Topic 5 China's Capital Markets I - zongxinqian.com · Topic 5 China’s Capital Markets I Zongxin...

139

Topic 5 China’s Capital Markets I Zongxin Qian Brief history 1978-1992 1993-1998 1999-2007 Reforms Non-tradable shares Issuance system Impact assessment Market structure Current market situation Supervision framework Topic 5 China’s Capital Markets I Zongxin Qian School of Finance, Renmin University of China July 10, 2014

Transcript of Topic 5 China's Capital Markets I - zongxinqian.com · Topic 5 China’s Capital Markets I Zongxin...

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Topic 5 China’s Capital Markets I

Zongxin Qian

School of Finance, Renmin University of China

July 10, 2014

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Table of Contents

1 Brief history1978-19921993-19981999-2007

2 ReformsNon-tradable sharesIssuance systemImpact assessment

3 Market structure

4 Current market situation

5 Supervision framework

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Three phases

The CRSC divides the history of China’s capital markets intothree phases

1978-1992, China’s capital markets began to emerge

1993-1998, National capital markets began to emerge

1999-2007, Further regulation and development of thecapital markets

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Three phases

The CRSC divides the history of China’s capital markets intothree phases

1978-1992, China’s capital markets began to emerge

1993-1998, National capital markets began to emerge

1999-2007, Further regulation and development of thecapital markets

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Three phases

The CRSC divides the history of China’s capital markets intothree phases

1978-1992, China’s capital markets began to emerge

1993-1998, National capital markets began to emerge

1999-2007, Further regulation and development of thecapital markets

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Three phases

The CRSC divides the history of China’s capital markets intothree phases

1978-1992, China’s capital markets began to emerge

1993-1998, National capital markets began to emerge

1999-2007, Further regulation and development of thecapital markets

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1978-1992: the emergence of stocks, bonds andfutures

1986, Provisions for Furthering Reform and RevitalizingEnterprises: SOE restructuring became a national strategy

1981, treasury bonds

1982, enterprise bonds

1984, financial bonds

1990, forward contracts (Zhengzhou Grain WholesaleMarket)

1992, “Standard Contract for Special Grade AluminumFutures”Shenzhen Nonferrous Metals Futures Exchange

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1978-1992: the emergence of stocks, bonds andfutures

1986, Provisions for Furthering Reform and RevitalizingEnterprises: SOE restructuring became a national strategy

1981, treasury bonds

1982, enterprise bonds

1984, financial bonds

1990, forward contracts (Zhengzhou Grain WholesaleMarket)

1992, “Standard Contract for Special Grade AluminumFutures”Shenzhen Nonferrous Metals Futures Exchange

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1978-1992: the emergence of stocks, bonds andfutures

1986, Provisions for Furthering Reform and RevitalizingEnterprises: SOE restructuring became a national strategy

1981, treasury bonds

1982, enterprise bonds

1984, financial bonds

1990, forward contracts (Zhengzhou Grain WholesaleMarket)

1992, “Standard Contract for Special Grade AluminumFutures”Shenzhen Nonferrous Metals Futures Exchange

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1978-1992: the emergence of stocks, bonds andfutures

1986, Provisions for Furthering Reform and RevitalizingEnterprises: SOE restructuring became a national strategy

1981, treasury bonds

1982, enterprise bonds

1984, financial bonds

1990, forward contracts (Zhengzhou Grain WholesaleMarket)

1992, “Standard Contract for Special Grade AluminumFutures”Shenzhen Nonferrous Metals Futures Exchange

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1978-1992: the emergence of stocks, bonds andfutures

1986, Provisions for Furthering Reform and RevitalizingEnterprises: SOE restructuring became a national strategy

1981, treasury bonds

1982, enterprise bonds

1984, financial bonds

1990, forward contracts (Zhengzhou Grain WholesaleMarket)

1992, “Standard Contract for Special Grade AluminumFutures”Shenzhen Nonferrous Metals Futures Exchange

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1978-1992: the emergence of stocks, bonds andfutures

1986, Provisions for Furthering Reform and RevitalizingEnterprises: SOE restructuring became a national strategy

1981, treasury bonds

1982, enterprise bonds

1984, financial bonds

1990, forward contracts (Zhengzhou Grain WholesaleMarket)

1992, “Standard Contract for Special Grade AluminumFutures”Shenzhen Nonferrous Metals Futures Exchange

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1978-1992: the emergence of stocks, bonds andfutures

1986, Provisions for Furthering Reform and RevitalizingEnterprises: SOE restructuring became a national strategy

1981, treasury bonds

1982, enterprise bonds

1984, financial bonds

1990, forward contracts (Zhengzhou Grain WholesaleMarket)

1992, “Standard Contract for Special Grade AluminumFutures”Shenzhen Nonferrous Metals Futures Exchange

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

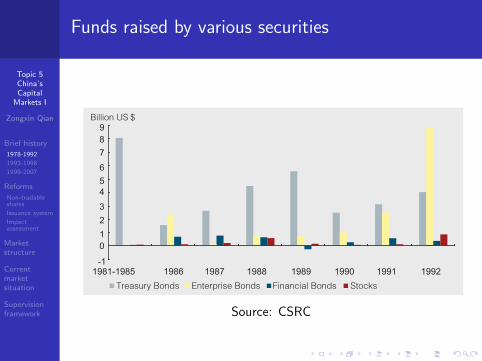

Funds raised by various securities

Figure 1.1 Funds raised by various securities, 1981-1992Source: CSRC

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1978-1992: the emergence of secondary markets

First brokage service: Shenyang Trust and InvestmentCorporation (1986)

First OTC trading of shares: Jing’an District Branch ofthe Shanghai Trust and Investment Company (1986)

OTC trading of treasury bonds allowed (1988)

Shanghai and Shenzhen securities exchange (1990)

Shanghai and Shenzhen composite index (1991; startedfrom 100 points).

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1978-1992: the emergence of secondary markets

First brokage service: Shenyang Trust and InvestmentCorporation (1986)

First OTC trading of shares: Jing’an District Branch ofthe Shanghai Trust and Investment Company (1986)

OTC trading of treasury bonds allowed (1988)

Shanghai and Shenzhen securities exchange (1990)

Shanghai and Shenzhen composite index (1991; startedfrom 100 points).

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1978-1992: the emergence of secondary markets

First brokage service: Shenyang Trust and InvestmentCorporation (1986)

First OTC trading of shares: Jing’an District Branch ofthe Shanghai Trust and Investment Company (1986)

OTC trading of treasury bonds allowed (1988)

Shanghai and Shenzhen securities exchange (1990)

Shanghai and Shenzhen composite index (1991; startedfrom 100 points).

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1978-1992: the emergence of secondary markets

First brokage service: Shenyang Trust and InvestmentCorporation (1986)

First OTC trading of shares: Jing’an District Branch ofthe Shanghai Trust and Investment Company (1986)

OTC trading of treasury bonds allowed (1988)

Shanghai and Shenzhen securities exchange (1990)

Shanghai and Shenzhen composite index (1991; startedfrom 100 points).

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1978-1992: the emergence of secondary markets

First brokage service: Shenyang Trust and InvestmentCorporation (1986)

First OTC trading of shares: Jing’an District Branch ofthe Shanghai Trust and Investment Company (1986)

OTC trading of treasury bonds allowed (1988)

Shanghai and Shenzhen securities exchange (1990)

Shanghai and Shenzhen composite index (1991; startedfrom 100 points).

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1978-1992: the emergence of secondary markets

First brokage service: Shenyang Trust and InvestmentCorporation (1986)

First OTC trading of shares: Jing’an District Branch ofthe Shanghai Trust and Investment Company (1986)

OTC trading of treasury bonds allowed (1988)

Shanghai and Shenzhen securities exchange (1990)

Shanghai and Shenzhen composite index (1991; startedfrom 100 points).

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

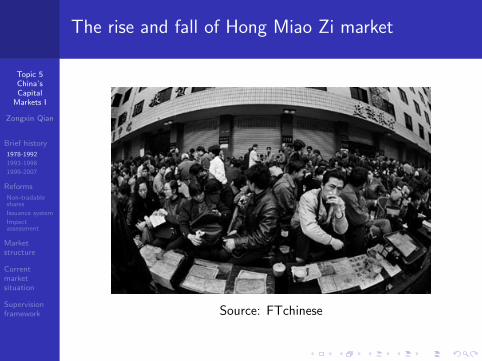

The rise and fall of Hong Miao Zi market

Source: FTchinese

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

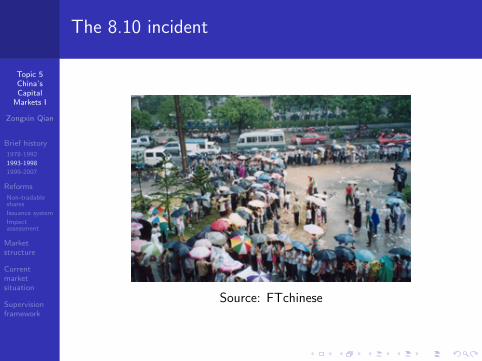

The 8.10 incident

Source: FTchinese

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The lottery ticket for stock purchase

Source: FTchinese

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1993-1998: development of the regulatoryframework

May 1992, Securities Supervision Office of PBC

October 1992, SCSC and CSRC

November 1997, separation of operation and supervisionof banking, securities, and insuranceThis is similar to the Glass-Steagall Act (1933-1999) ofthe US.

April 1998, consolidating the supervisory functions ofSCSC and PBC into the CSRC

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1993-1998: development of the regulatoryframework

May 1992, Securities Supervision Office of PBC

October 1992, SCSC and CSRC

November 1997, separation of operation and supervisionof banking, securities, and insuranceThis is similar to the Glass-Steagall Act (1933-1999) ofthe US.

April 1998, consolidating the supervisory functions ofSCSC and PBC into the CSRC

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1993-1998: development of the regulatoryframework

May 1992, Securities Supervision Office of PBC

October 1992, SCSC and CSRC

November 1997, separation of operation and supervisionof banking, securities, and insuranceThis is similar to the Glass-Steagall Act (1933-1999) ofthe US.

April 1998, consolidating the supervisory functions ofSCSC and PBC into the CSRC

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1993-1998: development of the regulatoryframework

May 1992, Securities Supervision Office of PBC

October 1992, SCSC and CSRC

November 1997, separation of operation and supervisionof banking, securities, and insuranceThis is similar to the Glass-Steagall Act (1933-1999) ofthe US.

April 1998, consolidating the supervisory functions ofSCSC and PBC into the CSRC

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1993-1998: development of the regulatoryframework

May 1992, Securities Supervision Office of PBC

October 1992, SCSC and CSRC

November 1997, separation of operation and supervisionof banking, securities, and insuranceThis is similar to the Glass-Steagall Act (1933-1999) ofthe US.

April 1998, consolidating the supervisory functions ofSCSC and PBC into the CSRC

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1993-1998: development of the legal framework

April 1993, Provisional Regulation on the Issuing andTrading of Shares

June 1993, Implementation Rules on InformationDisclosures of Companies Issuing Public Shares

August 1993, Provisional Measures on ProhibitingFraudulent Conducts Relating to Securities

July 1994, Company Law (issuance and transfer of shares)

October 1996, Circular on Prohibiting Securities MarketManipulation

November 1997, Provisional Administrative Procedures onSecurities Investment Funds

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1993-1998: development of the legal framework

April 1993, Provisional Regulation on the Issuing andTrading of Shares

June 1993, Implementation Rules on InformationDisclosures of Companies Issuing Public Shares

August 1993, Provisional Measures on ProhibitingFraudulent Conducts Relating to Securities

July 1994, Company Law (issuance and transfer of shares)

October 1996, Circular on Prohibiting Securities MarketManipulation

November 1997, Provisional Administrative Procedures onSecurities Investment Funds

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1993-1998: stock issuance and IPO pricing

a quota on the maximum number of shares that could beissued each year

provincial governments and industry supervising bodiesrecommend enterprises for listing

The CSRC would then give final approval on publicofferings

Issue price of a new share = Profit after tax per share×price earning ratio of the issue

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1993-1998: stock issuance and IPO pricing

a quota on the maximum number of shares that could beissued each year

provincial governments and industry supervising bodiesrecommend enterprises for listing

The CSRC would then give final approval on publicofferings

Issue price of a new share = Profit after tax per share×price earning ratio of the issue

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1993-1998: stock issuance and IPO pricing

a quota on the maximum number of shares that could beissued each year

provincial governments and industry supervising bodiesrecommend enterprises for listing

The CSRC would then give final approval on publicofferings

Issue price of a new share = Profit after tax per share×price earning ratio of the issue

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1993-1998: stock issuance and IPO pricing

a quota on the maximum number of shares that could beissued each year

provincial governments and industry supervising bodiesrecommend enterprises for listing

The CSRC would then give final approval on publicofferings

Issue price of a new share = Profit after tax per share×price earning ratio of the issue

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1993-1998: stock issuance and IPO pricing

a quota on the maximum number of shares that could beissued each year

provincial governments and industry supervising bodiesrecommend enterprises for listing

The CSRC would then give final approval on publicofferings

Issue price of a new share = Profit after tax per share×price earning ratio of the issue

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Funds raised by various securities

Source: CSRC

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

financial openness

B-shares: domestically-listed shares, denominated inRenminbi but subscribed to and traded in US or HongKong dollars by overseas investors.

listing of domestic companies in Hong Kong (H-shares)

listing of domestic companies in New York (N shares)

listing of PRC companies incorporated overseas in HongKong (red chips)

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

financial openness

B-shares: domestically-listed shares, denominated inRenminbi but subscribed to and traded in US or HongKong dollars by overseas investors.

listing of domestic companies in Hong Kong (H-shares)

listing of domestic companies in New York (N shares)

listing of PRC companies incorporated overseas in HongKong (red chips)

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

financial openness

B-shares: domestically-listed shares, denominated inRenminbi but subscribed to and traded in US or HongKong dollars by overseas investors.

listing of domestic companies in Hong Kong (H-shares)

listing of domestic companies in New York (N shares)

listing of PRC companies incorporated overseas in HongKong (red chips)

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Initial developments of the futures markets

December 1992, Treasury bond (T-bond) futures wereintroduced

November 1993, Circular on Preventing RecklessDevelopment of the Futures Market

May 1994, Instructions Requested for Certain Opinions onResolutely Preventing Reckless Development of theFutures Market

1995, 327 T-Bond Futures incident

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Initial developments of the futures markets

December 1992, Treasury bond (T-bond) futures wereintroduced

November 1993, Circular on Preventing RecklessDevelopment of the Futures Market

May 1994, Instructions Requested for Certain Opinions onResolutely Preventing Reckless Development of theFutures Market

1995, 327 T-Bond Futures incident

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Initial developments of the futures markets

December 1992, Treasury bond (T-bond) futures wereintroduced

November 1993, Circular on Preventing RecklessDevelopment of the Futures Market

May 1994, Instructions Requested for Certain Opinions onResolutely Preventing Reckless Development of theFutures Market

1995, 327 T-Bond Futures incident

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Initial developments of the futures markets

December 1992, Treasury bond (T-bond) futures wereintroduced

November 1993, Circular on Preventing RecklessDevelopment of the Futures Market

May 1994, Instructions Requested for Certain Opinions onResolutely Preventing Reckless Development of theFutures Market

1995, 327 T-Bond Futures incident

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

327 T-Bond Futures incident

327 is the series number of a futures contract on the3-year T-Bond to be delivered in June 1995

Background: high inflation in 1994 and the interest ratesubsidy as an inflation risk hedge

Market participants bet on the uncertainty surrounding thesubsidy

The futures margin was only 2.5%, three-monthannualized return of the was 20%.major players

1 long: China economic development Trust InvestmentCompany

2 short: Wangguo securities, Liaoning Guofa

From 16:22:13 to 16: 30, February 23, 1995, WanguoSecurities placed a massive sell order of 7 million contractsworth of USD 16.8 billion, which cut the closing price toUSD17.66, from the highest of USD18.12 that day

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

327 T-Bond Futures incident

327 is the series number of a futures contract on the3-year T-Bond to be delivered in June 1995

Background: high inflation in 1994 and the interest ratesubsidy as an inflation risk hedge

Market participants bet on the uncertainty surrounding thesubsidy

The futures margin was only 2.5%, three-monthannualized return of the was 20%.major players

1 long: China economic development Trust InvestmentCompany

2 short: Wangguo securities, Liaoning Guofa

From 16:22:13 to 16: 30, February 23, 1995, WanguoSecurities placed a massive sell order of 7 million contractsworth of USD 16.8 billion, which cut the closing price toUSD17.66, from the highest of USD18.12 that day

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

327 T-Bond Futures incident

327 is the series number of a futures contract on the3-year T-Bond to be delivered in June 1995

Background: high inflation in 1994 and the interest ratesubsidy as an inflation risk hedge

Market participants bet on the uncertainty surrounding thesubsidy

The futures margin was only 2.5%, three-monthannualized return of the was 20%.major players

1 long: China economic development Trust InvestmentCompany

2 short: Wangguo securities, Liaoning Guofa

From 16:22:13 to 16: 30, February 23, 1995, WanguoSecurities placed a massive sell order of 7 million contractsworth of USD 16.8 billion, which cut the closing price toUSD17.66, from the highest of USD18.12 that day

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

327 T-Bond Futures incident

327 is the series number of a futures contract on the3-year T-Bond to be delivered in June 1995

Background: high inflation in 1994 and the interest ratesubsidy as an inflation risk hedge

Market participants bet on the uncertainty surrounding thesubsidy

The futures margin was only 2.5%, three-monthannualized return of the was 20%.major players

1 long: China economic development Trust InvestmentCompany

2 short: Wangguo securities, Liaoning Guofa

From 16:22:13 to 16: 30, February 23, 1995, WanguoSecurities placed a massive sell order of 7 million contractsworth of USD 16.8 billion, which cut the closing price toUSD17.66, from the highest of USD18.12 that day

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

327 T-Bond Futures incident

327 is the series number of a futures contract on the3-year T-Bond to be delivered in June 1995

Background: high inflation in 1994 and the interest ratesubsidy as an inflation risk hedge

Market participants bet on the uncertainty surrounding thesubsidy

The futures margin was only 2.5%, three-monthannualized return of the was 20%.major players

1 long: China economic development Trust InvestmentCompany

2 short: Wangguo securities, Liaoning Guofa

From 16:22:13 to 16: 30, February 23, 1995, WanguoSecurities placed a massive sell order of 7 million contractsworth of USD 16.8 billion, which cut the closing price toUSD17.66, from the highest of USD18.12 that day

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

327 T-Bond Futures incident

327 is the series number of a futures contract on the3-year T-Bond to be delivered in June 1995

Background: high inflation in 1994 and the interest ratesubsidy as an inflation risk hedge

Market participants bet on the uncertainty surrounding thesubsidy

The futures margin was only 2.5%, three-monthannualized return of the was 20%.major players

1 long: China economic development Trust InvestmentCompany

2 short: Wangguo securities, Liaoning Guofa

From 16:22:13 to 16: 30, February 23, 1995, WanguoSecurities placed a massive sell order of 7 million contractsworth of USD 16.8 billion, which cut the closing price toUSD17.66, from the highest of USD18.12 that day

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The consequence of the 327 T-bond futuresincident

Source: Sina finance

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1999-2007: further regulations and developmentsof the markets

July 1999, The Securities Law

2002, special securities crime investigation bureau ofCSRC; Securities Crime Investigation Bureau of theMinistry of Public Security

2007, separate inspection and sanctions functions withinthe CSRC

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1999-2007: further regulations and developmentsof the markets

July 1999, The Securities Law

2002, special securities crime investigation bureau ofCSRC; Securities Crime Investigation Bureau of theMinistry of Public Security

2007, separate inspection and sanctions functions withinthe CSRC

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1999-2007: further regulations and developmentsof the markets

July 1999, The Securities Law

2002, special securities crime investigation bureau ofCSRC; Securities Crime Investigation Bureau of theMinistry of Public Security

2007, separate inspection and sanctions functions withinthe CSRC

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

1999-2007: further regulations and developmentsof the markets

July 1999, The Securities Law

2002, special securities crime investigation bureau ofCSRC; Securities Crime Investigation Bureau of theMinistry of Public Security

2007, separate inspection and sanctions functions withinthe CSRC

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Funds raised by various securities

Source: CSRC

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The Qiong Min Yuan incident

its share price rocketed 1,059% in 1996

USD 79 million of its capital surplus, as well as USD 68.1million out of the USD 68.7 million in profits as stated inits 1996 annual report, were fictitious

2003 (the year of SARS), 77.12 % of the shares of QiongMin Yuan was sold to Changchun Yeli at a price of zero

The reason for the zero price is that the evaluated netasset of the company was negative. However,according toan earlier report, the net asset by 1998 was 1 billion yuan.

2007, Min Yuan building was transferred to Beijing Yeli (8.24), then Beijing Yeli sold its assets to Huayuan real estateat the price of 521 million yuan (8. 30). The shares arethen sold to SOHO China at the price of 721 million yuan.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The Qiong Min Yuan incident

its share price rocketed 1,059% in 1996

USD 79 million of its capital surplus, as well as USD 68.1million out of the USD 68.7 million in profits as stated inits 1996 annual report, were fictitious

2003 (the year of SARS), 77.12 % of the shares of QiongMin Yuan was sold to Changchun Yeli at a price of zero

The reason for the zero price is that the evaluated netasset of the company was negative. However,according toan earlier report, the net asset by 1998 was 1 billion yuan.

2007, Min Yuan building was transferred to Beijing Yeli (8.24), then Beijing Yeli sold its assets to Huayuan real estateat the price of 521 million yuan (8. 30). The shares arethen sold to SOHO China at the price of 721 million yuan.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The Qiong Min Yuan incident

its share price rocketed 1,059% in 1996

USD 79 million of its capital surplus, as well as USD 68.1million out of the USD 68.7 million in profits as stated inits 1996 annual report, were fictitious

2003 (the year of SARS), 77.12 % of the shares of QiongMin Yuan was sold to Changchun Yeli at a price of zero

The reason for the zero price is that the evaluated netasset of the company was negative. However,according toan earlier report, the net asset by 1998 was 1 billion yuan.

2007, Min Yuan building was transferred to Beijing Yeli (8.24), then Beijing Yeli sold its assets to Huayuan real estateat the price of 521 million yuan (8. 30). The shares arethen sold to SOHO China at the price of 721 million yuan.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The Qiong Min Yuan incident

its share price rocketed 1,059% in 1996

USD 79 million of its capital surplus, as well as USD 68.1million out of the USD 68.7 million in profits as stated inits 1996 annual report, were fictitious

2003 (the year of SARS), 77.12 % of the shares of QiongMin Yuan was sold to Changchun Yeli at a price of zero

The reason for the zero price is that the evaluated netasset of the company was negative. However,according toan earlier report, the net asset by 1998 was 1 billion yuan.

2007, Min Yuan building was transferred to Beijing Yeli (8.24), then Beijing Yeli sold its assets to Huayuan real estateat the price of 521 million yuan (8. 30). The shares arethen sold to SOHO China at the price of 721 million yuan.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The Qiong Min Yuan incident

its share price rocketed 1,059% in 1996

USD 79 million of its capital surplus, as well as USD 68.1million out of the USD 68.7 million in profits as stated inits 1996 annual report, were fictitious

2003 (the year of SARS), 77.12 % of the shares of QiongMin Yuan was sold to Changchun Yeli at a price of zero

The reason for the zero price is that the evaluated netasset of the company was negative. However,according toan earlier report, the net asset by 1998 was 1 billion yuan.

2007, Min Yuan building was transferred to Beijing Yeli (8.24), then Beijing Yeli sold its assets to Huayuan real estateat the price of 521 million yuan (8. 30). The shares arethen sold to SOHO China at the price of 721 million yuan.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The Qiong Min Yuan incident

its share price rocketed 1,059% in 1996

USD 79 million of its capital surplus, as well as USD 68.1million out of the USD 68.7 million in profits as stated inits 1996 annual report, were fictitious

2003 (the year of SARS), 77.12 % of the shares of QiongMin Yuan was sold to Changchun Yeli at a price of zero

The reason for the zero price is that the evaluated netasset of the company was negative. However,according toan earlier report, the net asset by 1998 was 1 billion yuan.

2007, Min Yuan building was transferred to Beijing Yeli (8.24), then Beijing Yeli sold its assets to Huayuan real estateat the price of 521 million yuan (8. 30). The shares arethen sold to SOHO China at the price of 721 million yuan.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Minyuan building

Source: baidu photo

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The building was titled the NO.1 failed real estateproject

Source: baidu photo

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

SOHO2 concept figure

Source: baidu photo

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The Yin Guangxia Incident

1999-2000, the company announced false profits of USD 89.6million. The stock fell by the maximum permitted 10% eachday for 10 days when this was found out.

suspicious points

Annual profit rate in 2000 was reported to be 46%, morethan 20% higher than industry average

According to the reported export value, it should havetax-free benefit. But this was not in its financial reports.Its value-added tax was also too low to justify its hugeprofit.

The German importer was too small (with capital level ofonly 100,000 DM) to afford such a huge order (6 billionyuan)

The claimed production scale was not credible.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The Yin Guangxia Incident

1999-2000, the company announced false profits of USD 89.6million. The stock fell by the maximum permitted 10% eachday for 10 days when this was found out. suspicious points

Annual profit rate in 2000 was reported to be 46%, morethan 20% higher than industry average

According to the reported export value, it should havetax-free benefit. But this was not in its financial reports.Its value-added tax was also too low to justify its hugeprofit.

The German importer was too small (with capital level ofonly 100,000 DM) to afford such a huge order (6 billionyuan)

The claimed production scale was not credible.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The Yin Guangxia Incident

1999-2000, the company announced false profits of USD 89.6million. The stock fell by the maximum permitted 10% eachday for 10 days when this was found out. suspicious points

Annual profit rate in 2000 was reported to be 46%, morethan 20% higher than industry average

According to the reported export value, it should havetax-free benefit. But this was not in its financial reports.Its value-added tax was also too low to justify its hugeprofit.

The German importer was too small (with capital level ofonly 100,000 DM) to afford such a huge order (6 billionyuan)

The claimed production scale was not credible.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The Yin Guangxia Incident

1999-2000, the company announced false profits of USD 89.6million. The stock fell by the maximum permitted 10% eachday for 10 days when this was found out. suspicious points

Annual profit rate in 2000 was reported to be 46%, morethan 20% higher than industry average

According to the reported export value, it should havetax-free benefit. But this was not in its financial reports.Its value-added tax was also too low to justify its hugeprofit.

The German importer was too small (with capital level ofonly 100,000 DM) to afford such a huge order (6 billionyuan)

The claimed production scale was not credible.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The Yin Guangxia Incident

1999-2000, the company announced false profits of USD 89.6million. The stock fell by the maximum permitted 10% eachday for 10 days when this was found out. suspicious points

Annual profit rate in 2000 was reported to be 46%, morethan 20% higher than industry average

According to the reported export value, it should havetax-free benefit. But this was not in its financial reports.Its value-added tax was also too low to justify its hugeprofit.

The German importer was too small (with capital level ofonly 100,000 DM) to afford such a huge order (6 billionyuan)

The claimed production scale was not credible.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The newspaper reported the misreporting of YinGuangxia

Source: baidu photo

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Market manipulation of “ZhongkeVenture”(1998-2001)

buy and sell the shares using up to 1,500 accounts withoutany actual change of ownership

held up to 55.36% of total tradable shares

soar by over 1,000% to USD 10.15 per share

by the end of 2000, the stock price fell sharply to USD1.57 per share

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Market manipulation of “ZhongkeVenture”(1998-2001)

buy and sell the shares using up to 1,500 accounts withoutany actual change of ownership

held up to 55.36% of total tradable shares

soar by over 1,000% to USD 10.15 per share

by the end of 2000, the stock price fell sharply to USD1.57 per share

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Market manipulation of “ZhongkeVenture”(1998-2001)

buy and sell the shares using up to 1,500 accounts withoutany actual change of ownership

held up to 55.36% of total tradable shares

soar by over 1,000% to USD 10.15 per share

by the end of 2000, the stock price fell sharply to USD1.57 per share

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Market manipulation of “ZhongkeVenture”(1998-2001)

buy and sell the shares using up to 1,500 accounts withoutany actual change of ownership

held up to 55.36% of total tradable shares

soar by over 1,000% to USD 10.15 per share

by the end of 2000, the stock price fell sharply to USD1.57 per share

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Market manipulation of “ZhongkeVenture”(1998-2001)

buy and sell the shares using up to 1,500 accounts withoutany actual change of ownership

held up to 55.36% of total tradable shares

soar by over 1,000% to USD 10.15 per share

by the end of 2000, the stock price fell sharply to USD1.57 per share

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Table of Contents

1 Brief history1978-19921993-19981999-2007

2 ReformsNon-tradable sharesIssuance systemImpact assessment

3 Market structure

4 Current market situation

5 Supervision framework

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The share-split

shares publicly offered by a listed company were tradableon a stock exchange

all shares before public offering were still unlisted andnon-tradable

By December 2005, the non-tradable shares account for64% of the total shares

a huge source of uncertainty

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The share-split

shares publicly offered by a listed company were tradableon a stock exchange

all shares before public offering were still unlisted andnon-tradable

By December 2005, the non-tradable shares account for64% of the total shares

a huge source of uncertainty

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The share-split

shares publicly offered by a listed company were tradableon a stock exchange

all shares before public offering were still unlisted andnon-tradable

By December 2005, the non-tradable shares account for64% of the total shares

a huge source of uncertainty

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The share-split

shares publicly offered by a listed company were tradableon a stock exchange

all shares before public offering were still unlisted andnon-tradable

By December 2005, the non-tradable shares account for64% of the total shares

a huge source of uncertainty

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The share-split

shares publicly offered by a listed company were tradableon a stock exchange

all shares before public offering were still unlisted andnon-tradable

By December 2005, the non-tradable shares account for64% of the total shares

a huge source of uncertainty

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Origins of the issue

Economic transition

Concerns on lost of state assets

Desire for controls over large firms

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Origins of the issue

Economic transition

Concerns on lost of state assets

Desire for controls over large firms

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Origins of the issue

Economic transition

Concerns on lost of state assets

Desire for controls over large firms

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Origins of the issue

Economic transition

Concerns on lost of state assets

Desire for controls over large firms

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Origins of the issue

Economic transition

Concerns on lost of state assets

Desire for controls over large firms

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Origins of the issue

Economic transition

Concerns on lost of state assets

Desire for controls over large firms

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Origins of the issue

Economic transition

Concerns on lost of state assets

Desire for controls over large firms

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Origins of the issue

Economic transition

Concerns on lost of state assets

Desire for controls over large firms

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Problems

non-tradable share holders are less concerned with marketprice

tradable shares too small to affect management decision

market illiquid and volatile

force efficient firms to go public overseas

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Problems

non-tradable share holders are less concerned with marketprice

tradable shares too small to affect management decision

market illiquid and volatile

force efficient firms to go public overseas

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Problems

non-tradable share holders are less concerned with marketprice

tradable shares too small to affect management decision

market illiquid and volatile

force efficient firms to go public overseas

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Problems

non-tradable share holders are less concerned with marketprice

tradable shares too small to affect management decision

market illiquid and volatile

force efficient firms to go public overseas

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Problems

non-tradable share holders are less concerned with marketprice

tradable shares too small to affect management decision

market illiquid and volatile

force efficient firms to go public overseas

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Progress

May 2005, first batch (Sany Heavy Industry, ZijiangEnterprise, Jinniu Energy, and Tsinghua TongfangComputer) participated in the pilot program

June 2005, second batch (42 firms) participated in thepilot program

Nov. 2005, 39 major SOEs participated in the reform

April 2011, Listed companies that represented 99.32% ofthe market capitalization completed the reform or startedthe process.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Progress

May 2005, first batch (Sany Heavy Industry, ZijiangEnterprise, Jinniu Energy, and Tsinghua TongfangComputer) participated in the pilot program

June 2005, second batch (42 firms) participated in thepilot program

Nov. 2005, 39 major SOEs participated in the reform

April 2011, Listed companies that represented 99.32% ofthe market capitalization completed the reform or startedthe process.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Progress

May 2005, first batch (Sany Heavy Industry, ZijiangEnterprise, Jinniu Energy, and Tsinghua TongfangComputer) participated in the pilot program

June 2005, second batch (42 firms) participated in thepilot program

Nov. 2005, 39 major SOEs participated in the reform

April 2011, Listed companies that represented 99.32% ofthe market capitalization completed the reform or startedthe process.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Progress

May 2005, first batch (Sany Heavy Industry, ZijiangEnterprise, Jinniu Energy, and Tsinghua TongfangComputer) participated in the pilot program

June 2005, second batch (42 firms) participated in thepilot program

Nov. 2005, 39 major SOEs participated in the reform

April 2011, Listed companies that represented 99.32% ofthe market capitalization completed the reform or startedthe process.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Progress

May 2005, first batch (Sany Heavy Industry, ZijiangEnterprise, Jinniu Energy, and Tsinghua TongfangComputer) participated in the pilot program

June 2005, second batch (42 firms) participated in thepilot program

Nov. 2005, 39 major SOEs participated in the reform

April 2011, Listed companies that represented 99.32% ofthe market capitalization completed the reform or startedthe process.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The case of Sany heavy industry

Non-tradable share-holders pay each tradable share-holder3 stocks and 8 yuan per 10 shares in exchange for thetrading rights of the non-tradable shares.

Reason for the payment is a compensation for the impacton market price

A promise of the non-tradable share-holders: not to tradewithin 12 months after obtaining the rights

A promise of the dominating share-holder: after the initial12 months, the amount sold must be lower than5%(10%) the total number of the company’s shareswithin the next 12 (24) months.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The case of Sany heavy industry

Non-tradable share-holders pay each tradable share-holder3 stocks and 8 yuan per 10 shares in exchange for thetrading rights of the non-tradable shares.

Reason for the payment is a compensation for the impacton market price

A promise of the non-tradable share-holders: not to tradewithin 12 months after obtaining the rights

A promise of the dominating share-holder: after the initial12 months, the amount sold must be lower than5%(10%) the total number of the company’s shareswithin the next 12 (24) months.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The case of Sany heavy industry

Non-tradable share-holders pay each tradable share-holder3 stocks and 8 yuan per 10 shares in exchange for thetrading rights of the non-tradable shares.

Reason for the payment is a compensation for the impacton market price

A promise of the non-tradable share-holders: not to tradewithin 12 months after obtaining the rights

A promise of the dominating share-holder: after the initial12 months, the amount sold must be lower than5%(10%) the total number of the company’s shareswithin the next 12 (24) months.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The case of Sany heavy industry

Non-tradable share-holders pay each tradable share-holder3 stocks and 8 yuan per 10 shares in exchange for thetrading rights of the non-tradable shares.

Reason for the payment is a compensation for the impacton market price

A promise of the non-tradable share-holders: not to tradewithin 12 months after obtaining the rights

A promise of the dominating share-holder: after the initial12 months, the amount sold must be lower than5%(10%) the total number of the company’s shareswithin the next 12 (24) months.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The case of Sany heavy industry

Non-tradable share-holders pay each tradable share-holder3 stocks and 8 yuan per 10 shares in exchange for thetrading rights of the non-tradable shares.

Reason for the payment is a compensation for the impacton market price

A promise of the non-tradable share-holders: not to tradewithin 12 months after obtaining the rights

A promise of the dominating share-holder: after the initial12 months, the amount sold must be lower than5%(10%) the total number of the company’s shareswithin the next 12 (24) months.

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Stock market performance after the reform

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2,600

2,800

3,000

Jan-05 Mar-05 May-05 Jul-05 Sep-05 Nov-05 Dec-05 Mar-06 May-06 Jul-06 Aug-06 Nov-06 Dec-06

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

SSE Composite % of listed companies starting the restructuring

First pilote program

announced (April 2005)

Second pilote program

announced (June 2005)

Program extended to all listed companies

(August 2005)

Source: Beltratti et al. (2011)

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Before-reform characteristics and investor reactionsto the reform

Abnormal returns have been larger in firms

with stronger monitoring on the part of large shareholders

with a larger potential for privatization

in firms neglected by institutional investors

not traded by international investors through H-shares

In summary, “investors have marked up the prices of firms thathad the best potential to profit from the reform” (Beltratti etal., 2011).

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Before-reform characteristics and investor reactionsto the reform

Abnormal returns have been larger in firms

with stronger monitoring on the part of large shareholders

with a larger potential for privatization

in firms neglected by institutional investors

not traded by international investors through H-shares

In summary, “investors have marked up the prices of firms thathad the best potential to profit from the reform” (Beltratti etal., 2011).

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Before-reform characteristics and investor reactionsto the reform

Abnormal returns have been larger in firms

with stronger monitoring on the part of large shareholders

with a larger potential for privatization

in firms neglected by institutional investors

not traded by international investors through H-shares

In summary, “investors have marked up the prices of firms thathad the best potential to profit from the reform” (Beltratti etal., 2011).

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Before-reform characteristics and investor reactionsto the reform

Abnormal returns have been larger in firms

with stronger monitoring on the part of large shareholders

with a larger potential for privatization

in firms neglected by institutional investors

not traded by international investors through H-shares

In summary, “investors have marked up the prices of firms thathad the best potential to profit from the reform” (Beltratti etal., 2011).

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Before-reform characteristics and investor reactionsto the reform

Abnormal returns have been larger in firms

with stronger monitoring on the part of large shareholders

with a larger potential for privatization

in firms neglected by institutional investors

not traded by international investors through H-shares

In summary, “investors have marked up the prices of firms thathad the best potential to profit from the reform” (Beltratti etal., 2011).

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

Reform in the issuance system

Source: CRSC

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The public offering review committee

Established in September 1999

Members from government, stock exchanges, andacademia

At 2/3 votes of 9 members needed to pass an application

December 2003,number of members reduced from 80 to25 (13 full-time)

5/7 votes needed to pass

Voting members are known prior to each meeting (theywere anonymous before the reform)

May 2007, number of full-time members increased to 17

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The public offering review committee

Established in September 1999

Members from government, stock exchanges, andacademia

At 2/3 votes of 9 members needed to pass an application

December 2003,number of members reduced from 80 to25 (13 full-time)

5/7 votes needed to pass

Voting members are known prior to each meeting (theywere anonymous before the reform)

May 2007, number of full-time members increased to 17

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The public offering review committee

Established in September 1999

Members from government, stock exchanges, andacademia

At 2/3 votes of 9 members needed to pass an application

December 2003,number of members reduced from 80 to25 (13 full-time)

5/7 votes needed to pass

Voting members are known prior to each meeting (theywere anonymous before the reform)

May 2007, number of full-time members increased to 17

Topic 5China’sCapital

Markets I

Zongxin Qian

Brief history

1978-1992

1993-1998

1999-2007

Reforms

Non-tradableshares

Issuance system

Impactassessment

Marketstructure

Currentmarketsituation

Supervisionframework

The public offering review committee

Established in September 1999

Members from government, stock exchanges, andacademia

At 2/3 votes of 9 members needed to pass an application

December 2003,number of members reduced from 80 to25 (13 full-time)

5/7 votes needed to pass