To Tax or not to Tax – VAT is the Question! - CUBO -...

31

© The University of Sheffield / Taxation Department 2009 To Tax or not to Tax – VAT is the Question! Deborah Damment (Group Taxes Manager) Andy Jamieson (VAT Manager) University of Sheffield

Transcript of To Tax or not to Tax – VAT is the Question! - CUBO -...

© The University of Sheffield / Taxation Department 2009

To Tax or not to Tax – VAT is the Question!

Deborah Damment (Group Taxes Manager)

Andy Jamieson (VAT Manager)University of Sheffield

© The University of Sheffield / Taxation Department 2009

Agenda

Corporation tax

• Brief overview of universities and CT

VAT

• VAT Basics

• Quiz

• Catering

• Conferencing

© The University of Sheffield / Taxation Department 2009

CT and universities

Universities are charitable bodies and are subject to corporation tax on any non charitable / non primary purpose activities they undertake

• Charities Act 2006 and Finance Act 2006 introduced new and more onerous reporting requirements for universities

• “Non Student Lettings & Associated Income” has always been treated as non charitable activity

• The financial result of conferences and catering must be disclosed on an annual CT Self Assessment Return

• The disclosure must be supported by fully costedcomputations

© The University of Sheffield / Taxation Department 2009

CT and universities

Corporation Tax follows the charity law treatment of activities – if carried out as an integral part of the university’s charitable activities then it is tax exempt.

• Providing catering to students in the course of educating them is exempt from tax

• Providing the catering and accommodation for non educational events does not advance education and is a non primary activity subject to corporation tax

University of Sheffield discloses non academic conferences / external catering / non student outlets and vacation lettings as Non Primary Purpose activities annually to HMRC.

© The University of Sheffield / Taxation Department 2009

To Tax or not to Tax – VAT is the Question!

•VAT Basics

•Quiz

•Catering

•Conferencing

© The University of Sheffield / Taxation Department 2009

Rhetorical questions

Q. Do you treat all student income from cafes, etc as VAT exempt?

Q. Do you differentiate between “eat in” and “take away”?

Q. Do you treat any income from vending machines as VAT exempt?

Q. Should you?

Q. Why should you care?

© The University of Sheffield / Taxation Department 2009

VAT Basics

Taxable & exempt activity

Taxable activity

– Standard rate – 15% (17.5% w.e.f 1/1/2010)

– Reduced rate – 5%

– Zero rate – 0%

© The University of Sheffield / Taxation Department 2009

VAT Basics

Exempt activity

Activities listed in Schedule 9 of the VAT Act

Important ones for us:

– Group 1 – Land

– Group 6 - Education

© The University of Sheffield / Taxation Department 2009

VAT Basics

Taxable and exempt – why does it matter?

• You can recover/ offset VAT incurred against making taxable supplies

• You cannot recover VAT incurred against making exempt supplies

© The University of Sheffield / Taxation Department 2009

VAT Basics

Exempt and Zero rated – both have no VAT charged what’s the difference?

– Zero rate is “taxed” but at 0%

– Exempt is just that – exempt from VAT

Zero rate is the best category – as no VAT due to HMRC on sales but recovery of VAT on costs

© The University of Sheffield / Taxation Department 2009

VAT Basics

Partial exemption – what is it & why is it relevant?

VAT on purchase

Exempt Taxable

Residual

100% recovery

No recovery

Some recovery

© The University of Sheffield / Taxation Department 2009

What is catering?

• Legislation says (VAT Act 1994, Schedule 9, Group 6, Item 4)• The supply of goods and services (to a student) which are closely

related to a supply of ‘education’.• 8.2 What does “closely related” mean? • VAT Notice 701/30:• In general terms, “closely related” refers only to goods and services

that are:– for the direct use of the pupil, student or trainee; and necessary for

delivering the education to that person.

• However, if you’re and eligible body, you may treat as closely related any:– catering;

• that you provide, subject to the conditions of paragraphs 8.4 and 8.5.

© The University of Sheffield / Taxation Department 2009

What is catering?

• 8.3 What goods and services aren’t “closely related” to supplies of education?

• The following are examples of goods and services that are taxable in principle unless relief is available elsewhere. (This is subject to the overriding principle that supplies of catering by an eligible body to its pupils, students or trainees may be treated as closely related):

• supplies to staff (including tutors on summer schools) and to other non-students;

• sales of goods from school shops, campus shops and student bars;

• sales from vending machines;

© The University of Sheffield / Taxation Department 2009

What is catering?

• 8.4 What if my closely related goods and services qualify for zero-rating elsewhere?

• You may choose to either zero-rate or exempt them.

© The University of Sheffield / Taxation Department 2009

What is catering?

• 2.4 Vending machines• Vending machine supplies follow the same general principles as

food and drink supplied from catering outlets. In other words:• All supplies of food and drink from vending machines in canteens

and restaurant type areas are standard-rated as supplies to be consumed on the premises where they have been supplied. An apportionment will only be allowed if the food seller can produce evidence to show that a proportion of the items of cold food (that would be eligible for zero-rating) are taken-away from the canteen/restaurant premises (see section 3.3).

• All supplies from machines sited in thoroughfares and areas not designated for the consumption of food follow the liability of the product sold (see Notice 701/14 Food).

• If the vending machine is on a university campus and is run by the students’ union you will need to read section 5.5.

© The University of Sheffield / Taxation Department 2009

What is catering?

Vending Machines (Notice 709/1 – Catering & take away food)

5.5 Catering provided by student unions in universities and other higher education establishments

• If you are a student union and you are supplying catering or hot take-away food to students both on behalf, and with the agreement, of the parent institution, as a concession you can treat your supplies in the same way as the parent institution itself. This means that you can treat your supplies as exempt when made by unions at universities, and other institutions supplying exempt education, and outside the scope of VAT when supplied at further education and sixth form colleges.

• This means that most supplies of food and drink made by the union, where the food is sold for consumption in the course of catering (see sections 2 and 3 above), will be exempt. For example, food and drink sold from canteens, refectories and other catering outlets, plus food and drink sold from vending machines situated in canteens and similar areas.

• However, it does not cover food and drink sold from campus shops, bars, tuck shops, other similar outlets and certain vending machines (see 2.4 above) because they are not considered supplies that are made in the course of catering. Further the concession does not cover any other goods or services supplied by the student unions.

© The University of Sheffield / Taxation Department 2009

Catering or not?

• Cafe which services both staff and students, supplying hot food, cold food, packaged sandwiches and confectionary

© The University of Sheffield / Taxation Department 2009

VAT liability - catering income

Student or non-student?

Eat-in or take-out?

Eat-in or take-out?

“Supply in the course of catering”

Sandwich - Exempt

Coke - Exempt

Crisps - Exempt

“Sale of cold take-away food”

Sandwich Zero-rated

Coke - VATable / Exempt?

Crisps – VATable / Exempt?

“Supply in the course of catering”

Sandwich - VATable

Coke - VATable

Crisps - VATable

“Sale of cold take-away food”

Sandwich – Zero-rated

Coke - VATable

Crisps - VATable

Student

Eat-in

Non-Student

Take-out Eat-in Take-out

Note: food which is sold intended to be eaten hot is ALWAYS treated as a supply in the course of catering (e.g. soup, pizza).

© The University of Sheffield / Taxation Department 2009

03/08/2010 19

Issues to considerAll student income exempt, except take-away and all non-student income taxable, except take-

away?

Advantages• If you have price differential between students and non-students it could be reduced (i.e.

doesn’t have to be 15% uplift on non-student prices);• Increased competitiveness relative to local sandwich shops (which are able to zero-rate sales

of cold food for take-away)

Disadvantages• Would need to ask a second question at the till; time issue?• Need full product list to be VAT coded within the till system (and maintained);• New price lists?

Note; Could simply have two prices on sandwiches (a “take-out price” and an “eat-in price”).

© The University of Sheffield / Taxation Department 2009

Conference income

Basic starting point

• Education provided by an ‘eligible body’ is VAT exempt– Eligible body = school/ college/ uni and;

– A non-profit making body which applies any profits arising to the continuance or improvement of such supplies

• Education (not defined in law), but HMRC say it– includes conferences, symposia, etc

So if you as a University / College run your own conference then it is VAT exempt – Its all about the status of the provider, the recipient’s

status is irrelevant – when you run it yourself

© The University of Sheffield / Taxation Department 2009

Conferences

What if you provide a conference ‘package’?

• Conference

• Accommodation

• Dinner

• Transport

© The University of Sheffield / Taxation Department 2009

Conferences

• In isolation these would be standard rate supplies so VAT would be chargeable

• However, if it is a ‘package’ with a single price then the dominant supply is the conference and therefore you may treat the whole supply as exempt

© The University of Sheffield / Taxation Department 2009

Conferences

Bad news!

• What if you buy in some of the services?

• VAT charged on your purchase but no VAT recovery as your conference is exempt

• VAT on purchases needs to be built into your pricing

© The University of Sheffield / Taxation Department 2009

VAT Basics

VAT on purchase

Exempt Taxable

Residual

100% recovery

No recovery

Some recovery

© The University of Sheffield / Taxation Department 2009

Conferences

What if delegates have a choice to which elements they wish to purchase?

– In this case each separate item is looked at in isolation

Typically you can select

– Conference

– Accommodation

– Dinner

If this is the case then the conference is VAT exempt and the other two elements are standard rated

© The University of Sheffield / Taxation Department 2009

Conferences

Good news!

• If you charge VAT on the dinner and on accommodation then any VAT bearing costs which directly relate to these can be recovered/ offset

Bad news!

• Your delegates may not be able to recover the VAT

© The University of Sheffield / Taxation Department 2009

Conference facilities

What if you hold out your facilities for others to hold their conferences?

Now its all about their status and what the conference is about– If the conference provider is an ‘eligible body’ and the

conference is ‘educational’ then the package can be VAT exempt as if you were providing the conference yourself

– If the conference provider is not an eligible body then it is necessary to look at what you are providing

In most cases the supply will be one of facilities and services in which case VAT is chargeable on the whole sum

© The University of Sheffield / Taxation Department 2009

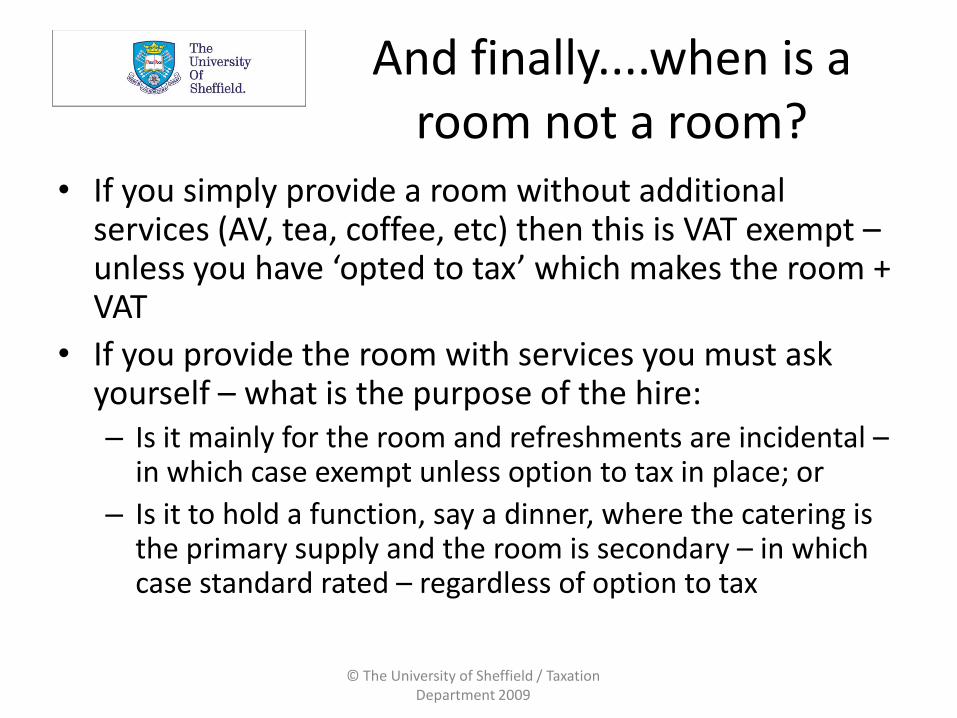

And finally....when is a room not a room?

• If you simply provide a room without additional services (AV, tea, coffee, etc) then this is VAT exempt –unless you have ‘opted to tax’ which makes the room + VAT

• If you provide the room with services you must ask yourself – what is the purpose of the hire:– Is it mainly for the room and refreshments are incidental –

in which case exempt unless option to tax in place; or

– Is it to hold a function, say a dinner, where the catering is the primary supply and the room is secondary – in which case standard rated – regardless of option to tax

© The University of Sheffield / Taxation Department 2009

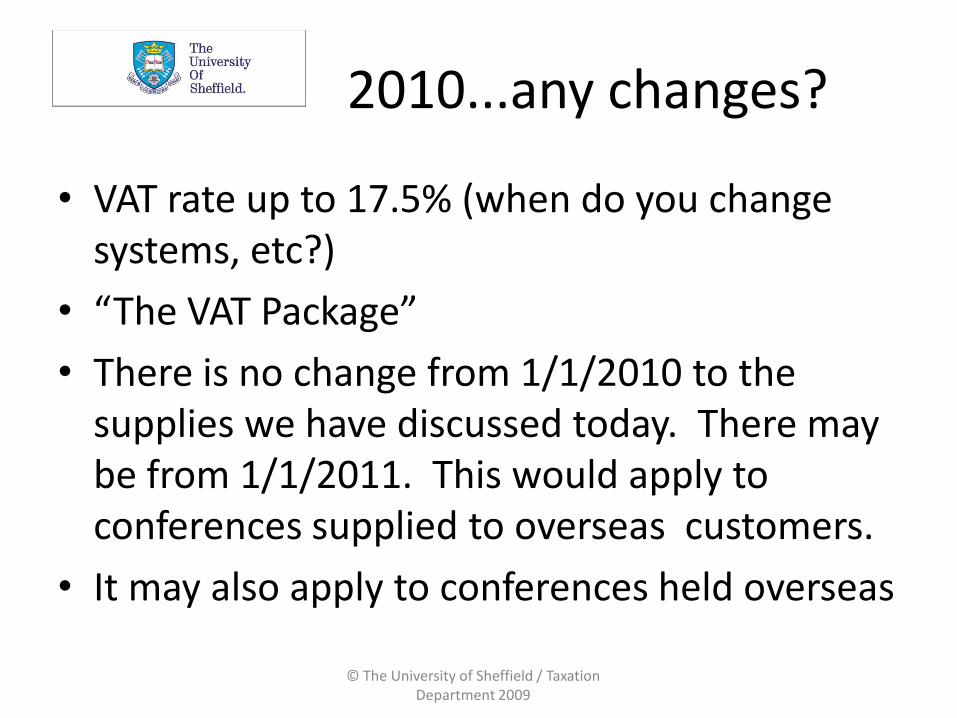

2010...any changes?

• VAT rate up to 17.5% (when do you change systems, etc?)

• “The VAT Package”

• There is no change from 1/1/2010 to the supplies we have discussed today. There may be from 1/1/2011. This would apply to conferences supplied to overseas customers.

• It may also apply to conferences held overseas

© The University of Sheffield / Taxation Department 2009

Disclaimer

• Please note that the views expressed in this presentation are those of the presenter and may represent either the treatment of VAT by the University of Sheffield or opportunities for different treatment. If your own institution’s treatment is different it may be based on individual circumstances or rulings from HMRC locally. If in any doubt please do contact your own tax department.

© The University of Sheffield / Taxation Department 2009

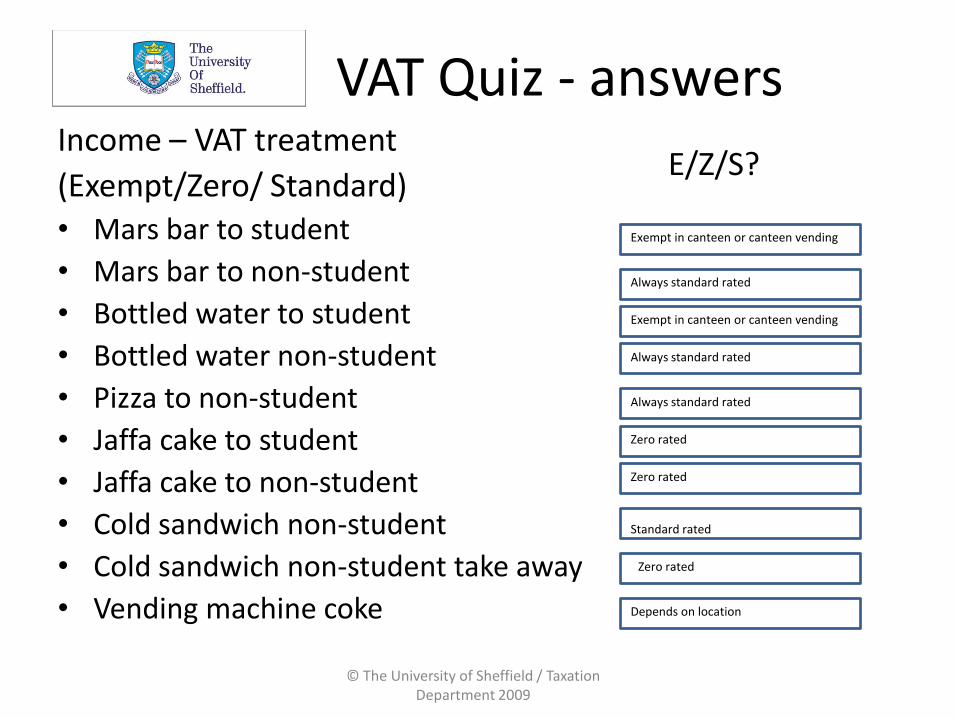

VAT Quiz - answersIncome – VAT treatment

(Exempt/Zero/ Standard)• Mars bar to student

• Mars bar to non-student

• Bottled water to student

• Bottled water non-student

• Pizza to non-student

• Jaffa cake to student

• Jaffa cake to non-student

• Cold sandwich non-student

• Cold sandwich non-student take away

• Vending machine coke

E/Z/S?

Exempt in canteen or canteen vending

Always standard rated

Exempt in canteen or canteen vending

Always standard rated

Always standard rated

Zero rated

Zero rated

Standard rated

Zero rated

Depends on location