TILA-RESPA Integrated Disclosure Guide to the Loan Estimate and Closing Disclosure forms Nuts &...

25

TILA-RESPA Integrated Disclosure Guide to the Loan Estimate and Closing Disclosure forms Nuts & Bolts Fayetteville Regional Association of REALTORS® June 23, 2015

-

Upload

kerry-fitzgerald -

Category

Documents

-

view

217 -

download

1

Transcript of TILA-RESPA Integrated Disclosure Guide to the Loan Estimate and Closing Disclosure forms Nuts &...

TILA-RESPA Integrated Disclosure

Guide to the Loan Estimate and Closing Disclosure forms

Nuts & Bolts

Fayetteville Regional Association of REALTORS®June 23, 2015

Disclaimer There is no express or implied warranty respecting the information presented and assumes no responsibility for errors or omissions. The presentation is for informational purposes only and is not and may not be construed as legal advice. You should consult with an attorney prior to embarking upon any specific course of action.

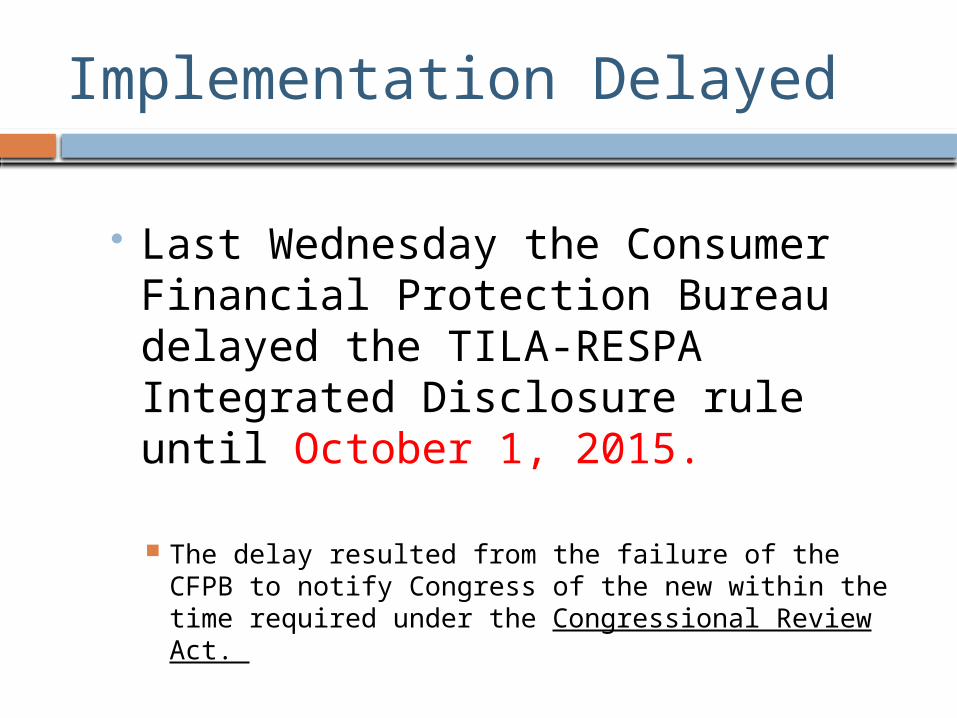

Implementation Delayed

Last Wednesday the Consumer Financial Protection Bureau delayed the TILA-RESPA Integrated Disclosure rule until October 1, 2015.

The delay resulted from the failure of the CFPB to notify Congress of the new within the time required under the Congressional Review Act.

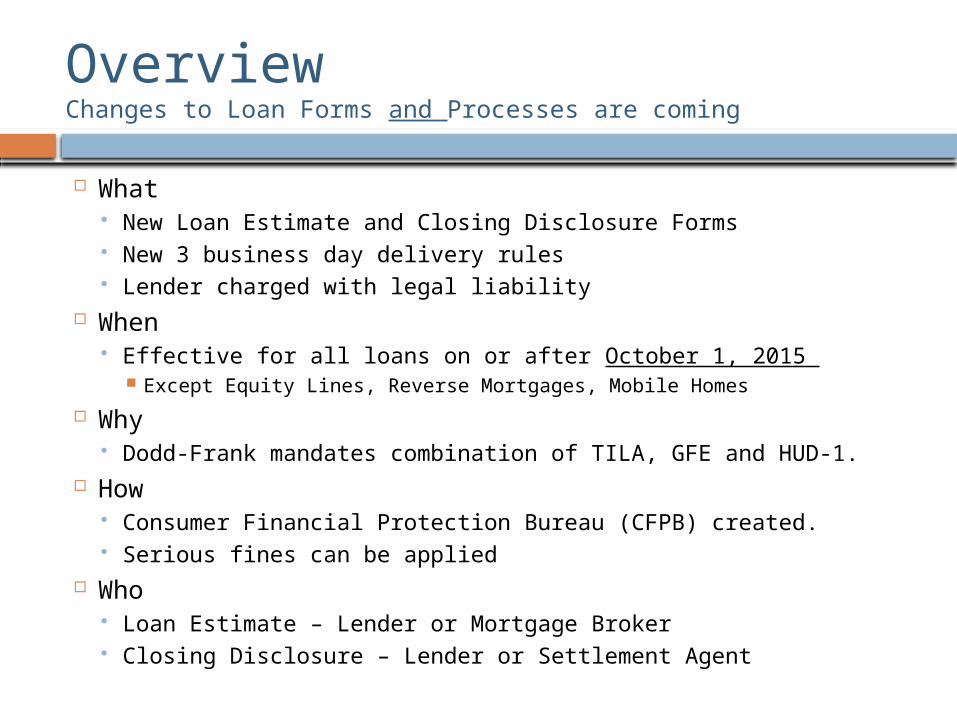

OverviewChanges to Loan Forms and Processes are coming

What New Loan Estimate and Closing Disclosure Forms New 3 business day delivery rules Lender charged with legal liability

When Effective for all loans on or after October 1, 2015

Except Equity Lines, Reverse Mortgages, Mobile Homes

Why Dodd-Frank mandates combination of TILA, GFE and HUD-1.

How Consumer Financial Protection Bureau (CFPB) created. Serious fines can be applied

Who Loan Estimate – Lender or Mortgage Broker Closing Disclosure – Lender or Settlement Agent

OverviewChanges to Loan Forms and Processes are coming

New Lender - Creditor Borrower – Consumer Tolerance – Variance Closing - Consummation

Probable Impacts CFPB erred on side of CONSUMER PROTECTION

versus CONVENIENCE Longer closing cycle Delays in closings – not seen as bad thing by CFPB Disruption Higher costs

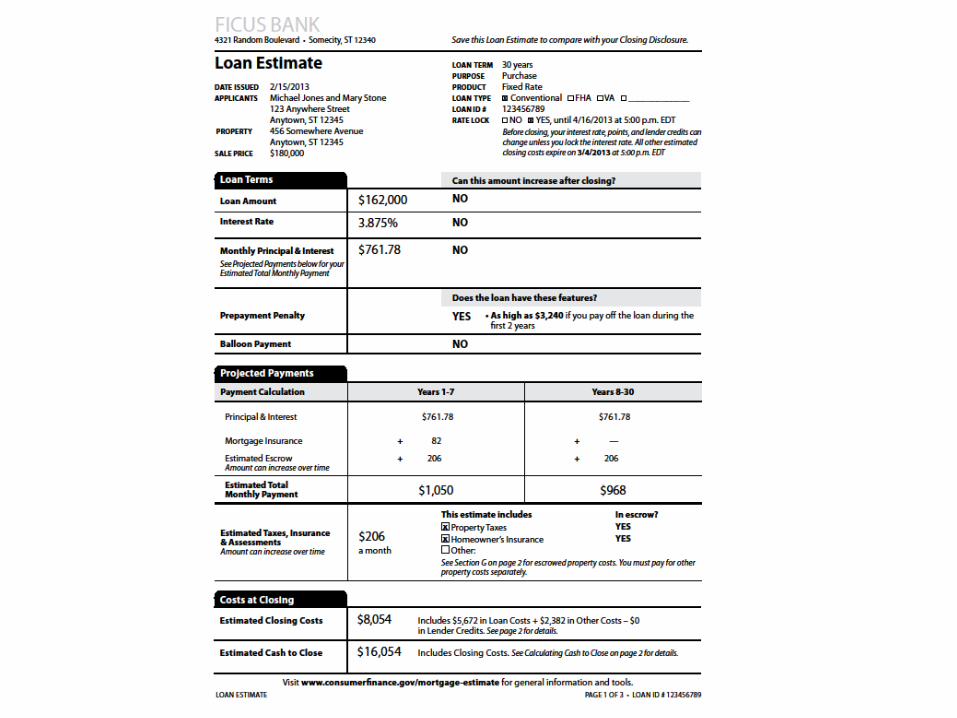

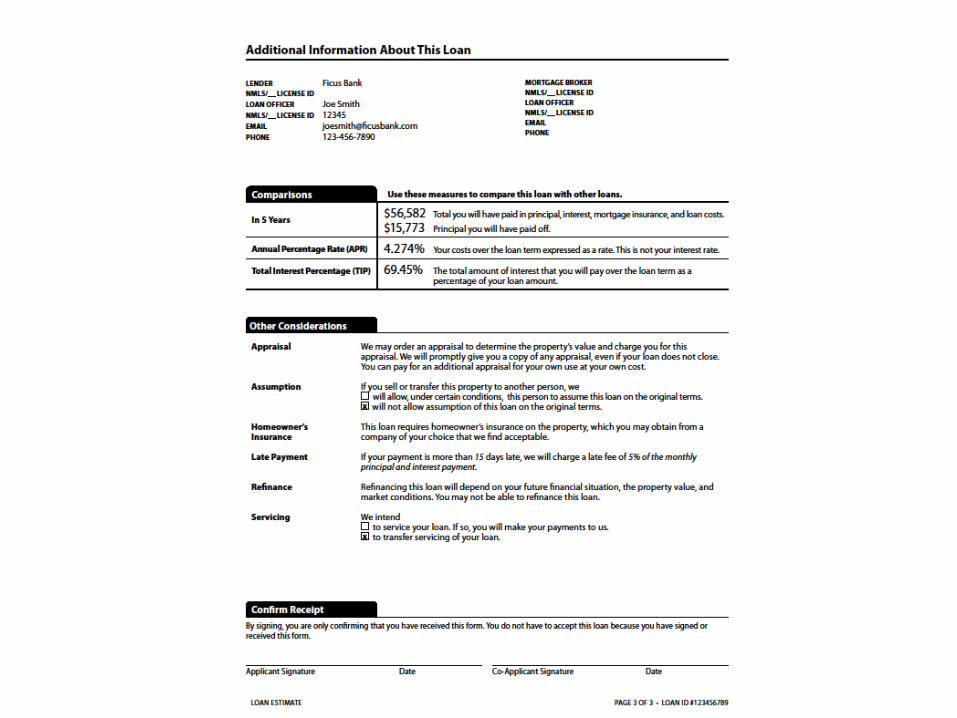

Loan Estimate (LE) Overview

Effective for loans originated on or after October 1, 2015

3-page form combines TILA and GFE Based on unverified information from consumer Have to be provided to consumer within 3

business days after submission Provides summary of key loan terms and

estimates of loan and closing costs Designed to mimic the Closing Disclosure Form. Identifies tolerances

The CFPB essentially has turned the Loan Estimate into an “exact” loan estimate by expanding the categories in which fees can’t change.

Unless an exception applies, charges of the following services cannot increase: The lender’s charges for its own services. Charges for services provided by an affiliate of the lender. Charges for services for services for which the lender does not permit the

consumer to shop.

Charges for other services can increase, but generally not by more than 10 percent.

(Charges for services recommended by the lender that were in the 10 percent bucket are now in the zero-variation bucket.)

Variances – the new Tolerances

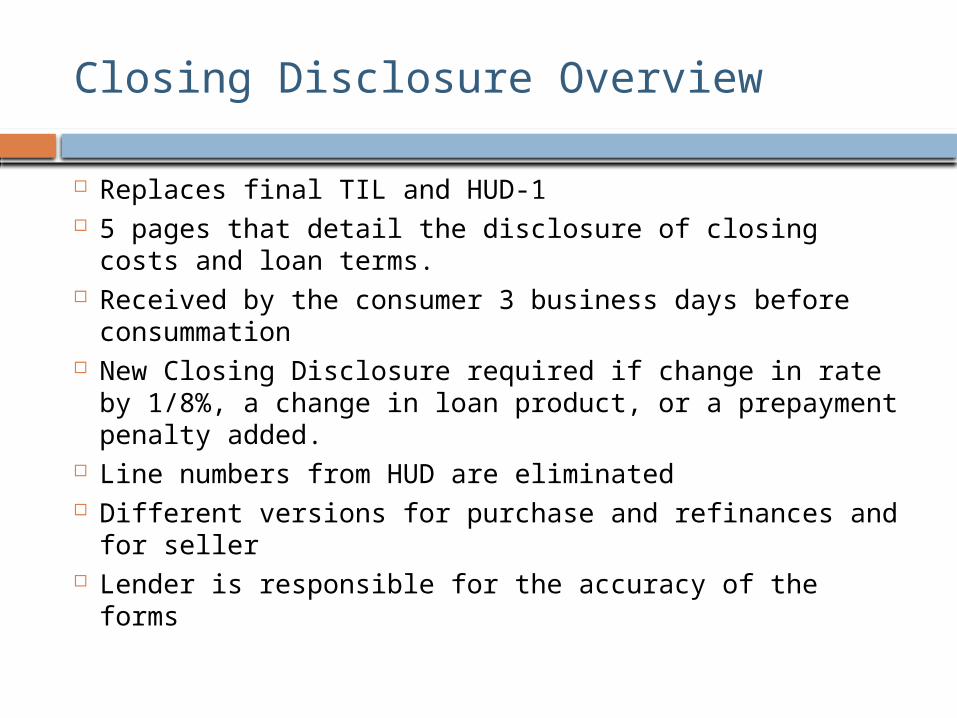

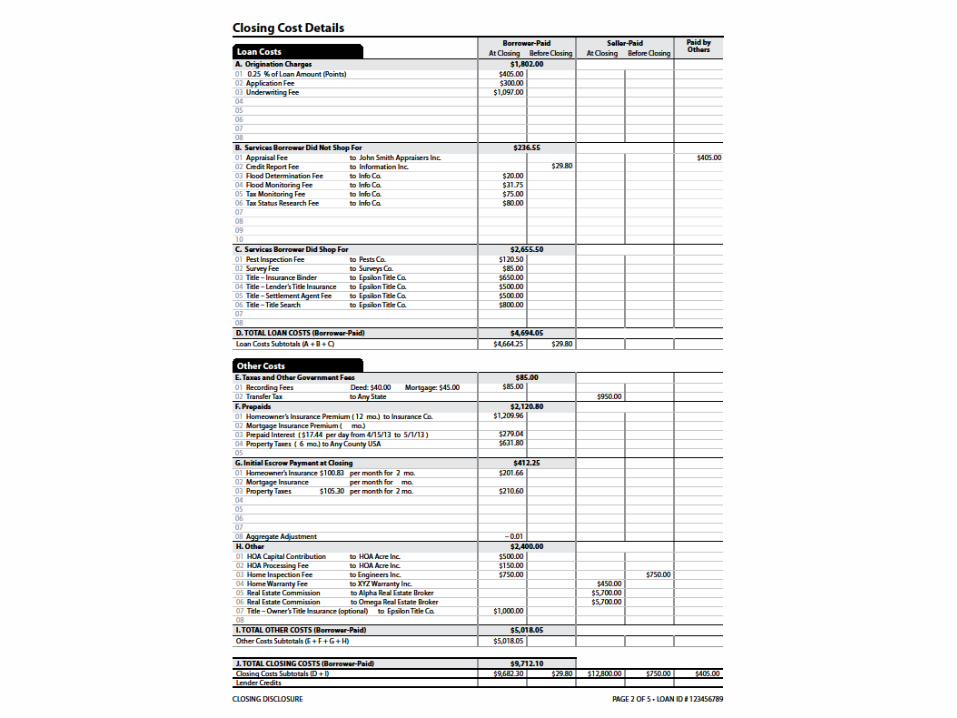

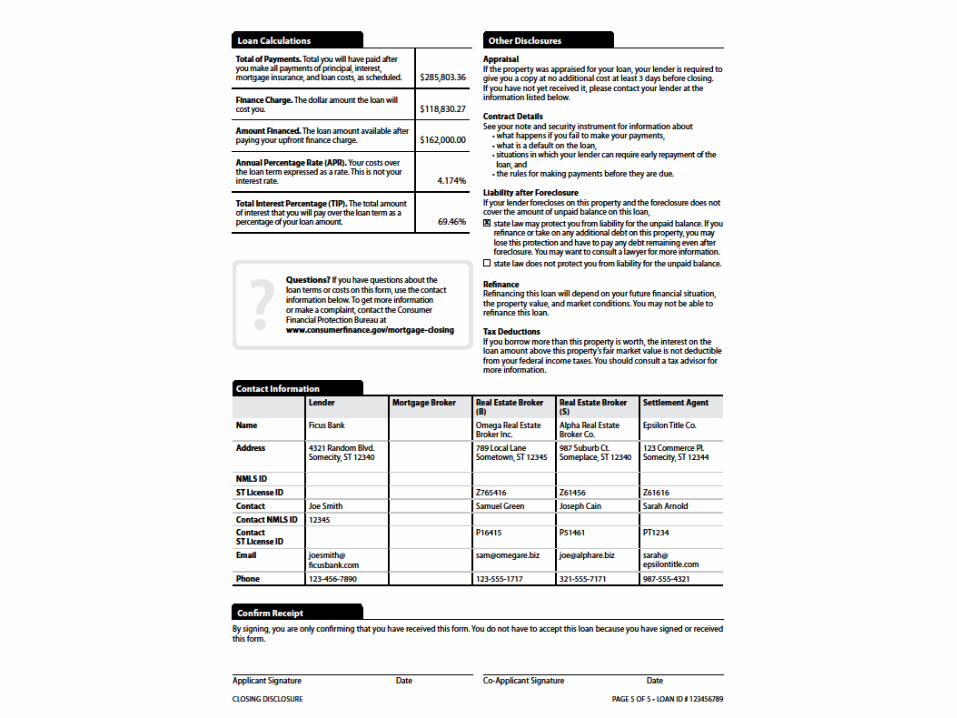

Closing Disclosure Overview

Replaces final TIL and HUD-1 5 pages that detail the disclosure of closing costs and

loan terms. Received by the consumer 3 business days before

consummation New Closing Disclosure required if change in rate by

1/8%, a change in loan product, or a prepayment penalty added.

Line numbers from HUD are eliminated Different versions for purchase and refinances and for

seller Lender is responsible for the accuracy of the forms

Three-Day Closing Disclosure Rule

Disclosure forms must be received by consumer three business days before consummation. The three-day period is measured by days, not hours.

Thus, disclosures must be delivered three days before closing, and not 72 hours prior to closing. If a federal holiday falls in the three-day period, add a day for disclosure delivery.

Delivery Options In person: A disclosure is deemed received by the consumer the day it is

delivered in person. Mail/Fed-Ex/courier: A lender or settlement agent can presume the

consumer received the disclosure three business days after mailing. Can be rebutted by evidence the consumer received earlier.

E-Mail: Same presumption as postal mail. Mail Box Rule – Safe Harbor

ALTA Settlement Statement

New Closing Disclosure from does not meet state requirements that accurate costs for seller and homebuyer are shown. Requires settlement providers to inaccurately disclose

the costs of title insurance to the consumer. To bring standardization to the industry, ALTA

developed model Settlement Statements for title insurance and settlement companies to use.

Four versions include combined, buyer/borrower, seller, and cash)

Document is signed by borrower at closing

What Are Lenders Doing?

National lenders dealing with CFPB for years. Wells, BOA and Chase have announced that they

will be responsible for the forms and the delivery. Proposed Process Flow

Engage the settlement agent 10 days prior to closing. Generate and send Closing Disclosure six business days

prior to scheduled closing. Require that all changes to the loan and fee data be

submitted through Closing Insight prior to signing. Closing Insight/ Simplifile portals Regional and local lenders will develop their own

procedures

What Should Realtors Be Doing Now?

Recognize that the Closing Disclosure will fundamentally change the closing process and ultimately impact their clients.

Learn as much as you can about the new rules and prepare for the changes in the transaction process well ahead of time.

Meet with lenders you trust to learn more about the new rules. Develop a process for Realtor to receive a copy of the Closing

Disclosure Forms. (Lenders will only send to borrower.) Make sure your closing partners are vetted and verified for Best

Practices by your lenders and meet with them to discuss the new disclosures and their preparations for the new regulatory environment.

Learn the lingo – CFPB, consummation, NPI, Best Practices, etc. You will need to change your scheduling calendar to

accommodate the additional days needed between delivery of documents, receipt of documents and closing date.

What Should Realtors Be Doing Now?

Educate the sellers on the importance of following contract terms – leave the appliances, etc.

You will need to get the borrower paid invoices to the settlement agent well in advance of the three day delivery requirement.

Consider policy of having two “walk-through” inspections – one several weeks early and then one at the end.

Consider policy restricting “back to back” closings. Consider policy on addressing “informal closings” in the parking lot

where buyer and seller agree to resolve small issues away from closing table for fear of closing delay.

Consider changes in Purchase Contract to: Protect the Seller in the event the Buyer’s lender delays the closing. Ensure that the Buyer understands and is protected with Owners

Title Insurance. Extend the contract expiration dates back to at least 60 days.

Proceed with changing current processes to accommodate new dates. Begin training now.

Questions?

David Allred

Cunningham & Company Mortgage Bankers

868-4300

Tony Chavonne

Single Source Real Estate Services

222-4444