Trade and other payables

16

Trade and other payables 1 Trade and other payables

-

Upload

tharindu-nishshanka-muhandiram -

Category

Education

-

view

113 -

download

0

Transcript of Trade and other payables

Trade and other payables

1Trade and other payables

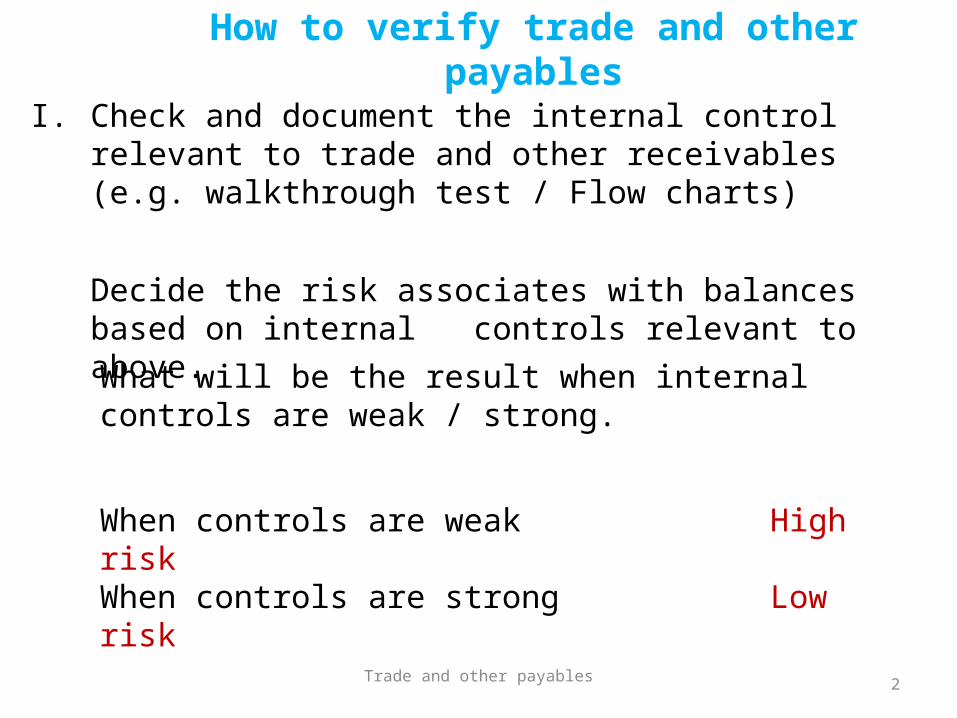

I. Check and document the internal control relevant to trade and other receivables (e.g. walkthrough test / Flow charts)

Decide the risk associates with balances based on internal controls relevant to above.

2Trade and other payables

How to verify trade and other payables

What will be the result when internal controls are weak / strong.

When controls are weak High riskWhen controls are strong Low risk

II. Decide material Level (Individual) based on risk

Document performance material level during the audit.

3Trade and other payables

How to verify trade and other payables

What will be the percentage when risk is high?

When risk is high?When risk is low?

Use low percentageUse high percentage

III. Select a sample.e.g.-Random basisSystematic selection

Document Sample Size which you have selected.

4Trade and other payables

How to verify trade and other payables

IV. Decide and perform audit procedures.

5Trade and other payables

How to verify trade and other payables

6Trade and other payables

Audit procedures for creditors Check a sample of creditors with supportive documents.

Obtain an aging analysis• Why we need an aging analysis.• When there is no aging can be obtained what needs to

be done.• Check whether the aging balance is tally with ledger

balance.• Check whether there are any related party balances

included in the creditor balance . If so cross check with inter company.

• If there are any long outstanding balances inquire the payment obligation thereto.

Check subsequent settlement details Check whether there are any unusual journal entries passed through

the creditors ledger.(Control account). Call confirmations for sample of creditors. Check the sample of opening creditors settled during the year.

7Trade and other payables

Audit procedures for creditors Perform cut-off procedures.

• How to perform a cut-off? • Why we need a cut-off?

Obtain a list of debit balances included in creditors.• Obtain the reasons for outstanding balances.• Check the materiality of thereto.• If it is material, separately mention the balances as advances /

receivables. Check the last month invoices with creditors control account. (fake

invoices) Check whether balances are included in the creditors aging analysis

other than creditors.e.g.- Other payables in ERP systems.

Foreign currency creditors should be converted to Rs using selling rates as at the reporting date.

Discuss why we should use selling rate.

8Trade and other payables

Converting of foreign currency creditors

9Trade and other payables

Converting of foreign currency creditors

Ex – Creditors balance as at 31st March 2016 $ 2,000Selling rate of 1$ as at 31st March 2016 Rs.130Balance of creditors as per ledger 240,000

RequiredJournal entries relevant to converting the creditors.

Exchange loss (Dr) 20,000 Trade creditors (Cr) 20,000

10Trade and other payables

Advances and other payables

Check the supportive documents for payables and advances as at the balance sheet date.Obtain a detailed schedule which supporting to the ledger balance.Check subsequence settlement detail.

• What are the documents Internal / external.Check whether the opening balances of advances appropriately recognized with income and payables have been settled.Obtain explanations for long outstanding balances and check the payment obligation of them.If the amounts are material obtain confirmations for the balances. Check the classification of advances and other payables.Check last month advances and make sure there is no revenue included in advances.

11Trade and other payables

Accruals

Obtain schedule for accruals.Check whether the schedule balance is tally with the ledger balance.Separately identify payables and provisions.

• What is the difference between provision and payable.“A provision is a liability of uncertain timing or amount.”

Separately identify over / under provisions and over / under payments.Document and refer supportive documents for the provision / payable.Document subsequence settlement details.

“A provision is a liability of uncertain timing or amount.”

12Trade and other payables

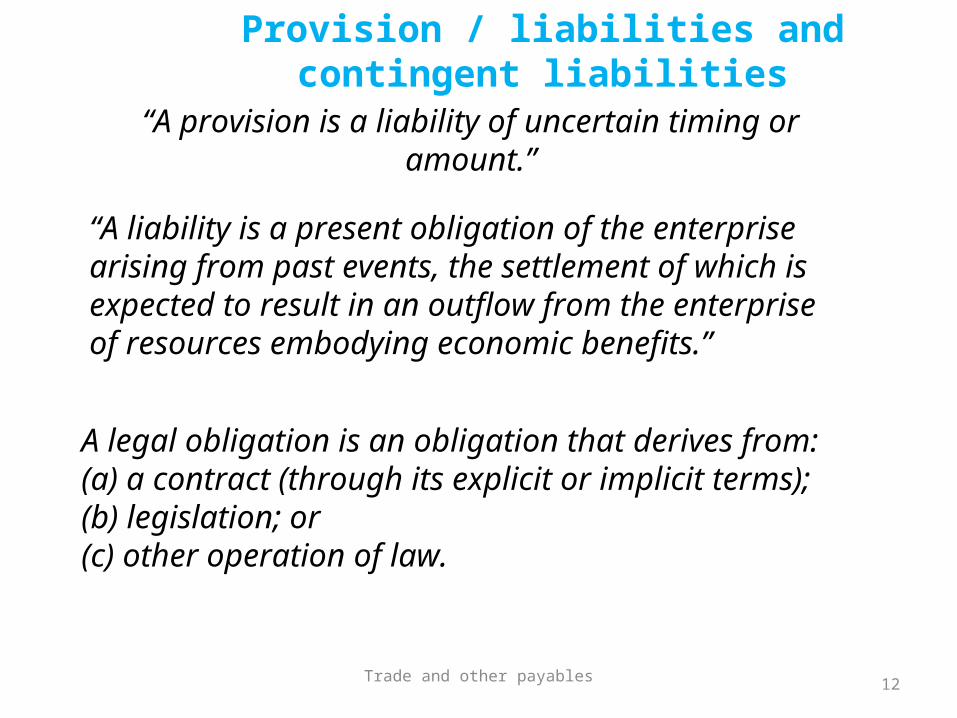

Provision / liabilities and contingent liabilities

“A liability is a present obligation of the enterprise arising from past events, the settlement of which is expected to result in an outflow from the enterprise of resources embodying economic benefits.”

A legal obligation is an obligation that derives from:(a) a contract (through its explicit or implicit terms);(b) legislation; or(c) other operation of law.

A constructive obligation is an obligation that derives from anenterprise’s actions where:

(a) by an established pattern of past practice, published policies or a sufficiently specific current statement, the enterprise has indicated to other parties that it will accept certain responsibilities; and

(b) as a result, the enterprise has created a valid expectation on the part of those other parties that it will discharge those responsibilities.

13Trade and other payables

Provision / liabilities and contingent liabilities

A contingent liability is: a possible obligation that arises from past events and whose existence will be confirmed only by the occurrence or nonoccurrence of one or more uncertain future events not wholly within the control of the enterprise.

14Trade and other payables

Provision / liabilities and contingent liabilities

Can we identify provision for future repair costs or losses?

15Trade and other payables

Provision for future repair costs

Provisions should not be recognized for future operating losses since its do not meet the definitions of a liability.

provision should be recognized when:(a) an enterprise has a present obligation (legal or constructive) as aresult of a past event;

(b) it is probable that an outflow of resources embodying economicbenefits will be required to settle the obligation; and

(c) a reliable estimate can be made of the amount of the obligation.

Trade and other payables 16