Tips and Tricks for Optimising Excel

77

www.hanrickcurran.com.au Optimising Excel™ Using Excel™ to optimise decision making and avoiding common problems with spreadsheets and financial analysis June 2014

-

Upload

hanrick-curran -

Category

Business

-

view

275 -

download

11

description

Tips and Tricks for Optimising and Using Excel - avoid common problems with spreadsheets and analysis

Transcript of Tips and Tricks for Optimising Excel

www.hanrickcurran.com.au

Optimising Excel™

Using Excel™ to optimise decision making and avoiding common problems with spreadsheets and financial analysis

June 2014

2experience. new thinking

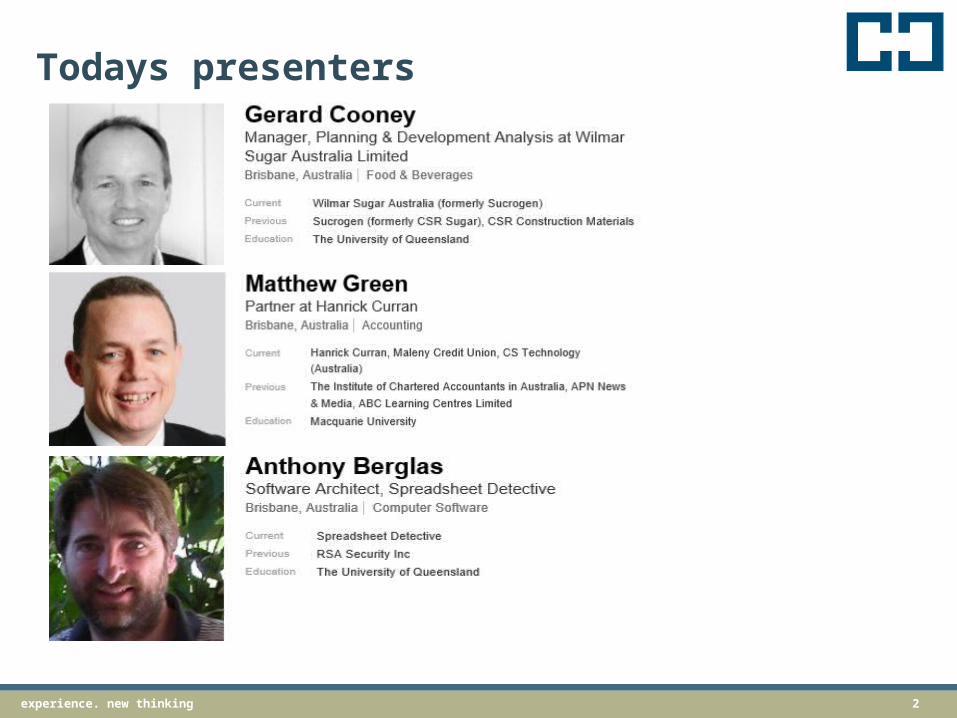

Todays presenters

3experience. new thinking

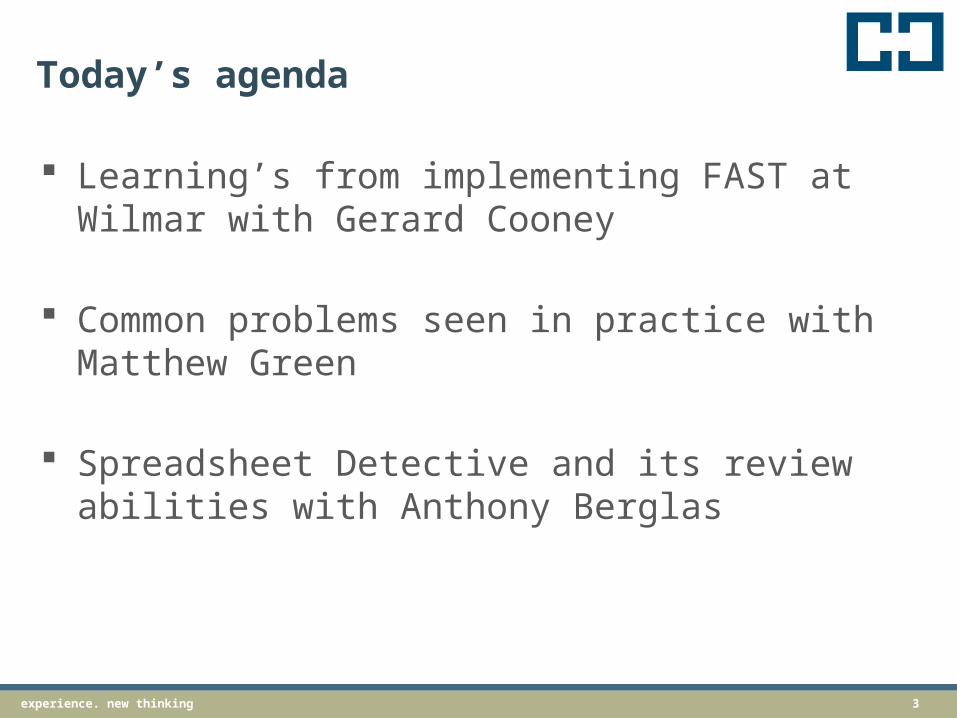

Today’s agenda

Learning’s from implementing FAST at Wilmar with Gerard Cooney

Common problems seen in practice with Matthew Green

Spreadsheet Detective and its review abilities with Anthony Berglas

4experience. new thinkingexperience. new thinking 4

Insights from implementing the FAST standard at Wilmar SugarGerard Cooney

Implementing FAST

5experience. new thinkingexperience. new thinking 5

A review of the implementation of the FAST modelling standard at Wilmar Sugar – Gerard Cooney(fomerly Sucrogen and CSR Sugar)

Implementing FAST

6experience. new thinking

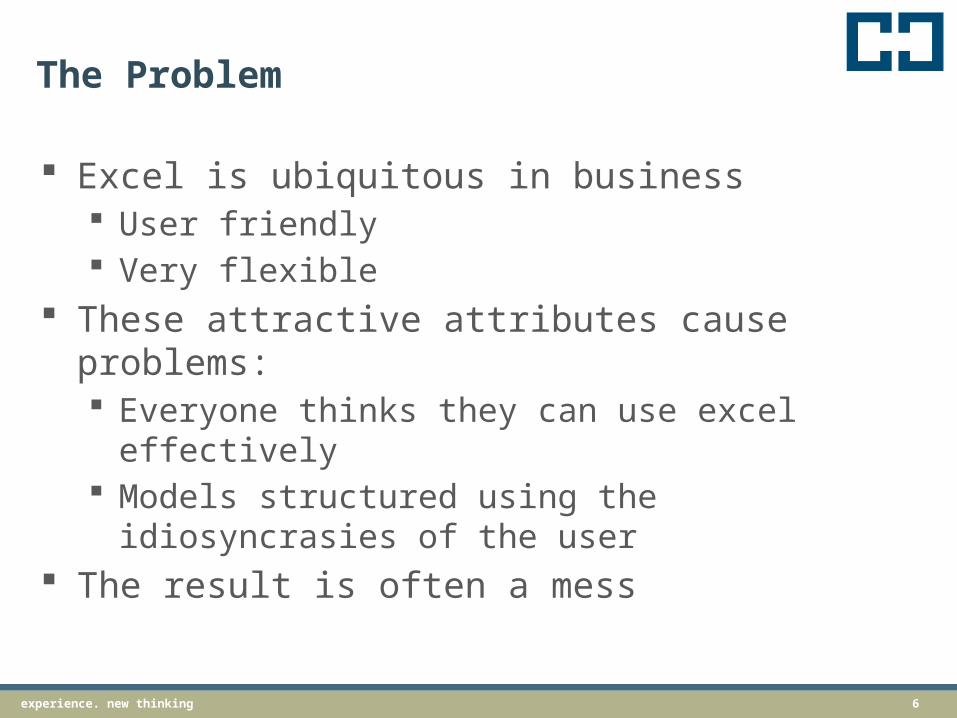

The Problem

Excel is ubiquitous in business User friendly Very flexible

These attractive attributes cause problems: Everyone thinks they can use excel

effectively Models structured using the idiosyncrasies of

the user The result is often a mess

7experience. new thinking

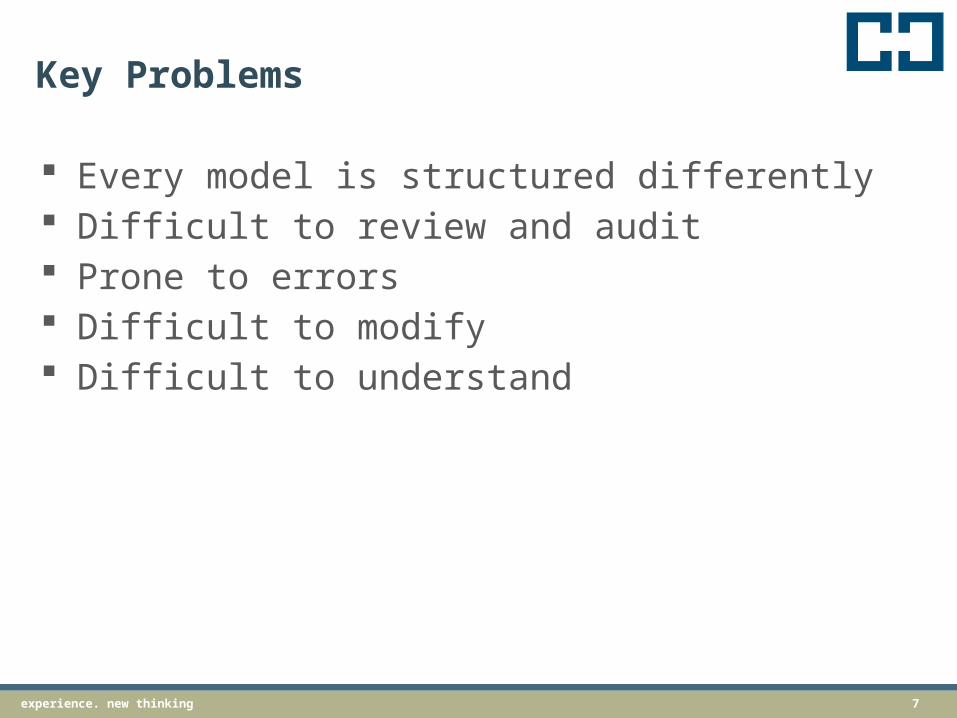

Key Problems

Every model is structured differently Difficult to review and audit Prone to errors Difficult to modify Difficult to understand

8experience. new thinking

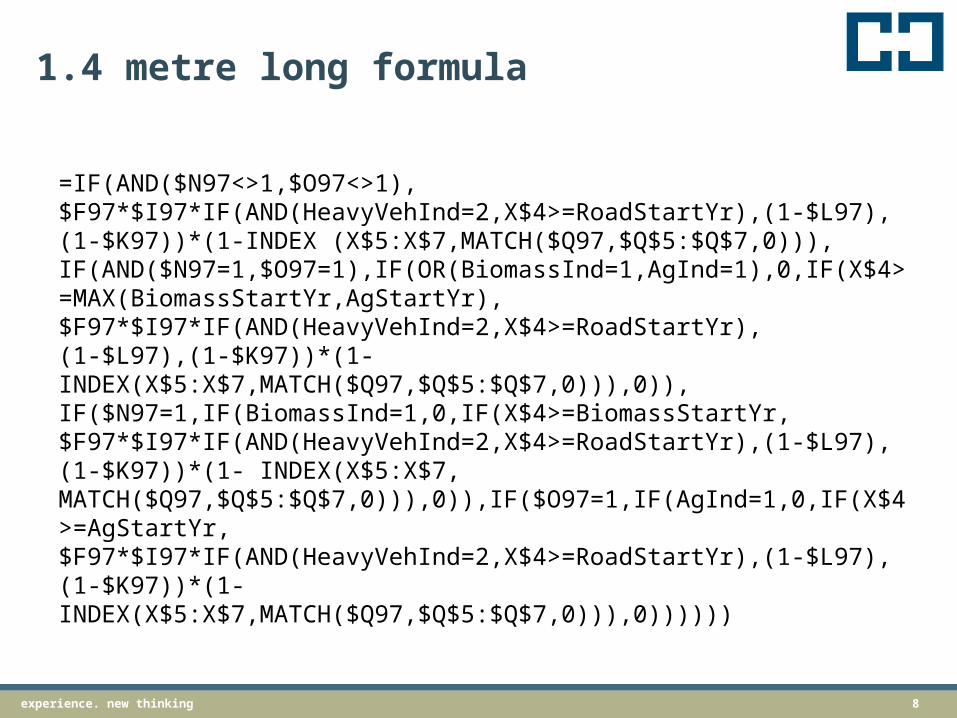

1.4 metre long formula

=IF(AND($N97<>1,$O97<>1),$F97*$I97*IF(AND(HeavyVehInd=2,X$4>=RoadStartYr),(1-$L97),(1-$K97))*(1-INDEX (X$5:X$7,MATCH($Q97,$Q$5:$Q$7,0))),IF(AND($N97=1,$O97=1),IF(OR(BiomassInd=1,AgInd=1),0,IF(X$4>=MAX(BiomassStartYr,AgStartYr), $F97*$I97*IF(AND(HeavyVehInd=2,X$4>=RoadStartYr),(1-$L97),(1-$K97))*(1-INDEX(X$5:X$7,MATCH($Q97,$Q$5:$Q$7,0))),0)),IF($N97=1,IF(BiomassInd=1,0,IF(X$4>=BiomassStartYr,$F97*$I97*IF(AND(HeavyVehInd=2,X$4>=RoadStartYr),(1-$L97),(1-$K97))*(1- INDEX(X$5:X$7,MATCH($Q97,$Q$5:$Q$7,0))),0)),IF($O97=1,IF(AgInd=1,0,IF(X$4>=AgStartYr,$F97*$I97*IF(AND(HeavyVehInd=2,X$4>=RoadStartYr),(1-$L97),(1-$K97))*(1-INDEX(X$5:X$7,MATCH($Q97,$Q$5:$Q$7,0))),0))))))

9experience. new thinking

THE FAST STANDARD

What does it stand for? Flexible Accurate Structured Transparent

http://www.fast-standard.org/

10experience. new thinking

FLEXIBLE

Design and modelling techniques must allow models to be both flexible in the immediate term and adaptable in the longer term.

Flexibility is born of simplicity.

11experience. new thinking

APPROPRIATE/ACCURATE

Models must reflect key business assumptions directly and faithfully without being over-built or cluttered with unnecessary detail.

12experience. new thinking

STRUCTURED

Rigorous consistency in model layout and organization is essential to retain a model’s logical integrity over time, particularly as a model’s author may change.

13experience. new thinking

TRANSPARENT

Simple, clear formulas that can be understood by other modellers and non-modellers alike. Confidence in a financial model’s integrity can only be assured with clarity of logic structure and layout.

14experience. new thinking

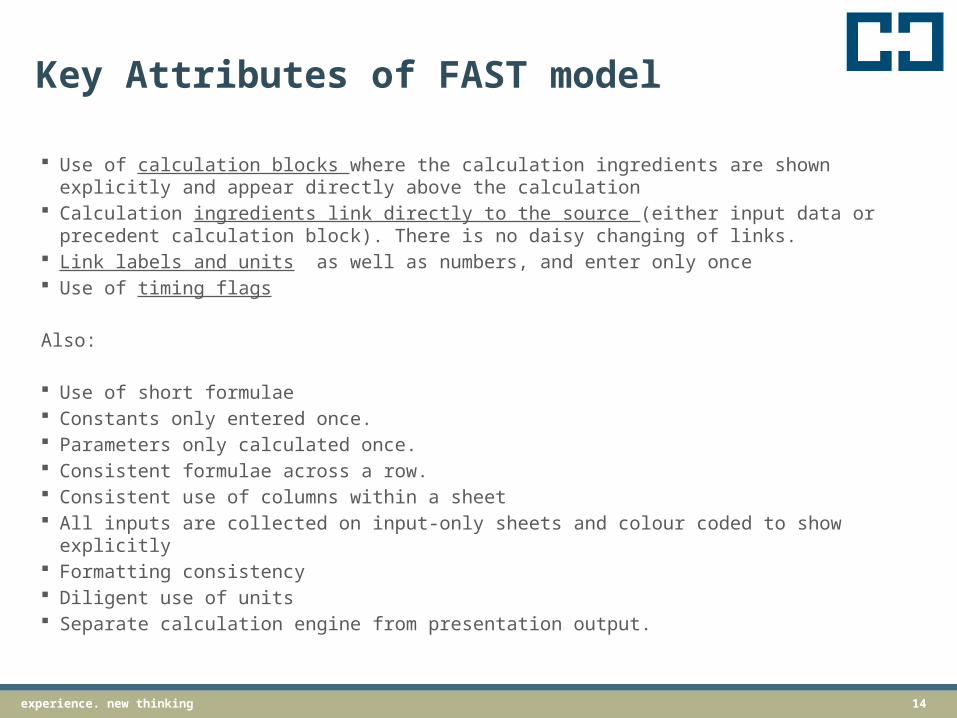

Key Attributes of FAST model

Use of calculation blocks where the calculation ingredients are shown explicitly and appear directly above the calculation

Calculation ingredients link directly to the source (either input data or precedent calculation block). There is no daisy changing of links.

Link labels and units as well as numbers, and enter only once Use of timing flags

Also:

Use of short formulae Constants only entered once. Parameters only calculated once. Consistent formulae across a row. Consistent use of columns within a sheet All inputs are collected on input-only sheets and colour coded to show explicitly Formatting consistency Diligent use of units Separate calculation engine from presentation output.

15experience. new thinking

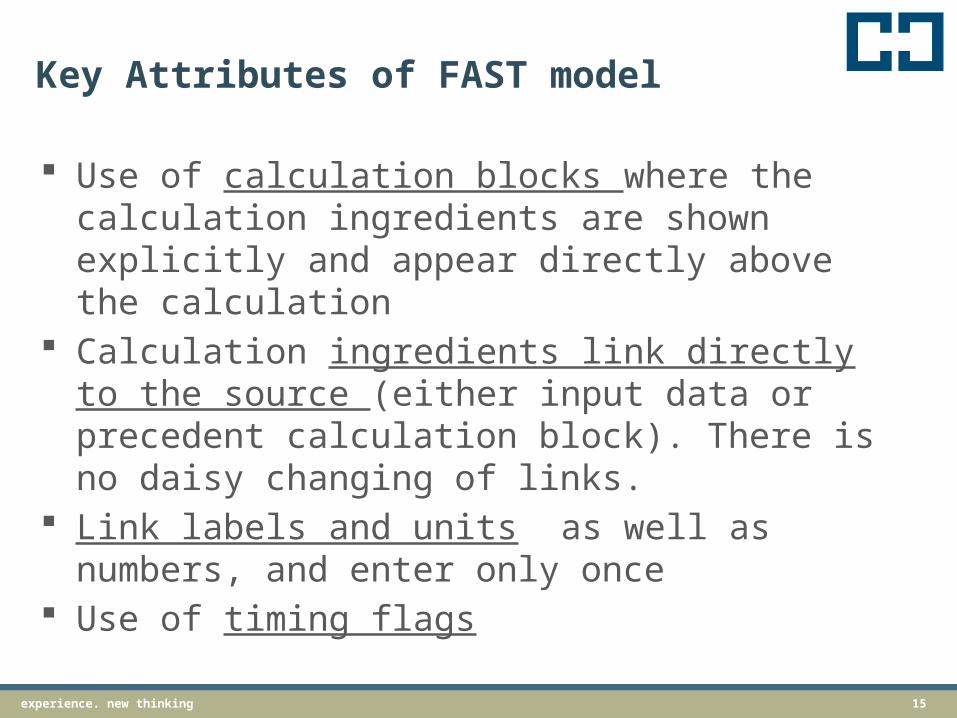

Key Attributes of FAST model

Use of calculation blocks where the calculation ingredients are shown explicitly and appear directly above the calculation

Calculation ingredients link directly to the source (either input data or precedent calculation block). There is no daisy changing of links.

Link labels and units as well as numbers, and enter only once

Use of timing flags

16experience. new thinking

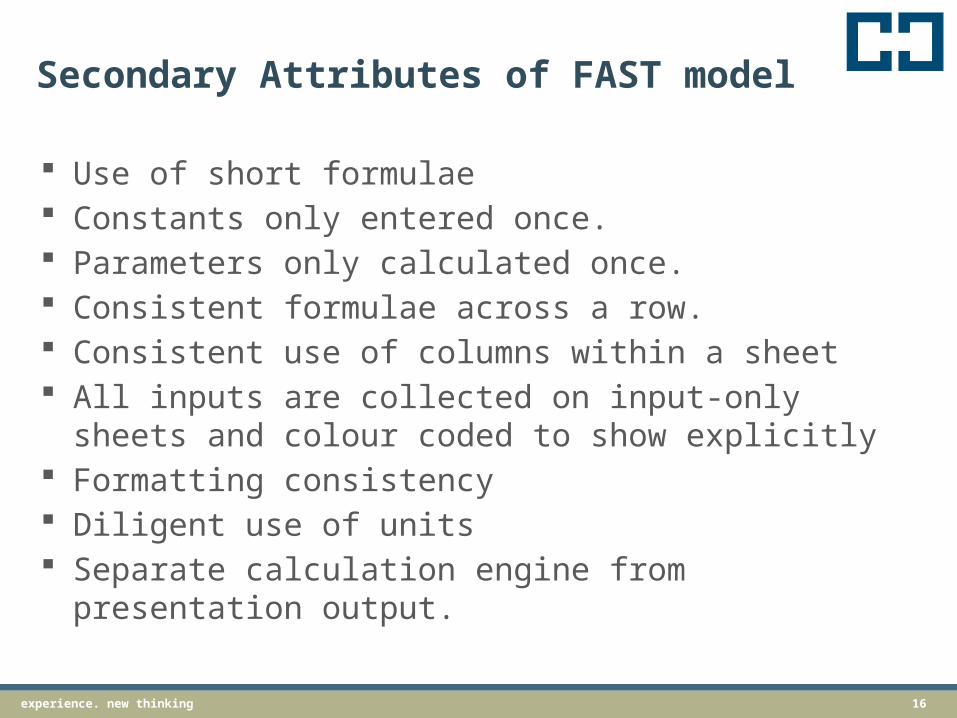

Secondary Attributes of FAST model

Use of short formulae Constants only entered once. Parameters only calculated once. Consistent formulae across a row. Consistent use of columns within a sheet All inputs are collected on input-only sheets

and colour coded to show explicitly Formatting consistency Diligent use of units Separate calculation engine from presentation

output.

17experience. new thinking

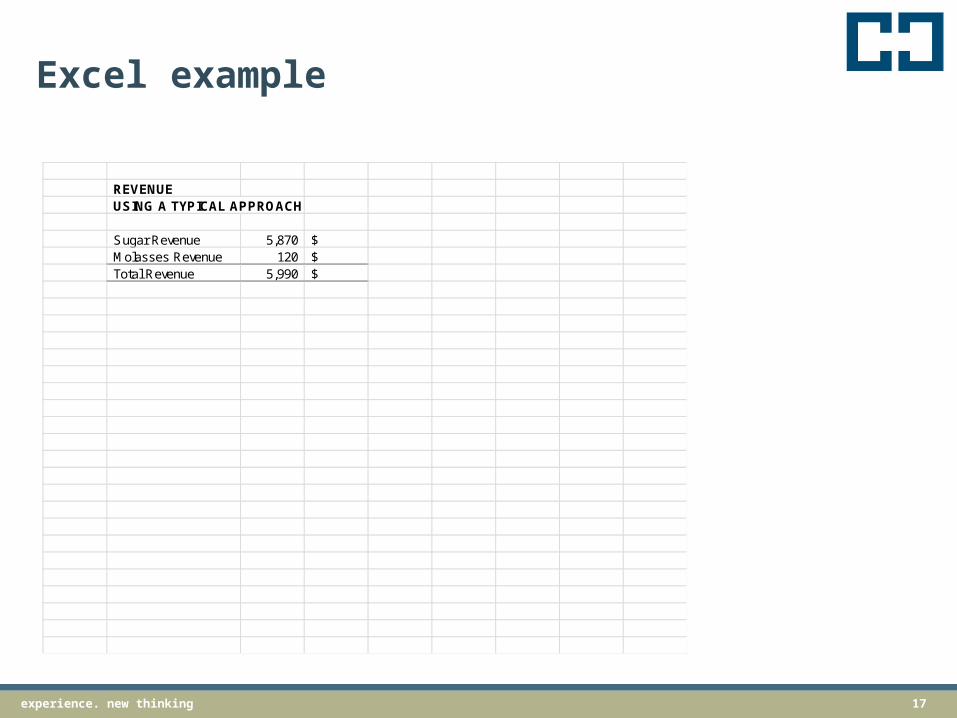

Excel example

REVENUE USING A TYPICAL APPROACH

Sugar Revenue 5,870 $ Molasses Revenue 120 $ Total Revenue 5,990 $

18experience. new thinking

Common Complaints

Doesn’t a standard approach stifle creativity It takes too long to model using the FAST

Standard

19experience. new thinking

Resources

http://www.fast-standard.org/

http://info.f1f9.com/31-day-financial-modelling-course

http://www.fi-mech.com/

http://www.financialmodellinghandbook.com/

20experience. new thinkingexperience. new thinking 20

Understanding the common issues we see with Excel™ spreadsheets, some conceptual insight into how errors occur and some suggestions on how to prevent them…Matthew Green

Common issues with Excel™ spreadsheets and models

21experience. new thinking

My agenda

How prevalent is Excel™ Common problems Error research The need for graphical presentation of data 7 steps to review your spreadsheets Practical learning's and takeaways

22experience. new thinking

Typical balance sheet

Excel used in the following key areas and calculations: Account reconciliations Other asset listings and

amortisation Fixed asset registers and

depreciation Deferred and current tax Intangible asset reconciliations Impairment models Debt covenants Interest accruals Employee benefits Derivative reconciliations and to

cross check bank valuations Spreadsheets for transactional

reports with Pivot tables for further analysis

Consolidation schedules

23experience. new thinkingexperience. new thinking 23

"I suppose it is tempting, if the only tool you have is a hammer, to treat everything as if it were a nail."

Abraham Maslow, 1966

24experience. new thinking

Excel & Accountants …“like giving your kid a chainsaw, powerful tool, but does he really understand what he’s got in his hands and how to use it?” You have to ask yourself: “Is this going to end well?” (And “No, he’s not getting one for Christmas!”)

25experience. new thinking

How many problems really exist?

“In our experience, most spreadsheets are poorly developed. This is probably because there isn’t much formal training on how to build a spreadsheet and people don’t have time to build them so that they are optimised for their purpose and to support decision making.”

Want to see some examples?

26experience. new thinking

Common problems

Confusing, complicated formula Unstructured layout Formula & Function errors Range & Pointing errors Hard coding Remote references Empty precedents

27experience. new thinking

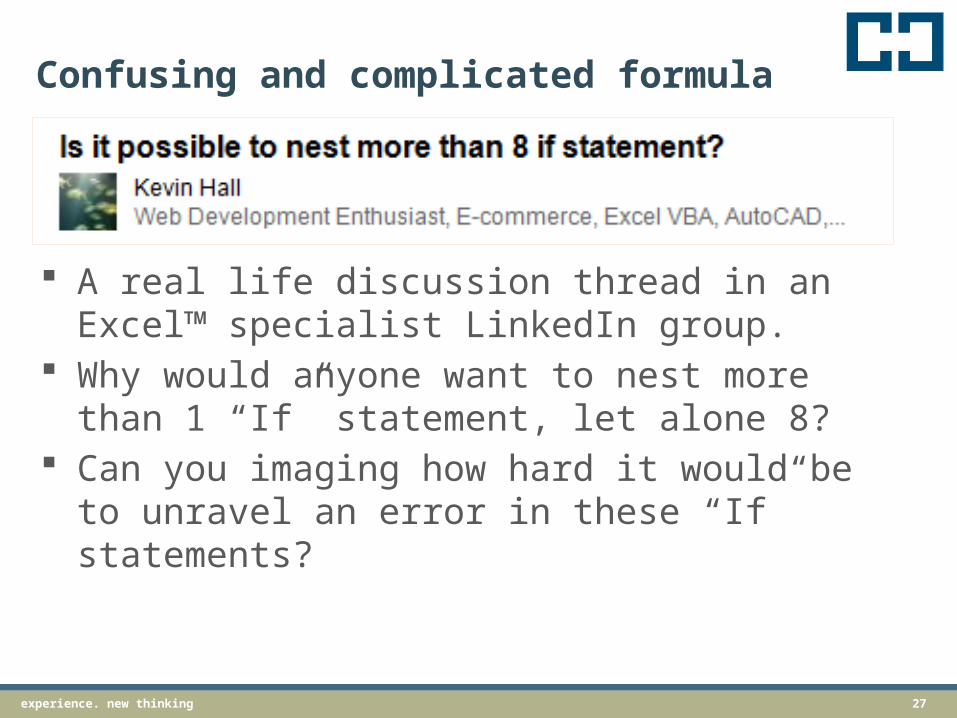

Confusing and complicated formula

A real life discussion thread in an Excel™ specialist LinkedIn group.

Why would anyone want to nest more than 1 “If” statement, let alone 8?

Can you imaging how hard it would be to unravel an error in these “If” statements?

28experience. new thinking

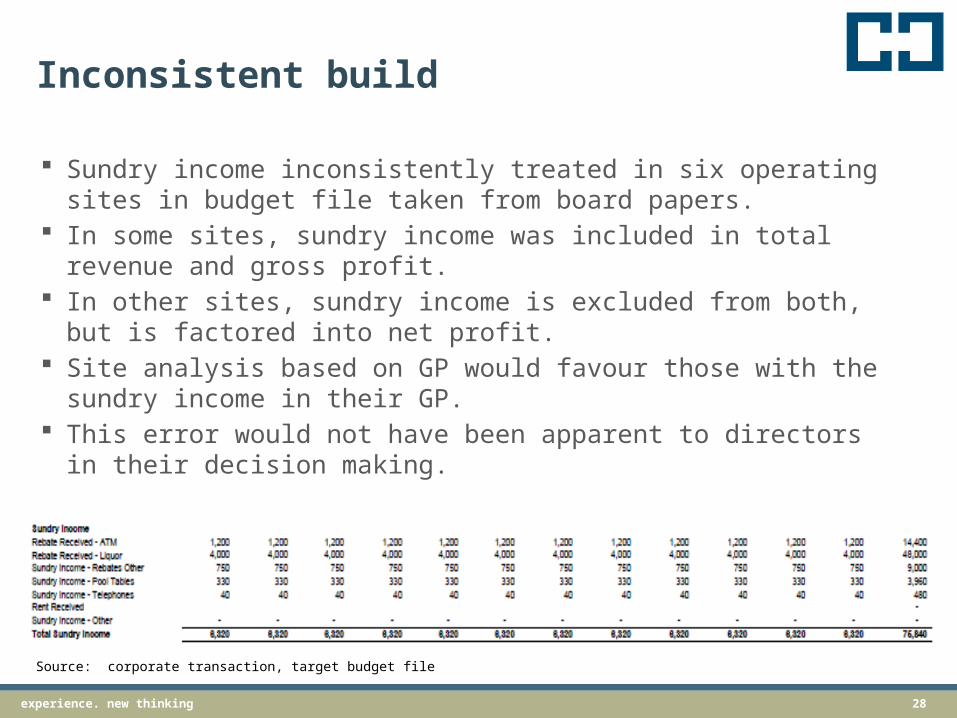

Inconsistent build

Sundry income inconsistently treated in six operating sites in budget file taken from board papers.

In some sites, sundry income was included in total revenue and gross profit.

In other sites, sundry income is excluded from both, but is factored into net profit.

Site analysis based on GP would favour those with the sundry income in their GP.

This error would not have been apparent to directors in their decision making.

Source: corporate transaction, target budget file

29experience. new thinking

Inconsistent build

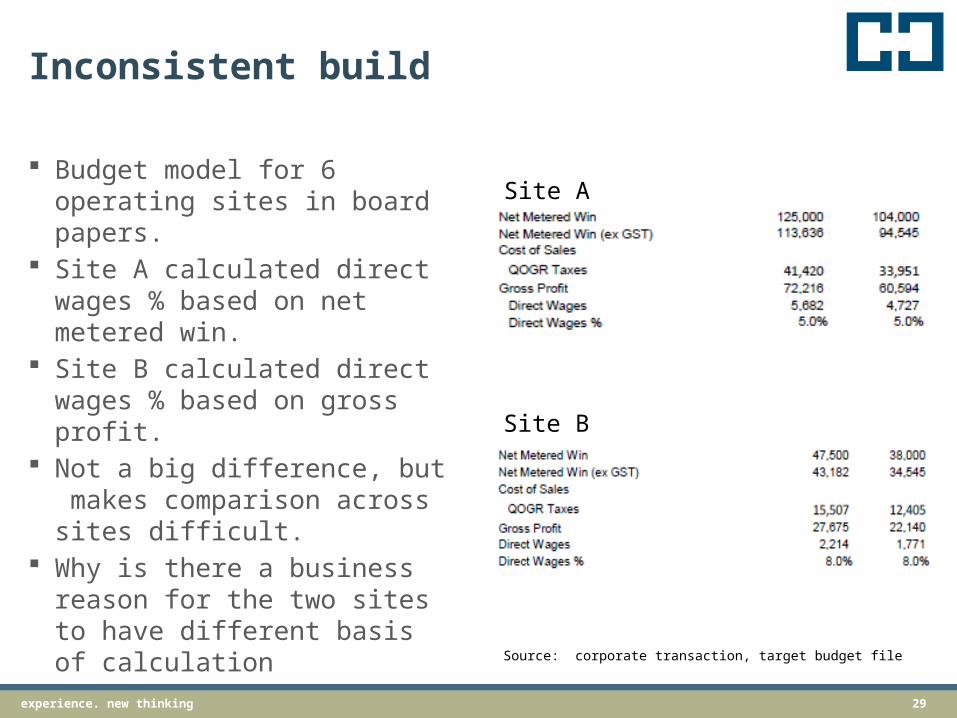

Budget model for 6 operating sites in board papers.

Site A calculated direct wages % based on net metered win.

Site B calculated direct wages % based on gross profit.

Not a big difference, but makes comparison across sites difficult.

Why is there a business reason for the two sites to have different basis of calculation

Site A

Site B

Source: corporate transaction, target budget file

30experience. new thinking

Hard coding and format

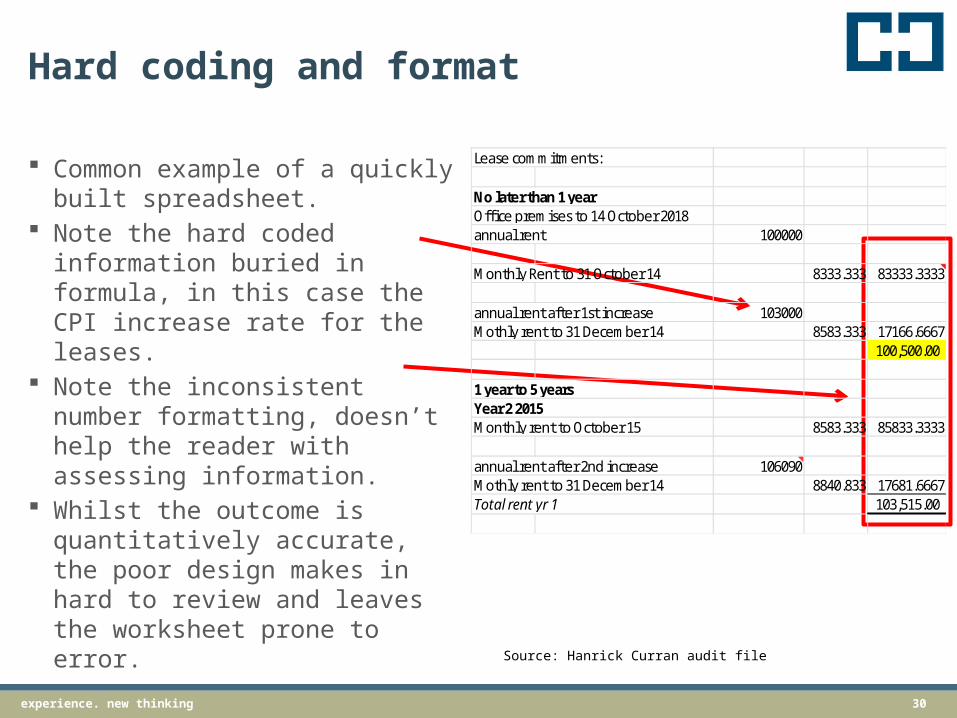

Common example of a quickly built spreadsheet.

Note the hard coded information buried in formula, in this case the CPI increase rate for the leases.

Note the inconsistent number formatting, doesn’t help the reader with assessing information.

Whilst the outcome is quantitatively accurate, the poor design makes in hard to review and leaves the worksheet prone to error.

Lease commitments:

No later than 1 yearOffi ce premises to 14 October 2018annual rent 100000

Monthly Rent to 31 October 14 8333.333 83333.3333

annual rent after 1st increase 103000Mothly rent to 31 December 14 8583.333 17166.6667

100,500.00

1 year to 5 years Year 2 2015Monthly rent to October 15 8583.333 85833.3333

annual rent after 2nd increase 106090Mothly rent to 31 December 14 8840.833 17681.6667Total rent yr 1 103,515.00

Source: Hanrick Curran audit file

31experience. new thinking

Hard coding

Commonly seen on ad hoc spreadsheets. Typically involves a formula like:

= C5 * (A36 + 1.03) – 408 + 12 The reviewer can usually decipher that the 1.03 is

probably CPI, but what about the other adjustments. A better way is to put the CPI number in its own cell

as an input. Hard coded adjustments should also be avoided. If

needed, build data entry cells for adjustments.Example of problem use of hard coding

Source: Hanrick Curran client board reporting file

32experience. new thinking

Remote references

A “remote reference” is a reference in a formula to cells that are remote from the worksheet the formula is on, either to another worksheet in the same file or to a different file.

Remote references are difficult to review and prone to errors. We recommend they be avoided by using a ‘links sheet’ in a

workbook for all ‘cross-file links’. Formula within a workbook should also avoid remote

references by gathering all needed data and then using the formula

Source: Hanrick Curran client board reporting file

Source: Hanrick Curran client board reporting file

Example of problem use of remote references

Example of corrected approach to use of remote references

33experience. new thinking

How big can the errors get?

In January 2010, academics Carmen Reinhart and Kenneth Rogoff published “Growth in a Time of Debt”.

Their report was widely cited by politicians as theoretical and research based support for reducing public debt and public spending.

Later analysis reveals errors with the underlying spreadsheet analysis; countries are excluded from the average because of a ‘range error’.

Great Brittan slashes spending by £10 billion, in response to the research and increase in debt following in the GFC.

Source: Quartz website, http://qz.com/75119Pasted from <http://qz.com/75119/how-to-avoid-making-an-excel-mistake-like-rogoff-and-reinhart/>

34experience. new thinking

Reinhart & Rogoff’s public problems

Source: Australian Financial Review, 23 April 2013

35experience. new thinking

Allied Irish Bank – US$691 m. Fraud

AIB is one of the Irish big 4 commercial banks, parent of Allfirst Bank, based in Baltimore, Maryland, US.

John Rusnak, committed a US$691 million currency trading fraud.

Rather than pay $10,000 fee for a Reuters feed to the treasury compliance team (back office) the data feed to the VaR calculation was based on data from Rusnak’s computer.

The data was loaded into a spreadsheet which Rusnak manipulated to ensure that trading losses were otherwise hidden from the VaR assessment.

Source: AIB p.l.c. SEC filing, March 12, 2002Source: R. Butler, “The role of Spreadsheets in the Allied Irish Bank / Allfirst Currency Trading Fraud” (2009) VaR = Value-at-Risk

36experience. new thinking

Allied Irish Bank – US$691 m. Fraud

AIB SEC Filing: “A simple check to see if the holdover figures were captured in the next day's trading activity would have caught this scheme.”

At least two points of failure:1. Data in spreadsheets was open to

manipulation2. Compensating controls were not

strong enough to detect the manipulation

Source: AIB p.l.c. SEC filing, March 12, 2002Source: Hanrick Curran research

37experience. new thinking

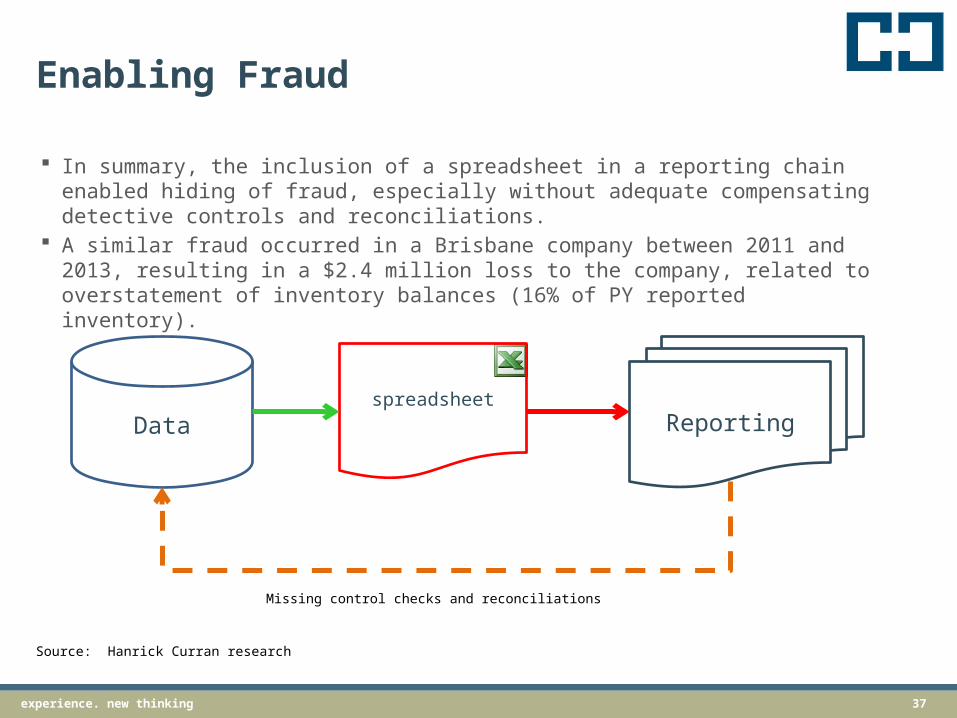

Enabling Fraud

In summary, the inclusion of a spreadsheet in a reporting chain enabled hiding of fraud, especially without adequate compensating detective controls and reconciliations.

A similar fraud occurred in a Brisbane company between 2011 and 2013, resulting in a $2.4 million loss to the company, related to overstatement of inventory balances (16% of PY reported inventory).

Source: Hanrick Curran research

Dataspreadsheet

Reporting

Missing control checks and reconciliations

38experience. new thinkingexperience. new thinking 38

Raymond Panko, University of Hawaii, has undertaken significant research into spreadsheet errors. Panko’s research informs the classification of errors in spreadsheets.

Error taxonomy and research

39experience. new thinking

Error research

There is a significant amount of research into human error from fields as diverse as mathematics, programming, aircraft accidents, nuclear incidents, proofreading and linguistics.

A key insight from these fields is that “human cognitive processes produce the correct result nearly all the time but have a small inherent error rate that stems from the same processes that produce correct results. In other words, the way we actually think … is the heart of the problem, not simple sloppiness.”

Source: Raymond Panko and Salvatore Aurigemma “Revising the Panko-Halverson Taxonomy of Spreadsheet Errors” (February 2010) p.4

40experience. new thinking

Mistakes, Slips and Lapses

When working with spreadsheets, errors can be categorised as follows (Reason, 1990): Mistake – an error in planning Slip – an error during a sensory-motor action, such

as typing the wrong number in a cell (e.g., $120,000 instead of $210,000)

Lapse – a failure in memory, usually caused by overloading the limited human memory capacity

In terms of error detection, planning and memory errors that occur ‘off spreadsheet’ leave little if any evidence for error detection.

Source: Raymond Panko and Salvatore Aurigemma “Revising the Panko-Halverson Taxonomy of Spreadsheet Errors” (February 2010) p.5

41experience. new thinking

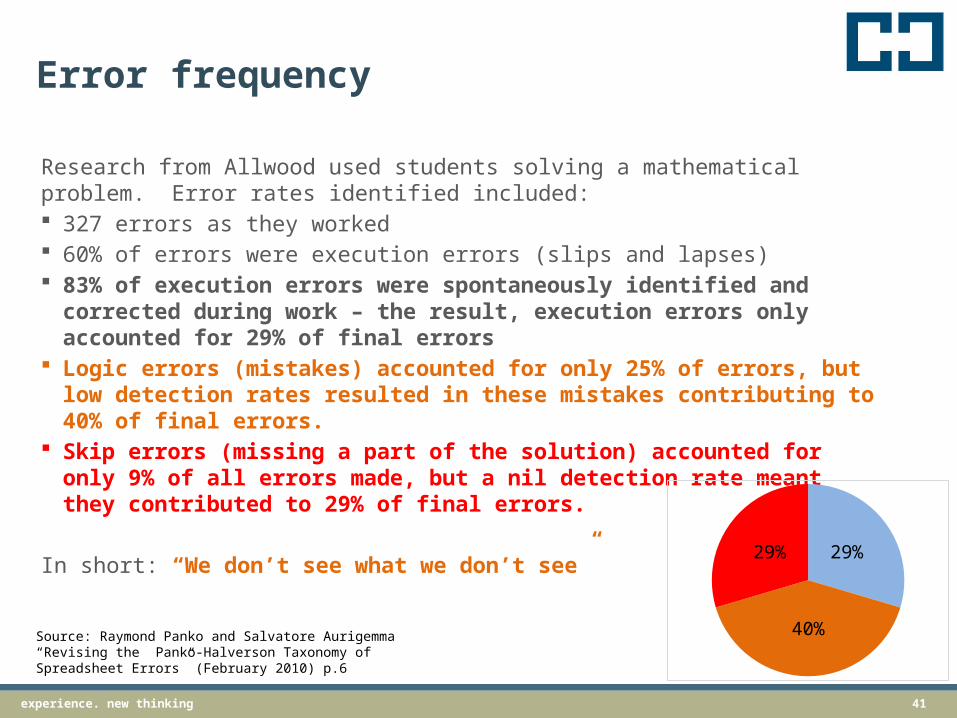

Error frequency

Research from Allwood used students solving a mathematical problem. Error rates identified included: 327 errors as they worked 60% of errors were execution errors (slips and lapses) 83% of execution errors were spontaneously identified and

corrected during work – the result, execution errors only accounted for 29% of final errors

Logic errors (mistakes) accounted for only 25% of errors, but low detection rates resulted in these mistakes contributing to 40% of final errors.

Skip errors (missing a part of the solution) accounted for only 9% of all errors made, but a nil detection rate meant they contributed to 29% of final errors.

In short: “We don’t see what we don’t see”

Source: Raymond Panko and Salvatore Aurigemma “Revising the Panko-Halverson Taxonomy of Spreadsheet Errors” (February 2010) p.6

29%

40%

29%

42experience. new thinking

Qualitative error impacts

When considering errors, we need to assess their impact on the final result. Panko suggests two approaches:1. Error magnitude – how big is the error

compared to the final correct bottom-line number

2. Would a different decision be taken based on correct versus incorrect results.

Panko and Halverson conclude that “most errors are either too small to be important or still give answers that lead to the correct decisions”.

Source: Raymond Panko and Salvatore Aurigemma “Revising the Panko-Halverson Taxonomy of Spreadsheet Errors” (February 2010) p.8

43experience. new thinking

Panko & Halverson error taxonomy

A revised error taxonomy is described by Panko and Halverson.

Source: Raymond Panko and Salvatore Aurigemma “Revising the Panko-Halverson Taxonomy of Spreadsheet Errors” (February 2010) p.25

44experience. new thinking

Panko & Halverson error taxonomy

A revised error taxonomy is described by Panko and Halverson.

Domain type errors (e.g., misunderstanding requirements or not correctly reflecting business requirements) are the most likely error to remain undetected and to result in an undetected error in the spreadsheet.

Execution errors (e.g., incorrect formula references) are most likely to be corrected during spreadsheet development and review, but can also leave undetected errors in spreadsheets (e.g., Reinhart & Rogoff).

Source: Raymond Panko and Salvatore Aurigemma “Revising the Panko-Halverson Taxonomy of Spreadsheet Errors” (February 2010) p.25

45experience. new thinkingexperience. new thinking 45

Graphing outputs of spreadsheets is important. Some examples of why follow…

A segue into the graphic display of information

46experience. new thinking

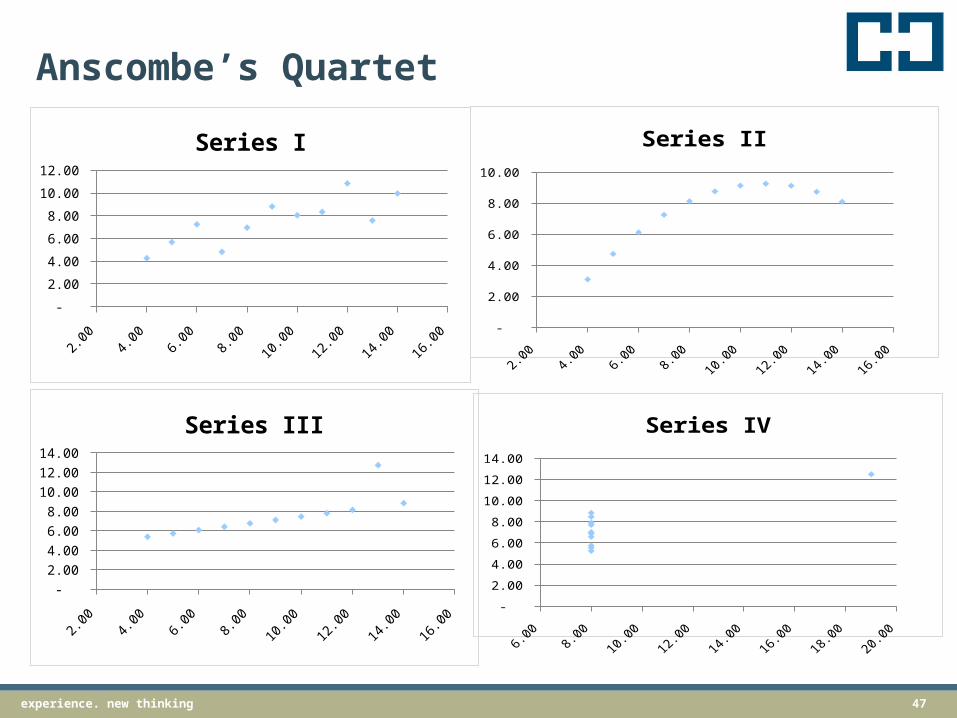

Anscombe’s Quartet

Four data sets with similar characteristics

X average = 9.0 Y average = 7.5

X sum = 99.0 Y sum = 82.5

x y x y x y x y 10.00 8.04 10.00 9.14 10.00 7.46 8.00 6.58 8.00 6.95 8.00 8.14 8.00 6.77 8.00 5.76 13.00 7.58 13.00 8.74 13.00 12.74 8.00 7.71 9.00 8.81 9.00 8.77 9.00 7.11 8.00 8.84 11.00 8.33 11.00 9.26 11.00 7.81 8.00 8.47 14.00 9.96 14.00 8.10 14.00 8.84 8.00 7.04 6.00 7.24 6.00 6.13 6.00 6.08 8.00 5.25 4.00 4.26 4.00 3.10 4.00 5.39 19.00 12.50 12.00 10.84 12.00 9.13 12.00 8.15 8.00 5.56 7.00 4.82 7.00 7.26 7.00 6.42 8.00 7.91 5.00 5.68 5.00 4.74 5.00 5.73 8.00 6.89 sum

99.0 82.5 99.0 82.5 99.0 82.5 99.0 82.5 Average

9.0 7.5 9.0 7.5 9.0 7.5 9.0 7.5

I II III IV

Source: Wikipedia

47experience. new thinking

Anscombe’s Quartet

2.00 4.00 6.00 8.00 10.00 12.00 14.00 16.00 -

2.00

4.00

6.00

8.00

10.00

12.00

Series I

2.00 4.00 6.00 8.00 10.00 12.00 14.00 16.00 -

1.00 2.00 3.00 4.00 5.00 6.00 7.00 8.00 9.00

10.00

Series II

2.00 4.00 6.00 8.00 10.00 12.00 14.00 16.00 -

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Series III

6.00 8.00 10.00 12.00 14.00 16.00 18.00 20.00 -

2.00

4.00

6.00

8.00

10.00

12.00

14.00

Series IV

48experience. new thinking

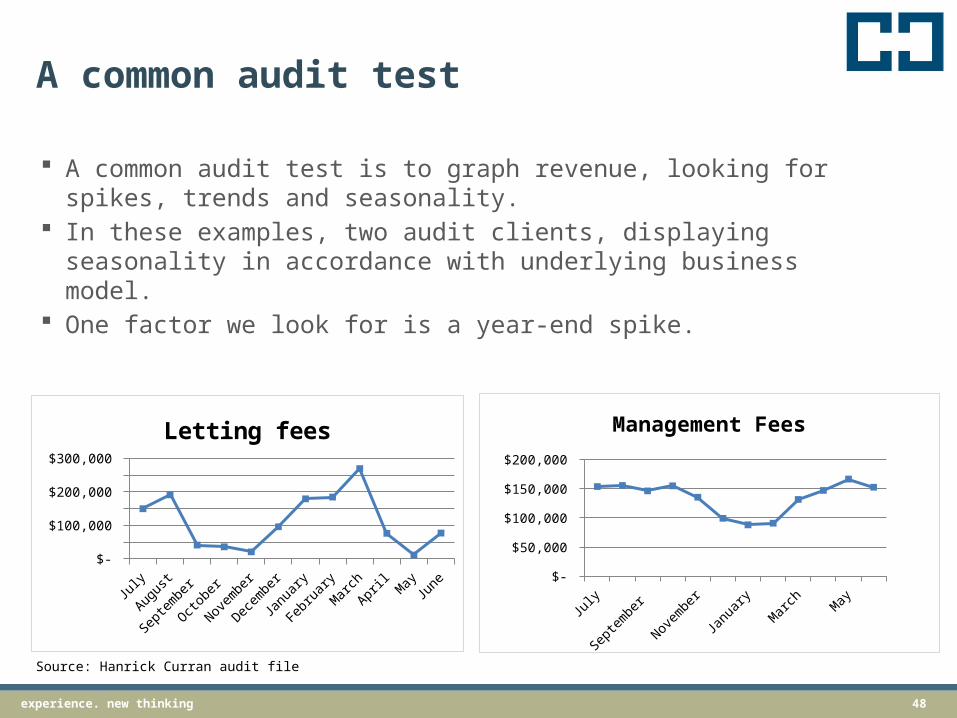

A common audit test

A common audit test is to graph revenue, looking for spikes, trends and seasonality.

In these examples, two audit clients, displaying seasonality in accordance with underlying business model.

One factor we look for is a year-end spike.

July

August

Septem

ber

October

November

December

January

Febru

aryMarc

hApril

MayJune

$-

$50,000

$100,000

$150,000

$200,000

$250,000

$300,000

Letting fees

July

Augus

t

Sept

embe

r

Octob

er

Novem

ber

Decem

ber

Janu

ary

Febr

uary

March

April

MayJu

ne $-

$50,000

$100,000

$150,000

$200,000

Management Fees

Source: Hanrick Curran audit file

49experience. new thinking

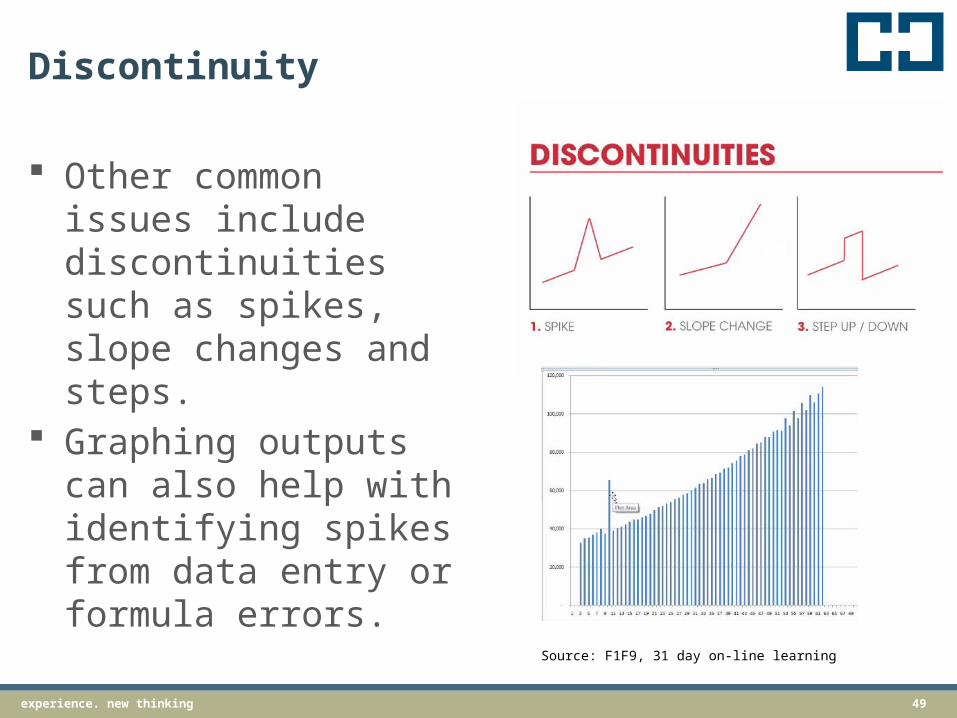

Discontinuity

Other common issues include discontinuities such as spikes, slope changes and steps.

Graphing outputs can also help with identifying spikes from data entry or formula errors.

Source: F1F9, 31 day on-line learning

50experience. new thinking

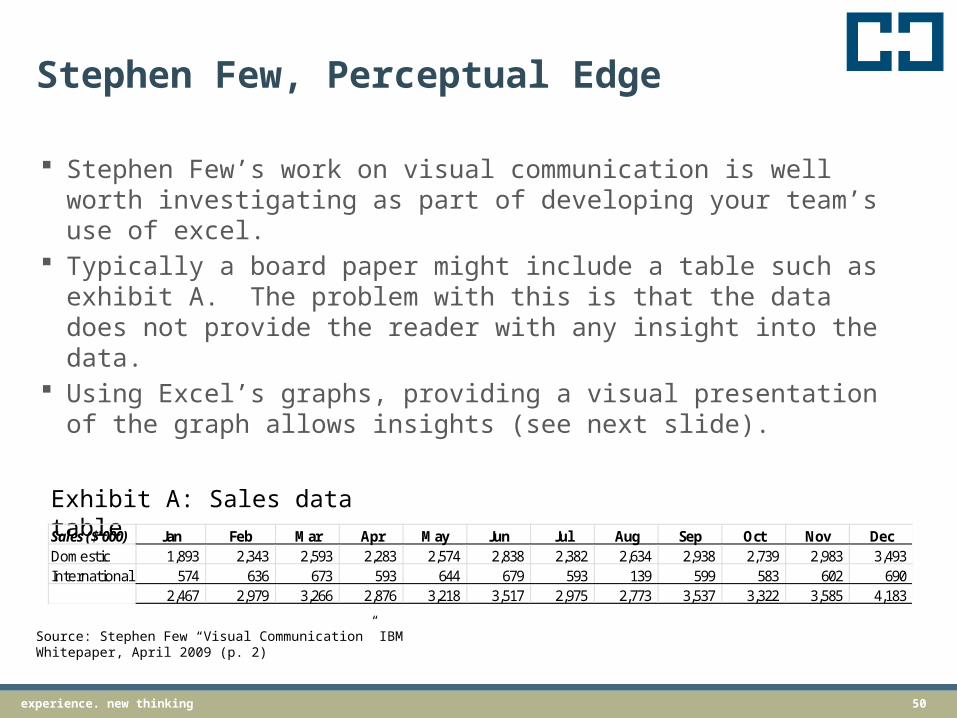

Stephen Few, Perceptual Edge

Stephen Few’s work on visual communication is well worth investigating as part of developing your team’s use of excel.

Typically a board paper might include a table such as exhibit A. The problem with this is that the data does not provide the reader with any insight into the data.

Using Excel’s graphs, providing a visual presentation of the graph allows insights (see next slide).

Sales ($'000) Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecDomestic 1,893 2,343 2,593 2,283 2,574 2,838 2,382 2,634 2,938 2,739 2,983 3,493 International 574 636 673 593 644 679 593 139 599 583 602 690

2,467 2,979 3,266 2,876 3,218 3,517 2,975 2,773 3,537 3,322 3,585 4,183

Exhibit A: Sales data table

Source: Stephen Few “Visual Communication” IBM Whitepaper, April 2009 (p. 2)

51experience. new thinking

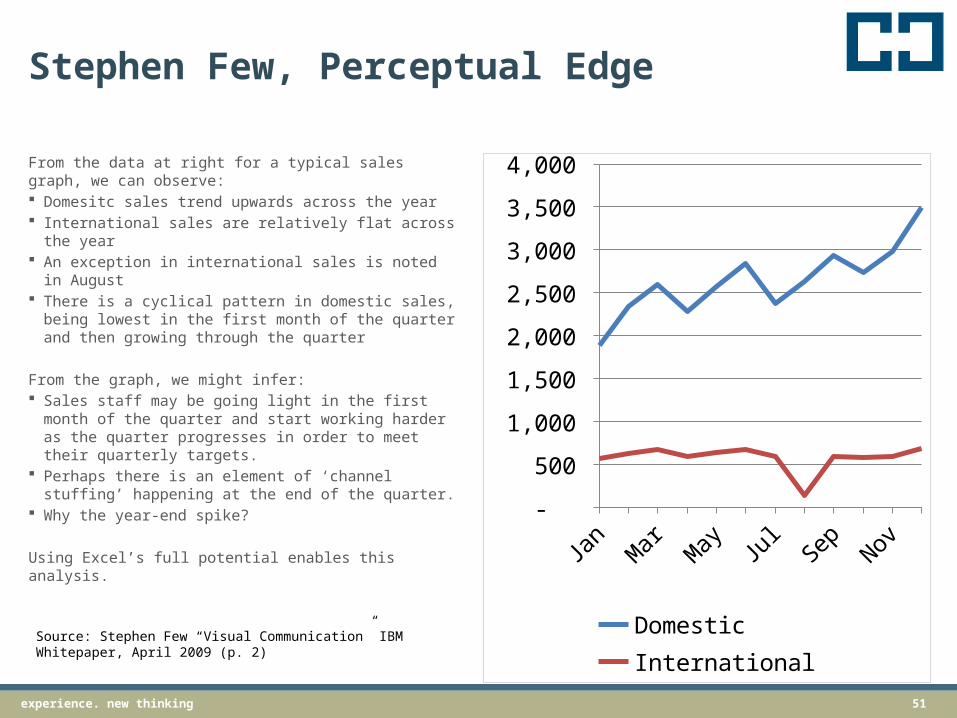

Stephen Few, Perceptual Edge

From the data at right for a typical sales graph, we can observe: Domesitc sales trend upwards across the year International sales are relatively flat across the

year An exception in international sales is noted in

August There is a cyclical pattern in domestic sales,

being lowest in the first month of the quarter and then growing through the quarter

From the graph, we might infer: Sales staff may be going light in the first month

of the quarter and start working harder as the quarter progresses in order to meet their quarterly targets.

Perhaps there is an element of ‘channel stuffing’ happening at the end of the quarter.

Why the year-end spike?

Using Excel’s full potential enables this analysis.Ja

nMar

May Ju

lSe

pNov

-

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Domestic InternationalSource: Stephen Few “Visual Communication” IBM Whitepaper, April 2009 (p. 2)

52experience. new thinkingexperience. new thinking 52

All is not lost, here is a 7 step process to review your spreadsheets.

7 steps to assure your spreadsheets

53experience. new thinking

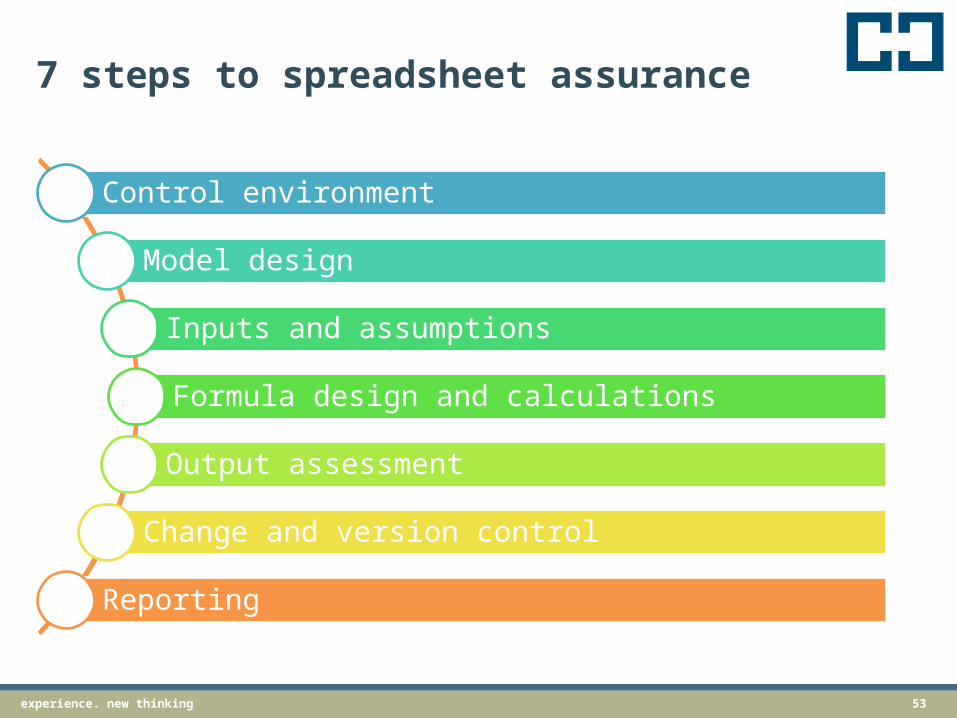

7 steps to spreadsheet assurance

Control environment

Model design

Inputs and assumptions

Formula design and calculations

Output assessment

Change and version control

Reporting

54experience. new thinking

Control environment

Review what spreadsheets exist and how they are controlled and developed

Review access and security arrangements for spreadsheets

Consider risk assessment for in-use spreadsheets

55experience. new thinking

Model design

Consider overall design and implementation of spreadsheets

Consider domain related information needed to understand model designs (e.g., are experts required such as geologists)

Consider periodicity and format consistency

56experience. new thinking

Inputs and assumptions

Review inputs and assumptions, consider approval requirements for assumptions included in spreadsheets

Consider inputs for data-entry errors

See: ASIC v MacDonald (No 11) [2009] NSWSC 287(James Hardy case)

Do key assumptions need board level approval?

57experience. new thinking

Formula design and calculation

Check formula for calculation consistency and accuracy

Examine model for potential errors including: hard coding, reference failures

How long can this take?Hanrick Curran were recently asked to review a transaction model with 1,173 unique formula and 50,028 total formula.At 1 minute per unique formula, that equates to 19.5 hours of review time or 2.6 days of just looking at formula. And this doesn’t even allow time to consider domain errors.

58experience. new thinking

Output assessment

Review model outputs for consistency Consider information accuracy Does the model promote effective decision

making

59experience. new thinking

Change and version control

Consider change controls implemented over the reviewed spreadsheet, including password protection

Consider version controls implemented over the model and to whom ownership of the spreadsheet is delegated

Tip: use a descriptive file name that includes information regarding status and version or date of the spreadsheet.Tip: put dates in YYYYMMDD order to enable auto-sortingExample: “division budget review (v2.3)(DRAFT).xlsx”

Example: “20140612”

60experience. new thinking

Reporting

Prepare and communicate with management regarding the outcomes of the spreadsheet review

61experience. new thinkingexperience. new thinking 61

Some suggestions on how to implement some key lessons from todays topics…

A brief summary and some practical solutions

62experience. new thinking

In summary

Errors will happen, if you plan well, their impact can be minimised.

Most errors are not material, but do you want to be the example that proves the rule?

Most errors are not actually on/in the spreadsheet.

63experience. new thinking

Practical solutions (I)

Set organisational spreadsheet standards; have a “this is the way we do it here.”

Implement a best practice standard (i.e., FAST).

Implement training in how to use Excel and how to design spreadsheets.

64experience. new thinking

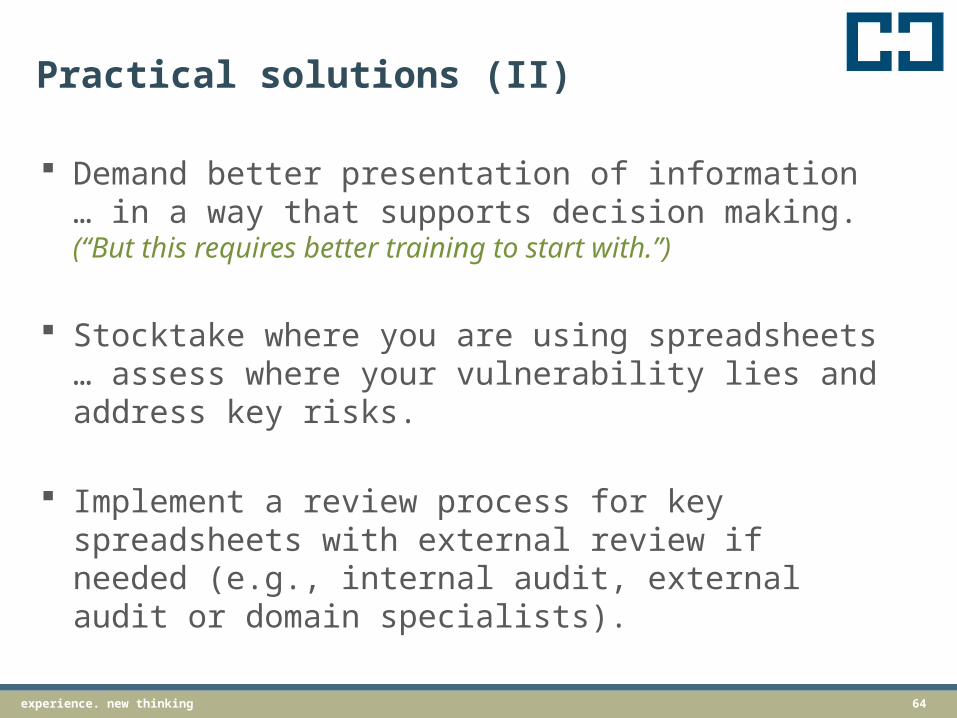

Practical solutions (II)

Demand better presentation of information … in a way that supports decision making.(“But this requires better training to start with.”)

Stocktake where you are using spreadsheets … assess where your vulnerability lies and address key risks.

Implement a review process for key spreadsheets with external review if needed (e.g., internal audit, external audit or domain specialists).

65experience. new thinking

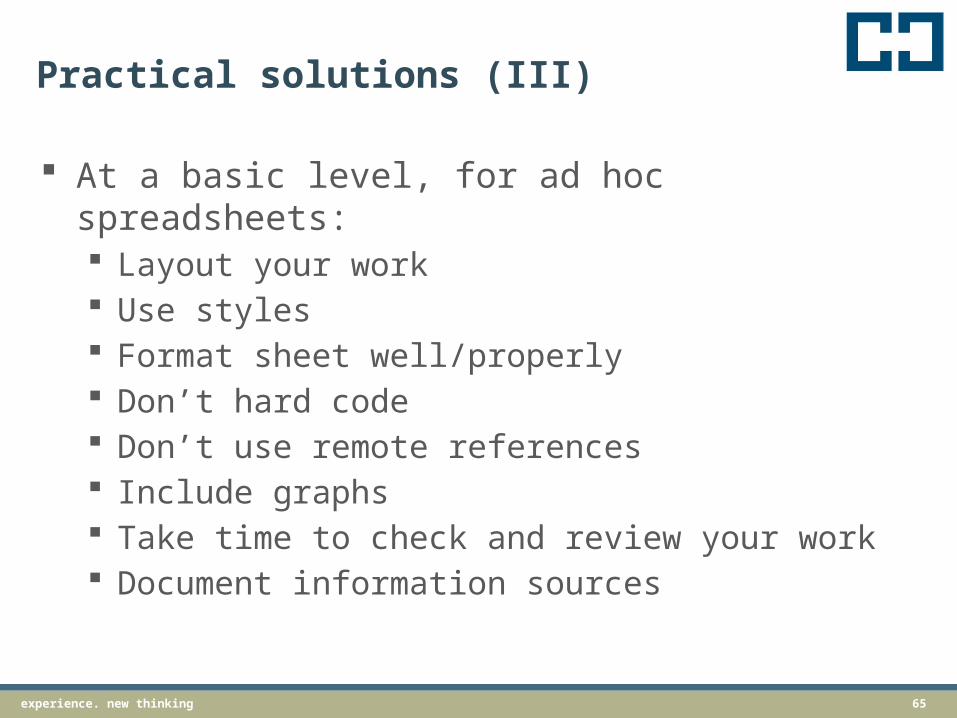

Practical solutions (III)

At a basic level, for ad hoc spreadsheets: Layout your work Use styles Format sheet well/properly Don’t hard code Don’t use remote references Include graphs Take time to check and review your work Document information sources

66experience. new thinking

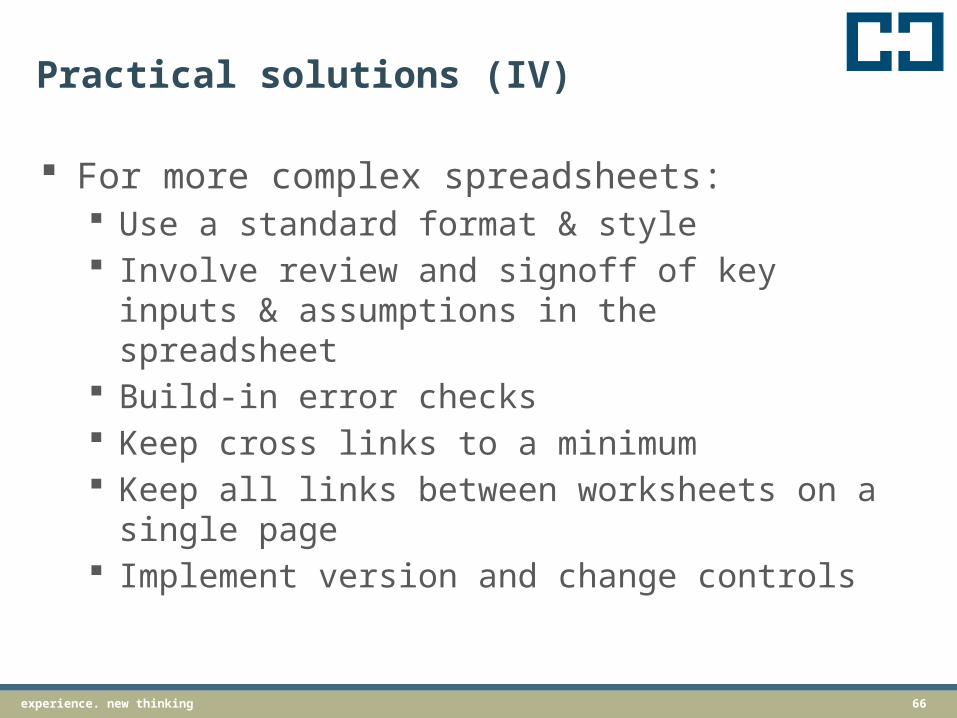

Practical solutions (IV)

For more complex spreadsheets: Use a standard format & style Involve review and signoff of key inputs &

assumptions in the spreadsheet Build-in error checks Keep cross links to a minimum Keep all links between worksheets on a single

page Implement version and change controls

67experience. new thinkingexperience. new thinking 67

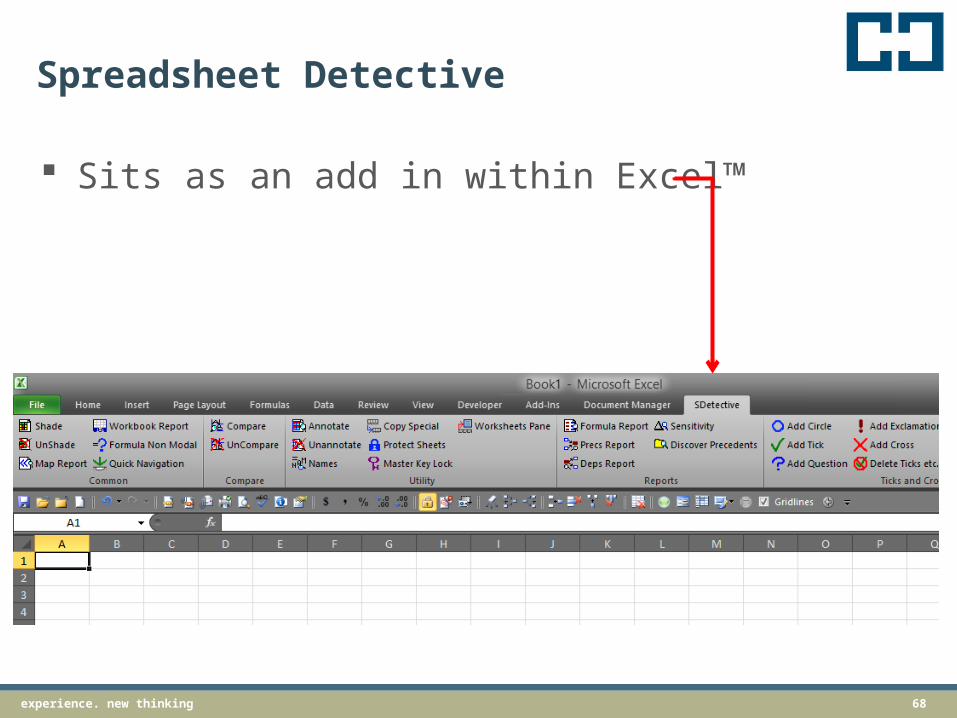

Self-checking your spreadsheets to avoid errors in decision making.Anthony Berglas

Spreadsheet Detective

68experience. new thinking

Spreadsheet Detective

Sits as an add in within Excel™

69experience. new thinking

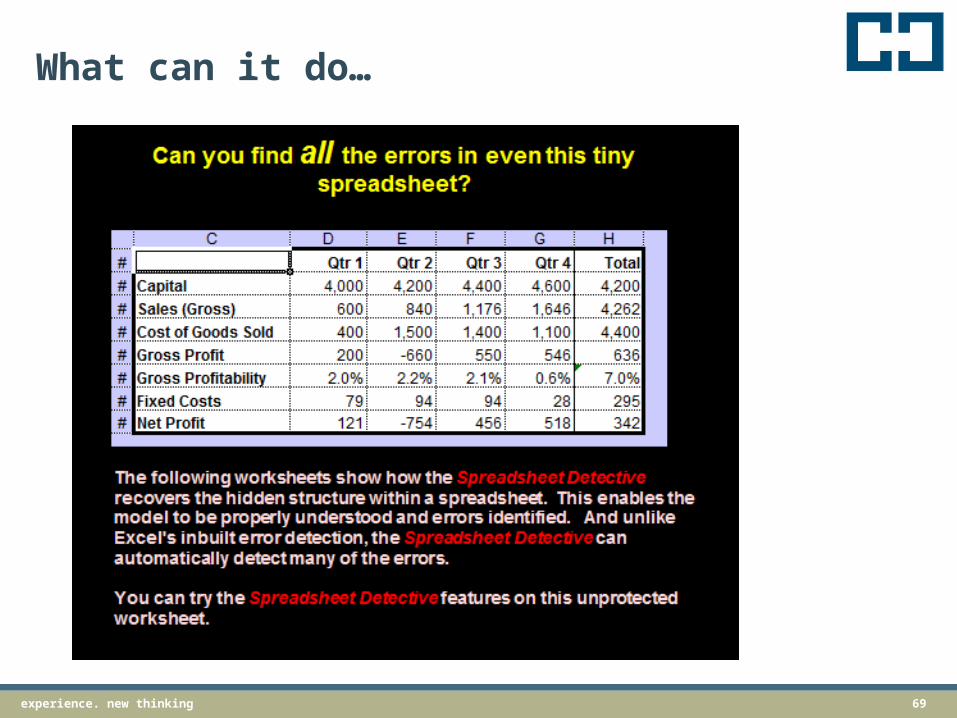

What can it do…

70experience. new thinking

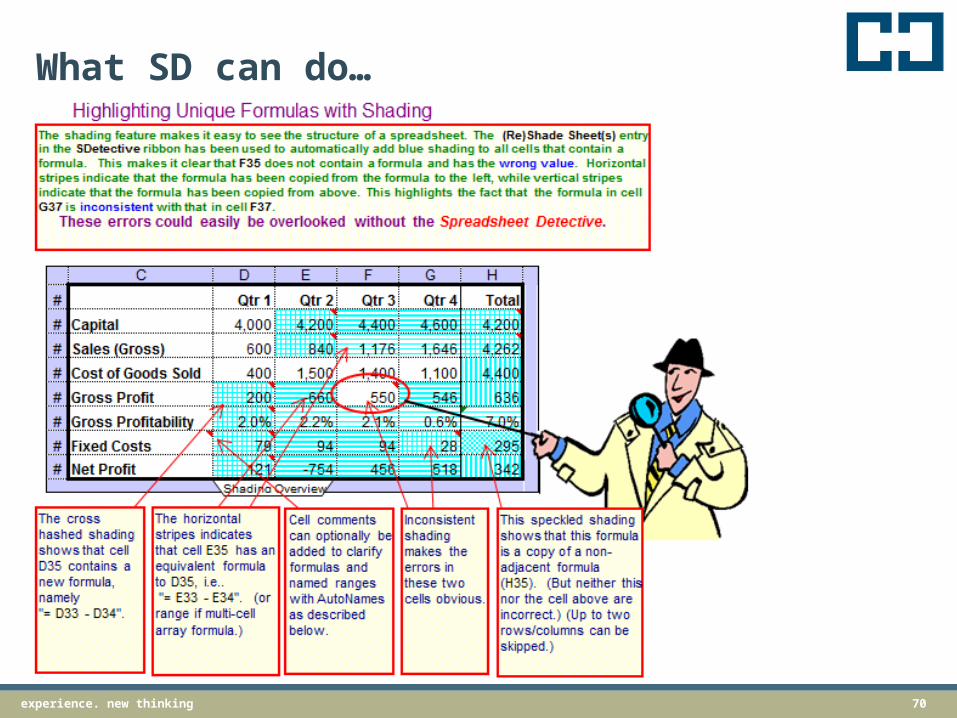

What SD can do…

71experience. new thinking

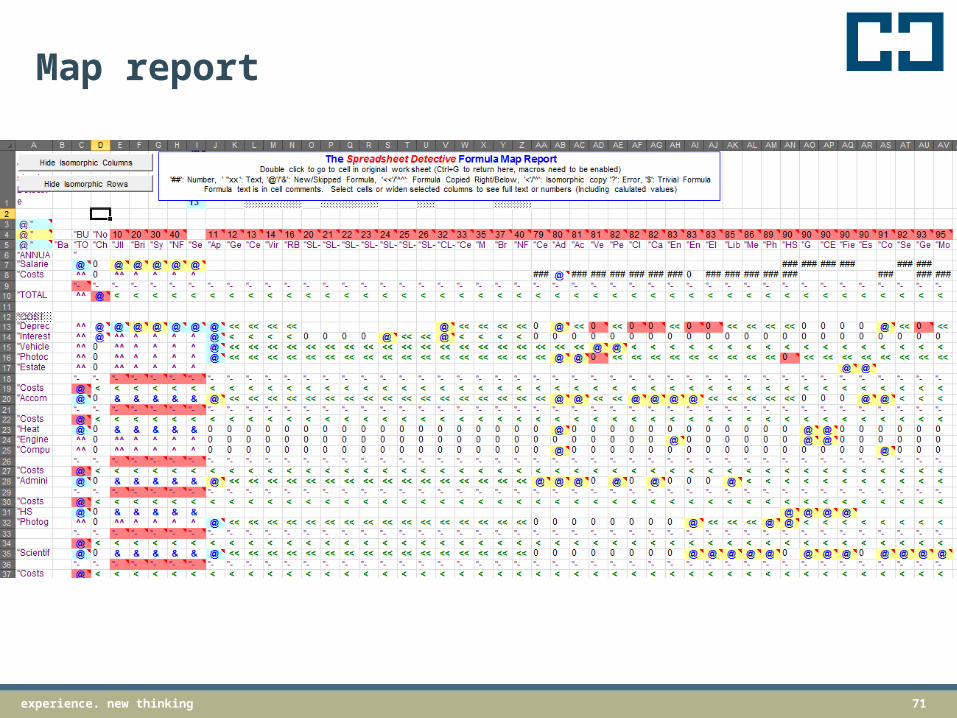

Map report

72experience. new thinking

Workbook report

73experience. new thinking

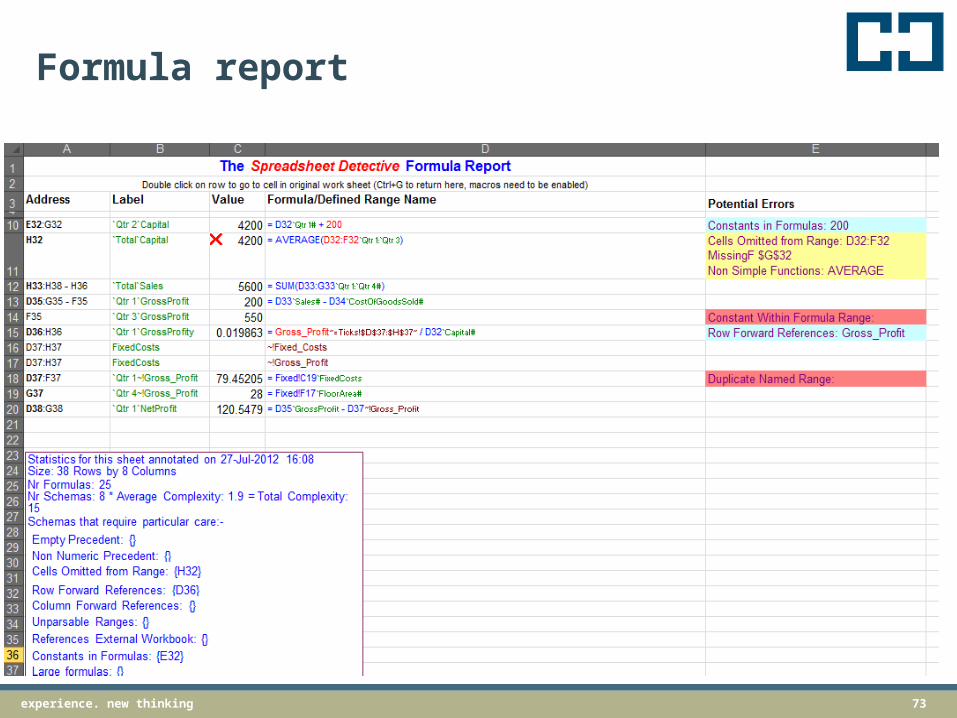

Formula report

www.hanrickcurran.com.au

Questions?

75experience. new thinking

More resources

www.f1f9.com“Well worth trying their 31 day free online course for a brush-up on your excel skills.”

www.spreadsheetdetective.com“Use the tools we use, to understand and self-audit your model.”

www.asap-utilities.com“Great tools for every excel user. If you ever work with data, you need these tools.”

www.perceptualedge.com“For enlightening analysis and communication.”

76experience. new thinking

Disclaimers

This document contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgement. It does not purport to be comprehensive or to render professional advice. The reader should not act on the basis of any matter contained in this publication without first obtaining specific professional advice.

We believe that the statements made by us in this document are accurate but no warranty of accuracy or reliability is given. Our conclusions are based on interpretations of accounting standards and other relevant professional pronouncements and legislation current as at the date of this document. Should the interpretations, accounting standards, other relevant professional pronouncements or legislation change, our conclusions may not be valid. We are under no obligation to update the matters considered in this document after its publication.

© Hanrick Curran, June 2014All rights reserved

Thank you

www.hanrickcurran.com.au