Transfer Pricing Analysis and Benchmarking in Light of ... Vispi... · Transfer Pricing Analysis...

39

Transfer Pricing Analysis and Benchmarking in Light of Benchmarking in Light of Recent Experiences and Judgment Vi i T P tl BCAS Vispi T. Patel

Transcript of Transfer Pricing Analysis and Benchmarking in Light of ... Vispi... · Transfer Pricing Analysis...

Transfer Pricing Analysis and Benchmarking in Light of Benchmarking in Light of Recent Experiences and

Judgment

Vi i T P t lBCAS

Vispi T. Patel

AgendaAgenda

BackgroundBackgroundCase Study

BackgroundBackground Presently five rounds of audit have been completed

TNMM is most commonly used by the taxpayers

Precedents set in earlier years – generally followed y g y

Emphasis has been laid on Documentation and Economic Analysis

Legal precedents available on transfer pricing – Mentor Graphics, Morgan Stanley, Development Consultant Engineers Ranbaxy I Gate Sony India Aztec Engineers, Ranbaxy, I-Gate, Sony India, Aztec, Instrumentarium Corporation, Vanenburg etc.

C St dCase Study

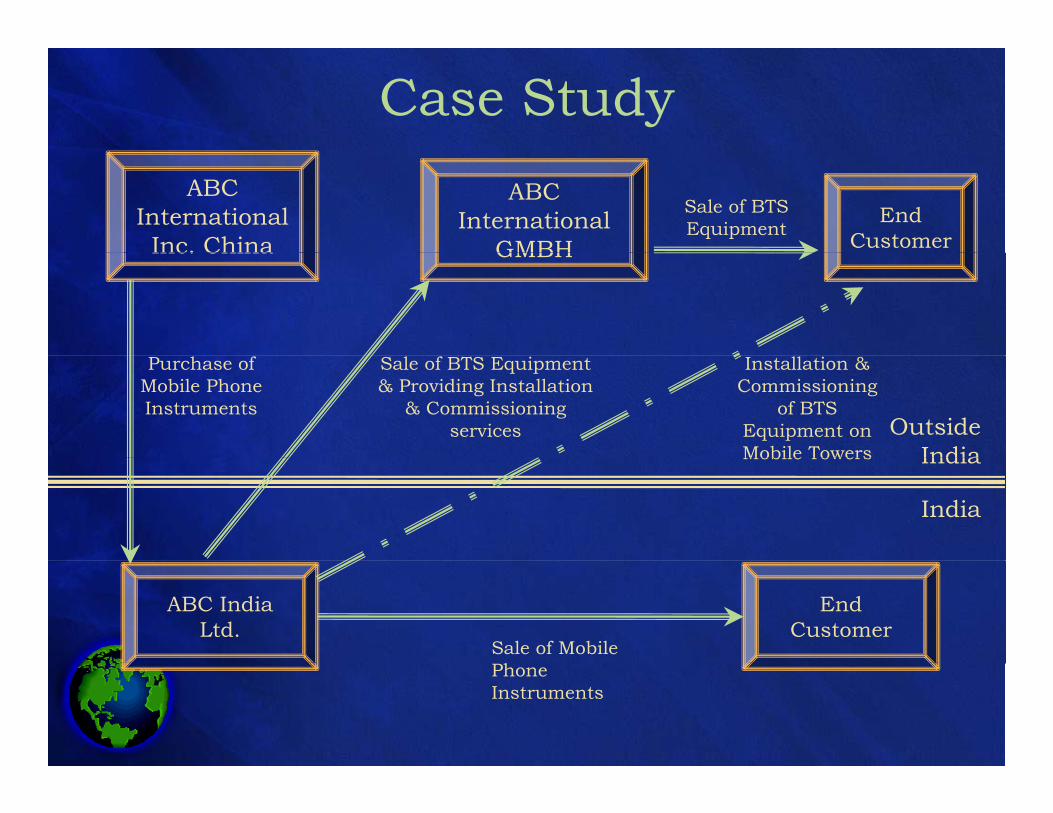

Case StudyABC

International Inc. China

ABC International

GMBHEnd

Customer

Sale of BTS Equipment

Inc. China GMBH

Outside India

Purchase of Mobile Phone Instruments

Sale of BTS Equipment & Providing Installation

& Commissioning services

Installation & Commissioning

of BTS Equipment on Mobile Towers

India

IndiaMobile Towers

End Customer

ABC India Ltd.

Sale of Mobile hPhone

Instruments

Facts ABC India Ltd. is engaged into manufacturing of BTS

Equipment, installation and commissioning of such BTS equipment and trading of Mobile Phone Equipmentsequipment and trading of Mobile Phone Equipments

ABC India sells the BTS Equipment to end customers through its Associated Enterprise (AE) in various countries

ABC India has entered into agreement with its AE for supply ABC India has entered into agreement with its AE for supply of BTS Equipment and installation and commissioning of such BTS Equipment

ABC India sells BTS Equipments to its AE at manufacturing ABC India sells BTS Equipments to its AE at manufacturing cost plus 10 per cent. Installation and commissioning cost is also charged at cost plus 10 per cent

FactsTechnical staff is deputed at the end clients

place for installation and commissioning of BTS Equipment;BTS Equipment;

For deputation of technical staff, following costs are recovered at cost plus 10 per cent p pmark-up:Travel Cost;Lodging and Boarding allowance;Lodging and Boarding allowance;Actual expenses incurred for installation and

commissioning of BTS Equipments;S l t f l b i f M DSalary cost of employees on basis of Man-Days

ABC India also imports Mobile Phone Equipments from ABC International Chinaq p

F ll i th i t ti l t ti Facts

Following are the international transaction entered into by ABC India Ltd. with its AEs

Sr. No. Name of theAE

Nature of Transaction

Amount (`)

(` in 000’s)

AE Transaction1 ABC

International GMBH

Sale of BTS Equipment

104,500

GMBH2 ABC

International GMBH

Commissioning and Installation

8,250

Charges3 ABC

InternationalPurchase of Mobile

48,580

China Ltd. Phone Equipments

Facts

ABC International GMBH sold the BTS Equipments at import cost plus 4 per cent mark-up

ABC International GMBH provided installation and commissioning services at cost plus 4 per cent commissioning services at cost plus 4 per cent mark-up

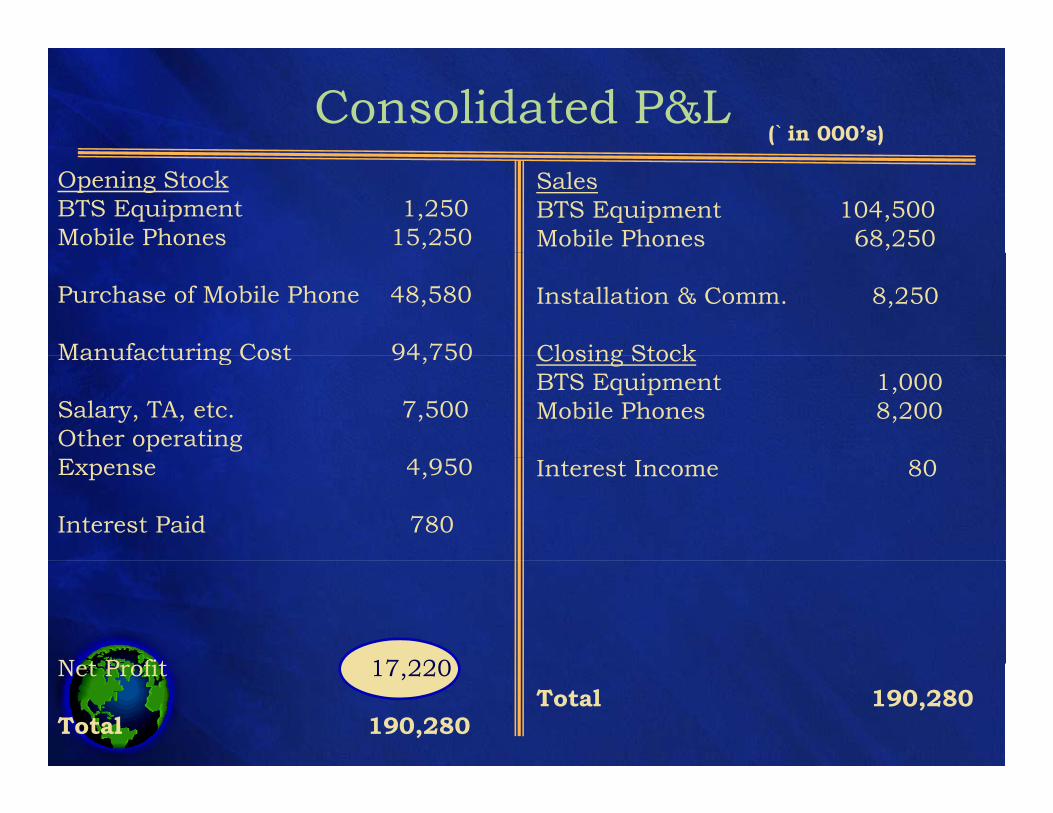

Consolidated P&L(` in 000’s)

Opening StockBTS Equipment 1,250Mobile Phones 15,250

Sales BTS Equipment 104,500Mobile Phones 68,250

Purchase of Mobile Phone 48,580

Manufacturing Cost 94 750

Installation & Comm. 8,250

Closing StockManufacturing Cost 94,750

Salary, TA, etc. 7,500Other operating

Closing StockBTS Equipment 1,000Mobile Phones 8,200

Expense 4,950

Interest Paid 780

Interest Income 80

N t P fit 17 220Net Profit 17,220

Total 190,280Total 190,280

FAR AnalysisFAR Analysis

11

Economic Analysis ?

BusinessFunction

Intangibles/Risks

ManagementStructure/Processes

Economic Analysis

Economic Profiling

ComparableStrategy

Most Appropriate

Method

FAR Analysis – Manufacturing SegmentFunctions Performed

Activities performed ABC India ABC International

Functions Performed

Development of global strategy / branding for the manufacture and sale of Group’s products

x

productsR&D activities x

Manufacture of BTS Equipment xManufacture of BTS Equipment x

Inventory Management

Selling & Distribution activities

13

FAR Analysis – Manufacturing SegmentA t l d

Assets ABC India ABC I i l

Assets employed

International

Manufacturing Facilities x

Technical know-how x

Trademarks x

W h i f iliti Warehousing facilities

Human Resources

14

FAR Analysis – Manufacturing SegmentRi k A d

Risks ABC India ABC International

Risks Assumed

Market risk

Legal risk

Inventory risk

Foreign exchange fluctuation risk xForeign exchange fluctuation risk x

Credit risk

ABC India can be characterised as a full fledged entrepreneurial entity owning significant intangibles

15

entrepreneurial entity owning significant intangibles pertaining to manufacturing of BTS Equipments

FAR Analysis – Trading SegmentF i P f d

Activities performed ABC India ABC International

Functions Performed

International China

Estimation of demand x

Manufacture of goods x

Customs clearance formalities x

Inventory Management Inventory Management

Marketing activities

16

FAR Analysis – Trading SegmentAssets employed

FAR Analysis Trading Segment

Assets ABC India ABC International

ChinaFixed Assets

Human Resources

Trademarks and brand names

x

17

Ri k A d

FAR Analysis – Trading Segment

Risks ABC India ABC International

Risks Assumed

ChinaMarket risk

Legal risk Legal risk

Inventory risk

Foreign exchange fluctuation xForeign exchange fluctuation risk

x

Credit risk x

ABC I di b h t i d f ll fl d d T d ABC India can be characterised as a full fledged Trader not owning significant intangibles in respect of trading

of Mobile Phone Equipments

Philips Software Centre Pvt Ltd Vs ACIT (26 SOT226)

18

Philips Software Centre Pvt. Ltd. Vs ACIT (26 SOT226)Mentor Graphics (Noida) Pvt. Ltd. Vs DCIT (109 ITD 101)

Which Way Forward ?Which Way Forward….?

Slicing Based On "Functions”On Functions”

19

Which Way forward……?

M f t iM f t iManufacturingManufacturing

Understanding the Business Model of

the Company

Installation& Commissioning

t e Co pa y

TradingTrading

Operating Operating II

20

IncomeIncome

Aggregation vs. Segregation

Manufacturing, Installation and Commissioning: Installation and Commissioning of the BTS Equipment is

inextricably linked to the sale of BTS Equipmentinextricably linked to the sale of BTS Equipment Trading of Mobile Phone Equipment:

Trading of Mobile Phone Equipment is a separate activity d i t i t i bl li k d t th l f BTS and is not inextricably linked to the sale of BTS

Equipment.

Development Consultants (P.) Ltd. vs DCIT (23 SOT 455)Global Vantedge vs. DCIT (37 SOT 1)

UCB I di (P ) Ltd ACIT (121 ITD 131) S litti f UCB India (P.) Ltd. vs. ACIT (121 ITD 131) – Splitting of Consolidated Accounts into Manufacturing & Trading Segments

21

Segment Analysis

Based on the business functions of ABC India, the business can be divided into the following segments:g g Manufacturing Segment – This involves manufacturing of BTS

Equipments. The international transactions in this segment include export of BTS Equipments

Installation and commissioning of BTS Equipment Trading Segment – This involves purchase and resale of Mobile

Phone Equipment. The international transactions in this segment include import of Mobile Phone Equipmentsegment include import of Mobile Phone Equipment.

Benchmarking of gInternational Transactions – Which Way

22

Forward?

Split P&L AccountTested Party P&L A/c – Manufacturing Segment Tested Party P&L A/c – Trading Segment

(` in 000’s)(` in 000’s)

Opening Stock 1,250

ManufacturingCost 94,750

Sale of BTS 104,500

Installation & Commissioning 8,250

Opening Stock 15,250

Purchases 48,580

Gross Profit 12 620

Sales 68,250

Closing Stock 8,200

,

Salary, TA, etc. 7,500

Net Profit 10,250

g ,

Closing Stock 1,000

Gross Profit 12,620

Total 76,450

Operating Expense

Total 76,450

Gross Profit 12,620

Total 113,750 Total 113,750

4,950

Interest Paid 780

Net Profit 6 970

Interest Income 80

Net Profit 6,970

Total 12,700 Total 12,700

Pricing Method SelectionPricing Method Selection

Transaction Based Methods Comparable Uncontrolled Price

Profit Based Methods TNMM Comparable Uncontrolled Price

(CUP) Resale Price Cost Plus

TNMM Profit Split

-Comparable -Residual

CUP Method

Product/Service Economic Conditions

Lik t Lik i l t i ibl

Contractual terms Like to Like comparison – almost impossible Hence, CUP is rejected as most appropriate

method

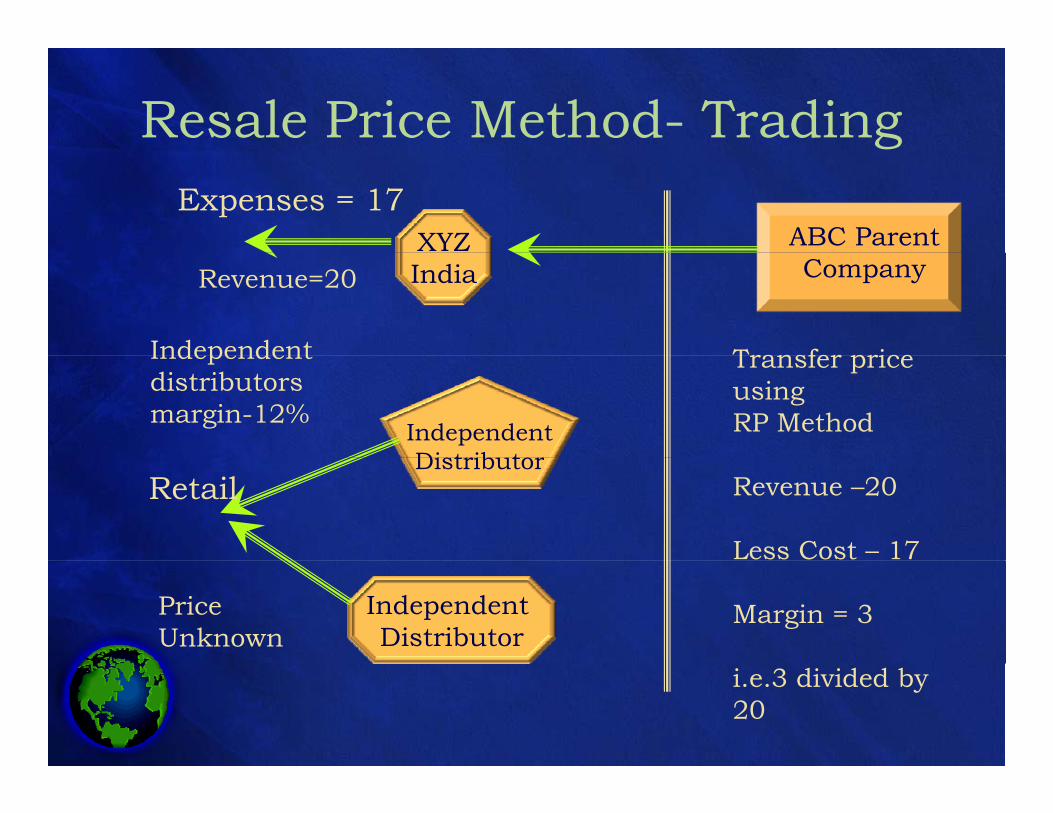

Resale Price Method

1Determine the gross profit marginearned in comparable uncontrolled 1 earned in comparable uncontrolled transactions

Steps 2Subtract the appropriate grossmargin from the applicable

l iSteps resale price

3The remainder will be thearm’s length price with thecontrolled entity

Resale Price Method- Trading

XYZ ABC Parent Expenses = 17

India Company

Transfer price Independent

Revenue=20

IndependentDistributor

Transfer price usingRP Method

Independent distributorsmargin-12%

DistributorRevenue –20

Less Cost – 17

Retail

Independent Distributor

Margin = 3PriceUnknown

i.e.3 divided by 20

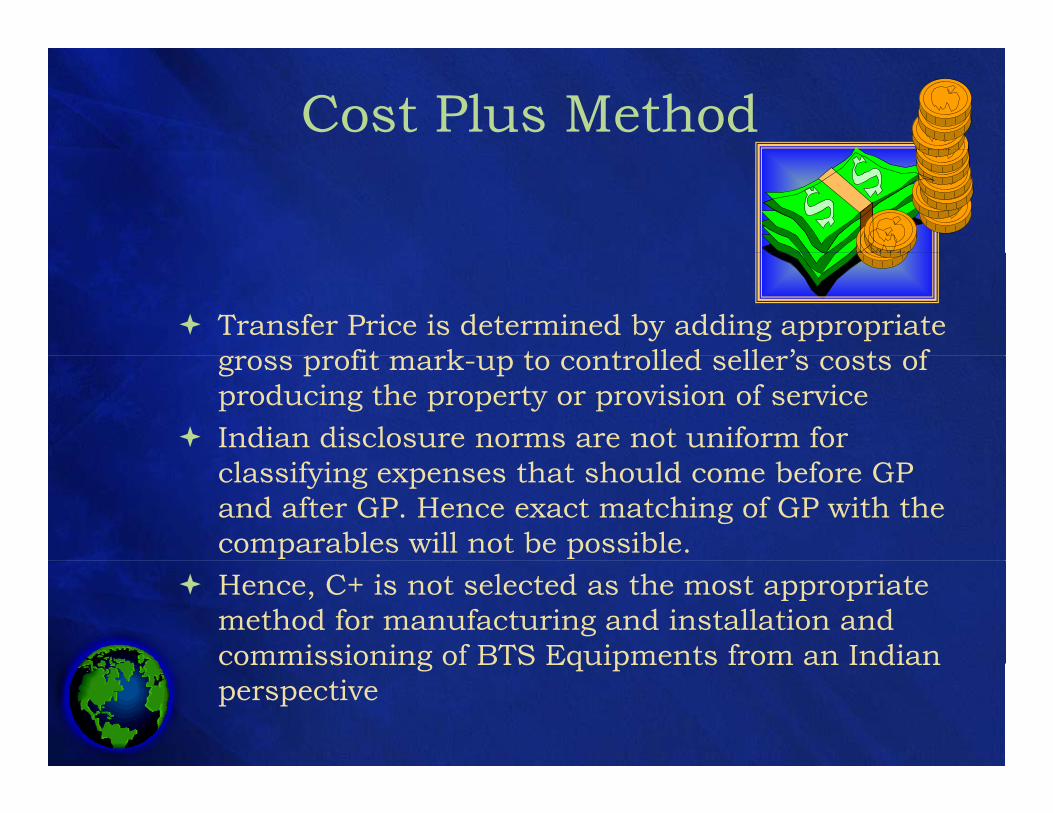

Cost Plus Method

Transfer Price is determined by adding appropriate fit k t t ll d ll ’ t f gross profit mark-up to controlled seller’s costs of

producing the property or provision of service Indian disclosure norms are not uniform for

classifying expenses that should come before GP and after GP. Hence exact matching of GP with the comparables will not be possible.

Hence, C+ is not selected as the most appropriate method for manufacturing and installation and commissioning of BTS Equipments from an Indian commissioning of BTS Equipments from an Indian perspective

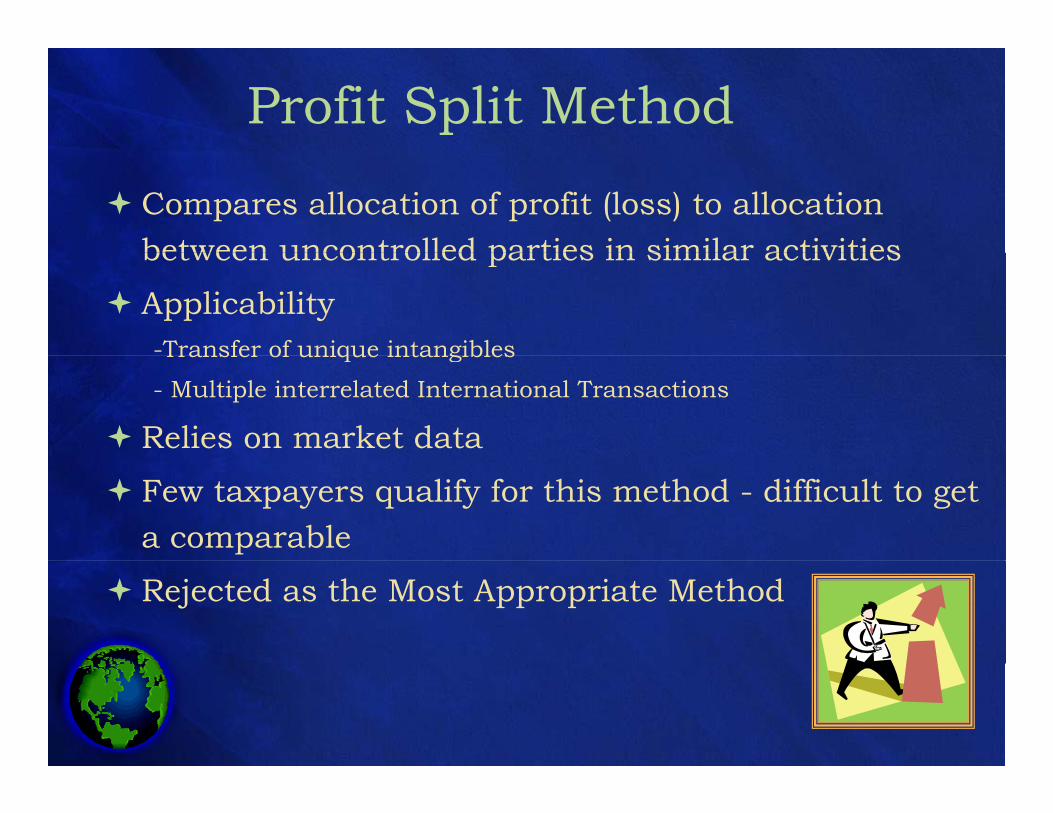

Profit Split Method

Compares allocation of profit (loss) to allocation between uncontrolled parties in similar activitiesbetween uncontrolled parties in similar activities

Applicability-Transfer of unique intangibles Transfer of unique intangibles

- Multiple interrelated International Transactions

Relies on market data

Few taxpayers qualify for this method - difficult to get a comparable

Rejected as the Most Appropriate Method

TNMMTNMM

CostStructures

ResourcesComparability

Factors Resources

Risks

TNMMTNMM Determine arm’s length price by comparing financial

results of tested party and selected uncontrolled parties

Apply Profit Level Indicators (PLIs)

TNMM is selected as the most appropriate method for benchmarking the international transaction of import f M bil Ph E i tof Mobile Phone Equipments

Selection of Tested Party OCED: The choice of the tested party should be consistent with the

functional analysis of the transaction. As a general rule, the tested party is the one to which a transfer pricing method can be applied in the most reliable manner and for which the most reliable comparables can be found, i.e. it will most often be the one that has the less complex functional analysis.

Based on FAR Analysis following entity are selected as Based on FAR Analysis following entity are selected as tested party Manufacturing, Installation & Commissioning Activity:

ABC International GMBH (AE selected as tested party – being the ABC International GMBH (AE selected as tested party being the simpler entity and reliable internal comparable data available).

Trading of Mobile Phone Equipments: ABC India Ltd (assessee selected as the tested party – being entity with simpler entity and external reliable comparable data is available)

Ranbaxy Laboratories Ltd. vs. ACIT [299 ITR (AT) 175]Development Consultants (P.) Ltd. vs DCIT (23 SOT 455)

Global Vantedge vs. DCIT (37 SOT 1)

Selection of the Most Appropriate Method

Manufacturing Activity:a u actu g ct ty: As discussed earlier, CPM is selected as the

most appropriate method by benchmarking f i AE foreign AE

Trading Activity: T h i ll RPM i li bl Technically RPM is applicable; But in view of lack of availability of data for

computation of gross profit margin;co putat o o g oss p o t a g ; TNMM is selected as the most appropriate

method.

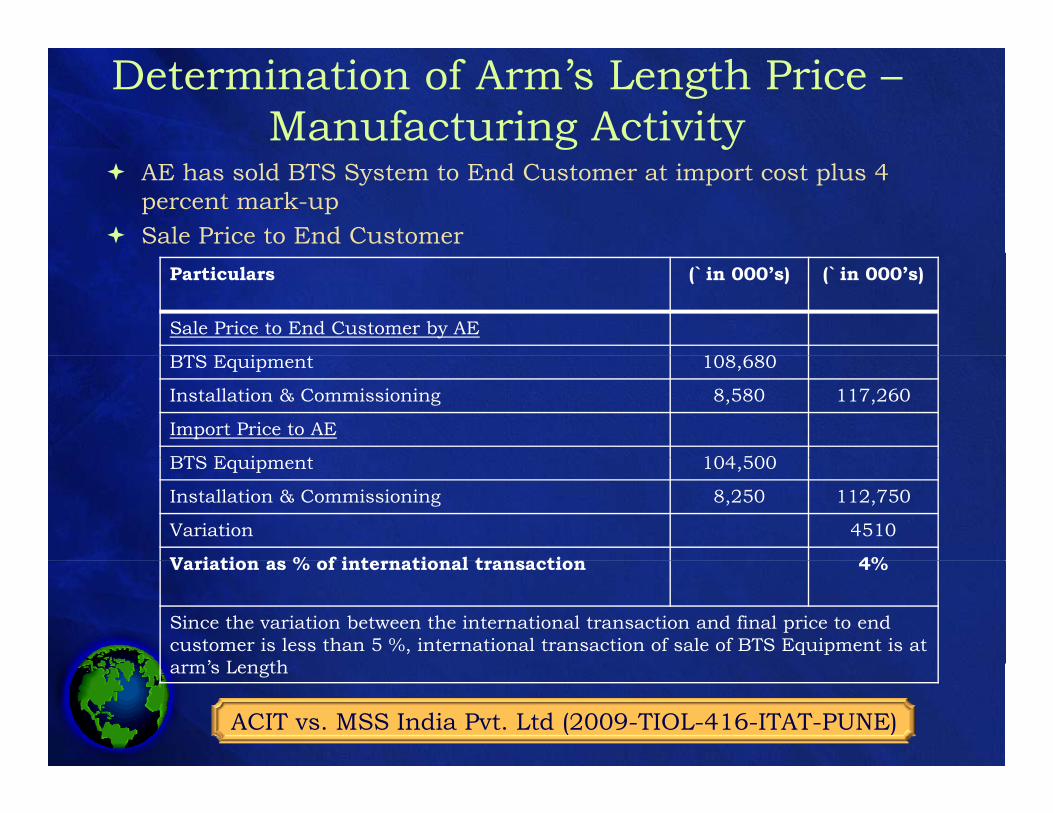

Determination of Arm’s Length Price –Manufacturing Activity

AE has sold BTS System to End Customer at import cost plus 4 percent mark-up

Sale Price to End CustomerParticulars (` in 000’s) (` in 000’s)

Sale Price to End Customer by AE

BTS E i 108 680BTS Equipment 108,680

Installation & Commissioning 8,580 117,260

Import Price to AE

BTS E i t 104 500BTS Equipment 104,500

Installation & Commissioning 8,250 112,750

Variation 4510

V i ti % f i t ti l t ti 4%Variation as % of international transaction 4%

Since the variation between the international transaction and final price to end customer is less than 5 %, international transaction of sale of BTS Equipment is at

’ L tharm’s Length

ACIT vs. MSS India Pvt. Ltd (2009-TIOL-416-ITAT-PUNE)

Determination of Arm’s Length Price –Trading Activity

Search for Comparable Companies D t b U d P Database Used – Prowess

Issues faced in case of the use of Comparable data Comparable contemporaneous data not available Whereas the Tax Department insists on same year data only Limitations of databases such as inadequate information, etc.

Philips Software Pvt. Ltd. vs. ACIT (26 SOT 226) – Use of contemporaneous data

Search Process – Trading Segment

Search criteria No. of companies passing the criteria

Product search Selected companies classified under 15Product search – Selected companies classified under Industry classification “Telephones and Mobile Phones”

15

Companies having Trading Sales / Total Sales > 90% 12

Accept companies ha ing Marketing & Ad ertisement 11Accept companies having Marketing & Advertisement Cost / Sales > 2.5%

11

Rejected companies making losses consistently 1

Qualitative Screening 5Qualitative Screening 5

Select Companies not having significant related party transactions

4

Arithmetic mean of Operating Profit / sales of comparable companies is 8.59%

36Philips Software Centre Pvt Ltd vs ACIT(26 SOT 226)

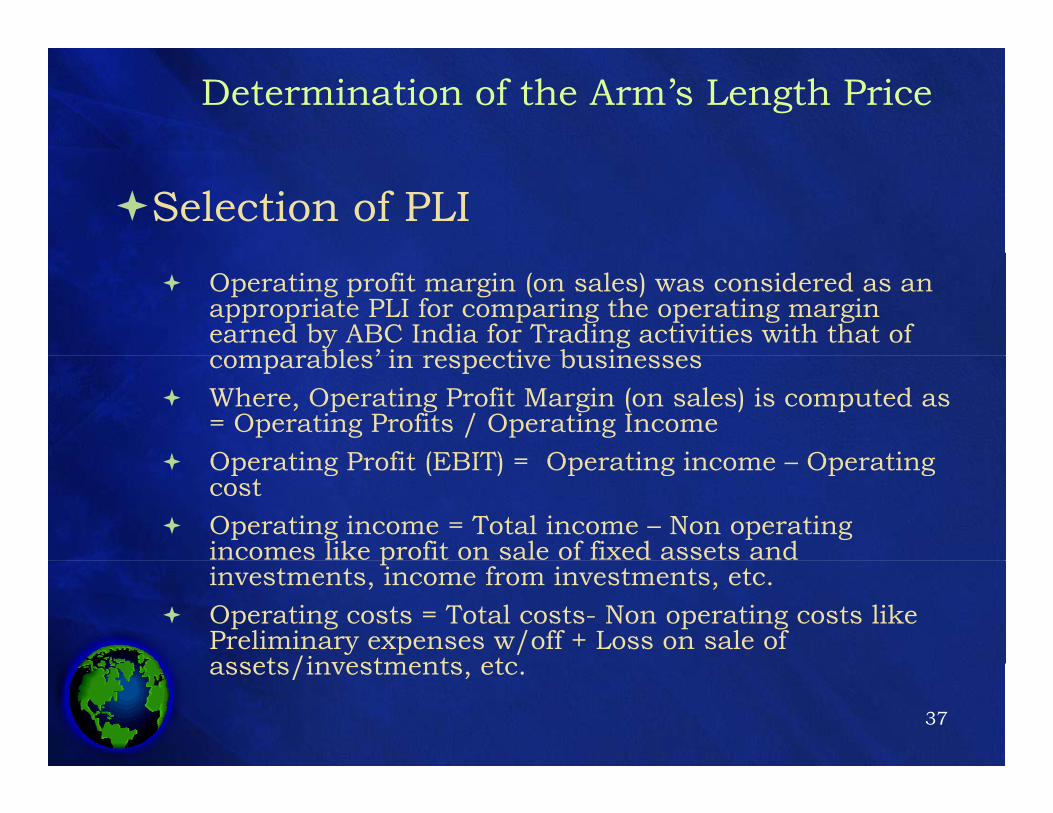

Determination of the Arm’s Length Price

Selection of PLI

Operating profit margin (on sales) was considered as an appropriate PLI for comparing the operating margin earned by ABC India for Trading activities with that of comparables’ in respecti e businessescomparables’ in respective businesses

Where, Operating Profit Margin (on sales) is computed as = Operating Profits / Operating Income

Operating Profit (EBIT) Operating income Operating Operating Profit (EBIT) = Operating income – Operating cost

Operating income = Total income – Non operating incomes like profit on sale of fixed assets and pinvestments, income from investments, etc.

Operating costs = Total costs- Non operating costs like Preliminary expenses w/off + Loss on sale of assets/investments etc

37

assets/investments, etc.

Tested Party P&L A/c – Trading Segment

Determination of the Arm’s Length Price(` in 000’s)

Opening Stock 15,250

Purchases 48,580

Sales 68,250

Closing Stock 8,200

Gross Profit 12,620

Total 76,450 Total 76,450

Operating Expense 4,950

Interest Paid 780

Net Profit 6,970

Gross Profit 12,620

Interest Income 80

Net Profit 6,970

Total 12,700 Total 12,700

Op Profit = NP - Interest Income + Interest O P fit / S l (T t d pPaid = 6,970 – 80 + 780 = 7,670

Op Profit / Sales = 7670 / 68250 * 100 = 11.24%

Op Profit / Sales (Tested Party) = 11.24%Op Profit / Sales

(Comparable Companies) = 8.59%

Since the Operating margin of ABC India is more than the operating margin of comparable companies, the transaction of import of Mobile Phones is at arm’s length

THANK YOU

QUESTIONS

39