Todd Hale SVP, Consumer & Shopper Insights August 5, 2014 STATE OF THE INDUSTRY.

62

Todd Hale SVP, Consumer & Shopper Insights August 5, 2014 STATE OF THE INDUSTRY

-

Upload

shyann-keatts -

Category

Documents

-

view

213 -

download

0

Transcript of Todd Hale SVP, Consumer & Shopper Insights August 5, 2014 STATE OF THE INDUSTRY.

Todd HaleSVP, Consumer & Shopper InsightsAugust 5, 2014

STATE OF THE INDUSTRY

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

2

TABLE OF CONTENTS

• Retail Landscape & Performance• What’s Selling• Retail Hot Buttons• Closing Thoughts

22

RETAIL LANDSCAPE & PERFORMANCE

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

4

IS FLAT THE BEST WE CAN EXPECT?

Source: Nielsen Strategic Planner; Total U.S. All Outlets Combined (plus Convenience), All Departments, All Brands (UPC), % Change, 52 week periods vs. year ago

2009 2010 2011 2012 2013 52 w/e 06/07/2014

$698,622,107,361

$713,847,575,906

$740,149,846,801

$759,794,372,855

$771,160,987,149

$776,894,706,455

244,590,449,475

248,138,265,939

250,002,998,385

249,980,015,395

250,912,427,784

251,476,953,652

Dollar Sales Unit Volume

Billi

ons

All Departments

Dollar Trend +2 +4 +3 +1 +1

Unit Trend +1 +1 -0 +0 +0

Average U Price Trend +1 +3 +3 +1 +1

Any Promo U Trend +2 -0 -2 +0 +1

Shouldn’t an economic recovery be delivering more growth?

5Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

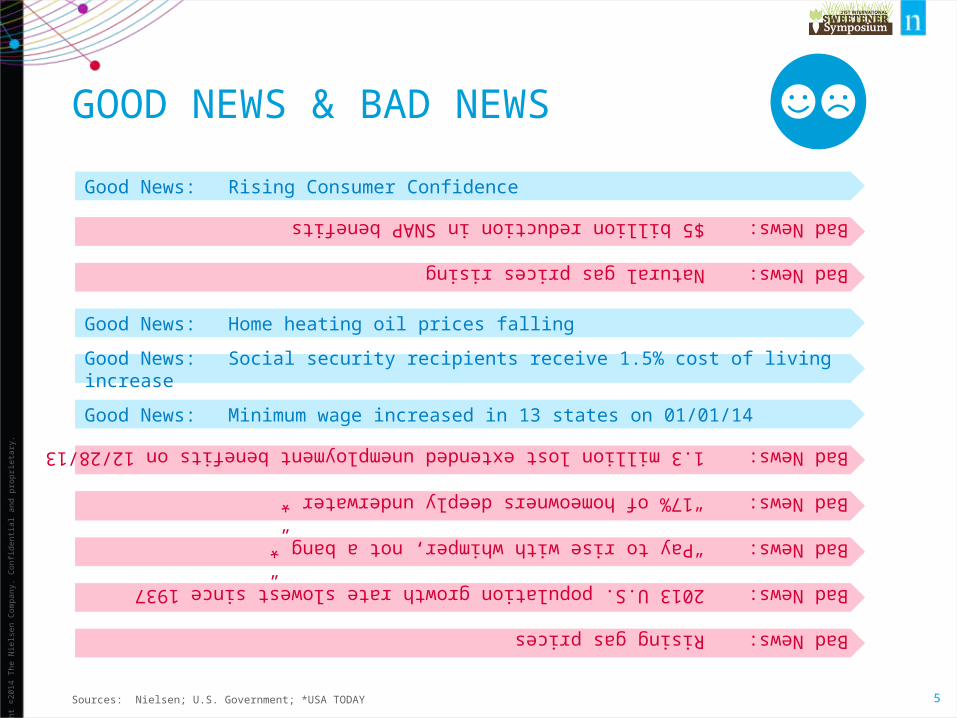

Good News: Rising Consumer Confidence

Bad News: $5 billion reduction in SNAP benefits

GOOD NEWS & BAD NEWS

Sources: Nielsen; U.S. Government; *USA TODAY

Bad News: Natural gas prices rising

Good News: Home heating oil prices falling

Good News: Social security recipients receive 1.5% cost of living increase

Good News: Minimum wage increased in 13 states on 01/01/14

Bad News: “17% of homeowners deeply underwater”*

Bad News: “Pay to rise with whimper, not a bang”*

Bad News: 2013 U.S. population growth rate slowest since 1937

Bad News: Rising gas prices

Bad News: 1.3 million lost extended unemployment benefits on 12/28/13

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

6

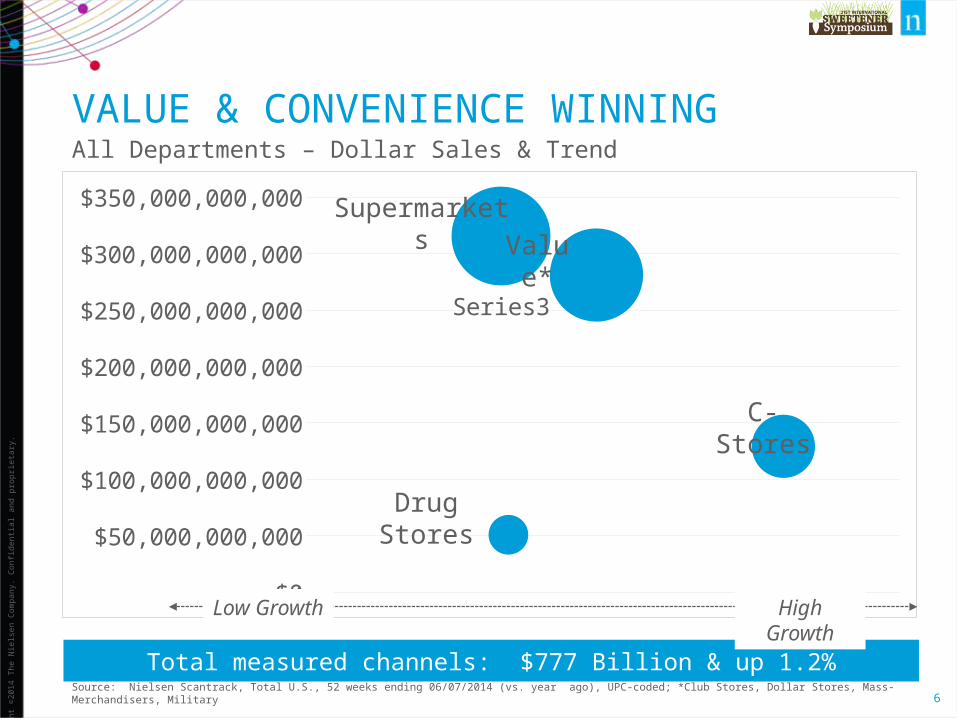

VALUE & CONVENIENCE WINNING

Source: Nielsen Scantrack, Total U.S., 52 weeks ending 06/07/2014 (vs. year ago), UPC-coded; *Club Stores, Dollar Stores, Mass-Merchandisers, Military

$0

$50,000,000,000

$100,000,000,000

$150,000,000,000

$200,000,000,000

$250,000,000,000

$300,000,000,000

$350,000,000,000

Series3

Total measured channels: $777 Billion & up 1.2%

All Departments – Dollar Sales & Trend

Supermarkets

C-Stores

Drug Stores

Value*

Low Growth High Growth

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

7

VALUE & CONVENIENCE DRIVE STORE EXPANSION

Source: Nielsen TDLinx

Convenience

Drug

Supermarkets $2MM+

Dollar Stores

Mass Merch

Supercenters

Warehouse Clubs

151,282

41,378

33,445

25,486

4,071

4,014

1,2862013

Expansion from all formats but Mass Merchandisers in 2013 vs. previous year

U.S. Store Counts

69% + of growth from niche formats

Value & Convenience

vs. 2005

RETAIL 2018 – WHAT’S IN STORE?

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

9

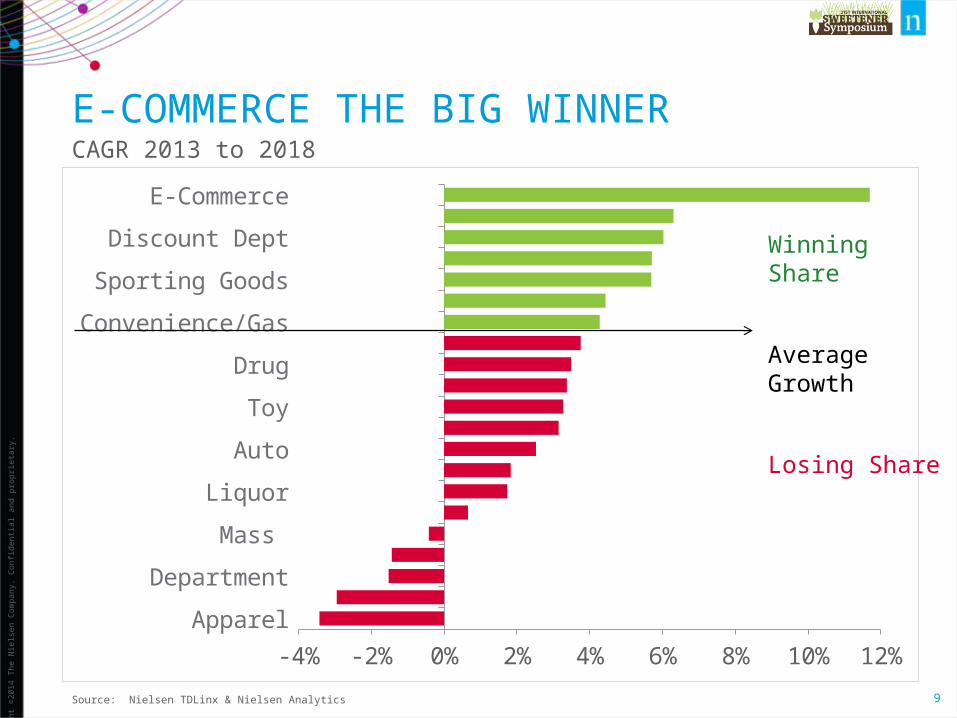

Apparel

Department

Mass

Liquor

Auto

Toy

Drug

Convenience/Gas

Sporting Goods

Discount Dept

E-Commerce

-4% -2% 0% 2% 4% 6% 8% 10% 12%

E-COMMERCE THE BIG WINNERCAGR 2013 to 2018

Source: Nielsen TDLinx & Nielsen Analytics

Winning Share

Average Growth

Losing Share

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

10

0

20,000

40,000

60,000

-10010203040

Retail E-Commerce Sales% of Total Retail SalesRetail E-Commerce Sales % Change vs. Year Ago

Percent

E-COMMERCE COMING TO CPG, BUT @ WHAT SPEED

Source: U.S. Census Bureau; company reports & websites

E-Commerce steadily growing sales

Amazon

$13.4

Walmart

$7.5

Kroger

$1.6

Amazon sales growth very impressiveGlobal annual sales growth versus prior year (in billions)

Step on the gas! Who can get there faster?AmazonFresh expanded from Seattle to Los Angeles & San Francisco

WHAT’S SELLING?

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

12

DEMAND SHIFTS BEHIND WINNERS & LOSERS

Source: Nielsen Strategic Planner, Total U.S. – All Outlets Combined (plus Convenience, 52 weeks ending 06/07/2014 (vs. 4-years ago), UPC-coded, 120 major category groupings

-$3,000,000,000

-$2,000,000,000

-$1,000,000,000

$0

$1,000,000,000

$2,000,000,000

$3,000,000,000

$4,000,000,000

$5,000,000,000

$6,000,000,000

Sugar & Sugar Substitutes off $64.2 million in annual sales

Overall gains were $72 billion versus four years ago; 23 categories with decreases; 97 categories with increases

Absolute Dollar Loss/Gain versus four years ago

Top 10 with decreases vs. 4-years ago

1. Computer/Electronic Prods 2. Magazines Selected Title 3. Film & Cameras 4. Gum 5. Cereal 6. Detergents 7. Disposable Diapers8. Office/School Supplies 9. Vegetables-Canned10. Puddings/Desserts-Dairy

Top 10 with increases vs. 4-years ago

1. Snacks2. Fresh Produce3. Candy4. Coffee5. Vitamins6. Packaged Meat7. Beer8. Tobacco & Accessories9. Cheese10. Wine

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

13

INFLATION & DEMAND DRIVING GROWTH

Source: Nielsen Strategic Planner, Total U.S. – All Outlets Combined (plus Convenience), 52 weeks ending 06/07/2014 (vs. year ago), UPC-coded

Fresh MeatFresh Produce

Packaged MeatAlcoholic Bevs

DeliDairyHBA

Dry GroceryNon-Food Grocery

Frozen FoodsGeneral MerchTotal All Depts

156

44

32

11

00

-41

All Outlets Combined (plus Convenience) – Dollar Trend

Center Store departments struggle

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

14

CONSUMERS SHIFTING SPEND OR BUYING LESS

Source: Nielsen Strategic Planner, Total U.S. – All Outlets Combined (plus Convenience), 52 weeks ending 06/07/2014 (vs. year ago), UPC-coded

Fresh MeatFresh ProduceAlcoholic Bevs

DeliDry Grocery

Packaged MeatDairy

Non-Food GroceryHBA

Frozen FoodsGeneral MerchTotal All Depts

114

31

10

-1-1-1

-1-3

0

All Outlets Combined (plus Convenience) – Unit Trend

Shouldn’t an economic recovery be delivering more unit growth?

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

15

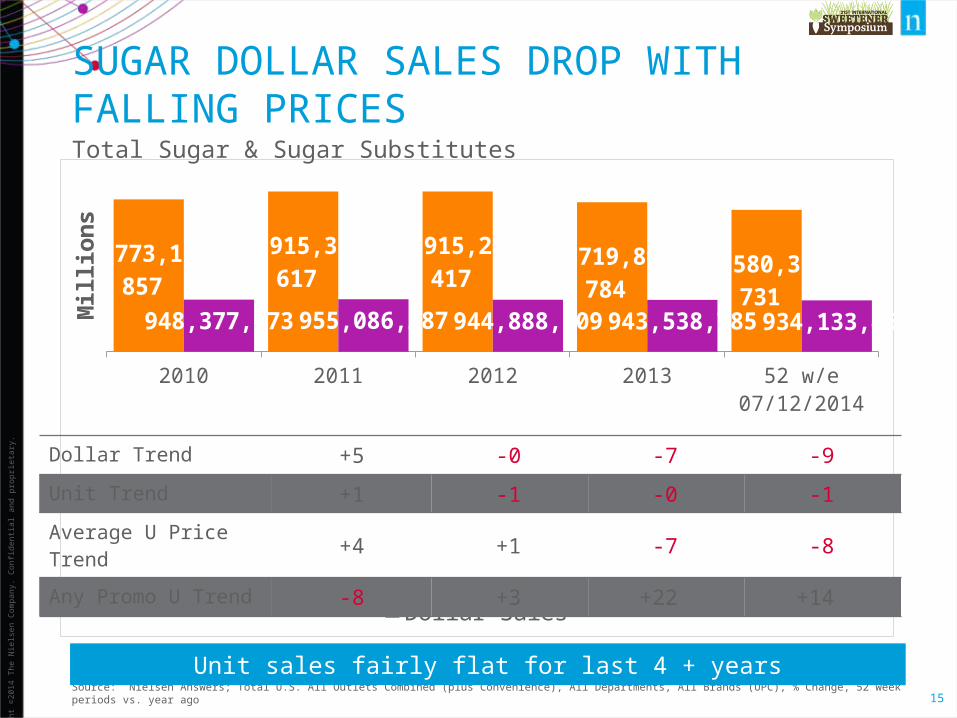

SUGAR DOLLAR SALES DROP WITH FALLING PRICES

Source: Nielsen Answers; Total U.S. All Outlets Combined (plus Convenience), All Departments, All Brands (UPC), % Change, 52 week periods vs. year ago

2010 2011 2012 2013 52 w/e 07/12/2014

$2,773,110,857 $2,915,333,617 $2,915,202,417 $2,719,807,784 $2,580,392,731

948,377,873 955,086,287 944,888,709 943,538,785 934,133,469

Dollar Sales Unit Volume

Mill

ions

Total Sugar & Sugar Substitutes

Dollar Trend +5 -0 -7 -9

Unit Trend +1 -1 -0 -1

Average U Price Trend +4 +1 -7 -8

Any Promo U Trend -8 +3 +22 +14

Unit sales fairly flat for last 4 + years

16Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

KEY SUGAR INGREDIENT CATEGORIES GENERATE A LOT OF RETAIL REVENUEDollar sales (billions) in Sugar categories

* Includes HFCS sweetened & sugar sweetenedSource: Nielsen Strategic Planner; Total U.S. All Outlets Combined (plus Convenience), All Brands (UPC), 52 weeks ending 7/5/2014

Sugar/Sugar Substitutes

Ice Cream & Frozen Novelties

Candy, exluding Dietetic

Juices/Drinks-SS/Ref/Frz

Carbonated Beverages, Regular*

Baked Goods/Cookies/Baking Mixes

$2,584,854,548

$9,957,907,140

$20,257,789,869

$21,242,047,703

$23,323,526,607

$33,783,352,165 + 2

% Change YAGO

- 9

+ 2

- 1

+ 3

NC

Sales up or flat in these categories

17Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

RETAIL HOT BUTTONS

Price & Value

Winning with Non-Edibles

Food Fight

Health & Wellness

Private Brands

Connecting with Shoppers That Matter

Sustainability

Right-Sized Box

Digital Shopping

Experiential Retailing

FOOD FIGHT

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

19

CONSUMERS FLOCK TO FRESH

Source: Nielsen Perishables Group FreshFacts , Total U.S. – Fresh Coverage Area (grocery + WM, Sam’s Club and Target); 52 weeks ending 5/31/2014 (vs. year ago)

Deli Pre-

pared Foods

Vegetables Fresh Seafood

Fruits Fresh Meat Deli Cheese Bakery Deli Meat-4%

-2%

0%

2%

4%

6%

8%

10%

Dollar Trend Volume Trend Price Change

Dollar growth for all & volume gains in most; higher prices part of the mix too

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

20

DELI PREPARED FOODS GROWING

Sources: *Nielsen Perishables Group FreshFacts , Total U.S. – Fresh Coverage Area (grocery + WM, Sam’s Club and Target); 52 weeks ending 5/31/2014 (vs. year ago); **Nielsen Scantrack, Total U.S. – All Outlets Combined, plus Convenience, 52 weeks ending 6/7/2014 (vs. year ago), UPC only; ***NPD Group

Deli SoupsPizza

Deli DessertsDeli Appetizers

Deli EntreesDeli Salads

Deli Breakfast FoodsDeli Platters

Deli SandwichesSushi

Deli Prepared ChickenDeli Snacks

Deli SidesDeli Dips/ Spreads/ Toppings

1%2%3%3%3%3%3%3%

4%6%

9%9%

14%17%

Volume Trend*

Growth continues as shoppers choose meals & meal components over ingredients

Total Store ** Unit Growth:

+0.2%

Prepared food purchases from supermarkets, drug stores & other retail outlets willGROW 10% BY 2022***

21Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

BAKERY DEPARTMENT CAPTURING GROWTH IN CATEGORIES WHERE SUGAR IS KEY INGREDIENTGrowth continues as shoppers choose meals & meal components over ingredients

Sources: *Nielsen Perishables Group FreshFacts , Total U.S. – Fresh Coverage Area (grocery + WM, Sam’s Club and Target); 52 weeks ending 5/31/2014 (vs. year ago); **Nielsen Scantrack, Total U.S. – All Outlets Combined, plus Convenience, 52 weeks ending 6/7/2014 (vs. year ago), UPC only; ***NPD Group

Brownies & Dessert BarsCinnamon & Sweet Rolls

MuffinsPies

BagelsSweet Goods

CookiesCakes

DonutsBreads

Rolls

1%1%

5%5%

6%7%

8%12%

15%19%

20%

Volume Trend*

Total Store ** Unit Growth:

+0.2%

22Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

• Daily dinner deals• “Grab & Go” foods• New garden cooler,

which keeps fruits and vegetables fresher, longer

• Expanded gluten-free section• $1 Deals• New Food Lion-brand beef in

sealed-fresh packaging

FOOD LION DEBUTS NEW STORE FORMAT

Sources: Food Lion, Supermarket News & Salisbury Post (photos)

23Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

SEE HOW YOUR TARGET'S BEEN REFRESHED1,261 Target stores w/expanded food

Source: Target

24Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

INTEGRATED CAMPAIGN TO REVIVE ESTABLISHED CATEGORIES

Source: Cans Get You Cooking

“Cans get you cooking, a multi-year, fully-integrated campaign”

25Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

Source: http://cargocollective.com/samcrews/Coke-Walmart-Goes-Well-With

“new displays, menu boards & signage in 3000+ Walmart’s gave Coke a level of branding never seen before”

FISH WHERE THE FISH ARE!Secondary location with multi-media support

26Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

Source: http://vmsd.com/content/mega-foods-eau-claire-wis; Photography: Mark A. Steele Photography, Columbus, Ohio; Note: capex = capital expenditures

SHAKING UP THE AISLEIs it time to convert trade spend to capex spend?

27Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

LONG-TERM FOOD-AWAY-FROM-HOME SHARE AT HIGHEST POINT EVERShare of total U.S. food expenditures:

Source: Calculated by the Economic Research Service, USDA, from various data sets from the U.S. Census Bureau and the Bureau of Labor Statistics.

19901992

19941996

19982000

20022004

20062008

20102012

42%

44%

46%

48%

50%

52%

54%

56%

58%

Food-at-home Food-away-from-home

Food expenditures based on actual sales

50.5%

49.5%

28Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

PERFORMANCE INDEX ABOVE 100 FOR THE 15TH CONSECUTIVE MONTH; HIGHEST IN OVER 2 YEARS

Source: http://www.restaurant.org//Downloads/PDFs/News-Research/index/RPIMay2014

PRIVATE BRANDS

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

30

Dollar Sales Trend

Private Brand +5% +8% +2% +2% +2%

Branded +1% +3% +2% +1% +1%

JUST OUTPACING BRAND GROWTH SINCE 2012

Source: Nielsen Strategic Planner, Total U.S. – All Outlets Combined (xAOC), Total All Departments, UPC-coded

2009 2010 2011 2012 2013 52 w/e 6/7/14

16.2%

16.7%

17.3% 17.3%17.5% 17.5%

Private Brand $ Share

All Departments

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

31

WHERE ARE THE GROWTH OPPORTUNITIES?

Source: Nielsen Strategic Planner, Total U.S. – All Outlets Combined (xAOC), 52 weeks ending 06/07/2014 (vs. year ago), UPC-coded, 116 major category groupings

0%

10%

20%

30%

40%

50%

60%

Are they bigger in low or high share categories? What other considerations?

Private Brands: Dollar Share

EdiblesNon-Edibles

Top 10

1. Milk 2. Eggs-Fresh 3. Sugar/Sugar Substitutes 4. Wrapping Materials Bags5. Dessert/Fruit/Tops-Froz6. Unprep Meat/Seafood-Frz7. Fruit-Canned8. Pain Remedies9. Cheese10. First Aid17.5%

Average $ Share

Bottom 10

1. Computer/Electronic Prods 2. Beer3. Deodorant 4. Tobacco & Accessories5. Gum6. Canning/Freezing Supplies7. Wine8. Liquor 9. Hair Care10. Insecticides Repellants

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

32

SUPERMARKETS DOMINATE BEST OF BREED

Source: Nielsen Homescan, 52 weeks ending 12/28/2013, UPC-coded items

Stater Bros

Safeway-Corp

Dollar General

Hannaford

Costco

Kroger Grocery-Corp

H-E-B

Wegmans

Save-A-Lot

Aldi

0% 10% 20% 30% 40% 50% 60% 70% 80% 90%

Limited assortment/extreme discount formats lead the way

Store Brands $ Share of Total Store

SupermarketsClubMass w/SupersDollarDrug

Average24%20%18%18%18%

33Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

“PRIVATE-LABEL FOODS OFTEN MEET OR BEAT THE BIG BRANDS”

Source: NBC News & Consumer Reports

Consumer ReportsAugust 2013

Our expert tasters judged 33 of 57 store-brand foods as good as or better than the national brand.In categories such as ice cream, trail mix, mozzarella, mixed vegetables, and more, we found at least one store brand from the national grocers Costco, Kmart, Sam's Club, Target, Trader Joe's, Walmart, and Whole Foods that was equal in quality to the big name.

34Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

KROGER SIMPLE TRUTH EXPECTED TO HIT $1 BILLION; H-E-B INTRODUCES AFFORDABLE ORGANIC OPTIONS

Source: Todd Hale (in-store photo); Kroger, http://www.simpletruth.com/; H-E-B

• Beef• Teas• Salads• Carrots• Café Ole• Oatmeal & Cereals

H-E-B- shelf tag

Kroger’s eye catching in-store merchandising; its own website & array of social media

35Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

WALMART & WILD OATS TO DRIVE DOWN ORGANIC FOOD PRICES

Source: Walmart

Nearly 100 organic products – no price premium

36Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

BACK TO THE FUTURE

Source: Facebook (Walmart-Lebanon); My Private Brand

Walmart testing Extreme Value Brand

37Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

FRESHDIRECT LAUNCHED TWO PRIVATE BRANDS

Source: mypbrand.com

Mypbrands.comDec. 2, 2013

Cloud 9 is about high quality, effective products in the household and cleaning categories that our customers can count on to get the job right.

JUST FreshDirect will include food products with a focus on simple, short ingredient statements, wholesome ingredients and transparency when it comes to what’s in each product. One of the key elements to our JUST FreshDirect brand is that we have a list of prohibited ingredients.

We have plans to launch over 150 new private brand products in 2014… We also have more brands in the works so expect more exciting news over the next year.

CONNECTING WITH SHOPPERS THAT MATTER

39Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

ALL GROUPS HAVE LOST SINCE 2000But Blacks & Hispanics have suffered the most

Source: USA TODAY (story by Tim Mullaney; graphics by Frank Pampa & Anne R. Carey – 9/18/2013))

% Change vs. 2000:Non-Hispanic White: -6.3%Asian: -7.7%Hispanic: -11.8%Black: -15.8%

40Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

DIVERSITY IN SUGAR BUYING & IN CATEGORIES WHERE SUGAR IS KEY INGREDIENT

Source: Nielsen Homescan, Total U.S. 52 weeks ending 12/28/2013, UPC-coded products; Note: Categories include sugar-free products

WHITE NON-HISPANIC

AFRICAN AMERICAN ASIAN HISPANIC

(any race)

CANDY 94 67 70 72

JAMS/JELLIES/ SPREADS 28 20 24 24

SUGAR/SUGAR SUBSTITUTES 22 25 16 22

BREAD & BAKED GOODS 116 90 87 109

CEREAL 73 63 65 80

COOKIES/ICE CREAM CONES 43 39 40 43

CARBONATED BEVERAGES 126 80 82 97

JUICES-DRINKS-SHELF STABLE 54 72 50 73

JUICES-DRINKS-REFRIGERATED 34 44 43 44

ICE CREAM 39 30 28 31

Annual $ Per Household Among Category Buyers

Watch Out: a number of categories with low buying rates among multicultural

41Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

BY 2020, MILLENNIALS WILL OUTNUMBER BOOMERS BY TEN MILLION U.S. Population Projections - 2020

Source: U.S. Census Bureau (2012 National Population Projections)

Population (millions)

01,000,0002,000,0003,000,000

Males(165 million)

06

121824303642485460667278849096

0 1,000,000 2,000,000 3,000,000

Females(169 million)

Millennials

Gen X

Boomers37 million

25 million

40 million

34 million

24 million

41 million

Age

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

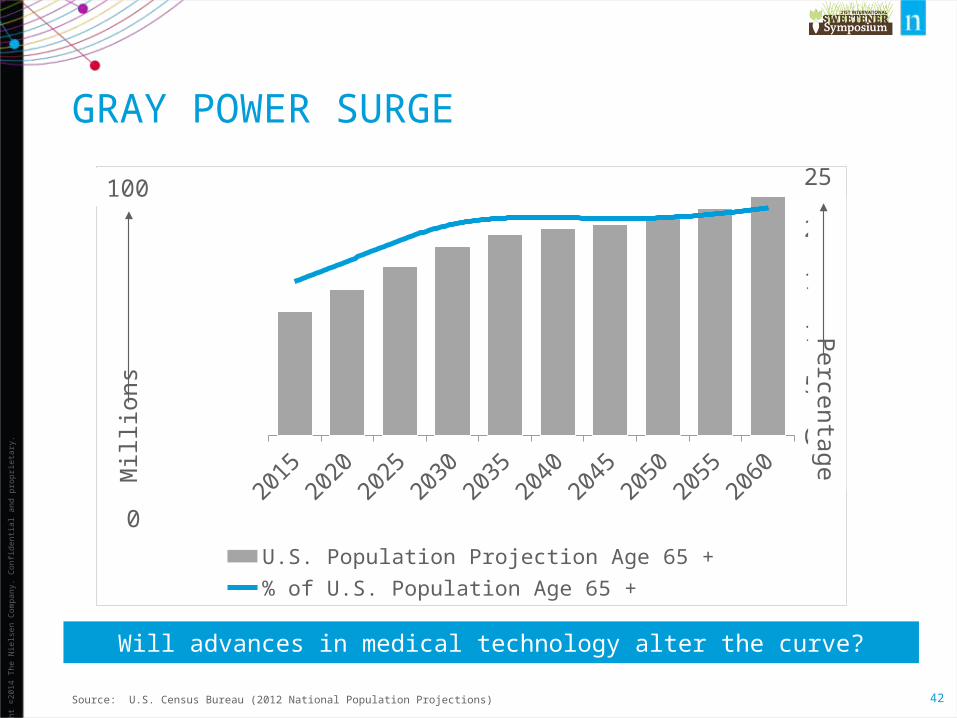

42

GRAY POWER SURGE

Source: U.S. Census Bureau (2012 National Population Projections)

2015 2020 2025 2030 2035 2040 2045 2050 2055 20600

10,000,00020,000,00030,000,00040,000,00050,000,00060,000,00070,000,00080,000,00090,000,000

100,000,000

0

5

10

15

20

25

U.S. Population Projection Age 65 + % of U.S. Population Age 65 +

Will advances in medical technology alter the curve?

Percentage M

illio

ns

100

0

Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

43

OLDER MORE TRIPS; YOUNGER BIGGER BASKETS

Source: Nielsen Homescan, Total U.S. 52 weeks ending 12/28/2013, excludes gas only or Rx only trips; *UPC-coded products

Total Retail Channels

Greatest Gen

Boomers

Gen X

Millennials

164

153

129

104

Shopping Trips per Household

Millennials more deal prone

Greatest Gen

Boomers

Gen X

Millennials

$37

$46

$54

$54

Basket Ring $ per Trip

Greatest Gen

Boomers

Gen X

Millennials

$6,110

$7,086

$7,007

$5,655

Basket Ring $ Per Household

Greatest Gen

Boomers

Gen X

Millennials

27%

25%

26%

29%

% Dollars on Deal*

44Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

MILLENNIALS LESS ENGAGED IN SUGAR & IN KEY SUGAR INGREDIENT CATEGORIES

Source: Nielsen Homescan, Total U.S. 52 weeks ending 12/28/2013, UPC-coded products; Note: Categories include sugar-free products

GREATEST GENERATION BOOMERS GENERATION X MILLENNIALS

CANDY 85 97 89 69

JAMS/JELLIES/ SPREADS 26 26 27 25

SUGAR/SUGAR SUBSTITUTES 23 24 22 18

BREAD & BAKED GOODS 112 118 117 93

CEREAL 61 67 84 81

COOKIES/ICE CREAM CONES 44 44 43 37

CARBONATED BEVERAGES 91 125 123 101

JUICES-DRINKS-SHELF STABLE 47 55 69 62

JUICES-DRINKS-REFRIGERATED 38 38 38 34

ICE CREAM 42 40 35 27

Annual $ Per Household Among Category Buyers

45Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

TARGET TRIES TO WIN HEARTS & CLICKS OF MILLENNIALS & COLLEGE STUDENTSReplacing in-store registry kiosks with iPads; replacing scanning guns with the iPod Touch

Source: Target

Target overhauling their wedding & baby registry business, integrated shopping lists with live store maps, and testing same-day delivery for some online orders; and

introduces first ever college registry

46Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

HEALTH & BEAUTY CARE SENIOR FOCUS

Sources: MultiAd Kwikee & company websites

47Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

SMALLER PORTION SIZES, BUT WHAT ELSE?

Source: MultiAd Kwikee

48Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

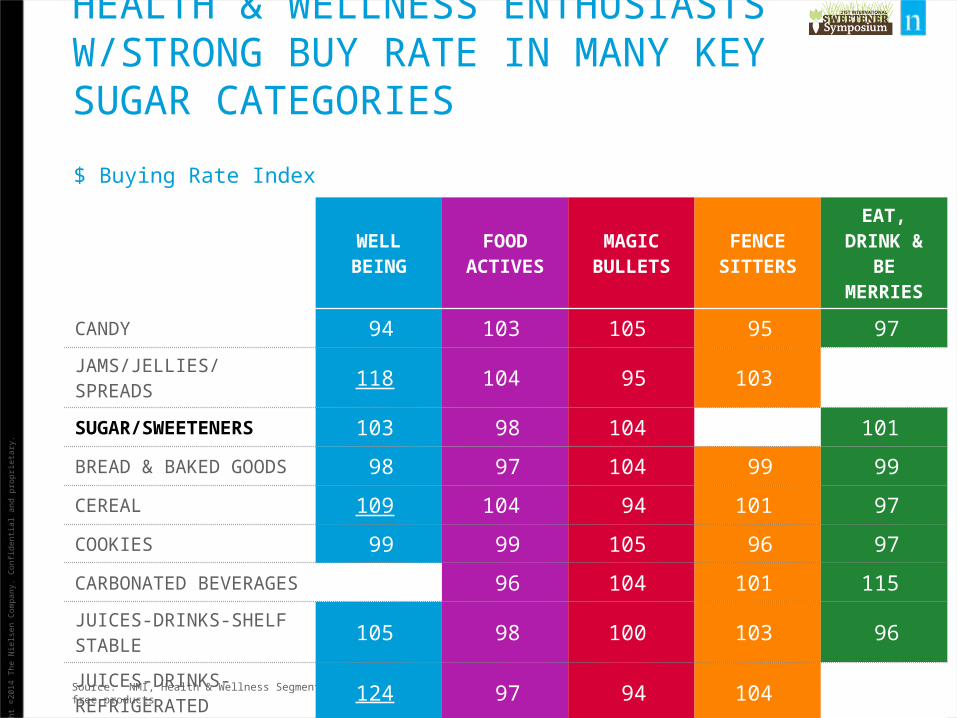

HEALTH & WELLNESS ENTHUSIASTS W/STRONG BUY RATE IN MANY KEY SUGAR CATEGORIES

Source: NMI, Health & Wellness Segmentation, Total U.S. – 52 weeks ending 12/28/2013, UPC-coded; Note: Categories include sugar-free products

WELL BEING FOOD ACTIVES

MAGIC BULLETS

FENCE SITTERS

EAT, DRINK & BE MERRIES

CANDY 94 103 105 95 97

JAMS/JELLIES/ SPREADS 118 104 95 103 87

SUGAR/SWEETENERS 103 98 104 89 101

BREAD & BAKED GOODS 98 97 104 99 99

CEREAL 109 104 94 101 97

COOKIES 99 99 105 96 97

CARBONATED BEVERAGES 76 96 104 101 115

JUICES-DRINKS-SHELF STABLE 105 98 100 103 96

JUICES-DRINKS-REFRIGERATED 124 97 94 104 88

ICE CREAM 103 103 103 88 96

$ Buying Rate Index

DIGITAL SHOPPING

50Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

AMAZON GETS IT

Sources: https://www.amazon.com/gp/subscribe-and-save/details/index.htmlhttp://www.amazon.com/gp/browse.html/?node=5856180011https://fresh.amazon.com/dash

AMAZON GOING AFTER REGULARLY SCHEDULED BUYS

COMPETITION HEATS UP W/AMAZON PRIME PANTRY

“THE NEW WAY TO SHOP FROM HOME”

51Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

“TARGET EXPANDS SUBSCRIPTION SERVICE TENFOLD”

Source: Target

nearly 1,600 items… Everything from beauty products and pet supplies to home office supplies, are now available for regular delivery… free subscription program allows people to schedule shipments in four, six, eight, 10 and 12-week installments.

Associated PressApr. 17, 2014

52Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

ONLINE GROCERY SALES TO DOUBLE IN FIVE KEY EUROPEAN MARKETS BY 2016

Source: Reuters

Britain, France, Germany, Switzerland and the Netherlands

Joanne Denney-Finch, chief executive, IGDReuters (Berlin), Oct. 23, 2013

Online retailing in food and consumer goods is growing at a phenomenal rate across Europe. Technology is empowering people, fundamentally changing the way they buy groceries

53Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

HIGH INTEREST IN CLICK & COLLECT

Source: Nielsen Global Consumer Confidence Survey About Aging, Q3 2013 (fielded 8/14/2013 – 9/6/2013)

GLOBAL AVERAGE NORTH AMERICA

Order online for home delivery

37%54%

20%64%

Order online pick-up inside of store

17%65%

17%68%

Order online pick-up via drive-thru

16%66%

12%68%

Order online pick-up curbside

13%64%

11%69%

ALREADY USING DEFINITELY/SOMEWHAT WILLING

54Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

TRADITIONAL RETAILERS MAKING AN IMPACT ONLINE

“Ahold has a company-wide target to triple its online food sales by 2016”

Sources: Ahold; Peapod; Crain’s Chicago Business; Chicago Tribune; Harris Teeter

HARRIS TEETER DEBUTS ANNUAL SUBSCRIPTION$99.95 for the entire year, no limit to number of orders placed; curbside pick up

PEAPOD EXPANDS NUMBER OF PICK UP LOCATIONS

55Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

WALMART INVESTING IN DRIVE THROUGH GROCERY PICK UP

Sources: The City Wire & ASDA

“The 15,000 square-foot facility will house 10,000 fresh and dry grocery products – from cereal, chips and bread to fresh produce, meat and milk”

The as-yet unnamed and unbuilt internet pick-up outlet will carry some 10,000 SKUs and be staffed by logistics employees at Walmart. They will assemble orders made online and deliver to cars in as many as 30 drive-up lanes. The concept is based on a similar offering at Walmart’s United Kingdom banner, Asda, said Judith McKenna, chief development officer at Walmart and a former Asda exec.

The City WireMay 7, 2014

56Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

MERCHANDISING WIDE VARIETY OF CATEGORIES

Source: Company websites

Have you noticed Walgreens online ad includes more pages

than their print edition?

57Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

WALMART TEXTING RECEIPTS TO BRING LOYALTY CARD CAPABILITIES TO THEIR OFFERING

Source: Milwaukee Journal Sentinel & NFC World(photo)

Milwaukee Journal SentinelApr. 23, 2014

Walmart plans to analyze the large amounts of data it collects through e-receipts and use it as a marketing tool. It enables Walmart to track what its customers buy, where and when and send personalized email offers to shoppers who want it.A Walmart executive said the retailer could send coupons to customers for their favorite brands or shopping lists of items they may want to buy during their next visit. Customers will be identified through their phone number.

CLOSING THOUGHTS

CHASING THE CUSTOMER … NOT THE COMPETITION!

RONALD LUNDE

WHAT WOULD YOU DO IF YOU WEREN’T AFRAID?

SPENCER JOHNSON

62Copy

right

©20

14 T

he N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

STAY CONNECTED

http://www.nielsen.com

LinkedIn @[email protected]