Title of Session Line 1 Title of Session Line 2€¦ · · 2014-10-08– Optimize maintenance...

17

Account Based Processing, Open Payments and Mobile David deKozan Vice President, Strategic Initiatives Cubic Transportation Systems, Inc. San Diego, CA

Transcript of Title of Session Line 1 Title of Session Line 2€¦ · · 2014-10-08– Optimize maintenance...

Account Based Processing, Open Payments and Mobile

David deKozanVice President, Strategic Initiatives

Cubic Transportation Systems, Inc.

San Diego, CA

Key Themes

How did we get here?

– AFC 101 in 10 minutes or less

Evolution or Revolution?

– Established vs. green field systems

Getting from Here to There

– Public Contracting and Transition Management

Lessons from The Trenches

– Card based

– Account based

– Open Payments

– Mobile

How did we get here? Automatic Fare Collection Objectives

– Streamline and accelerate fare payment process

– Automate and minimize cash handling

– Integrate payment and access control functions

– Simplify terminal interaction

– Enable creative fare tariffs while minimizing confusion

– Facilitate fare media and fare product distribution

– Promote connected journeys

– Create linkages across operators

– Collect and report on ridership

– Collect and report on revenues

– Optimize maintenance operations

– Graceful system degradation

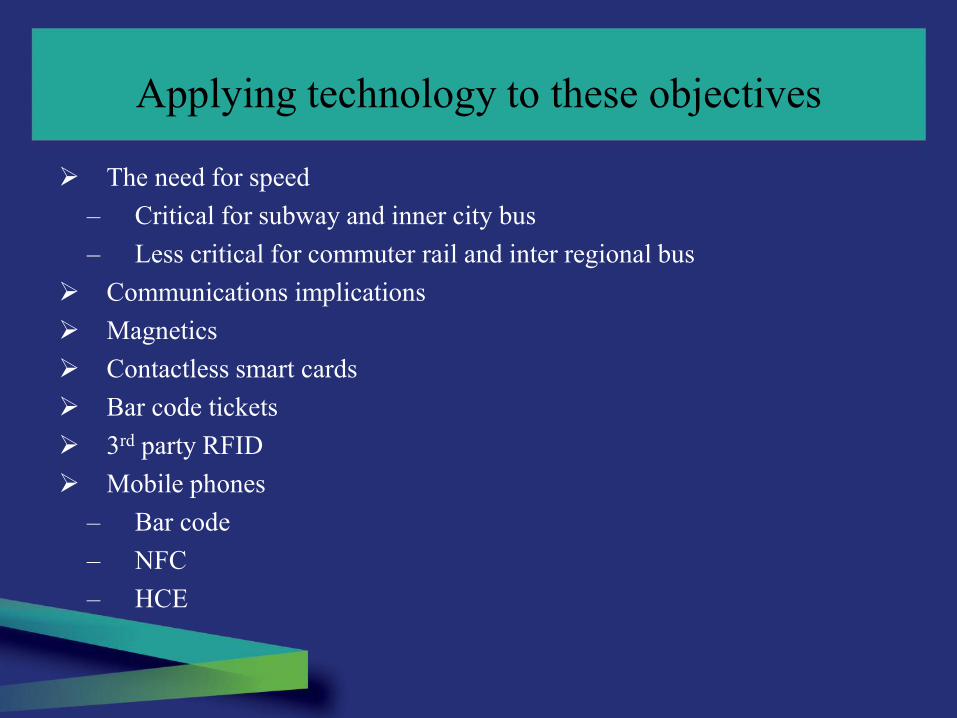

Applying technology to these objectives

The need for speed

– Critical for subway and inner city bus

– Less critical for commuter rail and inter regional bus

Communications implications

Magnetics

Contactless smart cards

Bar code tickets

3rd party RFID

Mobile phones

– Bar code

– NFC

– HCE

Card Based Processing

Benefits Challenges

Distributed transactional logic Greater terminal demands = more $

Store and Forward Short list of suppliers

High Speed Fare rule changes require system wide table update

Instant feedback Limited card options

No transactional risk Harder to partner with other verticals

Proof of payment Customer must acquire and load media

Can leverage NFC technology Must establish TSM linkages and supporting apps

The majority of established systems- does not require

real time comms

Account Based Processing

Benefits Challenges

Easier to update fare rules Slower

More terminal options and lower $ Real time communications = more $

Easier to partner with other verticals Limited customer feedback at terminal

A Variety of RF token options Greater transactional risk

Enables Open Payments

Reduced need to acquire and load media

Flexibility in how to address challenges

Now feasible with the latest in comms tech- changes the overall processing architecture

Contactless Open Payments

Benefits Challenges

Contactless Bank card can be used as a pre-paid token Dependent upon issuer strategies

Contactless Bank card can be accepted with no pre-paid account (PAYG) Dependent upon issuer strategies

NFC Mobile wallets can be accepted Wallet application OH takes too much time

No need for registration or pre-purchase may lift sales Requires terminal certification and maintenance

Simplicity for infrequent usersIncreased PCI compliance demands

Ease of flow for special eventsDecreased flexibility

Potential increases in transactional risk

Chicago Ventra- A Case Study"CTA performance report- February 14, 2014".

Tap times Count Percent Cumulative

0.5 seconds and

under 21,966,213 69.74%

96.54%

0.6 seconds – 1.0

seconds 8,440,555 26.80%

1.1 seconds – 2.5

seconds 1,079,568 3.43% 3.43%

Over 2.5 seconds

10,763 0.03% 0.03%

Transaction times- Rail

Chicago Ventra- A Case Study"CTA performance report- February 14, 2014".

Tap times Count Percent Cumulative

0.5 seconds and

under 23,381,510 62.62%

67.71%

0.6 seconds – 1.0

seconds 1,899,901 5.09%

1.1 seconds – 2.5

seconds 12,037,232 32.24% 32.24%

Over 2.5 seconds 18,483 0.05% 0.05%

Transaction Times- Bus

Ventra Accounts as of Feb 11

Ventra 767,563

RTA 294,436

Student/UPASS 243,377

Other 13,832

Much of your ridership will require dedicated media regardless of architecture

More than 1.4M accounts opened since September

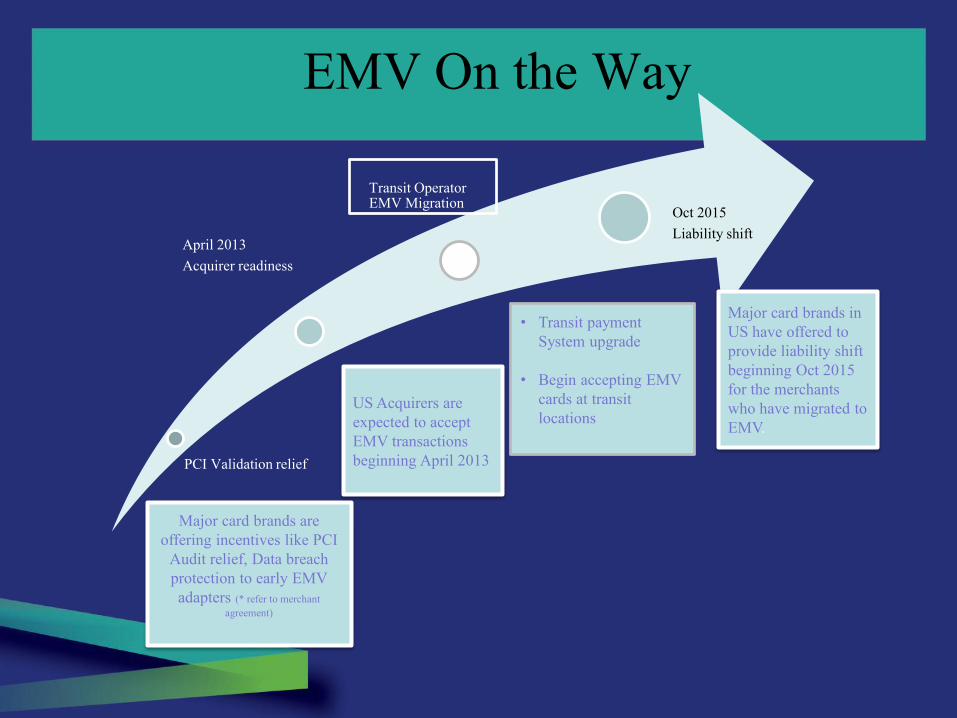

Major card brands are

offering incentives like PCI

Audit relief, Data breach

protection to early EMV

adapters (* refer to merchant

agreement)

EMV On the Way

PCI Validation relief

April 2013

Acquirer readiness

Transit Operator EMV Migration

Oct 2015

Liability shift

US Acquirers are

expected to accept

EMV transactions

beginning April 2013

• Transit payment

System upgrade

• Begin accepting EMV

cards at transit

locations

Major card brands in

US have offered to

provide liability shift

beginning Oct 2015

for the merchants

who have migrated to

EMV.

EMV Off-line Transaction Security

SDA/DDA/CDA

Card Authentication

• Offline CAM (Card Authentication)

• Offline CVM (Cardholder

Verification)

• Offline Authorization

*Source – EMV Migration forum

What are your regional card issuers doing?

Contactless MSD vs. EMV

Contactless MSD on hold?

Will EMV be contactless?

Key EMV considerations for Transit

– Automated Transaction Counter Synch

– Deferred Authorization Risk

• Local Authentication?

• Local Authorization?

– ID and PAN Tracking

– Card Not Present fraud

If the brands/issuers don’t accommodate then what?

What about Mobile?

Mobile responds to several facets of AFC

– Customer service• Real Time Passenger Information

• Card/Account management

• Trip planning and related tariffs

– Fare product sales• Payment optimization

– Media distribution

Advantages and Dis-AdvantagesApproach Advantage Dis-Advantage

Legible Script/Icons Low Cost Limited Data

No hardware required Increased fraud potential

2D Bar Code Low Cost, no required AFC

integration

Requires new hardware and/or

parallel back office and limited data

integration

Ability to authenticate and cancel

tickets

Ergonomic and transactional speed

challenges

NFC Transit Card High speed and compatible with

existing infrastructure

Requires commercial agreements

with SE owners

Familiar use case…just tap Requires TSM integration and

appropriate app infrastructure

NFC Token Lower provisioning costs Need account based back office

Familiar use case May need TSM engagement

NFC Bankcard Convenient for impulse users Use Case Overhead

Summary Observations

There is no one right answer

While the migration from card based to account based has

begun it will take time

– It may not make sense for everyone

– Public procurement by its nature is time consuming

There are interim steps that can be taken most

significantly using mobile

There are still a lot of questions about contactless

payments and the best way to leverage them

The keys to success will be balancing new benefits

against transition strategies and operator specific

needs/objectives

David L. deKozan

Vice President, Strategic Initiatives

Cubic Transportation Systems, Inc.