to incur substantial cost in handling cash and cheques.

• Instead of focusing on short-term ROI, banks should have better MIS and coordinated

revenue and expenditure strategies to achieve optimal financial performance.

Substantial potential for cost savings through displacement of cash

and cheques

6

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

2016 to 2020

• Strengthening coordination and alignment to

drive achievement of e-payment targets

• Continuous infrastructure enhancement to

keep pace with innovation and meet user

needs

2011 to 2015

• Strengthening regulatory frameworks,

addressing market distortions and establishing

incentive structures

• Expanding and enhancing market infrastructure

• Promoting awareness and instilling confidence

Fostering an enabling environment for accelerated migration

Measurable targets to be achieved by 2020

Indicators E-payments per

capita

Cheques cleared

(mil)

Card terminals per

1,000 inhabitants

Debit card trxn

per capita

2011 49 205 7 1

2015 82 148 9 3

2020 target 200 100 25 30

Financial Sector Blueprint 2011-2020 sets the direction for Malaysia’s

payment landscape

7

Key instruments

Electronic fund transfer

(to displace cheques)

Price signal

Debit card

(to displace cash)

IBG (30 banks with 99% CASA1 base)

IBFT (20 banks with 98% CASA base)

43 million debit cards

(for 19 mil bankable population2)

5 focus areas

Industry

incentive

structure

Access points

Quality and

value

proposition

Awareness

and

confidence

• The strategy is to leverage on and strengthen existing payment infrastructures which are

cost-effective and widely available to minimise duplicative investment cost.

1 Total number of current and savings accounts 2 Estimated based on the findings of the Financial Inclusion Demand-Side Survey which

found that about 92% of individuals aged 15 and above have a deposit account

Key instruments and focus areas

8

Cheques

IBG

0

2

4

6

8

10

12

14

16

18

20

J M M J S N J M M J S N J M M J S N J M M J S N J M M J S N

Million

2015 2014 2013 2012 2011

IBFT

Pricing Reform Framework

2 May 2013

Reduction of IBG fee and

introduction of cheque processing

fee.

IBG: 10 sen

Cheque: 50 sen (2 Jan 2015)

E-payment Incentive Fund

Framework

2 Jan 2015

Framework that allows fund to be

channeled to e-payment user

Tiered pricing structure and

disclosure requirement

1 Oct 2014

E-payment services priced based

on channels; and

Disclosure of e-payment fee

IBFT fee reduction

1 June 2015

IBFT fee is reduced from

between RM1 – RM4 to

50 sen

Cheques, IBG and IBFT

Transaction Volume

Strengthening regulatory framework and improving price signal

9

1. Banks to fulfil a

set of e-payment

prerequisites

100% of cheque fee collected

50% of cheque fee collected

ePIF account

2. Banks to utilise ePIF

funds to incentivise e-

payment adoption

Eligible incentives Individual banks’

customers

Funds collected will be used to provide the following incentives:

Waiver of security token and monthly maintenance fees

Waiver/discounts on e-payment transaction fee

Incentives for government payments using debit card

Other eligible expenses

ePIF account

Pre-requisites

NOT fully met

Pre-requisites

fully met

E-Payment Incentive Fund (ePIF) Framework:

A market driven framework to sustain the improvements in the

e-payment infrastructure and services

Market incentives structure to sustain improvement in infrastructure

and services

10

Internet banking

• IBG offered by 30 banks

(99% of CASA base)

• IBFT offered by 20 banks

(98% of CASA base)

Increased

access

points

Value

added

features

Safety and

security

Faster crediting time

• IBG payments before 5pm

credited on same business day

• IBFT payments credited

instantaneously

Safeguard against mistaken

payment

• IBG (online): I/C and

company no. verification

• IBFT: Beneficiary name

displayed before payment

confirmation

ATMs

• IBG offered at 11,356 ATMs

• IBFT offered at 12,287 ATMs

Payment details to facilitate

reconciliation

• Payer and beneficiary account

statement

BNM holds banks

responsible for-

• Ensuring security of

e-payment services

• Educate customers on

safety measures

Future-dated IBG services

• Offered by 24 out of 30 banks

(99% of cheque volume)

Enhancing access, quality and confidence

11

Policy objectives

• Curb indiscriminate increases in interchange fees

• Address market distortions to enhance payment efficiency and competition

1

2 Key measures

• Interchange fee ceilings

• Greater transparency in card acceptance cost

Unbundling of MDR for different payment card transactions

Disclosure of MDR and IF rates in merchant statements

• Empowering merchants to manage their card acceptance cost

Empowering merchants to steer customers to use cost-effective payment

cards (including setting priority routing for co-badged debit cards)

Facilitate identification of debit and prepaid cards

Payment Card Reform Framework (PCRF) to drive greater usage and

acceptance of debit cards

12

Risk of retail price increase due to interchange fee (IF) hikes

Payment

Network A

increased IF

Issuers lowered

income eligibility for

premium cards

May 2013 Feb 2014 June 2013 onwards

Acquirers

increased

MDRs

Card Type

Payment Network A Payment Network B

Before

1 May 13

Effective

1 May 13

Effective

14 Jun 14*

Before

1 Mar 14

Effective

1 Mar 14

Credit Card 1.1% 1.32% - 1.80% 1.32% - 1.85% 1.2% 1.2% - 1.8%

Debit Card 1.1% 1.1% 0.99% - 1.45% 1.15% 0.9% - 1.1%

April 2014

Payment Network A

announced further

IF hikes*

(unwound after

BNM’s engagement)

March 2014

Payment

Network B

increased IF

• Cost of higher IF is passed to merchants in the form of higher MDR.

• Merchants are pressured to pass on the higher cost to consumers by raising retail prices.

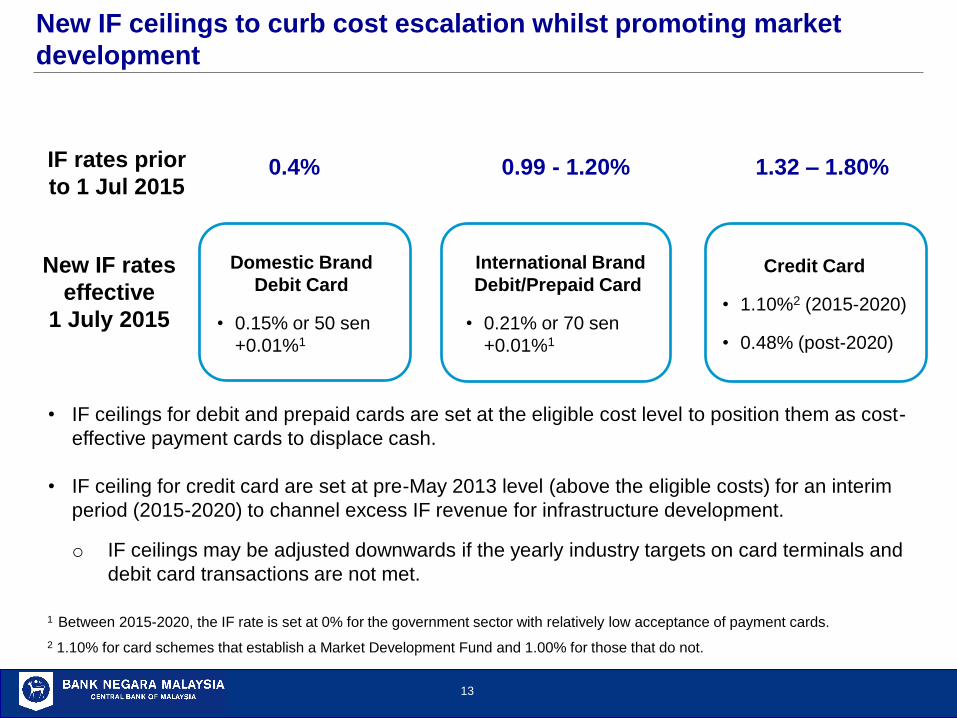

13

0.4% 0.99 - 1.20% 1.32 – 1.80% IF rates prior

to 1 Jul 2015

New IF rates

effective

1 July 2015

1 Between 2015-2020, the IF rate is set at 0% for the government sector with relatively low acceptance of payment cards.

2 1.10% for card schemes that establish a Market Development Fund and 1.00% for those that do not.

Domestic Brand

Debit Card

• 0.15% or 50 sen

+0.01%1

International Brand

Debit/Prepaid Card

• 0.21% or 70 sen

+0.01%1

Credit Card

• 1.10%2 (2015-2020)

• 0.48% (post-2020)

• IF ceilings for debit and prepaid cards are set at the eligible cost level to position them as cost-

effective payment cards to displace cash.

• IF ceiling for credit card are set at pre-May 2013 level (above the eligible costs) for an interim

period (2015-2020) to channel excess IF revenue for infrastructure development.

o IF ceilings may be adjusted downwards if the yearly industry targets on card terminals and

debit card transactions are not met.

New IF ceilings to curb cost escalation whilst promoting market

development

14

PCRF facilitates greater transparency and merchant empowerment in

card acceptance

Greater

transparency in

card acceptance

cost

Empowerment of

merchants to

accept the lower

cost card or

network

• Separate MDR for different

payment card and network

• Disclosure of MDR and IF in

merchant statement

• Notification on IF and MDR

reduction or reason for lack

thereof

• Merchants empowered to set priority routing to the preferred

debit card network

• Merchants empowered to steer cardholder to use lower cost

card or network

• Enhancement of debit and prepaid card design to facilitate

identification

15

Existing Debit / ATM cards New Debit / ATM cards

Domestic brand logo is displayed at the

back of the card due to restrictive rules

by international card schemes

1. Contactless function

2. Debit card brands displayed on the

front of the card.

• MyDebit will replace MEPS &

Bankard logo

3. ‘Debit’ imprinted on the front of the

card

1

2

3

Standalone Co-badged

with 2 debit brands Co-badged with 2 debit brands

Note: The display of payment card is for illustration purpose only and does

not represent an endorsement of any particular bank or payment card brand.

Facilitating identification of debit cards

16

Contactless debit card initiative (MCCS1)

Chip & PIN initiative

July 2015 2016 2017 2018 2019 2020

Deployment of 560,000 POS terminals (min. 30% contactless)

Increase debit card transactions to 1 billion per year

1 Under the Malaysian Chip Card Initiative, the domestic debit card (MyDebit) will migrate from its existing proprietary standard (PMPC) to adopt the

EMV standard and the contactless functionality.

+

EMV +

RM1.1 billion to be invested by the industry for infrastructure

development

17

Market Development Fund (MDF) to support expansion of card

terminals

• PCRF provides payment card schemes with the option of establishing a MDF to support

the deployment of new card terminals.

• Two major payment card schemes have established the MDF, which is expected to

channel approximately RM 455 million towards expanding the card network until 2020.

Interchange fee

Issuer A

Issuer A’s MDF funds

for terminal

deployment

0.1% of the value of

credit card transaction

Under-achievement of

Issuer A’s individual

target for terminal

deployment

Disburse pro-rated

MDF funds into a

pooled account

Pooled MDF

account

Funds available to

issuers who are able

to cover the shortfall

in POS terminal

deployment

1 2 3

18

Thank you