Modifying WildFire Behavior – The Effectiveness of Fuel Treatments

NATURAL RESOURCE MODELINGVolume 19, Number 1, Spring 2006

TIMBER MARKETS AND FUEL TREATMENTSIN THE WESTERN U.S.

KAREN L. ABTForestry Sciences Laboratory

USDA Forest ServiceP.O. Box 12254

Research Triangle Park, NC 27709E-mail: [email protected]

JEFFREY P. PRESTEMONForestry Sciences Laboratory

USDA Forest ServiceP.O. Box 12254

Research Triangle Park, NC 27709

ABSTRACT. We developed a model of interrelated timbermarkets in the U.S. West to assess the impacts of large-scalefuel reduction programs on these markets, and concomitanteffects of the market on the fuel reduction programs. Thelinear programming spatial equilibrium model allows inter-state and international trade with western Canada and therest of the world, while accounting for price effects of intro-ducing softwood logs to the market. The model maximizesarea treated, given fire regime-condition class priorities, max-imum increases in softwood processing capacity, maximumrates of annual treatments, prohibitions on exports of U.S. andCanadian softwood logs from public lands and a fixed annualtreatment budget. Results show that the loss to U.S. privatetimber producers is less than the gains for timber consumers(mills). Effects on Canadian private producers and Canadiantimber consumers depend on wildland-urban interface con-straints and condition class treatment priorities. States re-ceiving the greatest amount of treatments include California,Oregon, Washington and New Mexico, due to their concen-tration of stands with relatively low treatment costs.

KEY WORDS: Wildfire, mechanical treatments, spatialequilibrium, welfare.

Introduction. Recent increases in wildfire suppression expendituresand financial losses resulting from large fire events have increased theinterest in developing policies to address forest health conditions inwestern U.S. forests. One particular concern is that previous firesuppression and prevention, combined with climate change, has led

Received by the editors on June 1, 2004, and in revised form on Nov. 23, 2004.

Copyright c©2006 Rocky Mountain Mathematics Consortium

15

16 K.L. ABT AND J.P. PRESTEMON

to hazardous fuel accumulations in many forested areas (Parsons andDeBenedetti [1979], Bonnicksen and Stone [1982], Parker [1984], Chang[1996], Harrod et al. [1999], Arno et al. [1997], Skinner and Chang[1996]). A second concern is encroachment of human populationsinto these forests, often referred to as the wildland-urban interface(WUI), which creates the potential for increased loss of private propertyduring wildfire events. One proposed solution addressing both of theseconcerns is to reduce fuel accumulations in the WUI and surroundinglands using mechanical treatments.

The increase in fuel treatments has been promoted in the NationalFire Plan1 and the Healthy Forests Initiative (HFI)2 which Congressmodified and passed, as well as the Healthy Forests Restoration Act3.The USDA Forest Service adopted the Comprehensive Strategy andImplementation Plan4, partly in response to criticisms from the GAOregarding its lack of cohesion in developing a fuels reduction strategy(U.S. General Accounting Office [1999]). Current funding for fueltreatment programs on both public and private lands exceeds $1 billionper year, although the funding for mechanical treatments with biomassproduct removals is considerably smaller.

One effect of implementing these treatment programs is the de factoremoval of limits on federal harvests, in particular federal harvests thatwould result in below-cost timber sales. It is possible that areas mostin need of treatment are also the areas with the smallest proportionof high quality wood and the most expensive treatment costs. Thus,these treatments would require large subsidies in many areas becausethe treatments would not provide adequate products for sale whilesimultaneously reducing fuels.

Large-scale biomass removals programs done to lower wildfire risksand associated potential damages on National Forests, other govern-ment forests and private lands may have economic impacts across arange of temporal, spatial and sectoral scales, including short- andlong-run impacts on economies, impacts on local, regional and nationalforest product markets, and effects on other economic sectors in andaround the removal zone (Mercer et al. [2000]).

The treatments will affect the markets for privately supplied timberby increasing the supply of some products, thus lowering the avail-able prices and hence the quantity offered by private producers. In

TIMBER MARKETS AND FUEL TREATMENTS 17

a treatment program that maximizes treatment acreage subject to asubsidy computed as the costs of treatments minus revenues accruedfrom materials removed and sold, the market price effect could reducethe ultimate acreage treated. This paper presents a model wherein wemaximize acres treated given a subsidy, not allowing for offsetting treat-ment costs with treatment revenues. Instead, we assume that treatmentrevenues go to the Treasury and hence do not offset treatment costs.

The magnitude of the timber market effects will depend on thecurrent state of the market, including excess wood processing capacity.Some of these treatments would require a complete subsidy. That is,there would be no revenues from products removed. Others wouldpay at least partially for themselves through sales of timber products.Thus the amount of fuel treatment that could be accomplished woulddepend on the proportion of the treatments receiving subsidies, andthe subsidies would influence timber markets, and thus timber prices.

Two recent studies have addressed large scale fuel treatment pro-grams without directly addressing issues of market welfare and prices.A Strategic Assessment of Forest Biomass and Fuel Reduction Treat-ments in western States (Western Biomass Assessment) (Rummer etal. [2003]) quantified the biomass available for treatment in the west-ern U.S. by state. This study examined the potential biomass availableby using current prices, costs derived from a treatment model and in-ventory data from USDA Forest Service Forest Inventory and Analysis.A second study (Fried et al. [2003]) evaluated the potential location ofnew biomass processing facilities in Southern Oregon. Fried et al. [2003]evaluated conditions and treatable volumes in the region, as measuredon Forest Inventory and Analysis plots. Although their study did findlarge treatable volumes on the ground, some of which could be eco-nomically treated, investment potential hinged on the assumption thatprices were not endogenous to treatment quantities.

Our research extends the above analyses by directly addressing themarket impacts of alternative program scales. To account for marketprice effects, we use a spatial equilibrium market model of twelvewestern states and other trading partners, and assess the outcome of a$1 billion fuel treatment program. States included in the analysis areArizona, California, Colorado, Idaho, Montana, Nevada, New Mexico,Oregon, western South Dakota (the Black Hills), Utah, Washington andWyoming. The model objective is to maximize treated acres in federal

18 K.L. ABT AND J.P. PRESTEMON

forests, allowing for shifts in private timber harvest. After treatedacres (given price effects) are maximized, social welfare is maximizedas a secondary objective, allowing consuming mills to purchase woodand private producers to sell wood across state and national borders.The treatments by state, forest type and condition class, and thewelfare implications of alternative subsidy programs, are described anddiscussed. We also analyze how a national forest lands mechanical fuelreduction treatment program limited to the wildland-urban interfacewould affect timber markets and treatment applications.

Literature and methods. Timber markets of the western U.S. havelong been dominated by harvests from public lands, but the situationhas changed in the last decade (Haynes et al. [2001]). National forests ofthe West provided nearly half of all timber harvested during the period1950 1985. Since the late 1980s, however, harvests in the West aredominated by industrial and nonindustrial forestland owners. Marketsin the region have contracted overall, and timber outputs in majorproducing states have declined. Large-scale biomass removals couldresult in a near doubling of timber output in many parts of the fire-prone West.

Large changes in the amount of wood on local markets can affect thewelfare of timber producers and timber consumers by shifting supply(Holmes [1991]). Outward shifts in supply decrease prices and increaseoverall welfare. However, such shifts can have differential impactson various producer and timber consumer groups, especially whenthe outward shift in supply results in a contraction in demand foralternative products. Of particular interest is the effect of such shifts onprivate timber producers, whose outputs compete directly with outputsof national forests (Adams et al. [1996]).

Outward shifts in supply such as those associated with salvage re-moval programs are often short-run, affecting local markets for only afew months to a couple of years (Holmes [1991], Prestemon and Holmes[2000]). If such outward shifts in supply are perceived by demandersto be temporary, then demand will not increase and market responsesto supply increases are limited by local mill production capacities andmarkets for mill outputs. In the case of a short-run supply shift, timberconsumers gain but producers, especially producers not participatingin a biomass reduction program, may be harmed. This effect is similar

TIMBER MARKETS AND FUEL TREATMENTS 19

to programs such as tree planting incentives which are intended to in-crease future timber supplies (Boyd and Hyde [1989]). If supply shiftsare perceived as permanent, then arbitrage can lead to outward de-mand shifts that return prices to normal and increase economic welfaregenerally within the sector.

Timber supply in areas of significant federal timber harvests can bedescribed as consisting of two components: price-responsive privatesupply and policy-driven public supply. Increased public land timberharvests benefit mills but harm private timber suppliers by drivingdown the price of timber. In the calculation of timber market effects oftreatments, economic surplus is estimated using techniques describedby Just et al. [1982]. These techniques have been applied frequently inforestry, e.g., Holmes [1991], Wear and Lee [1993].

From the perspective of public timber supply, there are at leasttwo possible outcomes for the timber market with a biomass removalsprogram in place, and these two outcomes depend on whether biomassremovals substitute for regular removals from public lands or merelyadd to them. There would be no immediate market effects on producersor timber consumers in the short-run if (1) product removals frombiomass treatments substitute for regular harvests and (2) the costsper unit to get the product to markets are the same and (3) the mix ofproducts going to markets remains the same. Over the long run, theprograms would affect residual stands, including growth rates, finalproducts obtained from a different inventory structure and wildfiresalvage volumes obtained from the forests under an altered wildfirerisk.

In this analysis, biomass removals are assumed to supplement regularpublic harvests. The price effects of these programs would dependon how fast timber demand can adjust to a larger supply obtainedfrom the treatments. Large, brief programs of biomass removals willdepress prices, harming private producers and benefiting wood productmanufacturers (the timber consumers).

From the perspective of timber demand, the impact of biomassremovals programs on markets will depend on the demand response,either (1) affecting trade across regions and the process of spatialarbitrage and/or (2) altering capacity utilization rates at existing millsand/or (3) influencing the creation of new capacity in the vicinity of

20 K.L. ABT AND J.P. PRESTEMON

the treatment zones. The current study evaluates only the short-runsituation where local demand stays constant, thus market responses(1) trade and (2) capacity utilization will be incorporated. Local priceeffects may be moderated if the products from treatment programscan be profitably moved outside the region. Such movement, however,would have economic effects outside the region that should be accountedfor (Murray and Wear [1998]). Recent research (Prestemon and Holmes[2000], Nagubadi et al. [2001], Bingham et al. [2003]) has shown thatlow product values and high shipping costs or market inefficiencies canlimit the transmission of local market changes to more distant markets.

Figure 1 illustrates the welfare, price and quantity effects arising froma fuels treatment program in a market with both public and privateharvests but no trade. Private timber supply is price-responsive, in-creasing in quantity with increasing price. Public supply is symbolizedby a vertical line, SG

0 . Price in the market for timber is set where thecurve representing the sum of private supply and public supply, S0,intersects the timber derived demand curve, D, at point a, resulting inthe equilibrium price P0 and quantity Q0 without a fire-related biomassremovals program. Producer economic surplus is the area above theprivate supply curve and below price, area P0ac. Economic surplusaccruing to timber consumers is the area above price and below thedemand curve, area daP0.

Where the harvests from a large scale program of fire-related biomasstreatments on national forests add to regular removals, thus not sub-stituting for regular harvests, the government supply curve shifts toSG

1 , so that total supply shifts outward, to S1. The total quantityoffered with the shifted supply curve, including private supply, is Q1,and price drops to P1. Producer economic surplus for private timberproducers is area feb, while government revenues from treatments andregular harvests amount to area P1fe. Surplus accruing to timber con-sumers is larger than without the biomass removals and is now areadbP1. Note that the producer surplus accruing to private producersis reduced unambiguously by such a treatment program, as the mar-ket price declines and their volume sold shrinks5. Also, these changesmight apply to producers and consumers locally, but the opportuni-ties to ship product outside a region of fuel treatments can reduce thewelfare effects of such a program. Emphases on different parts of atreatment region can also have anomalous effects on consumers and

TIMBER MARKETS AND FUEL TREATMENTS 21

d

P0

P1

QG0 Q

G1 Q0 Q1

a

c e

b

S0

S1

SG0 SG

1

D

f

FIGURE 1. Timber market structure in areas with public timber harvests,with a representation of the effects of a biomass removals program.

producers. If treatment programs effectively substitute less valuabletreated material for more valuable untreated material, provided thatthe government subsidizes such treatments, consumers may be left onlymarginally better off and producers much worse off.

If supply shifts past the point where demand intersects the horizontalaxis, then producers lose all timber market surplus they sell no timber,as the market price for timber is zero and public landowners get novalue. In fact, the public would have to pay timber harvesters to removethe biomass. Timber consumers would still gain, however, as wood isprovided to them at no cost or they would need to be paid to cut it6.

A similar story could be told about benefits accruing to producersand consumers if, instead of new capacity developing locally, demandshifts outward as a result of expanded wood product exports out ofthe region to other parts of the United States or abroad. The timberconsumers benefited in that case would reside outside of the treatmentregion.

Another component of market analysis is identification of intermarketrelationships. If markets are integrated, that is, if local market shocksare transmitted, see Ravallion [1986], and biomass harvests are large,

22 K.L. ABT AND J.P. PRESTEMON

0

80,000

160,000

240,000

320,000

400,000

AZ

CA

CO ID MT

NV

NM OR

SD UT

WA

WY

Are

a T

reat

ed (

Acr

es)

CC 3 Only Available

CC 2 & CC 3 Available

All CC Available

A

B

0

80,000

160,000

240,000

320,000

400,000

AZ

CA

CO ID MT

NV

NM OR

SD UT

WA

WY

Are

a T

reat

ed (

Acr

es)

CC 3 Only Available

CC 2 & CC 3 Available

All CC Available

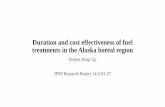

FIGURE 2. Treated by state under alternative condition class constraints,without (A) and with (B) state-level treatment proportional constraints, undera treated acreage maximization primary objective, on national forests of theUnited States.

TIMBER MARKETS AND FUEL TREATMENTS 23

then the price effects of these harvests can be transmitted across re-gions, resulting in economic effects of these harvests that go beyond thetreatment zone. Unless these intermarket relationships are understoodand quantified, single market analyses would reach erroneous conclu-sions. One method of evaluating the degree of market linkages is byexamining the costs of transfer of various forest products among pro-ducing and consuming markets. These are the methods outlined bySamuelson [1952] and Takayama and Judge [1964].

Data. The 12 states included in the model incorporate 13 foresttypes and are modeled as producing 4 softwood products which aregrouped here as (1) ponderosa pine, including ponderosa pine (Pinusponderosa) and sugar pine (Pinus lambertiana), (2) lodgepole pine(Pinus contorta), (3) other softwoods and (4) softwood chips. In thecurrent model, the chip market uses a fixed price of $0.35 per cubicmeter and is assumed to be not influenced by the treatment program7.

The model allows for trade with other regions by adding westernCanada and the rest of the world as two additional markets. West-ern Canada includes British Columbia and Alberta. The remainingCanadian provinces, the eastern and southern U.S., and all other coun-tries are referred to as the rest of the world. Northern Alberta andNorthern BC are modeled as lodgepole pine, southern Alberta as con-taining mainly ponderosa pine and BC as containing other softwood.Trade with the rest of the world is allowed only by the coastal statesand easternmost states, while trade with Canada is allowed only bythe northern border states. Exports of logs from public lands in boththe western U.S. and from Canada are restricted by law and thus areconstrained to zero in the model. Exports of logs from private landsare allowed from both countries. Import taxes on logs are set to zero,consistent with the North American Free Trade Agreement and the ma-jority of U.S. and Canadian log export destinations and import sources.

Inventory and acres. Inventory volume and acreage data are fromthe Western Biomass Assessment (Rummer at al. [2003]) and consistof volumes and acres by major species group by state, Table 1. Thesevolumes were then proportionately assigned to the wildland urban in-terface (WUI) and to fire regime-condition classes (CC) by the propor-tion of the total area in each state in these classes. Wildland-urban

TA

BLE

1.

Nati

onalfo

rest

tim

ber

land

acr

es,pro

port

ion

trea

table

,tr

eata

ble

acr

esby

fire

regim

e-co

nditio

ncl

ass

,and

pro

port

ion

inth

ew

ildla

nd

urb

an

inte

rface

.

Sta

teTota

lP

roport

ion

Tre

ata

ble

acr

esby

fire

Pro

port

ion

tim

ber

land

trea

table

regim

e-co

ndit

ion

class

ofacr

es

acr

esC

C1

CC

2C

C3

inW

UI

Ari

zona

18,3

64,4

81

0.5

11,1

35,3

20

5,5

48,0

57

2,6

91,0

24

0.0

5

Califo

rnia

38,4

59,6

10

0.4

02,8

01,0

71

7,7

07,6

96

4,8

08,2

16

0.1

8

Colo

rado

20,5

67,5

47

0.4

53,4

20,4

35

3,2

42,3

24

2,6

56,3

55

0.0

6

Idaho

21,9

38,0

49

0.5

11,9

24,5

02

5,8

25,4

47

3,3

94,1

00

0.0

1

Monta

na

21,2

72,3

89

0.5

12,6

46,0

15

4,6

35,8

77

3,5

36,8

36

0.0

1

Nev

ada

8,9

23,4

68

0.5

8783,7

11

2,8

85,9

08

1,4

76,2

79

0.0

3

New

Mex

ico

19,3

20,4

42

0.4

01,6

18,8

55

3,3

40,9

44

2,7

25,0

91

0.0

2

Ore

gon

27,7

38,7

34

0.4

01,9

10,8

62

4,6

92,7

01

4,5

68,9

23

0.0

4

South

Dakota

1,6

40,5

14

0.4

745,0

48

243,3

08

489,5

31

0.0

1

Uta

h15,2

44,3

99

0.4

83,8

52,1

92

2,9

58,8

95

502,6

21

0.0

4

Wash

ingto

n19,8

09,1

21

0.3

62,6

76,2

79

3,3

25,4

12

1,2

22,3

34

0.1

2

Wyom

ing

10,8

28,3

93

0.4

33,3

95,1

83

967,8

92

338,6

05

0.0

1

TIMBER MARKETS AND FUEL TREATMENTS 25

interface area was calculated using wildland-urban interface maps pro-vided directly by Radeloff (V. Radeloff, personal communication [May2003]). Fire regime-condition class represents a broad scale determina-tion of fire risk, where condition class represents the degree of departurefrom historical fire regimes, with CC 1 closest to historical and CC 3furthest away from the historical fire regime.

Treatments are applied only to national forest timberland and lessthan 60 percent of the timberland is assumed harvestable, consistentwith the Western Biomass Assessment (Rummer et al. [2003]). Ourestimates of potentially treatable acres by state by condition class arein Table 2. This table also shows the proportion of treatable timberlandin each state that is assumed to be in the wildland-urban interface.

Current production. Current harvest data were developed using the1997 Forest Statistics of the United States removals and product data(Smith et al. [2001]). Hardwood removals account for only 4 percentof all timber removals in the 12 states and were not further addressedin this study. The removals used as base data for the model are shownin Table 2. Removals are reported by national forest ownership and bynon-national forest ownership and by major species group.

Base level mill capacities and timber production levels in the U.S. andCanada derive from Spelter and Alderman [2003] and were adjusted foreach state to reflect non-included mills. Outside the U.S. and Canada,softwood log production and processing capacities were set at 100%and 110% of production, respectively, as reported by FAO [2004] for2002.

Treatments. The fuel reduction treatment, applied to all 13 foresttypes and 3 condition classes, removes volume on a stand to reducestand density to 30 percent of maximum stand density index for thatforest type and ecoregion. This treatment removes trees from all sizeclasses, concentrating most removals in the small to mid-sized diameterclasses. The prescription had no upper diameter limit on removals.Fiedler et al. [2001] found that removals from all diameter classes hadmore effect on reducing fire risk measures than did removals from onlythe smaller diameter classes. The SDI prescription is an ‘average’treatment that allows analysis of all western forests at an aggregate

TA

BLE

2.

Rem

ova

lsfr

om

nati

onalfo

rest

sand

oth

erow

ner

ship

s

by

majo

rsp

ecie

sgro

up

by

state

.

Nati

onalfo

rest

sN

on-n

ati

onalfo

rest

s

Sta

tePonder

osa

Lodgep

ole

Oth

erPonder

osa

Lodgep

ole

Oth

er

pin

epin

eso

ftw

ood

pin

epin

eso

ftw

ood

Thousa

nd

board

feet

Ari

zona

29,2

04

08,1

60

15,7

25

04,3

94

Califo

rnia

411,4

47

37,7

02

1,5

99,8

91

96,5

12

8,8

44

375,2

83

Colo

rado

3,5

89

5,4

33

22,0

27

1,9

33

2,9

25

11,8

61

Idaho

64,3

07

60,1

89

473,4

51

34,6

27

32,4

10

254,9

35

Monta

na

41,6

93

89,0

15

282,5

45

22,4

50

47,9

31

152,1

40

Nev

ada

1,0

91

433

1,7

25

587

233

929

New

Mex

ico

16,5

78

012,3

10

8,9

27

06,6

28

Ore

gon

272,1

49

44,5

63

2,4

84,7

29

79,0

11

12,9

38

721,3

73

South

Dakota

13,0

02

06,7

70

25,2

40

013,1

42

Uta

h1,7

01

1,5

01

14,8

35

916

808

7,9

88

Wash

ingto

n151,4

03

42,7

57

2,5

15,4

21

43,9

56

12,4

13

730,2

84

Wyom

ing

5,4

79

9,3

55

19,4

73

2,9

50

5,0

37

10,4

86

TIMBER MARKETS AND FUEL TREATMENTS 27

level. Actual treatments for stands are not expected to correspondto these prescriptions and should be designed for each stand usinginformation that is not available in the Forest Inventory and Analysisdatabase.

Although many mechanical fuel treatments will not remove anyproducts, these treatments are not discussed in this analysis as theywill not have any market effects. It is also possible that treatments willbe chosen that will remove some products and leave non-merchantablebiomass on site. The treatment applied in this model does not allow forpartial product removal from the stand. Only sawlogs were modeledin this analysis, and products were merchandized as in the WesternBiomass Assessment (Rummer et al. [2003]).

Costs and prices. Product prices were derived from National ForestSystem Cut and Sold reports for the second quarter of 20038 and areshown in Table 3. Regional prices were adjusted by the percentageof harvest from each species group to provide species prices. Pricesdiffer by state and major species group, ranging from a low of $39 perthousand board feet (mbf) in Arizona and New Mexico for lodgepolepine to a high of $528/mbf in Oregon and Washington for ponderosapine. Treatment costs are determined using the methodology of theWestern Biomass Assessment (Rummer et al. [2003]), Table 3. TheSTHarvest model (Hartsough et al. [2001]) was developed to assessthe costs of removing small diameter timber from stands in the PacificNorthwest and was applied to volumes and acres in all western states.The resulting costs range from a low of $288 per acre in Utah’s othersoftwood types to a high of $3,044 per acre in Utah’s lodgepole pinetype. Variations are due to slope and distances to mill differences acrossstate and differences in treating various species groups in each state.

Trade between states and regions will occur when the net cost to animporting region is less than the cost of procuring logs locally. Thustransportation costs will be essential to development of trade patternsin the model. Following Fight (personal communication [May 2003])and Rummer et al. [2003], we assume the cost of transporting woodbetween states is $0.35/bone dry ton (bdt) per mile or $1/mbf/mile.Distance from stump to mill is proxied by the distance to mill average ineach state. Distances between states for trade purposes are determinedby using the distance between spatial-center of forestland in each state.

TA

BLE

3.

Del

iver

edlo

gpri

ces

and

trea

tmen

tco

sts

by

majo

rsp

ecie

sgro

up

by

state

.

Log

pri

ceTre

atm

ent

cost

Sta

tePonder

osa

Lodgep

ole

Oth

erPonder

osa

Lodgep

ole

Oth

er

pin

epin

eso

ftw

ood

pin

epin

eso

ftw

ood

$/th

ousa

nd

board

feet

$/acr

e

Ari

zona

43

39

200

1,7

96

1,6

32

383

Califo

rnia

300

280

400

1,1

39

1,2

08

2,3

98

Colo

rado

219

204

200

1,1

29

2,0

35

1,3

63

Idaho

493

460

400

816

2,2

86

1,3

14

Monta

na

493

460

400

816

2,2

86

1,3

14

Nev

ada

98

91

200

680

3,0

24

397

New

Mex

ico

43

39

200

1,3

22

1,8

91

504

Ore

gon

528

493

400

1,0

20

1,8

47

1,7

28

South

Dakota

219

204

200

994

2,0

35

1,3

68

Uta

h98

91

200

680

3,0

24

288

Wash

ingto

n528

493

400

1,0

20

1,8

47

1,7

28

Wyom

ing

98

91

200

994

2,0

35

1,3

68

TIMBER MARKETS AND FUEL TREATMENTS 29

Western U.S. spatial equilibrium model. The model is currentlysolved for a single representative period. We assess a five-year programbut do not grow the stands, treated or untreated. The model maximizeswestern U.S. national forest acres treated in each year of a 5-yearprogram subject to constraints. The acreage maximization occurs overall available acres in each forest type and condition class within eachstate. The objective function and constraints are shown in Table 4,the elasticities assumed are in Table 5 and a summary of the modelsimulations is in Table 6.

The model is solved first as a base case with the objective of max-imizing social net welfare across all producers and timber consumers(summing across western U.S., western Canada and the rest of theworld), not allowing mechanical fuel treatments and thus requiring nosubsidy. Consistent with Samuelson [1952], social net welfare (SNW) isthe sum of producer surplus plus consumer surplus minus transporta-tion costs. In our case, SNW also includes government harvest andtreatment revenues less government harvest costs and less the subsidy.National forest timber harvests are held constant, and a market equi-librium of private plus public production, consumption, and trade arefound. For national forest timber, regardless of WUI, two sets of simu-lations were run, with each set including three condition class-restrictedmodels. The first set modeled a $1 billion subsidy without a limit onexpenditures by state. The second set limited expenditures by stateto a maximum equal to the proportion of timberland that state hadin each condition class. The condition class-restricted models allowedtreatments on (1) CC 3 only, (2) CC 2 + CC 3, and (3) all three condi-tion classes. A similar set of simulations was done restricting treatmentto only the designated WUI acres.

Products analyzed include softwood sawtimber and chips, and weallow for a maximum of a 30 percent outward shift in demand, i.e.,demand capacity within a region can expand by 30 percent. Demandand supply elasticities with respect to price are inelastic and inventorysupply elasticity is assumed to be one, Table 5. These elasticities areconsistent with the published literature (Adams and Haynes [1980],Majerus [1980], Regional Forester [1984], Adams et al. [1986], Wear[1989], Adams et al. [1991], Newman [1987], Abt et al. [2000], Hayneset al. [2001]).

TA

BLE

4.

Spati

aleq

uilib

rium

model

obje

ctiv

efu

nct

ions

and

const

rain

ts.

Base

Model

Obje

ctiv

efu

nct

ion

Maxim

ize

soci

alnet

wel

fare

=su

mofpro

duce

rsu

rplu

s

+su

mofco

nsu

mer

surp

lus

+gover

nm

ent

reven

ues

from

regula

rharv

est−

gover

nm

ent

harv

est

cost

s

Const

rain

tsP

ublic

log

export

=0

Harv

est

cannot

exce

ed1.3

tim

escu

rren

tharv

est

Capaci

tyuti

liza

tion

islim

ited

toa

maxim

um

of

1.3

tim

escu

rren

tpro

duct

ion

and

a

min

imum

of.4

5tim

escu

rren

tpro

duct

ion.

Tre

atm

ents

occ

ur

only

on

feder

alla

nds.

Non-t

reatm

ent

gover

nm

ent

harv

est

isco

nst

ant.

Acr

esTre

ate

dM

odel

s

Obje

ctiv

efu

nct

ion

Maxim

ize

acr

estr

eate

d

Const

rain

tsA

bove

const

rain

tsplu

slim

itati

ons

on

trea

ted

acr

esby

wildla

nd

urb

an

inte

rface

class

,co

ndit

ion

class

and

state

alloca

tion

TA

BLE

5.

Dem

and

and

supply

elast

icitie

suse

dto

dev

elop

linea

rdem

and

and

supply

funct

ions

at

curr

ent

price

sand

quanti

ties

. Oth

erst

ate

s:

Califo

rnia

,O

regon

&W

ash

ingto

n

Soft

wood

saw

tim

ber

Supply

with

resp

ect

topri

ce0.3

0.4

3

Supply

with

resp

ect

toin

ven

tory

volu

me

11

Dem

and

wit

hre

spec

tto

pri

ce-0

.5-0

.5

TA

BLE

6.

Sum

mary

ofsi

mula

tions

for

afive

yea

rm

echanic

altr

eatm

ent

pro

gra

mof$1

billion

per

yea

r.Sim

ula

tions

wer

eru

nfo

rall

nati

onalfo

rest

lands

and

for

WU

I-only

lands.

Label

Sim

ula

tion

des

crip

tion

Base

Maxim

ize

net

soci

alw

elfa

re,no

trea

tmen

ts

No

alloca

tion

by

state

Subsi

dy

alloca

tion

tost

ate

sis

unco

nst

rain

ed

CC

3M

axim

ize

trea

ted

acr

eson

condit

ion

class

3acr

esonly

CC

2+

3M

axim

ize

trea

ted

acr

eson

condit

ion

class

2and

3acr

esonly

CC

1+

2+

3M

axim

ize

trea

ted

acr

eson

all

condit

ion

class

es

Alloca

tion

lim

ited

by

state

Subsi

dy

alloca

tion

tost

ate

sis

lim

ited

by

pro

port

ion

ofst

ate

inea

chco

ndit

ion

class

CC

3M

axim

ize

trea

ted

acr

eson

condit

ion

class

3acr

esonly

CC

2+

3M

axim

ize

trea

ted

acr

eson

condit

ion

class

2and

3acr

esonly

CC

1+

2+

3M

axim

ize

trea

ted

acr

eson

all

condit

ion

class

es

32 K.L. ABT AND J.P. PRESTEMON

The model has specific requirements for U.S. federal ownerships,recalling that treatments are allowed only on national forests. Publictimber supply (nontreatment harvest) is assumed non-price responsive,and is held constant for the simulations. Export of logs from federallands in both Canada and the U.S. is prohibited. Calculation of surplusfrom national forest harvests and treatments represents governmentrevenues from sales less costs of treatment or harvest. We assume thecurrent level of national forest harvest generates no surplus (revenues =costs), and use current cost/mbf as the cost of national forests harvestin all simulations.

Simulation results.

No wildland-urban interface constraints. The effect of the treatmentprogram on private timber markets is broadly negative, Table 7, reduc-ing SNW by about 18 percent in the western U.S., as an average acrosstreatment scenarios. This effect is net of gains accruing to western U.S.timber consumers due to cheaper and larger aggregate log volumes en-tering mills, losses for western U.S. private timber producers due tolower prices and lower private timber harvests in response, the costsof wood transport, losses in the value of regular timber harvested fromnational forests also due to lower prices, and the cost to taxpayers ofthe subsidy. For example, under the scenario that limits treatmentsto stands classed as condition class 3 (CC 3), losses in SNW amountto $1.05B in the U.S. West resulting from treatment of about 833,000acres. Relaxing constraints on condition classes to allow any conditionclass stand to be treated leads to similar losses. Timber consumers inthe U.S. West are the primary beneficiaries of a treatment program, asprices drop and consumption increases, with gains ranging from $0.55to about $0.82B, or 12 18 percent. Private producers in the U.S. Westlose no more than $0.19B in economic surplus, losses ranging from 5to 10 percent. Their losses are due to price and output reductions.Similarly, Canadian timber consumers gain, by 2 9 percent, becausedomestic Canadian prices drop and consumption increases in westernCanada, even while total output in that region declines. For exam-ple, if treatments are restricted to CC 3 lands, then Canadian tim-ber consumers gain $0.01B. If treatments are allowed on all conditionclasses, then these effects are accentuated, with gains to Canadian log

TA

BLE

7.

Sim

ula

tion

outc

om

esunder

abase

case

with

aso

cialnet

wel

fare

obje

ctiv

eand

six

acr

eage

maxim

izati

on

obje

ctiv

esw

her

eboth

WU

Iand

non-W

UI

acr

esare

trea

table

.

Sim

ula

tion

WU

I+

non-W

UI

acr

es

Base

case

No

alloca

tion

by

state

Alloca

tion

lim

ited

by

state

CC

3C

C2+

3C

C1+

2+

3C

C3

CC

2+

3C

C1+

2+

3

Billion

dollars

Soci

alnet

wel

fare

,W

.U

.S.

6.1

95.1

44.9

84.7

35.2

45.1

55.0

9

Subsi

dy

use

d0.0

01.0

01.0

01.0

00.9

81.0

01.0

0

Govt.

trea

tmen

tre

ven

ues

0.0

00.2

70.2

30.1

90.3

00.2

60.2

2

Reg

ula

rgovt.

harv

est

reven

ues

1.0

90.9

20.9

50.9

60.9

20.9

30.8

9R

egula

rgovt.

harv

est

cost

s1.0

11.0

11.0

11.0

11.0

11.0

11.0

1

Consu

mer

surp

lus,

W.U

.S.

4.5

75.2

75.1

35.1

25.2

75.2

35.3

9

Pri

vate

pro

duce

rsu

rplu

s,W

.U

.S.

1.7

91.6

41.6

81.7

01.6

41.6

51.6

0Tra

nsp

ort

cost

s,W

.U

.S.

0.2

50.9

61.0

11.2

40.9

00.9

01.0

1

Consu

mer

surp

lus,

W.C

anada

0.6

10.6

20.6

50.6

60.6

20.6

40.6

6P

riva

tepro

duce

rsu

rplu

s,W

.C

anada

0.8

90.8

70.8

50.8

40.8

70.8

60.8

4C

onsu

mer

surp

lus,

rest

ofth

ew

orl

d3.8

93.9

93.9

83.9

84.0

03.9

93.9

7P

roduce

rsu

rplu

s,re

stofth

ew

orl

d15.4

215.3

315.3

315.3

315.3

115.3

315.3

4

Acr

es

Tota

lare

atr

eate

d0

832,6

41

1,0

73,7

22

1,2

21,1

64

814,9

34

1,0

11,4

66

1,0

62,1

41

Ponder

osa

pin

e0

423,7

93

734,7

78

776,8

81

394,9

01

627,3

06

605,1

60

Lodgep

ole

pin

e0

137,8

13

5,7

21

39,1

32

127,7

72

25,8

75

5,7

17

Oth

erso

ftw

ood

0271,0

35

333,2

22

405,1

51

292,2

61

358,2

85

451,2

63

34 K.L. ABT AND J.P. PRESTEMON

consumers as high as $0.06B. U.S. western exports to the eastern U.S.and elsewhere outside the West help to alleviate downward price pres-sure in the western U.S. Note that these effects ignore somewhat com-pensatory effects on secondary product markets, e.g., lumber, thatcould be quantified but were not explicitly modeled here.

When state-level restrictions on treatment subsidies are imposed, allof the effects of a treatment program are changed. Timber consumers inthe western U.S. are benefited in a manner similar to an unconstrainedprogram, because little new log volumes are produced and prices do notdrop much. Also, the state-level restrictions appear to work in favor ofconsumers, forcing more volume to be treated in places with higher millcapacities and higher value product. Private producers in the regionare harmed more, in contrast, as public production uses available millcapacity and replaces more valuable private timber to accommodate thetreatment program. The amount of forest treated is also smaller whena state-level spending constraint is imposed. On average, imposingsuch a constraint reduces the area treated by about 3 percent, from833,000 to 815,000 acres when only CC 3 lands are treatable; when allcondition classes can receive mechanical fuel treatments, the effect ofthe constraint is to reduce the area treated by 15 percent.

Under this set of scenarios, not limited to wildland-urban interfaceforests, the area treated differs greatly across forest types, Table 7.In most cases, ponderosa pine types receive the greatest amount oftreatment because these stands comprise much of the riskiest andtreatable area, Table 1. When less risky forest stands are includedin the available treatable forests, lodgepole pine stands go largelyuntreated, while resources are devoted substantially to other softwoodforest types and to ponderosa pine types. Despite this heterogeneityin the area treated across forest types, the share of land receivingtreatment differs less radically across the West than in the simulationswithout a state constraint. This rather even distribution is reflectiveof the fact that ponderosa and other softwood types are common inthe region, especially compared to lodgepole, a type most common innorthern and high elevation locations.

As constraints on the condition class are relaxed to include all classes,treatments shift across states. States such as New Mexico, Idaho,Montana and Oregon experience smaller changes or even negativechanges in treated areas as constraints on condition class are relaxed.

TA

BLE

8.

Sim

ula

tion

outc

om

esunder

abase

case

with

aso

cialnet

wel

fare

obje

ctiv

e

and

six

acr

eage

maxim

izati

on

obje

ctiv

esw

her

eonly

WU

Iacr

esare

trea

table

.

Sim

ula

tion

WU

I+

non-W

UI

acr

es

Base

case

No

alloca

tion

by

state

Alloca

tion

lim

ited

by

state

CC

3C

C2+

3C

C1+

2+

3C

C3

CC

2+

3C

C1+

2+

3

Billion

dollars

Soci

alnet

wel

fare

,W

.U

.S.

6.1

96.1

46.0

76.0

36.1

56.0

86.0

6

Subsi

dy

use

d0.0

00.0

70.1

70.2

60.0

60.1

40.2

0

Govt.

trea

tmen

tre

ven

ues

0.0

00.0

70.1

70.2

50.0

70.1

40.2

1

Reg

ula

rgovt.

harv

est

reven

ues

1.0

91.0

71.0

51.0

41.0

71.0

41.0

2R

egula

rgovt.

harv

est

cost

s1.0

11.0

11.0

11.0

11.0

11.0

11.0

1

Consu

mer

surp

lus,

W.U

.S.

4.5

74.6

54.7

24.8

14.6

44.7

94.8

7

Pri

vate

pro

duce

rsu

rplu

s,W

.U

.S.

1.7

91.7

61.7

31.6

91.7

71.7

21.6

8Tra

nsp

ort

cost

s,W

.U

.S.

0.2

50.3

40.4

20.4

80.3

30.4

60.5

0

Consu

mer

surp

lus,

W.C

anada

0.6

10.6

10.6

10.6

10.6

10.6

10.6

1P

riva

tepro

duce

rsu

rplu

s,W

.C

anada

0.8

90.8

90.8

90.8

90.8

90.8

90.8

9C

onsu

mer

surp

lus,

rest

ofth

ew

orl

d3.8

93.8

93.9

03.9

03.8

93.8

93.8

9P

roduce

rsu

rplu

s,re

stofth

ew

orl

d15.4

215.4

215.4

115.4

115.4

215.4

215.4

2

Acr

es

Tota

lare

atr

eate

d0

52,6

45

115,7

38

171,0

76

47,6

34

99,0

84

148,2

72

Ponder

osa

pin

e0

33,2

20

61,3

74

67,9

08

32,0

66

58,8

11

65,2

11

Lodgep

ole

pin

e0

4,6

52

9,7

51

18,3

29

3,5

71

7,5

08

14,1

54

Oth

erso

ftw

ood

04,7

73

44,6

12

84,8

39

11,9

96

32,7

66

68,9

07

36 K.L. ABT AND J.P. PRESTEMON

The area added to the total mainly comes from Utah and California,which have an abundance of CC 1 land that can be cheaply treated andfor which capacity constraints do not bind. When state-level treatmentspending constraints are enforced, added acres in CC 1 come principallyfrom Utah, Washington and Wyoming. Utah and Washington haveavailable demand capacity, while Wyoming has the ability to cheaplyexport more material to the consuming mills of the eastern U.S. andMontana.

Wildland-urban interface constraints imposed. When treatment pro-grams are limited to treating national forest lands in the West includedin the wildland-urban interface, the market impacts and area treatedare much smaller, Table 8. In this set of scenarios, the $1B subsidyavailable is never exhausted, i.e., it never binds in simulations. Thiskeeps the annual cost of such a treatment program low and moderatesthe negative overall effects on welfare. For example, SNW, includinggovernment harvest revenues and costs, decreases by an average of onlyabout 2 percent across all scenarios, declining from about $6.19B to anaverage of $6.09B. The beneficial effects on western U.S. consumers aresimilarly small, rising 1 percent under scenarios limiting treatments toCC 3 WUI lands and 7 percent when all condition class lands in theWUI are treatable. Western U.S. private timber producers lose from 1to 6 percent in economic surplus under alternative scenarios.

Forest types receiving treatments reflect which kinds of treatableacres exist close to urban areas. In this case, the focus on California,Oregon and Washington means that more non-ponderosa pine forestsare treated. In fact, when all condition class constraints are relaxed,non-ponderosa forests get most of the treatment dollars allocated. Theeffects of the wildlandurban interface constraint on treatment leadsto obvious biases in states receiving the bulk of the mechanical fueltreatments, Figure 3. These biases result directly from the amountof wildlandurban interface and the available capacity; large availablecapacities tend to limit the negative impacts of the treatment program.In this set of scenarios, states receiving the lion’s share of the programare California, Washington and Oregon, with intermediate amountsgoing to Colorado, New Mexico and Arizona. The program thereforeleaves out the low population and low-capacity states of Nevada, SouthDakota, Wyoming and Utah. Although Montana, Idaho and even

TIMBER MARKETS AND FUEL TREATMENTS 37

A

0

20,000

40,000

60,000

80,000

100,000

AZ

CA

CO ID MT

NV

NM OR

SD UT

WA

WY

Are

a T

reat

ed (

Acr

es)

All CC Available

CC 2 & CC 3 Available

CC 3 Only Available

B

0

20,000

40,000

60,000

80,000

100,000

AZ

CA

CO ID MT

NV

NM OR

SD UT

WA

WY

Are

a T

reat

ed (

Acr

es)

All CC Available

CC 2 & CC 3 Available

CC 3 Only Available

FIGURE 3. WUI-only area treated by state, without (A) and with (B) state-level treatment proportional constraints, under a treated acreage maximizationprimary objective, on National Forests of the United States.

38 K.L. ABT AND J.P. PRESTEMON

Arizona have at least some capacity, their low amounts of nationalforest land with significant urban interface pressure means that they,too, get little of the subsidy under this scenario.

Conclusions. While mechanical treatments may not be the closestsurrogate to wildfire in fire prone areas, mechanical methods may bepreferred to prescribed fire, for several reasons. Fire-related mechanicaltreatments are not constrained by the logistical difficulties of weathertiming or by risk of damage to adjacent properties and do not createsmoke, with its attendant air quality consequences. In addition, somehave viewed broad-scale fuel treatments as potentially beneficial to tim-ber markets, reinvigorating communities, which in places of substan-tial federal forest holdings have been negatively affected economicallyby federal harvest reductions (Spelter et al. [1996], USDA Forest Ser-vice [2000], Paun and Jackson [2000]). However, treatment programadministrators and timber market analysts should understand them asmultifaceted, affecting fire risk, ecological values and the timber mar-ket. Further, timber market analysts should place the program’s mar-ket impacts into the context of trade in forest products. Finally, giventhat one focus of the Healthy Forest Restoration Act is to reduce fuelsin the vicinity of communities at risk of catastrophic wildfires, such ananalysis should evaluate the market impacts of imposing WUI-relatedconstraints on program spending allocations. The research reportedhere is a first attempt to understand these issues.

Our analysis has shown that large scale programs of mechanical fueltreatments have the potential to influence the timber market signifi-cantly. With large fuel reduction programs, we find that timber con-sumer welfare in the western U.S. could be enhanced by up to 18 per-cent if managers were successful in implementing the program broadlyacross the region. On the other hand, private timber producers wouldface declines of up to 11 percent in welfare, due to lower productionand prices. The revenues accruing to the U.S. Treasury through na-tional forest harvests would increase, providing more payments in lieuof taxes for counties where treatments occur. However, the revenueswould not rise by as much as the timber volume, since mill capacitylimits would be quickly reached in certain locations and transportingsome of the material out of the treatment zone is relatively expen-sive and therefore would not be economically feasible. Also, decision

TIMBER MARKETS AND FUEL TREATMENTS 39

makers and land managers need to be cognizant of potential geographi-cal inequities in such treatment programs across counties. For example,one county could receive much of the treatment and payments in lieuof taxes, due to its large federal holdings, while the neighboring countywith mainly private lands could be negatively impacted by lower tim-ber prices and lower output. From a broader geographical perspective,a program focusing on treating as many acres as possible under a fixedbudget would result in certain states receiving most of the subsidy.Coastal states and states with ponderosa pine forests would get muchtreatment, while high-elevation and northerly states such as Montana,Wyoming and Colorado would get little.

From the standpoint of treatment efficacy, a treatment program thatreduced timber market welfare by these magnitudes should have fireeffects and ecosystem restoration benefits that are at least equal to themarket losses. Inclusion of the expected net benefits of the treatmentsin reducing aggregate losses and costs of wildfire may provide a differentperspective on the value of a mechanical treatment program.

Large scale programs would have uneven or scale-dependent effectson our trading partners and other parts of the U.S. Western Canadiantimber consumers were found to be beneficiaries of a U.S. mechanicalfuel treatment program through lower prices and greater volumesconsumed, while producers there appear to lose 1 6 percent in producersurplus (due to lower prices and lower volume produced). Prohibitionsagainst the export of softwood logs from public lands in the U.S. West,however, mean that the effects of a treatment program on Canadawould be muted and constrained. This conclusion, however, ignores thebeneficial impacts of greater treatment volumes in the lumber marketin the U.S.: domestic lumber manufacturers would find themselves ina more favorable position relative to competing Canadian softwoodlumber producers, compared to no treatment program.

A program exclusively focused on the wildland-urban interface wouldhave small impacts on western and non-western timber markets in theU.S., Canada and abroad. If a program were implemented so thatonly WUI lands would receive treatments on national forest land, thisprogram would be most active in California, Washington and Col-orado. States such as South Dakota, Wyoming and Nevada wouldbe essentially ignored. Our analysis did not address the potential

40 K.L. ABT AND J.P. PRESTEMON

benefits of a WUI-only program in terms of reducing the costs ofwildfires.

On the other hand, given that the budget for treatments in a WUI-only program never binds, it seems logical that the program evaluatedin our research is not the kind that would be implemented. Instead,government would most likely create a program that imposes a WUI-first constraint.

This research leaves substantial room for further analysis. First, weconfined our analysis to evaluating trade impacts with western Canadaand the rest of the world. A more disaggregated analysis, at leastquantifying effects in eastern Canada and the eastern U.S., could pro-vide more relevant information for decision makers in government andforest industry. Second, this study assumed that treatment programswould add to regular timber harvest on federal lands. Further analy-sis would quantify how differing rates of substitution between regularharvest and treatment removals would affect treatment revenues, reg-ular harvest revenues and the amount of treatments ultimately com-pleted under a fixed budget. Managerial limits on federal lands lead tothe expectation of at least some substitution. Third, our analysis wasshort-run and single-year, ignoring allocations over time and changesin demand capacity. The market effects of a treatment program couldbe smaller if the treatments were optimally spread out over time tomaintain a desired maximum fire risk or fire fuel level. This model alsoignored potential adaptations in timber demand, particularly capacityadjustments.

Fourth, a model that accounted for the potential differential costs oftreatment in the wildland-urban interface compared to merely wildlandforests would quantify the tradeoffs among alternative WUI-focusedstrategies. Fifth, our analysis was limited to federal lands of the West,which is naive in at least one respect: much of the forests especially inneed of risk reduction treatments are privately owned. An economicframework that could correctly describe a subsidy program for mechan-ical fuel treatments on private lands would need to account for exter-nalities including free-rider behavior, adoption behavior and methodsof encouraging optimal treatment patterns on the landscape. Sixth, ouranalysis used fire regime-condition classes as the yardsticks for prior-itizing treatments across the U.S. West. Alternative approaches include

TIMBER MARKETS AND FUEL TREATMENTS 41

treating stands to maximize fire risk reduction, or to maximize productvolumes removed, or to maximize long-run net benefits.

Acknowledgments. The authors thank Robert C. Abt, David T.Butry, Roger Fight, R. James Barbour, Robert Rummer and Peter Incefor their advice in various stages of this paper’s development.

ENDNOTES

1. The National Fire Plan is available at: http://www.fireplan.gov.

2. The Healthy Forests Initiative is available at: http://www.fs.fed.us/projects/documents/HealthyForests Pres Policy%20A6 v2.pdf.

3. Healthy Forests Restoration Act, HR 1904, December 3, 2003. Available at:http://frwebgate.access.gpo.gov/cgi-bin/getdoc.cgi?dbname=108 cong bills&docid=f:h1904enr.txt.pdf.

4. A collaborative approach for reducing wildland fire risks to communities andthe environment: 10 year comprehensive strategy (8/2001) (http://www.fireplan/gov/reports/7-19-en.pdf) and Implementation Plan (5/2002) (http://www.fireplan.gov/reports/11-23-en.pdf).

5. We note here that integrated forest products firms, with both timberlandsand mills, would be ambiguously affected by a treatment program simultaneouslyreducing the value of their timber and also the price of log inputs to their mills.

6. In areas of high wildfire risk, biomass removals that are done at negative pricesfor the biomass may still yield positive net economic benefits for society, if treatmentcosts are less than benefits derived from reducing expected losses from wildfire. Thepayoffs from these kinds of biomass removals programs therefore require an analysisof the trade-offs of the program costs and expected wildfire net value changes.

7. Chip values from treatment harvests are small relative to log values. Tothe extent that treatments introduce these chips into markets, welfare of chipconsumers, e.g., panel and pulp mills, and chip producers will be affected. Wehave found in initial analysis that chip market volume effects are second order tolog market effects.

8. Cut and sold reports, National Forest System, Second Quarter 2003, availableat: http://www.fs.fed.us/forestmanagement/reports/sold-harvest/2003q1harv.shtml. Accessed on October 6, 2004.

REFERENCES

R.C. Abt, F.W. Cubbage and G. Pacheco [2000], Southern Forest ResourceAssessment Using the Subregional Timber Supply (SRTS) Model, Forest Prod. J.50, 25 33.

D.M. Adams, R.J. Alig, B.A. McCarl, J.M. Callaway and S.M. Winnett [1996],An Analysis of the Impacts of Public Timber Harvest Policies on Private ForestManagement in the United States, Forest Sci. 42, 343 358.

42 K.L. ABT AND J.P. PRESTEMON

D.M. Adams, C.S. Binkley and P.A. Cardellichio [1991], Is the Level of NationalForest Timber Harvest Sensitive to Price? Land Econ. 67, 74 84.

D.M. Adams and R.W. Haynes [1980], The 1980 Softwood Timber AssessmentMarket Model : Structure, Projections and Policy Simulations, Forest Sci. Monogr.22, 64 pp.

D.M. Adams, B.A. McCarl and L. Homayounfarrokh [1986], The Role of ExchangeRates in Canadian-United States Lumber Trade, Forest Sci. 32, 973 988.

S.F. Arno, H.Y. Smith and M.A. Krebs [1997], Old Growth Ponderosa Pine andWestern Larch Stand Structures: Influences of Pre-1900 Fires and Fire Exclusion,USDA Forest Serv. Res. Paper INT-RP-495, 20 pp.

M. Bingham, J.P. Prestemon, D.J. MacNair and R.C. Abt [2003], Market Struc-ture in U.S. Southern Pine Roundwood, J. Forest Econ. 9, 97 117.

T.M. Bonnicksen and E.P. Stone [1982], Reconstruction of a Presettlement Gi-ant Sequoia-Mixed Conifer Forest Community Using the Aggregation Approach,Ecology 63, 1134 1148.

R.G. Boyd and W.F. Hyde [1989], Comparing the Effectiveness of Cost Sharingand Technical Assistance Programs, in Forestry Sector Intervention: The Impactsof Public Regulation on Social Welfare, Iowa State Univ. Press, Ames, IA, 48 89.

C. Chang [1996], Ecosystem Responses to Fire and Variations in Fire Regimes, inSierra Nevada Ecosystem Project: Final Report to Congress, Vol. II Assessmentsand Scientific Basis for Management Options, Wildland Resources Center Rep.No. 37, Centers for Water and Wildland Resources, Univ. of California, Davis,1071 1099.

FAO [2004], FAOSTAT Forestry Data, 2002. Data available on the Internetat http://faostat.fao.org/faostat/collections?subset=forestry. Accessed onMay 10, 2004.

C. Fiedler, C. Keegan, C. Woodall, T. Morgan, S. Robertson and J. Chmelik[2001], A Strategic Assessment of Fire Hazard in Montana, Report submitted tothe Joint Fire Science Program. http://jfsp.nifc.gov/documents/NMreport.pdf.Accessed on November 21, 2004.

J.S. Fried, J. Barbour and R. Fight [2003], FIA BioSum: Applying a Multi-ScaleEvaluation Tool in Southwest Oregon, J. Forest. 101, 8.

R.J. Harrod, B.H. McRae and W.E. Hartl [1999], Historical Stand Reconstruc-tion in Ponderosa Pine Forests to Guide Silvicultural Prescriptions, Forest Ecol.Manage. 114 (2-3), 433 446.

B.R. Hartsough, X. Zhang and R.D. Fight [2001], Harvesting Cost Model forSmall Trees in Natural Stands in the Interior Northwest, Forest Prod. J. 51, 54 61.

R.W. Haynes, D.M. Adams, R. Alig, D. Brooks, I. Durbak, J. Howard, P. Ince,D. McKeever, J. Mills, K. Skog and X. Zhou [2001], The 2000 RPA TimberAssessment: An Analysis of the Timber Situation in the United States, 1996 to 2050,http://www.fs.fed.us/pnw/sev/rpa/rpa2000.htm. Accessed on March 1, 2001.

T.P. Holmes [1991], Price and Welfare Effects of Catastrophic Forest Damagefrom Southern Pine Beetle Epidemics, Forest Sci. 37, 500 516.

B. Hartsough, X. Zhang and R. Fight [2001], Harvesting Cost for Small Trees inNatural Stands in the Interior Northwest, Forest Prod. J. 51, 54 61.

TIMBER MARKETS AND FUEL TREATMENTS 43

R.E. Just, D.L. Hueth and A.S. Schmitz [1982], Applied Welfare Economics andPublic Policy, Prentice-Hall, Inc., Englewood Cliffs, NJ, 491 pp.

G.A. Majerus [1980], Econometric Estimation of Demand and Supply Curves forTimber in Montana, 1962 1980, unpublished M.S. Thesis, University of Montana.

D.E. Mercer, J.M. Pye, J.P. Prestemon, D.T. Butry and T.P. Holmes [2000],Economic Effects of Catastrophic Wildfires: Assessing the Effectiveness of Fuel Re-duction Programs for Reducing the Economic Impacts of Catastrophic Forest FireEvents, Final Report, 68 pp. [Topic 8 of the research grant “Ecological and EconomicConsequences of the 1998 Florida Fires,” funded by the Joint Fire Science Program].http://flame.doacs.state.fl.us/joint fire sciences/economic.pdf. AccessedNovember 21, 2004.

B.C. Murray and D.N. Wear [1998], Federal Timber Restrictions and InterregionalArbitrage in U.S. Lumber, Land Econ. 74, 76 91.

V. Nagubadi, I.A. Munn and A. Tahai [2001], Integration of Hardwood StumpageMarkets in the Southcentral United States, J. Forest Econ. 7, 69 98.

D.H. Newman [1987], An Econometric Analysis of the Southern Softwood StumpageMarket: 1950 1980, Forest Sci. 33, 932 945.

A.J. Parker [1984], A Comparison of Structural Properties and CompositionalTrends in Conifer Forests of Yosemite and Glacier National Parks, USA, North-west Sci. 58, 131 141.

D.J. Parsons and S.H. DeBenedetti [1979], Impact of Fire Suppression on aMixed-Conifer Forest, Forest Ecol. Manage. 2, 21 33.

D. Paun and G. Jackson [2000], Potential for Expanding Small-Diameter TimberMarket: Assessing Use of Wood Posts in Highway Applications, USDA Forest Serv.Gen. Tech. Rep. FPL-GTR-120, 28 pp.

J.P. Prestemon and T.P. Holmes [2000], Timber Price Dynamics Following aNatural Catastrophe, Amer. J. Agr. Econ. 82, 145 160.

M. Ravallion [1986], Testing Market Integration, Amer. J. Agr. Econ. 68, 102 109.

Regional Forester [1984], Montana Timber Demand and Supply: A Short-RunModel of the Timber Market and an Assessment of the Economy, Employmentand Fuel Wood Use, unpublished report to the Montana State Forester from theNorthern Region, USDA Forest Serv., Missoula, MT.

B. Rummer, J.P. Prestemon, D. May, P. Miles, J.S. Vissage, R.E. McRoberts,G. Liknes, W.D. Shepperd, D. Ferguson, W. Elliot, S. Miller, S.E. Reutebuch, J.Barbour, J. Fried, B. Stokes, E. Bilek, K. Skog and B. Hartsough [2003], A StrategicAssessment of Forest Biomass and Fuel Reduction Treatments in Western States,http://www.fs.fed.us/research/pdf/Western final.pdf. Accessed on November21, 2004.

P. Samuelson [1952], Spatial Price Equilibrium and Linear Programming, Amer.Econ. Rev. 42, 283 303.

C.N. Skinner and C. Chang [1996], Fire Regimes, Past and Present, in SierraNevada Ecosystem Project: Final Report to Congress, Vol. II Assessments andScientific Basis for Management Options, Wildland Resources Center Rep. No. 37,Centers for Water and Wildland Resources, Univ. of California, Davis, 1041 1069.

W.B. Smith, J.S. Vissage, D.R. Darr and R.M. Sheffield [2001], Forest Resourcesof the United States, 1997. USDA Forest Serv. Gen. Tech. Rep. NC-219, 190 pp.

44 K.L. ABT AND J.P. PRESTEMON

H. Spelter and M. Alderman [2003], Profile 2003: Softwood Sawmills in the UnitedStates and Canada, USDA Forest Serv. Resource Paper FPL-RP-608.

H. Spelter, R. Wang and P. Ince [1996], Economic Feasibility of Products fromInland West Small-Diameter Timber, USDA Forest Serv. Gen. Tech. Rep. FPL-GTR-92, 17 pp.

T. Takayama and G.G. Judge [1964], Equilibrium among Spatially SeparatedMarkets: A Reformulation, Econometrica 32, 510 523.

U.S. General Accounting Office [1999], Western National Forests: A CohesiveStrategy Is Needed to Address Catastrophic Wildfire Threats, GAO/RCED 99-65,60 pp.

D.N. Wear [1989], Structural Change and Factor Demand in Montana’s SolidWood Products Industries, Canad. J. Forest. Research 19, 645 650.

D.N. Wear and K.J. Lee [1993], US Policy and Canadian Lumber : Effects of the1986 Memorandum of Understanding, Forest Sci. 39, 799 815.