Titre général de la présentation - Homepage - Ipsen …€¦ · JP Morgan 32nd Annual Healthcare...

28

Marc de Garidel – Chairman and CEO Claude Bertrand – CSO Ipsen JP Morgan 32 nd Annual Healthcare Conference 13-16 January 2014

Transcript of Titre général de la présentation - Homepage - Ipsen …€¦ · JP Morgan 32nd Annual Healthcare...

IPSEN pour nom de la société - 07/04/2011 / page 1

Marc de Garidel – Chairman and CEO

Claude Bertrand – CSO

Ipsen JP Morgan 32nd Annual Healthcare Conference

13-16 January 2014

2 Ipsen – JP Morgan 32nd Annual Healthcare Conference

This presentation includes only summary information and does not purport to be comprehensive.

Forward-looking statements, targets and estimates contained herein are for illustrative purposes only and

are based on management’s current views and assumptions. Such statements involve known and

unknown risks and uncertainties that may cause actual results, performance or events to differ materially

from those anticipated in the summary information. Actual results may depart significantly from these

targets given the occurrence of certain risks and uncertainties, notably given that a new product can

appear to be promising at a preparatory stage of development or after clinical trials but never be launched

on the market or be launched on the market but fail to sell notably for regulatory or competitive reasons.

The Group must deal with or may have to deal with competition from generic that may result in market

share losses, which could affect its current level of growth in sales or profitability. The Company

expressly disclaims any obligation or undertaking to update or revise any forward-looking statements,

targets or estimates contained in this presentation to reflect any change in events, conditions,

assumptions or circumstances on which any such statements are based unless so required by applicable

law.

All product names listed in this document are either licensed to the Ipsen Group or are registered

trademarks of the Ipsen Group or its partners.

The implementation of the strategy has to be submitted to the relevant staff representation authorities in

each country concerned, in compliance with the specific procedures, terms and conditions set forth by

each national legislation.

Disclaimer

3 Ipsen – JP Morgan 32nd Annual Healthcare Conference

The Group operates in certain geographical regions whose governmental finances, local currencies or

inflation rates could be affected by the current crisis, which could in turn erode the local competitiveness

of the Group’s products relative to competitors operating in local currency, and/or could be detrimental to

the Group’s margins in those regions where the Group’s drugs are billed in local currencies.

In a number of countries, the Group markets its drugs via distributors or agents: some of these partners’

financial strength could be impacted by the crisis, potentially subjecting the Group to difficulties in

recovering its receivables. Furthermore, in certain countries whose financial equilibrium is threatened by

the crisis and where the Group sells its drugs directly to hospitals, the Group could be forced to lengthen

its payment terms or could experience difficulties in recovering its receivables in full.

Finally, in those countries in which public or private health cover is provided, the impact of the financial

crisis could cause medical insurance agencies to place added pressure on drug prices, increase financial

contributions by patients or adopt a more selective approach to reimbursement criteria.

All of the above risks could affect the Group’s future ability to achieve its financial targets, which were set

assuming reasonable macroeconomic conditions based on the information available today.

Safe Harbor

4 Ipsen – JP Morgan 32nd Annual Healthcare Conference

Drug sales by segment

Specialty

care

42%

Primary

Care(*)

58%

France

43% Rest of

the world

50%

EM(2)

7% France

20%

Rest of the world

60%

EM(2)

20%

2002 2012

2002 2012 CAGR(1) 2002-2012

Primary care(*) -1%

Specialty care +12%

Emerging markets(2) +18%

Rest of the world +8%

France -2%

Drug sales by geography

(*) Including Drug-related sales (1) Compound Annual Growth Rate

(2) Main emerging markets: China, Russia and Brazil

CAGR(1) 2002-2012

€1,220m €699m

€1,220m €699m

Over the last decade, Ipsen has succeeded in adapting to a fast changing environment

Specialty

care

71%

Primary

care

29%(*)

5 Ipsen – JP Morgan 32nd Annual Healthcare Conference

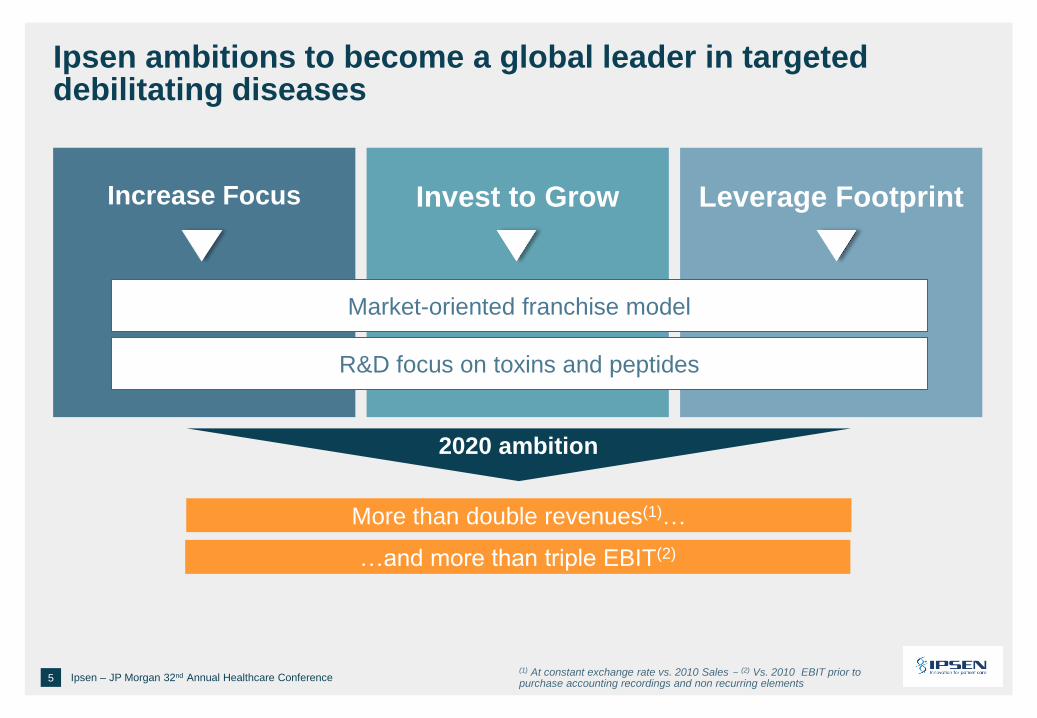

Increase Focus Invest to Grow Leverage Footprint

Market-oriented franchise model

R&D focus on toxins and peptides

(1) At constant exchange rate vs. 2010 Sales - (2) Vs. 2010 EBIT prior to purchase accounting recordings and non recurring elements

More than double revenues(1)…

…and more than triple EBIT(2)

2020 ambition

Ipsen ambitions to become a global leader in targeted debilitating diseases

6 Ipsen – JP Morgan 32nd Annual Healthcare Conference

1

2

3

4

2013, healthy performance in a challenging year

R&D delivering

Ipsen to launch Somatuline® in NET in the US

Concluding remarks and 2014 outlook

Executive summary

2013, healthy performance in a

challenging year

Marc de Garidel Chairman and CEO

8 Ipsen – JP Morgan 32nd Annual Healthcare Conference

6.0

29.4

48.7

92.2

10.7

12.5

42.3

186.3

186.6

222.9

Nisis /Nisisco

Forlax

Tanakan

Smecta

Hexvix

Increlex

Nutropin

Dysport

Somatuline

Decapeptyl

French primary care: (22.3%)

Sp

ec

ialt

y c

are

P

rim

ary

ca

re

®

®

®

®

®

®

®

®

®

+7.1%

+10.5%

(3.5%)

(20.2%)

+12.0%

+6.8%

0.2% ®

®

International primary care: +12.2%

+19.2%

(64.2%)

(41.4%)

Specialty care

€661.3m

+3.0%

Primary care

€242.6m

(1.3%)

Drug sales

€903.9m

+1.8%

Specialty care sales growth impacted by Decapeptyl® performance and Increlex® shortage

Increlex® resupplied in Europe

c.€15 million top-line FX impact in the first 9 months, partly flowing down to EBIT

Drug sales - 9M 2013 in million euros - % excluding foreign exchange impacts

9 Ipsen – JP Morgan 32nd Annual Healthcare Conference

Decapeptyl® sales in 9M 2013 impacted by headwinds in China and Europe

Europe

Top 4 negative

contributors

China Other

9M 2013 9M 2012

9M Decapeptyl sales

in million euros at constant currency Poland: price cuts and patient co-payment

France: consequences of French PC restructuring plan

Greece: price cuts & aggressive competitive landscape

Italy: price cuts & contracting market

231.1

222.9

(9.4)

(2.1) 3.3

Headwinds in Europe as anticipated

China below expectation, situation improving in Q4

10 Ipsen – JP Morgan 32nd Annual Healthcare Conference

Stabilizing Primary care driven by strong growth in emerging countries and slowdown of French decline

-40%

-30%

-20%

-10%

0%

10%

Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013

YoY growth rate at

current exchange rate

Evolution of quarterly Primary care sales

Global

France

Two 7.5% consecutive price cuts on Smecta® in France in 2014

Risk of Smecta® generic in France

New distribution model for Smecta® in Algeria

Dynamic international growth

Slowdown of French decline

Remaining challenges Recent trends

11 Ipsen – JP Morgan 32nd Annual Healthcare Conference

Successful R&D

execution

2013 key achievements beyond sales

New

organization

/execution

Successful

Business

development

New governance and organization (Split of Primary and Specialty care

businesses) to accelerate execution of the strategy

Successful completion of Primary care France and US Dysport® restructuring

Good cost control

Successful closing of Inspiration sale

CLARINET® positive results

AUL positive initial results

ELECT ® initial results

Acquisition of Syntaxin

French primary care partnership with Mayoly Spindler

Acquisition of Sativex® distribution rights for LatAm

R&D delivering

Claude Bertrand CSO

13 Ipsen – JP Morgan 32nd Annual Healthcare Conference

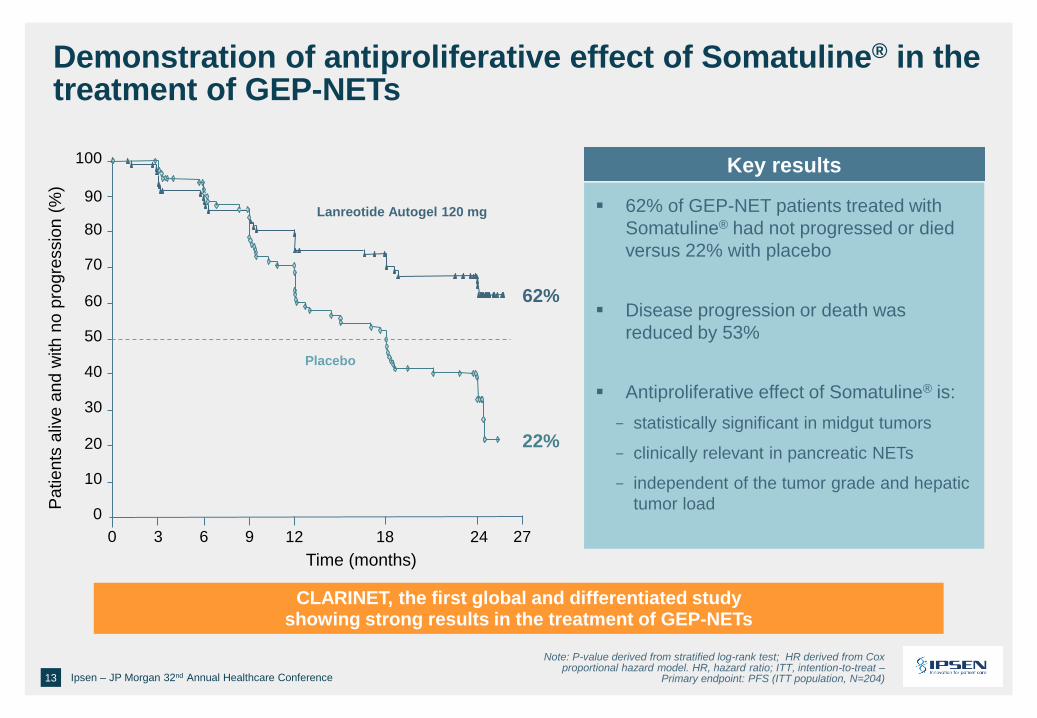

Demonstration of antiproliferative effect of Somatuline® in the treatment of GEP-NETs

Lanreotide Autogel 120 mg

Placebo

0 3 6 9 12 18 24 27

0

10

20

30

40

50

60

70

80

90

100

Patients

aliv

e a

nd w

ith n

o p

rogre

ssio

n (

%)

Time (months)

62%

22%

CLARINET, the first global and differentiated study showing strong results in the treatment of GEP-NETs

62% of GEP-NET patients treated with

Somatuline® had not progressed or died

versus 22% with placebo

Disease progression or death was

reduced by 53%

Antiproliferative effect of Somatuline® is:

- statistically significant in midgut tumors

- clinically relevant in pancreatic NETs

- independent of the tumor grade and hepatic

tumor load

Key results

Note: P-value derived from stratified log-rank test; HR derived from Cox proportional hazard model. HR, hazard ratio; ITT, intention-to-treat –

Primary endpoint: PFS (ITT population, N=204)

14 Ipsen – JP Morgan 32nd Annual Healthcare Conference

From natural BoNT expertise…

Scale-up

Pharmaco-

logical Manufacturing

Pre-clinical /

Clinical Development

Established

network of

BoNT experts

Recombinant

technology

Toxin

engineering

Intellectual

property

Targeted

Secretion

Inhibitors

Ipsen

Syntaxin

… to full recombinant potential

Highly complementary acquisition

Integration on track

Ipsen’s R&D toxin platform significantly reinforced by Syntaxin acquisition

Potential to

combine

toxins

and peptides

15 Ipsen – JP Morgan 32nd Annual Healthcare Conference

Positive initial results for Dysport® in Adult Upper Limb spasticity

243 adult hemiparetic spastic patients

Multicentric, prospective, double blind,

randomised, and placebo-controlled

Treatment with Dysport® showed a

statistically significant and clinically

meaningful improvement in:

─ Muscle tone

─ Clinical benefit

Safety profile consistent with the known

safety profile of Dysport®

Aesthetic use (marketed by Valeant)

Cervical Dystonia (marketed by Ipsen)

Adult Upper Limb (Positive initial results)

Pediatric Upper Limb (Study site initiation started)

Adult Lower Limb (PhIII results expected end of 2014)

Pediatric Lower Limb (PhIII results expected end of 2014)

Potential expansion of Dysport® indications

in the US Initial results

Full results to be disclosed in the coming months at major international congresses

16 Ipsen – JP Morgan 32nd Annual Healthcare Conference

Ipsen, potentially the first company to launch a ready-to-use toxin A with Dysport® Next Generation

First ready-to-use toxin A formulation

Full product range

Improved focus on patient care

Ability to reach more patients in need of treatment

Key characteristics

2 separate regulatory pathways

One single formulation accepted per API

Interchangeability of formulations to be addressed

Acceptance of several formulations per API

Equivalence to be demonstrated between both formulations of the same toxin

US Europe

17 Ipsen – JP Morgan 32nd Annual Healthcare Conference

Ipsen’s R&D reinforced through partnerships

ENDO-CRINOLOGY

ONCOLOGY

NEUROLOGY

2003 - 2005 2006 - 2013

Tasquinimod, an illustration of Ipsen’s R&D open model

18 Ipsen – JP Morgan 32nd Annual Healthcare Conference

Tasquinimod, a new first-in-class oral anti-cancer therapy

Tasquinimod, potentially a new therapeutic option for chemo naïve patients

with metastatic CRPC

A unique MoA targeting the tumor’s microenvironment,

mainly by binding the S100A9 protein

(1) Adapted from Raymond et al, Cancer Chemother Pharmacol, 2013

Ipsen to launch Somatuline®

in NET in the US

Marc de Garidel Chairman and CEO

20 Ipsen – JP Morgan 32nd Annual Healthcare Conference

Somatuline® well positioned in the US to seize significant NET opportunity

Differentiated NET data package with CLARINET®

Differentiated product/presentation with ~ 50% market in acromegaly(1)

Long acting formulation setting barrier for potential new entrants

2013 potential addressable market

c.$600m* c.$100m*

Ipsen

addressable market

x6

Acromegaly + NET

Acromegaly

(1) Somatuline® market share in acromegaly SSA market *Ipsen 2013 estimates (SSAs only)

21 Ipsen – JP Morgan 32nd Annual Healthcare Conference

Ipsen to launch Somatuline® in NET indication in the US to capture full value

Maintain full control over decisions

Build long term presence in US oncology

Secure Ipsen US strategic presence

Secure long term value

Impact

Expected maximum incremental

annual cost of €[30-40]m

US breakeven(1) postponed to

2017

Further cost containment initiatives to minimize impact on overall Group profitability

Rationale

Leverage global product expertise

(1) Commercial contribution, excluding revenues from Valeant Pharmaceuticals Intl Inc. and Increlex® sales

Concluding remarks and 2014 outlook

Marc de Garidel Chairman and CEO

23 Ipsen – JP Morgan 32nd Annual Healthcare Conference

Share price (€)

Note: CAC 40 and STOXX Europe TMI Pharma. have been rebased at Ipsen share price of 02/01/2013

15

20

25

30

35

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13

Ipsen STOXX Europe TMI Pharmaceuticals CAC 40

Ipsen share price up 50% in 2013, reflecting good momentum

+50%

+20%

+18%

24 Ipsen – JP Morgan 32nd Annual Healthcare Conference

Recurring adjusted(*)

operating margin Unchanged at around 16.0% of sales

– The Group continues to implement productivity measures while maintaining investment in R&D

– Benefits from the new organization of French primary care and US commercial operations expected to

materialize in 2014

2013 financial objectives confirmed

Primary care

Drug sales Decline of approximately -1.0% year-on-year

Specialty care

Drug sales Growth of approximately +3.0% year-on-year

– Realignment of the Decapeptyl® inventory situation in the distribution chain

– Launch of new Decapeptyl® local competitors

– Recent disruption in the Chinese market

Excluding further major deterioration of the Chinese and Middle Eastern markets

China

Middle East – Continued exceptional political situation in certain Middle Eastern countries

Note: the above sales growth objectives are set at constant currency. All the above objectives are set excluding major negative unforeseeable events, notably significant currency fluctuations in the context of

currency depreciation in certain emerging countries – (*) Prior to non-recurring expenses

25 Ipsen – JP Morgan 32nd Annual Healthcare Conference

Peptides Toxins

Dysport® NG GL

PhII results

Dysport® NG CD

PhIII results

H1 2014

A rich R&D news flow expected in 2014

Tasquinimod PhIII results

(PFS and OS data)

Uro-Oncology Endocrinology Neurology

Dysport® AUL full

PhIII data

Note: PFS = progression-free survival – OS = overall survival – CD = cervical dystonia – AUL = adult upper limb – PLL = pediatric lower limb – ALL = Adult lower limb

Dysport® NG

Preliminary stability data

Dysport® ALL and PLL

PhIII topline data

Somatuline® ELECT

PhIII full data Tasquinimod PhII results

Exploratory study in HCC,

RCC, Gastric cancer &

Ovarian cancer

H2 2014

Expected WW filing of

Somatuline® in GEP NETs

Expected filing of Dysport® in

AUL indication in the US

26 Ipsen – JP Morgan 32nd Annual Healthcare Conference

Differentiated presentation to gain market share

Spasticity

Ph III in adult upper limb

Dysport® Next Generation

Ph III in cervical dystonia (Europe)

tasquinimod

Ph III in mCRPC

(WW excl. US and Japan)

CLARINET Ph III

GEP-NET antitumoral effect (WW) Somatuline®

tasquinimod

Dysport®

Product Growth drivers Corresponding addressable

market

[€1.3bn - €1.5bn](3)

> €200m(2)

[€400m - €600m](1)

Pipeline molecules to significantly increase Ipsen’s market opportunity

Increased market opportunity in the context of fast growing markets

(1) IMS 2012 and SmartAnalyst 2010 – (2) Ipsen analysis (3) Decision Resources: in Ipsen territories and excl. GnRh analogs market

* NET associated with carinoide syndrome

27 Ipsen – JP Morgan 32nd Annual Healthcare Conference

R&D engine delivering

Strategic decision to invest in the US with Somatuline® launch in NET

2013, healthy performance in a challenging year

Key takeaways

Specialty care impacted by non-recurring elements in 2013, looking forward to a

smoother 2014…

Thank You