Towards a Comprehensive Private Health Insurance market …. Andrew Murray (final).pdf · Towards a...

38

Towards a Comprehensive Private Health Insurance market in China The Actuarial Society of Hong Kong Dr. Andrew Murray Senior Vice President: Strategic Risk Management, Discovery International 7 March 2013

-

Upload

phunghuong -

Category

Documents

-

view

215 -

download

0

Transcript of Towards a Comprehensive Private Health Insurance market …. Andrew Murray (final).pdf · Towards a...

Towards a Comprehensive Private Health Insurance market in China

The Actuarial Society of Hong Kong

Dr. Andrew MurraySenior Vice President: Strategic Risk Management, Discovery International

7 March 2013

2

1

2

3

Massive unmet need

Customers turn to PHI, but existing market in its infancy

Most dominant PHI category, Critical Illness, meets only limited needs

4 True financial risk relating to healthcare costs in China

5 Traditional PHI products offset OOP liability only partly

Agenda

3

Agenda

1

2

3

Massive unmet need

Customers turn to PHI, but existing market in its infancy

Most dominant PHI category, Critical Illness, meets only limited needs

4 True financial risk relating to healthcare costs in China

5 Traditional PHI products offset OOP liability only partly

4

China is already the No. 5 healthcare market in the world

-

500

1 000

1 500

2 000

2 500

3 000

2000 2005 2010 2015 2020

Growth of Asia’s healthcare market

China share of Asia

healthcare market

India share of Asia

healthcare market2% 4% 7% 7% 11%

China contribution

to global profit pool

US$22bn

4%

US$113bn

15%

AsiaUS$1 trillion~10% of global

market

US$2.6 trillion~20% of global

market

$ billion

10% 20% 29% 35% 40%

Source: Bain (2012); McKinsey (2010, 2012)

China

India

US$1 trillion~7% of global

market

US$91bn

41%

5

... but invests far less in healthcare than many otherinternational markets

8 362

3 503

649 221

US UK SA China

Population (in million)

THE in US$ billion

THE as % of GDP

2 605 291 22 297

312 63 51 1 344

Healthcare expenditure per person (in US$)

18% 10% 9% 5%

Public Expenditure as % THE 53% 84% 44% 54%

Private Expenditure as % THE 47% 16% 56% 46%

of which is OOP 25% 62% 30% 79%

OOP as % THE 12% 10% 17% 37%

Source: World Bank (2011 data); Discovery analysis

6

Growing burden of lifestyle disease increase both mortality and morbidity risk

… and an increase in Vitality Age, indicating

higher health risk

• On average the Vitality Age (a health-risk

adjusted age) of participants was 8.2

years higher than their real age

• Most health factors measured by the

Vitality Age are modifiable

Industrialization and poor lifestyle habits

lead to rise in chronic disease

• 260 million cases of chronic disease in 2008

• Incidence of hypertension and diabetes

quadrupled and heart disease and cancer

doubled in past decade

• <20% of 7 – 17 year-olds in large cities are

overweight or obese

Top 5 chronic conditions 2003 2008

Hypertension 26.2% 54.9%

Gastroenteritis 10.3% 10.7%

Diabetes 5.6% 10.7%

Rheumatoid Arthritis 8.6% 10.2%

Cerebrovascular disease 6.6% 9.7%

Source: clearstate (2012); Ping An Health (Vitality Age survey 2012)

2.5

3.5

4.5

5.5

6.5

7.5

8.5

9.5

<20 20-2425-3435-4950-59 >60 All

All

Female

Male

Vitality Age > chronological age

7

Current health financing approach offers inadequatefinancial protection

OOP spending decreased from 60%

before reform but remains high …

Source: Economist (2012); World Bank (2011)

… with significant risk of catastrophic

spending for low-income families

• High OOP costs driven by both

uncovered OP costs (particularly for

URBMI and NCRMS members) and IP

costs exceeding the annual limit

• Coverage level depends largely on

financial means of local government

0%

10%

20%

30%

40%

50%

60%

70%

1980 1985 1990 1995 2000 2005 2010

OOP

government

social

0%

2%

4%

6%

8%

10%

12%

• Rural inhabitants particularly at risk of

catastrophic healthcare spending:

average IP admission requires OOP

spending of 50% – 70% of their annual

income (double that for urban areas)

• 12th 5-Year Plan focus on shifting such

cost for CI conditions to PHI

urban L M S rural E C W

2003

2008

8

Current health delivery approach frustrates accessto quality care

Source: World Bank (2011); KPMG (2010); WSJ (2012)

… where access is limited due to over-

subscription of available capacity

• High demand leads to severe over-

crowding in Class 3 general hospitals

• Accessing care requires excessive

queuing or cash to navigate the system:

buy registration numbers from scalpers

or to give hongbao

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2003 2004 2005 2006 2007 2008

General

hospitals

THC

CHC

Healthcare funding strategy favors large,

urban hospitals …

• ~ 90% of healthcare funding allocated at

provincial or sub-provincial level

• Direct government subsidies to public

hospitals was US$7.4 billion in 2008:

>60% spend directed to urban hospitals;

only 10% spend on primary care

0%

5%

10%

15%

20%

25%

30%

35%

City Hospital CountyHospital

CHC THC

Government subsidy

Medical service fees

Drug revenue

Other revenue

CHC = Community Health Center; THC = Township Health Center

9

1

2

3

Massive unmet need

Customers turn to PHI, but existing market in its infancy

Most dominant PHI category, Critical Illness, meets only limited needs

4 True financial risk relating to healthcare costs in China

5 Traditional PHI products offset OOP liability only partly

Agenda

10

Small existing PHI market with lack of specialization

Market size of existing

PHI product categories

High-end coverRMB 800 million

Mid-market coverRMB 200 million

Other productsRMB 1.3 billion

*Graphic not to scale; ** Include investment componentsSource: Munich Health (2013)

Comprehensive coverRMB 30 billion

Covers SHI shortfalls for treatment

in public hospitals

Typical premium: RMB 500-2,000

In-patient only coverRMB 5 billion

Covers some additional costs for

treatment in public hospitals

Typical premium: RMB 10-200

SHI supplementary cover

Critical Illness cover**

RMB 49 billion

Commercial insurance for selected

conditions up to an agreed sum-insured

Typical premium: RMB 3-8 per RMB 1,000

of cover

RMB 86 billion* … 92% from CI and SHI supplementary cover

11

Small existing PHI market is dominated by CI andSHI supplementary cover

Market size of existing

PHI product categories

Source: Munich Health (2013); Mercer (2012)

Comprehensive SHI supplementary cover

Critical Illness cover**

RMB 86 billion*

Estimated market size: RMB 30 billion

• Cover is sold in units; Ping An Life sells cover with

each unit representing RMB 3,000 of cover

• Individual clients typically buy 2 – 3 such units

• Group-based cover has a median annual limit of

RMB 20,000 for IP and OP costs

Estimated market size: RMB 49 billion

• Typical sum insured is RMB 100,000

• Rider to life insurance (25% of the CI market) or

sold as a stand-alone product (75% of CI market)

• CI products in China cover a standard 25 conditions;

some products expand this list as product features

*Graphic not to scale; ** Include investment components

57%

35%

12

Mature high-end market continues to grow;infantile mid-market offers substantial growth opportunity

Market size of existing

PHI product categories

Source: Munich Health (2013); Mercer (2012)

High-end comprehensive cover

Mid-market comprehensive cover

RMB 86 billion*

Estimated market size: RMB 800 million

Typical premium: RMB 12,000 – RMB 30,000

• Cover is mostly sold to groups

• HR function typically acts as key decision maker

• Network and benefits selected drive pricing

Estimated market size: RMB 200 million

Typical premium: RMB 2,000 – RMB 12,000

• Cover is mostly sold to individuals, most likely middle-class

and affluent Chinese

• Some products assume partial cover for services by SHI;

other assume no SHI cover

• Few insureres have built distribution channels able to

support ‘high-advice’ products

*Graphic not to scale

~1%

<1%

13

Cash allowance products and travel health cover

Market size of existing

PHI product categories

Source: Munich Health (2013); Mercer (2012)

Hospital cash and surgical cash products

Travel health cover

RMB 86 billion*

Estimated market size: RMB 1 billion

Typical premium: RMB 100 – RMB 500

• Lump sum cash payments in case of

hospitalization or surgery

Estimated market size: RMB 300 million

Typical premium: RMB 1,500 – RMB 2,000

• Travel cover for clients that require

covcer outside of Mainland China

*Graphic not to scale

<1%

~1%

14

Need for Private Health Insurance – voice of the customer

Source: McKinsey consulting report (2009)

Market Research Insights

Core issues Details

Consumers perceive serious shortcomings in healthcare system

BMI coverage insufficient Low IP limit and low OP cover ratio

Insufficient BMI scope Some off-schedule tests, drugs, devices are not covered

Lack of access Poor access, long queuing time, hongbao

Consumers rely on commercial insurance products for additional security

Critical Illness products Perceived risk of a significant shortfall when diagnosis is a critical illness

Accidental Medical Reimbursement products

Uncertainty of expense for accident or emergency

Hospital cash products Provides cash to help cover shortfall and “navigate system”

Medical Reimbursement products

Traditionally offered as group BMI-supplementary product

Existing products address need only partially

1. Insufficient number of conditions covered for critical illness products.2. Complex and ambiguous coverage terms.3. Lack of a “suitable product for me”.

IP = in-patient; OP = out-patient; BMI = Basic Medical Insurance, the Chinese government insurance programs

15

1

2

3

Massive unmet need

Customers turn to PHI, but existing market in its infancy

Most dominant PHI category, Critical Illness, meets only limited needs

4 True financial risk relating to healthcare costs in China

5 Traditional PHI products offset OOP liability only partly

Agenda

16

Cheap product but meets only limited needs:# 1 – Sum insured does not reflect expected OOP cost

Different conditions have very

different cost profiles …

• DRG 16 – Diseases and disorders of

blood, blood forming organs,

immunological disorders

• DRG 21 – Injuries, poisoning, and toxic

effects of drugs

• DRG 22 – Burns

0%

50%

100%

150%

200%

250%

300%

350%

DRG 16

DRG 21

DRG 22

Source: Analysis of SHI hospital claims of Ping An insured clients (2010)

… and sum insured is frequently

higher than OOP costs for CI events

• Expected actual OOP costs for CI events

far less than sum insured

• Only 7 of the 20 most expensive claims

had OOP costs exceeding typical sum

insured (RMB 100,000) and not all of

these events would be CI events

0%

5%

10%

15%

20%

25%

1 2 3 4 5 6 7 8 9 10

OOP costs as % of sum insured*

distribution by decile

*for RMB 100,000 sum insured

Average IP claims

cost : RMB 9,545

17

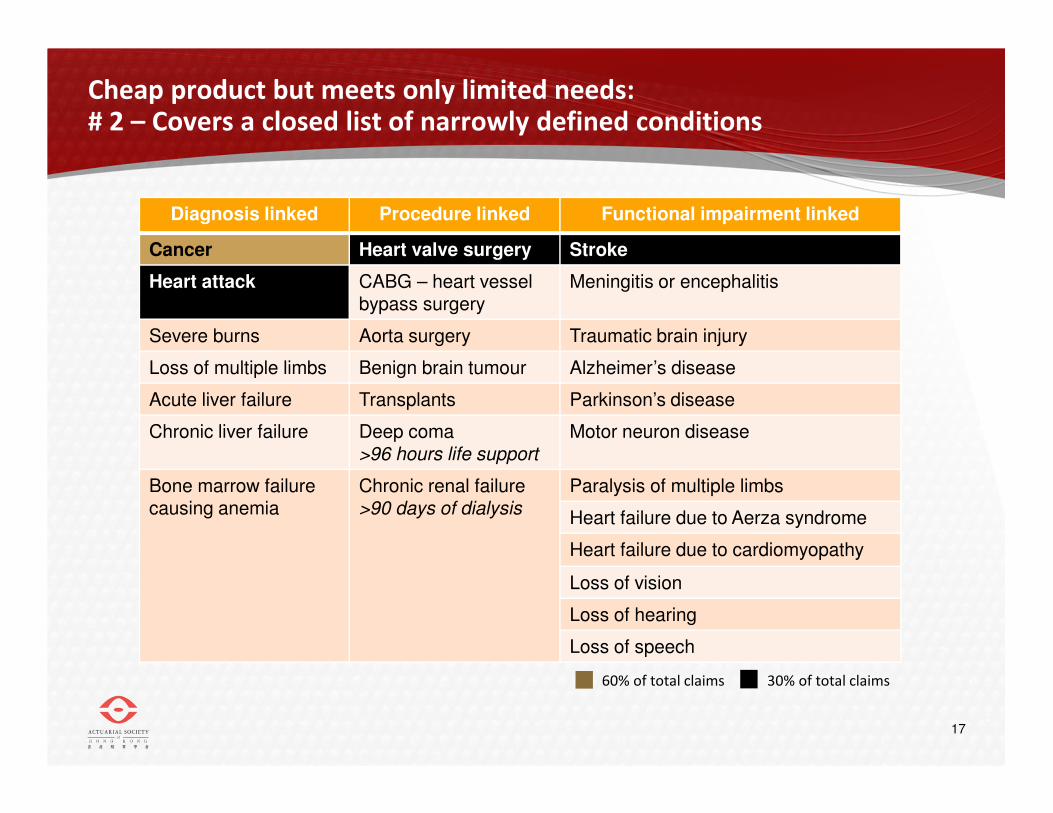

Cheap product but meets only limited needs:# 2 – Covers a closed list of narrowly defined conditions

Diagnosis linked Procedure linked Functional impairment linked

Cancer Heart valve surgery Stroke

Heart attack CABG – heart vessel bypass surgery

Meningitis or encephalitis

Severe burns Aorta surgery Traumatic brain injury

Loss of multiple limbs Benign brain tumour Alzheimer’s disease

Acute liver failure Transplants Parkinson’s disease

Chronic liver failure Deep coma >96 hours life support

Motor neuron disease

Bone marrow failure causing anemia

Chronic renal failure >90 days of dialysis

Paralysis of multiple limbs

Heart failure due to Aerza syndrome

Heart failure due to cardiomyopathy

Loss of vision

Loss of hearing

Loss of speech

60% of total claims 30% of total claims

18

Cheap product but meets only limited needs:# 3 – Low probability of meeting CI product criteria

CI insurance type: low incidence

and known sum insured

• Industry has a deep understanding of

utilization trends

• Known sum insured, so no CPE

uncertainty

Source: Munich Health; PAH analysis of high-end IP claims (2012)

Reimbursement-type: significant

utlization rate and CPE uncertainty

• Uncertain utilization rate – PAH

experience typical annual admission

rates in the 8% - 15% range

• CPE varies greatly by coverage area and

setting – surprisingly costly Public

Hospitals’ VIP setting

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

0-10 11-20 21-30 31-40 41-50 51-60 61-70 71-75

Typical RMB value paid out

per RMB 1,000 sum insured

distribution by age band

Males

Females

CPE = Cost per Event

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

Global HongKong

LuxuryPrivate

Private PublicVIP

Public

Mainland (excl Lux Priv)

Mainland (incl Lux Priv)

Regional and Global

CPE by setting Plan’s coverage area:

19

Cheap product but meets only limited needs:# 4 – CI products may impose a heavy cash flow burden

Actual case study:

52 year-old male insured by Ping An

Treated in a public hospital

Source: Analysis of SHI hospital claims of Ping An insured clients (2010)

Day 1 Day 122 Day 180

Stroke

Hospitalization

Discharge

Hospital claim settled

112 days hospitalization

Total cost = RMB 218,855

16% of total costs OOP

7% of costs off-schedule

1 2Evaluation of severity of

functional impairment3

20

Cheap product but meets only limited needs:# 5 – CI products does not facilitate access to care

Ou

tpa

tien

t ha

llsIn

pa

tien

t wa

rds

General consultation Special consultation

21

Cheap product but meets only limited needs:# 5 – CI products does not facilitate access to care

• Assistant chief doctors and higher level in tier-3

hospitals

• Average diagnosis time exceeds 30min

• Detailed explanation about pathology, status of

illness, treatment scheme and self health care

• Separate room, one-on-one communication

• Seniority of doctors varies greatly

• Short diagnosis time (generally within 5min)

• Lack of sufficient communication

• Surrounded by other awaiting patients, meaning

case privacy cannot be guaranteed

General consultation Special consultation

22

1

2

3

Massive unmet need

Customers turn to PHI, but existing market in its infancy

Most dominant PHI category, Critical Illness, meets only limited needs

4 True financial risk relating to healthcare costs in China

5 Traditional PHI products offset OOP liability only partly

Agenda

23

Real impact of healthcare costs in China:More than half of all SHI claims value paid OOP

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2 3 4 5 6 7 8 9 10

Source: Analysis of SHI hospital claims of Ping An insured clients (2010)

Ratio of costs by decile Cost type

Type A

SHI paid

Type B

SHI shortfalls

Type C

off-schedule

Ratios of which for

48%

28%

24%

overall non-CI

events

CI events

84%

88%

90%

16%

12%

10%

All costs 87% 13%

24

Real impact of healthcare costs in China:CI coverage would either under or over-insure clients

Source: Analysis of SHI hospital claims of Ping An insured clients (2010); CI events modeled

Over-insured: CI payouts typically

exceeds actual OOP costs

• For most CI events, the payout reeceived

would far exceed the event cost

0%

5%

10%

15%

20%

25%

1 2 3 4 5 6 7 8 9 10

OOP costs as % of sum insured*

distribution by decile

Under-insured: low probability of

hospitalization being a CI event

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

0.16

1 2 3 4 5 6 7 8 9 10

• Model classified 5.3% of admissions in

sample as potential CI events

• Higher cost events are more likely CI

events than lower cost events

Probability of hospitalization a CI event

distribution by decile

*for RMB 100,000 sum insured

Overall probability of

being a CI event

25

Real impact of healthcare costs in China:Analysis of 20 most expensive claims

Diagnosis LOS Total Cost Type A Type B Type CAcute pancreatitis 72 296 333 45 815 172 211 78 307

Chronic liver disease 95 263 354 52 290 72 858 138 207

Rectal cancer - early stage 8 228 676 93 371 31 530 103 776

Stroke 112 218 855 183 815 20 102 14 939

Carotid artery injury 10 151 006 11 412 2 445 137 149

Aorta aneurism 15 131 062 16 924 9 689 104 448

Brain tumour 52 127 570 - 125 770 1 800

Stomach cancer - early stage 41 114 197 31 231 34 078 48 887

Pneumonia 46 110 122 59 500 47 694 2 928

Stroke 22 107 958 49 314 14 527 44 117

Aorta aneurism 40 107 864 - - 107 864

Colon cancer - early stage 22 105 535 57 295 41 429 6 811

Epilepsy 50 104 352 33 534 8 697 62 121

Liver cancer 57 95 361 38 064 11 114 46 183

Stomach cancer - early stage 48 92 725 55 105 15 514 22 107

Heart valve disease 73 90 347 62 018 23 468 4 860

Breast cancer - early stage 121 87 052 57 124 26 277 3 651

Heart valve disease 29 85 920 64 193 19 813 1 914

Heart vessel disease 3 85 023 - - 85 023

Stroke 14 80 795 27 545 11 369 41 881

TOTAL COST 2 684 107 938 548 688 586 1 056 973

Category share of total cost 35% 26% 39%CI cost as ratio of total category cost 27% 27% 32% 23%

Source: Analysis of SHI hospital claims of Ping An insured clients (2010) LOS = length of stay

26

Case #1: 30 year-old maleK85.9 – Acute Pancreatitis

Source: Analysis of SHI hospital claims of Ping An insured clients (2010) LOS = length of stay

Likely conclusion:72 days hospitalization

85% of total costs OOP

26% of costs off-schedule

Pancreatitis is not a

standard CI condition and

this event would

therefore not qualify for

a CI payout

Diagnosis LOS Total Cost Type A Type B Type CAcute pancreatitis 72 296 333 45 815 172 211 78 307

Chronic liver disease 95 263 354 52 290 72 858 138 207

Rectal cancer - early stage 8 228 676 93 371 31 530 103 776

Stroke 112 218 855 183 815 20 102 14 939

Carotid artery injury 10 151 006 11 412 2 445 137 149

Aorta aneurism 15 131 062 16 924 9 689 104 448

Brain tumour 52 127 570 - 125 770 1 800

Stomach cancer - early stage 41 114 197 31 231 34 078 48 887

Pneumonia 46 110 122 59 500 47 694 2 928

Stroke 22 107 958 49 314 14 527 44 117

Aorta aneurism 40 107 864 - - 107 864

Colon cancer - early stage 22 105 535 57 295 41 429 6 811

Epilepsy 50 104 352 33 534 8 697 62 121

Liver cancer 57 95 361 38 064 11 114 46 183

Stomach cancer - early stage 48 92 725 55 105 15 514 22 107

Heart valve disease 73 90 347 62 018 23 468 4 860

Breast cancer - early stage 121 87 052 57 124 26 277 3 651

Heart valve disease 29 85 920 64 193 19 813 1 914

Heart vessel disease 3 85 023 - - 85 023

Stroke 14 80 795 27 545 11 369 41 881

TOTAL COST 2 684 107 938 548 688 586 1 056 973

Category share of total cost 35% 26% 39%CI cost as ratio of total category cost 27% 27% 32% 23%

27

Case #2: 55 year-old femaleD01.2 – Carcinoma in situ: rectum

Source: Analysis of SHI hospital claims of Ping An insured clients (2010) LOS = length of stay

Likely conclusion:8 days hospitalization

59% of total costs OOP

45% of costs off-schedule

Cancer is a standard CI

condition but carcinoma

in situ (early stage

cancer) is excluded and

this event would

therefore not qualify for

a CI payout

Diagnosis LOS Total Cost Type A Type B Type CAcute pancreatitis 72 296 333 45 815 172 211 78 307

Chronic liver disease 95 263 354 52 290 72 858 138 207

Rectal cancer - early stage 8 228 676 93 371 31 530 103 776

Stroke 112 218 855 183 815 20 102 14 939

Carotid artery injury 10 151 006 11 412 2 445 137 149

Aorta aneurism 15 131 062 16 924 9 689 104 448

Brain tumour 52 127 570 - 125 770 1 800

Stomach cancer - early stage 41 114 197 31 231 34 078 48 887

Pneumonia 46 110 122 59 500 47 694 2 928

Stroke 22 107 958 49 314 14 527 44 117

Aorta aneurism 40 107 864 - - 107 864

Colon cancer - early stage 22 105 535 57 295 41 429 6 811

Epilepsy 50 104 352 33 534 8 697 62 121

Liver cancer 57 95 361 38 064 11 114 46 183

Stomach cancer - early stage 48 92 725 55 105 15 514 22 107

Heart valve disease 73 90 347 62 018 23 468 4 860

Breast cancer - early stage 121 87 052 57 124 26 277 3 651

Heart valve disease 29 85 920 64 193 19 813 1 914

Heart vessel disease 3 85 023 - - 85 023

Stroke 14 80 795 27 545 11 369 41 881

TOTAL COST 2 684 107 938 548 688 586 1 056 973

Category share of total cost 35% 26% 39%CI cost as ratio of total category cost 27% 27% 32% 23%

28

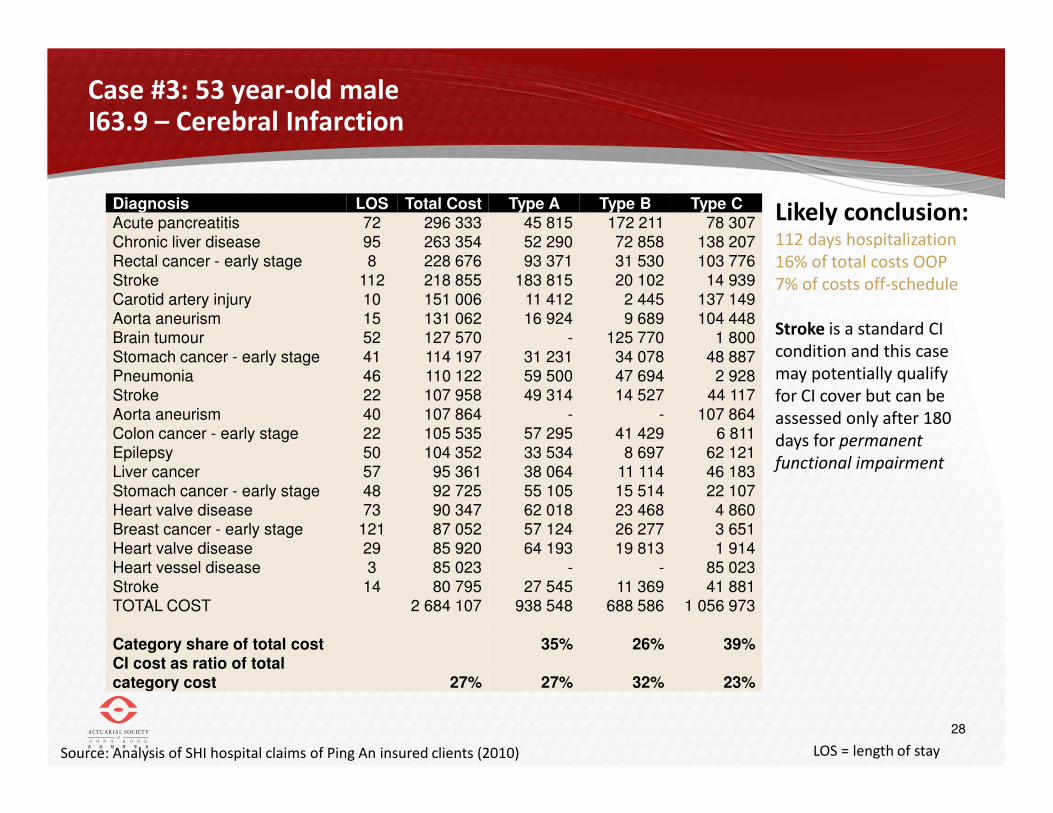

Case #3: 53 year-old maleI63.9 – Cerebral Infarction

Source: Analysis of SHI hospital claims of Ping An insured clients (2010) LOS = length of stay

Likely conclusion:112 days hospitalization

16% of total costs OOP

7% of costs off-schedule

Stroke is a standard CI

condition and this case

may potentially qualify

for CI cover but can be

assessed only after 180

days for permanent

functional impairment

Diagnosis LOS Total Cost Type A Type B Type CAcute pancreatitis 72 296 333 45 815 172 211 78 307

Chronic liver disease 95 263 354 52 290 72 858 138 207

Rectal cancer - early stage 8 228 676 93 371 31 530 103 776

Stroke 112 218 855 183 815 20 102 14 939

Carotid artery injury 10 151 006 11 412 2 445 137 149

Aorta aneurism 15 131 062 16 924 9 689 104 448

Brain tumour 52 127 570 - 125 770 1 800

Stomach cancer - early stage 41 114 197 31 231 34 078 48 887

Pneumonia 46 110 122 59 500 47 694 2 928

Stroke 22 107 958 49 314 14 527 44 117

Aorta aneurism 40 107 864 - - 107 864

Colon cancer - early stage 22 105 535 57 295 41 429 6 811

Epilepsy 50 104 352 33 534 8 697 62 121

Liver cancer 57 95 361 38 064 11 114 46 183

Stomach cancer - early stage 48 92 725 55 105 15 514 22 107

Heart valve disease 73 90 347 62 018 23 468 4 860

Breast cancer - early stage 121 87 052 57 124 26 277 3 651

Heart valve disease 29 85 920 64 193 19 813 1 914

Heart vessel disease 3 85 023 - - 85 023

Stroke 14 80 795 27 545 11 369 41 881

TOTAL COST 2 684 107 938 548 688 586 1 056 973

Category share of total cost 35% 26% 39%CI cost as ratio of total category cost 27% 27% 32% 23%

29

1

2

3

Massive unmet need

Customers turn to PHI, but existing market in its infancy

Most dominant PHI category, Critical Illness, meets only limited needs

4 True financial risk relating to healthcare costs in China

5 Traditional PHI products offset OOP liability only partly

Agenda

30

Real impact of healthcare costs in China:Very substantial OOP liability

-

5,000

10,000

15,000

20,000

25,000

1 2 3 4 5 6 7 8 9 10

Value of OOP liabilitydistribution by decile

Average OOP liability

in RMB

Type C

off-schedule costs

Type B

SHI shortfalls

Source: Analysis of SHI hospital claims of Ping An insured clients (2010)

OOP as % of

total cost78% 51%

31

Existing insurance options decrease OOP liability:SHI coverage leave clients very exposed

Source: Analysis of SHI hospital claims of Ping An insured clients (2010)

Ratio of OOP liabilitydistribution by decile

Average OOP liability

as % of total cost

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1 2 3 4 5 6 7 8 9 10

SHI cover only

32

Existing insurance options decrease OOP liability:Adding CI coverage decrease OOP marginally

Ratio of OOP liabilitydistribution by decile

Average OOP liability

as % of total cost

Model

assumptions:

1. CI cover with RMB 100,000 sum insured

2. CI events modeled using PAH classification algoritm

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1 2 3 4 5 6 7 8 9 10

SHI cover only

SHI + CI

Source: Analysis of SHI hospital claims of Ping An insured clients (2010); CI events modeled

33

Existing insurance options decrease OOP liability:SHI supplementary cover more effective to decrease OOP

Source: Analysis of SHI hospital claims of Ping An insured clients (2010); CI events modeled

Ratio of OOP liabilitydistribution by decile

Average OOP liability

as % of total cost

Model

assumptions:

1. SHI supplementary cover with RMB 9,000 annual limit

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1 2 3 4 5 6 7 8 9 10

SHI cover only

SHI + SHI-

supplementary

34

Existing insurance options decrease OOP liability:Adding CI to SHI supplementary cover has marginal impact

Source: Analysis of SHI hospital claims of Ping An insured clients (2010); CI events modeled

Ratio of OOP liabilitydistribution by decile

Average OOP liability

as % of total cost

Model

assumptions:

1. SHI supplementary cover with RMB 9,000 annual limit

2. CI cover with RMB 100,000 sum insured

3. CI events modeled using PAH classification algoritm

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1 2 3 4 5 6 7 8 9 10

SHI cover only

SHI + SHI-

supplementary + CI

35

Existing insurance options decrease OOP liability:Comprehensive reimbursement insurance close all gaps

Source: Analysis of SHI hospital claims of Ping An insured clients (2010); CI events modeled

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1 2 3 4 5 6 7 8 9 10

Ratio of OOP liabilitydistribution by decile

Average OOP liability

as % of total cost

Model

assumptions:

1. Comprehensive reimbursement-type insurance with annual

limit of RMB 500,000

2. No SHI entitlement required

SHI cover only

Comprehensive

reimursement type

insurance product

36

Introducing Ping An Health’s latest thinking:the Comprehensive Health Protector

Helps make clients healthier by:

• Understanding their health

• Making it easier to get healthy

• Making it cheaper to get healthy

• Helping them track their progress

towards health goals

• Providing rewards to keep them

motivated

Offers comprehensive cover both on-

schedule and off-schedule costs are

covered up to high annual limits –

ensuring any gaps are covered in full

Improves access to quality care by

extending cover to treatment in VIP

wards of public hospitals and making

available expert guidance on accessing

hospitals and famous specialists

Vitality Health Investment Account offers

tangible value that helps clients build up

equity and overcome lack of familiarity

with pure protection insurance

37

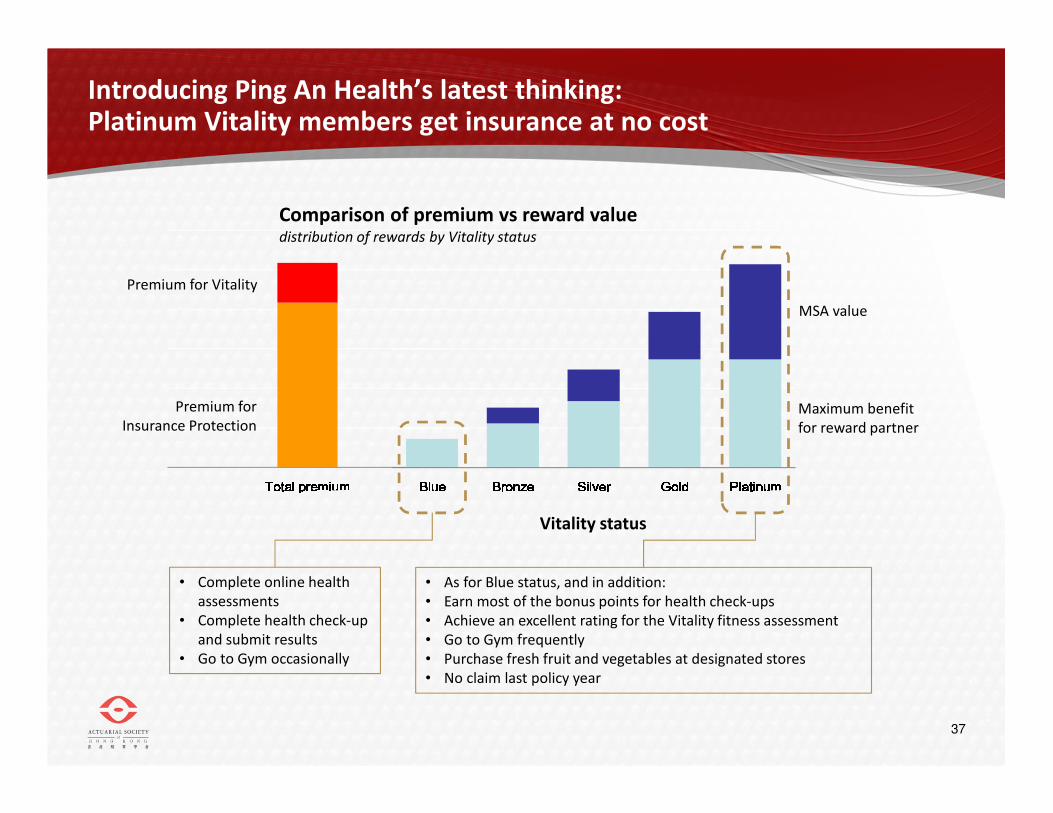

Introducing Ping An Health’s latest thinking:Platinum Vitality members get insurance at no cost

Total premiumTotal premiumTotal premiumTotal premium BlueBlueBlueBlue BronzeBronzeBronzeBronze SilverSilverSilverSilver GoldGoldGoldGold PlatinumPlatinumPlatinumPlatinumMSA value

Maximum benefit

for reward partner

Premium for Vitality

Premium for

Insurance Protection

Comparison of premium vs reward valuedistribution of rewards by Vitality status

Vitality status

• Complete online health

assessments

• Complete health check-up

and submit results

• Go to Gym occasionally

• As for Blue status, and in addition:

• Earn most of the bonus points for health check-ups

• Achieve an excellent rating for the Vitality fitness assessment

• Go to Gym frequently

• Purchase fresh fruit and vegetables at designated stores

• No claim last policy year

Towards a Comprehensive Private Health Insurance market in China

The Actuarial Society of Hong Kong

Dr. Andrew MurraySenior Vice President: Strategic Risk Management, Discovery International

7 March 2013