Time Value of Money - Lakehead Universityflash.lakeheadu.ca/~pgreg/assignments/timevaluen.pdf ·...

43

Time Value of Money Lakehead University Fall 2004 Outline of the Lecture • Future Value and Compounding • Present Value and Discounting • More on Present and Future Values 2

Transcript of Time Value of Money - Lakehead Universityflash.lakeheadu.ca/~pgreg/assignments/timevaluen.pdf ·...

Time Value of Money

Lakehead University

Fall 2004

Outline of the Lecture

• Future Value and Compounding

• Present Value and Discounting

• More on Present and Future Values

2

Future Value and Compounding

Future valuerefers to the amount of money an investment would

grow to over some length of time at a given rate of interest.

To determine this value, it is important to know when interest is

calculated. Is it once a year? Every six months? Each month?

When many payments are involved, it is also important to know

the timing of these payments.

3

Future Value and Compounding

Investing for a Single Period

Suppose $100 is invested in an account that pays 10% per year.

This investment will then be worth

100 + 0.10×100 = (1+0.10)×100

= 1.1×100

= $110

after one year.

4

Future Value and Compounding

Investing for More than One Period

Suppose $100 is invested in an account that pays 10% per year.

After one year, this investment will be worth $110. If the interest

payment is reinvested, this investment will be worth, after two

years,

110 + 0.10×110 = 1.1×110

= 1.1×1.1×100

= (1.1)2×100 = $121.

5

5.1 Future Value and Compounding

Decomposing(1.1)2×100gives us

1.1×1.1×100 =(1+ .2+ .12)×100

= 100︸︷︷︸Capital

+ 20︸︷︷︸Interest

on capital⇓

Simpleinterest

+ 1︸︷︷︸Interest

on interest⇓

Compoundinterest

6

Future Value and Compounding

More generally, $m invested at a period interest rater will grow

to

(1+ r)t ×m = m︸︷︷︸Capital

+ t× r×m︸ ︷︷ ︸Simpleinterest

+ Compound interest

aftert periods.

7

Future Value and Compounding

Compound interestcan be significant over the long run.

Take $100 invested forT years at 10% compounded annually:

Ending Simple CompoundT Amount Capital Interest Interest

1 110.00 = 100 + 10 + 0.00

5 161.05 = 100 + 50 + 11.05

10 259.37 = 100 + 100 + 59.37

15 417.72 = 100 + 150 + 167.72

20 672.75 = 100 + 200 + 372.75

8

Future Value and Compounding

Examples of Future Value Calculations

1. $2,250 invested for 30 years at 18% compounded annually

gives

2,250× (1.18)30 = $322,583.94.

2. $9,310 invested for 15 years at 6% compounded annually

gives

9,310× (1.06)15 = $22,311.96.

9

Future Value and Compounding

One More Example

3. You are scheduled to receive $22,000 in two years. When

you receive it, you will invest it for six more years at 6

percent per year. How much will you have in eight years?

Answer:

22,000× (1.06)8−2 = 22,000× (1.06)6 = $31,207.42.

10

5.2 Present Value and Discounting

Present valuerefers to the amount of money that has to be

invested today to obtain a specific amount of money after a

specific length of time at a given rate of interest.

If, for example, we want to know how much to invest to obtain

$1 after one year at 10% interest, we need to solve

Present value×1.1 = $1 ⇒ Present value=1

1.1= $0.909.

11

Present Value and Discounting

More generally, the amount of money that needs to be invested

today to obtain $1 int years at the annual rate of interestr is

PV =1

(1+ r)t .

This amount is the present value, as of today, of $1 to be received

in t years discounted at the annual rater.

12

Present Value and Discounting

Examples of Present Value Calculations

1. The present value of $15,000 to be received in 5 years,

discounted at the annual rate 12%, is

PV =15,000(1.12)5 = $8,511.40.

2. The present value of $25,000 to be received in 10 years,

discounted at the annual rate 8%, is

PV =25,000(1.08)10 = $11,579.84.

13

5.3 More on Present and Future Values

With a period rate of interestr and a number of periodst, we can

define

Future value factor = (1+ r)t

Present value factor=1

(1+ r)t

14

More on Present and Future Values

Let PV0 denote the present value, as of today (date 0), of an

investment that will grow to the future value FVt in t periods, the

period interest rate beingr. Then

PV0× (1+ r)t = FVt and, equivalently PV0 =FVt

(1+ r)t .

This result is thebasic present value equation.

15

More on Present and Future Values

Determining the Discount Rate

What mustr be for PV0 to grow to FVt in t periods?

PV0× (1+ r)t = FVt

(1+ r)t =FVt

PV0

1+ r =(

FVt

PV0

)1/t

r =(

FVt

PV0

)1/t

−1.

16

More on Present and Future Values

Example of Discount Rate Determination

You are offered an investment that requires you to put up

$12,000 today in exchange for $40,000 12 years from now. What

is the annual rate of return on the investment?

Answer: In this example, PV0 = 12,000, FVt = 40,000and

t = 12. Therefore,

r =(

40,00012,000

)1/12

− 1 = 10.55%.

17

More on Present and Future Values

Finding the Number of Periods

What mustt be for PV0 to grow to FVt at a rater?

Note: We will be using the following rules:

ln(ab) = ln(a) + ln(b)

ln(ab) = bln(a)

ln(a

b

)= ln(a) − ln(b).

18

Finding the Number of Periods

PV0× (1+ r)t = FVt

ln(PV0× (1+ r)t) = ln(FVt)

ln(PV0) + ln((1+ r)t) = ln(FVt)

ln(PV0) + t ln(1+ r) = ln(FVt)

t =ln(FVt)− ln(PV0)

ln(1+ r)

t =ln(FVt/PV0)

ln(1+ r)

19

How Long to Double Your Money?

Knowing r, how many periods is needed for PV0 to double?

t =ln(FVt/PV0)

ln(1+ r)

=ln(2PV0/PV0)

ln(1+ r)

=ln(2)

ln(1+ r)

20

The Rule of 72

Note that

• whenr is small,ln(1+ r)≈ r (slightly belowr);

• ln(2) = 0.6931(slightly below 0.72).

A good approximation of the time it takes to double an

investment is0.72

r=

72100r

.

If r = 8%, PV0 will double in approximately72/8 = 9 years.

21

The Rule of 72

r ln(1+ r) ln(2)ln(1+r)

72100r

2% 0.01980 35.00 36

4% 0.03922 17.67 18

6% 0.05827 11.90 12

8% 0.07696 9.01 9

10% 0.09531 7.27 7.2

12% 0.11333 6.12 6

14% 0.13103 5.29 5.14

22

The Rule of 72

The rule of 72 holds exactly at around 7.85%.

The rule of 72 will

• overestimate the time it takes to double an investment when

r < 7.85%;

• underestimate the time it takes to double an investment when

r > 7.85%;

23

The Rule of 72

Whenr is small, the error will be insignificant.

The error is significant when using large numbers.

Taker = 72%, for instance. According to the rule of 72, an

investment doubles in approximately one year at this rate.

This makes no sense: it takesr = 100%to double an investment

in one year.

24

Finding the Number of Periods: An Example

You are trying to save to buy a new $120,000 Ferrari. You have

$40,000 today that can be invested at 8% compounded annually.

How long will it take before you have enough money to buy the

car?

Answer:

t =ln(120,000/40,000)

ln(1.08)=

ln(3)ln(1.08)

= 14.27years.

25

Future and Present Values of Multiple Cash Flows

Future Value with Multiple Cash Flows

Suppose $100 is invested today and another $100 is invested in

one year at an annual rate of 8%. How much will this investment

be worth in two years?

-

$100 -×1.08 $108

$100

$208 -×1.08 $224.64

Time

0 1 2

26

Future Value with Multiple Cash Flows

The same example, put differently:

-

$100 -×1.08 $108 -×1.08 $116.64

$100 -×1.08 $108.00

$224.64

Time

0 1 2

That is,

FV = $100× (1.08)2 + $100×1.08 = $224.64.

27

Future Value with Multiple Cash Flows

Suppose now that the two payments are made at theendof each

period. This gives us

-

$100 -×1.08 $108

$100

$208

Time

0 1 2

and thus, in this case

FV = $100×1.08 + $100 = $208.

28

Future Value with Multiple Cash Flows

More generally, let

dt ≡ payment made in periodt;

r ≡ period interets rate;

T ≡ the total number of periods.

Then

FV = (1+ r)Td0 + (1+ r)T−1d1 + . . . + (1+ r)dT−1 + dT

=T

∑t=0

(1+ r)T−tdt .

29

An example withT = 4.

d0 -×(1+ r) ×(1+ r) ×(1+ r) ×(1+ r) (1+ r)4d0

d1 -×(1+ r) ×(1+ r) ×(1+ r) (1+ r)3d1

d2 -×(1+ r) ×(1+ r) (1+ r)2d2

d3 -×(1+ r) (1+ r)d3

d4

4

∑t=1

(1+ r)4−tdt

0 1 2 3 4

30

Present Value with Multiple Cash Flows

What is the present value of $100 to be received one year from

now and another $100 to be received in two years, the annual rate

of interest being 8%?

-

$100¾×1/1.08$92.59

$100¾×1/1.08 ×1/1.08$85.73

$178.32

Time

0 1 2

That is, PV = $1001.08 + $100

(1.08)2 = $178.32.

31

Future Value with Multiple Cash Flows

More generally, let

dt ≡ payment made in periodt;

r ≡ period interets rate;

T ≡ the total number of periods.

Then

PV = d0 +d1

1+ r+

d2

(1+ r)2 + . . . +dT

(1+ r)T

=T

∑t=0

dt

(1+ r)t .

32

A Note on Cash Flow Timing

Unless specified otherwise, cash flows are assumed to take place

at the end of each period.

A cash flow in year 2, for instance, means a cash flow to be

received two years from now, and thus at the end of the second

year.

33

A Note on Cash Flow Timing

If you are told that a three-year investment has a first-year cash

flow fo $100, a second-year cash flow of $200 and a third-year

cash flow of $300, then the timing of cash flows is as follows:

-

$100 $200 $300

0 1 2 3

34

6.2 Valuing Level Cash Flows

A ordinaryannuityis a series of constant, or level, cash flows that

occur at theendof each period for some fixed number of periods.

An annuity dueis a series of constant, or level, cash flows that

occur at thebeginningof each period for some fixed number of

periods.

A perpetuityis an annuity in which the cash flows continue

forever.

35

A Note on How to Value Level Cash Flows

Let

S =T

∑t=1

qt = q + q2 + q3 + . . . + qT−1 + qT .

Then

qS = qT

∑t=1

qt = q2 + q3 + q4 + . . . + qT + qT+1,

and thus, ifq≥ 0 andq 6= 1,

S− qS = q − qT+1 ⇒ S =q−qT+1

1−q=

q1−q

(1−qT)

.

36

A Note on How to Value Level Cash Flows

If q = 1, thenS= ∑Tt=1qt = T.

What happens whenT is arbitrarily large?

limT→∞

q1−q

(1−qT)

=

q1−q if 0≤ q < 1,

∞ if q > 1.

37

A Note on How to Value Level Cash Flows

Suppose that we have

S =1

1+ r+

(1

1+ r

)2

+(

11+ r

)3

.

Let q = 11+r , wherer > 0 is a discount rate. Then

S = q + q2 + q3 =q

1−q

(1−q3) .

38

A Note on How to Value Level Cash Flows

Replaceq with 11+r in the last equation. This gives

S =1/(1+ r)

1−1/(1+ r)

(1−

(1

1+ r

)3)

=1

1+ r−1

(1−

(1

1+ r

)3)

=1r

(1−

(1

1+ r

)3)

39

A Note on How to Value Level Cash Flows

So if we have

S =T

∑t=1

(1

1+ r

)t

=1

1+ r+

(1

1+ r

)2

+ . . . +(

11+ r

)T

,

then

S =1r

(1−

(1

1+ r

)T)

.

40

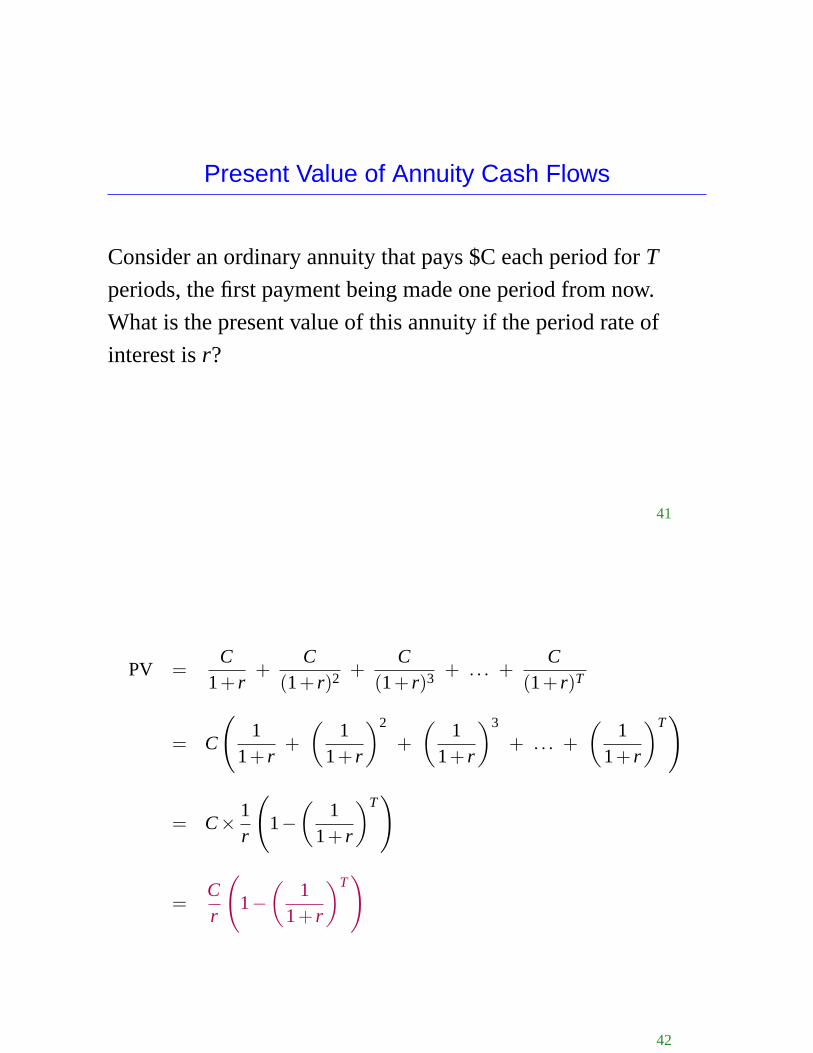

Present Value of Annuity Cash Flows

Consider an ordinary annuity that pays $C each period forT

periods, the first payment being made one period from now.

What is the present value of this annuity if the period rate of

interest isr?

41

PV =C

1+ r+

C(1+ r)2 +

C(1+ r)3 + . . . +

C(1+ r)T

= C

(1

1+ r+

(1

1+ r

)2

+(

11+ r

)3

+ . . . +(

11+ r

)T)

= C× 1r

(1−

(1

1+ r

)T)

=Cr

(1−

(1

1+ r

)T)

42

Present Value of Annuity Cash Flows

The term1− ( 1

1+r

)T

ris often referred to as thepresent value interest factor for

annuitiesand abbreviated PVIFA(r,T).

Note that

PVIFA(r,T) =1− ( 1

1+r

)T

r=

1−Present Value factorr

43

Present Value of Annuity Cash Flows

Consider now an annuitydue involving T payments of $C, theperiod interest rate beingr. Then

PV = C +C

1+ r+

C

(1+ r)2 + . . . +C

(1+ r)T−1

= (1+ r)C

(1

1+ r+

(1

1+ r

)2

+(

11+ r

)3

+ . . . +(

11+ r

)T)

= (1+ r)C× 1r

(1−

(1

1+ r

)T)

= (1+ r)×C×PVIFA(r,T).

44

Present Value of Annuity Cash Flows

The present value of an annuity due is equal to1+ r times its

ordinary counterpart.

Using the above equations, we can answer questions similar to

those in chapter 5, such as finding the fixed payment that will

repay a loan, or finding the number of periods necessary to repay

a loan, etc..

45

Present Value of Annuity Cash Flows

Example 1

An investment offers $2,250 per year for 15 years, with the first

payment occurring one year from now. If the required return is

10 percent, what is the value of the investment?

Answer:

PV =2,2500.1

(1−

(1

1.1

)15)

= $17,113.68.

46

Present Value of Annuity Cash Flows

Example 2

Betty’s Bank offers a $25,000, seven-year loan at 11 percent

annual interest payable in equal annual amounts. What will the

annual payment be?

Answer:

C =PV

1r

(1− ( 1

1+r

)T) =

25,0001

0.11

(1− ( 1

1.11

)7) = $5,305.38.

47

Present Value of Annuity Cash Flows

Example 3

How long does it take to repay a $25,000 loan with fixed annual

payments of $4,000 at an 11% annual interest rate?

We will be using the “ln” trick to solve this problem.

48

Example 3

Answer:

PV =Cr

(1−

(1

1+ r

)T)

rPVC

= 1−(

11+ r

)T

(1

1+ r

)T

= 1− rPVC

T ln

(1

1+ r

)= ln

(1− rPV

C

)

T =ln

(1− rPV

C

)

ln( 1

1+r

)

49

Example 3

Answer:

T =ln

(1− rPV

C

)

ln( 1

1+r

)

=ln

(1− 0.11×25,000

4,000

)

ln( 1

1.11

)

= 11.15years,

and thus it takes 12 years to repay such a loan, the last payment

being less than $4,000.

50

Present Value of Annuity Cash Flows

Example 4

What must the annual rate of interest be in order to fully repay a$25,000 loan in 10 years with fixed annual payments of $4,000?Answer:

PV =Cr

(1−

(1

1+ r

)T)

25,000 =4,000

r

(1−

(1

1+ r

)10)

.

Can’t solve this equation analytically.

51

Example 4

The solution can be found by trial-and-error or by using a

computer.

In Excel:

RATE(NPER,PMT,PV)= RATE(10,-4000,25000)= 9.61%.

52

Future Value of Annuity Cash Flows

Consider an ordinary annuity that pays $C each period forT

periods, the first payment being made one period from now.

What is the future value of this annuity if the period rate of

interest isr?

53

Future Value of Annuity Cash Flows

Answer:

FV = (1+ r)T−1C + (1+ r)T−2C + . . . + (1+ r)C + C

= C((1+ r)T−1 + (1+ r)T−2 + . . . + (1+ r) + 1

)

= C(

1 + (1+ r) + . . . + (1+ r)T−2 + (1+ r)T−1)

= C

(1− (1+ r)T

1− (1+ r)

)

= C

(1− (1+ r)T

−r

)

= C

((1+ r)T −1

r

)

54

Future Value of Annuity Cash Flows

The term(1+ r)T −1

ris often referred to as thefuture value interest factor for annuities

and abbreviated FVIFA(r,T).

Note that

FVIFA(r,T) =(1+ r)T −1

r= (1+ r)T 1− (

11+r

)T

r= (1+ r)TPVIFA(r,T).

55

Perpetuities

A perpetuity is an annuity with perpetual cash flows.

The future value of a perpetuity is always infinite.

The present value of a perpetuity paying$C forever at theendof

each period, the period interest rate beingr > 0, is

limT→∞

C

(1− ( 1

1+r

)T

r

)=

Cr,

sincelimT→∞( 1

1+r

)T = 0.

56

Perpetuities

The present value of a perpetuity paying$C forever at the

beginningof each period, the period interest rate beingr > 0, is

limT→∞

C(1+ r)

(1− ( 1

1+r

)T

r

)=

(1+ r)Cr

.

57

Relationship between Annuities and Perpetuities

Consider the following perpetuities:

Perpetuity P1: Pays$C forever, the first payment being made

one period from now.

Perpetuity P2: Pays$C forever, the first payment being made

at timeT +1 (i.e. at the end of periodT, which is the

beginning of periodT +1).

. . . -0 1 2 3 4 5 T−1 T T+1 T+2 T+3

P1 :

P2 :

C C C C C C C C C C

C C C

58

Relationship between Annuities and Perpetuities

Note that

P1 − P2 = A(C,T),

whereA(C,T) denotes the (ordinary) annuity that pays$C for T

periods.

Hence, the present value ofP1−P2 must be equal to the present

value ofA(C,T).

59

Relationship between Annuities and Perpetuities

Let r denote the period interest rate. Then

PV(P1) =Cr

and PV(P2) =C/r

(1+ r)T ,

and thus

PV(P1−P2) =Cr− C/r

(1+ r)T

=Cr

(1−

(1

1+ r

)T)

= PV(A(C,T)).

60

Growing Annuities

Consider an annuity in which the payment grows at the rateg

from one period to the other. That is, the cash flows from this

annuity are as follows:

. . . -0 1 2 3 T−1 T

C (1+g)C (1+g)2C (1+g)T−2C (1+g)T−1C

61

The present value of this annuity is

PV =C

1+ r+

(1+g)C(1+ r)2 +

(1+g)2C(1+ r)3 + . . . +

(1+g)T−1C(1+ r)T

=C

1+g

(1+g1+ r

+(

1+g1+ r

)2

+(

1+g1+ r

)3

+ . . . +(

1+g1+ r

)T)

=C

1+g× (1+g)/(1+ r)

1− (1+g)/(1+ r)

(1−

(1+g1+ r

)T)

=C

1+g× 1

(1+ r)/(1+g)−1

(1−

(1+g1+ r

)T)

= C× 11+ r− (1+g)

(1−

(1+g1+ r

)T)

=C

r−g

(1−

(1+g1+ r

)T)

62

Growing Annuities

The present value of an annuity in which the payments grow at

the constant rateg, the first payment beingC, is

PV =C

r−g

(1−

(1+g1+ r

)T)

,

whereT is the number of payments andr is the period discount

rate.

What is the present value of a growing perpetuity?

63

Growing Annuities

If g < r, then1+g1+ r

< 1 and limT→∞

(1+g1+ r

)T

= 0.

If g > r, then1+g1+ r

> 1 and limT→∞

(1+g1+ r

)T

= ∞.

Therefore,

limT→∞

Cr−g

(1−

(1+g1+ r

)T)

=

Cr−g if g < r,

∞ if g≥ r.

64

Growing Annuities

Example

Problem 77. Consider a firm that is expected to generate a net

cash flow of $10,000 at the end of the first year. The cash flows

will increase by 3 percent a year for seven years and then the firm

will be sold for $120,000. The relevant discount rate for the firm

is 11 percent. What is the present value of the firm?

65

Answer: The total cash flows generated by this firm are the 8cash flows from its operations and the terminal value of$120,000, which will materialize eight years from now. Thepresent value of the firm is then (numbers in 000’s)

PV =10

1.11+

1.03×10(1.11)2 +

(1.03)2×10(1.11)3 + . . . +

(1.03)7×10(1.11)8 +

120(1.11)8

=10

0.11−0.03

(1−

(1.031.11

)8)

+120

(1.11)8

= $108,360.

66

The Effect of Compounding

Interest rates can be quoted in many different ways.

How rates are quoted may come from tradition or regulation.

Very often, rates are quoted in a misleading manner.

What’s under a quoted rate?

67

Effective Annual Rates and Compounding

Suppose a rate is quoted at 10% compounded semiannually.

This means that 5% is charged every six months.

10%, thequoted rate, is the interest charged on theprincipal

during the year, it does not include the interest on interest

(compound interest).

The rate that takes into account compound interest is called the

effective annual rate (EAR).

What is the EAR in the above example?

68

Effective Annual Rates and Compounding

With a 10% interest rate compounded semiannually, the EAR is

EAR = (1.05)2 − 1 = 1.1025− 1 = 10.25%.

Note that

0.25% = 5%×5%

is the interest on interest charged during the year.

69

Effective Annual Rates and Compounding

More generally, the EAR of a quoted annual rate compoundedm

times during the year is

EAR =(

1+Quoted Rate

m

)m

− 1.

Compare the following rates:

Bank A: 15% compounded daily

Bank B: 15.5% compounded quarterly

Bank C: 16% compounded annually

70

Effective Annual Rates and Compounding

Bank A:

EARA =(

1+0.15365

)365

− 1 = 16.18%.

Bank B:

EARB =(

1+0.155

4

)4

− 1 = 16.42%.

Bank C:

EARC =(

1+0.16

1

)1

− 1 = 16.00%.

71

Quoting a Rate

What is the quoted rate, compounded monthly, that provides an

effective return of 15%?

72

Quoting a Rate

Answer:

0.15 =(

1+Quoted rate

12

)12

− 1

1.15 =(

1+Quoted rate

12

)12

(1.15)1/12 = 1+Quoted rate

12

(1.15)1/12 − 1 =Quoted rate

12

12×((1.15)1/12−1

)= Quoted rate = 14.06%.

73

Mortgages

Regulations for Canadian institutions require that mortgage rates

be quoted with semiannual compounding. Payments, however,

are made each month.

How to calculate monthly payments from a quoted mortgage

rate?

(i) When quoting a rate, a financial institution is thinking EAR,

so the first step is to find the EAR implied by the quoted rate.

(ii) Calculate the monthly rate prodiving the EAR in (i).

(iii) Using the annuity formula, find the monthly payment.

74

Mortgages

Example 1

Find the monthly payment on a $300,000 mortgage quoted at 14percent and amortized over 25 years.

EAR =(

1+Quoted rate

m

)m

−1 =(

1+0.14

2

)2

−1 = 14.49%.

Find the monthly rate that gives an EAR of 14.49%:

(1+Monthly Rate)12−1 = 14.49%

⇒ Monthly Rate= (1.1449)1/12−1 = 1.13%.

75

Mortgages

Example 1 (continued)

Find the monthly payment (T = 25×12= 300):

PV =Cr

(1−

(1

1+ r

)T)

300,000 =C

0.0113

(1−

(1

1.0113

)300)

C =0.0113×300,000

1− (1

1.0113

)300

C = $3,510.61.

76

Mortgages

Example 2

An entrepreneur is considering the purchase of an office in a new

high-rise complex. The office is worth $1,000,000 and a bank is

offering a mortgage for the whole amount at 8 percent APR. If

the entrepreneur’s budget allows payments of $7,000 a month,

how long will it take to pay off the purchase?

77

EARs and APRs

Cost of borrowing disclosure regulations in Canada require that

lenders disclose anannual percentage rate (APR)in a prominent

and unambiguous manner.

By law, the APR is the interest rate per period multiplied by the

number of periods in a year. This is indeed the quoted rate

mentioned earlier.

For example, the APR on a loan at 1.5% monthly interest rate is

12×1.5% = 18%.

78

Continuous Compounding

What is the EAR when the quoted rate is compounded every

nanosecond?

Take, for example, a 12% APR:

Compounded EAR

Annually 12.00%

Quarterly 12.55%

Monthly 12.68%

Weekly 12.73%

Daily 12.75%

Continuously ?

79

Continuous Compounding

The more often a quoted rate is compounded, the greater the

EAR.

Continuous compounding thus yields the maximum EAR from a

given APR.

Given a quoted rateq,

limm→∞

(1+

qm

)m− 1 = eq − 1.

Note thateq−1 is thehighestEAR that can be obtained with an

APR ofq.

80

Loan Types and Loan Amortization

We will see three types of loan in this section:

Pure Discount Loans: Usually short-term loans, such as T-bills.

Interest-Only Loans: Usually long-term loans, such as

government and corporate bonds.

Amortized Loans: Majority of individual loans.

81

Pure-Discount Loans

In a pure discount loan, the borrower receives money today and

makes one lump-sum payment at some time in the future.

Consider, for example, a T-bill that promises to pay $1,000 in one

year. When the interest rate is 3.48%, the value of this T-bill is

PV =1,0001.0348

= $966.37.

If the repayment (L) takes place aftert periods, the present value

of the loan is

PV =L

(1+ r)t .

82

Interest-Only Loans

With this type of loan, the borrower pays interest each period and

repays the principal at some point in the future.

Take, for example a 5-year loan of $1,000 at an 8% annual

interest rate.

Each year the borrower pays $80 in interest and the principal

($1,000) is repaid after 5 years. Cash flows to the lender are then

-0 1 2 3 4 5

Interest

Principal

$80 $80 $80 $80 $80

$1,000

83

Interest-Only Loans

The present value of the above loan, at a discount rater, is

PV =80r

(1−

(1

1+ r

)5)

+1,000

(1+ r)5 .

Note that

PV

> $1,000 if r < 8%,

= $1,000 if r = 8%,

< $1,000 if r > 8%.

84

Amortized Loans

An amortized loan is such that interest and principal are repaid

each period.

This type of loan can be such that a constant amount of the

principal is repaid each period, or can be such that a constant

payment is made each period.

How long would it take to repay a $5,000 loan with an APR of

10% compounded monthly if $500 in principal has to be repaid

each month?

85