topic 3 Investment in Equity Debt Securities

54

7/27/2019 topic 3 Investment in Equity Debt Securities http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 1/54 TOPIC 3 INVESTMENTS IN EQUITY AND DEBT SECURITIES 1

-

Upload

jayjay-hanj -

Category

Documents

-

view

217 -

download

0

Transcript of topic 3 Investment in Equity Debt Securities

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 1/54

TOPIC 3

INVESTMENTS IN EQUITY ANDDEBT SECURITIES

1

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 2/54

LEARNING OUTCOMES

Explain types and classification of investment

Record the investment using various methods

a) Cost method

b) Equity method

Account for changes in method

Distinguish between share dividend, share split

and share right Record investment in debt securities

2

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 3/54

INVESTMENTS IN

EQUITY SECURITIES

Investment – assets owned to acquire additional income,

increase capital and other benefits.

Types of investment:

a) Short-term investment

b) Long-term investment

Classification of Investment:

1) Investment in Subsidiary2) Invetment in Associate

3) Other Investment

3

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 4/54

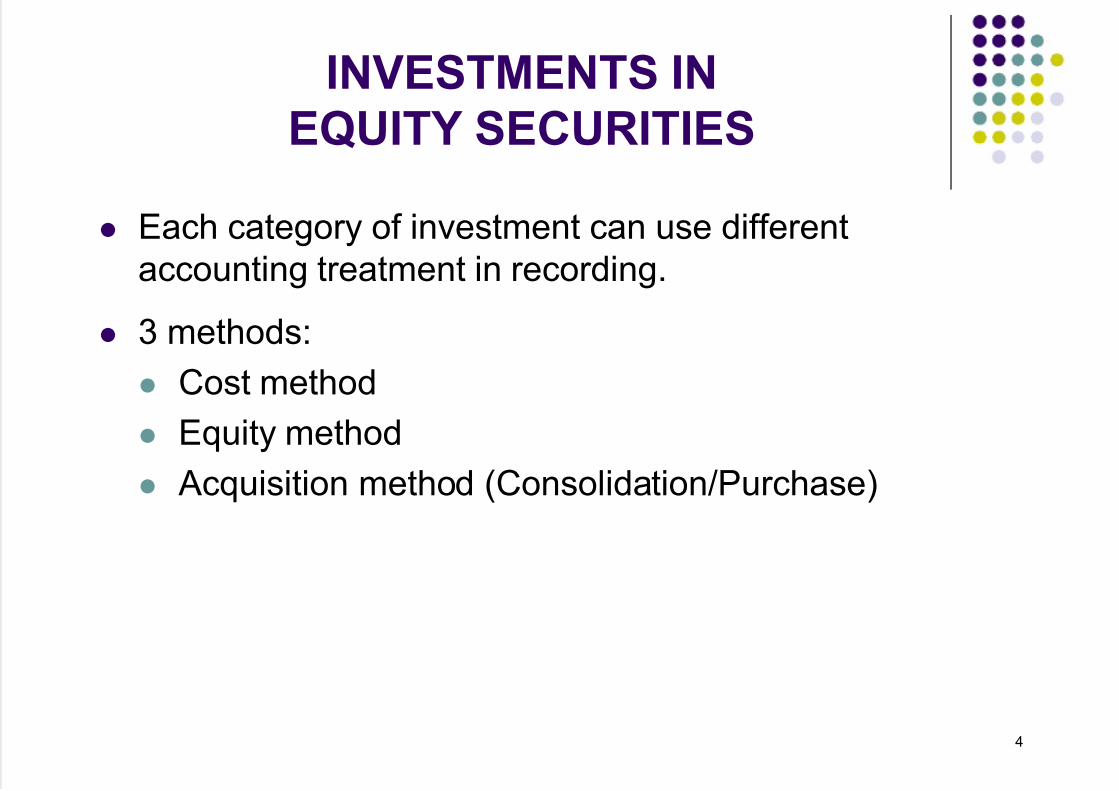

INVESTMENTS IN

EQUITY SECURITIES

Each category of investment can use different

accounting treatment in recording.

3 methods:

Cost method

Equity method

Acquisition method (Consolidation/Purchase)

4

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 5/54

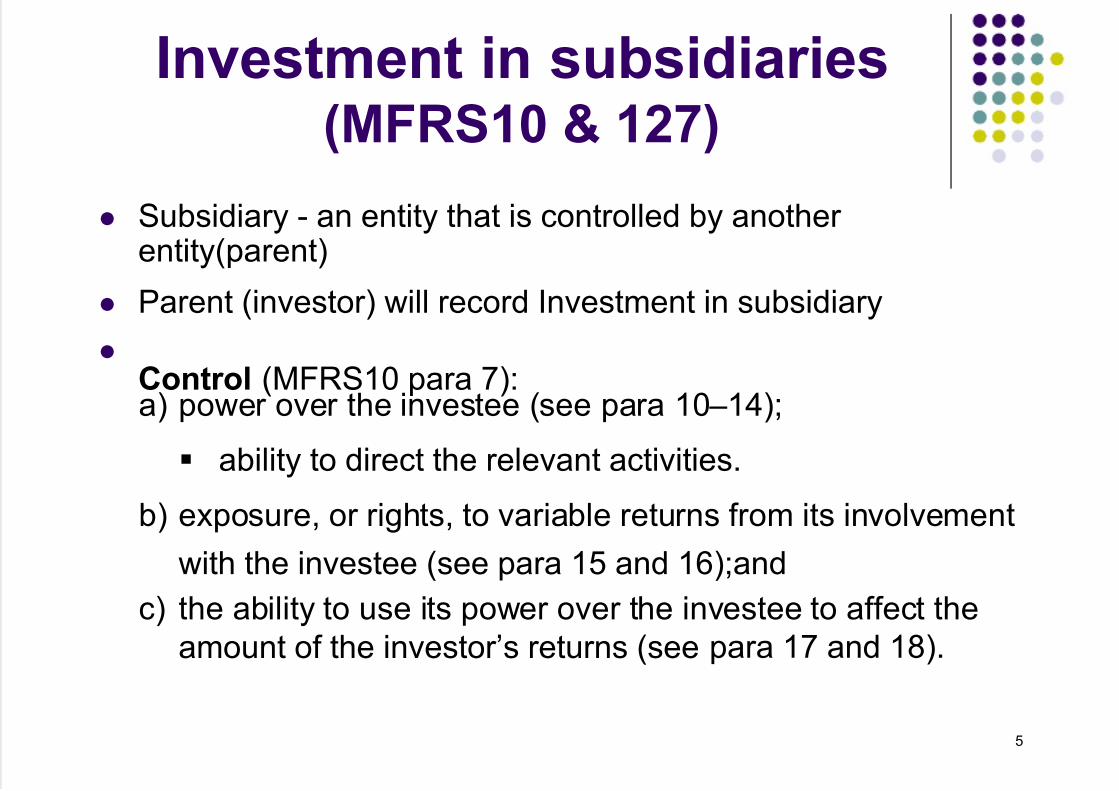

Investment in subsidiaries(MFRS10 & 127)

Subsidiary - an entity that is controlled by another entity(parent)

Parent (investor) will record Investment in subsidiary

Control (MFRS10 para 7):a) power over the investee (see para 10 –14);

ability to direct the relevant activities.

b) exposure, or rights, to variable returns from its involvement

with the investee (see para 15 and 16);and

c) the ability to use its power over the investee to affect the

amount of the investor’s returns (see para 17 and 18).

5

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 6/54

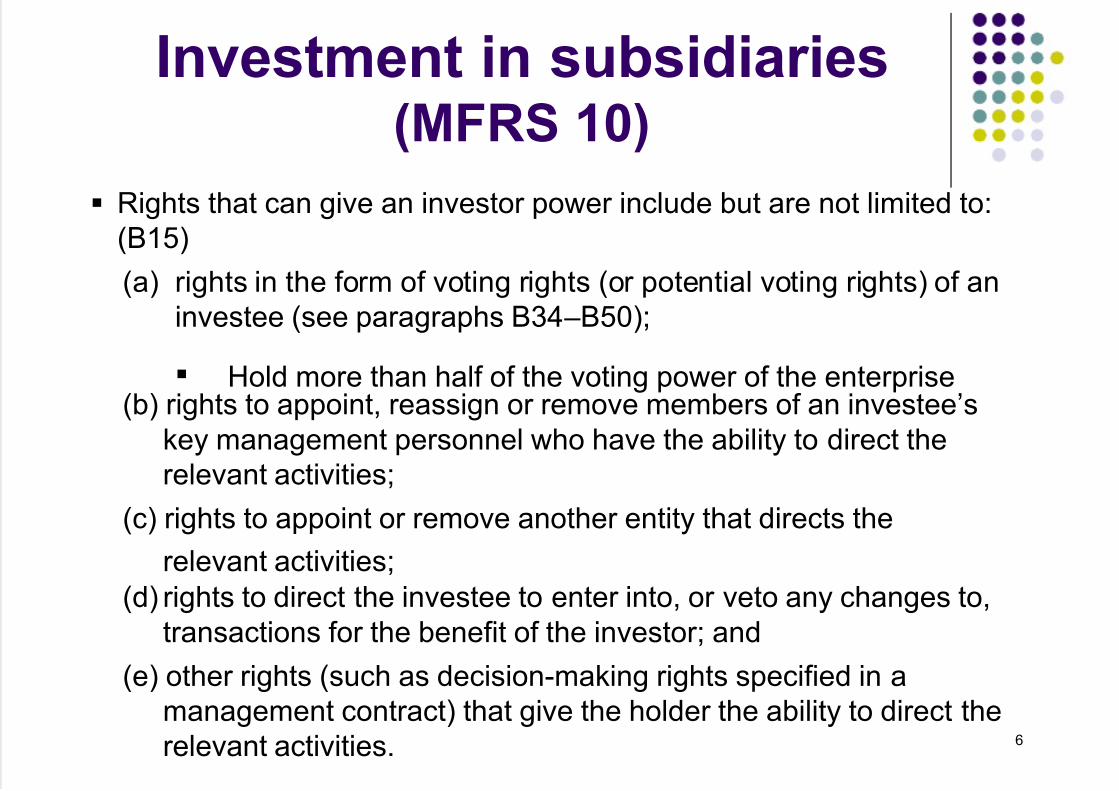

Investment in subsidiaries(MFRS 10)

6

Rights that can give an investor power include but are not limited to:

(B15)

(a) rights in the form of voting rights (or potential voting rights) of an

investee (see paragraphs B34 –B50);

Hold more than half of the voting power of the enterprise(b) rights to appoint, reassign or remove members of an investee’s

key management personnel who have the ability to direct the

relevant activities;

(c) rights to appoint or remove another entity that directs the

relevant activities;

(d) rights to direct the investee to enter into, or veto any changes to,

transactions for the benefit of the investor; and

(e) other rights (such as decision-making rights specified in a

management contract) that give the holder the ability to direct the

relevant activities.

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 7/54

Investment in subsidiaries(MFRS 127)

Parent should present

1) Its financial statement (MFRS 127)

2) a consolidated financial statement (parent and subsidiaries)

(MFRS 10)

In parent’s separate financial statements, it shall account for investments in subsidiaries either:

(a) at cost, or

(b) in accordance with MFRS 9.

The entity shall apply the same accounting for each category of

investments.

Investments accounted for at cost shall be accounted for in

accordance with MFRS 5 Non-current Assets Held for Sale and

Discontinued Operations when they are classified as held for sale.

7

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 8/54

Investment in

Associate companies (MFRS 128)

Associate companies – an enterprise in which the

investor has significant influence

Significant influence - power to participate in the financial

and operating policy

decisions of an investee but not control over those

policies.

Ownership of voting share – 20% - 50%

8

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 9/54

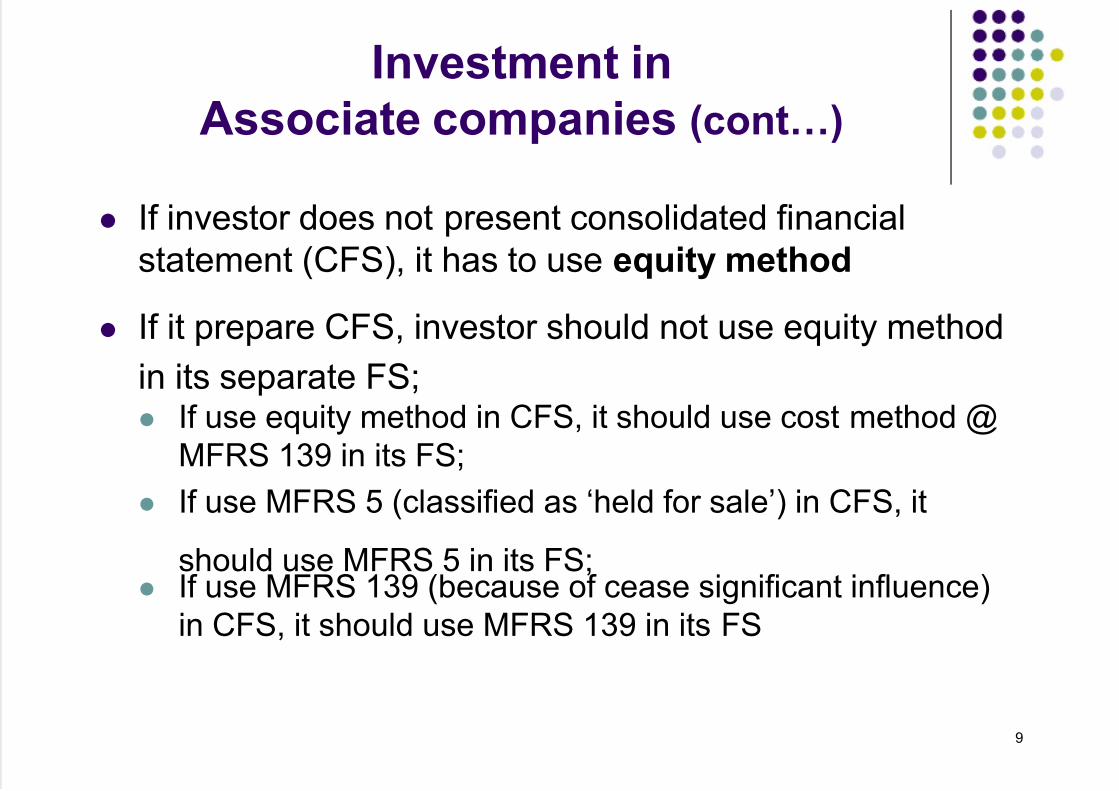

Investment in

Associate companies (cont…)

If investor does not present consolidated financial

statement (CFS), it has to use equity method

If it prepare CFS, investor should not use equity method

in its separate FS; If use equity method in CFS, it should use cost method @

MFRS 139 in its FS;

If use MFRS 5 (classified as ‘held for sale’) in CFS, it

should use MFRS 5 in its FS; If use MFRS 139 (because of cease significant influence)

in CFS, it should use MFRS 139 in its FS

9

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 10/54

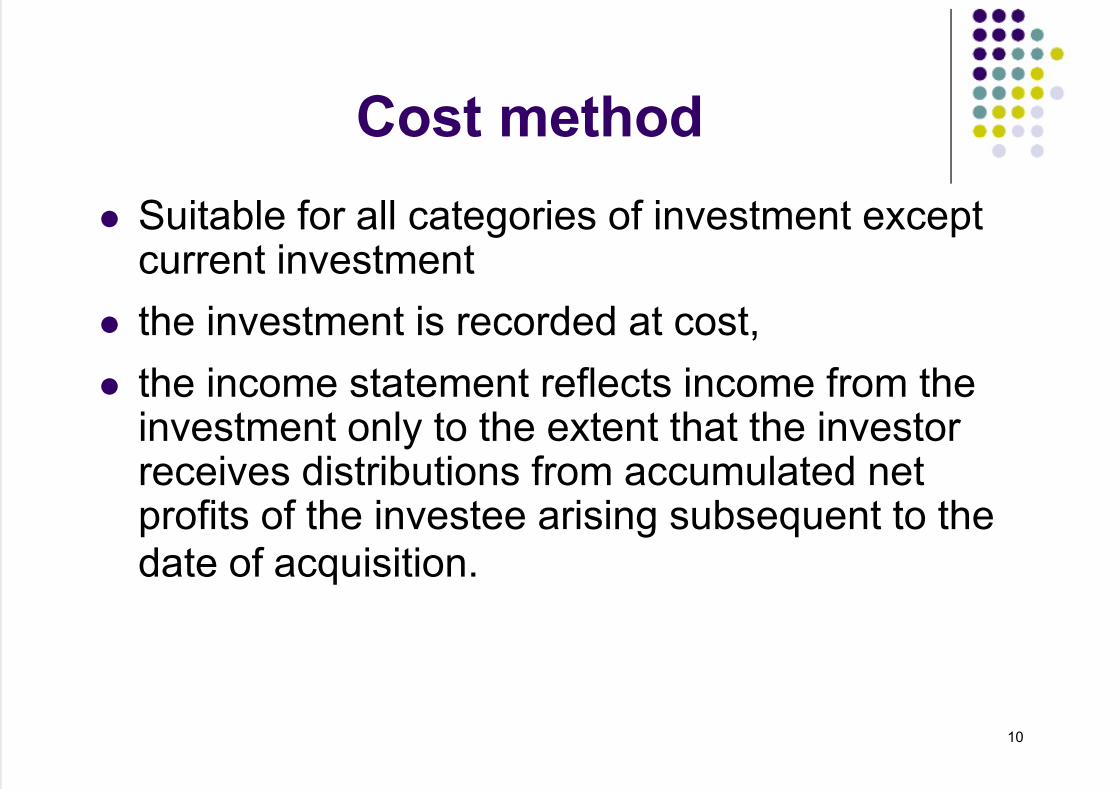

Cost method

Suitable for all categories of investment exceptcurrent investment

the investment is recorded at cost,

the income statement reflects income from theinvestment only to the extent that the investor receives distributions from accumulated netprofits of the investee arising subsequent to thedate of acquisition.

10

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 11/54

Cost method (cont..)

Cost of investment

= Purchase price + all charges involved while

acquiring (broker fees, bank charge)

Share of investee’s earning (SIE) = % of holdings x profit If dividend received < share of investee’s earning

recorded as investment income / dividend

If dividend is received > share of investee’s earning

investee give dividends more than retained earnings

they have.

Recorded as declining in carrying amount of investment.

11

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 12/54

Cost method (cont..)

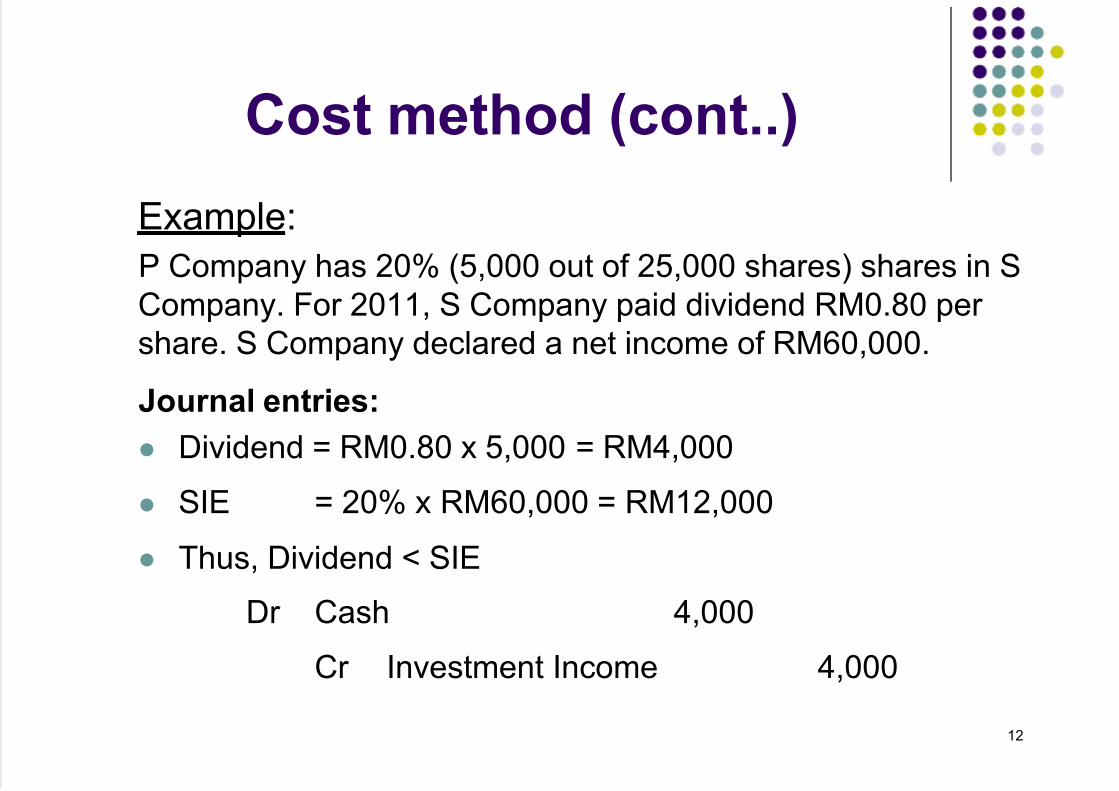

Example:

P Company has 20% (5,000 out of 25,000 shares) shares in S

Company. For 2011, S Company paid dividend RM0.80 per

share. S Company declared a net income of RM60,000.

Journal entries:

Dividend = RM0.80 x 5,000 = RM4,000

SIE = 20% x RM60,000 = RM12,000

Thus, Dividend < SIE

Dr Cash 4,000

Cr Investment Income 4,000

12

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 13/54

Cost method (cont..)

Otherwise, if S Company paid dividend of RM2.50

per share:

Dividend = RM2.50 x 5,000 = RM12,500

SIE = 20% x RM60,000 = RM12,000 Dividend > SIE

Dr Cash 12,500

Cr Investment Income 12,000

Cr Investment in shares 500

13

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 14/54

14

If there is a decline in the value of investment (‘not temporary’ innature), the cost of the investment will also be declined and the lossis charged to the Income Statement.

Dr Loss of declining in investment value XX

Cr Investment in shares XX

If there is a sale of investment in shares, gain or loss on disposalshould be recognized (Difference between selling price and cost of investment)

Dr. Cash XX

Dr. Loss on securities sold XX

Cr. Investment in shares XX

Cr. Gain on Securities sold XX

Cost Method (cont.)

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 15/54

Equity method

Used in the preparation of the Consolidated FinancialStatement

the investment is initially recorded at cost and adjustedthereafter for the post-acquisition change in the investor’s

share of net assets of the investee. The Income Statement reflects the investor’s share of

the results of operations of the investee.

Carrying Amount of Investment

= Cost

(+) Allocation of income in SIE, @ (-) Allocation of loss

(-) Dividend received from investee

15

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 16/54

Equity method (cont..)

Adjustments are also needed to be made for:

eliminating gain / loss from the transactions between

companies

difference in amortization of goodwill between original

investor’s cost (purchase price) and investee’s net

book value at the date of acquisition

extraordinary items

16

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 17/54

Equity method (cont..)

Example:

On January 2012, Firdaus Company owns 25% shares of Idani Company at a price of RM700,000. At the date of the

ownership, fair value of the depreciable assets isRM100,000, and yearly depreciation of RM12,500. Thefollowings are the information taken from Idani Company in2000:

Net Income declared RM 90,000

Dividend issued RM 70,000

17

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 18/54

Equity method (cont..)

Solution:

Dr Investment in shares 700,000

Cr Cash 700,000

(to record the acquisition/ownership of shares 25%)

Dr Investment in shares 22,500

Cr Investment Income 22,500

(to record SIE 25% x 90,000)

Dr Cash (25% x 70,000) 17,500Cr Investment in shares 17,500

(to record the dividend received)

18

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 19/54

Equity method (cont..)

Solution (cont..):

Dr Investment Income 3,125

Cr Investment in shares 3,125

(to record the amortization of the depreciable assets) (25% x 12,500)

Thus;

Carrying amount of investment in shares:= RM700,000 + RM22,500 – RM17,500 – RM3,125

= RM701,875

19

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 20/54

Acquisition method

MFRS 3 (para1) specifies that all business combinationsshould be accounted for by applying the acquisitionmethod.

Views a business combination from the perspective of

the acquirer. The acquirer is the combining entity that obtains control

of the other combining entities or businesses.

The acquirer purchases net assets and recognizes the

assets acquired and liabilities and contingent liabilitiesassumed, including those not previously recognized bythe acquiree.

The acquirer records the assets and liabilities at fair values. 20

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 21/54

Acquisition method (cont..)

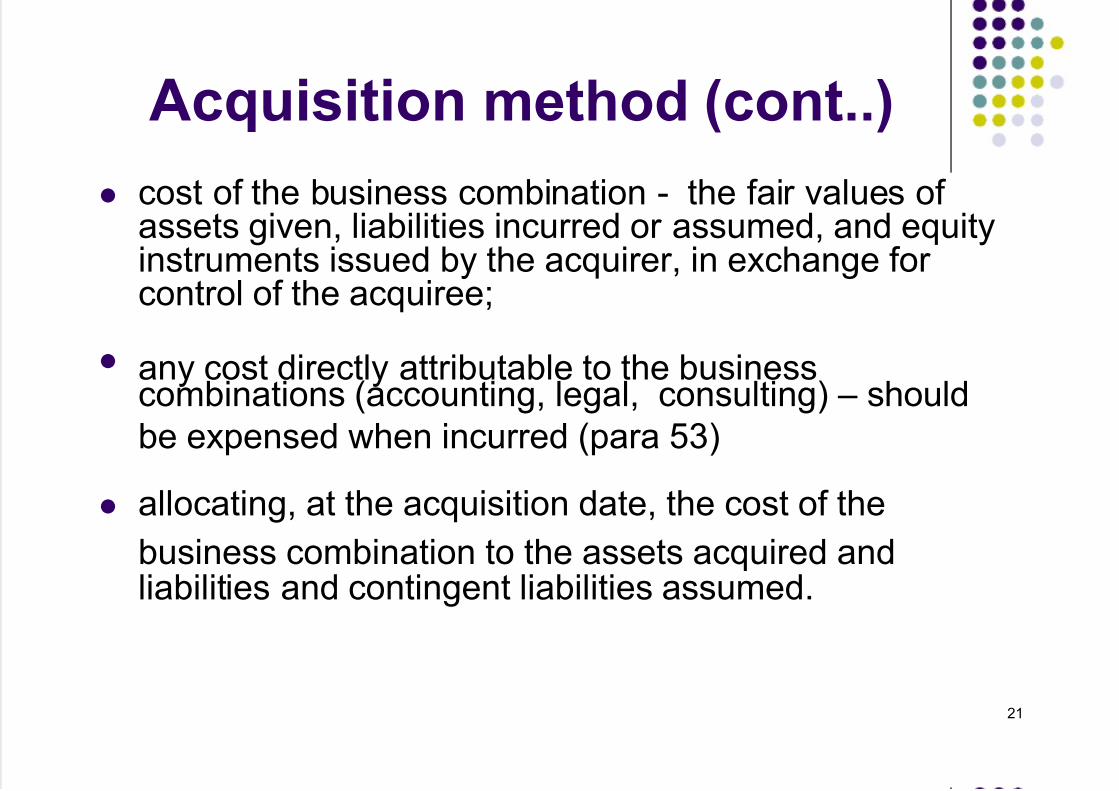

cost of the business combination - the fair values of assets given, liabilities incurred or assumed, and equityinstruments issued by the acquirer, in exchange for control of the acquiree;

any cost directly attributable to the businesscombinations (accounting, legal, consulting) – should

be expensed when incurred (para 53)

allocating, at the acquisition date, the cost of the

business combination to the assets acquired andliabilities and contingent liabilities assumed.

21

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 22/54

Acquisition method (cont..)

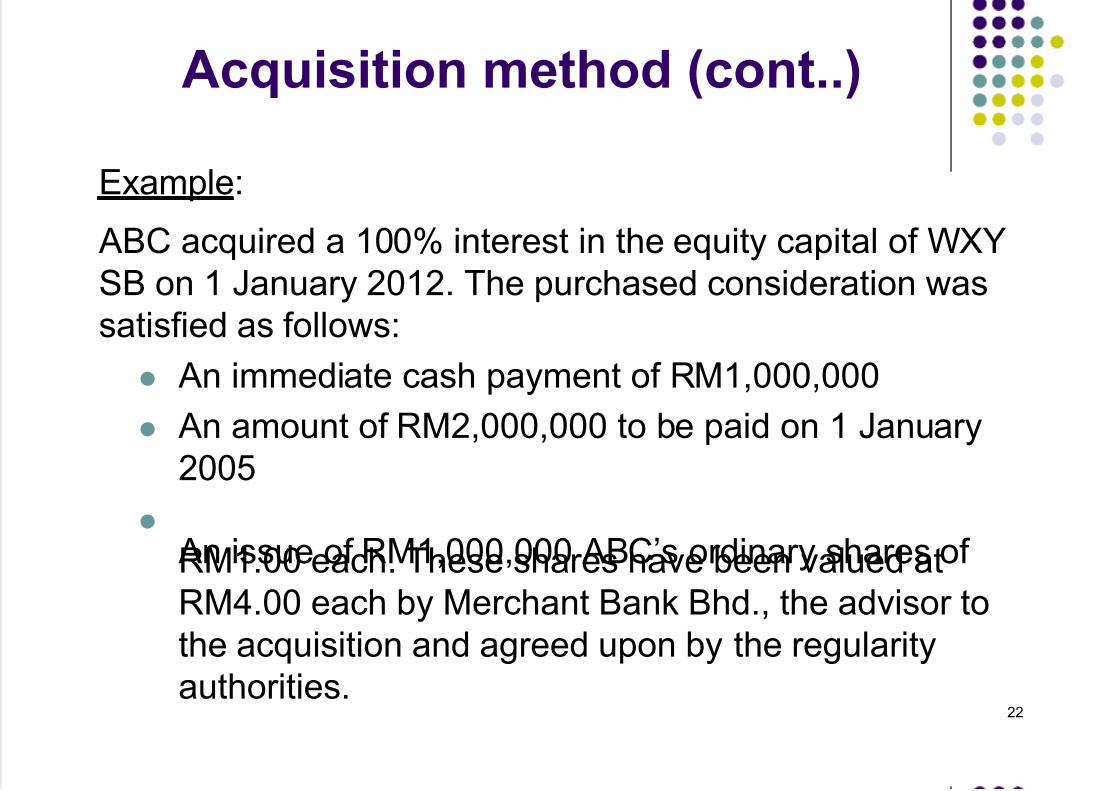

Example:

ABC acquired a 100% interest in the equity capital of WXY

SB on 1 January 2012. The purchased consideration was

satisfied as follows:

An immediate cash payment of RM1,000,000

An amount of RM2,000,000 to be paid on 1 January

2005

An issue of RM1,000,000 ABC’s ordinary shares of RM1.00 each. These shares have been valued at

RM4.00 each by Merchant Bank Bhd., the advisor to

the acquisition and agreed upon by the regularity

authorities.22

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 23/54

Acquisition method (cont..)

Example (cont..)

Cost incurred that were directly attributable to the

acquisition totaled RM500,000 and these have not

been paid. The cost of registration for issuing sharesis RM100,000 paid by cash. ABC’s incremental

borrowing cost was 8% per annum.

Required:

Calculate the COI and record the related journal entry.

23

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 24/54

Acquisition method (cont..)

Solution:

Cost of Investment:

Immediate cash consideration 1,000

PV of deferred consideration (2,000/(1.08)^2) 1,715

Fair value of shares issued (1,000 x 4) 4,000

COI 6,715

Investment in Subsidiary 6,715

Cash 1,000Deferred liability 1,715

Share capital 1,000

Share premium 3,000

24

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 25/54

Changes in Method

Changes from equity method to cost method

Changes of method when percentage of ownershipdecline.

Carrying amount of investment at the date of changing themethod will be a base for the investment cost.

Amortization of the excess ownership costs on net bookvalue of depreciable assets need not to be done again.

Not retroactive in nature (prior period adjustment)

25

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 26/54

Changes in Method (Cont..)

Example:

On January 1, 2010, Alma Company purchased 250,000 unit sharesof Berjaya Company at the cost of RM8,500,000. Total shares of

Berjaya Company are 1,000,000 units. Assume that on 1/1/2011, Berjaya Company issued 1,500,000

ordinary shares to the public. This has caused percentage of ownership of Alma Company reduced from 25% (250,000 /1,000,000) to 10% (250,000 / 2,500,000).

Carrying value of investment of Alma Company in Berjaya Companyat 31/12/2010 is RM8,924,000.

26

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 27/54

Changes in Method (Cont..)

Example (cont…) The followings are the net income (loss) and dividend of

Berjaya Company (investee) from year 1996 – 1998.

Investor’s position

in investee’s Net Income

Dividend received

by investor

2011 RM600,000 RM400,000

2012 RM350,000 RM400,000

2013 - RM210,000

Assume that a change from equity method to the cost

method is effective at 1/1/2011.

27

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 28/54

Changes in Method (Cont..)

Solution:

Calculation of cumulative net income on the investor’s

dividend

2011 RM600,000 – RM400,000 RM200,000

2012 (RM350,000 – RM400,000) + RM200,000 RM150,000

2013 (RM0 – RM210,000) + RM150,000 (RM60,000)

28

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 29/54

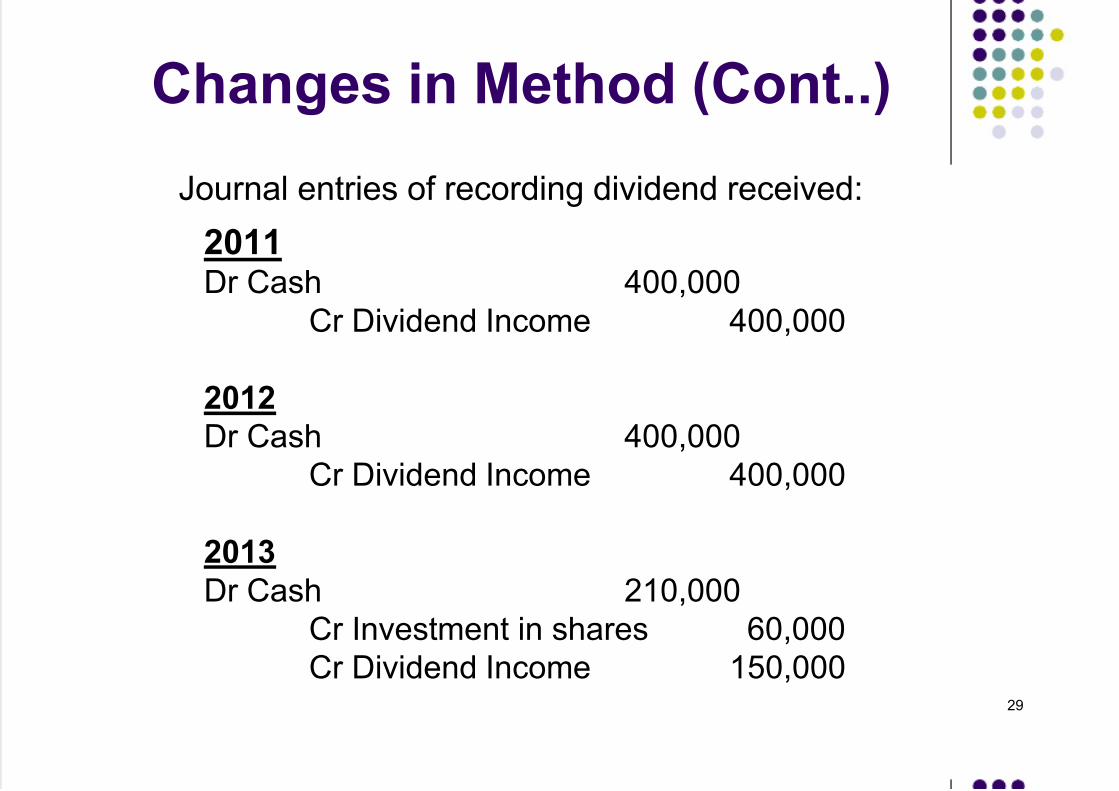

Changes in Method (Cont..)

Journal entries of recording dividend received:

2011

Dr Cash 400,000

Cr Dividend Income 400,000

2012

Dr Cash 400,000

Cr Dividend Income 400,000

2013

Dr Cash 210,000

Cr Investment in shares 60,000

Cr Dividend Income 150,00029

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 30/54

Changes in Method (Cont..)

Changes from cost method to equity method:

Retroactive in nature, i.e. prior period adjustment

should be made.

Unrealized profit / loss account and adjustment of the

fair value securities should be eliminated

30

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 31/54

INVESTMENTS IN DEBT SECURITIES

A debt security is an investment in bonds issued by thegovernment or a corporation

Bond – a certificate issued to the public whereby the companywho issued the bonds (issuer) agreed to pay the bonds holder

(investor) the face value of the bonds at a certain maturitydate including the interest at the agreed rate.

Characteristics:

nominal value or face value of the bond

normally stated at RM1,000.

is the value that can be repaid at the maturity date.

maturity date

date whereby the issuer of the bonds has to pay backthe face value of the bond to the investor.

31

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 32/54

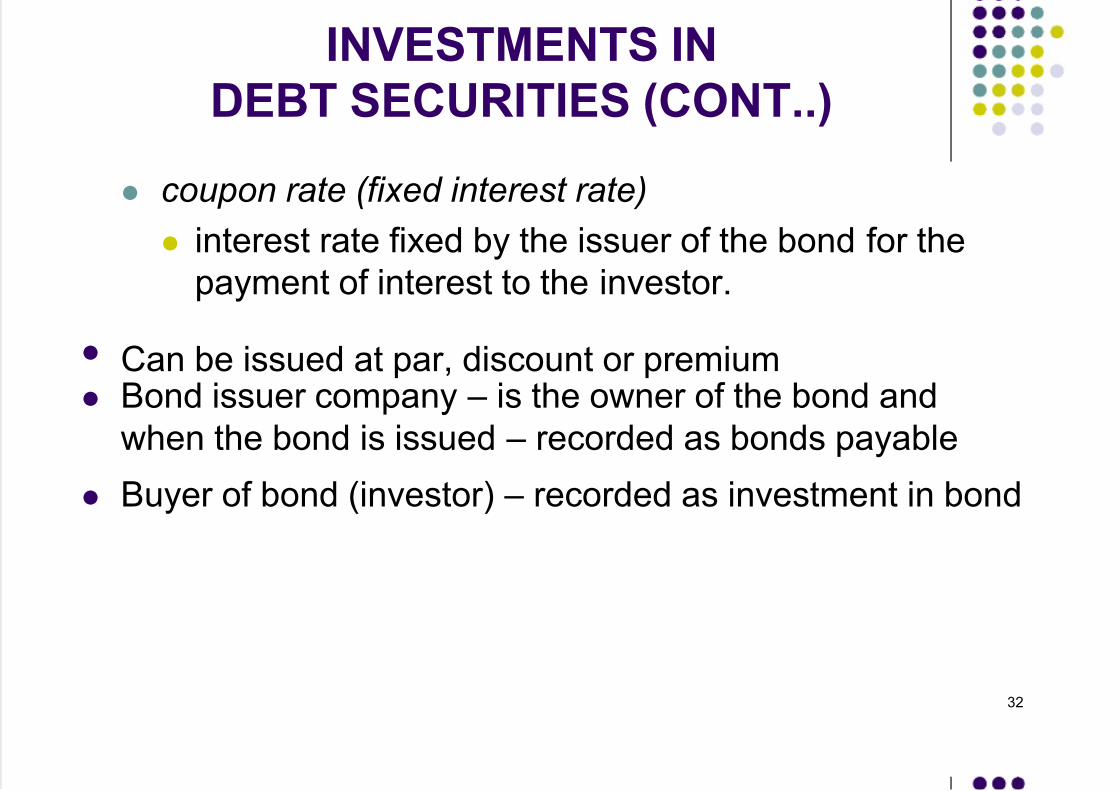

INVESTMENTS IN

DEBT SECURITIES (CONT..)

coupon rate (fixed interest rate)

interest rate fixed by the issuer of the bond for the

payment of interest to the investor.

Can be issued at par, discount or premium Bond issuer company – is the owner of the bond and

when the bond is issued – recorded as bonds payable

Buyer of bond (investor) – recorded as investment in bond

32

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 33/54

Types of Debt Securities

Terms v. Ser ial Bond

Terms bonds – issued and will mature at the same date. Issuer of

the bond has to pay certain amount of money at the maturity date

for all bonds issued.

Serial bonds – has more than one maturity date (i.e. matureaccording to levels).

Registered v. Bearer (Coupon Bonds )

Registered bonds – payment of interest and principal of the bondmatured will be paid to the owner of the bond according to the

name listed in the record of the trustee holder. Coupon bonds – payment of interest will be paid to the person

who submitted the coupon interest to the issuer company.

Junk Bond

High-risk bond. Thus, high return.33

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 34/54

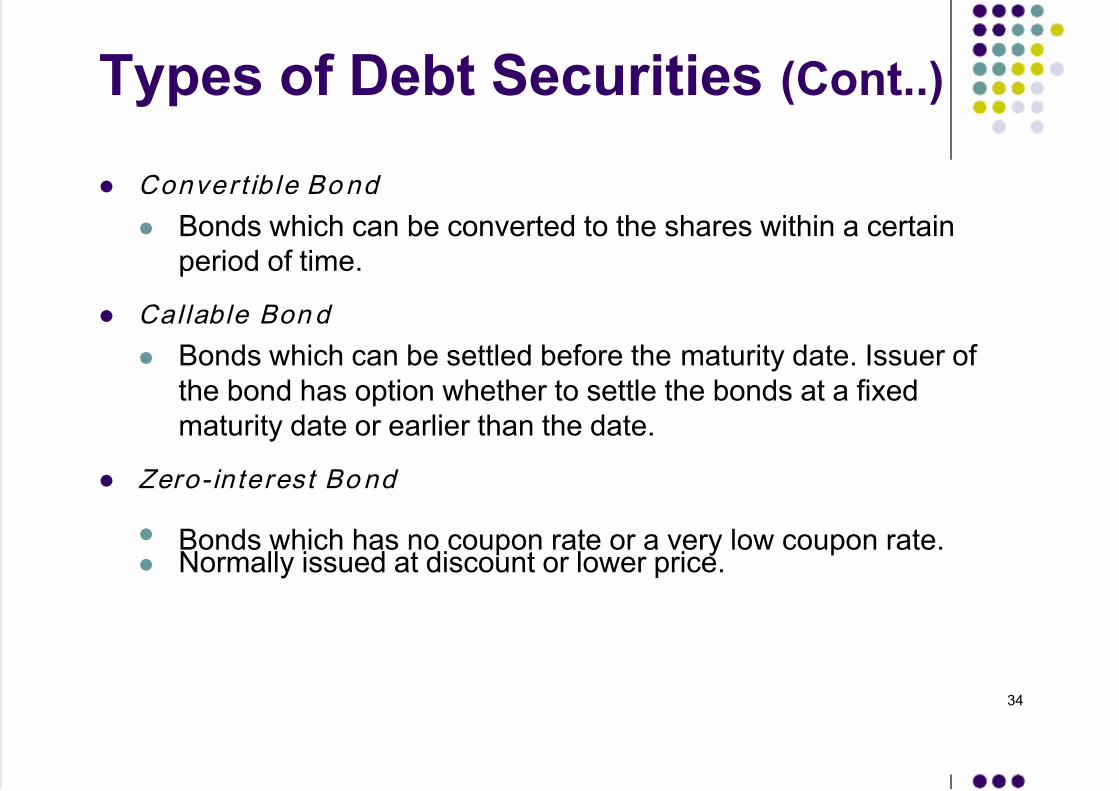

Types of Debt Securities (Cont..)

Conver t ib le Bond

Bonds which can be converted to the shares within a certain

period of time.

Callable Bond

Bonds which can be settled before the maturity date. Issuer of

the bond has option whether to settle the bonds at a fixed

maturity date or earlier than the date.

Zero- interest Bond

Bonds which has no coupon rate or a very low coupon rate. Normally issued at discount or lower price.

34

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 35/54

Determining and Recording Initial

Cost for Bonds Purchased

Purchase price/selling price of the bond is determined by

calculating:

a) Present Value of the bond

b) Amount at the issuance rate given

Example:

ABC Bhd issues RM300,000 of 9% bonds, due in 10

years, with interest payable semiannually. At the time

of issue, the market rate for such bonds is 10%.Compute the issue price of the bonds.

35

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 36/54

Determining and Recording Initial

Cost for Bonds Purchased (Cont..)

Solution:

n = 10 x 2 i = 10%/2

PV of the principal:300,000 x 0.37689 113,067

PVOA of interest payable:

[(9% x 300,000)/2] x 12.46221 168,240

Price f bond 281,307

36

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 37/54

Determining and Recording Initial

Cost for Bonds Purchased (Cont..)

The price of a bond is determined by the interaction between

the bond's stated interest rate and its market rate.

A bond's price is equal to the sum of the present value of the

principle and the present value of the periodic interest.

If the stated rate = the market rate, the bond will sell at par.

If the stated rate < the market rate, the bond will sell at a

discount.

If the stated rate > the market rate, the bond will sell at apremium.

37

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 38/54

Example:

ABC Bhd issued RM200,000 of 8% bonds on 1 Jan2010. The bonds are due on 1 Jan 2015, withinterest payable each 1 July and 1 Jan. Compute theissue price at

a)100b) 97

c) 105

Prepare journal entries for investor.

38

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 39/54

Solution:

a) At 100:

Dr Investment in Bonds 200

Cr Cash 200

b) At 97:

Dr Investment in Bonds 194

Cr Cash 194

c) At 105:

Dr Investment in Bonds 210

Cr Cash 210

39

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 40/54

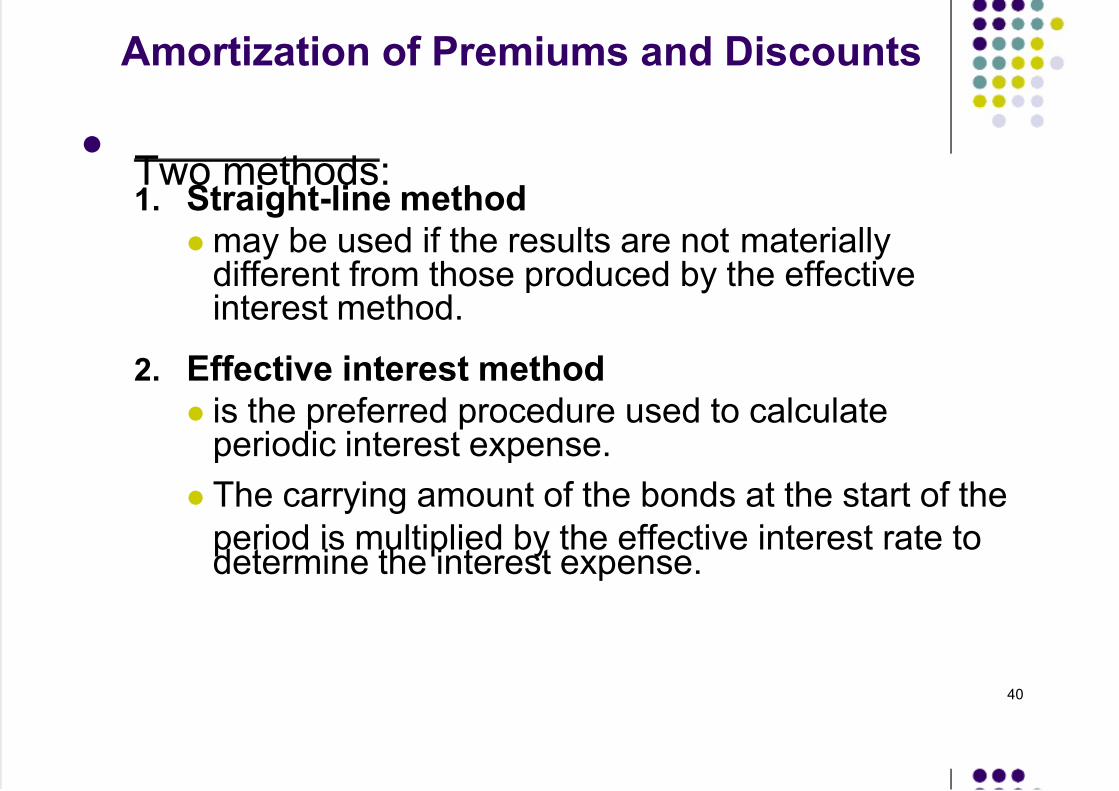

Amortization of Premiums and Discounts

Two methods:1. Straight-line method

may be used if the results are not materiallydifferent from those produced by the effectiveinterest method.

2. Effective interest method

is the preferred procedure used to calculateperiodic interest expense.

The carrying amount of the bonds at the start of the

period is multiplied by the effective interest rate todetermine the interest expense.

40

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 41/54

Amortization of Premiums

and Discounts (Cont..)

Interest Revenue (Effective interest method)

= Effective Interest Rate x Carrying Value of Bonds.

Journal entry:If a premium exists:

Dr Cash/interest receivable XX

Dr Interest Revenue XXCr Investment in Bonds XX

If a discount exists:

Dr Cash/interest receivable XX

Dr Investment in Bonds XX

Cr Interest Revenue XX41

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 42/54

Amortization of Premiums

and Discounts (Cont..)

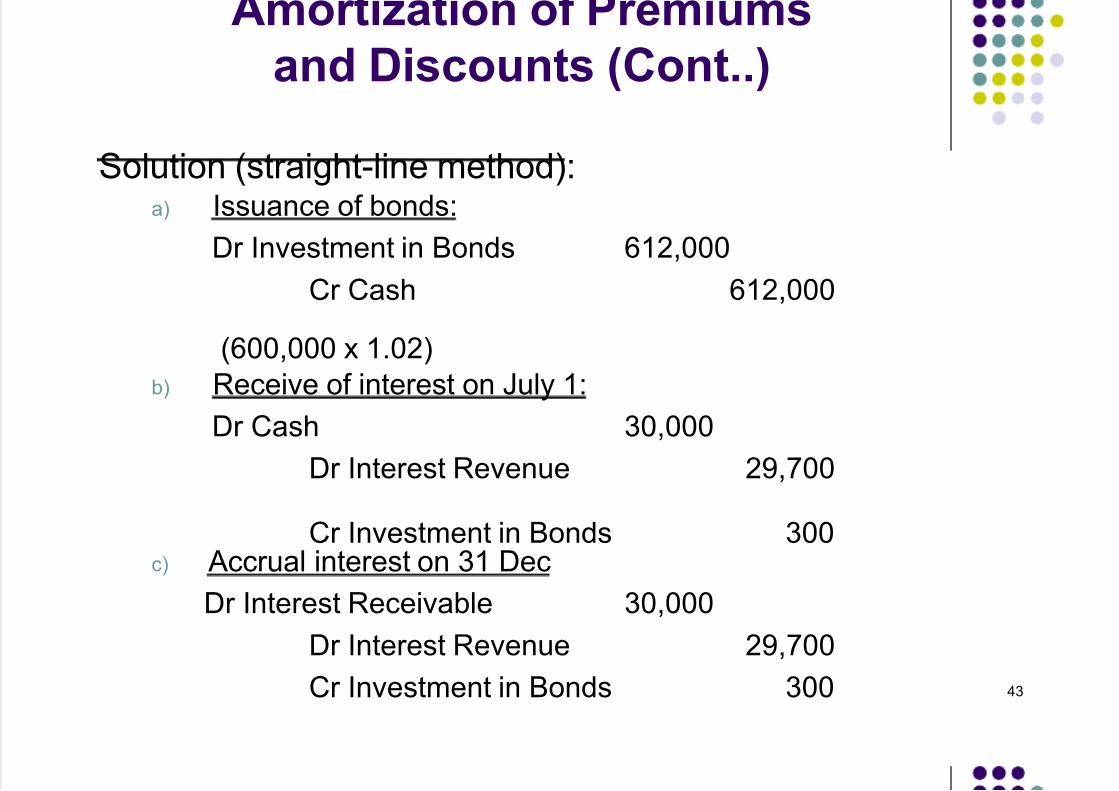

Example (straight-line method):

ABC Bhd issued RM600,000 of 10%, 20-year bonds on1 Jan 2012, at 102. Interest is payable semiannually on

1 July and 1 Jan. ABC Bhd uses straight-line method of amortization for bond premium/discount.

Prepare the journal entries to record:

a) The issuance of the bonds

b) The payment of interest on 1 July

c) The accrual of interest on 31 Dec

42

A ti ti f P i

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 43/54

Amortization of Premiums

and Discounts (Cont..)

Solution (straight-line method):a) Issuance of bonds:

Dr Investment in Bonds 612,000

Cr Cash 612,000

(600,000 x 1.02)

b) Receive of interest on July 1:

Dr Cash 30,000

Dr Interest Revenue 29,700

Cr Investment in Bonds 300c) Accrual interest on 31 Dec

Dr Interest Receivable 30,000

Dr Interest Revenue 29,700

Cr Investment in Bonds 300 43

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 44/54

Amortization of Premiums

and Discounts (Cont..)

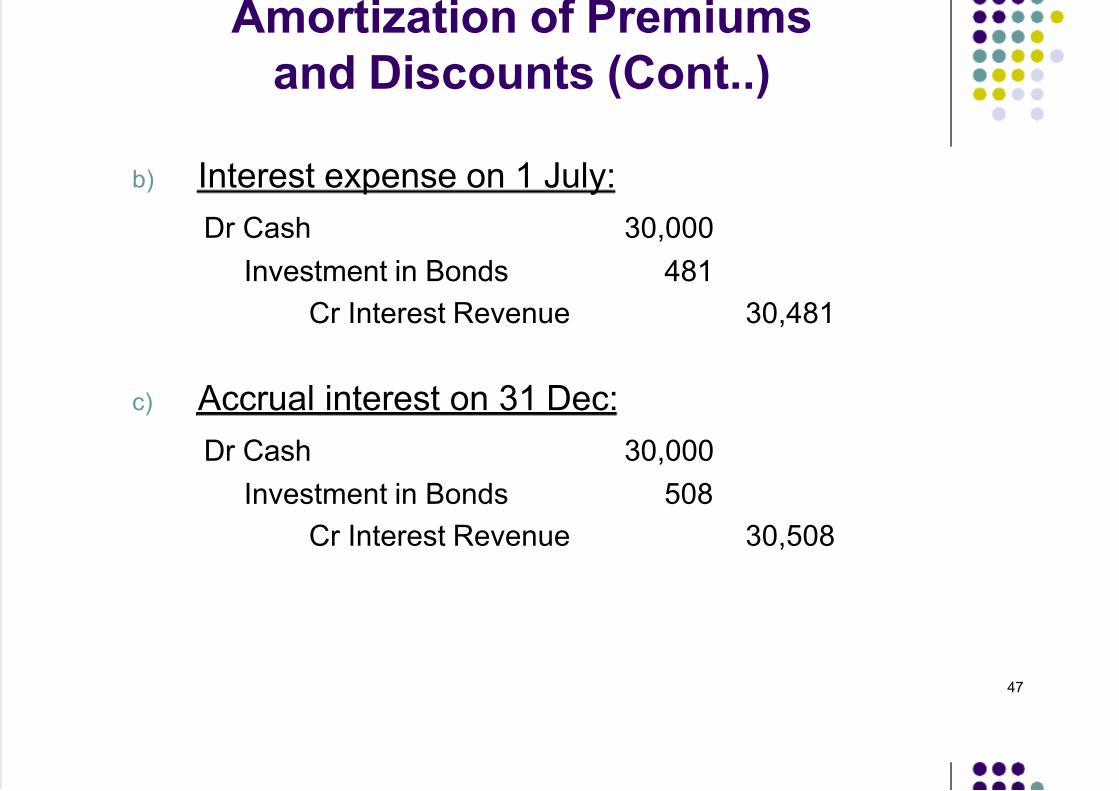

Example (effective interest method):

XYZ Bhd issued RM600,000 of 10%, 20-year bondson 1 Jan 2012. Interest is payable semiannually on 1

July and 1 Jan. XYZ Bhd uses effective interestmethod of amortization for bond premium/discount. Assume an effective rate yield of 11.5%

Prepare the journal entries to record:

a) The issuance of the bonds

b) The payment of interest on 1 July

c) The accrual of interest on 31 Dec

44

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 45/54

Amortization of Premiums

and Discounts (Cont..)

Solution (effective interest method):

a) Issuance of bonds:

i=11.5/2, n=20x2

PV 600,000 x 0.10685 = 64,110

PVOA 30,000 x 15.5330 = 465,990

Price on 1 Jan = 530,100

Dr Investment in Bond 530,100Cr Cash 530,100

45

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 46/54

Amortization of Premiums

and Discounts (Cont..)

Cash Interest

exp.

Amort. Disc Balance of

Bonds

530,100

1/7/12 30,000 30,481a 481b 530,581c

1/1/13 30,000 30,508 508 531,089

1/7/13 30,000 30538 538 531,627

a: 11.5% x 530,100 x 6/12 = 30,481

b: 30,481 – 30,000 = 481

c: 530,100 + 481 = 530,58146

f

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 47/54

Amortization of Premiums

and Discounts (Cont..)

b) Interest expense on 1 July:

Dr Cash 30,000

Investment in Bonds 481

Cr Interest Revenue 30,481

c) Accrual interest on 31 Dec:

Dr Cash 30,000

Investment in Bonds 508

Cr Interest Revenue 30,508

47

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 48/54

Bonds Acquired between Interest Dates

Adjustment for accrued interest should be done.

Accrued interest is calculated for the period in between

of the date of previous interest payment with date of

bond is sold.

Cash paid by buyer is the price of the bonds together

with the accrued interest.

Price of bonds is the present value of the bond at the

date of selling/buying.

48

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 49/54

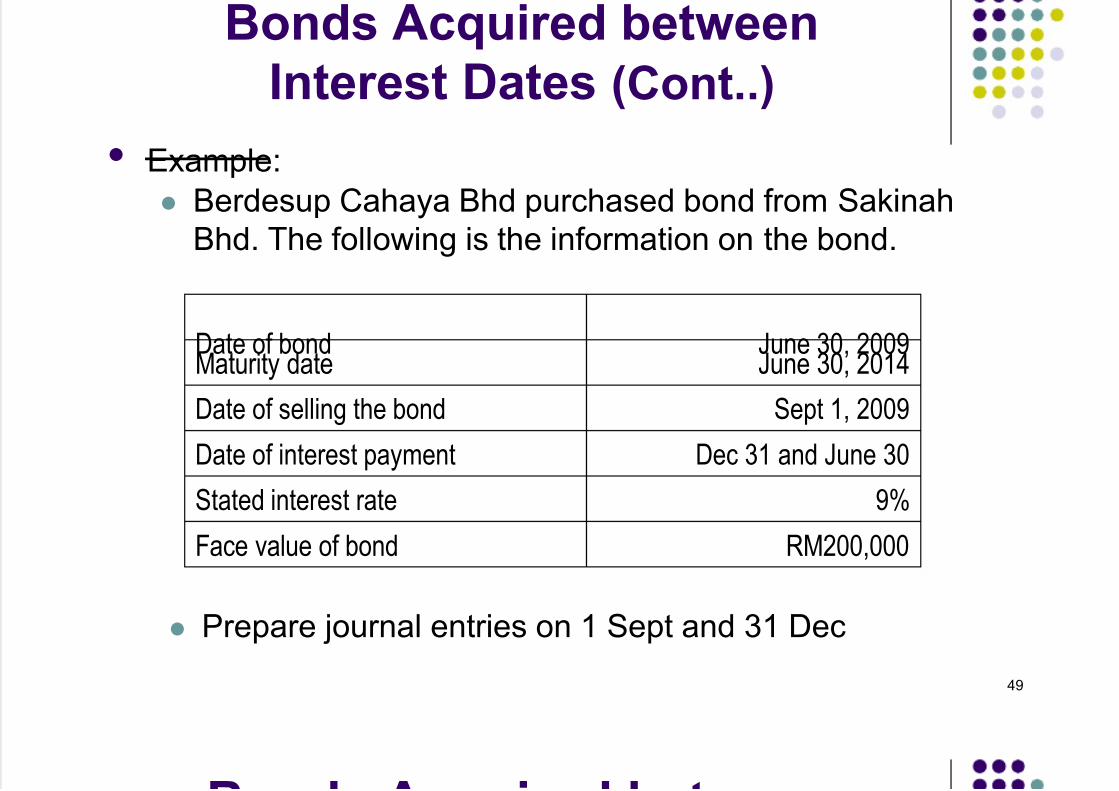

Bonds Acquired between

Interest Dates (Cont..)

Date of bond June 30, 2009Maturity date June 30, 2014

Date of selling the bond Sept 1, 2009

Date of interest payment Dec 31 and June 30

Stated interest rate 9%

Face value of bond RM200,000

Example:

Berdesup Cahaya Bhd purchased bond from Sakinah

Bhd. The following is the information on the bond.

Prepare journal entries on 1 Sept and 31 Dec

49

B d A i d b t

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 50/54

Bonds Acquired between

Interest Dates (Cont..)

Issued at discount

Effective interest rate = 11%

Price of bond at 30/6/09

Face value [PV5.5%, 10 200,000 = 0.58543 x 200,000] 117,086

Interest [PVOA5.5%, 10 9,000 = 7.53763 x 9,000] 67,839Present Value 184,925

(+) Increment of bond’s value from

30/6 – 1/9 [184,925 x 11% x 2/12] 3,390

Cash 188,315

(-) Cash paid for interest from

30/6 – 1/9 [200,000 x 9% x 2/12] (3,000)

PRICE OF BOND AT 1/9/09 185,315

50

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 51/54

Bonds Acquired between

Interest Dates (Cont..)

Journal Entries

Issuer:

Sept 1

Dr Cash 188,3151

Disc on Bond 14,6852 Cr Interest Payable 3,0003

Bonds Payable 200,000

1. 185,315 + 3,000 (interest)

2. 200,000 – 185,3153. 200,000 x 9% x 2/12

Buyer:

Sept 1

Dr Investment Bonds 185,315

Interest Receivable 3,000

Cr Cash 188,315

51

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 52/54

Bonds Acquired between

Interest Dates (Cont..)

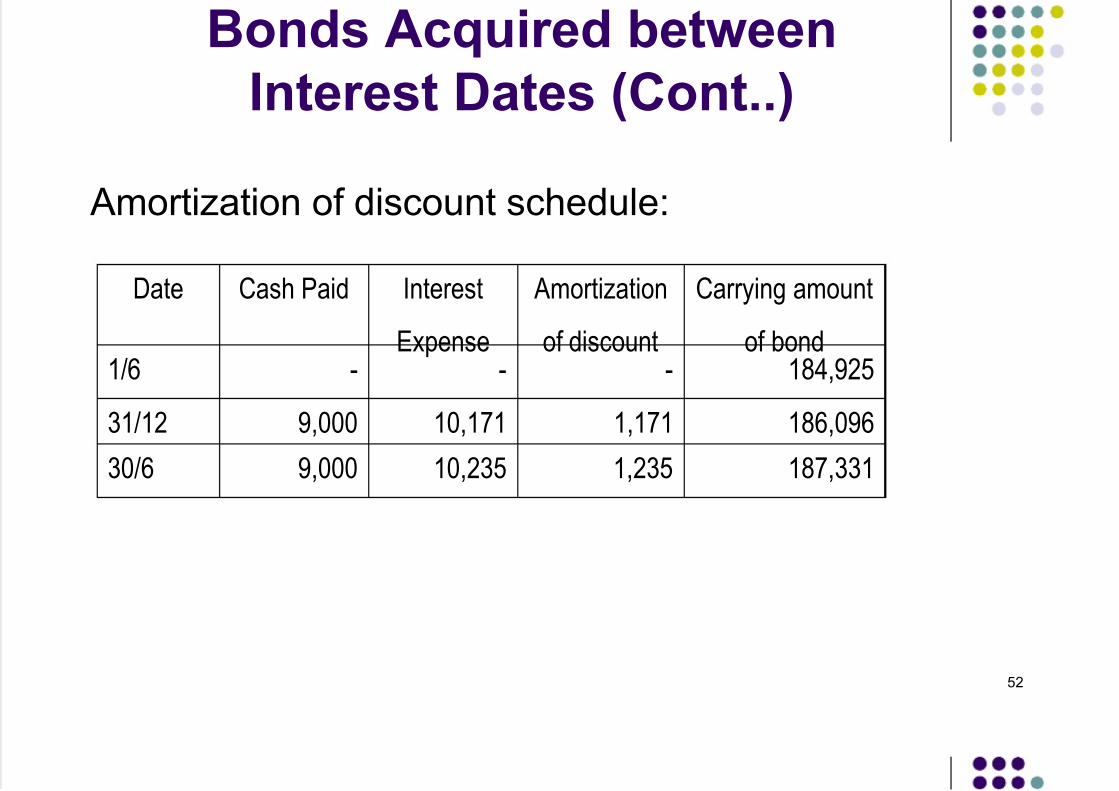

Amortization of discount schedule:

Date Cash Paid Interest

Expense

Amortization

of discount

Carrying amount

of bond1/6 - - - 184,925

31/12 9,000 10,171 1,171 186,096

30/6 9,000 10,235 1,235 187,331

52

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 53/54

Bonds Acquired between

Interest Dates (Cont..)

Journal Entries

Dec. 31

Dr Interest Expense 6,7811

Interest Payable 3,000

Cr Disc on Bonds 7812

Cash 9,000

1. 10,171 x 4/6

2. 1,171 x 4/6

Dec. 31

Dr Investment in Bonds 781Cash 9,000

Cr Interest Revenue 6,781

Interest Receivable 3,000

53

7/27/2019 topic 3 Investment in Equity Debt Securities

http://slidepdf.com/reader/full/topic-3-investment-in-equity-debt-securities 54/54

End of the Topic

54