Tocqueville Gold Strategy Third Quarter 2016 Investor...

15

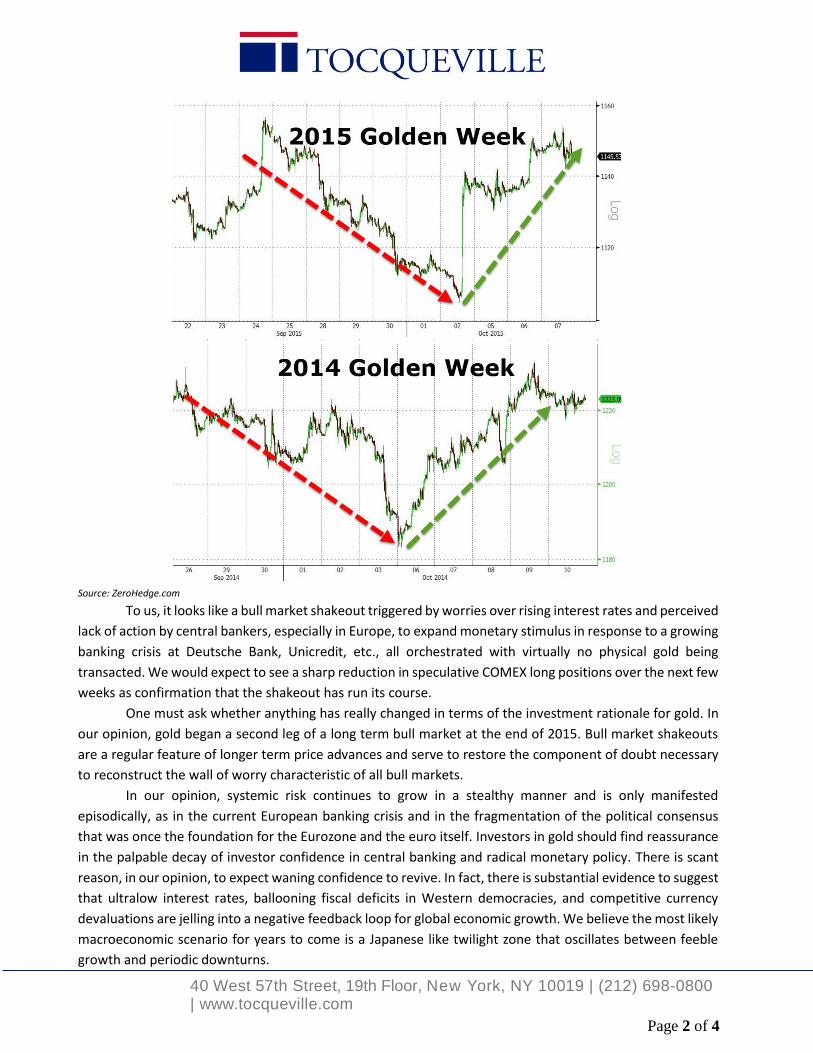

40 West 57th Street, 19th Floor, New York, NY 10019 | (212) 698-0800 | www.tocqueville.com Page 1 of 4 Tocqueville Gold Strategy Third Quarter 2016 Investor Letter During the third quarter of 2016, gold and gold mining shares consolidated in a narrow range following substantial gains in the first half of the year. On a year to date basis (9/30/16) gold bullion rose 24% while most gold mining shares gained 3x-4x the gold price. During the first few days of October, the gold price broke sharply lower beneath the consolidation range of the third quarter. The decline in gold accelerated after breaking through technical support zones clustered around $1300/oz. in only a few days. High frequency and short term momentum traders piled on as they typically do when technical support is breached. Intense short selling by these players accelerated the market decline. Bearishness has replaced the euphoria and overconfidence that dominated only a few months ago in early July. It must be remembered that these short term gyrations reflect synthetic or paper trading, which we have discussed frequently over the past two years, and is almost completely disconnected from flows of physical metal. Long term, we don’t think this washout signals a structural change in gold’s outlook; it may have been a clean-out of weak holders as prices recalibrate lower towards physical support from Asian buyers. The correction of the past few days coincided with an absence of Chinese buyers due to the “Golden Week” holiday there. “With China (by far the largest buyer of physical gold) closed, the markets were open for rampant manipulation, which is exactly what happened as several billion dollars in paper assets were dumped.” (Zero Hedge Oct. 9, 2016) As noted in the October 10 Belkin report, “who sells $22 billion of gold for maximum market impact over a very short period of time? The global monetary cabal (central banks, BIS) have a long history of suppressing gold prices because a rising gold price discredits their legitimacy. But never mind, gold is still up 18% year to date …even after last week’s intervention.” As the charts below show, this intervention was very similar to the previous two years. Paper losses inflicted by synthetic speculators during Golden Week were recouped in the subsequent trading sessions.

Transcript of Tocqueville Gold Strategy Third Quarter 2016 Investor...

40 West 57th Street, 19th Floor, New York, NY 10019 | (212) 698-0800 | www.tocqueville.com

Page 1 of 4

Tocqueville Gold Strategy

Third Quarter 2016 Investor Letter

During the third quarter of 2016, gold and gold mining shares consolidated in a narrow range

following substantial gains in the first half of the year. On a year to date basis (9/30/16) gold bullion rose 24%

while most gold mining shares gained 3x-4x the gold price.

During the first few days of October, the gold price broke sharply lower beneath the consolidation

range of the third quarter. The decline in gold accelerated after breaking through technical support zones

clustered around $1300/oz. in only a few days. High frequency and short term momentum traders piled on

as they typically do when technical support is breached. Intense short selling by these players accelerated

the market decline. Bearishness has replaced the euphoria and overconfidence that dominated only a few

months ago in early July. It must be remembered that these short term gyrations reflect synthetic or paper

trading, which we have discussed frequently over the past two years, and is almost completely disconnected

from flows of physical metal.

Long term, we don’t think this washout signals a structural change in gold’s outlook; it may have

been a clean-out of weak holders as prices recalibrate lower towards physical support from Asian buyers.

The correction of the past few days coincided with an absence of Chinese buyers due to the “Golden Week”

holiday there. “With China (by far the largest buyer of physical gold) closed, the markets were open for

rampant manipulation, which is exactly what happened as several billion dollars in paper assets were

dumped.” (Zero Hedge Oct. 9, 2016) As noted in the October 10 Belkin report, “who sells $22 billion of gold

for maximum market impact over a very short period of time? The global monetary cabal (central banks, BIS)

have a long history of suppressing gold prices because a rising gold price discredits their legitimacy. But never

mind, gold is still up 18% year to date …even after last week’s intervention.” As the charts below show, this

intervention was very similar to the previous two years. Paper losses inflicted by synthetic speculators during

Golden Week were recouped in the subsequent trading sessions.

40 West 57th Street, 19th Floor, New York, NY 10019 | (212) 698-0800 | www.tocqueville.com

Page 2 of 4

Source: ZeroHedge.com

To us, it looks like a bull market shakeout triggered by worries over rising interest rates and perceived

lack of action by central bankers, especially in Europe, to expand monetary stimulus in response to a growing

banking crisis at Deutsche Bank, Unicredit, etc., all orchestrated with virtually no physical gold being

transacted. We would expect to see a sharp reduction in speculative COMEX long positions over the next few

weeks as confirmation that the shakeout has run its course.

One must ask whether anything has really changed in terms of the investment rationale for gold. In

our opinion, gold began a second leg of a long term bull market at the end of 2015. Bull market shakeouts

are a regular feature of longer term price advances and serve to restore the component of doubt necessary

to reconstruct the wall of worry characteristic of all bull markets.

In our opinion, systemic risk continues to grow in a stealthy manner and is only manifested

episodically, as in the current European banking crisis and in the fragmentation of the political consensus

that was once the foundation for the Eurozone and the euro itself. Investors in gold should find reassurance

in the palpable decay of investor confidence in central banking and radical monetary policy. There is scant

reason, in our opinion, to expect waning confidence to revive. In fact, there is substantial evidence to suggest

that ultralow interest rates, ballooning fiscal deficits in Western democracies, and competitive currency

devaluations are jelling into a negative feedback loop for global economic growth. We believe the most likely

macroeconomic scenario for years to come is a Japanese like twilight zone that oscillates between feeble

growth and periodic downturns.

40 West 57th Street, 19th Floor, New York, NY 10019 | (212) 698-0800 | www.tocqueville.com

Page 3 of 4

In our opinion, numerous catalysts are aligning to stoke broader interest and a renewed advance in

gold prices:

Spreading loss of confidence in central banking, both from investors and policy insiders. Trial balloons

to eliminate cash, ramp up fiscal deficits, and push nominal interest rates below the zero bound seem

to proliferate. Commentary in main stream financial media openly questions the efficacy of ultralow

interest rates and QE to stimulate economic growth.

Interest rates appear set to rise on a schedule not orchestrated by the Fed but by the financial

markets. Both political candidates favor fiscal stimulus that will inflate deficits at a time when non

US buyers of treasuries, a principal source of demand in recent years, have been in a liquidation

mode for the past twelve months. In our opinion, a continuation of rising interest rates will lead to

steep capital losses for holders of low to negative yielding sovereign debt, and cause considerable

collateral damage to equities.

Global gold mining production, in our opinion, appears locked into an irreversible decline for the next

5 to 10 years. Because exploration has slowed sharply, there are fewer new deposits to mine.

Industry reserve life is dwindling. Barriers to new mine construction seem more formidable than at

any time for the past twenty years.

The US economy is cruising at stall speed on a best case basis and more likely teetering on recession.

Should interest rates rise at this precarious juncture, monetary policy, perceived to be in a tightening

mode, could be forced into another phase of QE or even more radical measures.

Gold is extremely under owned in Western investment portfolios. Because supplies of above ground

stocks normally available to satisfy Western investment demand have been severely depleted by

flows to Asian investors, the price dynamics could be explosive.

Gold has enjoyed a stealth bull market since the advent of radical monetary policies around 2000. As

the chart below shows, gold has been the best performing asset class since then, a fact that is

completely unrecognized by main stream media and conventional investors. The painful correction

from 2011 to year end 2015 camouflaged gold’s strength and explains why most investors remain

complacent as to systemic risk, intellectually understanding the unsustainability of radical monetary

policy but unmotivated to seek gold’s protection.

40 West 57th Street, 19th Floor, New York, NY 10019 | (212) 698-0800 | www.tocqueville.com

Page 4 of 4

It seems unlikely that the long term erosion of investment confidence, the onset of a secular bear

market in financial assets, and further advances in the stealth bull market for gold will take place in a linear

fashion. There are bound to be shakeouts and fake outs along the way to camouflage the underlying reality

that the global financial system as we know it is in extremis. We also believe that the current sharp correction

in the precious metals complex is a setup for another major advance toward new highs in metal and share

prices. We therefore recommend taking advantage of current weakness to build or establish new positions.

John Hathaway

Senior Portfolio Manager

© Tocqueville Asset Management L.P.

October 12, 2016

This article reflects the views of the author as of the date or dates cited and may change at any time. The information should not be construed as investment advice. No representation is made concerning the accuracy of cited data, nor is there any guarantee that any projection, forecast or opinion will be realized. References to stocks, securities or investments should not be considered recommendations to buy or sell. Past performance is not a guide to future performance. Securities that are referenced may be held in portfolios managed by Tocqueville or by principals, employees and associates of Tocqueville, and such references should not be deemed as an understanding of any future position, buying or selling, that may be taken by Tocqueville. We will periodically reprint charts or quote extensively from articles published by other sources. When we do, we will provide appropriate source information. The quotes and material that we reproduce are selected because, in our view, they provide an interesting, provocative or enlightening perspective on current events. Their reproduction in no way implies that we endorse any part of the material or investment recommendations published on those sites.

1

Section I. Macro

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

2000 2002 2004 2006 2008 2010 2012 2014 2016-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%Fig.1. Gold and US Real Rates

US Real Rates

Gold ($/Oz)

Source: Bloomberg

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

$4,500

$5,000

1995 1998 2001 2004 2007 2010 2013 2016

Fig.2. Fed Balance Sheet ($B)

Source: Bloomberg

-3%

-2%

-1%

0%

1%

2%

3%

4%

2000 2002 2004 2006 2008 2010 2012 2014 2016€ 0

€ 200

€ 400

€ 600

€ 800

€ 1,000

€ 1,200

€ 1,400

€ 1,600H

un

dre

dsFig.3. Gold and ECB Real Rates

Gold (€/Oz)ECB Real Rates

Source: Bloomberg

€ 500

€ 1,000

€ 1,500

€ 2,000

€ 2,500

€ 3,000

€ 3,500

€ 4,000

1999 2001 2003 2005 2007 2009 2011 2013 2015

Fig.4. ECB Balance Sheet (€B)

Source: Bloomberg

¥0

¥2,000

¥4,000

¥6,000

¥8,000

¥10,000

¥12,000

¥14,000

2000 2002 2004 2006 2008 2010 2012 2014 2016-2%

0%

2%

4%

6%

8%

10%

12%

14%Fig.5. Gold and PBC Real Rates

PBC Real Rates

Gold (¥/Oz)

Source: Bloomberg

¥5,000

¥10,000

¥15,000

¥20,000

¥25,000

¥30,000

¥35,000

¥40,000

2003 2005 2007 2009 2011 2013 2015

Fig.6. PBC Balance Sheet (¥B)

Source: Bloomberg

2

Section I. Macro

$4

$6

$8

$10

$12

$14

$16

$18

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Fig.7. The Biggest 6 Central Bank Balance SheetsUS, UK, Japan, China, EU & Switzerland (US$T)

Source: Bloomberg

-5%

0%

5%

10%

15%

20%

25%

1999 2001 2003 2005 2007 2009 2011 2013 2015

Fig.9. US M1 YoY%

Source: Bloomberg

0%

2%

4%

6%

8%

10%

12%

1999 2001 2003 2005 2007 2009 2011 2013 2015

Fig.10. US M2 YoY%

Source: Bloomberg

0%

5%

10%

15%

20%

1999 2001 2003 2005 2007 2009 2011 2013 2015

Fig.11. ECB M1 YoY %

Source: Bloomberg

0%

2%

4%

6%

8%

10%

12%

1999 2001 2003 2005 2007 2009 2011 2013 2015

Fig.12. ECB M2 YoY %

Source: Bloomberg

0%

5%

10%

15%

20%

25%

30%

35%

40%

1999 2001 2003 2005 2007 2009 2011 2013 2015

Hu

nd

red

s Fig.13. PBC M1 YoY %

Source: Bloomberg

0%

5%

10%

15%

20%

25%

30%

35%

1999 2001 2003 2005 2007 2009 2011 2013 2015

Fig.14. PBC M2 YoY %

Source: Bloomberg

$0

$10

$20

$30

$40

$50

1999 2002 2005 2008 2011 2014

$0

$500

$1,000

$1,500

$2,000

Tho

usa

nd

s

Fig.8. Gold and M2 (US$B, Fed, ECB & PBC)

Gold

M2

Source: Bloomberg

3

Section I. Macro

Fig.15. Inflation August 2016

US Euro Area China

Headline CPI 1.1 0.2 1.3

Core CPI 2.3 0.8 n/a

Shadowstats 8.2 n/a n/a

$13

$14

$15

$16

$17

$18

$19

$20

2011 2012 2013 2014 2015 2016

Fig.18. The Debt Ceiling ($T)

Total Federal Debt

Debt Ceiling Limit

Source: Bloomberg

Source: Bloomberg, Shadow Government Statistics.

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

2000 2002 2004 2006 2008 2010 2012 2014 2016

Fig.19. Average Annual Interest Rate on US Debt

Source: US Treasury, Meridian Macro.

$0

$5

$10

$15

$20

$25

1940 1950 1960 1970 1980 1990 2000 2010

Fig.16. US National Debt ($T)

Source: TreasuryDirect.gov, USDebtClock.org

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

1966 1976 1986 1996 2006 2016

Fig.17. Total Pubic Market Debt as % of GDP

Source: Stlouisfed.org

0%

5%

10%

15%

20%

25%

1988 1992 1996 2000 2004 2008 2012

Fig.20. Interest Expense as % of Total Government Outlays

Source: Bloomberg; US Treasury

4

Section I. Macro

-$20

$20

$60

$100

$140

$180

$220

$260

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Fig.23. China Net Purchases Long-Term US Securities(annual US$B)

Source: US Treasury; MacroMavens, LLC

-$800

-$300

$200

$700

$1,200

$1,700

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Fig.21. Global Forex Accumulation (US$B, 12 month sum)

Source: Bloomberg; MacroMavens, LLC

-$100

$100

$300

$500

$700

1978 1983 1988 1993 1998 2003 2008 2013

Fig.22. Net Purchases of US Treasury Notes and Bonds by All Foreign Countries (US$B, 12 month sum)

Source: US Treasury; MacroMavens, LLC

5

Section II. Gold

19.6%21.8%

3.1%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

1934 1982 2015

Fig.25. Market Value of Above Ground Gold as % of Total US Financial Assets

Source: Federal Reserve, World Gold Council

0

40

80

Oct-03 Oct-05 Oct-07 Oct-09 Oct-11 Oct-13 Oct-15

Mill

ion

s o

f O

un

ces

Fig.26. Gold Held by ETFs

All ETFS

SPDR Trust

Source: Bloomberg, Company Filings.

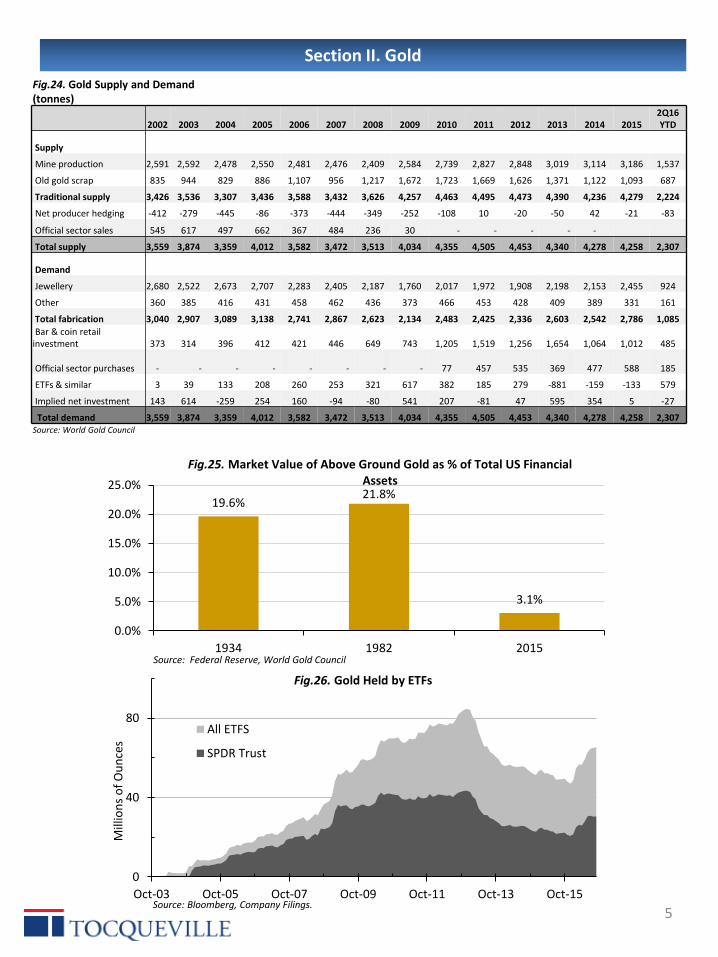

Fig.24. Gold Supply and Demand (tonnes)

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 20152Q16 YTD

Supply

Mine production 2,591 2,592 2,478 2,550 2,481 2,476 2,409 2,584 2,739 2,827 2,848 3,019 3,114 3,186 1,537

Old gold scrap 835 944 829 886 1,107 956 1,217 1,672 1,723 1,669 1,626 1,371 1,122 1,093 687

Traditional supply 3,426 3,536 3,307 3,436 3,588 3,432 3,626 4,257 4,463 4,495 4,473 4,390 4,236 4,279 2,224

Net producer hedging -412 -279 -445 -86 -373 -444 -349 -252 -108 10 -20 -50 42 -21 -83

Official sector sales 545 617 497 662 367 484 236 30 - - - - -

Total supply 3,559 3,874 3,359 4,012 3,582 3,472 3,513 4,034 4,355 4,505 4,453 4,340 4,278 4,258 2,307

Demand

Jewellery 2,680 2,522 2,673 2,707 2,283 2,405 2,187 1,760 2,017 1,972 1,908 2,198 2,153 2,455 924

Other 360 385 416 431 458 462 436 373 466 453 428 409 389 331 161

Total fabrication 3,040 2,907 3,089 3,138 2,741 2,867 2,623 2,134 2,483 2,425 2,336 2,603 2,542 2,786 1,085

Bar & coin retail investment 373 314 396 412 421 446 649 743 1,205 1,519 1,256 1,654 1,064 1,012 485

Official sector purchases - - - - - - - - 77 457 535 369 477 588 185

ETFs & similar 3 39 133 208 260 253 321 617 382 185 279 -881 -159 -133 579

Implied net investment 143 614 -259 254 160 -94 -80 541 207 -81 47 595 354 5 -27

Total demand 3,559 3,874 3,359 4,012 3,582 3,472 3,513 4,034 4,355 4,505 4,453 4,340 4,278 4,258 2,307Source: World Gold Council

6

Section II. Gold

Investment Adviser, 20.6%

Broker, 6.2%

Private Banking, 8.1%

Pension Fund, 0.6%

Hedge Fund, 7.2%

Mutual Fund, 4.4%

Insurance Company, 0.2%

Non-Institutional,

52.7%

Fig.27. SPDR Gold Trust Ownership by Type

Source: FactSet

-800-700-600-500-400-300-200-100

0100200300400500600700800

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

Fig.29. Central Banks Net Purchases (tonnes)

Source: World Gold Council

Fig.28. Notable Transaction in Aug 2016 (YTD)

Country Tonnes Transaction

Russia 112 Purchase

Turkey 60 Decrease

China 71 PurchaseSource: World Gold Council

8%

9%

10%

11%

12%

13%

14%

3/00 3/02 3/04 3/06 3/08 3/10 3/12 3/14 3/16

Fig.31. Gold as % of Total Reserves

Source: World Gold Council

29,500

30,000

30,500

31,000

31,500

32,000

32,500

33,000

33,500

34,000

2000 2002 2004 2006 2008 2010 2012 2014 2016

Fig.30 Central Banks Holdings of Gold (tonnes)

Source: World Gold Council

7

Section II. Gold

0

20

40

60

80

100

Sep-07 Sep-08 Sep-09 Sep-10 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15 Sep-16

Fig.32. Web searches for "Gold Bubble"

Source: GoogleTrends

0

20

40

60

80

100

Oct-04 Oct-05 Oct-06 Oct-07 Oct-08 Oct-09 Oct-10 Oct-11 Oct-12 Oct-13 Oct-14 Oct-15

Fig.33. Web searches for "Gold Investment"

Source: GoogleTrends

$0$200$400$600$800$1,000$1,200$1,400$1,600$1,800$2,000

0

20

40

60

80

100

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Fig.34. Bernstein's Daily Sentiment Index

DSI

Gold

Source Bloomberg, Bernstein's DSI

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

-

20.00

40.00

60.00

80.00

100.00

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Fig.35. Market Vane Sentiment Index

MV

Gold

Source Bloomberg, Market Vane

8

Section II. Gold

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

800

1,000

1,200

1,400

1,600

1,800

2,000

2006 2008 2010 2012 2014 2016

Fig.36. Comex Gold Futures Open Interest (tonnes)

Open Interest

Gold ($/Oz)

Source: Bloomberg

-20%

80%

180%

280%

380%

480%

2000 2002 2004 2006 2008 2010 2012 2014 2016

Fig.37. Gold vs Continuous Commodity Index Performance

CCI Index

Gold

Source: Bloomberg

$-

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

0%

20%

40%

60%

80%

100%

7/10 7/11 7/12 7/13 7/14 7/15 7/16

Fig.39. Commercial Net Shorts as % of Total Open Interest

Net Short/OpenInterestGold

Source: Bloomberg; The McClellan Market Report

More Net Short

Less Net Short

$0

$500

$1,000

$1,500

$2,000

-1,200

-700

-200

300

800

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Fig.38. Comex Gold Futures Activity (tonnes)

Net Large Speculators

Net Hedgers/Commercials

Gold ($/Oz)

Source: CFTC

0

100

200

300

400

500

600

0

1

2

3

4

5

6

2003 2005 2007 2009 2011 2013 2015

Mill

ion

s o

f O

un

ces

Fig. 40. Registered COMEX Gold Stocks vs. Owners per Ounce

Registered Stocks

Owners per Ounce

Source: Bloomberg

9

Section III. Gold Mining Equities

0%

10%

20%

30%

40%

50%

60%

70%

1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

Fig.41. XAU and HUI as a Ratio of Gold

HUI/GoldXAU/Gold

Source: FactSet

-$4,000

-$3,000

-$2,000

-$1,000

$0

$1,000

$2,000

$3,000

$4,000

1H

07

2H

07

1H

08

2H

08

1H

09

2H

09

1H

10

2H

10

1H

11

2H

11

1H

12

2H

12

1H

13

2H

13

1H

14

2H

14

1H

15

2H

15

1H

16

2H

16

Fig.42. Net Fund Flows For Lipper's Equity Precious Metals Fund Universe ($M)

Source: Morningstar 2H16 is through 8/31/16

0

100

200

300

400

500

600

$0

$2

$4

$6

$8

$10

$12

$14

$16

03 04 05 06 07 08 09 10 11 12 13 14 15

Fig.44. Equity Capital Issued by Gold Miners

$B of Equty Issued

# of Transactions

Source: Bloomberg

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

5/06 5/07 5/08 5/09 5/10 5/11 5/12 5/13 5/14 5/15 5/16

Fig.43. Market Cap of Van Eck Gold Equity ETFs ($B)

Source: FactSet

10

Section III. Gold Mining Equities

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

02 03 04 05 06 07 08 09 10 11 12 13 14 15

Fig.45. Senior Producers Return On Capital

Source: FactSet. Universe: NEM, ABX, GG, KGC, AUY, NCM, AU, GFI, HMY

0%

20%

40%

60%

80%

100%

120%

$0

$200

$400

$600

$800

$1,000

$1,200

05 06 07 08 09 10 11 12 13 14 15

Fig.46. Average Cost of Acquisitions in the Gold Sector ($/Oz)

Acquisition Cost As Ratio of Gold Price

Source: RBC Capital Markets, Bloomberg.

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 20152016

E

After Tax Cash Cost ($/oz) 209 210 253 311 363 413 552 738 661 814 987 1,108 1,087 988 903 868

Margin (%) 23% 32% 30% 24% 18% 32% 21% 15% 32% 34% 37% 34% 23% 22% 22% 24%

0%

5%

10%

15%

20%

25%

30%

35%

40%

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400Fig.47. Gold Mining Industry Production Costs

After Tax Cash Cost ($/oz)

Margin (%)

Source: Tocqueville Asset Management, FactSet.

11

Section III. Gold Mining Equities

Source: BMO Capital Markets

Fig.48. Gold Price Discounted by Market ($/Oz)

Fig.49. NAV Premiums – Senior & Intermediate Producers (N.A.)

Source: ScotiabankSource: Scotiabank

Fig.50. P/CF – Universe of Coverage AverageFig.51. Adjusted Market Cap per Oz of Resource

Divided by Gold Price

Source: BMO Capital Markets