Topic 2.3 Theory of the Firm. Cost Theory Fixed Cost: costs that do not vary with changes in output...

22

Topic 2.3 Theory of the Firm

-

Upload

branden-mosley -

Category

Documents

-

view

218 -

download

1

Transcript of Topic 2.3 Theory of the Firm. Cost Theory Fixed Cost: costs that do not vary with changes in output...

Topic 2.3 Theory of the Firm

Cost Theory

Fixed Cost: costs that do not vary with changes in output

example: rent

Variable Cost: costs that vary with quantity of output produced

example: labor, materials, fuel

Total Cost: sum of fixed cost and variable cost at each level of output

TC= FC + VC

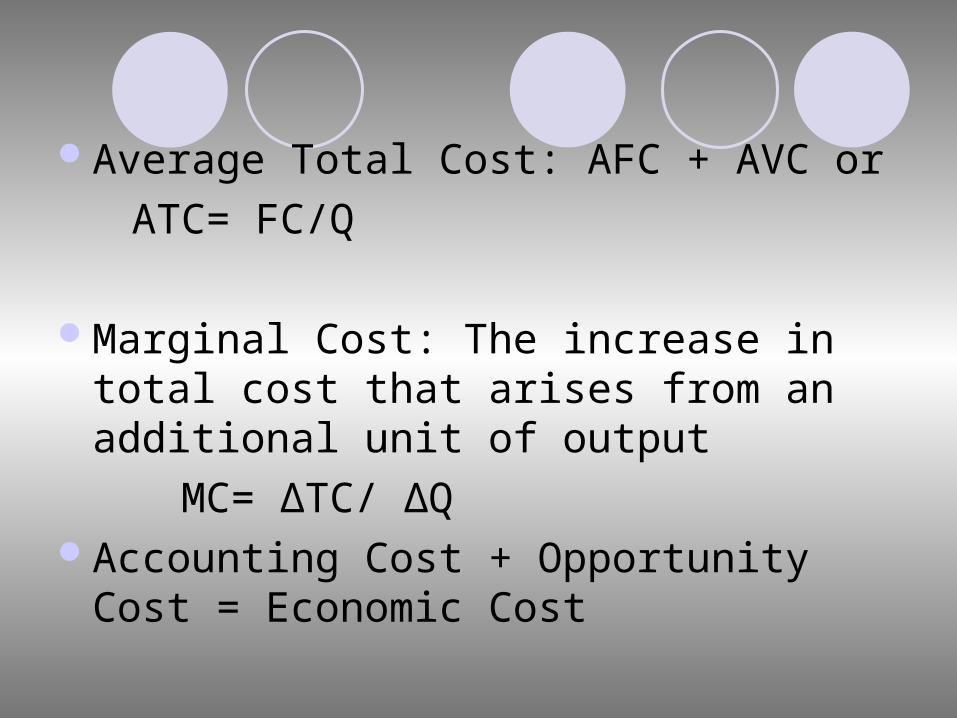

Average Total Cost: AFC + AVC or ATC= FC/Q

Marginal Cost: The increase in total cost that arises from an additional unit of output

MC= ∆TC/ ∆QAccounting Cost + Opportunity Cost

= Economic Cost

Average Fixed Cost: Fixed costs divided by the quantity output

AFC= FC/Q

Average Variable Cost: Variable costs divided by the quantity of output

AVC= VC/Q

Short-Run

Law of Diminishing Returns:

each additional unit of variable input eventually yields a decreasing output

Long-Run Economies of scale: long-run ATC as Q Diseconomies of scale: long-run ATC as Q

RevenuesTotal Revenue: The total amount of

money received from the sale of a good or service at any given quantity of output.

Marginal Revenue: The additional revenue added to the total revenue that isgained from selling one more unit.

Average Revenue: Total revenue divided by the number of units sold

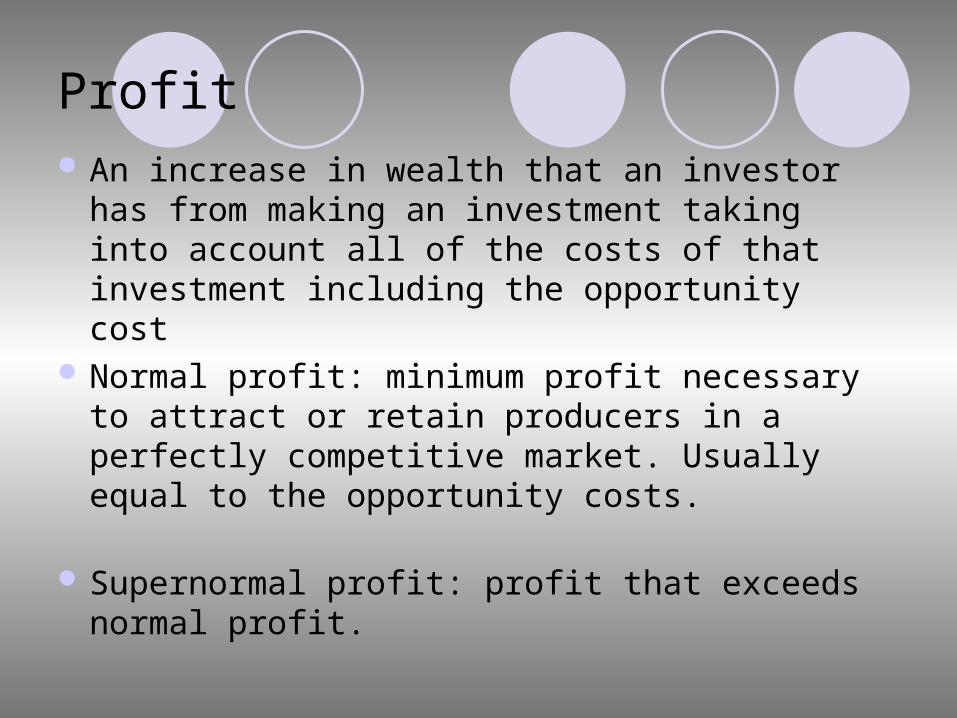

Profit An increase in wealth that an investor has

from making an investment taking into account all of the costs of that investment including the opportunity cost

Normal profit: minimum profit necessary to attract or retain producers in a perfectly competitive market. Usually equal to the opportunity costs.

Supernormal profit: profit that exceeds normal profit.

Thou shalt produce where MC=MR

Profit (continued)

Perfect Competition

>Numerous buyers and sellers of which none are able to influence the market.

>Everyone is privy to all information >Products are homogeneous >No barriers to entry and no barriers

to exit.

Perfect Competition

Thou shalt produce where MC = MR. Efficiency in perfect Competition is both

allocatively and productively efficient Allocative efficiency occurs when output is

at society's optimum level. P=MC Productive efficiency is when a firm

produces at the lowest possible cost per unit. AC=MC

Perfect Competition

Monopoly

>One firm >Unique product, no close substitutes>Considerable control over price>Entry of additional firms are blocked>No effort in advertising

Monopoly (continued) Sources of Power1. Status secured by patents,

economies of scale, or resources ownership

2. Not regulated by government3. Costs of production make a single

producer more efficient than a large number of producers

Monopoly

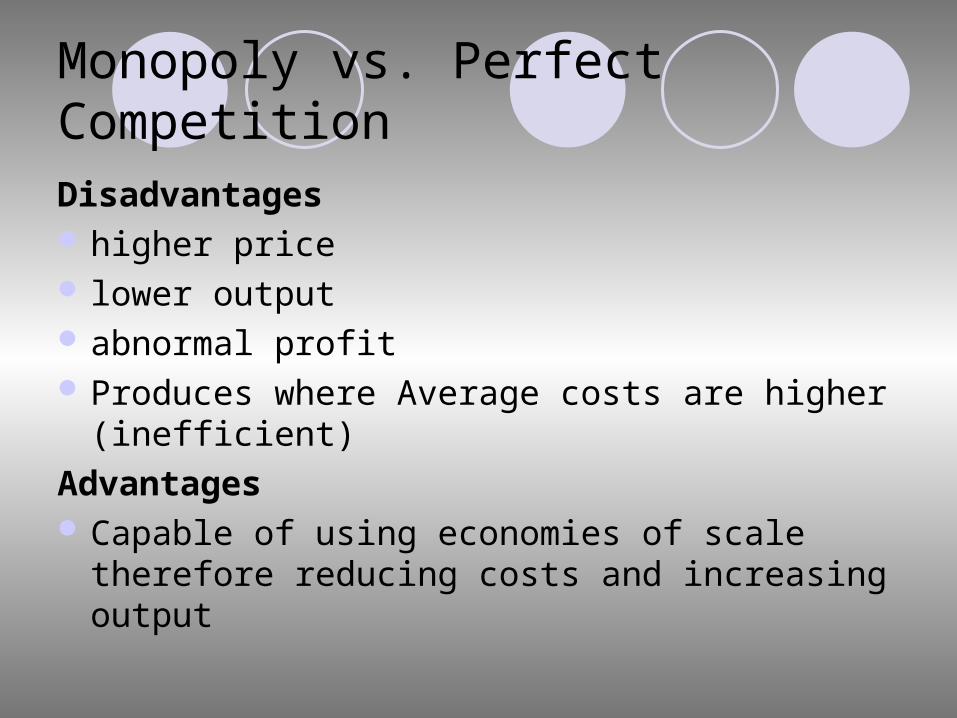

Monopoly vs. Perfect CompetitionDisadvantages higher price lower output abnormal profit Produces where Average costs are higher

(inefficient)Advantages Capable of using economies of scale

therefore reducing costs and increasing output

Natural MonopolyMonopoly that arises because a

single firm can supply a good or service to an entire market at a smaller cost than could two or more

Monopolistic Competition

Large number of small firms. (Almost) perfect knowledge. Differentiated products. No barriers to entry or exit. In the short-run abnormal profits can

be earned (at MC=MR) In the long-run only normal profits

can be earned.

Oligopoly

Competition between a few firms many buyers, few sellers differentiated products Barriers to entry present If one firm reduces its price

competitors will follow example

Oligopoly (continued)

Non-collusive Oligopoly: firms compete against each other in a normal way

Collusive Oligopoly: firms try to come to an agreement to reduce the amount of competition.

Cartels: OPEC

Price Discrimination

Different people are charged different prices for exactly the same good.

Conditions>Time>Income>Age