TO TRANSITION VIETNAM CONSUMER TRENDS 2017 TRANSITION VIETNAM CONSUMER TRENDS 2017 AMCHAM VIETNAM...

30

1 FROM TRADITION TO TRANSITION VIETNAM CONSUMER TRENDS 2017 AMCHAM VIETNAM APRIL 19,2017

Transcript of TO TRANSITION VIETNAM CONSUMER TRENDS 2017 TRANSITION VIETNAM CONSUMER TRENDS 2017 AMCHAM VIETNAM...

1

FROM TRADITION

TO TRANSITION

VIETNAM CONSUMER TRENDS 2017AMCHAM VIETNAM APRIL 19,2017

2

2017 Consumer Confidence and Retail Impact

INFOCUS MEKONG RESEACRH

3

Consumer confidence is what drives economic growth world-wide and Vietnam is no different.

4

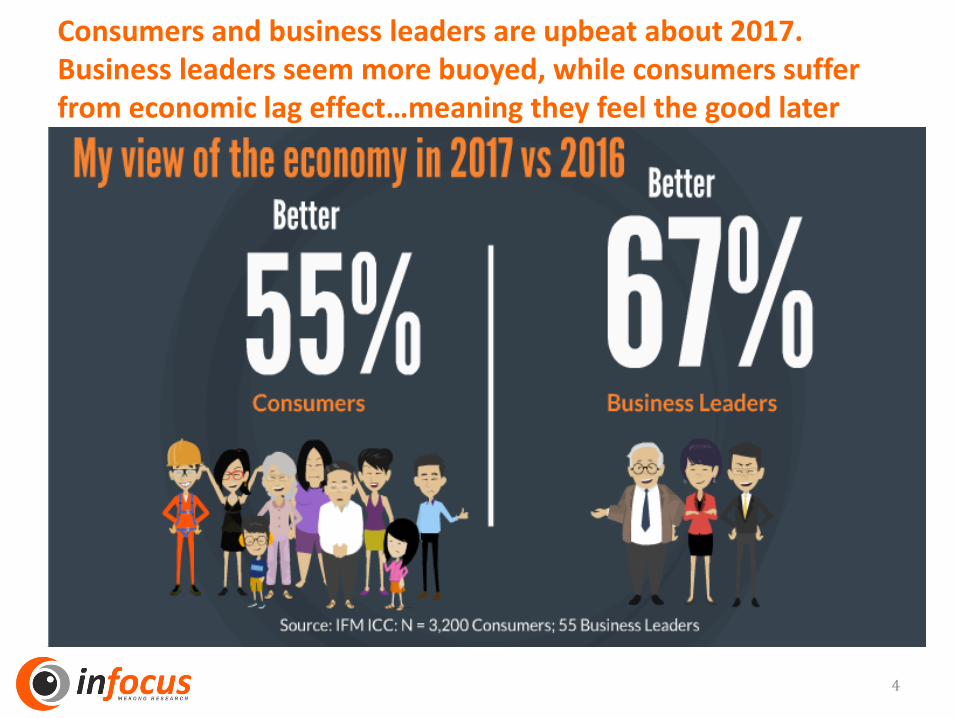

Consumers and business leaders are upbeat about 2017. Business leaders seem more buoyed, while consumers suffer from economic lag effect…meaning they feel the good later

5

Key concerns for 2017 revolve around the value of the local currency and the increase in the cost of living.

6

For consumers the VND devaluation is seen as a major concern, due to declining purchasing power, driving increased price sensitivity. For business Leaders, economic impact, both global & domestic are worries

7

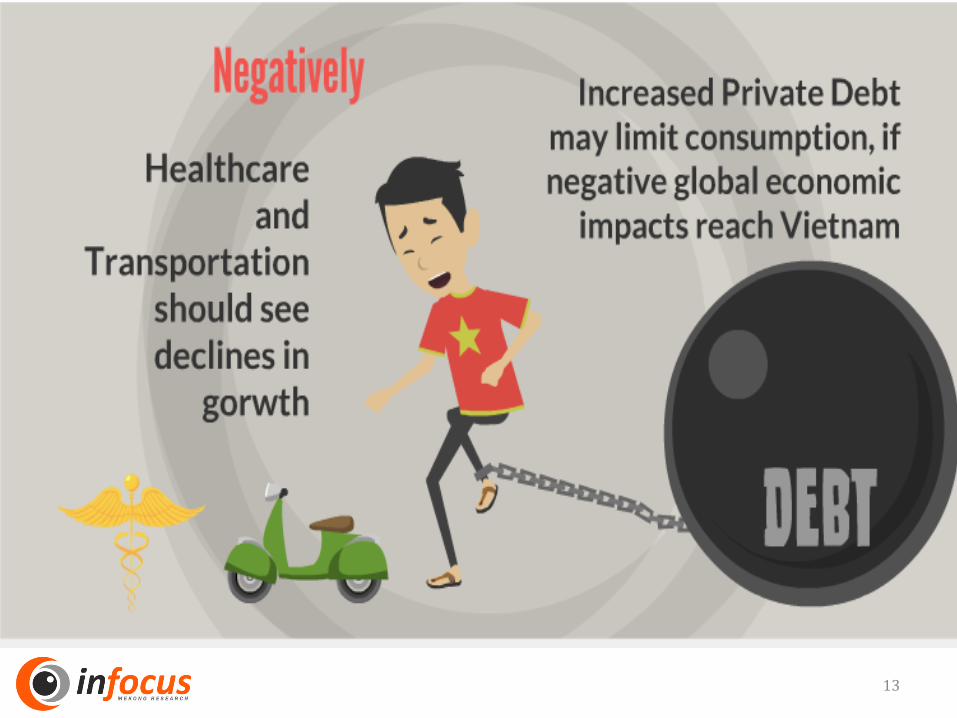

2017 should see continued growth in consumer spend with Education, Entertainment, and Food & Beverage sectors driving growth. Healthcare spend has dropped from the 2nd to the 9th position in the past 4 years.

30%

10%

8

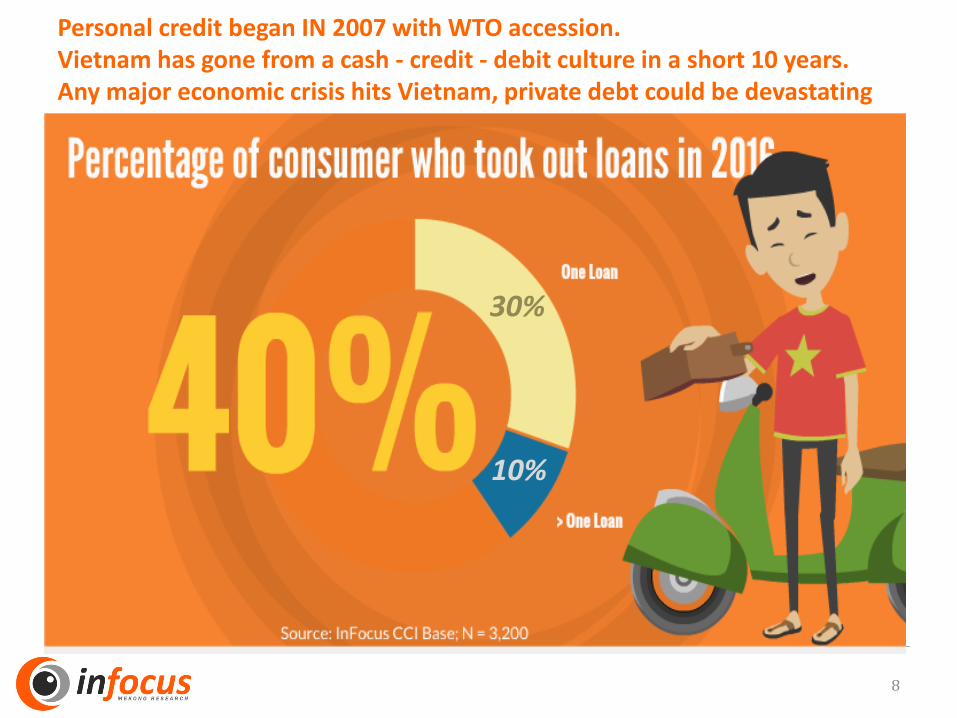

Personal credit began IN 2007 with WTO accession. Vietnam has gone from a cash - credit - debit culture in a short 10 years. Any major economic crisis hits Vietnam, private debt could be devastating

9

Loans were driven by personal item purchases, business & real estate investments. Hence, consumers are beginning to live above their means.

10

Savings are in decline, largely due to an increase in conspicuous spending, stuff we want but are not necessities… showing further consumer confidence

11

12

13

DIGITAL VIETNAM

41

54

60

81

84

86

4

11

42

37

58

31

Smart TV

iPad /Tablet

Desktop

Laptop

Home WIFI

Smartphone

Digital Ownership 20132016

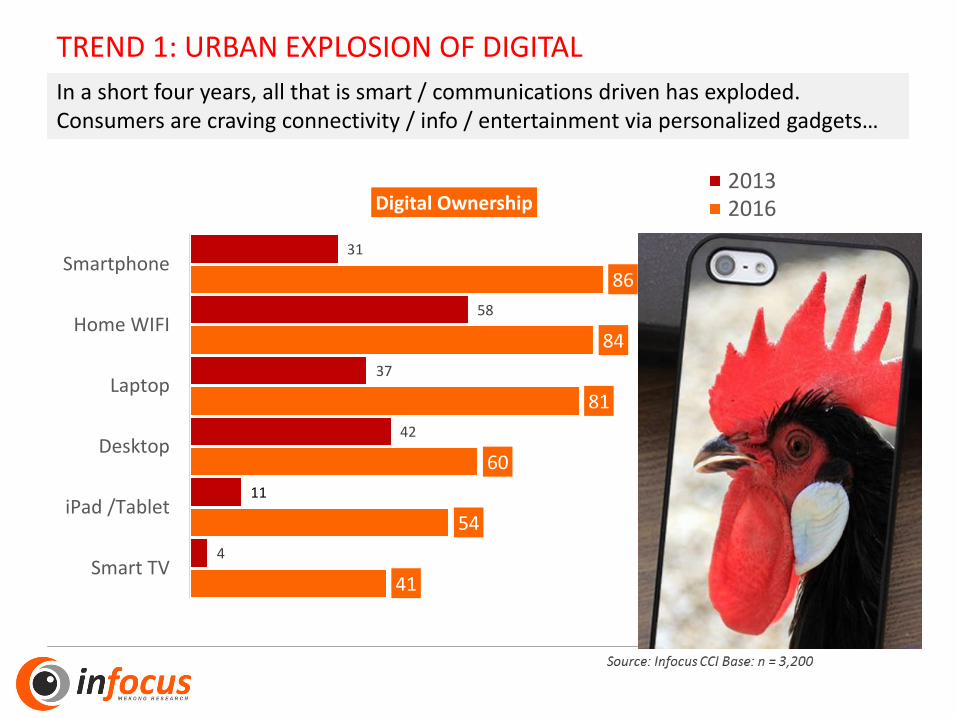

TREND 1: URBAN EXPLOSION OF DIGITAL

In a short four years, all that is smart / communications driven has exploded. Consumers are craving connectivity / info / entertainment via personalized gadgets…

TREND 2: PURCHASING FOR SELF FULLFILLMENT “CONFIDENCE”

All things that give pleasure for work, rest and play are now key purchase items

82%

47%

42%

40%

14%

12%

7%

5%

Smartphone

Laptop

Motorbike

Smart TV

House

Apartment

New Car

Used car

TREND 3: SMARTPHONE CONVERGENCE AS EVERYTHING DEVICE

51 52 53 54 5556

3238 43

4853

56

2932

3538

42

46

2015 2016 2017 2018 2019 2020

INTERNET

SMARTPHONE

PC

Vietnam embraces all things digital, as witnessed by past and forecasted growth. In a short 4 years, Mobile looks to converge with all things digital at the key digital platform in Vietnam

Millions of USERS2020

62 Million

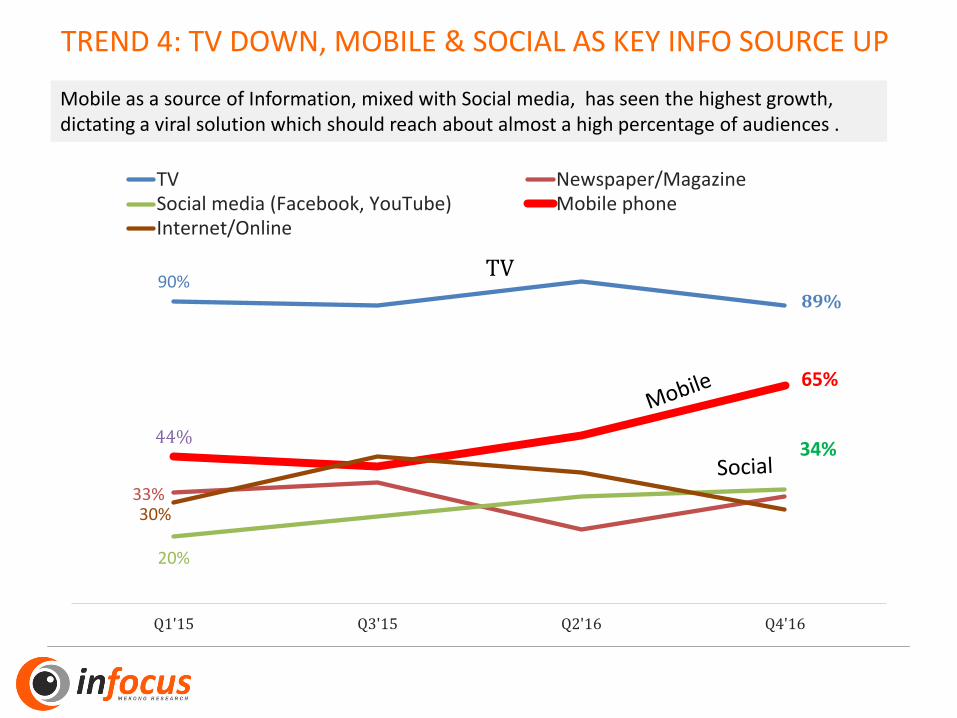

TREND 4: TV DOWN, MOBILE & SOCIAL AS KEY INFO SOURCE UP

Mobile as a source of Information, mixed with Social media, has seen the highest growth, dictating a viral solution which should reach about almost a high percentage of audiences .

90%

33%

20%

44%

30%

Q1'15 Q3'15 Q2'16 Q4'16

TV Newspaper/MagazineSocial media (Facebook, YouTube) Mobile phoneInternet/Online

89%

65%

34%

TV

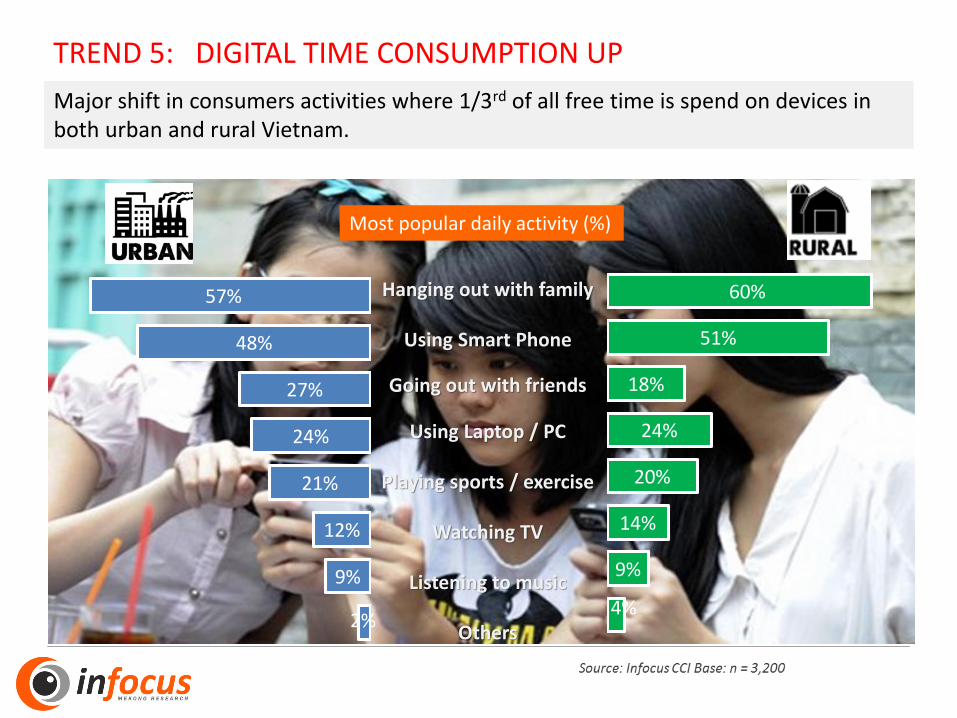

TREND 5: DIGITAL TIME CONSUMPTION UP

Most popular daily activity (%)

Major shift in consumers activities where 1/3rd of all free time is spend on devices in both urban and rural Vietnam.

2%

9%

12%

21%

24%

27%

48%

57%

4%

9%

14%

20%

24%

18%

51%

60%Hanging out with family

Using Smart Phone

Going out with friends

Using Laptop / PC

Playing sports / exercise

Watching TV

Listening to music

Others

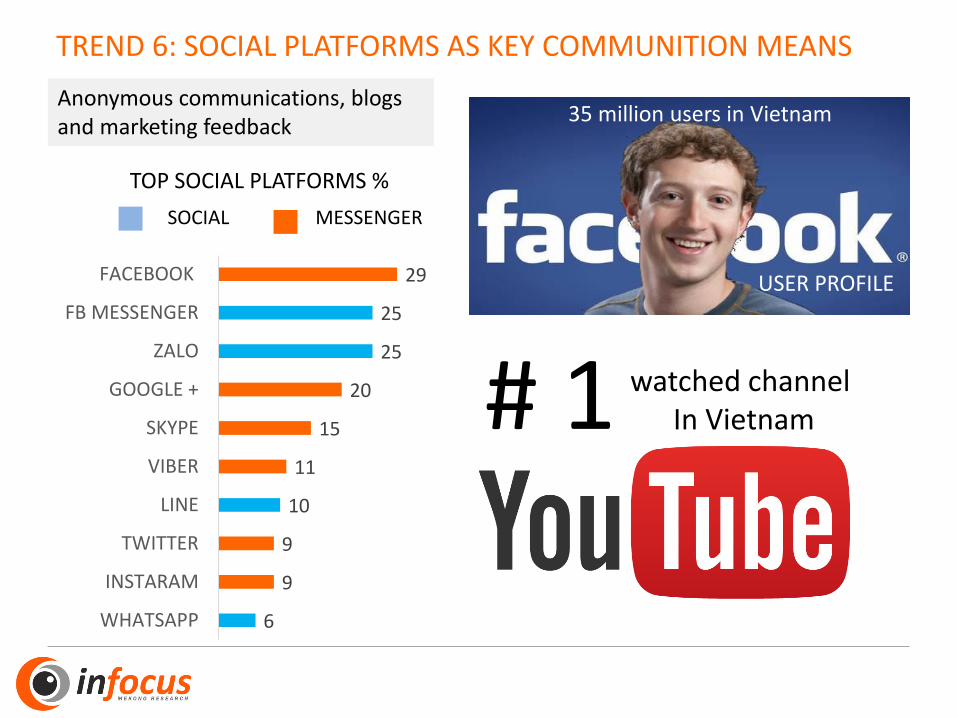

TREND 6: SOCIAL PLATFORMS AS KEY COMMUNITION MEANS

TOP SOCIAL PLATFORMS %

6

9

9

10

11

15

20

25

25

29

INSTARAM

LINE

VIBER

SKYPE

GOOGLE +

ZALO

FB MESSENGER

SOCIAL MESSENGER

USER PROFILE

35 million users in VietnamAnonymous communications, blogs and marketing feedback

# 1 watched channel In Vietnam

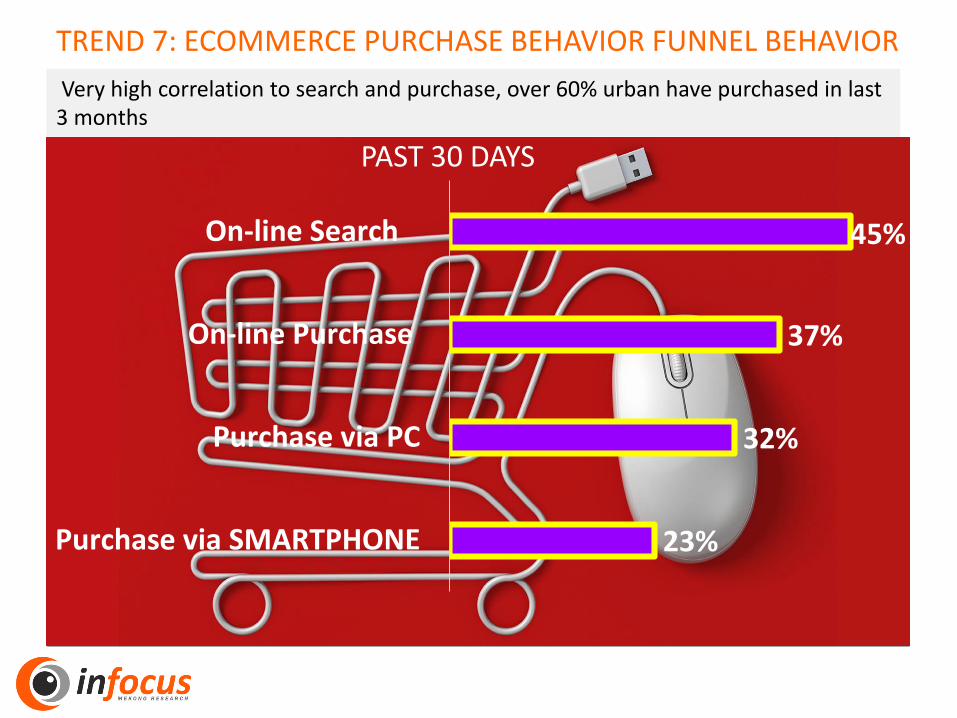

TREND 7: ECOMMERCE PURCHASE BEHAVIOR FUNNEL BEHAVIOR

23%

32%

37%

45%

Purchase via SMARTPHONE

Purchase via PC

On-line Purchase

On-line Search

Very high correlation to search and purchase, over 60% urban have purchased in last 3 months

PAST 30 DAYS

KEY DIGITAL INSIGHTS

Smartphones are already the #1 digital device in urban Vietnam, with rural to follow, thus communications and marketing need to catch up to reality and will become the number platform nation wide by 2020

Personal SELF FULLFILLMENT driven by consumer “CONFIDENCE” the and convenience of digital is driving purchasing as well as debt culture

1

3

2

We don’t even know what is

does yet?

In Vietnam, Social platforms have become a daily means of communications

4

Digital is redefining consumer product awareness & shoppingbehavior

THE FUTURE OF SHOPPING IN HCMC

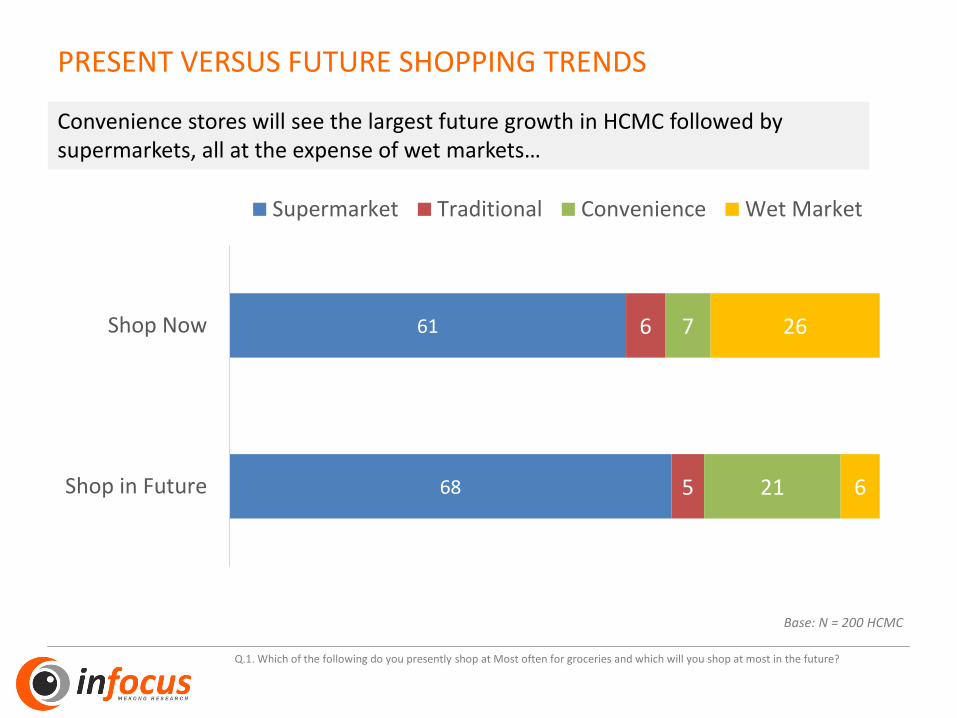

PRESENT VERSUS FUTURE SHOPPING TRENDS

68

61

5

6

21

7

6

26

Shop in Future

Shop Now

Supermarket Traditional Convenience Wet Market

Q.1. Which of the following do you presently shop at Most often for groceries and which will you shop at most in the future?

Base: N = 200 HCMC

Convenience stores will see the largest future growth in HCMC followed by supermarkets, all at the expense of wet markets…

0

10

20

30

40

50

60

70

80

My favorite place to shop

My most often shopped atstore

Has more reasonable pricesthan other places

Has more range of productsthan other places

Has more services thanother places

More secure than otherplaces

Offer more promotions thanother places

Supermarkets / Hypermarket Wet markets Traditional

Modern trade = promotion, security and product range Traditional trade = reasonable price

Base: N = 200 HCMC

GROCERY SHOPPING PHONE ORDER / ONLINE / SMARTPHONE

Ever shopped

77%

23%

Yes No

Future shopping intent

Q.5 have you ever shopped for Groceries on-line, by telephone or smartphone and if the service were available, would you use?

Base: N = 200 HCMC

A surprising 77% have shopped for groceries via Phone, Mobile or On-line, while future intent is also strong

31%

Other

Smartphone

On-line

Modern trade

27

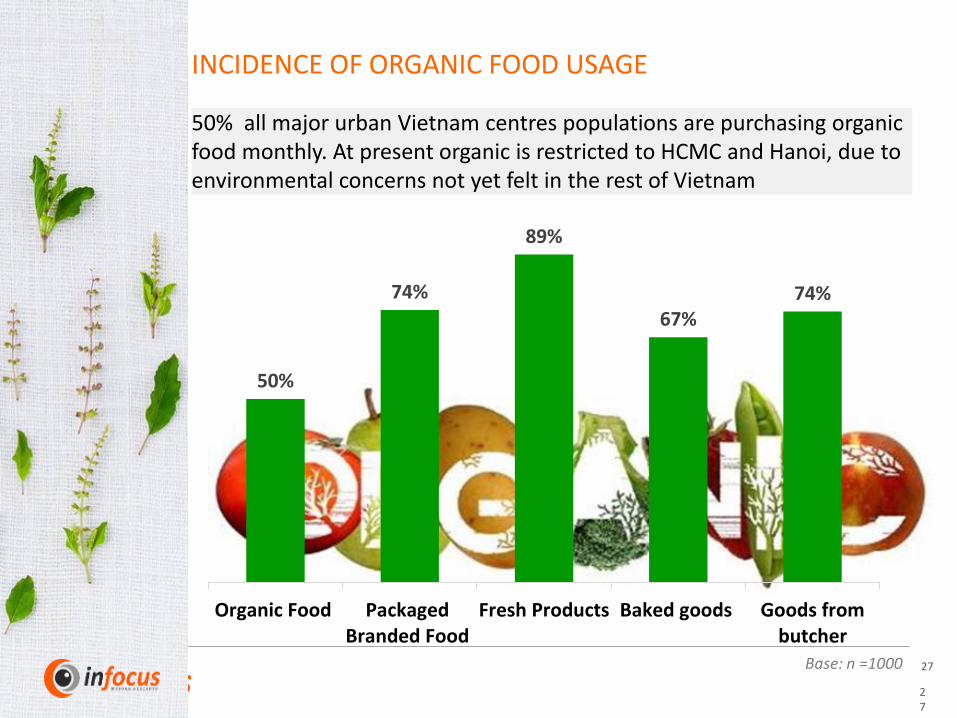

27Base: n =1000

50%

74%

89%

67%74%

Organic Food PackagedBranded Food

Fresh Products Baked goods Goods frombutcher

INCIDENCE OF ORGANIC FOOD USAGE

50% all major urban Vietnam centres populations are purchasing organic food monthly. At present organic is restricted to HCMC and Hanoi, due to environmental concerns not yet felt in the rest of Vietnam

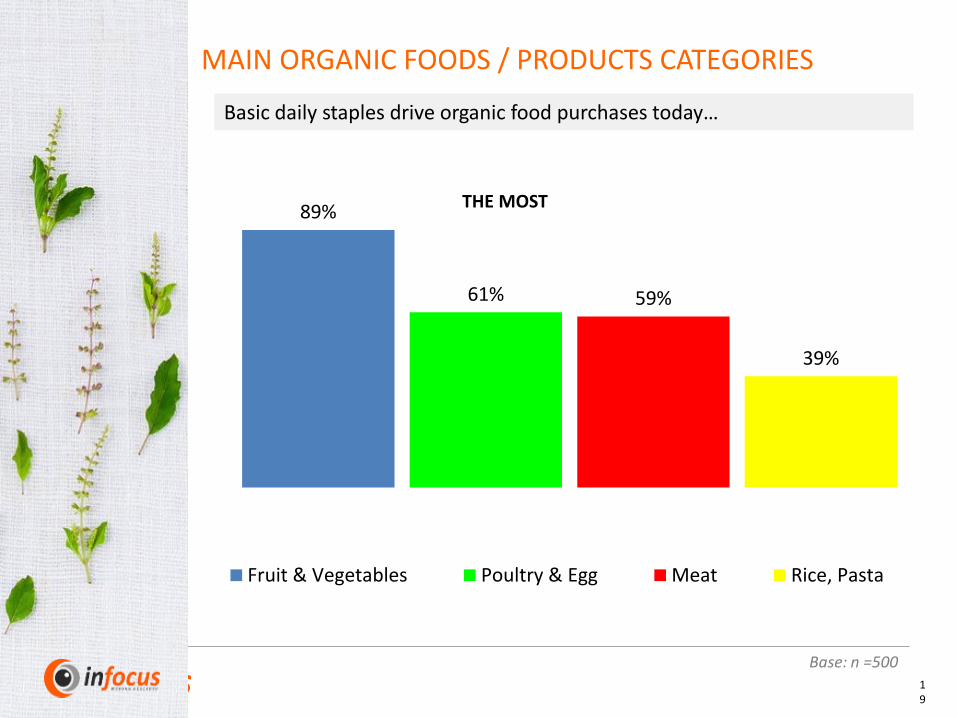

89%

61% 59%

39%

Fruit & Vegetables Poultry & Egg Meat Rice, Pasta

19

MAIN ORGANIC FOODS / PRODUCTS CATEGORIES

Basic daily staples drive organic food purchases today…

Base: n =500

THE MOST

RETAIL SOLUTIONS

Mobile New ways to reach consumers

POD Maslow’s Priority of hierarchal needs changing

Security More focus on health and eating healthy

Transport Location less critical to store choice

Convenience All in one concepts attracting shoppers

30

Thank you for your time and please contact us for more!