Title of report/proposal - Home - Ofcom · Non-Confidential November 2014 | Frontier Economics 5...

28

© Frontier Economics Ltd, London. An analysis of certain aspects of BT’s response to Ofcom’s VULA consultation A REPORT PREPARED FOR TALKTALK (NON-CONFIDENTIAL) November 2014

Transcript of Title of report/proposal - Home - Ofcom · Non-Confidential November 2014 | Frontier Economics 5...

© Frontier Economics Ltd, London.

An analysis of certain aspects of BT’s

response to Ofcom’s VULA

consultation A REPORT PREPARED FOR TALKTALK (NON-CONFIDENTIAL)

November 2014

Non-Confidential November 2014 | Frontier Economics i

Contents

An analysis of certain aspects of BT’s

response to Ofcom’s VULA

consultation

1 Introduction and summary 3

2 There is a strong case for using a bright-line test 6

The suggested differences between the approaches proposed by BT

and Ofcom should not be expected to be material ..................... 7

The available evidence suggests that existing remedies would be

insufficient .................................................................................. 9

Ofcom should not need to carry out an “effects-based” analysis at this

stage ........................................................................................ 11

Suggestions that recent market developments show an ex ante test is

not required should be treated with caution ............................. 12

Competition from Virgin does not remove the need for an ex-ante

margin test ............................................................................... 13

It is likely to be challenging to implement a dynamic test ................... 13

3 It is appropriate to include the cost of BTS within the

margin tests 15

It is unlikely that the cost of acquiring BT’s sports right overstates the

value that consumers attach to these rights ............................. 16

CL understates the number of customers that need to be contestable to

prevent competition from being distorted ................................. 18

Consumers’ heterogeneous valuation of BTS is consistent with (a)

a need to adopt disaggregated tests and (b) a larger

proportion of the costs of BTS being recovered from fibre

customers 22

ii Frontier Economics | November 2014 Non-Confidential

Tables & Figures

An analysis of certain aspects of BT’s

response to Ofcom’s VULA

consultation

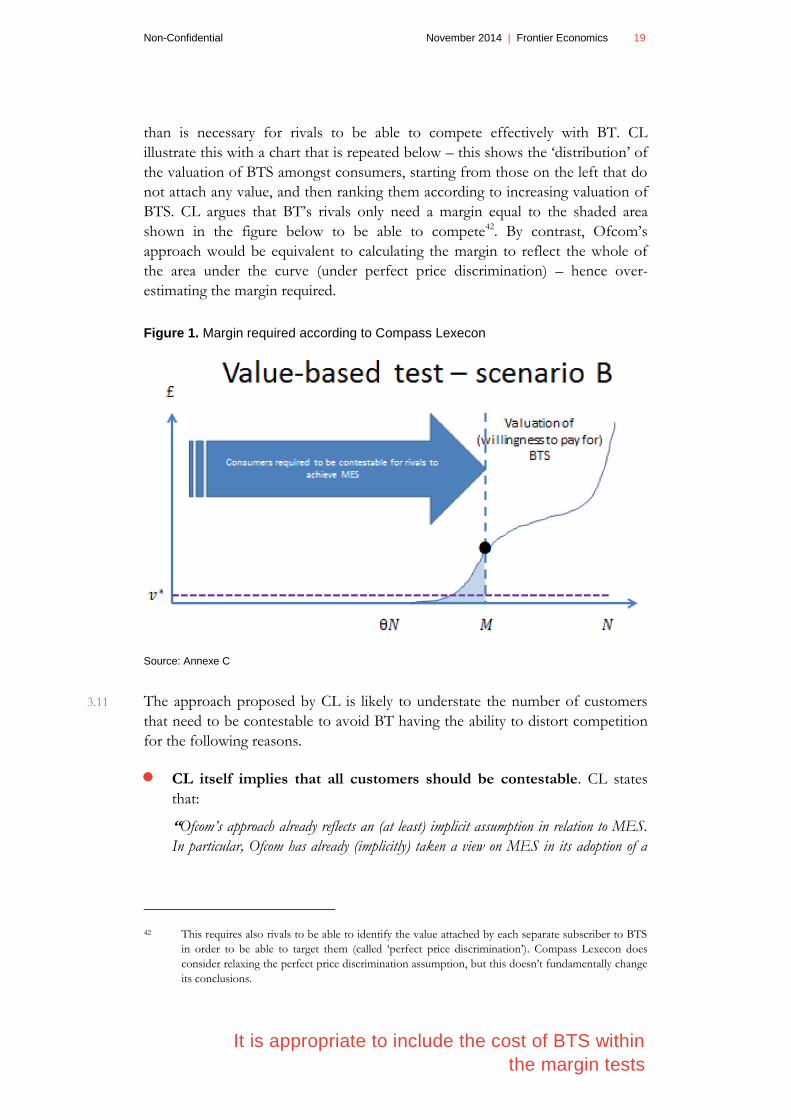

Figure 1. Margin required according to Compass Lexecon 19

Non-Confidential November 2014 | Frontier Economics 3

Introduction and summary

1 Introduction and summary

1.1 Ofcom has produced a consultation document1 on its proposed approach to

adopting an ex-ante margin test for VULA products. This was in response to its

provisional finding2 that BT has Significant Market Power (SMP) in the

Wholesale Local Access (WLA) market.

1.2 In BT’s response (5 September 2014) to the consultation, it disagreed with

several parts of Ofcom’s proposed approach. TalkTalk has asked Frontier

Economics to consider:

BT’s claim that any ex ante ‘bright line’ margin squeeze test is both

unnecessary and disproportionate, and

the Compass Lexecon (CL) report3, submitted to Ofcom on behalf of

BT, which argues that Ofcom should include a much lower (or no) cost

of BT Sport (BTS) within the margin test.

1.3 In its response, BT argues that a bright-line test is inappropriate, as BT could fail

Ofcom’s proposed test without excluding rivals4. Therefore, BT argues that

Ofcom should adopt more of an effects-based, ex-post or blurred line approach.

BT further argues that there is no need for a bright-line margin test, as current

market developments indicate there is no problem at present and BT states that

Ofcom could rely on ex-post competition policy and FRAND5.

1.4 Ofcom considers that there is a risk of distortion to competition for superfast

broadband in the next market review period which the VULA test aims to ensure

does not materialise. It is notable that both Sky and TTG have a much lower

share in the SFBB than they do in the SBB market, and Ofcom is already

conducting an ex-post margin squeeze case based on a complaint by TTG.

Further, Ofcom has already found that BT has SMP in the WLA market, and BT

does not dispute this.

1 Ofcom’s Consultation of 19 June 2014 – “Fixed Access Market Reviews: Approach to the VULA

margin”

2 Ofcom, Fixed access market reviews: wholesale local access, wholesale fixed analogue exchange lines,

ISDN2 and ISDN30 Volume 1: Draft statement on the markets, market power determinations and

remedies, 19 May 2014

3 The Compass Lexecon report was submitted as Annexe C of BT’s response. We have also reviewed

the relevant parts of BT’s main response.

4 BT Group plc’s response to Ofcom’s consultation of 19 June 2014 - “Fixed Access Market Reviews:

Approach to the VULA margin” – paragraph 7.10

5 BT Group plc’s response to Ofcom’s consultation of 19 June 2014 - “Fixed Access Market Reviews:

Approach to the VULA margin” paragraph 1.16.

4 Frontier Economics | November 2014 Non-Confidential

Introduction and summary

1.5 We find that, given Ofcom’s objective and the position of the main broadband

providers in the UK SFBB market, Ofcom’s assessment that ex-post competition

policy and Fair Reasonable and Non-Discrimination (FRAND) obligations are

unlikely to be adequate substitutes for an ex-ante margin test for VULA products

is appropriate. Ex-post competition policy may be a less effective deterrent if

there is less certainty about how the tests would be conducted. It is also likely

that there would be a significant lag between any abuse and its identification

under ex-post competition policy. FRAND will also be a weaker deterrent as it is

likely more open to interpretation.

1.6 Failing to adopt a bright-line test would also be inconsistent with the EC’s

costing recommendation (2013)6, which we understand does not foresee

circumstances under which there should be both no regulated access prices and

no ex-ante margin test. The EC recommendation states that a bright-line test is

only a substitute for regulated access prices when other safeguards are in place.

1.7 CL has argued that Ofcom should not include TV content within the margin test

because (a) the cost of BT’s sports rights could overstate consumers’ valuation of

these rights and (b) consumers will have heterogeneous valuations of these rights.

BT’s downstream rivals therefore need to be provided with sufficient margins to

be able to ‘contest’ only a part of BT’s subscriber base.

1.8 We consider that CL’s proposed approach would be inconsistent with Ofcom’s

main objective for the VULA margin tests, namely to ensure that BT does not

distort retail competition for SFBB. First, it is unlikely that the cost of the sports

rights will overstate consumers’ valuation of these rights. BT had commercial

freedom in deciding how much it bid for the rights in the auctions. The

maximum amount that BT would have bid should have been equal to the extra

profits that BT expected to make, which would have depended on consumers’

valuation of the rights. Even if BT’s main objective was to defend its position

against Sky, this could still have been a profit-maximising strategy. After having

acquired the rights, BT announced that its financial outlook remained unchanged

which in turn is consistent with BT not considering that it had overpaid for the

rights.

1.9 Second, we consider that CL’s approach, as set out, does not appropriately reflect

the margins that are necessary for BT’s downstream rivals to be able to compete

in the retail market. Whilst we agree that consumers will not all value BTS rights

in the same way, this does not necessarily imply that the cost of such rights

should be excluded from a margin test: the reason is that BT’s rivals will be

expected to compete to attract subscribers to different BT products, and

subscribers to the same BT product can be expected to have different valuations

of BT Sport (BTS) rights. Furthermore, there are constraints on the ability of

6 Commission Recommendation of 11.9.2013 on consistent non-discrimination obligations and costing

methodologies to promote competition and enhance the broadband investment environment.

Non-Confidential November 2014 | Frontier Economics 5

Introduction and summary

rivals to discriminate between consumers with different valuations of BTS.

Ofcom’s stated objective to “enable an operator that has slightly higher costs than BT (or

some other slight commercial drawback relative to BT) to profitably match BT’s retail superfast

broadband offers7” implies that rivals should be able to compete for all segments of

the market. This means that using an average margin is appropriate.

1.10 We note also that one of the implications of the existence of heterogeneous

consumers and BT’s main downstream rivals focussing on different parts of the

market, is that Ofcom should adopt disaggregated tests and allocate a greater

proportion of the costs of BTS to fibre customers, as we have argued in our

previous report.

1.11 The rest of this report is structured as follows:

In section 2, we explain why meeting Ofcom’s main objective in relation to

the identified risk of distortion to competition in the UK market is

consistent with the application of a bright-line test. In particular, we explain

why Ofcom does not need to conduct an “effects-based” analysis at this

stage, and why existing remedies are unlikely to be substitutes for a bright-

line test.

In section 3, we set out the outcome of our review of the CL report (and

related BT arguments). We start by setting out why the cost of BTS should

not be expected to exceed the value attached to BTS by

consumers/subscribers. We then present our understanding of CL’s analysis

in support of the case to modify the margin test to exclude BTS costs and

explain why this is inconsistent with Ofcom’s objectives. We then conclude

on why it is appropriate to include BTS costs within the margin tests, and

note that some of the CL’s arguments lend support to the proposals of the

previous Frontier report for a disaggregate test, and the need for Ofcom to

use the take-up method.

7 Ofcom’s Consultation of 19 June 2014 – “Fixed Access Market Reviews: Approach to the VULA

margin” - paragraph 1.9

6 Frontier Economics | November 2014 Non-Confidential

There is a strong case for using a bright-line test

2 There is a strong case for using a bright-

line test

2.1 Ofcom proposes to apply an ex ante margin squeeze test to BT’s VULA services

for several reasons:

(a) it considers that the period considered in this market review will be important

for the development of the superfast broadband retail market in the UK8, for

which VULA is the critical input. Ofcom therefore considers that were BT to

unfairly acquire significant first mover advantages during this period, it may be

difficult for competition to develop in subsequent periods (in addition to

consumer harm which would arise in the period itself).

(b) a margin squeeze is one means by which competition could be distorted in

the downstream market, and so effective remedies are required to prevent this.9

Ofcom considers that, as a vertically integrated firm with SMP, BT has the

incentive and ability to engage in margin squeeze. BT’s own forecasts, and recent

market evidence, indicate to Ofcom that BT expects to acquire a large share of

the superfast broadband retail market in the next period.10

(c) Ofcom does not propose to regulate the wholesale prices which BT can

charge for VULA, which is a measure that might otherwise reduce concerns

about BT’s ability to engage in margin squeeze. Ofcom also considers that

existing competition law safeguards would not meet its objectives (since they may

involve a different test to that Ofcom proposes and would carry greater risks of

non-compliance11)

(d) Ofcom considers that an ex ante test would provide BT with greater certainty

in setting prices than existing ‘fair and reasonable’ obligations and would not

impose a significant burden upon BT in the process12.

2.2 In its response, BT argues that Ofcom’s bright-line ex ante test is inappropriate

and disproportionate. It claims that existing obligations to offer VULA on fair

8 Ofcom’s Consultation of 19 June 2014 – “Fixed Access Market Reviews: Approach to the VULA margin”,

paragraph 1.5.

9 Ofcom’s Consultation of 19 June 2014 – “Fixed Access Market Reviews: Approach to the VULA margin”,

paragraph 3.40-

10 Ofcom’s Consultation of 19 June 2014 – “Fixed Access Market Reviews: Approach to the VULA margin”

paragraph 3.55-3.69

11 Ofcom’s Consultation of 19 June 2014 – “Fixed Access Market Reviews: Approach to the VULA margin”

paragraph 4.42

12 Ofcom’s Consultation of 19 June 2014 – “Fixed Access Market Reviews: Approach to the VULA margin”

paragraph 4.67-

Non-Confidential November 2014 | Frontier Economics 7

There is a strong case for using a bright-line test

and reasonable terms, combined with competition law, are a better approach. In

doing so, BT argues, amongst other things, that:

(a) there is no evidence that existing obligations to supply VULA on fair and

reasonable terms have been ineffective or have resulted in margin squeeze in the

past.

(b) the next review period is not decisive to the development of superfast

broadband, as Ofcom claims. In any event, if evidence of margin squeeze

emerges, Ofcom can intervene during the period to impose an ex ante test at that

point rather than now.

(c) ex ante margin tests fail to consider the effects of the margin squeeze on

competition. Without this, BT could fail Ofcom’s proposed test without

excluding rivals13.

(d) Ofcom should adopt a more dynamic test rather than a static test14.

2.3 In this section we assess BT’s arguments and conclude that BT’s proposal for a

continuation of current remedies does not seem consistent with either Ofcom’s

objective to ensure that BT does not distort retail competition for SFBB; or the

European Commission’s proposed approach to the regulation of SFBB wholesale

access prices in its recent costing recommendation. Given this, the suggestion

that Ofcom should complement the margin test with an “effects-based” analysis

at this stage seems inappropriate. Also, suggestions that recent market

developments show an ex ante test is not required should be treated with caution

and, whilst there is merit to the principle of a dynamic approach to the margin

test, it is likely to prove challenging to implement such a test.

The suggested differences between the

approaches proposed by BT and Ofcom should

not be expected to be material

2.4 When arguing why there is no need for a bright-line test, BT often refers to the

substance of the test rather than whether an ex ante test is necessary at all. It

seems to us that BT’s objections to Ofcom’s proposals appear to relate to the

13 BT Group plc’s response to Ofcom’s consultation of 19 June 2014 - “Fixed Access Market Reviews:

Approach to the VULA margin” – paragraph 7.10

14 BT Group plc’s response to Ofcom’s consultation of 19 June 2014 - “Fixed Access Market Reviews:

Approach to the VULA margin” – paragraph 1.4

8 Frontier Economics | November 2014 Non-Confidential

There is a strong case for using a bright-line test

substance (or what Annex II of the Costing Recommendation15 refers to as the

‘parameters’) of the test which Ofcom propose, rather than the form.

2.5 Many of the distinctions that BT draws between ex ante and ex post margin

squeeze tests on the one hand, and the application of existing FRAND and

proposed margin squeeze rules on the other, may not be that material. For

example:

An ex post or competition law based test still requires BT to make

assumptions about the form of the test to be applied and would therefore be

expected to exert a constraint on BT’s behaviour. Under a FRAND

obligation it is therefore likely that BT will have some view about how a

margin squeeze test (ex post) would be applied when setting its prices. The

difference between the two approaches in practice is that the form of the ex

ante test will be more clearly specified in advance. We note that this is a key

reason why Ofcom itself prefers the ex ante test.

Ofcom’s proposed ex ante test is one of the least intrusive regulatory

measures when compared to those implemented by NRAs in other Member

States16. Furthermore, it is not clear how the proposed test deprives BT of

commercial flexibility when compared to the application of competition law

(other than requiring the test to be ‘specified’ differently). For example,

Ofcom does not propose to require BT to notify individual retail tariffs for

approval by the NRA in advance of launch. The ex ante test will therefore

not delay or otherwise inhibit BT’s capacity to act in order to meet

competition. BT has not put forward example(s) of the type of tariff

packages that it could launch under a FRAND obligation but would be

prevented from launching under an ex ante margin test. Moreover, the

substantive form of the test, by being applied to the aggregate portfolio of

BT’s fibre products, is designed to give BT considerable flexibility as to how

it will recover retail costs between different services (and how it therefore

structures its retail prices).

BT proposes that Ofcom could instead retain the existing FRAND rules and

provide more detailed guidelines on how it would apply them in relation to

concerns about margin squeeze. Again, the practical result of this could be

indistinguishable from the ‘bright line’ margin squeeze test which Ofcom

proposes. It would however be unusual for FRAND rules to consider retail

15 Commission Recommendation of 11.9.2013 on consistent non-discrimination obligations and

costing methodologies to promote competition and enhance the broadband investment

environment.

16 For example, 14 NRAs are still imposing some form of price control method on fibre access

products (BEREC Report – Regulatory Accounting in Practice 2014 – Figure 5).

Non-Confidential November 2014 | Frontier Economics 9

There is a strong case for using a bright-line test

costs as the starting point for determining whether a particular wholesale

price was ‘fair and reasonable’, which is precisely why Ofcom considers it

necessary to supplement FRAND with an ex ante margin squeeze test

designed specifically for that purpose. The distinctions which BT seeks

therefore to draw between the different remedies do not appear therefore as

sharp as BT seems to suggest.

2.6 It is also important to note that BT does not appear to make an attempt to

challenge the benefits of greater certainty which are offered by an ex ante margin

test and which may be of significant assistance to BT itself (as well as to other

parties in the market). This is particularly relevant as the intent of the EC

Recommendation is to promote investment in SFBB. Greater certainty and

predictability as to how it may set both retail and wholesale prices in future may –

all else equal - assist BT in the development of its investment case for SFBB and

to reduce its risks.

2.7 BT’s argument is instead that these benefits are offset by the costs, which it

describes as a loss of ‘flexibility’17. Yet, as explained above, it is not clear that

Ofcom’s proposed approach to the ex ante test would deprive BT of any

significant flexibility. To the extent that it does, this is again due to the form or

substance of the test rather than to the application of an ex ante test per se.

The available evidence suggests that existing

remedies would be insufficient

2.8 The inadequacy of competition law is a precondition for a finding that the

market requires ex ante regulation under the European framework. For example,

in the latest Recommendation on Relevant Markets, the Commission states18:

2.9 “The third criterion serves to assess the adequacy of corrective measures that can be imposed

under competition law to tackle identified persistent market failure(s), in particular given that

ex ante regulatory obligations may effectively prevent competition law infringements. Competition

law interventions are likely to be insufficient where for instance the compliance requirements of

an intervention to redress persistent market failure(s) are extensive or where frequent and/or

timely intervention is indispensable. Thus, ex ante regulation should be considered an

appropriate complement to competition law when competition law alone would not adequately

address persistent market failure(s) identified.”

2.10 The reasons for insufficiency of competition law in circumstances where firms

have enduring market power are well known and provide the underlying basis for

17 BT Group plc’s response to Ofcom’s consultation of 19 June 2014 - “Fixed Access Market Reviews:

Approach to the VULA margin” - paragraph 6.3

18 Recital 16 of Commission Recommendation on relevant product and services markets within the

electronic communications sector, 9 October 2014

10 Frontier Economics | November 2014 Non-Confidential

There is a strong case for using a bright-line test

the European regulatory framework under which Ofcom operates. There is

evidence that the majority of European competition case law on margin squeeze

derives from cases in the telecommunications sector over the past 15 years19. In

some cases, it has taken years for the European Commission’s Competition

Directorate to come to a decision and impose fines, many of which have been

substantial. During the development of the EC Recommendation (which we

discuss below), the European Competition Directorate did not suggest that ex

ante measures were inappropriate or that competition law would prove a

sufficient deterrent in the telecommunications sector.

2.11 BT’s case would then appear to be that the additional ex ante obligations it

already carries, and in particular FRAND, mitigate any need for an ex ante

margin squeeze test. BT argues that little has changed since the 2010 FAMR, in

which Ofcom was content to limit its ex ante remedies to FRAND obligations,

and that there is no evidence that these have been ineffective.

2.12 We consider BT’s claims about the development of competition in SFBB since

2010 later (paragraph 2.21 onwards). Since the 2010 FAMR, the European

Commission has adopted the Non Discrimination and Costing

Recommendation, of which Ofcom must now take utmost account and which

recommends that NRAs apply an ex ante margin squeeze test to safeguard

competition in the absence of ex ante price controls.

2.13 It is important to recall the origins of the Recommendation: a key motivation is

the promotion of investment in next generation networks. To do this, it proposes

that NRAs can forebear from setting cost oriented wholesale prices for SFBB

products such as VULA (under certain conditions to ensure minimisation of

non-price discrimination risks). The intention is that by allowing SMP operators

to set wholesale prices themselves while the technology is new, investment in

next generation fibre networks will be encouraged.

2.14 However, the Recommendation recognises that removing wholesale price

controls could jeopardise competition unless additional safeguards were put in

place. NRAs are not allowed to remove price controls unless wholesale prices are

constrained. Amongst the constraints required by the Recommendation is ‘the ex

ante economic replicability test’. Paragraph 56 of the Recommendation details what

that test should comprise of, and Annex II then outlines the ‘parameters’ to be

adopted.

2.15 The Recommendation does not qualify the requirement for an ex ante test with

reference to whether the SMP operator is gaining or losing market share, or

whether its position in the downstream market is not the result of its commercial

strategy but reflects rather the commercial strategies of rivals. The

19 For example, EC cases include Deutsche Telekom in Germany and Slovakia, and Telefonica in

Spain.

Non-Confidential November 2014 | Frontier Economics 11

There is a strong case for using a bright-line test

Recommendation starts from the presumption that SMP in the upstream market,

combined with vertical integration, confers an incentive and ability to exclude

rivals which must be constrained. The Commission considers this to be a

sufficient basis to require the application of an ex ante margin squeeze test if the

SMP operator is to be allowed to set wholesale prices for itself.

Ofcom should not need to carry out an “effects-

based” analysis at this stage

2.16 BT argues that a ‘bright line’ test based ‘on the numbers’ is inappropriate and that

an ex post test would allow Ofcom to consider the effects of the practice on

competition. It claims that some actions which fail the bright line test may

nonetheless not impede competition and so should be allowed.

2.17 An analysis of effects at this stage is unlikely to be necessary.

2.18 First, even competition law does not require an effect on the market to be

established. It is sufficient that the conduct is capable of having or likely to have

an (anti-competitive) effect20.

2.19 Second, as indicated above, under the EU regulatory framework, there is a

presupposition that there is a material risk of distortion of competition, leading

to detrimental consumer effects, absent appropriate ex ante regulatory measures.

2.20 BT’s central claim on ‘effects’ appears to be that Sky enjoys certain strategic

advantages in the Pay TV market which would render an attempt by BT to

margin squeeze ineffective. As a result, BT claims, Ofcom should take a less

restrictive view of margin squeeze in order to allow BT to more effectively meet

competition. BT however appears to ignore other competitors, notably TTG,

which do not enjoy the strategic advantages BT attributes to Sky. Ofcom’s

objective is to protect competition in general, including that provided by TTG

today21. Furthermore, it would be inappropriate for Ofcom to seek to

compensate for any potential distortions in one upstream market (Pay TV) via

increasing the risk of distortions through a ‘relaxation’ of the conditions of the

application of a margin test in another. A more appropriate response to any

competition concerns in the Pay TV market would be to consider the

20“In a general statement, the Court of First Instance ruled that: “for the purposes of establishing an infringement

of Article [102 TFEU], it is not necessary to demonstrate that the abuse in question had a concrete effect on the

markets concerned. It is sufficient in that respect to demonstrate that the abusive conduct of the undertaking in a

dominant position tends to restrict competition, or, in other words, that the conduct is capable of having, or likely to

have, such an effect”. BEREC (2014) - Draft Guidance on the economic replicability test (p.47).

21 Which, as TTG explained in its submission, is particularly important in constraining BT in the ‘value’

segment of the SFBB market

12 Frontier Economics | November 2014 Non-Confidential

There is a strong case for using a bright-line test

necessary/appropriate regulatory or competition policy interventions in that

market directly.

Suggestions that recent market developments

show an ex ante test is not required should be

treated with caution

2.21 BT argues that TTG and Sky’s recent entry into the SFBB market and their

growing share of VULA net adds is evidence that competition is effective. But

BT refers to developments over the past 12 months involving relatively low

volumes of fibre connections (relative to what might be anticipated in the period

to 2017, during which time BT’s fibre roll out will be largely complete and

consumer demand for SSFB products is expected to increase substantially).

2.22 TTG has argued that BT is already engaging in margin squeezing behaviour.

Furthermore, Ofcom itself has found that under its proposed test, BT’s current

pricing behaviour only ‘marginally’ passes the test. These results have been

obtained during a period when BT was engaged in the FAMR and during which

it had an incentive to demonstrate to Ofcom that competition in SFBB was

effective. These incentives may, of course, be dampened once Ofcom makes its

final decision. BT’s historic behaviour and related market outcomes, even if they

did not raise competition concerns, may not be reliable to inform BT’s future

behaviour in the critical period of the market’s development until 2017. As

Ofcom notes, this is the timeframe during which the competitive landscape for

SFBB is likely to be determined.

2.23 BT’s claim that Ofcom could always intervene during the period (i.e. before

2017) if competition appeared to be threatened is unlikely to be consistent with

Ofcom’s objectives. Ofcom would be required to consult and may well

encounter objections from BT that mid-period changes deter investment and

undermine the credibility of the regime. It would take likely years rather than

months to implement effective measures22, whilst the ex ante test being proposed

would ensure Ofcom had the data and powers to investigate complaints

promptly.

2.24 In summary, Ofcom is not required by the Recommendation to have regard to

recent market developments. But, even if it were, such developments can be

expected to offer relatively limited insight into BT’s likely conduct once the

22 For example, TalkTalk lodged a margin squeeze complaint for SFBB with Ofcom in March 2013,

but Ofcom is yet to reach a Statement of Objections or No Grounds for Action decision. Thus and

Gamma complained of a margin squeeze for wholesale end-to-end calls in June 2008. Ofcom did

not close the case until 5 years later in June 2013

(http://stakeholders.ofcom.org.uk/binaries/enforcement/competition-bulletins/closed-cases/all-

closed-cases/cw_988/final.pdf)

Non-Confidential November 2014 | Frontier Economics 13

There is a strong case for using a bright-line test

FAMR is concluded. They should therefore carry little or no weight in Ofcom’s

assessment.

Competition from Virgin does not remove the

need for an ex-ante margin test

2.25 BT argues that the presence of Virgin eliminates the incentive to squeeze because

BT could not recoup sacrificed profits in the retail market. But 55% of

Openreach’s residential coverage is not covered by Virgin, which means that

BT’s only rivals in such areas are Sky, TTG and EE23). Even in areas where

Virgin is present, Ofcom has indicated that it considers it desirable that other

rivals are also able to be effective competitors.

2.26 In this connection, it is also important to note that the Recommendation does

not consider ‘a demonstrable retail pricing constraint from infrastructure

competition’ to be a substitute for the ex ante replicability test (see para 52). This

is an additional condition to be met before NRAs can remove wholesale price

controls from SFBB wholesale products.

It is likely to be challenging to implement a

dynamic test

2.27 BT argues that it is still relatively new to the Pay TV market, which means that it

may initially make a loss on such products, which will then be compensated by

future profits. BT therefore states that a static analysis of margins is

inappropriate. For example, BT states that:

“Ofcom would in any event need to adopt a more forward looking MST reflecting the realities of

market dynamics24”.

2.28 Whilst we do see merit in the principle of the argument set out by BT, the

implementation of a forward looking multi-period approach, such as a

discounted cash flow approach, which would deal with BT’s criticism, would

need to address a number of issues:

Uncertainty. Carrying out a dynamic analysis of costs and revenues over the

average customer lifetime (ACL) and estimating subscriber terminal values

23 There are also other smaller operators, albeit with a market share below 1%.

24 BT Group plc’s response to Ofcom’s consultation of 19 June 2014 - “Fixed Access Market Reviews:

Approach to the VULA margin” - paragraph 1.23

14 Frontier Economics | November 2014 Non-Confidential

There is a strong case for using a bright-line test

would be challenging given the level of uncertainty. BT itself highlights that

there is significant uncertainty in the fibre broadband market25.

Biased forecasts. According to BEREC26, the primary source of cost and

revenue forecasts is likely to be the SMP operator, which could undermine

the ability of any DCF test to protect competition, as these forecasts could

be biased.

Foreclosure can lead to a positive NPV. BEREC has also stated that even

when the DCF approach does show a positive NPV, it is not always clear

whether positive margins are due to legitimate pricing or the exclusion of

competitors27.

Inconsistent with other NRAs. At present, only one NRA relies

exclusively on a DCF test28, which highlights some of the difficulties of

implementing such a test in this context.

25 BT Group plc’s response to Ofcom’s consultation of 19 June 2014 - “Fixed Access Market Reviews:

Approach to the VULA margin” - paragraph 6.18

26 BEREC guidance on the regulatory accounting approach to the economic replicability test (i.e. ex-

ante/sector specific margin squeeze tests) 26 September 2014 (page 23).

27 BEREC guidance on the regulatory accounting approach to the economic replicability test (i.e. ex-

ante/sector specific margin squeeze tests) 26 September 2014 (page 23).

28 BEREC guidance on the regulatory accounting approach to the economic replicability test (i.e. ex-

ante/sector specific margin squeeze tests) 26 September 2014.

Non-Confidential November 2014 | Frontier Economics 15

It is appropriate to include the cost of BTS within

the margin tests

3 It is appropriate to include the cost of BTS

within the margin tests

3.1 BT has argued that any margin test should exclude BTS, relying on a Compass

Lexecon (CL) report submitted to Ofcom on its behalf. Compass Lexecon’s

main arguments are that:

Consumers’ total valuation of BT Sport (BTS) is likely to be less than

the costs of BTS, and

consumers have heterogeneous valuations of BTS.

Based on this, CL argues that BT’s rivals only need to target consumers who

attach a low value to BTS to be able to reach the minimum size to remain in the

market (called Minimum Efficient Scale (MES)); and, the overall margins

resulting from Ofcom’s approach are more than are necessary for BT’s

downstream rivals to be able to compete effectively. CL therefore suggests that

Ofcom should not include BTS within the margin test “until the MES required by

TTG or a notional entrant required some proportion of BT’s BTS subscribers to be

contestable”29. It then goes on to say that if Ofcom does decide that it has to take

into account BTS for rivals to achieve MES, then Ofcom should focus on the

value of BTS rather than the cost of BTS, given that CL argues that BT has

overpaid for the rights.

3.2 We consider that CL’s proposed approach would not meet Ofcom’s main

objective for the VULA margin tests, as it does not provide sufficient protection

to ensure that BT does not distort retail competition for SFBB. First, we consider

that it is unlikely that the cost of BTS rights would overstate the value that

consumers attach to such rights. Second, we consider that CL understates the

number of customers that need to be contestable. Instead, to meet Ofcom’s

objectives, all customers should be contestable, which means that the use of an

average margin is appropriate.

3.3 Further, we note that some of the arguments in the CL report are consistent with

the arguments that Frontier made in its previous report30, namely that a larger

proportion of the costs of BTS should be recovered from fibre customers and

there is therefore the need to adopt a disaggregate test.

3.4 In the rest of this section, we explain why:

29 BT Group plc’s response to Ofcom’s consultation of 19 June 2014 - “Fixed Access Market Reviews:

Approach to the VULA margin” – Annexe C – paragraph 131

30 Frontier Economics - Ofcom’s VULA margin test – report prepared for TTG (October 2014)

16 Frontier Economics | November 2014 Non-Confidential

It is appropriate to include the cost of BTS within

the margin tests

It is unlikely that the cost of the BTS rights overstates the value that

consumers attach to these rights;

CL understates the number of customers that need to be contestable to

prevent competition from being distorted; and

If consumers have a heterogeneous valuation of BTS, then this implies

that a larger proportion of the costs of BTS should be recovered from

fibre customers and there is a need to adopt disaggregated tests.

It is unlikely that the cost of acquiring BT’s

sports right overstates the value that consumers

attach to these rights

3.5 Compass Lexecon argues that the cost of BTS31 (the cost of the sports rights that

BT has acquired) may overstate the value that consumers attach to such content.

In particular, Compass Lexecon states that:

“BT is exposed to the risk of overpaying for rights if it bids aggressively in content auctions given

Sky’s strong incumbent position”32.

3.6 Given this, CL argues that it would be inappropriate to include the net cost of

BTS within the VULA margin test as this is likely to overstate the margin

necessary for BT’s rivals to be able to compete effectively with BT in the

downstream market.

3.7 For the following reasons, it is unlikely that the cost of BTS overstates the value

that consumers attach to such content.

BT should have been following a profit-maximising strategy. BT had

complete freedom in deciding how much it bid for the sports rights in both

the 2012 Premier League auction and the 2013 Champions League auction.

The amount that BT chose to spend on sports rights should in general be

expected to reflect the additional profits (or net revenues) that BT expects to

make from acquiring these rights. The additional profits that BT can make

from BTS will depend on how much consumers’ value BTS33. If anything,

31 CL refers to the costs/value of BTS (BT Sports) – we use these terms BTS and sports rights

interchangeably.

32 BT Group plc’s response to Ofcom’s consultation of 19 June 2014 - “Fixed Access Market Reviews:

Approach to the VULA margin” – Annexe C – paragraph 11.

33 We are assuming that BT would be able to ‘monetise’ the value of BTS to BT’s subscribers, and that

subscribers would not be prepared to pay more for BTS than the value they place to it. Given the

nature of competition in broadband markets, ‘monetisation’ need not involve charging a price for

BTS, but may also reflect for example a reduction in the expected switching rate to Sky and/or

other rivals as a result of the acquisition of the rights.

Non-Confidential November 2014 | Frontier Economics 17

It is appropriate to include the cost of BTS within

the margin tests

the amount that BT paid for content should represent a lower bound on the

value that consumers attach to it because:

BT would expect to make a profit on the acquisition of content,

otherwise there would be no point in acquiring it in the first place;

BT would be unlikely to be able to extract the full value placed on BTS

by its subscribers. To do so, would require BT to be able to identify and

target every individual subscriber with a price/service package that

matched that subscriber’s valuation, and that subscriber’s valuation only.

This would require a degree of customer targeting that is non-feasible in

practice;

In the Premier League auction, no bidder could acquire more than 116

games out of the 154 live matches on offer, which means that BT was

not directly competing with Sky for the 38 matches that BT won34; and

The price per Premier League game paid by BT was slightly lower than

that paid by Sky (£6.47m compared to £6.55m)35 36.

Defending against Sky could still be a profit-maximising strategy.

Even if BT has mainly acquired sports rights to defend against Sky, as long

as this is a profit-maximising strategy, this still doesn’t undermine the

assumption that the cost of these rights would be reflective of the value that

consumers would be expected to attach to such rights.

BT’s financial outlook remained unchanged. In the BT press release

following the announcement of the Premier League auction results, BT

stated that the “outlook for 2012/13 remains unchanged”37. Likewise, when

34 ESPN also bid in the auction, but did not acquire any rights. This means that BT would have had to

outbid ESPN.

35

http://corporate.sky.com/investors/press_releases/2012/sky_remains_home_of_premier_league

_football

http://www.btplc.com/News/Articles/ShowArticle.cfm?ArticleID=5b3742c3-7ecf-482e-b309-

dd5237069dd8

36 It is debatable whether Sky or BT won the better matches on average. BT won package A and G.

Package A contained 13 first pick matches and 13 fourth pick matches, whereas Package G

contained 5 first pick matches, 5 second pick matches and 2 fifth pick matches. The only package

that Sky won with first pick matches was package D with 20 first pick matches.

37 BT Press Release 13th of June 2012:

http://www.btplc.com/News/Articles/ShowArticle.cfm?ArticleID=5b3742c3-7ecf-482e-b309-

dd5237069dd8

18 Frontier Economics | November 2014 Non-Confidential

It is appropriate to include the cost of BTS within

the margin tests

winning the UEFA Champions League rights, BT stated that it expected its

financial outlook to remain unchanged.38

No asset write-downs. In BT’s annual accounts, it has not carried out any

asset write-down, which is inconsistent with a position that the cost of the

rights exceeds the (incremental) value to BT’s subscribers.

3.8 For the above reasons, the cost of BTS should be expected to reflect the value

that consumers39 attach to such rights (on average), so the margin test should

include the cost of BTS.

CL understates the number of customers that

need to be contestable to prevent competition

from being distorted

3.9 Compass Lexecon argues that consumers have heterogeneous valuations of BTS.

In particular, in Annexe C, Compass Lexecon states that:

“consumers will clearly have highly heterogeneous valuations for sports content including

specifically for BTS”40.

Compass Lexecon considers that the aim of the margin test should be to prevent

‘exclusion’ which it defines as a weakening of competition by preventing rivals

from reaching the minimum size (called Minimum Efficient Scale (MES))

necessary for them to compete effectively. Although CL does not define

explicitly the number of subscribers needed to reach MES, it assumes that rivals

can reach such a size by competing for some, but not all, of BT’s

(current/potential) subscribers. As different subscribers put different value on

BTS, CL argue that BT’s rivals need only compete for those subscribers that

attach a relative low value to BTS, to reach MES. For example, CL states that:

“BT’s rivals may reach MES by targeting the many users who attribute no or only a very low

value to BTS”41.

3.10 According to CL, Ofcom’s proposed test, by effectively calculating a margin that

reflects the ‘average’ value of BTS to BT’s subscribers, provides a higher margin

38 BT Press Release 9th of November 2013:

http://www.btplc.com/News/Articles/ShowArticle.cfm?ArticleID=15D869F4-C14E-44A2-956E-

A2C18B1751A9

39 By consumers, we mean actual and potential subscribers to BT’s products that include BTS.

40 BT Group plc’s response to Ofcom’s consultation of 19 June 2014 - “Fixed Access Market Reviews:

Approach to the VULA margin” – Annexe C – paragraph 105.

41 BT Group plc’s response to Ofcom’s consultation of 19 June 2014 - “Fixed Access Market Reviews:

Approach to the VULA margin” – Annexe C – paragraph 12.

Non-Confidential November 2014 | Frontier Economics 19

It is appropriate to include the cost of BTS within

the margin tests

than is necessary for rivals to be able to compete effectively with BT. CL

illustrate this with a chart that is repeated below – this shows the ‘distribution’ of

the valuation of BTS amongst consumers, starting from those on the left that do

not attach any value, and then ranking them according to increasing valuation of

BTS. CL argues that BT’s rivals only need a margin equal to the shaded area

shown in the figure below to be able to compete42. By contrast, Ofcom’s

approach would be equivalent to calculating the margin to reflect the whole of

the area under the curve (under perfect price discrimination) – hence over-

estimating the margin required.

Figure 1. Margin required according to Compass Lexecon

Source: Annexe C

3.11 The approach proposed by CL is likely to understate the number of customers

that need to be contestable to avoid BT having the ability to distort competition

for the following reasons.

CL itself implies that all customers should be contestable. CL states

that:

“Ofcom’s approach already reflects an (at least) implicit assumption in relation to MES.

In particular, Ofcom has already (implicitly) taken a view on MES in its adoption of a

42 This requires also rivals to be able to identify the value attached by each separate subscriber to BTS

in order to be able to target them (called ‘perfect price discrimination’). Compass Lexecon does

consider relaxing the perfect price discrimination assumption, but this doesn’t fundamentally change

its conclusions.

20 Frontier Economics | November 2014 Non-Confidential

It is appropriate to include the cost of BTS within

the margin tests

‘+’ in LRIC+ (meaning Ofcom must have a view on the fixed costs of the retail supply of

SFBB).”43.

Given that Ofcom is using an EEO test, the implication of this statement by

CL is that rivals must be able to achieve (broadly44) the same scale as BT in

order to be able to recover fixed costs. If a rival had a smaller scale, then,

under the EEO assumption, the fixed costs that it would have to recover per

subscriber would be higher than BT’s (all else the same). CL’s own statement

therefore seems to lead to the implication that all of BT’s subscribers should

be contestable.

It is the combined MES of the different rivals that matters. Ofcom has

set out that its approach to the margin test aims to ensure that there is a

sufficient margin on average for all of BT’s main rivals to be able to compete

with BT. CL does not set out what the MES is for different rivals, but does

argue that the MES of a given rival is likely to be low. BT has three main

rivals that it competes with in different parts of the retail market, and

therefore it may well be the case that the sum of the MES of BT’s three

main rivals would require them to be able to compete for the whole (or

substantially the whole) of BT’s subscriber base.

Operators cannot perfectly target different customer segments. BT and

its rivals do not and cannot compete at the level of each individual

subscriber with propositions tailored to them. The nature of competition is

that BT (and rivals) offer a range of packages targeting different segments of

the market, and do so by offering bundles of services – without being able to

perfectly target individual customers. The implication is that a rival to BT

that wishes to compete for a BT subscriber will need to offer a package that

BT’s subscribers find more attractive than BT’s. To illustrate the point,

assume that a rival wishes to target BT’s Infinity 1 subscribers. BT’s

subscribers to Infinity 1 product will in general be expected to include

subscribers that place different levels of value to BTS. Absent any evidence

to the contrary, there is no a priori reason to expect that these subscribers

would place, on average, no (or little) value to BTS. Absent the ability of

rivals to perfectly target individual customers, excluding the BTS costs from

the Infinity 1 margin would effectively imply that all Infinity 1 subscribers

that place some value on BTS would be non-contestable. In general, the

lower the ability of operators to target individual customers, the higher the

margin required to be able to contest BT’s subscriber base.

43 BT Group plc’s response to Ofcom’s consultation of 19 June 2014 - “Fixed Access Market Reviews:

Approach to the VULA margin” – Annexe C – paragraph 50.

44 The reason is that the test is an adjusted EEO test – hence it is designed to allow a rival with

‘slightly higher costs than BT’ to be able to trade profitably.

Non-Confidential November 2014 | Frontier Economics 21

It is appropriate to include the cost of BTS within

the margin tests

Triple play customers should be included within the margin test. CL

argues that Ofcom should only be concerned about dual play customers.

“Market-level exclusion concerns can only arise when the lower BTS valuation consumers of BT become uncontestable and where that deprives a dual play rival of achieving MES on the assumption that triple play rivals enjoy economies of scope with their dual play offers or have a countervailing advantage from positions of strength in CPSCs (or both). Henceforth, we confine attention on a dual play rival.”45.

CL appears to have misinterpreted Ofcom’s tests, as BT does not need to

recover any BTS costs from dual play customers. Under Ofcom’s proposed

aggregate test, BT would have the freedom to choose how it recovers the

costs of BTS from its customer base. Under the disaggregated tests that we

proposed in our previous report, no BTS costs would be recovered from

(pure) dual play customers46.

Furthermore, even if it was possible to distinguish between dual play and

triple play fibre customers, triple play customers should still be included

within the margin test. The reason is that competition could be distorted if

BT’s rivals cannot compete for such customers. Given that BTS is a key part

of BT’s strategy to drive fibre take-up, not taking into account the value

attached to BTS by those subscribers that take-up the service in the margin

test would risk rivals not being able to compete effectively for such

customers.

Too much focus on Sky. CL’s argument that other rivals have

countervailing advantages in triple-play seems to be primarily geared towards

Sky. For example, CL states that:

“Sky has available counterstrategies because it can seek to leverage its market power in CPSCs to attract SFBB subscribers” 47

If Ofcom does decide that Sky has a dominant position in the Pay TV

market, then it should deal with this directly, rather than trying to level the

playing field by distorting competition in the broadband market, and thereby

impacting rivals such as TalkTalk and EE.

45 BT Group plc’s response to Ofcom’s consultation of 19 June 2014 - “Fixed Access Market Reviews:

Approach to the VULA margin” – Annexe C – paragraph 81.

46 We note in this respect that as BTS is currently offered for ‘free’ with fibre subscription there are no

pure double play customers on BT’s fibre products. Even if some of BT’s subscribers do not

actively take-up the BTS service, they have the option to do so at any point which may well act as a

barrier to switching to other rivals. As BT also plans to introduce new premium content in its BTS

package the historic valuation of BTS amongst BT’s subscribers may also be a poor predictor of

future valuation.

47 BT Group plc’s response to Ofcom’s consultation of 19 June 2014 - “Fixed Access Market Reviews:

Approach to the VULA margin” – Annexe C – paragraph 71.

22 Frontier Economics | November 2014 Non-Confidential

Consumers’ heterogeneous valuation of BTS is

consistent with (a) a need to adopt disaggregated

tests and (b) a larger proportion of the costs of

BTS being recovered from fibre customers

3.12 Given the above points, the appropriate approach would be to design the margin

test, such that rivals can compete for all segments of the market. This would be

consistent with Ofcom’s stated objective to “enable an operator that has slightly higher

costs than BT (or some other slight commercial drawback relative to BT) to profitably match

BT’s retail superfast broadband offers48”.

3.13 Under an aggregate test, ensuring that all customer segments are contestable

could be achieved by using the average margin as Ofcom has proposed.

However, as we argued in our previous report, we consider that there would be

merit in adopting disaggregated tests. Under such tests, the BTS costs that are

recovered from different packages may depend on the value that customers

attach to BTS. We discuss this in further detail below.

Consumers’ heterogeneous valuation of

BTS is consistent with (a) a need to adopt

disaggregated tests and (b) a larger

proportion of the costs of BTS being

recovered from fibre customers

3.14 Compass Lexecon argues that:

“the value of BTS is likely to be far from uniform, and to be zero for a large number of final

consumers”49

3.15 As mentioned earlier, the heterogeneous valuation of BTS is consistent with

some of the arguments that we made in our previous report, namely that:

Ofcom should conduct disaggregated tests; and

A greater proportion of the costs of BTS should be recovered from

fibre customers.

The need for disaggregated tests

3.16 If consumers have heterogeneous valuations for BTS, this is also consistent with

the arguments used in the previous Frontier report on the need for Ofcom to

carry out disaggregated tests, to prevent BT targeting particular segments of the

48 Ofcom’s Consultation of 19 June 2014 – “Fixed Access Market Reviews: Approach to the VULA

margin” - paragraph 1.9

49 BT Group plc’s response to Ofcom’s consultation of 19 June 2014 - “Fixed Access Market Reviews:

Approach to the VULA margin” – Annexe C – paragraph 11.

Non-Confidential November 2014 | Frontier Economics 23

Consumers’ heterogeneous valuation of BTS is

consistent with (a) a need to adopt

disaggregated tests and (b) a larger proportion of

the costs of BTS being recovered from fibre

customers

market. Under such disaggregated tests, at least in principle, the cost of BTS

could arguably have to be recovered based on the value that consumers attach to

it50. If such an approach is contemplated, in order to ensure consistency, the tests

should seek to reflect other characteristics of these consumers which could be

expected to affect the margins such as potentially shorter ACLs or different

usage of voice telephony.

3.17 As we stated in our previous report, if there are concerns about the

proportionality or practicality of performing disaggregate tests across all five

product groups, then a margin test for Infinity 1 products with and without TV

would be the priority, given Ofcom’s stated objectives. In such a case, it would

still be desirable for such a disaggregate test(s) to be complemented by an

aggregate test, to ensure that the overall margins allow rivals to compete with BT

across BT’s customer portfolio.

A greater proportion of the costs of BTS should be recovered from fibre

customers

3.18 In our previous report we argued why the “take-up approach” was more

appropriate than the “all-broadband approach”. The heterogeneity in consumers’

valuation of BTS provides further support for the “take-up” approach, as it

implies that a greater proportion of the costs of BTS should be recovered from

fibre customers, to the extent that such customers are more likely to value/take-

up BTS.

3.19 In addition, the heterogeneity in valuations also seems to be consistent with the

argument that consumers value watching BTS more over their TV than they do

over apps or online.

50 We did not suggest this in our previous report, as we had not seen any data on the differences in

consumers’ valuation of BTS.

Frontier Economics Limited in Europe is a member of the Frontier Economics network, which

consists of separate companies based in Europe (Brussels, Cologne, London & Madrid) and Australia

(Melbourne & Sydney). The companies are independently owned, and legal commitments entered

into by any one company do not impose any obligations on other companies in the network. All

views expressed in this document are the views of Frontier Economics Limited.

FRONTIER ECONOMICS EUROPE

BRUSSELS | COLOGNE | LONDON | MADRID

Frontier Economics Ltd 71 High Holborn London WC1V 6DA

Tel. +44 (0)20 7031 7000 Fax. +44 (0)20 7031 7001 www.frontier-economics.com