TOP-30 PRE-PACKAGED SOFTWARE COMPANIES

35

Secrets of Software Success: Chapter 2007 January 16, 2007 Gareth Morgan, McKinsey & Co Irish Software Association

description

Transcript of TOP-30 PRE-PACKAGED SOFTWARE COMPANIES

Secrets of Software Success: Chapter 2007January 16, 2007Gareth Morgan, McKinsey & CoIrish Software Association

Secrets of Software Success

•Quick overview of Global Software landscape

–Dimensions for key segments

•Macro-economic industry trends

•Traditional success factors in software industry

•Building blocks for successful software companies in the future

•Open discussion

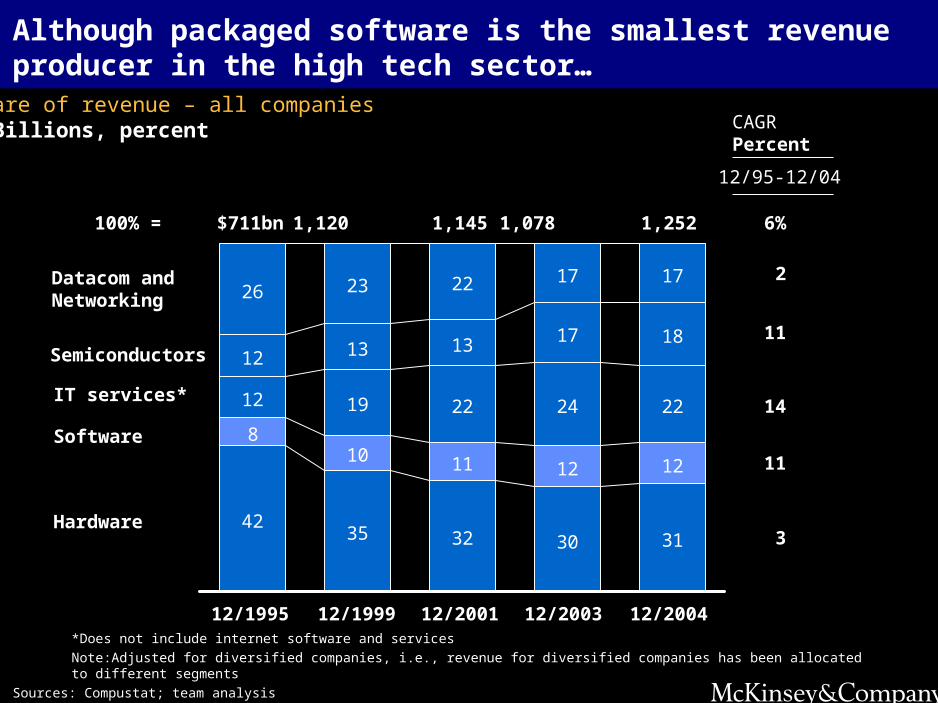

Although packaged software is the smallest revenue producer in the high tech sector…

*Does not include internet software and services

Note:Adjusted for diversified companies, i.e., revenue for diversified companies has been allocated to different segments

Sources: Compustat; team analysis

Share of revenue – all companies$ Billions, percent

4235 32 30 31

810 11 12 12

12 19 22 24 22

12 13 13 17 18

26 23 22 17 17

$711bn

IT services*

Datacom and Networking

12/200112/1995 12/1999 12/2003

100% =

Semiconductors

1,120 1,145 1,078

Software

Hardware

CAGRPercent

12/95-12/04

6%

2

11

3

11

14

12/2004

1,252

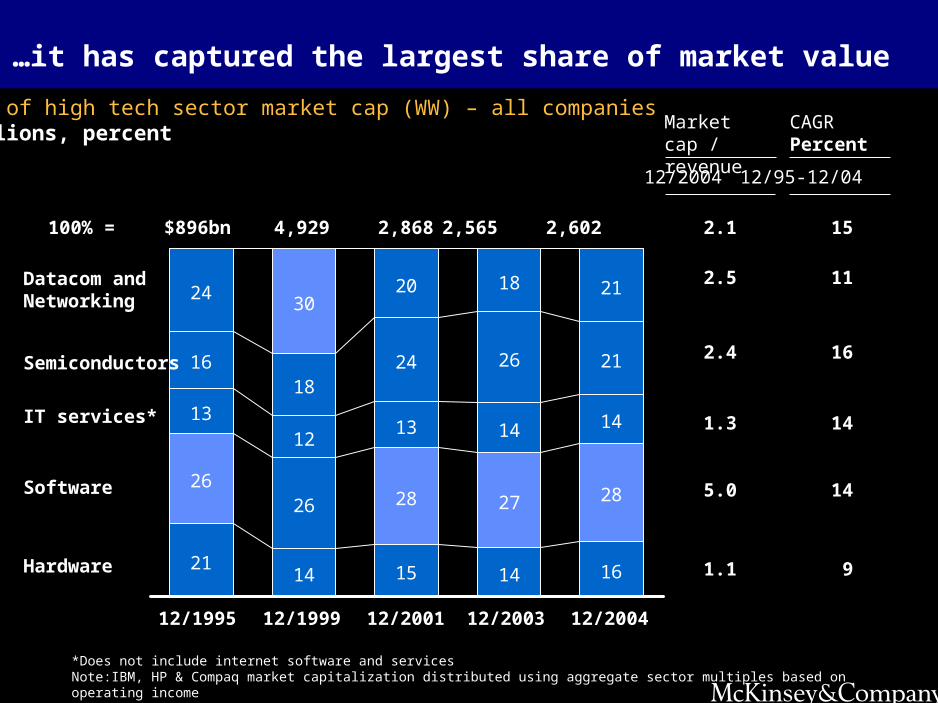

…it has captured the largest share of market value

*Does not include internet software and servicesNote:IBM, HP & Compaq market capitalization distributed using aggregate sector multiples based on operating incomeSources:Compustat; team analysis

Share of high tech sector market cap (WW) – all companies$ Billions, percent

$896bn

12/200312/1995 12/2001

100% = 4,929 2,868 2,565

CAGRPercent

12/95-12/04

15

2114 15 14 16

28

1312

13 14 14

1618

24 26 21

2430

20 18 21

26 28 2726

IT services*

Datacom and Networking

Semiconductors

Software

Hardware

11

16

9

14

14

12/1999

Market cap / revenue

2.1

12/2004

2.5

2.4

1.3

5.0

1.1

12/2004

2,602

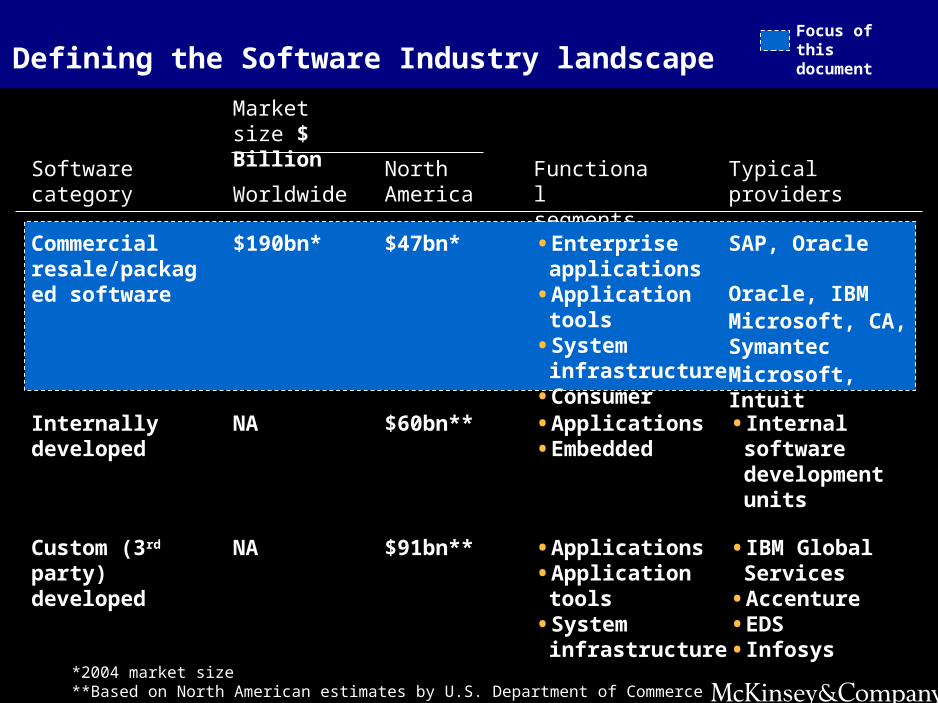

Defining the Software Industry landscape

Software category

Market size $ Billion

Functional segments

Typical providers

Commercial resale/packaged software

$190bn* • Enterprise applications

• Application tools• System

infrastructure• Consumer

SAP, Oracle

Oracle, IBMMicrosoft, CA, SymantecMicrosoft, Intuit

Internally developed

NA • Applications• Embedded

• Internal software development units

Custom (3rd party) developed

NA • Applications• Application tools• System

infrastructure

• IBM Global Services

• Accenture• EDS• Infosys

Focus of this document

WorldwideNorth America

$47bn*

$60bn**

$91bn**

*2004 market size**Based on North American estimates by U.S. Department of Commerce

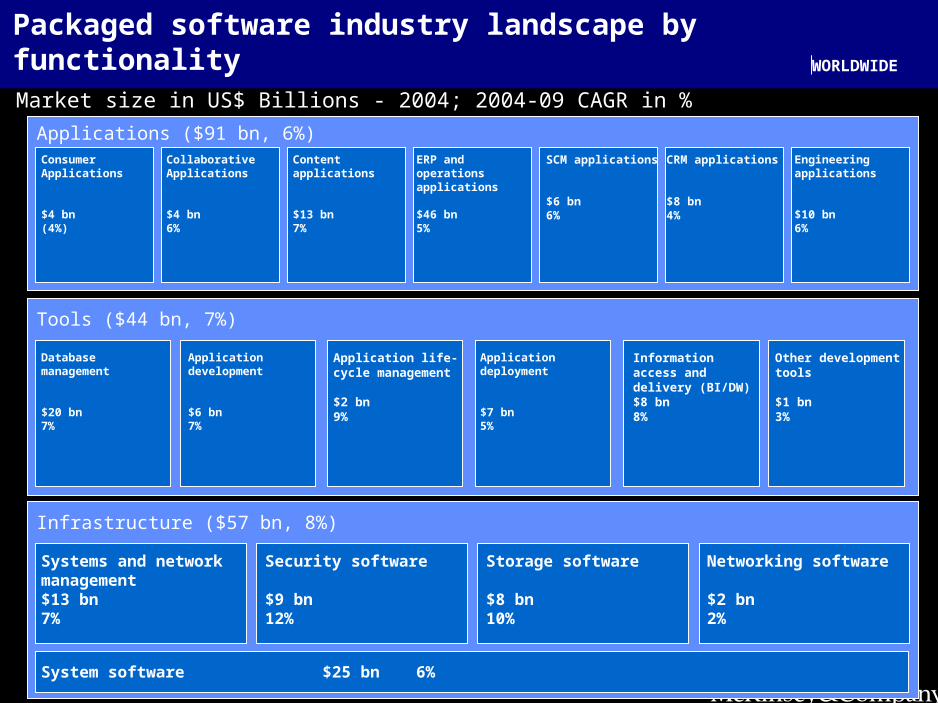

Packaged software industry landscape by functionality

Applications ($91 bn, 6%)

Market size in US$ Billions - 2004; 2004-09 CAGR in %

ConsumerApplications

$4 bn (4%)

Tools ($44 bn, 7%)

Infrastructure ($57 bn, 8%)

CollaborativeApplications

$4 bn6%

Content applications

$13 bn7%

ERP and operations applications

$46 bn5%

SCM applications

$6 bn6%

CRM applications

$8 bn4%

Engineering applications

$10 bn6%

Systems and network management$13 bn7%

Security software

$9 bn12%

Storage software

$8 bn10%

Networking software

$2 bn2%

System software $25 bn 6%

Database management

$20 bn7%

Application development

$6 bn7%

Application life-cycle management

$2 bn9%

Application deployment

$7 bn5%

Information access and delivery (BI/DW)$8 bn8%

Other development tools

$1 bn3%

WORLDWIDE

Secrets of Software Success

•Quick overview of Global Software landscape

–Dimensions for key segments

•Macro-economic industry trends

•Traditional success factors in software industry

•Building blocks for successful software companies in the future

•Open discussion

Macro-economic industry trends- observations

•Growth stabilizing; margins increasing

•Restructuring continues and investment increases

•Both supply and demand continue to globalize

0

5

10

15

20

25

1995 1998 2001 2004

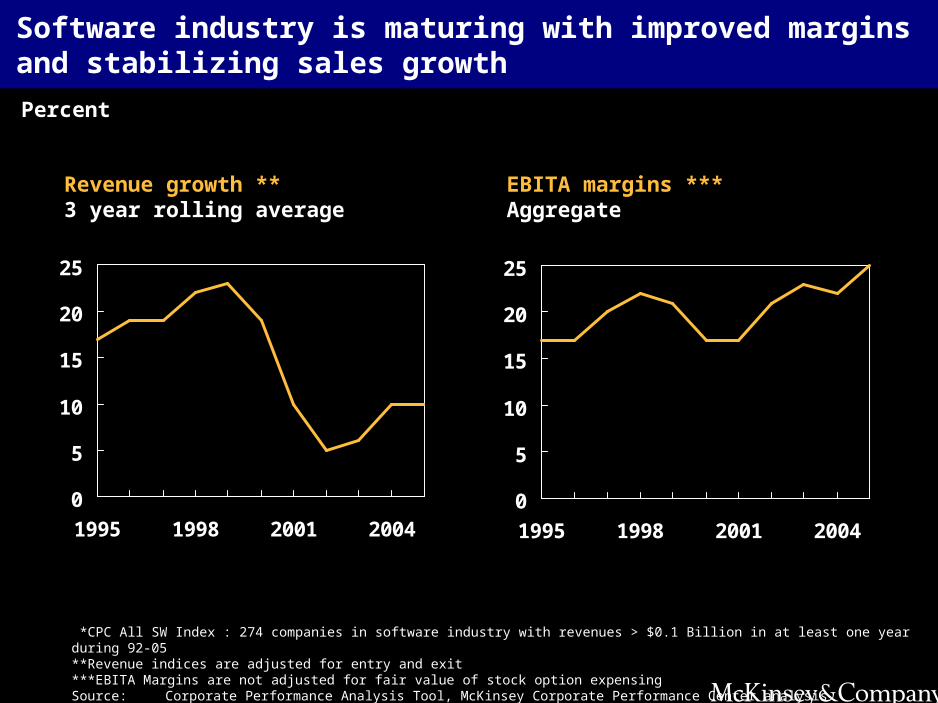

Software industry is maturing with improved marginsand stabilizing sales growth

0

5

10

15

20

25

1995 1998 2001 2004

Revenue growth **3 year rolling average

Percent

EBITA margins ***Aggregate

*CPC All SW Index : 274 companies in software industry with revenues > $0.1 Billion in at least one year during 92-05**Revenue indices are adjusted for entry and exit***EBITA Margins are not adjusted for fair value of stock option expensingSource:Corporate Performance Analysis Tool, McKinsey Corporate Performance Center analysis

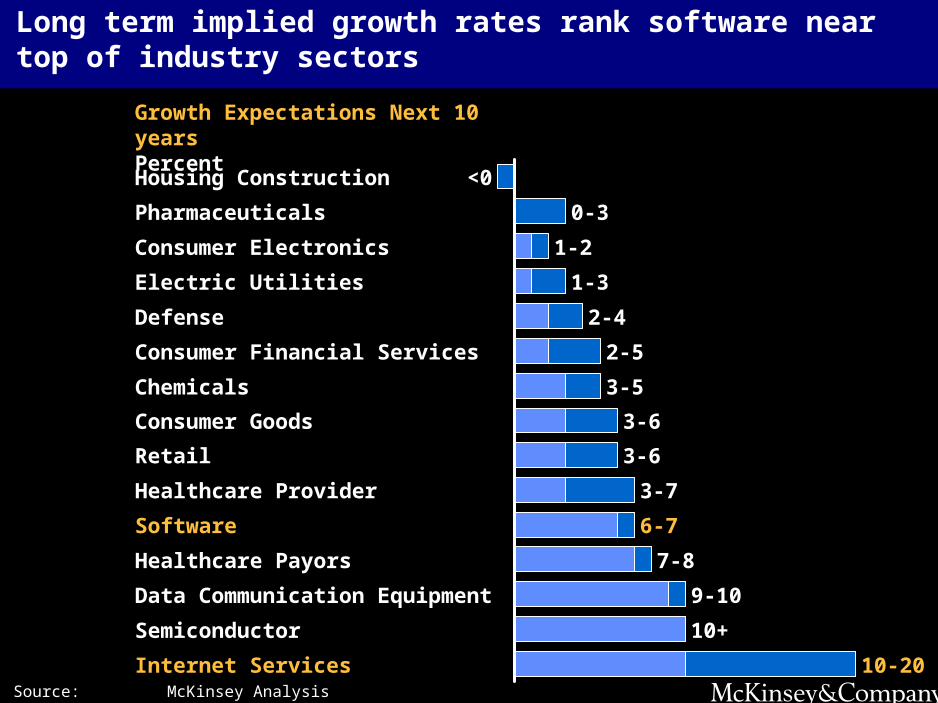

Long term implied growth rates rank software near top of industry sectors

Source: McKinsey Analysis

Data Communication Equipment

Consumer Goods

Retail

Semiconductor

Healthcare Payors

Chemicals

Defense

Healthcare Provider

Consumer Financial Services

Consumer Electronics

Electric Utilities

Housing Construction <0

Pharmaceuticals

Internet Services

10+

9-10

7-8

6-7

3-7

3-6

3-6

3-5

2-5

Software

1-3

0-3

1-2

2-4

10-20

Growth Expectations Next 10 yearsPercent

-10

0

10

20

30

40

50

1995 1998 2001 2004

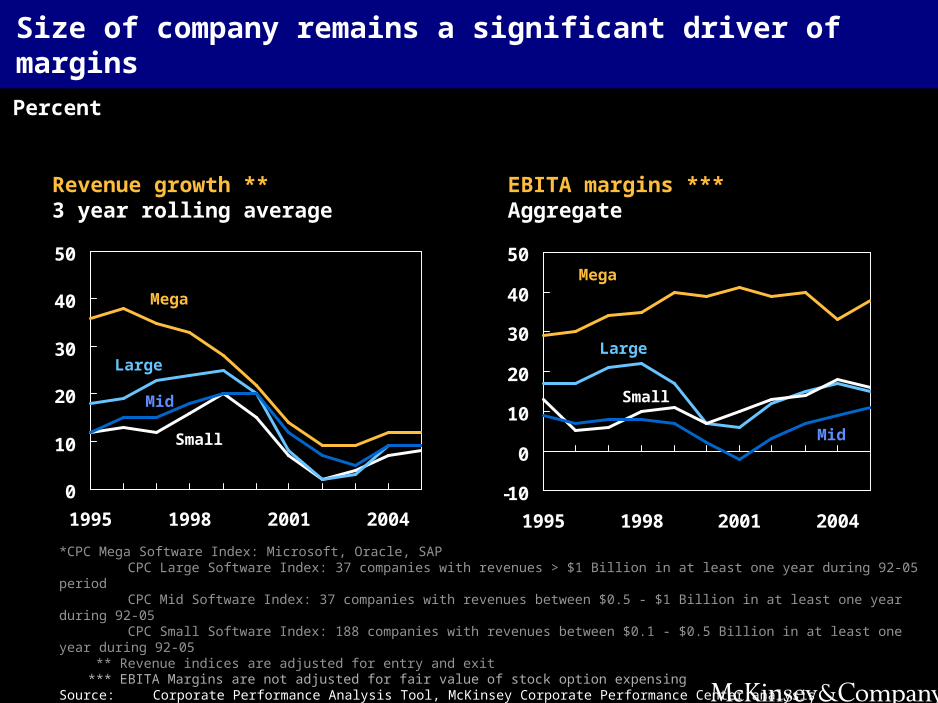

Size of company remains a significant driver of margins

0

10

20

30

40

50

1995 1998 2001 2004

Percent

Revenue growth **3 year rolling average

EBITA margins ***Aggregate

*CPC Mega Software Index: Microsoft, Oracle, SAP CPC Large Software Index: 37 companies with revenues > $1 Billion in at least one year during 92-05 period CPC Mid Software Index: 37 companies with revenues between $0.5 - $1 Billion in at least one year during 92-05 CPC Small Software Index: 188 companies with revenues between $0.1 - $0.5 Billion in at least one year during 92-05 ** Revenue indices are adjusted for entry and exit *** EBITA Margins are not adjusted for fair value of stock option expensing

Source:Corporate Performance Analysis Tool, McKinsey Corporate Performance Center analysis

Mega

Mega

LargeLarge

Mid

Mid

Small

Small

Global software deal volume and values are growing steadily

10

38 44

86

11 1125 20

4132

0

20

40

60

80

100

120

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006*

0

200

400

600

800

M&A* Value of Deals$ Billion

Count of DealsNumber

* Global Software Industry , ** United States and Europe , *** Through 11/1/2006

Source: Dealogic , Thomson Financial , Capital IQ

1 26

17

84 3

7 7 8

0

10

20

30

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006*

0

200

400

600

800

PE & VC ** Value of Deals$ Billion

Count of DealsNumber

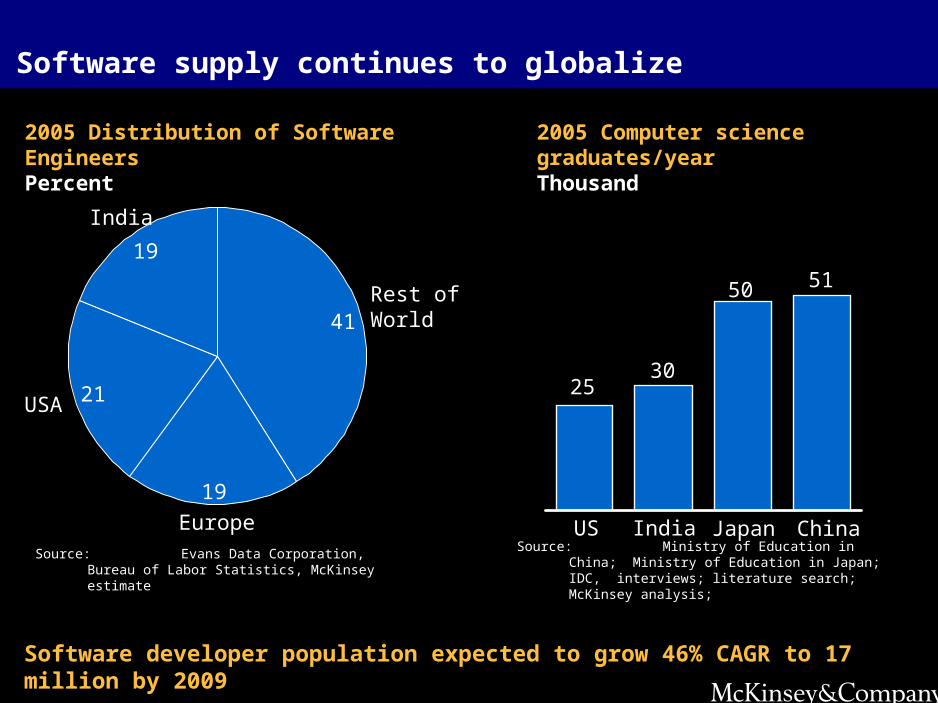

Software supply continues to globalize

2005 Computer science graduates/yearThousand

51

2530

50

US India Japan China

Source: Ministry of Education in China; Ministry of Education in Japan; IDC, interviews; literature search; McKinsey analysis;

Source: Evans Data Corporation, Bureau of Labor Statistics, McKinsey estimate

India

19

USA 21

Europe

19

Rest ofWorld41

2005 Distribution of Software EngineersPercent

Software developer population expected to grow 46% CAGR to 17 million by 2009

Secrets of Software Success

•Quick overview of Global Software landscape

–Dimensions for key segments

•Macro-economic industry trends

•Traditional success factors in software industry

•Building blocks for successful software companies in the future

•Open discussion

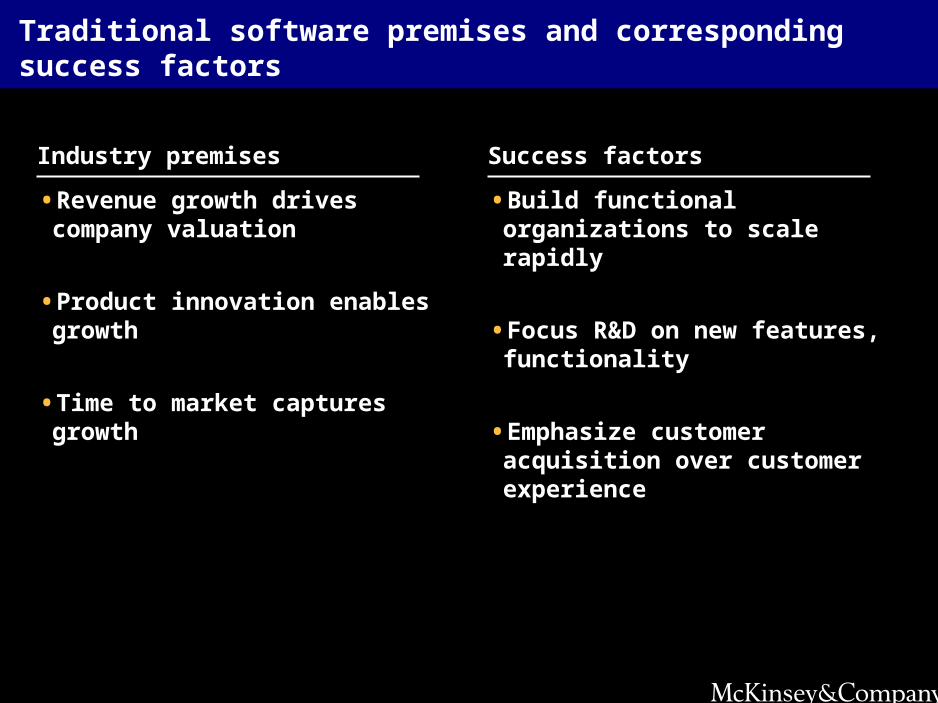

Traditional software premises and corresponding success factors

•Revenue growth drives company valuation

•Product innovation enables growth

•Time to market captures growth

Industry premises

•Build functional organizations to scale rapidly

•Focus R&D on new features, functionality

•Emphasize customer acquisition over customer experience

Success factors

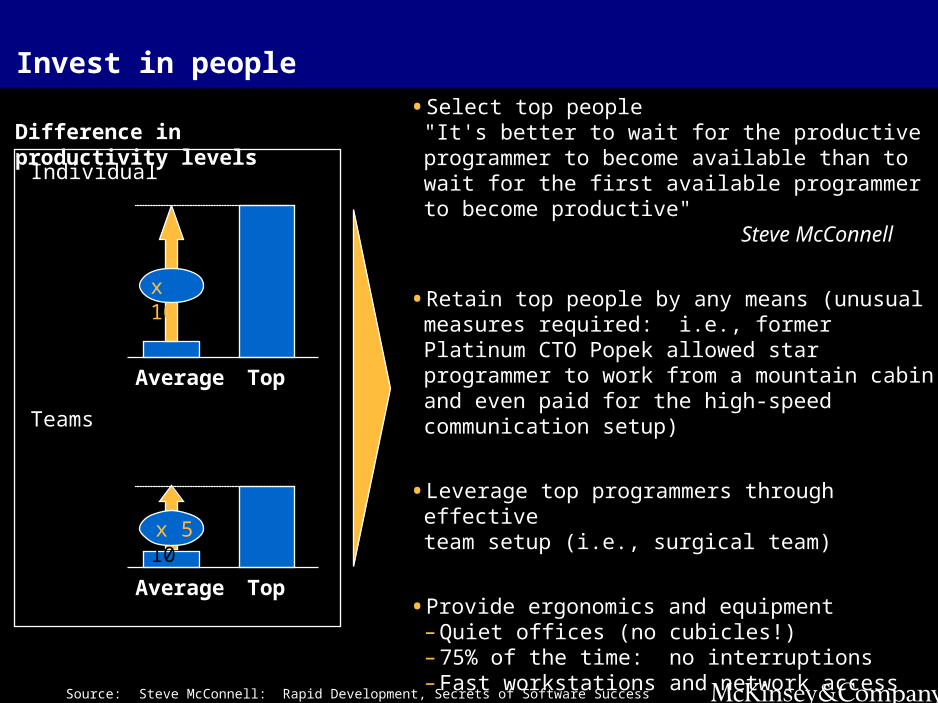

Invest in people

Source:Steve McConnell: Rapid Development, Secrets of Software Success

Difference in productivity levels

Individual

Average Top

Average Top

Teams

x 10

x 10x 5

• Select top people"It's better to wait for the productive programmer to become available than to wait for the first available programmer to become productive" Steve McConnell

• Retain top people by any means (unusual measures required: i.e., former Platinum CTO Popek allowed star programmer to work from a mountain cabin and even paid for the high-speed communication setup)

• Leverage top programmers through effective team setup (i.e., surgical team)

• Provide ergonomics and equipment– Quiet offices (no cubicles!)– 75% of the time: no interruptions– Fast workstations and network access

• Training programs– 5 - 15 days per year internal training– 1 - 4 paid external conferences– Material for autodidactic training

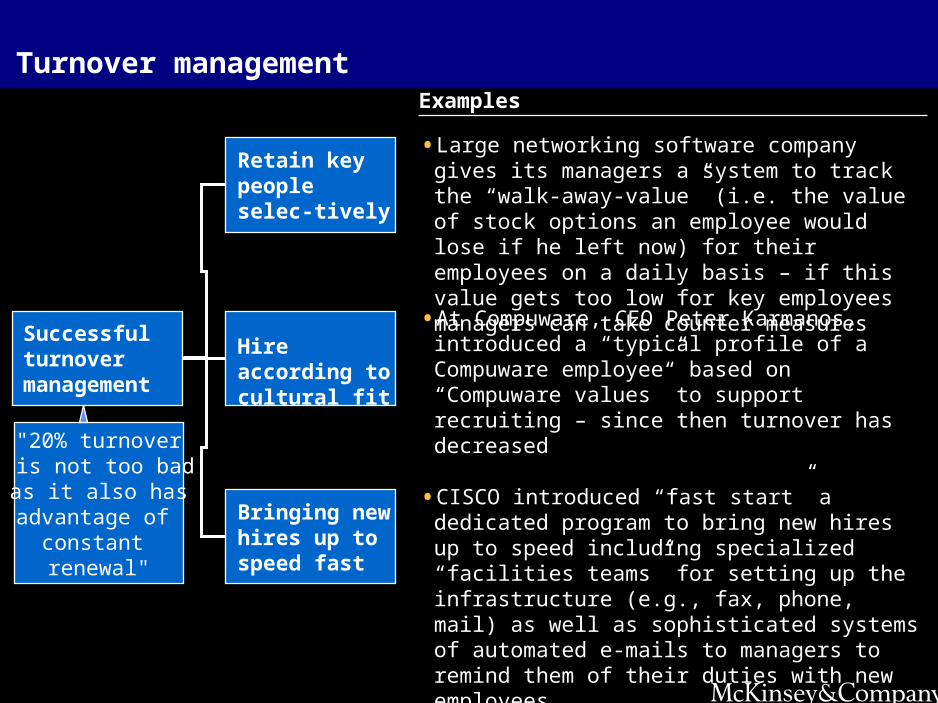

Turnover management

Source:Secrets of Software Success

Examples

• Large networking software company gives its managers a system to track the “walk-away-value” (i.e. the value of stock options an employee would lose if he left now) for their employees on a daily basis – if this value gets too low for key employees managers can take counter measures

Retain key people selec-tively

• At Compuware, CEO Peter Karmanos, introduced a “typical profile of a Compuware employee” based on “Compuware values” to support recruiting – since then turnover has decreased

Hire according to cultural fit

• CISCO introduced “fast start” a dedicated program to bring new hires up to speed including specialized “facilities teams” for setting up the infrastructure (e.g., fax, phone, mail) as well as sophisticated systems of automated e-mails to managers to remind them of their duties with new employees

Bringing new hires up to speed fast

Successful turnover management

"20% turnover is not too bad as it also has advantage of

constant renewal"

But the world has changed

• Growth constrained by macro- and microeconomics

• Customers want improved experience, not just innovation

• Global mobility of capital and talent straining organizations

• Competition for software margins increasing, both inside and outside industry

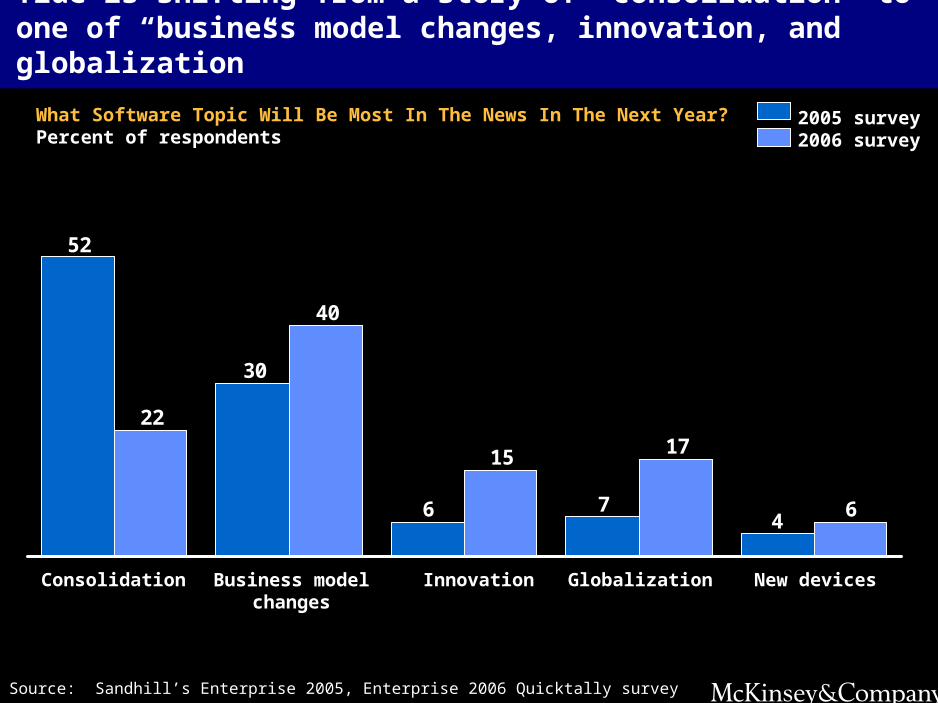

Tide is shifting from a story of “consolidation” to one of “business model changes, innovation, and globalization”

476

30

52

6

1715

40

22

Business model changes

Consolidation Innovation Globalization New devices

What Software Topic Will Be Most In The News In The Next Year?Percent of respondents

2005 survey2006 survey

Source: Sandhill’s Enterprise 2005, Enterprise 2006 Quicktally survey

Secrets of Software Success

•Quick overview of Global Software landscape

–Dimensions for key segments

•Macro-economic industry trends

•Traditional success factors in software industry

•Building blocks for successful software companies in the future

•Open discussion

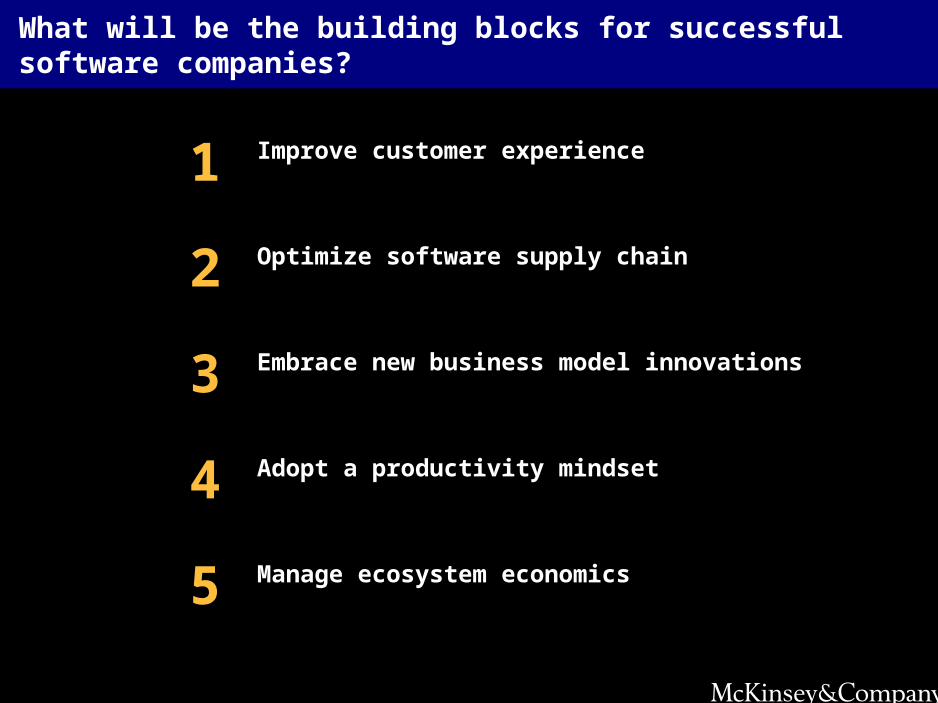

What will be the building blocks for successful software companies?

Adopt a productivity mindset4

Embrace new business model innovations3

Improve customer experience1

Optimize software supply chain2

Manage ecosystem economics5

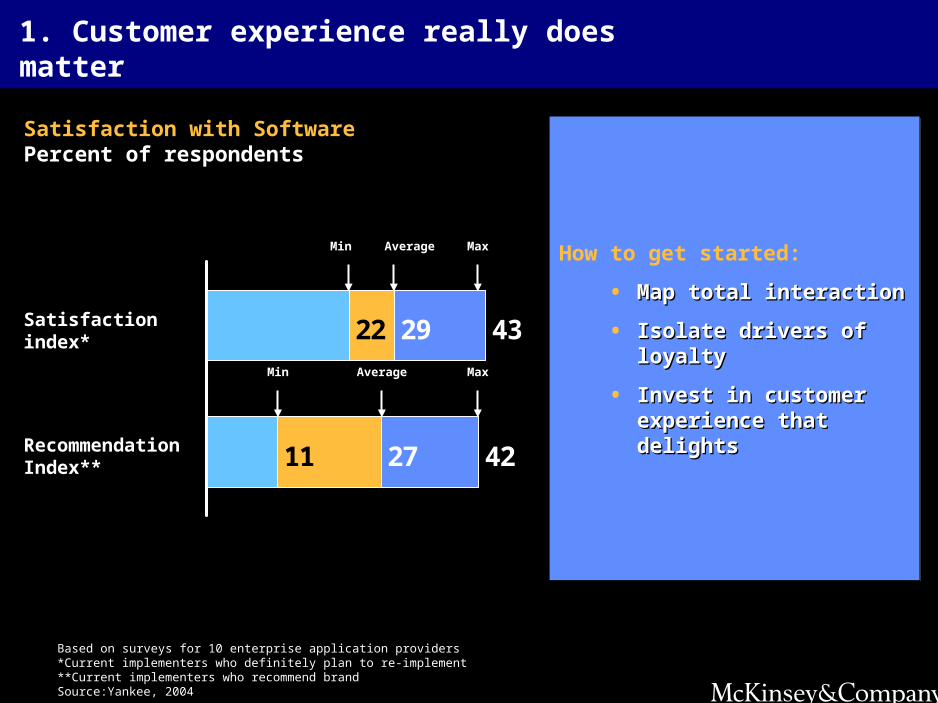

1. Customer experience really does matter

Based on surveys for 10 enterprise application providers*Current implementers who definitely plan to re-implement**Current implementers who recommend brandSource:Yankee, 2004

Satisfaction index*

Recommendation Index**

2922

11

43

4227

Min MaxAverage

Min MaxAverage

Satisfaction with Software Percent of respondents

How to get started:

• Map total interactionMap total interaction

• Isolate drivers of loyaltyIsolate drivers of loyalty

• Invest in customer Invest in customer experience that delightsexperience that delights

How to get started:

• Map total interactionMap total interaction

• Isolate drivers of loyaltyIsolate drivers of loyalty

• Invest in customer Invest in customer experience that delightsexperience that delights

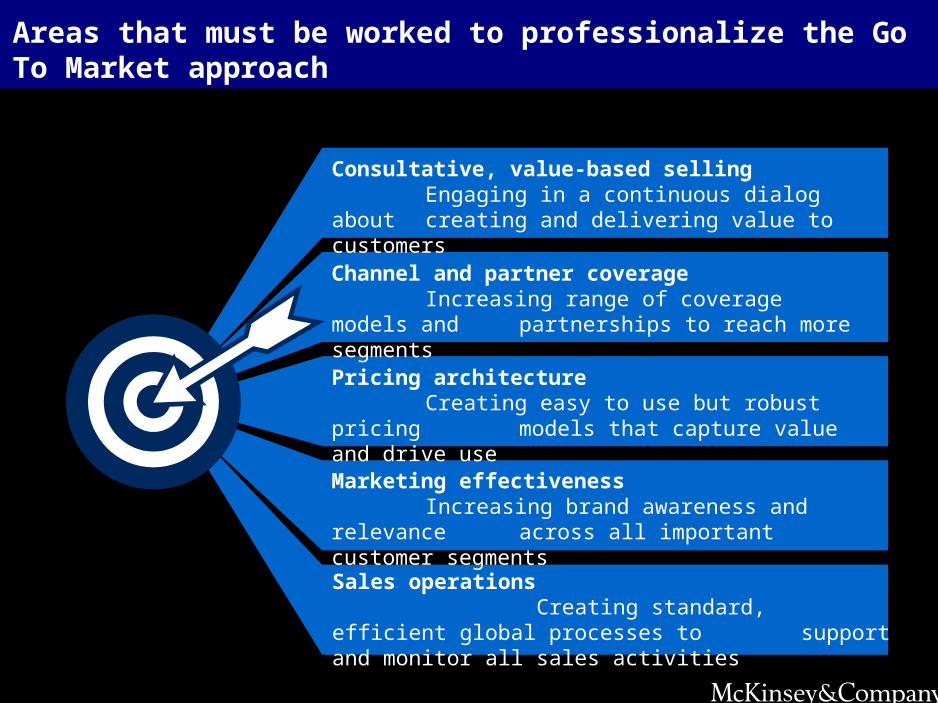

Areas that must be worked to professionalize the Go To Market approach

Consultative, value-based sellingEngaging in a continuous dialog about

creating and delivering value to customers

Channel and partner coverageIncreasing range of coverage models and partnerships to reach more segments

Marketing effectivenessIncreasing brand awareness and relevance across all important customer segments

Pricing architectureCreating easy to use but robust pricing

models that capture value and drive use

Sales operations Creating standard, efficient global processes to

support and monitor all sales activities

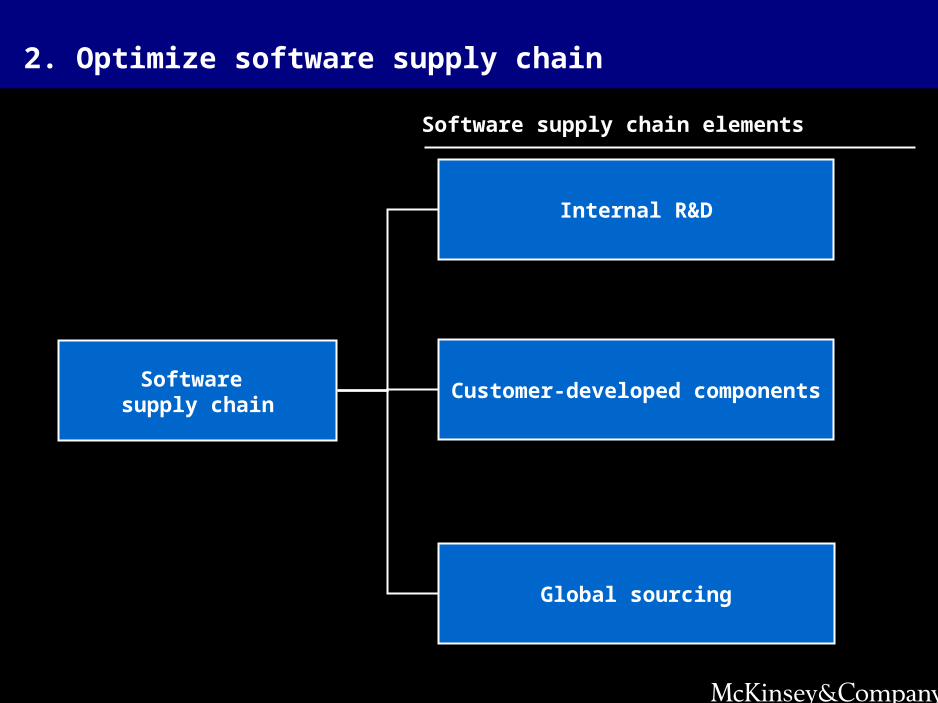

2. Optimize software supply chain

Software supply chain elements

Software supply chain

Internal R&D

Global sourcing

Customer-developed components

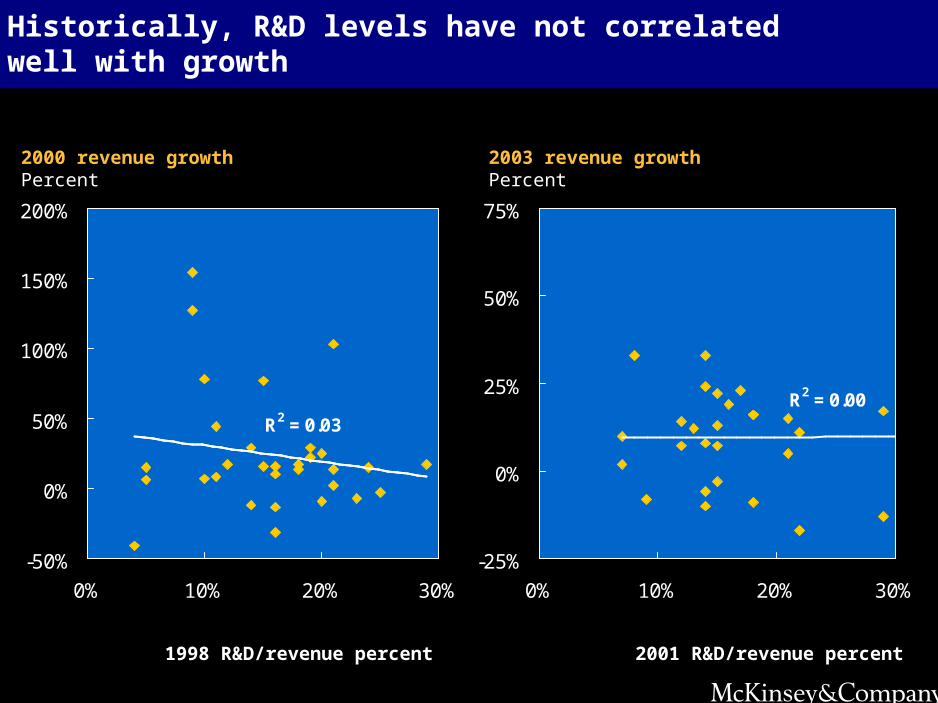

Historically, R&D levels have not correlated well with growth

2000 revenue growth Percent

1998 R&D/revenue percent

R2 = 0.03

-50%

0%

50%

100%

150%

200%

0% 10% 20% 30%

2003 revenue growth Percent

2001 R&D/revenue percent

R2 = 0.00

-25%

0%

25%

50%

75%

0% 10% 20% 30%

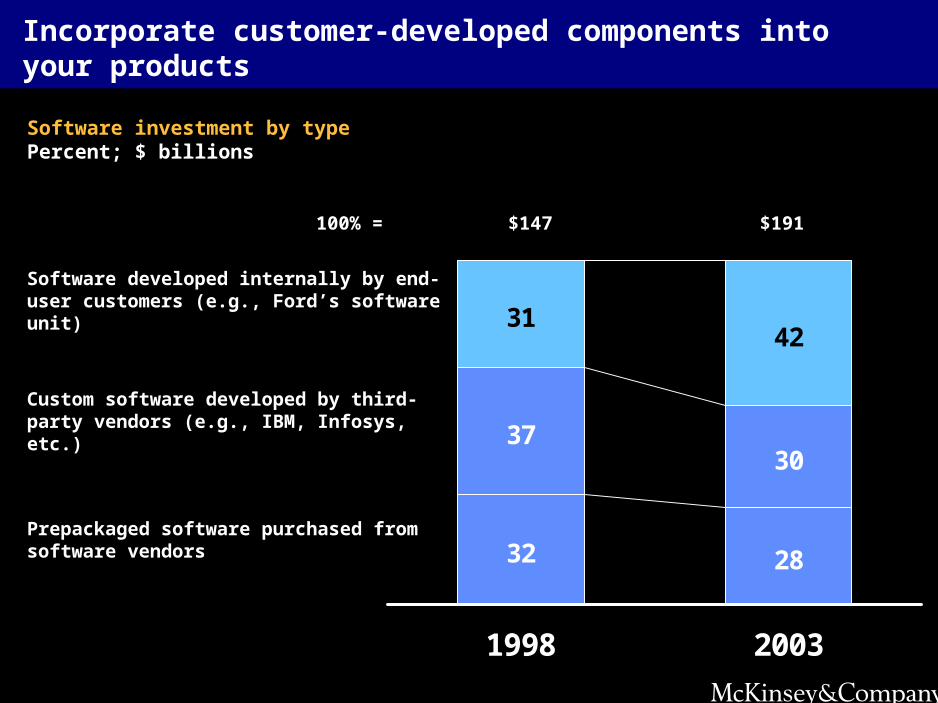

Incorporate customer-developed components into your products

Software investment by type Percent; $ billions

28

30

3142

32

37

1998 2003

Software developed internally by end-user customers (e.g., Ford’s software unit)

Custom software developed by third-party vendors (e.g., IBM, Infosys, etc.)

Prepackaged software purchased from software vendors

100% = $147 $191

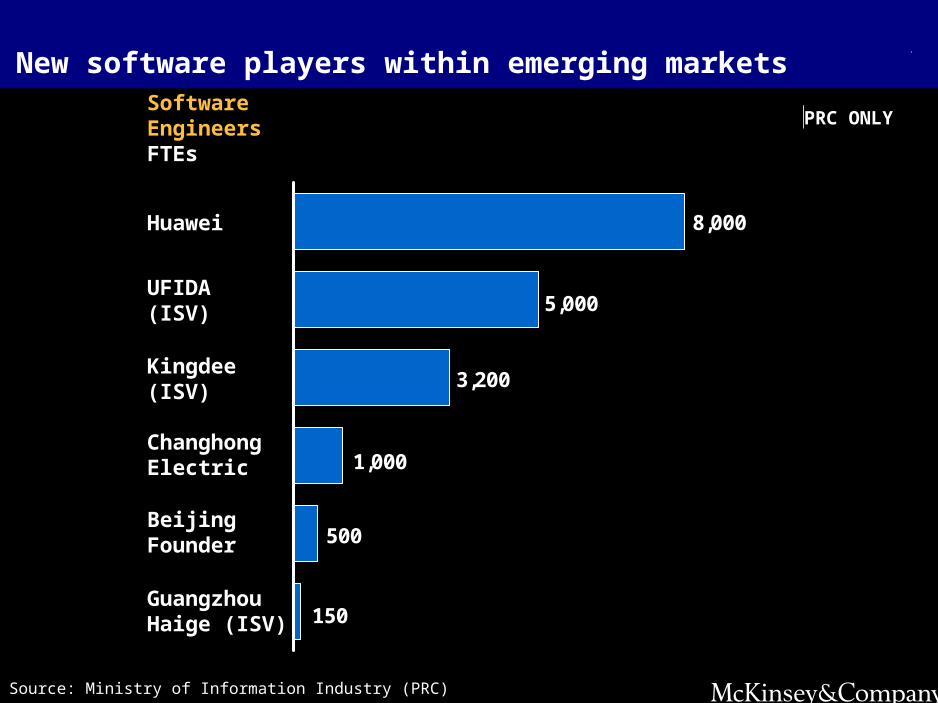

8,000

5,000

3,200

1,000

500

150

Software EngineersFTEs

Huawei

UFIDA(ISV)

Changhong Electric

Beijing Founder

Guangzhou Haige (ISV)

*Footnote

Source: Source

Kingdee(ISV)

Source: Ministry of Information Industry (PRC)

New software players within emerging markets

PRC ONLY

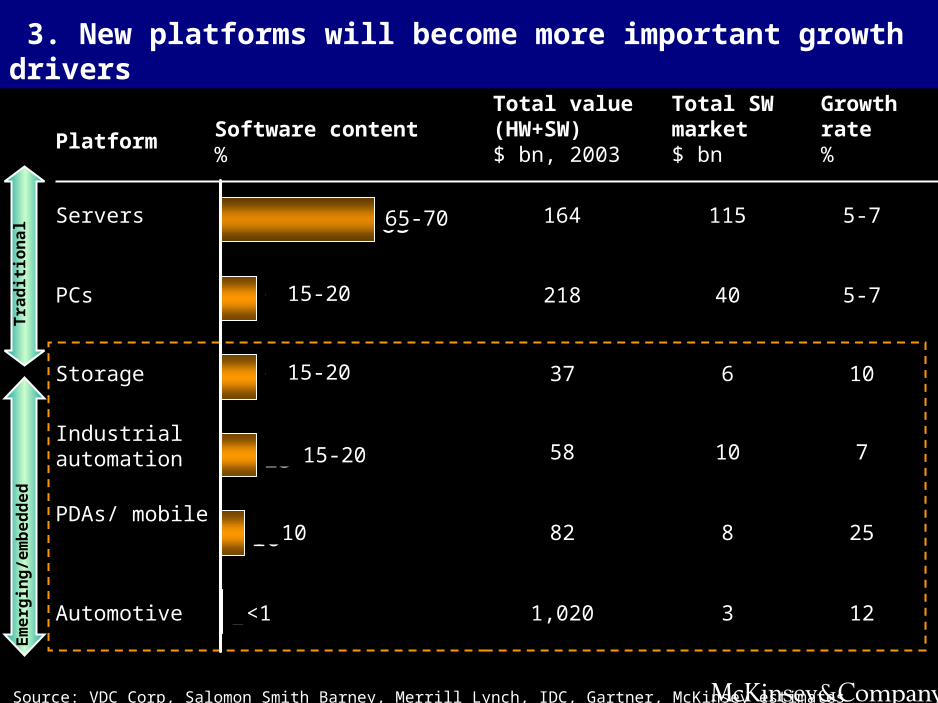

3. New platforms will become more important growth drivers

Source: VDC Corp, Salomon Smith Barney, Merrill Lynch, IDC, Gartner, McKinsey estimates

Total value (HW+SW)$ bn, 2003

PlatformSoftware content %

Total SW market $ bn

Tra

dit

ion

al

Em

erg

ing

/em

be

dd

ed

Growth rate%

PCs 218 40 5-7

Servers 164 115 5-7

Industrial automation 58 10 7

Automotive 1,020 3 12

PDAs/ mobile82 8 25

Storage 37 6 10

1

10

15

15

15

65

15-20

65-70

15-20

<1

10

15-20

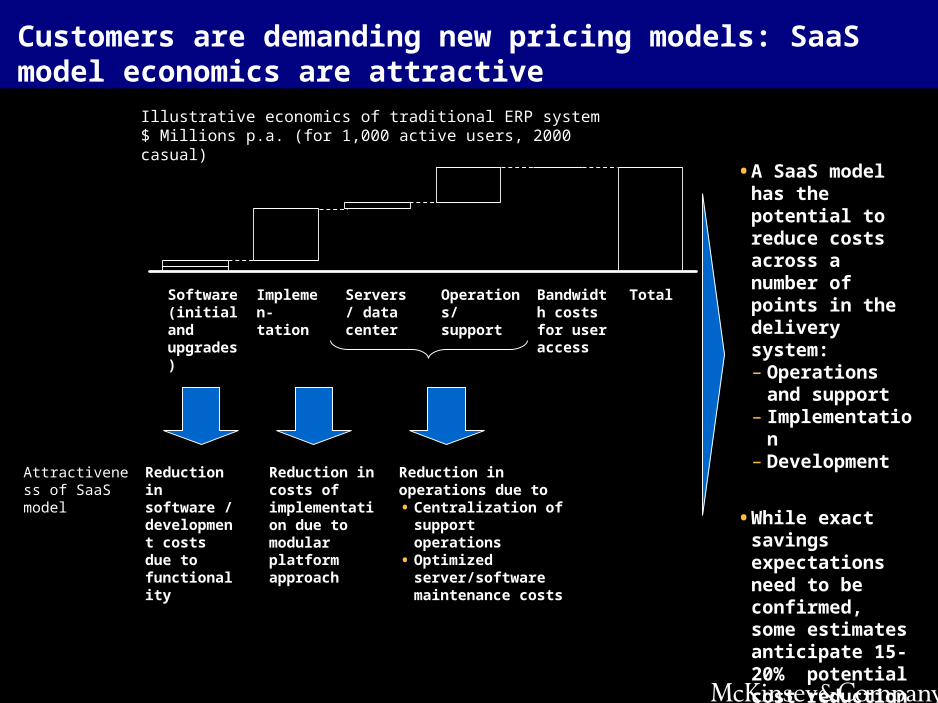

Illustrative economics of traditional ERP system $ Millions p.a. (for 1,000 active users, 2000 casual)

Software (initial and upgrades)

Implemen-tation

Servers/ data center

Operations/ support

Bandwidth costs for user access

Total

• A SaaS model has the potential to reduce costs across a number of points in the delivery system:– Operations and

support– Implementation– Development

• While exact savings expectations need to be confirmed, some estimates anticipate 15-20% potential cost reduction

Customers are demanding new pricing models: SaaS model economics are attractive

Reduction in costs of implementation due to modular platform approach

Reduction in operations due to • Centralization of

support operations• Optimized

server/software maintenance costs

Reduction in software / development costs due to functionality

Attractiveness of SaaS model

114 148 185 204

79 100 134

4. Productivity creates leadership

Wal-MartIndexed to 1995 = 100

1987 1995 2002*2000

Productivity levelsWal-Mart

Remainder of industry

241286

346

110 100 97DellIndexed to 1998 = 100

Dell

Remainder of industry118%118% 186%186%

255%255%

1995-96 1998-99 2002-03

147

304 312

100 135 175MicrosoftIndexed to 1994 = 100

Microsoft

Top 2-99

1994 1999 2004

47%47%125%125% 78%78%

44%44%48%48% 38%38%

24

35

55 53 51 49

29

1319

10 82 5 5 3 1 0

5 3 37

0.00 -0.05

0.05 -0.10

0.10 -0.15

0.15 -0.20

0.20 -0.25

0.25 -0.30

0.30 -0.35

0.35 -0.40

0.40 -0.45

0.45 -0.50

0.50 -0.55

0.55 -0.60

0.60 -0.65

0.65 -0.70

0.70 -0.75

0.75 -0.80

0.80 -0.85

0.85 -0.90

0.90 -0.95

0.95 -1.00

> 1.0

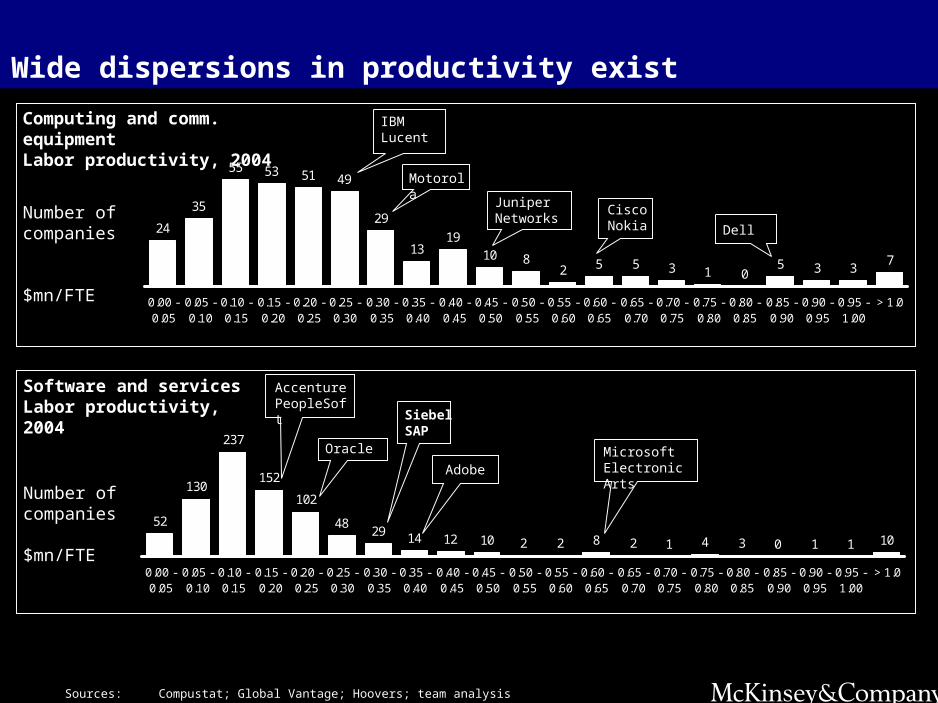

Wide dispersions in productivity exist

Sources:Compustat; Global Vantage; Hoovers; team analysis

Computing and comm. equipmentLabor productivity, 2004

Dell

CiscoNokia

Motorola

IBMLucent

Number of companies

$mn/FTE

Juniper Networks

52

130152

102

4829 14 12 10 2 2 8 2 1 4 3 0 1 1 10

237

0.00 -0.05

0.05 -0.10

0.10 -0.15

0.15 -0.20

0.20 -0.25

0.25 -0.30

0.30 -0.35

0.35 -0.40

0.40 -0.45

0.45 -0.50

0.50 -0.55

0.55 -0.60

0.60 -0.65

0.65 -0.70

0.70 -0.75

0.75 -0.80

0.80 -0.85

0.85 -0.90

0.90 -0.95

0.95 -1.00

> 1.0

Software and servicesLabor productivity, 2004

MicrosoftElectronic ArtsAdobe

Oracle

SiebelSAP

AccenturePeopleSoft

Number of companies

$mn/FTE

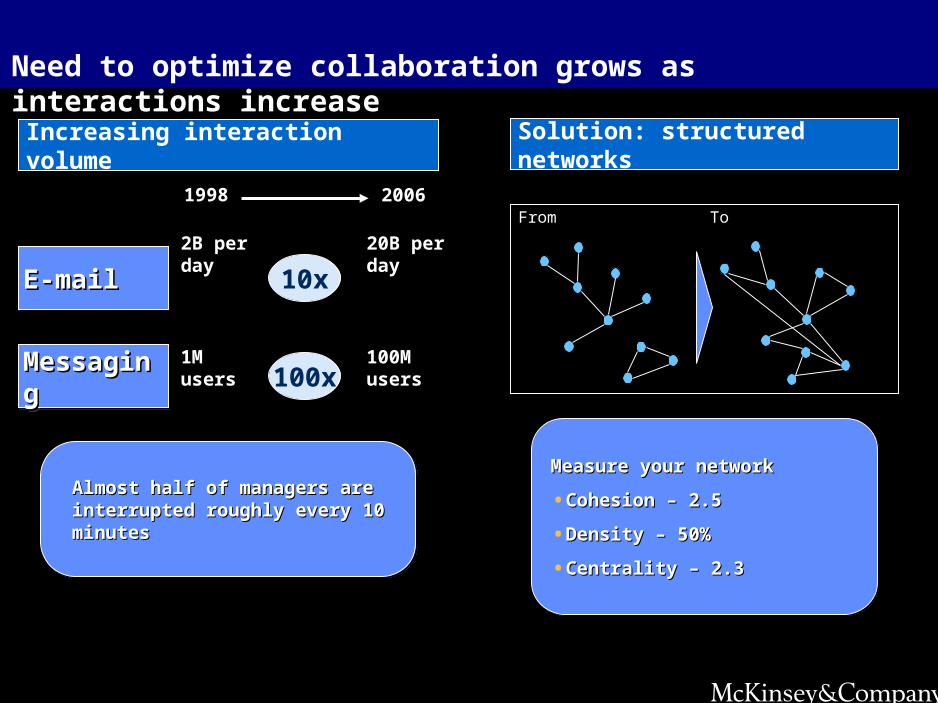

1998 2006

E-mailE-mailE-mailE-mail

2B per day

20B per day

10x

MessagingMessagingMessagingMessaging1M users

100M users100x

Increasing interaction volume

Almost half of managers are Almost half of managers are interrupted roughly every 10 minutesinterrupted roughly every 10 minutesAlmost half of managers are Almost half of managers are interrupted roughly every 10 minutesinterrupted roughly every 10 minutes

Need to optimize collaboration grows as interactions increase

Solution: structured networks

From To

Measure your networkMeasure your network

• Cohesion – 2.5Cohesion – 2.5

• Density – 50%Density – 50%

• Centrality – 2.3Centrality – 2.3

Measure your networkMeasure your network

• Cohesion – 2.5Cohesion – 2.5

• Density – 50%Density – 50%

• Centrality – 2.3Centrality – 2.3

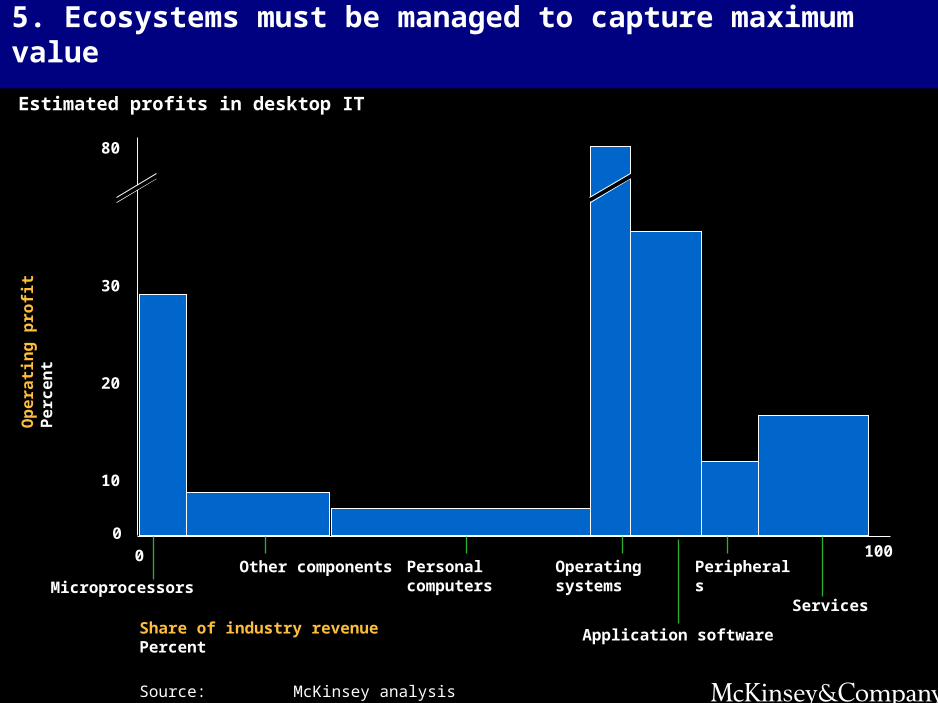

5. Ecosystems must be managed to capture maximum value

Estimated profits in desktop IT

Source: McKinsey analysis

Share of industry revenuePercent

80

0

0 100

30

20

10

MicroprocessorsOther components Personal

computersOperating systems

Application software

Peripherals

Services

Op

era

tin

g p

rofi

t P

erc

en

t

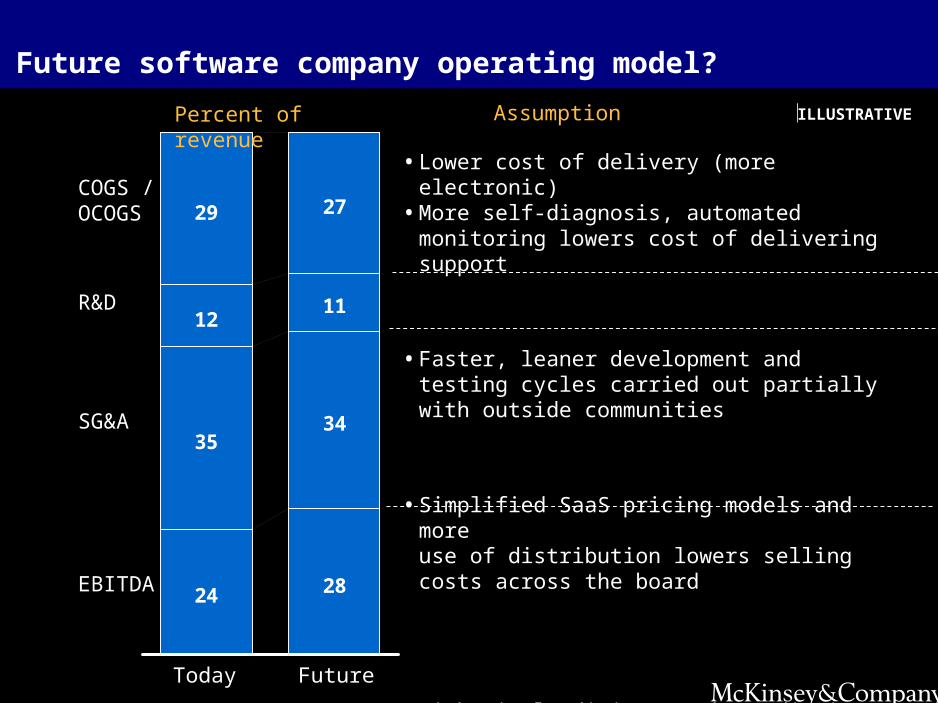

Future software company operating model?

24 28

3534

1211

29 27

SG&A

Today Future

Percent of revenue

COGS /OCOGS

R&D

EBITDA

• Lower cost of delivery (more electronic)• More self-diagnosis, automated monitoring lowers

cost of delivering support

• Faster, leaner development and testing cycles carried out partially with outside communities

• Simplified SaaS pricing models and more use of distribution lowers selling costs across the board

• High single digit growth predictions come true• Price pressure remains limited in enterprise

segments

Assumption ILLUSTRATIVE

Contact Information

Gareth MorganHigh Tech and Telecom Engagement Manager, McKinsey DublinDirect 01- 405 [email protected]