Title insurance industry in the u.s. – market and business opportunity. ver.1.3

53

-

Upload

harshvardhan1 -

Category

Real Estate

-

view

56 -

download

2

Transcript of Title insurance industry in the u.s. – market and business opportunity. ver.1.3

INDUSTRY STATISTICS & MARKET SIZE

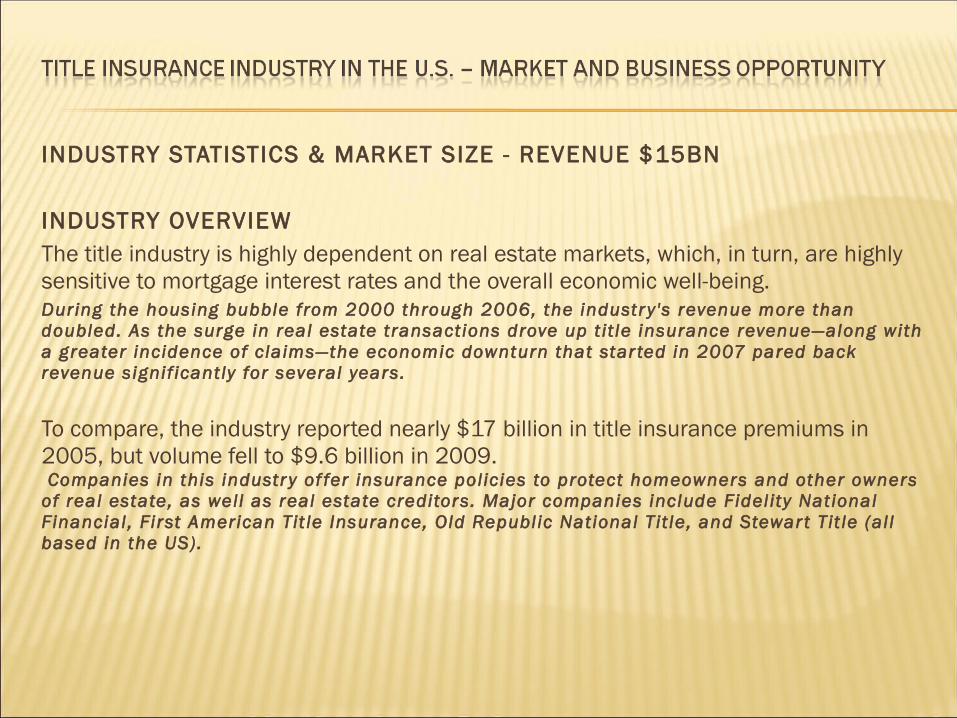

INDUSTRY STATISTICS & MARKET SIZE - REVENUE $15BN

INDUSTRY OVERVIEWThe title industry is highly dependent on real estate markets, which, in turn, are highly sensitive to mortgage interest rates and the overall economic well-being. During the housing bubble from 2000 through 2006, the industr y 's revenue more than doubled. As the surge in real estate transactions drove up t it le insurance revenue—along with a greater incidence of claims—the economic downturn that star ted in 2007 pared back revenue signif icantly for several years.

To compare, the industry reported nearly $17 billion in title insurance premiums in 2005, but volume fell to $9.6 billion in 2009. Companies in this industr y of fer insurance policies to protect homeowners and other owners of real estate, as well as real estate creditors. Major companies include Fidel ity National Financial , First American Tit le Insurance, Old Republic National Tit le, and Stewar t Tit le (al l based in the US).

INDUSTRY OVERVIEWMany large US-based companies provide title insurance in Europe and in countries such as Australia, Canada, China, Mexico, and South Korea, often for US buyers and lenders. The reliabi l i ty of government systems of land registration reduces the market for t i t le insurance in countries other than the US, however. The US has no single, comprehensive system of land registration.

The US title insurance industry includes about 1,900 companies with combined annual revenue of about $13 billion.

COMPETITIVE LANDSCAPEHome sales and mortgage refinancing are the primary drivers of demand for the title insurance industry. The profitability of individual companies depends on efficient operations because of the large volume of transactions.

Large companies benefit from economies of scale in access to large accumulated databases of proper ty records. Small companies can mainly compete by special izing in nonstandard t i t les or in geographical regions that the large companies don't cover. The US industry is highly concentrated: the 50 largest companies account for about 95 percent of revenue.More than 80 percent of industr y revenue comes from ti t le insurance products and premiums; about 10 percent comes from tit le search, t it le reconveyance and other fees.

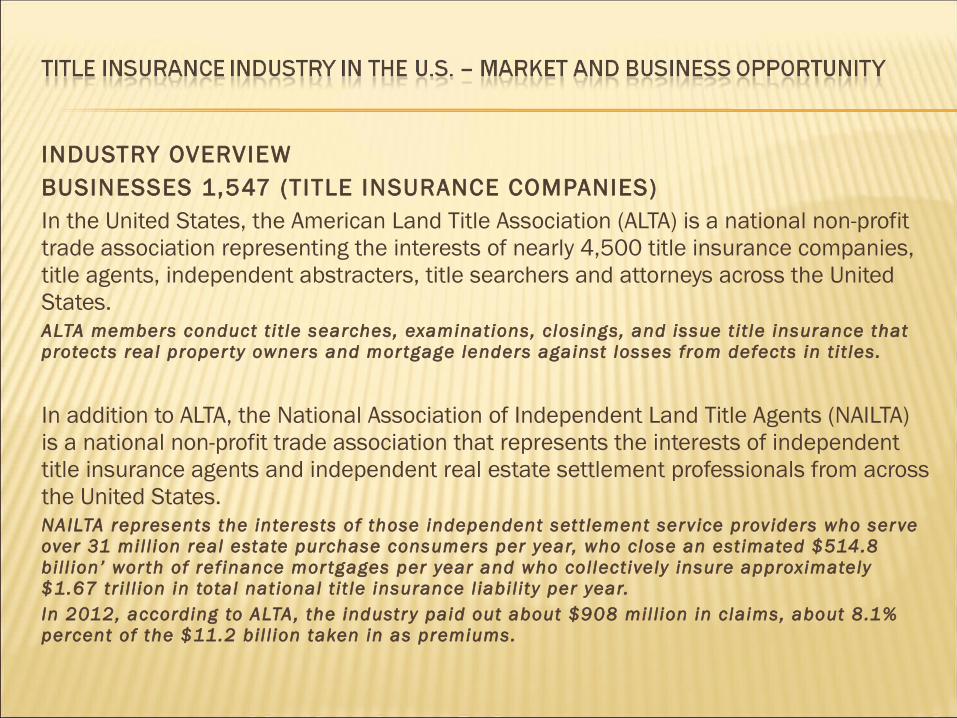

INDUSTRY OVERVIEWBUSINESSES 1,547 (TITLE INSURANCE COMPANIES)In the United States, the American Land Title Association (ALTA) is a national non-profit trade association representing the interests of nearly 4,500 title insurance companies, title agents, independent abstracters, title searchers and attorneys across the United States. ALTA members conduct t i t le searches, examinations, closings, and issue t it le insurance that protects real proper ty owners and mortgage lenders against losses from defects in t i t les.

In addition to ALTA, the National Association of Independent Land Title Agents (NAILTA) is a national non-profit trade association that represents the interests of independent title insurance agents and independent real estate settlement professionals from across the United States.NAILTA represents the interests of those independent sett lement service providers who serve over 31 mil l ion real estate purchase consumers per year, who close an estimated $514.8 bil l ion’ wor th of ref inance mor tgages per year and who collectively insure approximately $1.67 tr i l l ion in total national t it le insurance l iabi l ity per year.In 2012, according to ALTA, the industr y paid out about $908 mil l ion in claims, about 8.1% percent of the $11.2 bil l ion taken in as premiums.

INDUSTRY OVERVIEWEMPLOYMENT -46,076The Title Insurance industry dealt with some shaky foundations during the recession as potential homebuyers shied away from homeownership. However, this has since reversed due to the housing market recovery. Positive growth will continue through 2018 as more homes are built and renters move to buy.

TITLE INSURANCE

TITLE INSURANCEAn abstract and title company does vital research to make sure a real estate transaction is legal. The company provides the lender, insurance company and buyer with information about any issue surrounding the property. These issues might include unpaid taxes or liens against the property that will need to be paid before a new owner can take possession.

WHO IS COVERED BY TITLE INSURANCE?For most Americans, purchasing real estate represents the largest single investment they will make. Given the cost of real estate, very few consumers can purchase home, vacation or investment properties by paying cash. Instead, we borrow the funds from banks, savings and loans, mortgage companies, or other lenders, granting them a secured interest in the property.

TITLE INSURANCEOne of the conditions that lenders place on the buyer is that a lender’s title insurance policy must be purchased in an amount equal to the mortgage loan. However, a lender’s policy only protects the f inancial insti tution in the event that a valid t it le claim arises. In a worst-case scenario, a buyer could make mor tgage payments for 20 or 30 years when an unknown ti t le defect comes to l ight, creating a val id claim that causes the buyer to lose the t i t le. The lender would be covered, to the extent of the outstanding mor tgage, and the owner could lose the proper ty and all equity acquired over the 20 years that he “owned” the proper ty.

To avoid this scenario, an option available to the buyer is the purchase an owner’s title insurance policy. This would protect the buyer’s interest in the real proper ty. If the decision is made to purchase an owner’s pol icy and a lender’s policy at the same t ime, there may be considerable premium savings. In the t i t le insurance business, this is known as a “simultaneous issue,” and the premium rates charged for the owner’s pol icy wil l be calculated on the dif ference between the amount of coverage provided to the lender (amount borrowed) and the amount of coverage provided to the owner (purchase price).

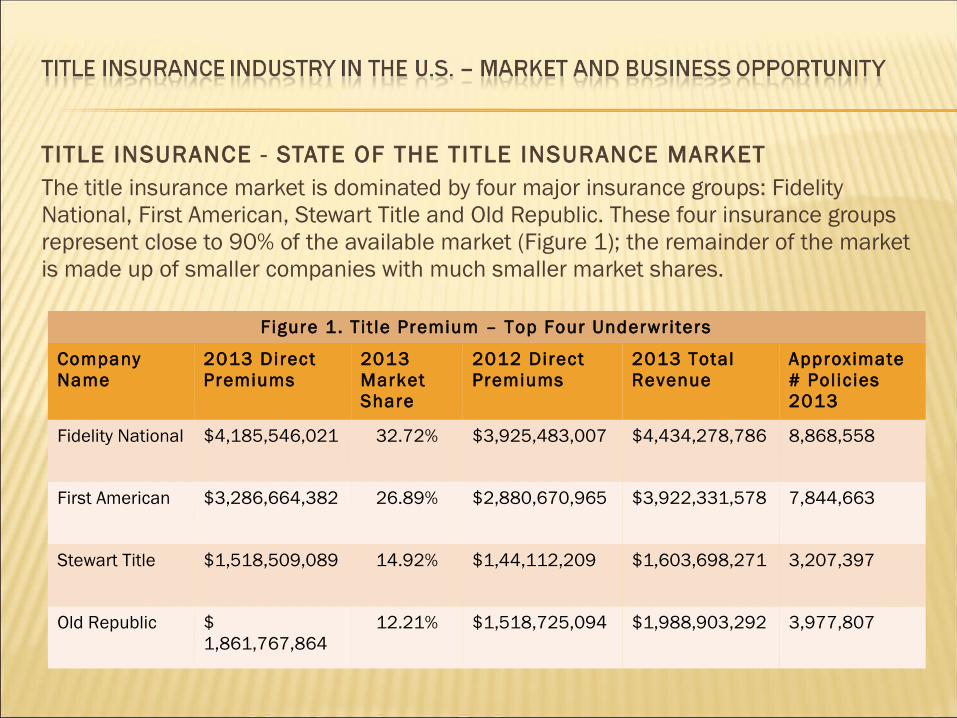

TITLE INSURANCE - STATE OF THE TITLE INSURANCE MARKETThe title insurance market is dominated by four major insurance groups: Fidelity National, First American, Stewart Title and Old Republic. These four insurance groups represent close to 90% of the available market (Figure 1); the remainder of the market is made up of smaller companies with much smaller market shares.

Figure 1. Tit le Premium – Top Four Underwriters

Company Name

2013 Direct Premiums

2013 Market Share

2012 Direct Premiums

2013 Total Revenue

Approximate # Policies 2013

Fidelity National $4,185,546,021 32.72% $3,925,483,007 $4,434,278,786 8,868,558

First American $3,286,664,382 26.89% $2,880,670,965 $3,922,331,578 7,844,663

Stewart Title $1,518,509,089 14.92% $1,44,112,209 $1,603,698,271 3,207,397

Old Republic $ 1,861,767,864

12.21% $1,518,725,094 $1,988,903,292 3,977,807

TITLE INSURANCE - STATE OF THE TITLE INSURANCE MARKET

Figure 2. Tit le Premium – Next Five Underwriters

Company Name

2013 Direct Premiums

2013 Market Share

2013 Total Premiums

2013 Total Revenue

Approximate # Policies 2013

Westcor Land Title

$326,046 2.42% $308,723,731 $315,197,510 630,395

Title Resource Guaranty

$2,065,821 2.10% $267,322,257 $269,975,087 539,950

National Title Ins. Of NY

$3,996,363 1.84% $234,828,128 $244,853,960 489,708

WFG National Title

$ 11,835,744 1.43% $182,754,270 $193,593,679 387,187

North American Title

0.98% $125,131,294 $125,131,394 250,263

PROPERTY ABSTRACT

PROPERTY ABSTRACTA property abstract is a collection of legal documents that chronicles activities associated with a particular parcel of land. Generally included are references to deeds, mor tgages, wil ls, probate records, cour t l i t igations and tax sales--basically, any essential legal documents that af fect the proper ty. The abstract wi l l also show the names of al l proper ty owners and how long a par ticular holder owned it , as wel l as showing the price the land was exchanged for when it changed owners. Rarely wil l an abstract mention capital improvements to the proper ty. Proper ty abstracts are considered good star ting places for research on historical bui ldings.

A property abstract catalogues, in chronological fashion, all legal documents pertaining to a parcel of land. Included are references to deeds, mortgages, wills, probate records, court litigation, and tax sales--the essential legal proceedings that affect property ownership. The abstract reveals the names of al l people who have owned the proper ty, how long each owner had it , and how much it sold for when it changed hands. Only rarely, however, does i t mention buildings or capital improvements to the proper ty. The abstract is a good star ting place for research of a histor ic building because it deals with real proper ty and not specif ical ly the bui ldings and other improvements. The abstract also confirms that there are no outstanding l iens or back taxes.

ABSTRACT OF TITLEAn abstract of title is the condensed history of title to a particular parcel of real estate, consisting of a summary of the original grant and all subsequent conveyances and encumbrances affecting the property and a certification by the abstractor that the history is complete and accurate. In the United States, the abstract of t it le furnishes the raw data for the preparation of a policy of t it le insurance for the parcel of land in question, except for in Iowa, where a Tit le Guaranty policy is issued instead of t i t le insurance.

An abstract of title should be distinguished from an opinion of title. While an abstract states that al l of the public record documents concerning the proper ty in question are contained therein, an opinion states the professional judgment of the person giving the opinion as to the vesting of the t i t le and other matters concerning the status of the chain of t i t le. Many jurisdict ions def ine the giving of an opinion of t it le as the practice of law, thus making i t unlawful for a non-attorney to do so.

COMMENT AND SUMMARY Each financial entry in an abstract can provide information. A substantial increase in price in two consecutive sales, for example, from $500 in 1880 to $4,000 in 1885, usually indicates capital improvement on the land sometime during that period. Be cautious, however, when using f inancial transactions to date buildings. Many factors other than construct ion can af fect proper ty value. Among them are general economic inflation or a speculative market, caused, for example, by a railroad locating a depot in the vicinity. Thus, it is impor tant to be aware of the histor y of the area in question, and par ticularly i ts economic f luctuations.

Some property abstract entries yield more historical information than others, and it is often a good idea to make a trip to the courthouse to read the entire document. Abstractors usual ly include the most impor tant information, leaving out the legal ist ic verbiage; but, af ter al l , your concerns are dif ferent from those of the abstractors, and what may have appeared tr ivial to them could be of impor tance to you. Unfor tunately not al l proper ties in Wisconsin have abstracts. I f you f ind that an abstract is not avai lable for the proper ty you are researching, it is st i l l possible to gather the information that would have been included. In Wisconsin, vir tually everything that might be entered into a proper ty abstract may be found in the Register of Deeds and Register of Probate of f ices at the appropriate county cour thouse.

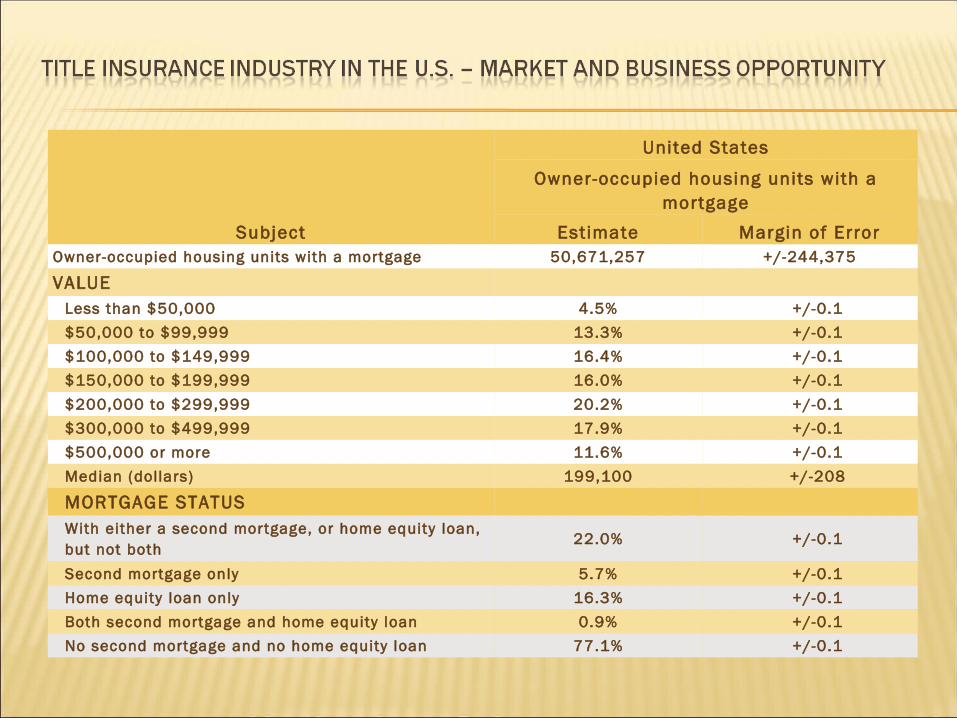

TITLE ABSTRACT AND SETTLEMENT OFFICESThis U.S. industry comprises establishments (except offices of lawyers and attorneys) primarily engaged in one or more of the following activities: (1) researching public land records to gather information relating to real estate ti t les.(2) preparing documents necessary for the transfer of the ti t le, f inancing, and settlement. (3) conducting f inal real estate sett lements and closings.(4) f i l ing legal and other documents relating to the sale of real estate. Real estate settlement of f ices, t i t le abstract companies, and t it le search companies are included in this industry.Housing units, 2012 132,452,405

Homeownership rate, 2008-2012 65.5%

Households, 2008-2012 115,226,802

Persons per household, 2008-2012 2.61

Subject

United States

Owner-occupied housing units with a mortgage

Estimate Margin of ErrorOwner-occupied housing units with a mortgage 50,671,257 +/-244,375

VALUE

Less than $50,000 4.5% +/-0.1

$50,000 to $99,999 13.3% +/-0.1

$100,000 to $149,999 16.4% +/-0.1

$150,000 to $199,999 16.0% +/-0.1

$200,000 to $299,999 20.2% +/-0.1

$300,000 to $499,999 17.9% +/-0.1

$500,000 or more 11.6% +/-0.1

Median (dollars) 199,100 +/-208

MORTGAGE STATUS

With either a second mortgage, or home equity loan, but not both

22.0% +/-0.1

Second mortgage only 5.7% +/-0.1

Home equity loan only 16.3% +/-0.1

Both second mortgage and home equity loan 0.9% +/-0.1

No second mortgage and no home equity loan 77.1% +/-0.1

REAL ESTATE TRANSACTIONS AND TITLE SEARCHES

REAL ESTATE TRANSACTIONS AND TITLE SEARCHESThere are two basic types of title insurance: coverage for the homeowners and coverage for the mortgage lenders. Title insurance for the owner is issued for the purchase price of the property and lasts as long as the purchaser’s ownership interests in the property. Tit le insurance for the lenders is similar to personal mor tgage insurance in that the coverage amount decreases with the principal loan amount over t ime and eventually disappears, along with the lender’s interest. The lender’s policy is usually issued with the owner 's policy for an addit ional nominal fee.

Prior to 1987, there were no deductibles or coinsurance required in standard title insurance policies. Typically, coinsurance and deductibles are used as risk sharing mechanisms to control adverse behavior of the insureds (e.g., moral hazard). Because t it le insurance is designed to insure against events that have occurred prior to the insured’s involvement with the proper ty, not against future events, these r isk sharing mechanisms are unnecessary.

Since 1987, however standard t i t le insurance pol icies that are issued for less than 80 percent of the market value of the proper ty contain coinsurance provisions. This feature is used to prevent under-insuring the proper ty, not moral hazard.

REAL ESTATE TRANSACTIONS AND TITLE SEARCHESSince a majority of mortgage lenders require lenders title insurance as part of the mortgage requirements, a background discussion of real estate transactions is in order. At the time of closing, the purchaser and lender must be satisfied that: 1) there are no t it le defects and 2) the sel ler actual ly owns the t i t le to the proper ty. In addit ion, i t should be noted that t it le insurance is the l ingua franca of the secondary mortgage market because of its uniform coverage of the t i t le and the val idity and priority of the mortgage.

To verify the condition of the title, a title insurance company must complete a title search. A title search is an examination of all public records to determine whether any defects exist in the chain of title. A defect is any hidden risk that may cause loss of title or create an encumbrance on the title.The search begins with researching public records or re- indexed copies of the publ ic records, called t i t le plants, that contain detai led information about each piece of proper ty and its owners in a given region (city or county). Written documents that af fect the land (l iens, loans, and easements) are required to be recorded in the publ ic record of the county where the real estate is located. The conclusion of the t i t le search produces an abstract, or summary repor t, which is then used by the t i t le insurance company in issuing a commitment. This commitment, made prior to the issuance of a t i t le insurance pol icy, protects the pol icyholder from losses arisingf rom defects in the t it le .

TITLE INSURANCEStandard title insurance policy coverage includes defects in public records, forgeries, incompetent grantors, incorrect marital statements, and improperly delivered deeds, that may lead to potential liabilities. Tit le insurance provides indemnif ication to the degree that the policy/repor t is incorrect and lessor damage results. This policy also covers unrecorded l iens not known by the pol icyholder.Items not covered by the policy include: defects and l iens l isted in the policy, defects known to the buyer, and changes brought about by zoning (although zoning coverage is available).I f any defects are found, the insurer may use i ts discret ion to exclude them from coverage:

The title insurer searches and examines the public record to identify those matters of record that affect real property and then determines whether any of these defects in title pose a threat of lossThis marks a major difference between a typical property-casualty (P & C) insurance policy (occurrence policy) and a title insurance policy. A typical P & C insurer expects a higher frequency of losses than a typical title insurer. This dif ference is reflected in the degree of r isk and level of r isk avoidance services provided by the insurer. Typical P & C premiums are charged annually and contain a large r isk bearing capacity (this capacity varies by l ine of insurance), whi le t it le insurance premiums are charged once (premiums average about 1/2 of 1 percent of proper ty value) and contain l itt le r isk bearing capacity.

TITLE INSURANCEAnother difference between a normal P & C policy and a title insurance policy is the length of coverage. A typical P & C contract is annual, while the title coverage is at least for the length of ownership of the property.

Unfortunately for title insurers, there are no statutes that require notification of property sale to title insurers from previous transactions. Thus, a title insurer has no way of knowing if its policy coverage has ended unless it is also the title insurer for the new owner.

COSTS OF TITLE INSURANCE Title insurance protection is significantly different from other lines of insurance. Typically, other types of insurance assume a particular risk and provide financial indemnity in the event the risk occurs. Title insurance, on the other hand, emphasizes loss prevention by eliminating risks caused by title problems arising from past events.

Approximately 25 percent of all residential real estate transactions have issues with the title – issues that are resolved by title professionals before closing. This emphasis on loss prevention results in fewer claims paid by title insurers compared to other lines of insurance.

However, loss prevention and clearing title issues is a labor-intensive and costly component of a title company’s operating budget. To compare, the expense ratio for title insurers averages 90 percent, while the expense ratio for property and casualty companies is less than 30 percent.

THE SEARCH PROCESS Searching the public records provides a basis for title insurance and usually includes visits to the offices of recorders or registers of deeds, clerks of courts and other officials. Title searchers look in the records for mortgages, judgments, street and sewer system assessments, special taxes and levies, and numerous other matters. In many jurisdictions, information about a piece of property and any liens against it may be filed in different ways. They can be filed under the seller’s name, the owner’s name, by lot number or by street address. To make the search process less cumbersome, many title companies have created title plants, which contain virtually the same information as the county records, but indexed in a consistent matter (i.e. by name or lot number) so that title searches may be performed more quickly and accurately. In major metropolitan areas, the title can be searched and title insurance issued within 24-48 hours. The following shows why it is a good idea to involve the title company in the early stages of a land transfer. In one transaction, the title search revealed that two acres of land being purchased were once part of a five-acre tract. A prior deed to the five acres restricted use of the property to “a single family dwelling and the usual out-buildings.”

THE SEARCH PROCESS The other three acres from the original tract already contained a single family dwelling, and there was a serious question as to whether the purchaser could build a home on his two acres. With assistance from the title company, releases were obtained from the appropriate parties to remove the problem and allow the house to be built.

Occasionally, title problems may be so serious that the most prudent course is not to proceed with a transaction. For example, a buyer was about to close his purchase when the title search revealed pipeline, utility, flood and road easements across the property that would have severely limited his use of the land. When these findings became known, the buyer declined to continue with the transaction. Only a title search would have uncovered these problems.

BENEFITING PARTIES Title insurance services offer a wide range of protection to the many different parties who have various interests in real estate transactions. The benefits of title insurance protect:

• Real Estate purchasers • Sel lers • Lenders • Real Estate Brokers • Attorneys • Homebuilders

BENEFITING PARTIES BUYERS Whether the transaction involves a multi-million dollar office building or a single-family home, the purchaser faces possible serious financial loss, or could lose the right to own the property altogether, if a serious cloud on the title goes undetected. An expert title search before the purchase will identify the nature of title and fix most problems that might be present. An Owner’s Policy offers protection against various hazards, including those even the most thorough search of the public records do not disclose, such as forgeries, missing heirs or recording errors. And, the Owner’s Policy will pay valid claims as well as defense costs against attacks on the title.

For a one-time premium that is modest in relation to the value of property involved, the purchaser receives the protection of a title policy backed by the reserves and solvency of an insurance company. In the unlikely event the insurance company ceases to operate, reserves offer the assurance that another insurer will accept risk for the existing policyholders.

BENEFITING PARTIES SELLERS Similarly, the seller wants to be sure his or her title is marketable in order to sell the property. A title insurer facilitates the flow of mortgage money by identifying title problems so they can be resolved whenever possible, and then by insuring against title risks. Title insurance encourages the expeditious completion of a transaction, thus the seller receives his or her money in a timely fashion. LENDERS Financial organizations are acutely concerned when it comes to the security of the funds they lend for real estate investments. The Loan Policy provides the lender a high degree of safety against loss of capital from title hazards. By identifying risks and eliminating them whenever possible, the title industry is a major element in encouraging lenders to invest in mortgages – rather than in other assets with lower risk.

BENEFITING PARTIES

LENDERS

The Loan Policy guarantees the lender a valid and enforceable lien, and assures that no claimant other than those noted in the policy has a prior claim against the real estate. The policy assures that the purchaser-borrower has title to the property being pledged as security for the loan. And, the policy obligates the title insurer to pay for defending against any claim filed against the title that might supersede the lender’s lien. If unsuccessful, it must also satisfy that claim should it be upheld in court.

Another benefit is the in-depth expertise of title company experts, who facilitate the mortgage loan process and help in resolving differences among the various parties in a transaction. This can range from relatively routine assistance in a basic residential loan to helping with the multifaceted legal and financial aspects of a complex, multi-million dollar commercial transaction. In the more complicated examples, the title company’s efforts on behalf of the lender can extend even further.

BENEFITING PARTIES BROKERS There is much to be gained by the real estate broker who calls the title insurance company in the early stages of a transaction. The security of title insurance greatly enhances the possibility for loan approval. And, abstract or title insurance personnel – by fast accurate verification of title or by swift resolution of a title problem – often make it possible to promptly complete a transaction that would have been seriously delayed or lost altogether. By calling the title company or its agent, the broker promptly becomes informed of the alternatives for clearing up title problems found in a search of public records, and learns in a timely manner what information the title company needs to issue the insurance. This close contact also enables the broker to become better informed on available title coverage so the parties can be readily assisted with their needs. .

BENEFITING PARTIES ATTORNEYS In some states, it is a real estate attorney who handles the closing. The attorney will create an attorney’s opinion to assess the condition of the real estate title. Title insurance enables the real estate attorney to offer the client substantially greater protection than what is attainable with a legal opinion alone. Title insurance resolves this dilemma by backing up the attorney’s title search with guaranteed financial indemnity from a licensed, regulated corporate insurer, and providing adequate capital and reserves to respond to claims.

The protection of title insurance extends far beyond the risk that may be incurred by the purchaser as a result of an error or negligence by the person performing the search and examination. Among the many risks covered by title insurance (that would not be covered by the attorney’s malpractice insurance) are: • Mistakes in the interpretation of wil ls or other legal documents • Impersonation of the owner • Forged deeds, mor tgage releases, etc.

BENEFITING PARTIES ATTORNEYS • Instruments executed under fabricated or expired powers of attorney • Deeds delivered af ter death of sel ler or buyer • Undisclosed or missing heirs • Wil ls not probated • Deeds or mor tgages by those mentally incompetent or of minor age (or supposedly single but actually married) • Bir th or adoption of children af ter date of wil l • Mistakes in the public records • Falsif ied records • Confusion from similarity of names • Transfer of t it le through foreclosure sale where requirements of foreclosure statue have not been strict ly met

While ALTA recommends that all parties to real estate transactions be represented by their own counsel, it is the view of the association that no real estate attorney adequately protects the interest of a client without advising that client of the availability and protection of title insurance.

HOMEBUILDERS Delays for the homebuilder can also be minimized by contacting the title company early in the building process. Actions initiated by the title company that have a positive effect on the builder’s project completion time can include the following:

• Cal l ing a meeting of everyone involved to establish coordination and minimize problems (bui lder, developer, attorney, engineer, architect, escrow holder, etc.) • Expediting t it le search and examination so any dif f icult ies can be dealt with more quickly • Advising on mechanic’s l ien coverage and other tit le insurance needs of par ties to the transaction • Setting up sale escrow accounts and handling disbursements upon closing • Coordinating with subcontractors so their problems can be dealt with in the early stages of the project • Arranging for prompt handling of any tit le claims that arise

By assuring priority of the first lien mortgage for the lender, title insurance makes construction loan financing considerably more attractive.

HOMEBUILDERS Title company personnel help the builder or developer establish ownership rights to assure local government that a project may proceed. This normally expedites plat approval. And, title companies will insure titles to individual lots in a development on a mass production basis, often at a reduced rate, so new owner’s policies can be promptly furnished to home buyers after updating of title work, rather than extensive and time-consuming back searches upon the issuance of each policy. Besides the basic owner and loan policies, title insurers offer various special coverages that are important to different parties. Additional coverages relating to new construction are available in some areas. These coverages could include mechanic’s lien protection, or special coverage regarding surveys or zoning.

SECONDARY MORTGAGE MARKET Beginning in the mid-1940s, the nationwide growth of a secondary mortgage market has proved to be an especially dramatic benefit for millions of American home buyers.

The positive effects of this phenomenon have reached out to numerous other related sectors of the economy. Essentially, the purpose of the secondary market is to broaden the base of investment for mortgage financing and attract funds from areas of the country with abundant capital to areas where mortgage money is needed. Unlike the New York Stock Exchange and other organized trading markets where representatives of buyers and sellers meet in a single location, the secondary market consists of a complex network of organizations, intermediaries and various channels of communication. Through this facility, lenders in one area of the country with funds to invest can readily make or purchase mortgage loans on real property located elsewhere. Secondary market operations may be as simple as a lender in California selling mortgage loans to another lender in New York, or as complex as the development and sale of Government National Mortgage Association pass-through securities, which are guaranteed by GNMA and are backed by a pool of mortgages worth millions of dollars.

SECONDARY MORTGAGE MARKET The need for protection from title problems is even more acute in dealing with mortgages in the secondary market than what is normally encountered by a local lender. Knowing the local customer and the attorney rendering an opinion may be sufficient for a local lender to lend and portfolio a mortgage. However, a title opinion from a local attorney will not provide the assurance for a national lender that is unfamiliar with local risks and/or unwilling to take a chance. In view of these considerations, it is easy to see why virtually every mortgage traded in the secondary market is covered by a Loan Policy. With financially sound corporate insurers standing behind the validity and enforceability of mortgage liens, marketability of insured loans is greatly improved.

National or out-of-town lenders know that, should a title problem develop on property located in a distant part of the country, they can deal with title company experts whose capabilities are well known who can quickly come to grips with the difficulty and initiate appropriate action.

SECONDARY MORTGAGE MARKET Mortgage loans on all types of real property constitute the nation’s largest single category of institutional investment. Loan policies have enhanced the remarkable growth in the availability of mortgage funds, which has brought an impressive stimulus to real estate investment from coast to coast. This expansive viability has been characterized by two major developments -- both directly linked to title insurance. • Mor tgage investment has become more secure.

• Mor tgage money has become widely avai lable throughout the country through the post -World War II development of a nationwide secondary mor tgage market.

SECONDARY MORTGAGE MARKET Safety of investment ranks at least equally with return realized where institutional investors are concerned. This fiduciary emphasis on security by the lending community means that the protection brought to real estate transactions by title insurance is vital if mortgage money is to remain widely available.

Without the title company’s assurance that the lender has a valid and enforceable lien, and that the borrower has marketable title, real estate investment would be considered highly speculative and would not enjoy its current high acceptance among lending institutions. Most lenders also know that the familiar ALTA Loan Policy, developed based on their input and voluntarily used by ALTA member title insurers, is a nationally prominent means of protection that adds even greater facility to trading within the secondary market.

OFFSHORE OUTSOURCING: A CASE STUDY

OFFSHORE OUTSOURCING: A CASE STUDY For years, title insurance companies have been using offshore data entry firms for back plant automation and day forward posting. This article is a case study of how First Dakota Title of South Dakota used offshore outsourcing to produce abstract and informational reports, saving the company time and money. ABSTRACT PROBLEM, CONCRETE SOLUTION Dennis Anderson, founder and president of First Dakota Title, was with his vice president of operations on a four hour drive from his headquarters in Sioux Falls, South Dakota, to Fargo, North Dakota, when the idea came up: Why not use his offshore data entry firm not just to key in information but to take the next step and actually produce complete reports? North and South Dakota both require title insurance companies to establish and maintain their own databases containing historical records of all real estate transactions in the counties where they do business. (In the Dakotas, such records can date back to land patents established in the late 19th century.)

OFFSHORE OUTSOURCING: A CASE STUDYHowever, unlike South Dakota, North Dakota requires the creation of an abstract for almost all transactions. This became a major consideration when Anderson decided to cross state lines and acquire a title company in Fargo. “We were wondering how we were going to do the abstracts,” says Anderson. “It seemed to us that they were time intensive, labor intensive and redundant. We considered what our of fshore data entry f irm was doing for us already: looking at the documents, determining who the grantors and grantees were, locating legal descriptions, and adding recording dates, f i l ing dates, and document numbers.

Then we thought: An abstract is basical ly a recompilation of that information. In addit ion to identifying bits and pieces, you’re retyping the document in the format required for an abstract. So we said, ‘They should be able to do that.’ And that star ted the wheels turning.”

OFFSHORE OUTSOURCING: A CASE STUDYFirst Dakota Title’s experience with offshore data entry began in 1989, before the company opened its doors. Anderson had averted a financially burdensome late start up by hiring a company called HDEP International to help create his backplant. A Honolulu based firm with data entry facilities in Manila, Philippines, HDEP took responsibility for the entry of 600,000 records—about half of First Dakota Title’s entire two county project. Anderson was pleased with the speed, accuracy, and motivation of the Manila operators.

Since then, the company has continued to rely on offshore outsourcing for an expanding array of products and services. In the mid ‘90s HDEP helped modernize First Dakota’s database by converting its microfilm records to digital images. By the time the company decided to expand to North Dakota last year, HDEP was providing offshore day forward data entry services for the company’s five South Dakota title plants—with the attendant advantages of reduced personnel requirements, lower labor costs, improved work flow, and off site security backup.

OFFSHORE OUTSOURCING: A CASE STUDY

“Deciding to outsource repor ts wasn’t easy,” says Anderson, “but we had worked with HDEP for over ten years and established a relationship of trust. We knew that their people understood not just the basics of real estate but how the bits and pieces of information f i t together. That made the process much easier than bringing in someone who didn’t have a clue what a deed or a mortgage is.

We also knew what HDEP was capable of doing and that they never promised what they couldn’t deliver. This comfor t level laid the foundation for having them advance through the examination process.”

THE HISTORY OF OFFSHORE DATA ENTRY American companies have sent large scale data entry work overseas since the early 1970s, taking advantage of lower labor costs outside the U.S. The first offshore projects went to the Caribbean, Ireland, the Philippines, Singapore, Taiwan and Korea. As the world adjusted to new computer and telecommunications technologies, the early years were filled with glitches. But the advent of fax services, inexpensive e mail, high speed Internet and T1 lines made communication between offshore data entry companies and their clients flow smoothly and easily. Courier and next day mail services became faster and more reliable as well. With the passage of time, countries developed their own specialty tasks—sometimes accidentally, sometimes because a country is geographically, linguistically, or sociologically closer to a particular type of customer. Economics also weighs in: Because of rising labor costs, Singapore, Taiwan, and Korea have proved unable to compete with companies in India, China, Sri Lanka, and the Philippines.

THE HISTORY OF OFFSHORE DATA ENTRYToday, due to its proximity to large New York advertising agencies, the Caribbean is regarded as the center for direct mail entry. Several Caribbean nations are also becoming centers for everything from toll free and directory assistance to the processing of tickets for U.S. based airlines. Due to English language limitations, the Chinese tend to concentrate on full text data entry from printed materials.

Companies in the Philippines, thanks to the strong English fluency of a large percentage of the populace, have gained expertise in difficult data entry tasks, including keying from public records, library conversions, and litigation support work. In the title insurance industry, as costs have lowered and speed and reliability have risen, offshore outsourcing has become increasingly attractive. Title plant managers who face shortages of skilled and committed data entry operators locally now turn with confidence to established offshore firms.

THE HISTORY OF OFFSHORE DATA ENTRY - THE QUANTUM LEAP It’s one thing to key in information for a title plant. It’s another thing to search and examine documents to create reports. The nature of basic data entry is “key what you see,” and although real estate data entry requires some interpretation, the operators are still basically looking at documents and filling in fields. Searching and examining the documents requires additional training, as does assembling findings into a finished report. That’s why, when Anderson first presented the idea to Virendra Nath, president of HDEP International, and Doug Bello, president of D. Bello Associates, Inc., they weren’t certain whether they wanted to take on the task. Bello, a consultant who specializes in designing and developing title plants and works with Nath as part of an industry alliance, the Title Team, whose services include consulting, data entry, digital imaging, and Internet hosting, was initially more reluctant than Nath.

THE HISTORY OF OFFSHORE DATA ENTRY - THE QUANTUM LEAP “When they asked us to consider doing the abstracts for them,” says Bello, “at f irst I thought, that’s not what we do. We should focus on bui lding t it le plants. But the more I thought about it and the more I talked to Virendra, the better the idea sounded. There’s no reason in this day and age that this type of a job can’t be done anywhere in the world, as long as you have the necessary experience.” Nath and Bello decided to accept the challenge and train a select group of their most experienced and motivated data entry operators in Manila to prepare reports for First Dakota Title.

“It was more than a minor step up,” says Shirley Thoelke, First Dakota Title’s operations officer, who in 1989 spent seven weeks in Manila training the HDEP staff in basic title insur ance data entry for her company. “The training required was over and above the usual, so it was a pretty big jump.” “We had our work cut out for us,” says Bello. “It was an entirely dif ferent process, a dif ferent set of ski l ls we had to generate. I would call i t a quantum leap.”

THE HISTORY OF OFFSHORE DATA ENTRY - THE QUANTUM LEAPOUT BY 5 P.M., BACK BY 8 A.M. Bello prepared himself by personally generating one hundred reports from his office in Burbank, CA. In this way he could replicate what the staff in Manila would be doing. When he felt confident that he had learned the procedure, he went to the Philippines to conduct the training. “In Burbank,” he says, “I was excited to be operating in real t ime on First Dakota’s system. Then I realized that at the end of the workday in Manila—literally on the other side of the world—the staf f would send the repor ts and go home; when they came back in the morning, our customers’ feedback (from Sioux Falls) would already be available. It was as if no time had passed.” The time difference between Manila and Sioux Falls works in everyone’s favor, because 5 p.m. in Sioux Falls is 6 or 7 a.m. in Manila, depending on daylight saving time.

THE HISTORY OF OFFSHORE DATA ENTRY - THE QUANTUM LEAPOUT BY 5 P.M., BACK BY 8 A.M.“We send Manila e mails with orders attached in two batches,” says Thoelke, “the f irst at about four in the af ternoon and the rest before we go home for the day.” The company sends an average of 20 to 24 orders a day, some days topping 30. “When we show up for work at eight in the morning,” says Thoelke, “they’re back. And they’re done right.” “It’s a 12 hour turnaround,” says Bello. “Like clockwork.” Accessing the server over a T 1 line, the Manila staff accesses First Dakota Title’s title plant and image data base, searches the property and the GI, enters reports directly onto First Dakota’s computers, then sends an e mail to confirm the submission. After a senior examiner reviews the reports on the computer, the process is complete.

THE HISTORY OF OFFSHORE DATA ENTRY - THE QUANTUM LEAP HDEP provides its title company clients with more than data entry, producing detailed exception reports that alert examiners to potential problem areas. It’s a relationship in which HDEP acts as a partner to the title company, acknowledging that both are involved in a complex process with high liabilities and experienced enough to intuitively recognize areas that require additional scrutiny. “Another thing,” says Thoelke, “is that the typing is accurate. We’ve tradit ionally had typists in the of f ice produce these repor ts, and we were always sending f i les back just for plain old, dumb clerical errors. That doesn’t happen anymore. They’re doing a wonder ful job. And they’ve taken a load of work away from our searchers and examiners.” “It’s worked out very well ,” says Anderson. “We’re pleased with their quality and their accuracy. And it has given us an oppor tunity to expand our services without signif icantly having to expand our staf f.”

THE HISTORY OF OFFSHORE DATA ENTRY - THE LEARNING CURVE Is of fshore outsourcing of f inished repor ts appropriate for every ti t le insurance company? “Back in 1989,” says Anderson, “when we were f irst considering doing of fshore keying, we were cautioned very strongly to be careful who we were working with. But we decided to go ahead with it , and over the years our relationship with HDEP grew stronger. If we hadn’t had this history with them, our l ikelihood of outsourcing repor ts to an of fshore company would have been very low.” “People used to have reservations about outsourcing of fshore,” says Thoelke. “Frankly, back in ’89 I had them too. But now we’ve been working successfully with HDEP for a long time. It’s the same as in any other industry, whether you’re outsourcing of fshore or within the states: Your success depends on the relationship you have with your service bureau and your own wil l ingness to provide the feedback they need. That’s a huge par t of i t .”

THE HISTORY OF OFFSHORE DATA ENTRY - THE LEARNING CURVE Is of fshore outsourcing of f inished repor ts appropriate for every ti t le insurance company? “When people cal l and ask for references,” says Anderson, “I always tell them to be very explicit in their instructions, so that everybody knows where they’re coming from and going to. You can expect i t to take some time for everybody to understand the terminology and the ideas behind it. In this industry we’re all doing the same thing, but we describe it in 20 dif ferent ways.” BEYOND THE ABSTRACT Abstracts aren’t the only reports HDEP creates for First Dakota. They also produce informational reports— basic profiles of properties, rather than in depth interpretations, also known as tract checks, letter reports or O&E searches. “Banks want this information at a minimal cost,” says Anderson, “because they use it primarily for home equity loans and other l ines of credit.” HDEP also prepares preliminary commitments for First Dakota—generally those involving properties which the company has already insured in a previous transaction.

THE HISTORY OF OFFSHORE DATA ENTRY - THE LEARNING CURVE Is of fshore outsourcing of f inished repor ts appropriate for every ti t le insurance company?BEYOND THE ABSTRACT “Next,” says Bello, “we’ll be doing commitments on proper ties they haven’t previously insured. Who would have thought?”

“We haven’t gone completely down the road to having HDEP do every thing ,” says Anderson, “but you can see where it’s heading. As they become more ski l led and competent at what they’re doing, as they gain a greater understanding of the process, we can definitely move ahead in that area.” “Today ,” says Nath, “an order comes directly in, we search the plant, identify documents and review them, prepare a repor t, and submit i t . The examiner reviews it, presses a button and prints i t out on company letterhead. At a time when the ti t le insurance industry is being compelled by customers to reduce costs and improve the t imeliness of their products, this is an excel lent way to do it.”