Today’s Agenda

24

FORECLOSURE PREVENTION AND LOSS MITIGATION OVERVIEW FEBRUARY 24, 2011 FAITH-BASED AND NEIGHBORHOOD PARTNERS FORECLOSURE PREVENTION EDUCATION WORKSHOP 1

-

Upload

sylvester-kirk -

Category

Documents

-

view

37 -

download

0

description

FORECLOSURE PREVENTION AND LOSS MITIGATION OVERVIEW FEBRUARY 24, 2011 FAITH-BASED AND NEIGHBORHOOD PARTNERS FORECLOSURE PREVENTION EDUCATION WORKSHOP. Today’s Agenda. Reasons For Default. Foreclosure Prevention Tips. FHA’s Loss Mitigation Program. Strategic Foreclosures. Mortgage Scams. - PowerPoint PPT Presentation

Transcript of Today’s Agenda

FORECLOSURE PREVENTION AND LOSS MITIGATION

OVERVIEW

FEBRUARY 24, 2011FAITH-BASED AND NEIGHBORHOOD PARTNERS

FORECLOSURE PREVENTION EDUCATION WORKSHOP

1

Today’s Agenda

Reasons For

DefaultFHA’s Loss Mitigation Program

Strategic Foreclosures Mortgage Scams

Questions

Resources

Foreclosure Prevention Tips

2

3

The Crisis Continues

Reasons for DefaultPoor money managementOver extended obligationsLoss of incomeLack of concern or Understanding mortgage

obligationIllnessDivorce

4

Foreclosure Prevention Tips

Don’t ignore the problem/Open and respond to mail

Contact Lender and HCAsPrioritize spendingKnow Your Mortgage rightsUnderstand Foreclosure Prevention Options

5

FHA Loss Mitigation General Criteria

Borrower must be Owner OccupantLoan must not be delinquent more than 12

months (PITI)LM is mandatory on FHA loans that are

delinquentLM Options are in order of effectiveness

6

FHA’s Loss Mitigation Program

Home Retention Tools:

Special Forbearance AgreementLoan ModificationPartial ClaimFHA-HAMP

7

FHA’s Loss Mitigation Program

Home Disposition Tools:

Pre-Foreclosure Sale (Short Sale)Deed In Lieu

8

Special Forbearance Agreement: Written agreement between lender and

borrower which contains a plan to reinstate the loan

Three months delinquent but no more than 12 months

Minimum duration of four months – no maxLate fees not accessed

9

Home Retention Tools

Home Retention Tools

Loan Modification:

A permanent change in the terms of a Mortgagor’s loan.

Interest Rate shall be reduced.

Legal fees and related foreclosure costs may be capitalized.

Allows a loan to be reinstated

10

Partial Claim:FHA advances funds on behalf of a borrower in an amount necessary to reinstate a delinquentNot to exceed the equivalent of 12 months PITI.Promissory Note is executedMortgage is subordinated to HUDInterest rated shall be reduced Not due and payable until the borrower pays off

the 1st mortgage or no longer owns property

11

Home Retention Tools

FHA’s Home Affordable Modification Program: Designed to help homeowners retain property and prevent foreclosure:

Provides borrowers with reduced mortgage payment

Combines Loan Mod with Partial claimResults in a 30 year fixed rate mortgageImminent default or default mortgage

12

FHA-HAMP

Pre-Foreclosure Sale (Short sale): Allows a borrower in default to sell their home and use sale proceeds to satisfy mortgage debt.

At the time of sale, the property must be at least 31 days, but no more than 12 months

PFS is unavailable if a property has been abandoned or Mortgagor has ability to pay the debt.

The PFS must be an outright sale of the property.

13

Home Disposition Tools

Deed In Lieu (of foreclosure): Borrower voluntarily deeds collateral property toHUD in exchange for a release from all obligations under the mortgage

No walk aways/owner-occupant statusBorrower may receive up to $2,000 (Must be used to

help pay off liens if needed)Property must be left in good condition

14

Home Disposition Tools

Borrowers with mortgages appraised significantly lower than property value often just walk away from their principal residence

This occurs when negative equity in the home reaches a level whereby, the mortgage substantially exceeds the property value

FHA’s Buy and Bail Policy

15

Strategic Foreclosures

Mortgage Scams

Be cautious of companies making donations to the church or requesting church approvals

Work with HUD Approved Housing counseling agencies, or verify authenticity of Housing Counselors/agencies invited to church events

Borrower should never make payments to anyone but lender or lender approved entity

Be aware of fake “government” modification programs

16

Mortgage Scams

Common Scam TypesPhantom Help – The “rescuer” charges high

fees for work that the homeowner could do for themselves, or charges for strong representation that never materializes

Bailout – Includes various schemes where homeowners surrender their house title thinking that they will be able to remain as renters and buy the house back

17

Mortgage ScamsBait and Switch – Homeowners think they

are signing documents for a new loan making the mortgage current, but actually sign away rights to the home. They are left still holding the mortgage payments.

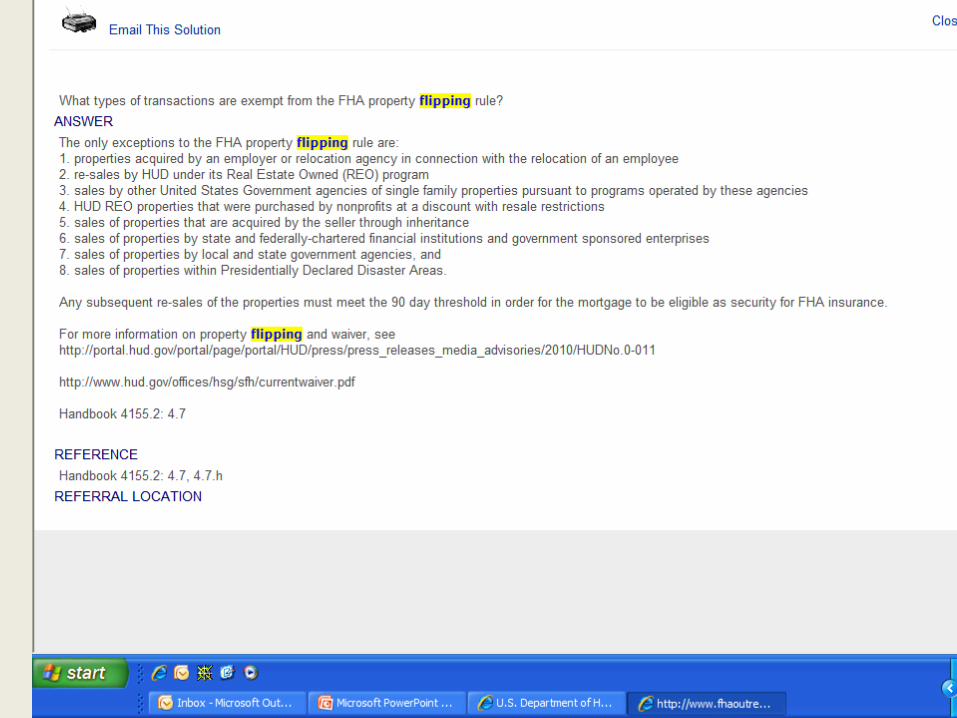

Equity Stripping – A buyer purchases the home for the amount of the arrearage and flips the home for a quick profit.

18

HUD/FHA Resourceswww.hud.gov

19

20

21

HUD/FHA Resources• Join HUD’s email list: http://www.hud.gov/offices/hsg/sfh/ref/hsgregst.cfm

Receive email notification of important industry announcements such as new mortgagee letters, handbooks, FHA mortgage limit increases, events and training opportunities.

• For borrowers facing foreclosure, struggling with their mortgages and/or trying to avoid foreclosure, visit www.MakingHomeAffordable.gov

• Join Free FHA Webinars: http://www.hud.gov/offices/hsg/sfh/events/events.cfmSign up and join other National FHA Mortgage industry partners

• HUD’s Office of Inspector General: http://www.hud.gov/offices/oig/hotline/Contact OIG to report fraud, waste, abuse, mismanagement or violations of law, rules or regulations by HUD employees or HUD program participants. Call: 1-800-347-3735

22

HUD/FHA Resources

• FHA Call Center 1-800 Call FHA 800-225-5342• Loss Mitigation – [email protected]• HECM (Reverse Mortgages) –

[email protected]• National Servicing Call Center – 1-877-622-

8525• HUD Approved Housing Counseling Agencies

www.hud.gov/offices/hsg/sfh/hcc/hcs.cfm

23