Transfer Pricing Draft Guidelines – Part 2 Pricing Draft Guidelines – Part 2 ... Profit split...

28

Transfer Pricing Draft Guidelines – Part 2 A guide to the application of section GD 13 of New Zealand’s Income Tax Act 1994 This appendix contains the second part of a series of draft guidelines on New Zealand’s transfer pricing rules. The first part, issued in October 1997, contained a general overview of the framework in which transfer pricing operates. This part deals with the remaining issues covered in the OECD guidelines issued to date, namely intangible property, intra-group services and cost contribution arrangements (CCAs). Subsequent guidelines will deal with advance pricing agreements (APAs) and the application to branches of section FB 2 of the Income Tax Act 1994. Inland Revenue welcomes submissions on the material in this part of the draft guidelines. Please make these by 31 March 2000, addressed to: General Manager Policy Advice Division Inland Revenue Department PO Box 2198 WELLINGTON Inland Revenue fully endorses the OECD guidelines in relation to issues dealt with in this part of the guidelines. This part should be read, therefore, as supplementing the OECD guidelines, rather than superseding them. On matters not addressed in draft guidelines issued to date, Inland Revenue will continue to follow the OECD guidelines. This document is also available on the Internet. Visit Inland Revenue’s website at http://www.ird.govt.nz and choose the Tax Information Bulletin section. The document is listed as an appendix to TIB Volume Twelve, No.1 (January 2000) Inland Revenue Te Tari Taake

Transcript of Transfer Pricing Draft Guidelines – Part 2 Pricing Draft Guidelines – Part 2 ... Profit split...

Transfer PricingDraft Guidelines – Part 2

A guide to the application of section GD 13of New Zealand’s Income Tax Act 1994

This appendix contains the second part of a series of draft guidelines on New Zealand’s transferpricing rules. The first part, issued in October 1997, contained a general overview of the frameworkin which transfer pricing operates. This part deals with the remaining issues covered in the OECDguidelines issued to date, namely intangible property, intra-group services and cost contributionarrangements (CCAs). Subsequent guidelines will deal with advance pricing agreements (APAs) andthe application to branches of section FB 2 of the Income Tax Act 1994.

Inland Revenue welcomes submissions on the material in this part of the draft guidelines. Pleasemake these by 31 March 2000, addressed to:

General ManagerPolicy Advice DivisionInland Revenue DepartmentPO Box 2198WELLINGTON

Inland Revenue fully endorses the OECD guidelines in relation to issues dealt with in this part of theguidelines. This part should be read, therefore, as supplementing the OECD guidelines, rather thansuperseding them. On matters not addressed in draft guidelines issued to date, Inland Revenue willcontinue to follow the OECD guidelines.

This document is also available on the Internet. Visit Inland Revenue’swebsite at http://www.ird.govt.nz and choose the Tax Information

Bulletin section.

The document is listed as an appendix to TIB Volume Twelve, No.1(January 2000)

Inland RevenueTe Tari Taake

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

2

Contents

References in this table of contents are to paragraph numbers, not page numbersAll section references in these guidelines are to the Income Tax Act 1994

PrefaceIntroduction ............................................................. 1

Inland Revenue’s approach to this part ofguidelines ................................................................ 2

Scope ....................................................................... 5

Application of section FB 2 to branches ................. 6

Submissions on Part 1 of guidelines ..................... 11

Intangible propertyIntroduction ........................................................... 13

Identifying types of intangible property ................ 26

Applying arm’s length principle ........................... 32

Ascertaining what the transaction involves ........... 36

Ownership of intangible property ......................... 40

Factors in pricing .................................................. 44

Terms and conditions of transfer ........................... 50

Calculating arm’s length price .............................. 55

Comparability ....................................................... 61

Profit split method ................................................. 71

Valuation-based approach to intangible property . 79

Applying a valuation-based approach ................... 82

Observations on valuation approach ..................... 87

Valuation highly uncertain at time of transaction . 95

Use of standard international royalty rate ........... 101

Marketing activities of enterprise not owningmarketing intangible ........................................... 108

Allocating return attributable to marketingintangibles ........................................................... 117

Summary ............................................................. 119

Intra-group servicesIntroduction ......................................................... 120

Key issues in intra-group services ....................... 124

Has a service been provided? .............................. 125

Determining an arm’s length charge ................... 128

Applying a pricing method ................................. 134

Profit element ...................................................... 140

Determining the cost base for cost-plus method . 142

Global formula approach..................................... 148

Time expended .................................................... 152

Income producing units ....................................... 156

Gross profit allocation basis ................................ 160

Other methods ..................................................... 162

Pitfalls and potential audit issues ........................ 163

Administrative practice for services .................... 166

Caveat to administrative practice ........................ 174

Practical solutions ............................................... 177

Summary ............................................................. 179

Cost contribution arrangements(CCAs)

Introduction ......................................................... 180

Applying arm’s length principle to CCAs........... 187

Identification of participants ............................... 190

Amount of participant’s contribution .................. 194

Appropriateness of allocation ............................. 198

Balancing payments ............................................ 200

Tax treatment of contributions and balancingpayments ............................................................. 201

Conclusions of applying arm’s length principleto CCAs............................................................... 204

Structure of CCA ................................................ 206

Summary ............................................................. 207

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

3

PREFACE

Application of section FB 2 to branches6. Inland Revenue has received several commentsexpressing concern that no guidance has been issued todate on the application of section FB 2 to branches.

7. Section FB 2 was intentionally drafted to parallelthe wording contained in Article 7 of the OECD ModelTax Convention, and in particular that part of Article7(2) that attributes to a permanent establishment:

“... the profits which it might be expected to make if it were adistinct and separate enterprise engaged in the same or similaractivities under the same or similar conditions and dealingwholly independently with the enterprise of which it is apermanent establishment.”

8. The drafting of section FB 2(1) follows closelythat of the OECD, because of New Zealand’s policy offollowing, in relation to branches, the positionestablished by the OECD for permanent establishments.

9. The OECD is continuing to work on developingguidelines on the application of the arm’s lengthprinciple to permanent establishments. Inland Revenue’sguidelines will follow the OECD position, once it isfinalised and published.

10. In the interim, Inland Revenue will continue tofollow the OECD’s current published position on theissue, set out in the loose-leaf version of the OECD’sModel Tax Convention on Income and on Capital(November 1997), specifically, the:

• Commentary on Article 7 (Business Profits) involume 1; and

• Report on the Attribution of Income to PermanentEstablishments in volume 2.

Submissions on Part 1 of guidelines11. Submissions have been received on Part 1 of thetransfer pricing guidelines, released in draft as anappendix to Tax Information Bulletin Vol. 9 No.10(October 1997).

12. Submissions have not identified any areas wherea substantive revision of the draft will be required. It isproposed, therefore, that a further draft of Part 1 will notbe prepared for release at this stage. Instead, it isplanned to issue a final version later this year,incorporating the final version of the material included inthis draft and on APAs.

Introduction1. This is the second part in the series of guidelineson New Zealand’s transfer pricing rules. The first part, adraft of which was issued in October 1997, contained ageneral overview of the framework in which transferpricing operates. This part deals with the remainingissues covered in the OECD guidelines issued to date,namely intangible property, intra-group services and costcontribution arrangements (CCAs). Subsequentguidelines will deal with advance pricing agreements(APAs), and the application of section FB 2 to branches.

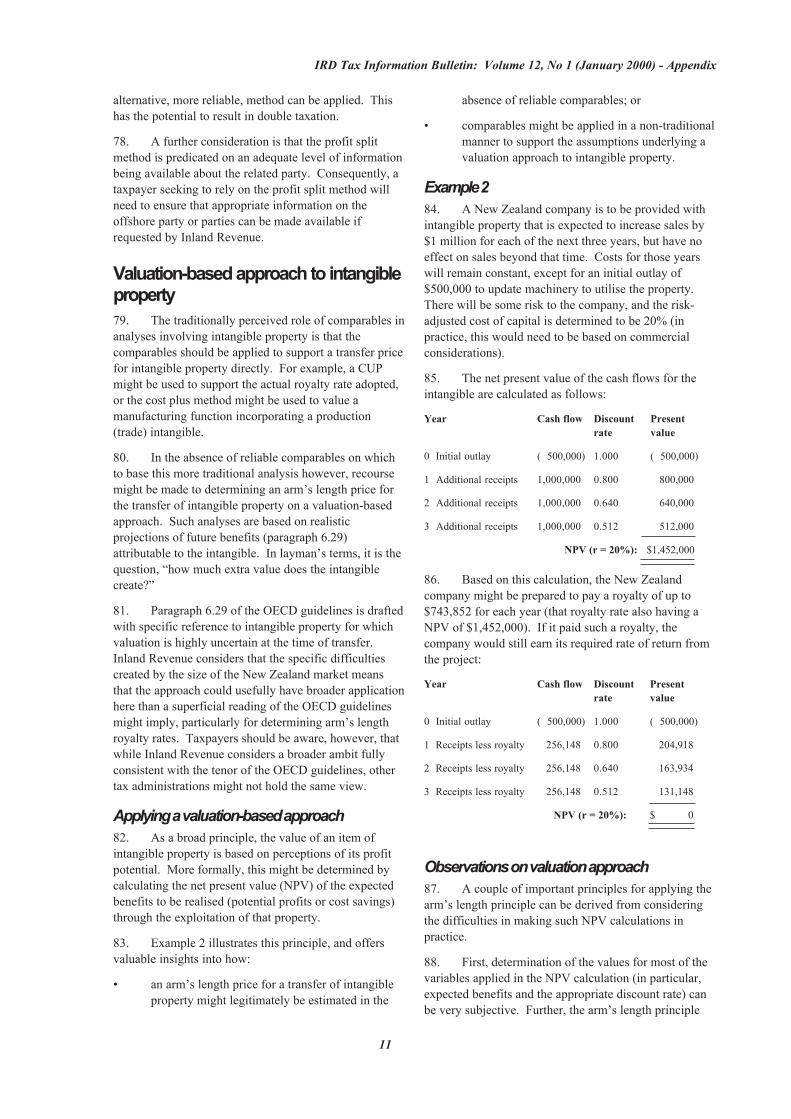

Inland Revenue’s approach to this partof guidelines2. This part of the guidelines deals with material ofa specialised nature covered in chapters 6 to 8 of theOECD Transfer Pricing Guidelines for MultinationalEnterprises and Tax Administrations (referred to in theseguidelines as the “OECD guidelines”). Inland Revenueconsiders there to be little value to replicating theanalysis of those guidelines here. Consequently, this partof the guidelines consists substantially of a summary ofthe key points made in the OECD guidelines (cross-referenced to relevant paragraphs in those guidelines),supplemented by Inland Revenue’s views on thoseguidelines and comments on areas where it is consideredthat further clarification is useful. If more detail isrequired than is provided in this part of the guidelines,reference should be made to the OECD guidelines.

3. Inland Revenue fully endorses the material inchapters 6 to 8 of the OECD guidelines and proposes tofollow the positions outlined in those chapters inadministering New Zealand’s transfer pricing rules. Thispart of the guidelines should, therefore, be read assupplementing the OECD guidelines, rather thansuperseding them. This applies for the domesticapplication of New Zealand’s rules, as well as in relationto issues raised under New Zealand’s double taxationagreements.

4. The OECD is continuing to undertake work onspecialist transfer pricing areas such as global tradingand insurance. At this stage, Inland Revenue does notpropose to issue its own guidelines in these areas.Instead, Inland Revenue is likely to endorse the OECDguidelines, once issued, in the administration of theseareas in the form in which the OECD releases them.

Scope5. This part of the guidelines applies only to theapplication of section GD 13 (as modified by section GC1 where relevant). It therefore applies only totransactions between separate entities.

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

4

INTANGIBLE PROPERTY

Key points• The process for applying the arm’s length principle to intangible property is no different than for other

property. It can be more problematic to apply, however, because:

• Valid comparables can be difficult, if not impossible, to locate.

• For entirely commercial reasons, multinational enterprises (MNEs) may structure their arrangements indifferent ways to independent firms.

• Functional analysis is critical in determining the real nature of intangible property being transferred. The valueof intangible property can be more sensitive to small differences than other property, so it is important that thenature of the transaction (and relevant pricing factors) be fully understood.

• If one party to a transaction does not contribute intangible property, the most straightforward analysis is likelyto involve using that party as the “tested party”, even if it is outside New Zealand.

• The value of intangible property is broadly based on perceptions of its profit potential. If there are no reliablecomparables on which to apply the pricing methods directly, alternatives may be to:

• Apply the profit split method, which requires a less rigorous application of comparables than do the othermethods.

• Value intangibles based on evaluations of profit potential.

• When dealing with marketing activities of firms that do not own the marketing intangible, it is important toensure that their compensation is commensurate with what independent entities would have accepted given therights and obligations under the arrangement.

Introduction13. Chapter 6 of the OECD guidelines discusses theapplication of the arm’s length principle to intangibleproperty. Inland Revenue fully endorses the positionestablished in those guidelines. This chapter should,therefore, be read as supplementing, but not supplanting,the OECD guidelines.

14. Paragraph 6.2 of the OECD guidelines provides ageneral description of intangible property:

The term “intangible property” includes rights to use industrialassets such as patents, trademarks, trade names, designs ormodels. It also includes literary and artistic property rights,and intellectual property such as know-how and trade secrets.… These intangibles are assets that may have considerablevalue even though they may have no book value in thecompany’s balance sheet. There also may be considerable risksassociated with them (eg, contract or product liability andenvironmental damages).

15. The OECD guidelines focus on trade andmarketing intangibles (referred to collectively ascommercial intangibles). The reason for distinguishingbetween these two types of intangibles is that they havedifferent features that lead to the creation of theirrespective values. Understanding the distinction aidssignificantly in applying the arm’s length principlecorrectly.

16. The treatment of intangible property can be oneof the most difficult areas to apply correctly in transferpricing practice. Transactions involving intangibleproperty are often difficult to evaluate for tax purposes,because:

• It can be difficult to discern the precise nature ofthe transaction – the transaction may represent anumber of components, both tangible andintangible, bundled together to form a singleproduct.

• The property may have a special charactercomplicating the search for comparables – thismight make value difficult to determine at thetime of the transaction, or to confirmsubsequently as being arm’s length.

• MNEs may, for entirely commercial reasons,structure their transactions in ways that would notbe adopted by independent firms.

17. A sound functional analysis (see paragraphs 164-211 in the draft of Part 1 of the guidelines) is animportant first step in applying the arm’s length principleto intangible property. Functional analysis can helpidentify:

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

5

• the factors that have led to the creation ofintangible value, and consequently where onemight expect the rewards to that intangible toaccrue;

• who the “owner” of the intangible is;

• what the true nature of the property beingtransferred is;

• the terms and conditions under which a relatedparty is using an intangible (for example, whetherthe user is a licensee of the intangible, or merely acontract distributor);

18. The results of the analysis can identify thosefeatures of a transaction for which comparables ideallyshould be identified. It also better enables a check thatthe price determined is consistent with the true nature ofthe property being transferred. (Table 2, which containsa list of specific factors that can be particularly relevantin determining the nature of intangible property beingtransferred, is a key reference in this chapter.)

19. The most desirable way to determine the arm’slength price is through the direct application of reliablecomparables. For example, the arm’s length price mightbe determined directly by reference to the transfer ofsimilar intangible property in an uncontrolled transaction(a comparable uncontrolled price, or CUP), or bycomparing the return to a manufacturing functionincorporating equivalent intangible property (a cost plusapproach). One possibility here is that if one of theparties to the transaction does not contribute anyintangible property, that party might be used as the“tested party”, even if it is not the New Zealand party tothe transaction (see paragraphs 134 to 138 in the draft ofPart 1 of the guidelines). Alternatively, internalcomparables (the transfer of the same property to anindependent third party), if available, could prove avaluable source of information (see paragraphs 243 to246 in the draft of Part 1 of the guidelines).

20. The often unique nature of intangible propertydoes mean, however, that applying comparables directlymay not always be practicable. Further, even if anapparent comparable can be located, it would beerroneous to assume it can usefully be appliedmechanically. The key issue in section GD 13 is whetherthe most reliable measure of the arm’s length price hasbeen determined, not whether a comparable has beenidentified and applied in a process. In some cases, it maybe better that no comparable is applied, rather thanapplying a patently bad comparable.

21. If comparables cannot be applied directly,recourse might be made to the profit split method, whichrequires a less rigorous application of comparables thanthe other methods. Alternatively, the intangible might bevalued by reference to reliable projections of future cashflows attributable to that property. Comparables might

still be usefully applied in such an approach, possibly,for example, as support for the variables underlying thevaluation.

22. One issue that taxpayers should be conscious of,and will need to address in their analysis, is thepossibility that a double deduction might arise if a localoperation, either directly or indirectly, is meeting thecosts of maintaining intellectual property (generally anissue associated with marketing intangibles). If anindependent party would not be required to maintain theintangible in a similar transaction, the local operationshould not be paying the same price for the propertybeing transferred as the independent firm, as well asmeeting the maintenance expenditure.

23. As with any other area of transfer pricing, thequality of a taxpayer’s analysis and documentation willbe a factor in supporting the credibility of its transferprices. As discussed in the documentation chapter in thedraft of Part 1 of the guidelines, taxpayers should weighthe cost of preparing documentation against the risk thatInland Revenue might make an adjustment indetermining the extent to which documentation should beprepared for a transaction. In this regard, taxpayersmight usefully consider whether an APA would representa cost-effective way of obtaining greater certainty thattheir transfer prices will be acceptable to Inland Revenue.

24. This chapter discusses first the identification ofthe nature of the intangible property being transferred. Itthen considers ways in which the arm’s length price forthe transfer might be determined. Finally, it considersspecifically the treatment of marketing intangibles.

25. This chapter is based on the OECD guidelines,and cross-referenced to paragraphs in those guidelineswhen relevant. If further detail is required, referenceshould be made to those guidelines.

Identifying types of intangible property26. The OECD guidelines begin their discussion ofintangible property by distinguishing between two broadtypes of intangible property – marketing intangibles andtrade intangibles (which are essentially non-marketingintangibles). An important reason for this distinction isthat the two types of intangible property have differentcharacteristics that give rise to the creation of theirintangible value. An awareness of the distinction can beuseful in identifying the factors contributing to anintangible’s value, and aids significantly in applying thearm’s length price correctly.

27. For example, the effectiveness of the promotionof a trade name (a marketing intangible) is likely to be asignificant factor in determining its value (although thequality of the underlying product or service will also beimportant). This suggests that an important factor inassessing the value of a marketing intangible used in a

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

6

transaction will be how that intangible is maintained.For example, a marketing intangible may have a verylimited life unless supported by current marketingexpenditure (in other words, if current marketing iseliminated, its value will quickly evaporate). Such anintangible is likely to have little or no inherent value, andit would be inconsistent with the arm’s length principlefor the intangible to earn anything beyond a nominalreturn.

28. The value of a trade intangible, by contrast, ismore likely to be determined by the use to which it canbe applied. It is the inherent quality in the intangibleproperty that is dominant in creating its value.

29. Table 1 summarises the general differencesbetween the two types of intangibles.

Table 1: Distinguishing trade and marketingintangiblesTrade intangibles Marketing intangibles

1. Tend to arise from 1. Often cheap to createrisky and costly research legally (such as trademarksand development. and trade names) but

very costly to developand maintain value.

2. Generally associated 2. Associated with thewith the production of promotion of goodsgoods. or services.

3. Use of a patented trade 3. Competitors are ableintangible may result to enter the same marketin a monopoly for a if products areproduct differentiated.

4. Any legal rights 4. May have an indefiniteestablished (for example, life (if properlya patent) are likely to have maintained).a limited life.

30. Consideration of these differences will beimportant in determining the nature of any intangibleproperty that is applied in a transaction, and the type ofcomparables that might need to be identified to assess thevalue of that property. Thus it will be important indetermining:

• the value of any intangible property transferredwithin a MNE; and

• the amount of income attributable to intangibleproperty and how:

• the income should be allocated between theparties if ownership of the property is shared.

• one party to a transaction should becompensated if it contributes to the value ofintangible property owned by the other party.

31. The focus, however, should be not so much theability to correctly classify intangibles into trade andmarketing intangibles (because the boundary may beblurred in many instances), but rather on developing anawareness of factors that lead to the creation of value inintangible property of different natures. If the nature ofthe intangible property under consideration is betterunderstood, so too will be the ability to ascertaineffectively the appropriate arm’s length price for itstransfer.

Applying arm’s length principle32. In principle, the arm’s length standard applies tointangible property in the same way as for any other typeof property – the methods in section GD 13(7) areapplied to determine the most reliable measure of thearm’s length price. As noted in paragraph 16, however,the arm’s length principle can be difficult to apply inpractice to controlled transactions involving intangibleproperty, because:

• It can be difficult to discern the precise nature ofthe transaction – the transaction may represent anumber of components, both tangible andintangible, bundled together to form a singleproduct.

• The property may have a special charactercomplicating the search for comparables – thismight make value difficult to determine at thetime of the transaction.

• MNEs may, for entirely commercial reasons,structure their transactions in ways that would notbe adopted by independent firms (paragraph6.13).

33. For example, a MNE might transfer property thatan independent firm would not be prepared to transfer. Itis common for MNEs to licence technology to theirsubsidiaries because they retain control over how thattechnology is exploited. An independent firm, bycontrast, may be more reluctant to licence its technology,out of concern that the other party might use or disclosethe detail of the property inappropriately.

34. When attempting to apply comparables to transferpricing analyses involving intangible property, a keyconsideration is how reliable those comparables are inpractice. Because of the special character of intangibleproperty, it is possible that even apparently smalldifferences between two items being compared couldhave a significant effect on their relative value.Consequently, a greater level of care is likely to berequired in assessing comparability when intangibleproperty is involved. It cannot be automatically assumed

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

7

that because two items of intangible property appearcomparable outwardly, they are directly comparable.Detailed analysis will often be necessary to determine theextent to which the two items are truly comparable.

35. It is also important to consider both parties to thetransaction (paragraph 6.14). One might, for example,perform an analysis that demonstrates, from atransferor’s perspective, the price at which anindependent party would be prepared to transferproperty. However, this may not be the same price thatan independent party would be prepared to pay, based onthe value and usefulness of the intangible in its business.At arm’s length, the transaction would not proceed at theprice determined from the transferor’s perspective. Thatprice could not, therefore, be an arm’s length price. (Theasymmetry of the interests of the transferor andtransferee is commented on further in paragraph 90, inthe context of valuation-based approaches to determiningthe arm’s length price.)

Ascertaining what the transactioninvolves36. Before appraising whether the price for intangibleproperty is arm’s length, it is necessary to ascertainexactly what the transaction involves. This identifieswhat it is that will need to be priced, ideally by referenceto independent comparables. For example, a transactionmay involve the transfer of a bundle of rights in a waythat is not representative of how independent firms mighthave undertaken a similar transaction. Segmenting thetransfer into its component parts may give a clearerpicture of exactly what is being transferred. It might alsopermit reliable comparables to be more readily identifiedfor each component part, rather than requiringcomparables to be located for the transaction as a whole.

37. A central tool for ascertaining what thetransaction involves will be a functional analysis.Failure to perform an adequate functional analysis hasthe potential to cause much controversy and confusionover inter-company transfer pricing for intangibleproperty. In the absence of an adequate analysis, it islikely there will be no meeting of the minds betweentaxpayers and Inland Revenue on what the transactioninvolves, let alone how it should be priced.

38. Functional analysis can be used to answer threethreshold questions for appraising intangible property:

• Who is the “owner” of the intangible property fortransfer pricing purposes?

• What is the true nature of the intangible propertybeing transferred?

• What are the terms and conditions under which arelated party is using an intangible? For example,is the user a licensee of the intangible, or merely acontract distributor?

39. The answer to the first question is relevant inidentifying where returns to the intangible might beexpected to accrue. The answers to the second and thirdquestions identify factors that will be relevant in actuallypricing the transfer of the intangible.

Ownership of intangible property40. A general rule of thumb is that intangibleproperty is owned initially by the party that bears theexpenses and risks associated with its development,whether incurred directly, or indirectly throughrecompensing another entity undertaking work on itsbehalf. The owner of that property is then entitled to allof the income attributable to that intangible. Theprinciple behind this is that, at arm’s length, anindependent party would not be prepared to incur suchexpenditure and assume such risk if it were not going tobenefit from what is produced by its efforts.

41. The initial owner of an intangible may choose totransfer some or all of the rights to exploit the intangible.However, an arm’s length charge should be imposed forthe transfer of those rights. The party to whom the rightsare transferred will then be entitled to the incomeattributable to the intangible rights that are transferred.

42. It is possible, however, that legal ownership ofintangible property (such as a patent) does not vest withthe party that has developed the property. In that case,the arm’s length principle would treat the legal owner asbeing entitled to the income attributable to thatintangible, even though the legal owner has notcontributed to its development. However, the developerof the intangible property would be expected to havereceived an arm’s length consideration for itsdevelopment services. This might, for example, take theform of:

• a cost reimbursement (with an appropriate profitelement), if the developer is a contract developer(effectively a service provider); or

• lump-sum compensation, if the developer bore allof the expenses and risks of development.

43. Whether or not the developer is a contractdeveloper should be determined on the facts of therelationship between the parties during the developmentprocess. If the developer is a contract developer, itwould seem reasonable to expect that at the outset of thedevelopment process, an arrangement would be in placefor costs to be reimbursed during the process or a formalunderstanding already established that the developer willnot own any intangible property produced.

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

8

Factors in pricing44. An understanding of the exact nature of theintangible property being transferred is fundamental tothe correct evaluation of the arm’s length price for thatproperty.

45. There are two aims in identifying the nature ofthe intangible property being transferred.

46. First, the key features of the intangible propertythat have led to the creation of its value are identified,giving an indication of the important factors that willneed to be priced. This helps identify what it is that willgive rise to the expected benefits, and to differentiateprofit attributable to that intangible from the profitattributable to other factors, such as functions performedand other assets employed.

47. Second, if the intangible property is to be valuedby reference to comparables, and it must beacknowledged that in many cases, this may not readily bepossible, it will enable the true extent of comparabilitybetween the transactions being compared to be betterascertained.

48. The OECD guidelines (paragraphs 6.20 to 6.24)and the United States section 482 regulations (1.482-4(c)(2)(iii)(B)(2)) identify a number of specific factorsthat may be particularly relevant to consider indetermining the nature of intangible property beingtransferred. Table 2 lists the more significant of thesefactors (but is not an exhaustive list).

Table 2: Factors in determining nature ofintangible property(a) The expected benefits from the intangible

property, determined possibly through a netpresent value calculation.

(b) The terms of the transfer, including theexploitation rights granted in the intangible, theexclusive or non-exclusive character of any rightsgranted, any restrictions on use, or any limitationson the geographic area in which the rights mightbe exploited.

(c) The stage of development of the intangible in themarket in which the intangible is to be exploited,including, where appropriate:

• the extent of any capital investment, start-upexpenses or development work required; and

• necessary governmental approvals,authorisations, or licenses required.

(d) Rights to receive updates, revisions, ormodifications of the intangible.

(e) The uniqueness of the property and the period for

which it remains unique, including the degree andduration of protection afforded to the propertyunder the laws of the relevant countries, and thevalue that the process in which the property isused contributes to the final product.

(f) The duration of the license, contract, or otheragreement, and any termination or negotiationrights.

(g) Any economic and product liability risks to beassumed by the transferee.

(h) The existence and extent of any collateraltransactions or on-going business relationshipbetween the transferee and transferor.

(i) The functions to be performed by the transferee,including any ancillary or subsidiary services.

49. Each of the factors in the table will influence theprice for the intangible property. For example, if thetransferee is to assume economic and product liabilityrisks (paragraph (g)), the arm’s length price for theproperty transferred will be lower (perhaps by way of alower royalty rate) than if the transferor retained thoserisks.

Terms and conditions of transfer50. The conditions for transferring intangibleproperty may be those of an outright sale of theintangible or, perhaps more commonly, a licensingarrangement for rights in respect of the intangibleproperty (paragraph 6.16). This identifies those aspectsof the transaction for which a price needs to bedetermined. It also identifies the type of comparablesthat need to be identified if the arrangement is to bebenchmarked against an uncontrolled transaction.

51. Determining the conditions of the transfer willnot necessarily be a straightforward task. For example, itmay be difficult to differentiate between a transfer of anintangible, and the supply of a product or service thatbenefits from the intangible.

52. One area of potential confusion is the treatment ofembedded intangibles – for example, tangible propertycarrying rights to use a tradename or trade mark, which issold by a manufacturer to a related distributor.

53. There are a number of issues to be consideredwhen dealing with the transfer of tangible property thatincludes an intangible element such as a trademark.First, it must be considered whether intangible rightshave actually been transferred. For example, the mereacquisition of branded goods will in many cases notinvolve the transfer of intangible rights.

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

9

54. Second, if it is considered that an intangible righthas been transferred then consideration must be given towhether that right should be valued separately from thetangible property. This will be a question of fact andwill depend on the available comparable data andavailable transfer pricing methods. In addition, aconsideration of the industry specific factors might alsobe made. For example, in some industries the mere factthat an intangible right has been transferred with thetangible property may not give rise to a valuable right,such as when the intangible element has no value. Insuch a case, there would be no reason to attempt toseparate the arm’s length value of the tangible propertyfrom the intangible property.

Calculating arm’s length price55. Several issues arise when calculating the arm’slength price for intangible property.

56. First, in applying the traditional transactionalmethods (CUP, resale price and cost plus methods) or thecomparable profits methods (including the transactionalnet margin method (TNMM)) to determine the arm’slength price for a transaction involving intangibleproperty, it will be very important to identify that theindependent transaction used as a benchmark is trulycomparable. If the independent transaction is notcomparable, perhaps because an important functionaldifference has not correctly been identified, the analysisbased on that comparable is likely to have no value. Theprinciples of comparability applied to intangible propertyare discussed in paragraphs 61 to 70 below.

57. Second, in many cases, taxpayers will facedifficulties in identifying reliable comparables on whichto base a sound transfer pricing analysis. Taxpayers maythen need to examine alternative approaches forperforming an analysis.

58. One option available to taxpayers is the use of theprofit split method. This is discussed in paragraphs 71 to78. A key feature of the profit split method is that itrequires a less rigorous application of comparables thanis required for analysis under the other methods. Thedownside of this, however, is that because the methodtends to be more subjective in application than the othermethods, it can increase the potential for disagreementbetween taxpayers and Inland Revenue over whattransfer prices are appropriate.

59. As an alternative, recourse might be made to avaluation-based approach to determining the arm’slength price. As paragraph 6.29 of the OECD guidelinesnotes, in relation to transactions when valuation is highlyuncertain at the time of the transfer:

One possibility is to use anticipated benefits (taking intoaccount all relevant economic factors) as a means forestablishing the pricing at the outset of the transaction.

60. It is likely that comparables might still play a partin a valuation-based approach. For example,comparables might be located to lend support to theassumptions underlying the valuation model applied.The use of comparables is not essential to this approach,but would be expected to increase the credibility of theanalysis, if applied. Valuation-based approaches arediscussed further in paragraphs 79 to 100.

Comparability61. As noted in paragraph 56, it will be veryimportant to identify that the independent transactionused as a benchmark is truly comparable whenconsidering transactions involving intangible property.If the independent transaction is not comparable, perhapsbecause an important functional difference has not beencorrectly identified, the analysis based on thatcomparable is likely to have no value.

62. The OECD guidelines, at paragraph 6.25, containa detailed example illustrating various considerations indetermining comparability for controlled transactions.The example contemplates how the arm’s length price fora branded athletic shoe might be determined.

63. The first approach suggested is to value the shoe,including its brand value, by reference to a comparableuncontrolled price. This might be done if there is asimilar athletic shoe, both in terms of the quality andspecification of the shoe itself and also in terms of theconsumer acceptability and other characteristics of thebrand name in that market, transferred under a differentbrand name in an uncontrolled transaction.

64. The second approach involves estimating thevalue of the brand name itself, with the price of theunbranded shoe and the extra value attributable to thebrand name being determined separately. The OECDguidelines (paragraph 6.25) suggest the following as oneapproach that might be taken:

Branded athletic shoe ‘A’ may be comparable to an unbrandedshoe in all respects (after adjustments) except for the brandname itself. In such a case, the premium attributable to thebrand might be determined by comparing an unbranded shoewith different features, transferred in an uncontrolledtransaction, to its branded equivalent, also transferred in anuncontrolled transaction. Then it may be possible to use thisinformation as an aid in determining the price of branded shoe‘A’, although adjustments may be necessary for the effect ofthe difference in features on the value of the brand.

65. Paragraph 6.25 does conclude, however, bynoting that:

… adjustments may be particularly difficult where atrademarked product has a dominant market position such thatthe generic product is in essence trading in a different market,particularly where sophisticated products are involved.

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

10

Example 1, adapted from the United States’ section 482regulations (1.482-4(c)(4), example 4), further illustratesconsiderations in identifying intangibles.

Example 166. A German pharmaceutical company hasdeveloped a new drug that is useful for treating migraineheadaches and produces no significant side effects. Thenew drug replaces an older drug that the company hadpreviously produced and marketed as a treatment formigraine headaches.

67. A number of drugs for treating migraineheadaches are already on the market. However, becauseall of these other drugs have side effects, the new drugcan be expected quickly to dominate the worldwidemarket for such treatments and to command a premiumprice. Thus the new drug can be expected to earnextraordinary profits.

68. The German company had previously marketedits drug through an independent company in NewZealand. It now decides to establish a New Zealandsubsidiary, and assign that subsidiary the rights toproduce and market the new drug in New Zealand. Thequestion arises as to what might be an appropriateroyalty rate to charge for those rights.

69. On further research, it is determined that the oldand new drugs were licensed at the same stage in theirdevelopment and the agreements conveyed identicalrights to the licensees. There has also been no change inthe New Zealand market for migraine headachetreatments since the earlier drug was introduced. Primafacie, therefore, it might be concluded that the licenceagreement for the new drug might be closely comparableto the previous licence agreement with the independentcompany, allowing the previous agreement to be used asa CUP.

70. Given the nature of the new drug, however, it isclear that its profitability is likely to be higher, and thatthe reward for that additional profitability should lie withits developer. This consideration would need to befactored into the license agreement for the new drug.

Profit split method71. As noted in paragraphs 57 and 58, taxpayers will,in many cases, face difficulties in identifying reliablecomparables on which to base a sound transfer pricinganalysis. The profit split method might then be a usefulalternative approach for performing an analysis,particularly as it requires a less rigorous application ofcomparables than is required for analysis under the othermethods.

72. Paragraph 6.26 of the OECD guidelines similarlystates that:

In cases involving highly valuable intangible property, it maybe difficult to find comparable uncontrolled transactions. Ittherefore may be difficult to apply the traditional transactionalmethods and the transactional net margin method, particularlywhere both parties to the transaction own valuable intangibleproperty or unique assets used in the transaction thatdistinguish the transaction from those of potential competitors.In such cases the profit split method may be relevant althoughthere may be practical problems in its application.

73. Inland Revenue acknowledges that comparableuncontrolled transactions may be particularly difficult tolocate for New Zealand, given the size of our market andthe nature of adjustments that might be required ifoverseas data is applied. In the absence of reliablecomparable transactions, Inland Revenue considers theprofit split method could represent a useful tool. If themethod is to be used for more significant transactions,however, it may be prudent for taxpayers to considerwhether there would be sufficient merit to seeking anAPA.

74. Application of the profit split method requiresthat profit be allocated based on the relative contributionof each party to a transaction. Although this allocationideally should be made by reference to how independentfirms have allocated profits in similar transactions, it maynot be essential to apply comparables in practice,particularly if locating comparables will not be apracticable exercise.

75. In such cases, profits will need to be allocatedbased on a subjective assessment of the relativecontribution of each of the parties to the transaction.There is, however, no prescriptive way in which thisjudgement should be exercised, and each case will needto be assessed on its own facts and circumstances. Inallocating profits, taxpayers should aim to determinecompensation for each party that is consistent with eachparty’s functions, assets used and risks assumed inrelation to the transaction (to put it another way, anappropriate allocation based on a sound functionalanalysis).

76. Second, in many cases, taxpayers will facedifficulties in identifying reliable comparables on whichto base a sound transfer pricing analysis. Taxpayers maythen need to examine alternative approaches forperforming an analysis. As paragraph 117 of the draft ofPart 1 of the guidelines noted:

in practice, the assessment of relative contribution may, ofnecessity, need to be a somewhat subjective measure based onthe facts and circumstances of each case.

77. An important caveat should be noted in applyingthe profit split method. The subjective nature of theprofit allocation between the parties means that themethod might reasonably be considered the least reliableof the transfer pricing methods. Because of this, themethod is perhaps less likely to be, or may not be,acceptable in foreign jurisdictions, particularly if an

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

11

alternative, more reliable, method can be applied. Thishas the potential to result in double taxation.

78. A further consideration is that the profit splitmethod is predicated on an adequate level of informationbeing available about the related party. Consequently, ataxpayer seeking to rely on the profit split method willneed to ensure that appropriate information on theoffshore party or parties can be made available ifrequested by Inland Revenue.

Valuation-based approach to intangibleproperty79. The traditionally perceived role of comparables inanalyses involving intangible property is that thecomparables should be applied to support a transfer pricefor intangible property directly. For example, a CUPmight be used to support the actual royalty rate adopted,or the cost plus method might be used to value amanufacturing function incorporating a production(trade) intangible.

80. In the absence of reliable comparables on whichto base this more traditional analysis however, recoursemight be made to determining an arm’s length price forthe transfer of intangible property on a valuation-basedapproach. Such analyses are based on realisticprojections of future benefits (paragraph 6.29)attributable to the intangible. In layman’s terms, it is thequestion, “how much extra value does the intangiblecreate?”

81. Paragraph 6.29 of the OECD guidelines is draftedwith specific reference to intangible property for whichvaluation is highly uncertain at the time of transfer.Inland Revenue considers that the specific difficultiescreated by the size of the New Zealand market meansthat the approach could usefully have broader applicationhere than a superficial reading of the OECD guidelinesmight imply, particularly for determining arm’s lengthroyalty rates. Taxpayers should be aware, however, thatwhile Inland Revenue considers a broader ambit fullyconsistent with the tenor of the OECD guidelines, othertax administrations might not hold the same view.

Applying a valuation-based approach82. As a broad principle, the value of an item ofintangible property is based on perceptions of its profitpotential. More formally, this might be determined bycalculating the net present value (NPV) of the expectedbenefits to be realised (potential profits or cost savings)through the exploitation of that property.

83. Example 2 illustrates this principle, and offersvaluable insights into how:

• an arm’s length price for a transfer of intangibleproperty might legitimately be estimated in the

absence of reliable comparables; or

• comparables might be applied in a non-traditionalmanner to support the assumptions underlying avaluation approach to intangible property.

Example 284. A New Zealand company is to be provided withintangible property that is expected to increase sales by$1 million for each of the next three years, but have noeffect on sales beyond that time. Costs for those yearswill remain constant, except for an initial outlay of$500,000 to update machinery to utilise the property.There will be some risk to the company, and the risk-adjusted cost of capital is determined to be 20% (inpractice, this would need to be based on commercialconsiderations).

85. The net present value of the cash flows for theintangible are calculated as follows:

Year Cash flow Discount Presentrate value

0 Initial outlay ( 500,000) 1.000 ( 500,000)

1 Additional receipts 1,000,000 0.800 800,000

2 Additional receipts 1,000,000 0.640 640,000

3 Additional receipts 1,000,000 0.512 512,000

NPV (r = 20%): $1,452,000

86. Based on this calculation, the New Zealandcompany might be prepared to pay a royalty of up to$743,852 for each year (that royalty rate also having aNPV of $1,452,000). If it paid such a royalty, thecompany would still earn its required rate of return fromthe project:

Year Cash flow Discount Presentrate value

0 Initial outlay ( 500,000) 1.000 ( 500,000)

1 Receipts less royalty 256,148 0.800 204,918

2 Receipts less royalty 256,148 0.640 163,934

3 Receipts less royalty 256,148 0.512 131,148

NPV (r = 20%): $ 0

Observations on valuation approach87. A couple of important principles for applying thearm’s length principle can be derived from consideringthe difficulties in making such NPV calculations inpractice.

88. First, determination of the values for most of thevariables applied in the NPV calculation (in particular,expected benefits and the appropriate discount rate) canbe very subjective. Further, the arm’s length principle

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

12

does not appear to apply NPV calculations directly.However, in appraising how independent firms havevalued intangible property, the arm’s length principle isimplicitly testing what the market has established thevariables in the NPV (or similar) calculation should be.

89. Consider, for example, a CUP that is being usedto determine an arm’s length price for the transfer ofintangible property. In negotiating their price, theindependent firms would each have evaluated the profitpotential of the intangible property. Although theseevaluations may not have used formal NPV calculations,it is to be expected that they would at least have beenbased on some views of what the likely future incomeattributable to the intangible property would be, and thecosts and risks involved in its exploitation. If a CUP isbeing used, therefore, the projections made by theuncontrolled participants in the market are implicitlyforming the basis for establishing the transfer price in thecontrolled transaction.

90. Second, it is important to consider both parties tothe transaction (paragraph 6.14), a point noted inparagraph 35. Example 2 determined the maximumvalue the transferee would be prepared to pay for theintangible property – the price commensurate with thevalue and usefulness of the intangible property in itsbusiness, given its risk-tolerance preference. At arm’slength, however, the transferor is unlikely to have accessto the same information as the transferee, and may forexample, based on its own perceptions of profit potential,be prepared to license the intangible property for aroyalty of only $500,000 per year. The parties mightthen be expected to negotiate a royalty somewherebetween these two reservation prices.

91. In principle, therefore, it should be possible toappraise intangible property without reference tocomparables, and in the absence of reliable comparablesor where only a limited amount of revenue is at issue,this may be the prudent approach for a taxpayer to take.Several cautions should, however, be noted.

92. First, ideally, transfer prices will be benchmarkedagainst comparable transactions between independentfirms, because this allows the reliability of assumptionsmade in performing NPV (or similar) calculations to betested against a more objective base. The absence of oneor more reliable comparables may reduce the credibilityof the analysis.

93. Second, although Inland Revenue considers avaluation-based approach can be undertaken to fallbroadly within the acceptable transfer pricing methods,this view may not be respected by other taxadministrations. Double taxation may then result.Taxpayers should, therefore, exercise caution in adoptingsuch an approach if the resulting analysis is also to beprovided to justify the transfer price to an overseas taxadministration.

94. Finally, the analysis in this section does notexhaust the theoretical underpinnings of valuation-basedapproaches. For example, it does not deal nicely withrelatively immaterial transactions (because the size of thetransaction is small relative to the overall size ofoperations), when cost of capital considerations maybecome unimportant in determining whether atransaction proceeds at a given price. If a valuation-based approach is to be adopted, particularly for largervalue transactions, greater consideration will need to begiven to the theoretical underpinnings of valuationtechniques.

At arm’s length, the value of intangible property isoften ascertained from perceptions of its profitpotential. This approach may also be feasible inmany transfer pricing cases. The value ofcomparables is then found in the support they give tovalues adopted in that calculation, such asappropriate discount rates and whether independentfirms would have been prepared to rely on theprojections made in entering into the transaction onthe terms agreed. Applying comparables in thismanner is not essential, but is likely to add to thecredibility of the analysis.For more complex or high-valued transactions, itmay be prudent for taxpayers to consider the meritsof seeking an APA.

Valuation highly uncertain at time oftransaction95. The OECD guidelines, at paragraphs 6.28 to 6.35,discuss the application of the arm’s length principle totransfers of intangible property when valuation of thatproperty is highly uncertain when it is transferred. Oneimportant issue in the discussion is whether taxadministrations should be able to review the transferprice adopted by reference to a form of the arrangementthat differs from that adopted by the taxpayer.

96. When the value of the intangible property isuncertain, the risks and rewards of transferring thatproperty will typically be shared between the partieswhen it is transferred. A MNE might structure atransaction in a number of ways, depending on the levelof risk, and the various types of risk, each of its membersare to assume. For example, the initial owner ofintangible property (see paragraphs 40 to 43) may chooseto exploit that property with the following levels ofmarket risk (paragraphs 6.29 to 6.31):

• No risk: The developer sells the entireresults of its development for a fixed sum, withthe purchaser then assuming the entire risk of thecommercial success or failure of the intangible.

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

13

• Complete risk: The developer mightmanufacture and market the final product itself,using a contract distributor to get the product tothe market.

• Partial risk: The developer might retainownership, but license the use of that property toanother entity in return for some form of royalty.Such an arrangement results in risk being sharedbetween the developer (the licensor) and the otherparty (the licensee). The developer’s royaltyreturn depends on the level of sales by the otherentity, and is subject, therefore, to market risk.The other entity’s return will similarly bedependent on how well the product performs inthe market. Royalties with periodic adjustmentsare a subset of this category.

97. Given that the structure of the arrangement can beseen to be a way of sharing market, credit, country andother risks between the parties, the form of thetransaction is not usually the most important aspect fortransfer pricing purposes. Rather, the central issue in anyaudit activity should generally be whether the allocationof rewards, including the royalty rate set in a taxpayer’sarrangements, is consistent with the level of all the risksassumed by the taxpayer. This examination needs to beset in the context of the functional analysis for eachparties’ actions. As with third party dealings,consideration should also be given to the circumstancesof other dealings between the parties, and each party’soverall level of risk. An appropriate allocation of riskand reward would be determined by reference to whatindependent parties would have done in similarcircumstances.

98. In evaluating a taxpayer’s transfer price, InlandRevenue will need to benchmark its analysis against anobjective external standard. If the form of a taxpayer’sarrangement is unique, therefore, Inland Revenue might,in evaluating the transfer price adopted, need to look to:

the arrangements that would have been made in comparablecircumstances by independent enterprises … Thus, ifindependent enterprises would have fixed the pricing based ona particular projection, the same approach should be used … inevaluating the pricing. … [Inland Revenue] could, for example,enquire into whether the associated enterprises made adequateprojections, taking into account all the developments that werereasonably foreseeable, without using hindsight (paragraph6.32).

99. As with other transfer pricing issues, taxpayersare in the best position to ensure there are no surprises inthe way Inland Revenue reviews their transfer prices.This can be achieved by documenting, in as much detailas prudent, why a transaction has been structured in theway it has, and how the components of that price havebeen determined by reference to what independentparties in similar circumstances would have done.

100. Further, the more thorough a taxpayer’s analysis,the less likely it will be that the Commissioner will beable to meet the burden of proof required if thetaxpayer’s determination of the arm’s length price is tobe overturned. Taxpayers should consider costs, risksand benefits in determining the extent to which theyshould develop and document their policy, as indicatedin the previously published draft chapter ondocumentation.

Use of standard international royaltyrate101. One question that is often posed is whether aroyalty rate established as arm’s length in relation to onemember of a MNE will be accepted automatically byInland Revenue as also being arm’s length in relation toNew Zealand. This issue is discussed in the example 3.

Example 3102. A United States company licences technology toa number of subsidiaries around the world. Acomprehensive analysis has been performed to supportthat an arm’s length royalty rate for its Japanesesubsidiary is 7%. On the basis of this analysis, thecompany also charges the same royalty rate to all of itsother subsidiaries. The question arises as to whetherInland Revenue will accept 7% as an arm’s lengthroyalty rate for the New Zealand subsidiary.

103. There are two issues in this question. First, thereis the question of whether 7% is actually an arm’s lengthroyalty rate for the Japanese subsidiary. Second, if it isan arm’s length rate for Japan, are the economic featuresof the New Zealand and Japanese markets sufficientlysimilar that the same royalty rate should be expected toapply in both markets?

(a) 7% is an arm’s length royalty for Japan104. Even if 7% is an arm’s length royalty rate forJapan, it is still necessary to examine the relativeeconomics of the New Zealand and Japanese markets totest whether 7% is also appropriate for New Zealand. Ifthe differences between the markets were relativelysmall, 7% would be an appropriate royalty rate for NewZealand. However, if significant differences exist,adjustments could be made to reflect these if they can bevalued.

105. At arm’s length, both the licensor and licenseewill look at profit potential from intangible property innegotiating a royalty rate. If markets are different,potential profits from those markets are also likely todiffer, and so too would acceptable royalty rates.

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

14

(b) Arm’s length royalty for Japan is not 7%106. From an alternative perspective, even if 7% is notan arm’s length royalty rate for the Japanese subsidiary,it may still be an arm’s length rate for the New Zealandsubsidiary. For example, it might be determined that anarm’s length royalty rate for Japan is only 5%, but that a2% premium is justified by the geographical differencesbetween Japan and New Zealand.

107. Significantly, even though incorrect analysismight have been used to ascertain the 7% royalty rate forNew Zealand, the important thing is that a correct royaltyrate has been determined. There would, therefore, be nojustification for Inland Revenue to attempt to substitutean alternative royalty rate under section GD 13.

Marketing activities of enterprises notowning marketing intangible108. Marketing activities are often undertaken byenterprises that do not own the trademarks or tradenames they promote. The question is how the marketershould be compensated for those services. Two keyissues arise:

• Should the marketer be compensated as a serviceprovider or might it be entitled to a share in anyadditional return attributable to the marketingintangibles?

• How should the return attributable to marketingintangibles be identified?

109. Whether the marketer is entitled to a return on themarketing intangibles above a normal return onmarketing activities will depend on the obligations andrights implied by the agreement between the parties(paragraph 6.37) – in other words, what compensationwould an independent party have sought given its rightsand obligations under the agreement. The OECDguidelines contain a couple of illustrative examples:

• A distributor acting merely as agent and beingreimbursed for its promotional expenditure wouldbe entitled to compensation appropriate to itsagency activity, but not to any share in returnsattributable to marketing intangibles (paragraph6.37).

• A distributor bearing the cost of its ownmarketing activity would expect to share in thepotential benefits of those activities (paragraph6.38). However, it is important to consider therights of the distributor in determining whetherany extra return is justified. For example:

• The distributor may benefit directly from itsinvestment in developing the value of atrademark from its turnover and market shareif it has a long-term sole distribution contract

for the trademarked product.

• Unless a distributor bears expenditure beyondthat which an independent distributor withsimilar rights would bear, there is nojustification for it to receive an additionalmargin relative to an independent distributor.

110. A further factor to consider, not explicitlyaddressed above, is the extent to which the distributor isbearing real risk, relative to independent firms in themarket. If a controlled distributor were bearing relativelygreater risk than comparable independent firms, it would,prima facie, also be expected to derive a greater marginfrom its activities.

111. Example 4, adapted from examples 2 & 3 of theUnited States section 482 regulations at 1.482-4(f)(3)(iv),illustrates these principles further.

Example 4112. Gizmo Co owns all of the worldwide rights for aname. The name is widely known outside New Zealand,but is not known within New Zealand. Gizmo Codecides to enter the New Zealand market and establishesa subsidiary here, to distribute in New Zealand and toundertake the advertising and other marketing effortsrequired to establish the name in the New Zealandmarket.

113. The New Zealand subsidiary incurs expenses indeveloping the New Zealand market that are notreimbursed by Gizmo Co. However, the level of theseexpenses are comparable to those incurred byindependent firms in the same industry when introducinga product in the New Zealand market under a brand nameowned by a foreign manufacturer.

114. Because the subsidiary would have been expectedto incur the development expenses if it were unrelated toGizmo Co, no adjustment needs to be made in respect ofthe marketing expenses.

115. The situation would be different, however, if thesubsidiary incurred expenses that are significantly largerthan would independent firms under similarcircumstances. Expenses incurred in excess of the levelincurred by independent firms should be treated as aservice to Gizmo Co, as they effectively represent aservice adding to the value of Gizmo Co’s intangibleproperty.

116. There is a caveat to this conclusion. The analysisdoes not contemplate whether the price for the productbeing transferred is arm’s length. If, for example, theNew Zealand subsidiary were undercharged for theproduct it receives, this would compensate for itsexcessive expenses. When both the transfer price for theproduct and the expenses are considered together, it maybe determined that there is no overall transfer pricingissue. This observation also illustrates that it may often

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

15

not be appropriate to stop with an analysis at the grosslevel. From Gizmo Co’s perspective, charginginadequate consideration would reduce its gross marginrelative to comparable firms. However, this is offset bythe New Zealand subsidiary not charging explicitly forits services, which reduces the costs Gizmo Co wouldrecognise in calculating its net profit.

Allocating return attributable to marketingintangibles117. Identifying the return attributable to marketingactivities if it is to be allocated between the parties to atransaction is not straightforward (paragraph 6.39). TheOECD guidelines identify several difficult questions thatmust be considered in identifying the amount of anyreturn:

• To what extent have advertising and marketingactivities contributed to the production or revenuefrom a product?

• What value, if any, did a trademark have whenintroduced into a new market – it is possible thatits value in a particular market is whollyattributable to its promotion in that market.

•· Does a higher return for a trademarked productrelative to other products in the market trace backto the marketing of the product, its superiorcharacteristics relative to other products, or amixture of both?

118. Little guidance can be given on how thesequestions should be evaluated, and each case will need tobe determined based on its own facts and circumstances.However, as with the general application of the arm’slength principle, taxpayers should aim to determinetransfer prices that result in the compensation adistributor receives for its marketing activity beingconsistent with what an independent entity would haveaccepted given similar rights and obligations.

Summary119. This chapter has considered the following keypoints:

• Intangible property poses some specialdifficulties in determining the arm’s length price,particularly because of the complexity of somearrangements and the difficulties in identifyingcomparable transactions.

• If one party to a transaction does not contributeintangible property, the most straightforwardanalysis is likely to involve using that party as the

“tested party”, even if it is outside New Zealand.

• Two particular areas where sufficient care is oftennot taken are:

• A local operation is meeting costs formaintaining intellectual property that anindependent party would not be required tomeet, while at the same time paying the sameamount as the independent firm for property itacquires (a double deduction).

• Analysis being based on what outwardlyappear to be reliable comparables but that arenot reliable, because the nature of intangibleproperty (potentially high price variations fordifferences that superficially appear quitesmall) has not been considered adequately.

• In many cases (particularly using the profit splitmethod), the analysis of intangible property mayneed to be based on a subjective judgement withlimited recourse to reliable comparables. Inexercising such judgement, taxpayers will need tobe conscious that the final result should seek toensure that each party to the transaction obtains areturn that is broadly consistent with its functionsperformed, assets employed and risks assumed inrelation to the transaction involving the intangibleproperty.

• Valuing intangible property based on realisticprojections of future benefits may be anappropriate response to the limited availability ofcomparables in the New Zealand market,particularly in relation to determining arm’slength royalty rates.

• When dealing with marketing activities of firmsthat do not own the marketing intangible, it isimportant to ensure that their compensation iscommensurate with what independent entitieswould have accepted given the rights andobligations under the arrangement.

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

16

INTRA-GROUP SERVICES

Key Points• The OECD guidelines identify two key issues in the treatment of intra-group services:

• Has a service been provided?

• If so, how should the arm’s length price be determined?

• The central test of whether an intra-group service is provided is whether the recipient of an activity receivessomething that an independent enterprise in comparable circumstances would have been prepared to pay for orperform for itself in-house.

• The arm’s length price can be determined using either:

• a direct charge approach, when charges are identified for specific services; or

• an indirect charge approach, when costs are indirectly allocated against all services provided in determininga cost base on which charges are to be determined.

• The costs attributable to a particular service will often not be able to be discerned directly, meaning that anindirect cost allocation will need to be applied:

• An appropriate allocation key will need to be used, based on the facts and circumstances of each case.

• The key focus is a realistic allocation, not accounting perfection – Inland Revenue is looking for a faircharge for the services provided and a reasonable effort into establishing a basis for future calculations.

Key issues in intra-group services124. The OECD guidelines, in paragraph 7.5, identifytwo key questions in applying the arm’s length principleto intra-group services:

• Has an intra-group service in fact been provided?

• If so, what charge for that service is consistentwith the arm’s length principle?

Has a service been provided?125. Each case must be tested on its own facts andcircumstances (paragraph 7.7). However, as a generalrule, the central issue in determining whether an intra-group service has been provided will be whether therecipient of an activity receives something that anindependent firm in comparable circumstances wouldhave been willing to pay for or would have performed in-house for itself. If the activity is not one for which theindependent enterprise would have been willing to pay orperform for itself, the activity ordinarily should not beconsidered as an intra-group service under the arm’slength principle (paragraph 7.6).

126. The OECD guidelines contain several examplesthat illustrate this principle:

• If a service is performed to meet an identifiedneed of one or more specific members of thegroup, an intra-group service would ordinarily befound to exist, because an independent party

Introduction120. Chapter 7 of the OECD guidelines discusses theapplication of the arm’s length principle in relation tointra-group services. Inland Revenue fully endorses theOECD position on intra-group services.

121. Essentially, this chapter summarises the materialin the OECD guidelines. For greater detail, recourseshould be made to those guidelines.

122. This chapter does, however, discuss issues thatwill be of particular interest to Inland Revenue inadministering the transfer pricing rules. The discussionincludes, for example, an analysis of possible allocationkeys that might be applied in determining the cost base ifthe cost-plus method is to be applied to determine thearm’s length price.

123. Inland Revenue expects that cost allocations willbe commonly employed in determining an arm’s lengthprice for services. This being the case, however, it isimportant not to lose sight of the big picture. InlandRevenue is looking for a realistic allocation of costs(with due regard to considerations of materiality), notaccounting perfection. Ultimately, the test is whether afair charge is determined for services provided to arelated company from the perspective of both theprovider and the recipient. Inland Revenue would alsoexpect to see that taxpayers have put a reasonable effortinto establishing a framework from which the price forfuture services can be readily determined.

IRD Tax Information Bulletin: Volume 12, No 1 (January 2000) - Appendix

17

would be willing to pay to have that need met(paragraph 7.8).

• “Shareholder activities” performed because of anownership interest in a group member (such asmeetings of the shareholders of the parentcompany of the group) would not justify a chargeto the recipient company, because the groupmembers do not need the activity (paragraph 7.9).

• An incidental benefit derived by a group memberfrom an activity performed for another groupmember does not mean that it has received aservice, because independent enterprises wouldnot be willing to pay for the activities giving riseto the benefit (paragraph 7.12).

• An “on call” service may be an intra-groupservice to the extent that it would be reasonableto expect an independent enterprise incomparable circumstances to incur ‘standby’charges to ensure the availability of the serviceswhen the need for them arises (paragraph 7.16).

127. The OECD guidelines also confirm that theprovision of centralised services by a parent company ora group service centre and made available to some or allmembers of the group will ordinarily be treated as intra-group services. Paragraph 7.14 contains an illustrativelist of a number of centralised services that are likely tobe intra-group services because independent enterpriseswould be willing to pay for or perform them forthemselves:

• Administrative services:

• planning, co-ordination, budgetary control,financial advice, accounting, auditing, legal,factoring, computer services;

• Financial services:

• supervision of cash flows and solvency,capital increases, loan contracts, managementof interest and exchange rate risks, andrefinancing;

• Assistance in the fields of production, purchasing,distribution and marketing;

• Services in staff matters such as recruitment andtraining;

• Research and development or administration andprotection of intangible property for all or part ofthe MNE group.

Central test for intra-group service: Does therecipient of an activity receive something that anindependent enterprise in comparable circumstanceswould have been prepared to pay for or perform foritself in-house? If so, that activity will ordinarily betreated as an intra-group service.

Determining an arm’s length charge128. Once it has been determined that a service hasbeen provided, the issue is to determine what wouldconstitute an arm’s length charge. As with othertransactions, the arm’s length charge is one that isconsistent with what would have been charged andaccepted in a transaction between independententerprises in comparable circumstances.

129. The OECD guidelines identify two generalapproaches to determining arm’s length prices for intra-group services. Which approach is followed will tend todepend on whether each service provided and itsrecipient is identified separately, or whether the servicesare more generic in nature and their recipients notspecifically identified.

130. The direct-charge approach can be applied whena member of the group is charged for specific services.In principle, it should be a relatively straightforwardexercise to determine the arm’s length price for thatservice, either by reference to the charge for that servicewhen provided to independent third parties (an internalCUP) or by reference to charges made for comparableservices between independent firms.

131. The indirect-charge approach may be applied ifthe direct-charge approach is impractical, or ifarrangements within the group are not readily identifiableand either incorporated into the charge for othertransfers, allocated among group members on somebasis, or in some cases not allocated among groupmembers at all (paragraph 7.22). In such cases, costallocation and apportionment approaches, often withsome degree of estimation or approximation, may need tobe used (paragraph 7.23).

132. Examples in the OECD guidelines of when theindirect-charge approach may be applicable include:

• The proportion of the value of the servicesrendered to various members of a group cannot bequantified except on an approximate basis (forexample, central sales promotion activities).