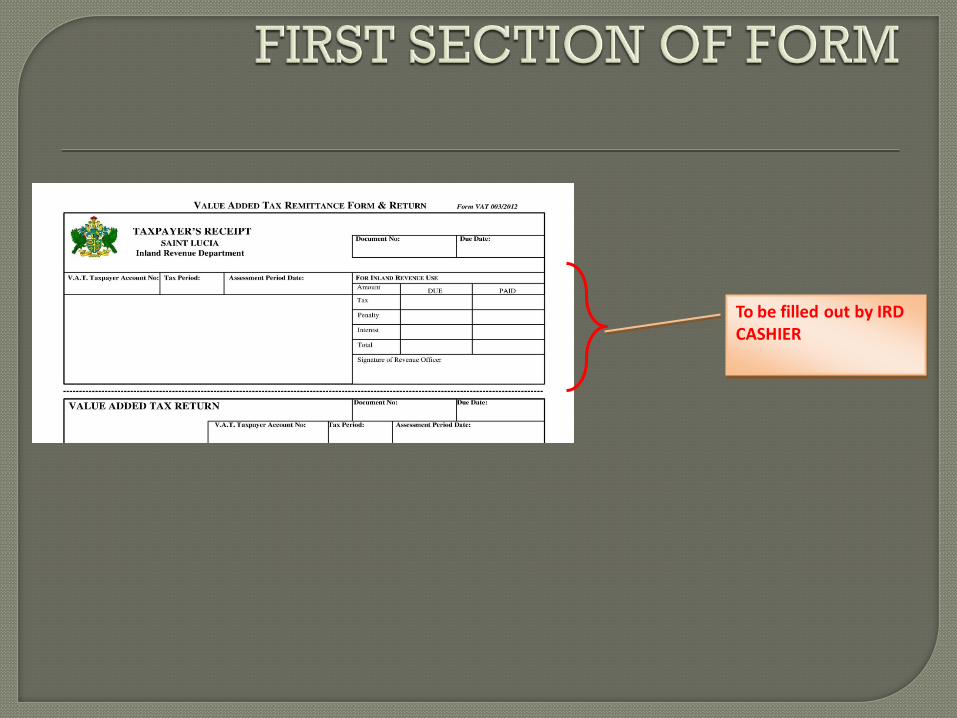

To be filled out by IRD CASHIER - VATvat.gov.lc/nc-cms/content/upload/VAT PRESENTATION... · To be...

18

Transcript of To be filled out by IRD CASHIER - VATvat.gov.lc/nc-cms/content/upload/VAT PRESENTATION... · To be...

To be filled out by IRD CASHIER

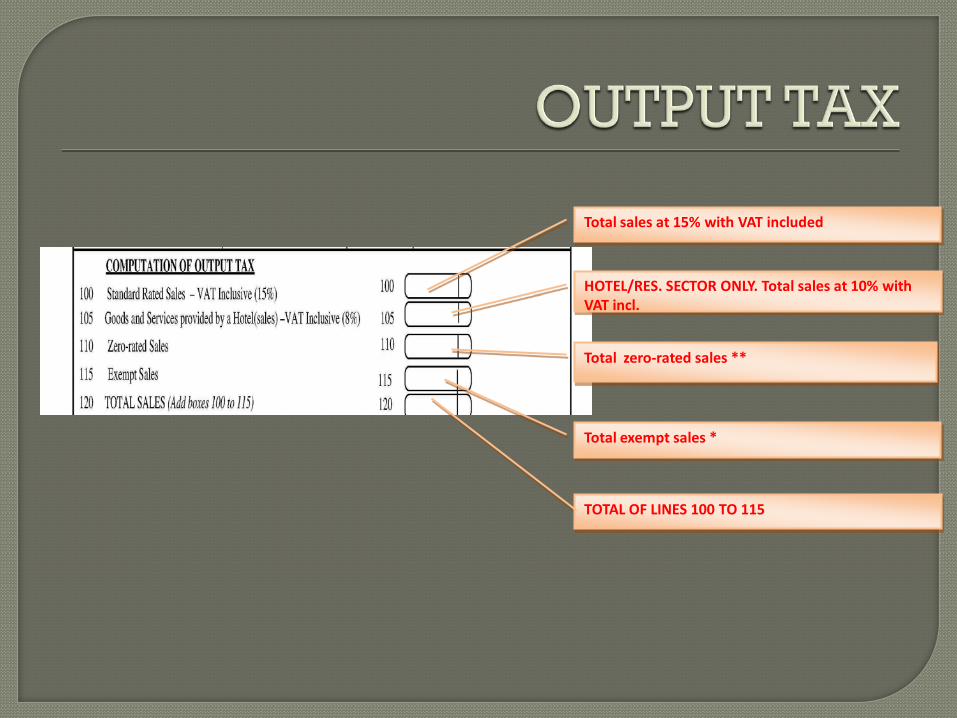

Total sales at 15% with VAT included

HOTEL/RES. SECTOR ONLY. Total sales at 10% with VAT incl.

Total exempt sales *

Total zero-rated sales **

TOTAL OF LINES 100 TO 115

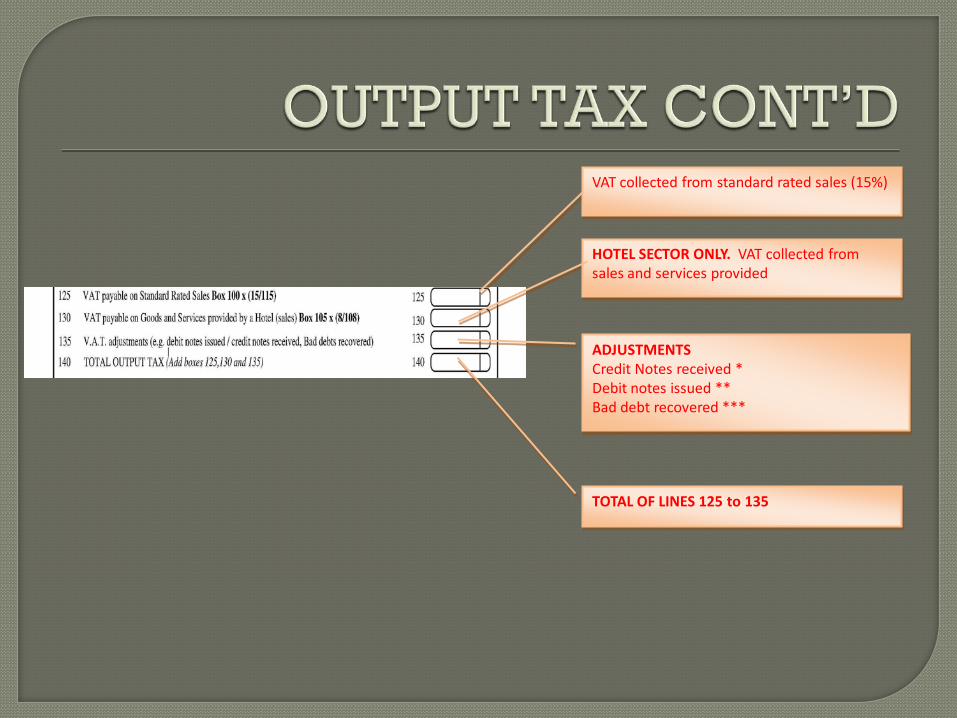

HOTEL SECTOR ONLY. VAT collected from sales and services provided

ADJUSTMENTSCredit Notes received *Debit notes issued **Bad debt recovered ***

TOTAL OF LINES 125 to 135

VAT collected from standard rated sales (15%)

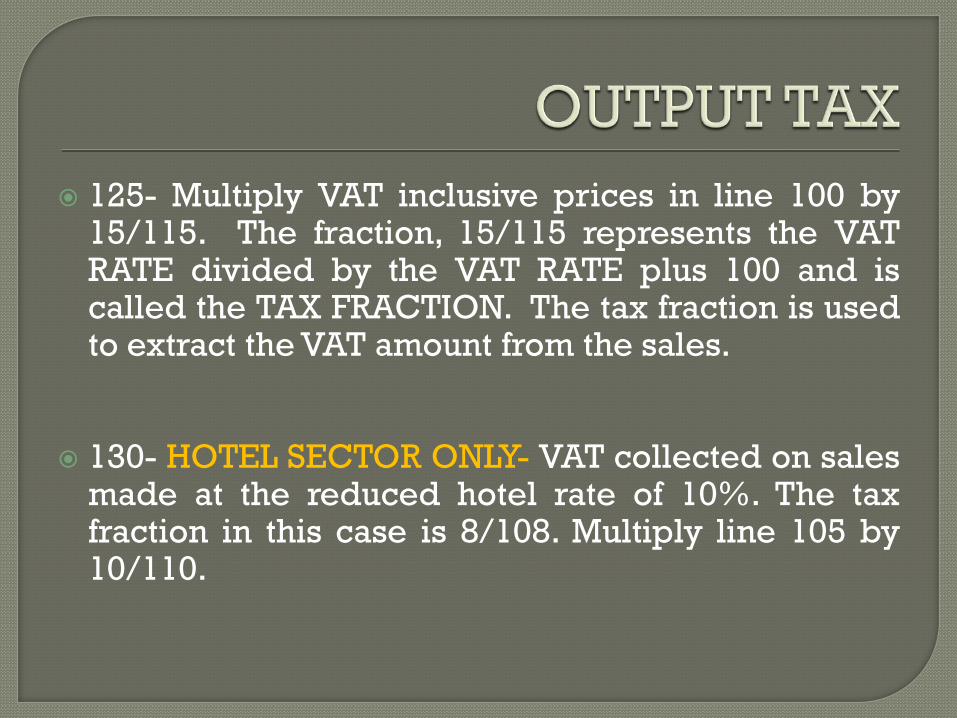

125- Multiply VAT inclusive prices in line 100 by15/115. The fraction, 15/115 represents the VATRATE divided by the VAT RATE plus 100 and iscalled the TAX FRACTION. The tax fraction is usedto extract the VAT amount from the sales.

130- HOTEL SECTOR ONLY- VAT collected on salesmade at the reduced hotel rate of 10%. The taxfraction in this case is 8/108. Multiply line 105 by10/110.

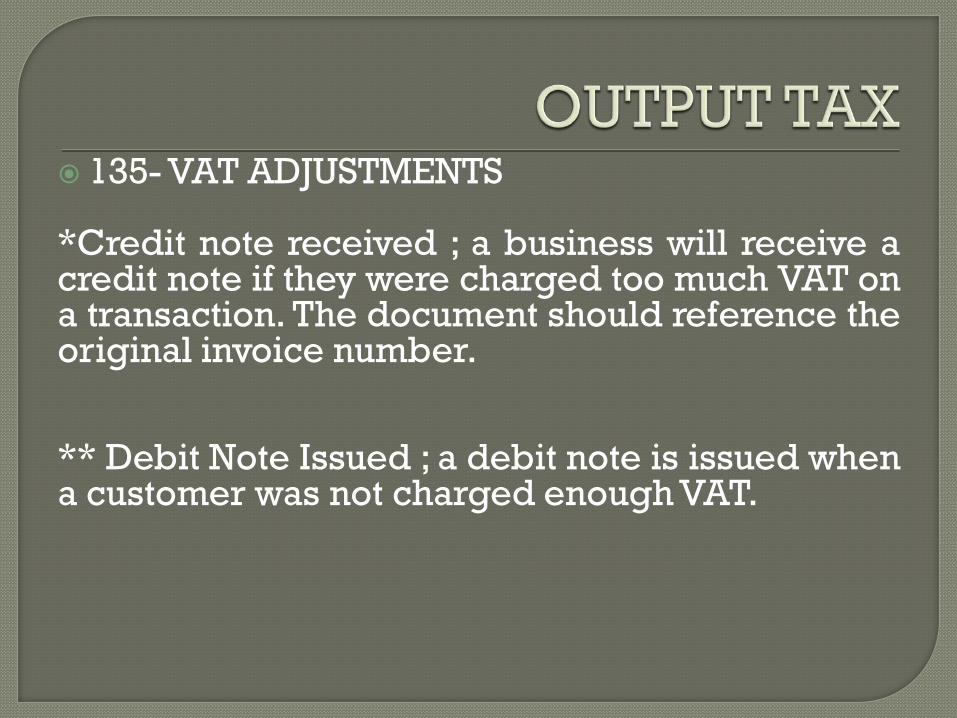

135- VAT ADJUSTMENTS

*Credit note received ; a business will receive acredit note if they were charged too much VAT ona transaction. The document should reference theoriginal invoice number.

** Debit Note Issued ; a debit note is issued whena customer was not charged enough VAT.

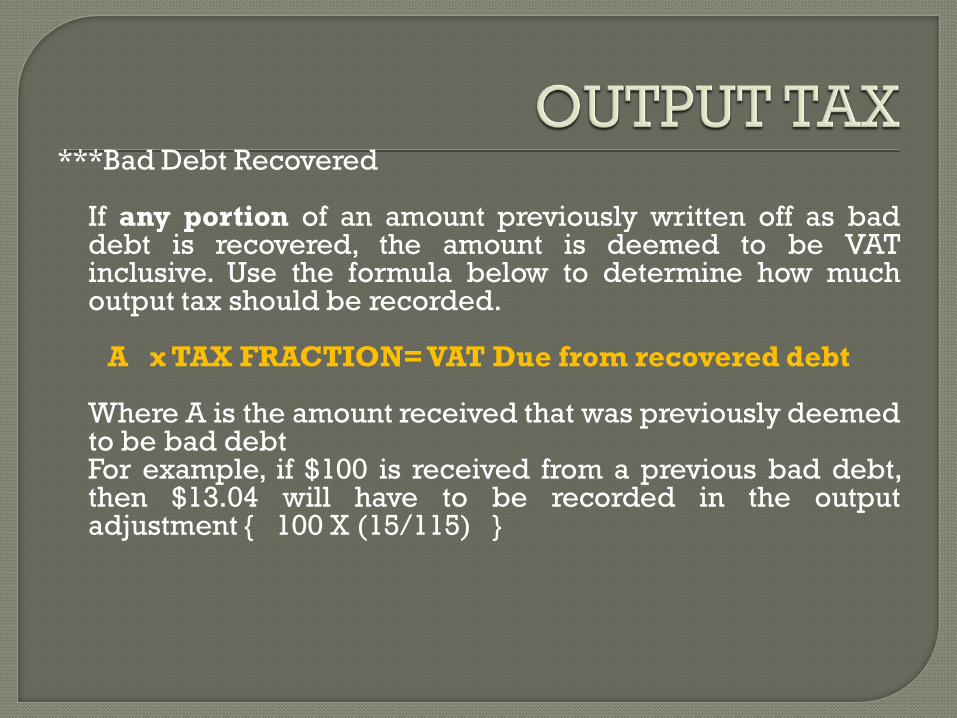

***Bad Debt Recovered

If any portion of an amount previously written off as baddebt is recovered, the amount is deemed to be VATinclusive. Use the formula below to determine how muchoutput tax should be recorded.

A x TAX FRACTION= VAT Due from recovered debt

Where A is the amount received that was previously deemedto be bad debtFor example, if $100 is received from a previous bad debt,then $13.04 will have to be recorded in the outputadjustment { 100 X (15/115) }

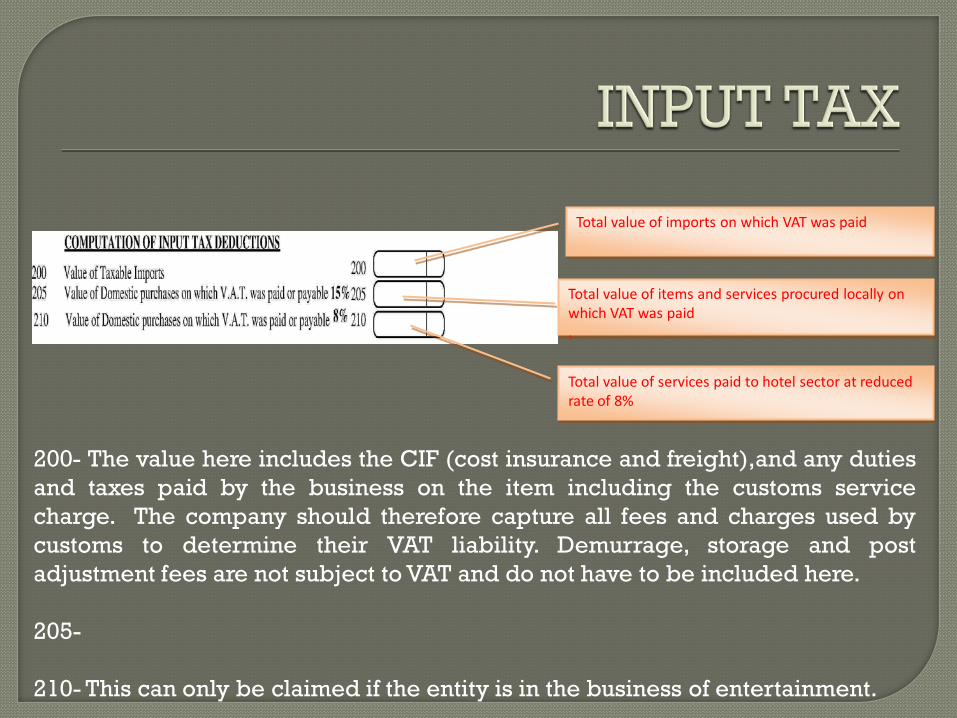

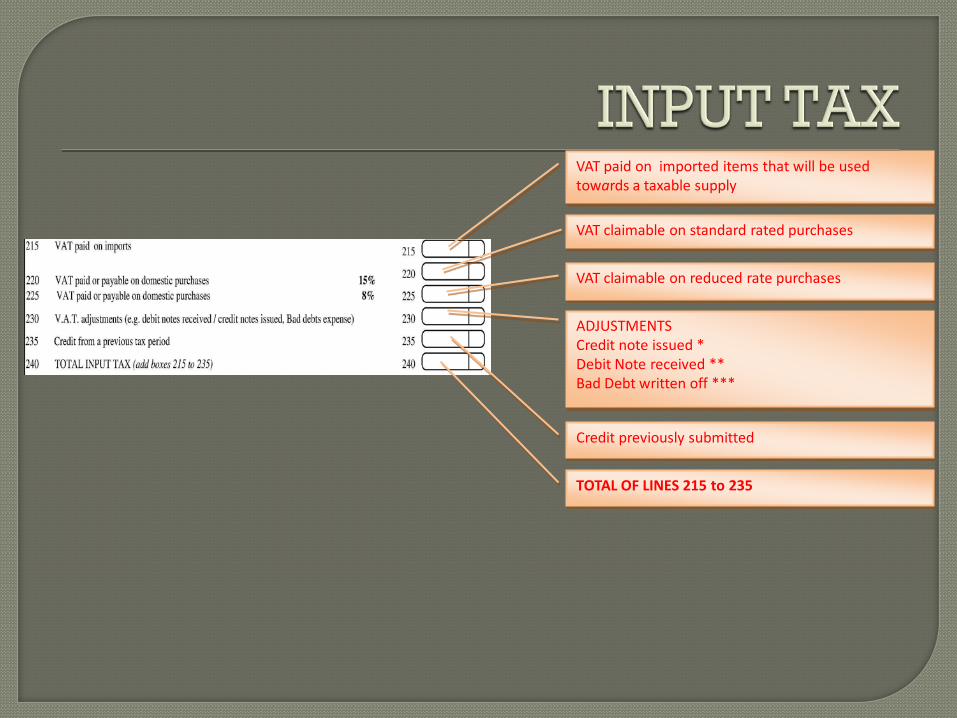

Total value of items and services procured locally on which VAT was paid.

Total value of services paid to hotel sector at reduced rate of 8%

Total value of imports on which VAT was paid

200- The value here includes the CIF (cost insurance and freight),and any dutiesand taxes paid by the business on the item including the customs servicecharge. The company should therefore capture all fees and charges used bycustoms to determine their VAT liability. Demurrage, storage and postadjustment fees are not subject to VAT and do not have to be included here.

205-

210- This can only be claimed if the entity is in the business of entertainment.

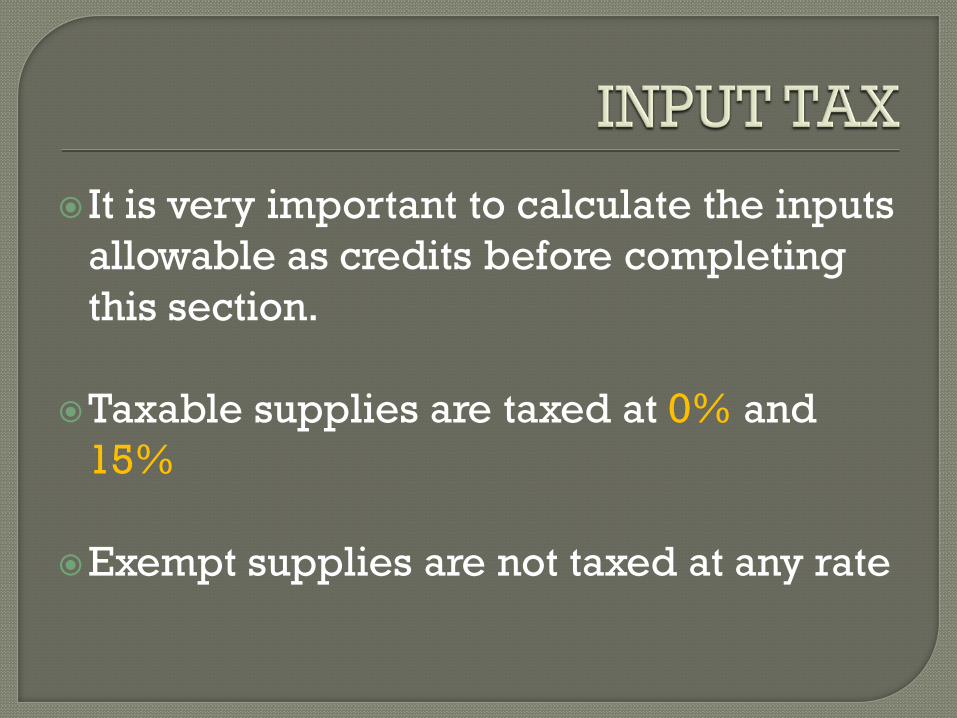

It is very important to calculate the inputs allowable as credits before completing this section.

Taxable supplies are taxed at 0% and 15%

Exempt supplies are not taxed at any rate

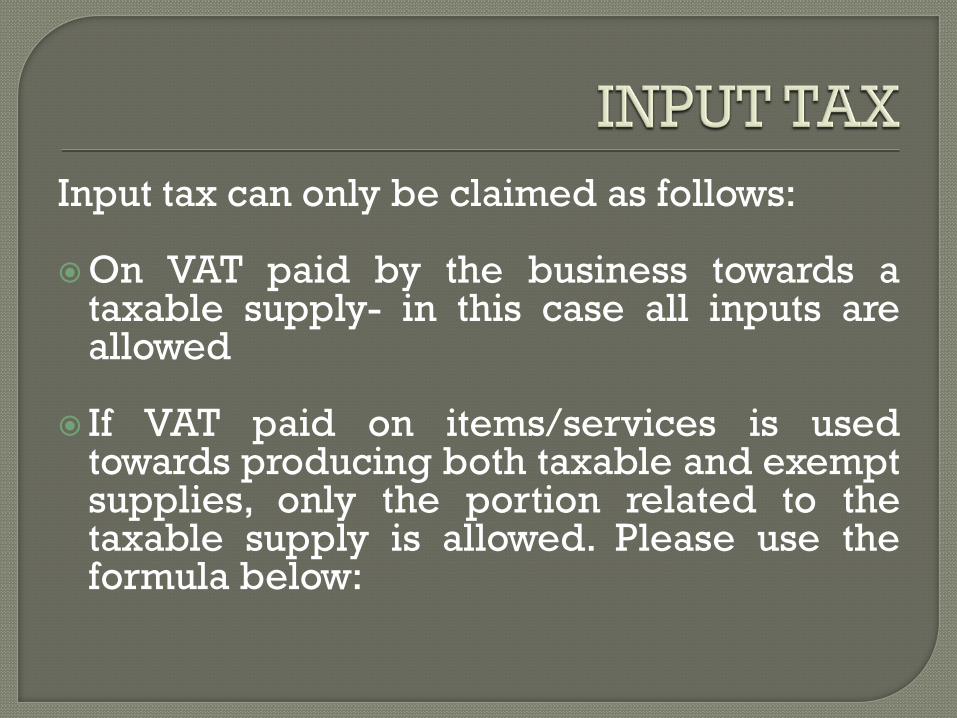

Input tax can only be claimed as follows:

On VAT paid by the business towards ataxable supply- in this case all inputs areallowed

If VAT paid on items/services is usedtowards producing both taxable and exemptsupplies, only the portion related to thetaxable supply is allowed. Please use theformula below:

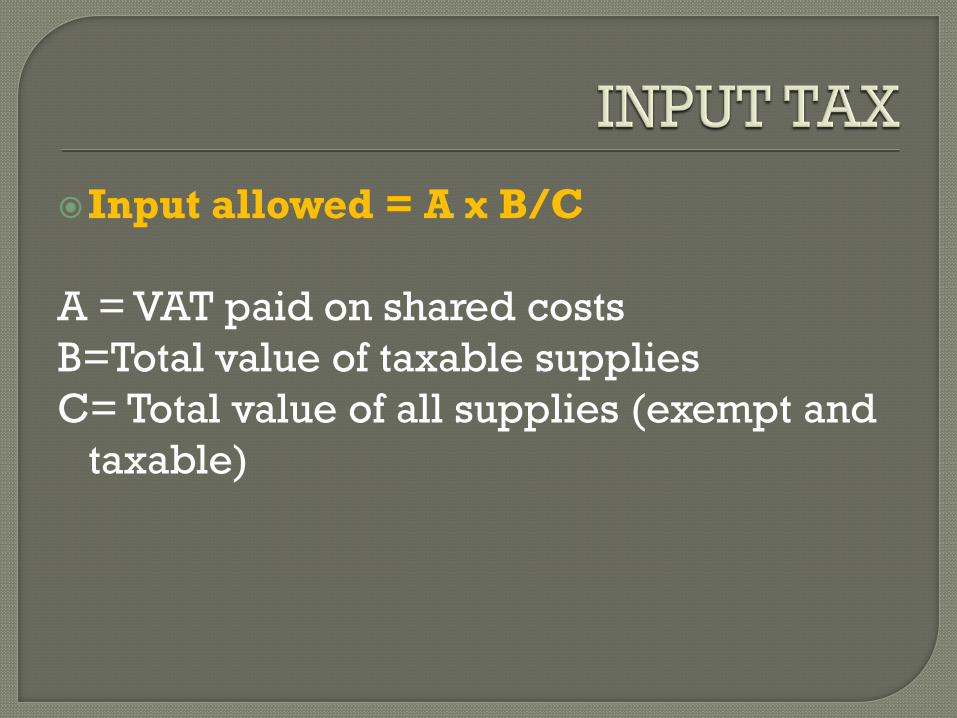

Input allowed = A x B/C

A = VAT paid on shared costsB=Total value of taxable suppliesC= Total value of all supplies (exempt and

taxable)

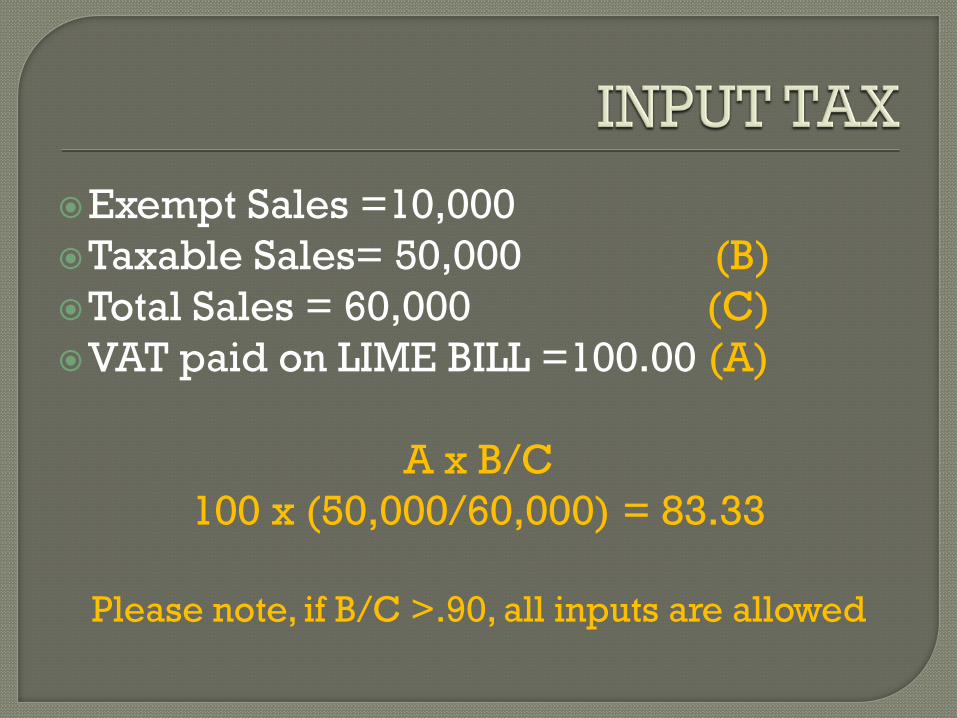

Exempt Sales =10,000Taxable Sales= 50,000 (B)Total Sales = 60,000 (C)VAT paid on LIME BILL =100.00 (A)

A x B/C100 x (50,000/60,000) = 83.33

Please note, if B/C >.90, all inputs are allowed

Please note that inputs are not allowed onpassenger vehicles unless the business is inthe business of renting vehicles. If thecompany owns a pick up truck, inputs willonly be allowed if the vehicle is used solelyfor business purposes.

Also note that food, beverages, tobacco,accommodation, amusement, recreation orother hospitality are not allowed unless thetaxpayer is the business of entertainment

VAT paid on imported items that will be used towards a taxable supply

VAT claimable on standard rated purchases

VAT claimable on reduced rate purchases

ADJUSTMENTSCredit note issued *Debit Note received **Bad Debt written off ***

Credit previously submitted

TOTAL OF LINES 215 to 235

230

Credit Notes are issued if a customer wascharged too much VAT.

Debit Notes are received when a company wasnot charged enough VAT.

Any amount of bad debt written off must becaptured here. The registered person owingshould be issued with a Credit Note as well.

235 - Credits from previous period must beincorporated into the equation to determine thetrue liability. Remember that filling out the returnis a matter of self assessment.

For example if the previous credit was $200 andthe company has to pay in $400 in output tax inthe subsequent period, then the company canuse the previous credit and pay in $200.

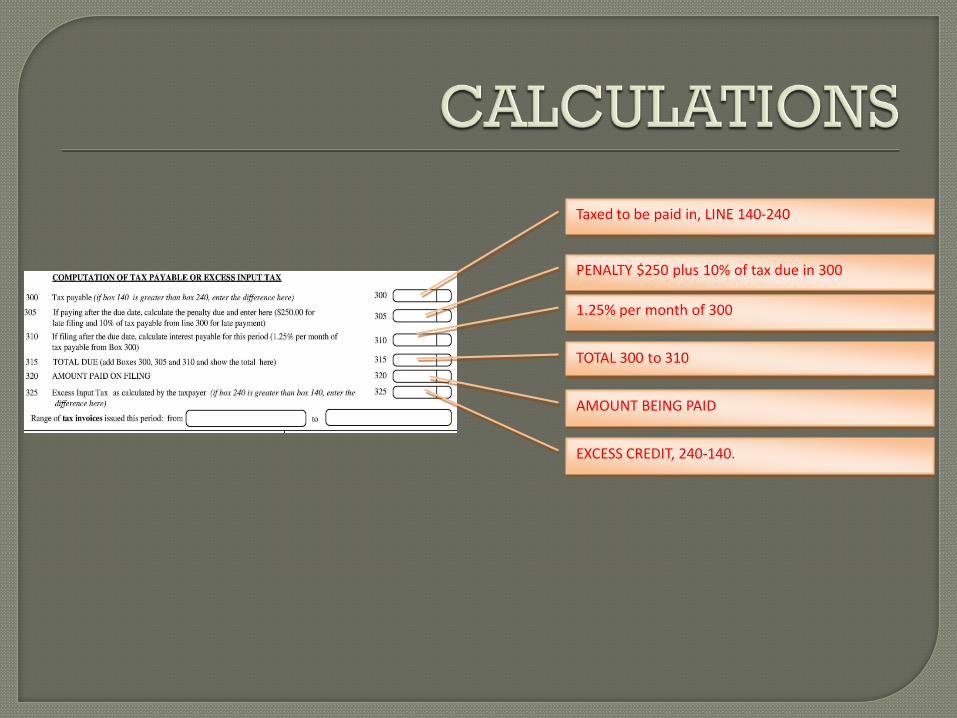

Taxed to be paid in, LINE 140-240

PENALTY $250 plus 10% of tax due in 300

1.25% per month of 300

TOTAL 300 to 310

AMOUNT BEING PAID

EXCESS CREDIT, 240-140.

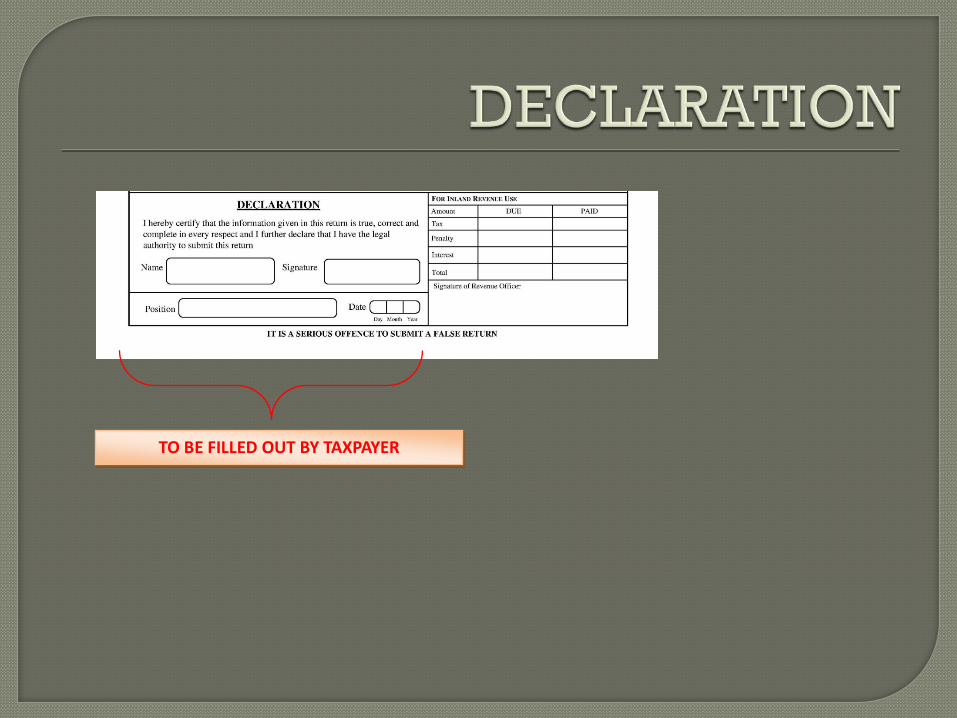

TO BE FILLED OUT BY TAXPAYER