Tight oil and shale gas – global implications€¦ · Global supply growth and shale gas Bcf/d...

33

Tight oil and shale gas – global implications Washington, March 2013 Christof Rühl, Chief Economist, BP © BP 2012

Transcript of Tight oil and shale gas – global implications€¦ · Global supply growth and shale gas Bcf/d...

Tight oil and shale gas –global implicationsWashington, March 2013Christof Rühl, Chief Economist, BP

© BP 2012

Tight oil and shale gas: global implications

Global energy trendsGlobal energy trends

- Characteristics

- Implications

© BP 2013Energy Outlook 2030

Population, income and energy growth

128 100

BillionPopulation GDP

Trillion $2011 PPP Billion toePrimary energy

9

12 OECDnon-OECD

6

8 OECDNon-OECD

75

100 OECDNon-OECD

64 50

0

3

0

2

0

25

© BP 2013

01990 2010 2030

01990 2010 2030

01990 2010 2030

Energy Outlook 2030

Industrialisation drives energy growth

Billion toe

18 18

By primary use By fuelBy regionBillion toe Billion toe

18

12

15

18

12

15

18

P 12

15

18

HydroNuclear

Renew.*

Non-OECD6

9

12

Non-OECD

6

9

12 Power generation Coal

GIndustry 6

9

12Coal

Gas

OECD

0

3

6

OECD

0

3

6

OtherTransport Oil

GasIndustry

0

3

6

Oil

Gas

© BP 2013Energy Outlook 2030

01990 2010 2030

01990 2010 2030 1990 2010 2030

*Includes biofuels

Fuel shares and energy pricesShares of world primary energy

50%

Energy prices$2011/boe

40%

50% Oil

Coal80

100

120 Oil - BrentGas - basketCoal - basket

20%

30%

Gas 40

60

80

0%

10% HydroNuclear Renewables* 0

20

40

© BP 2013Energy Outlook 2030

0%1965 1980 1995 2010 2025

*Includes biofuels1965 1980 1995 2010

Energy efficiency improvements

0 5

Energy intensity by regionToe per thousand $2011 GDP (PPP)

20050

Energy and GDPBillion toe Trillion $2011 (PPP)

0.4

0.5

China

US

150

200

40

50

0.2

0.3100

20

30

GDP (RHS)

0.0

0.1 WorldEU*

0

50

0

10Energy

© BP 2013Energy Outlook 2030

1870 1890 1910 1930 1950 1970 1990 2010 2030 1970 1990 2010 2030*Euro4 (France, Italy, Germany, UK) pre-1970

Energy supply growth

17

Demand SupplyBillion toe

16

17

NuclearHydro

Renew.*2030 level

14

15

Other

12

13

2011 OECD Non 2011 Oil Natural Coal Non

TightOther

Shale

© BP 2013

2011 OECD Non-OECD

2011 Oil Natural gas

Coal Non-fossil

Energy Outlook 2030

*Includes biofuels

Tight oil and shale gas: global implications

Global energy trendsGlobal energy trends

- Characteristics

- Implications

© BP 2013Energy Outlook 2030

Tight oil and shale gas: resources and production

60Billion toe

Current resources Production in 2030

0 9Billion toe

40

60 GasOil

0.6

0.9

0

20

0.0

0.3

0

sia

Pac

ific

. Am

eric

a

S. &

C.

Am

eric

a

Afri

ca

Eur

ope

&

Eur

asia

ddle

Eas

t 0.0

sia

Pac

ific

. Am

eric

a

S. &

C.

Am

eric

a

Afri

ca

Eur

ope

&

Eur

asia

ddle

Eas

t

© BP 2013

As N Mi

Energy Outlook 2030

As N Mi

Resources data © OECD/IEA 2012

US tight oil and shale gas: infrastructure requirements

Onshore oil & gas rigs 2011Thousands

Oil wells drilled and output

515

Mb/d

2 0

Thousands

4

5

12

15 2012* 20112010 Output (RHS)1.5

2.0

2

3

6

9

0.5

1.0

0

1

0

30.0

© BP 2013

Bakken Canada Colombia

Energy Outlook 2030

*Annualised from 1Q-3Q data

Global supply growth and tight oil

10%10

Liquids supply by type

45%105

Mb/dTight oil output

% of totalMb/d

8%

10%

8

10 ChinaRussiaS. AmericaN America

45%

75

90

105OPEC NGLs

OPEC crude

OPEC share (RHS)% of total

(RHS)

4%

6%

4

6N. America

45

60 Biofuels

Oil sands

0%

2%

0

2

30%0

15

30 Tight oil

Other non-OPECNGLs

© BP 2013

%2000 2010 2020 2030

%1990 2000 2010 2020 2030

Energy Outlook 2030

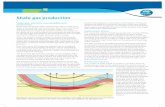

Global supply growth and shale gas

Bcf/dGas production by type and region Shale gas production

Bcf/d

400

500 Non-OECD otherNon-OECD shaleOECD shaleOECD th 12%

18%

60

80 RoWChinaEurope & EurasiaC d & M i

200

300 OECD other

6%

12%

40

Canada & MexicoUS

0

100

0%

6%

0

20 % of total (RHS)

© BP 2013Energy Outlook 2030

1990 2000 2010 2020 20300%0

1990 2000 2010 2020 2030

Tight oil and shale gas: global implications

Global energy trendsGlobal energy trends

- Characteristics

- Implications

© BP 2013Energy Outlook 2030

Unconventional oil and the call on OPEC

369

Mb/d

Call on OPEC & spare capacityMb/d

Unconventionals share of net global supply growth

100%

33

36

6

9 Spare capacityCall on OPEC (RHS)

75%

100% Biofuels

Oil sands

30

33

3

6

50%

Tight oil

27

30

0

3

0%

25%

© BP 2013

2000 2010 2020 20300%

2000-10 2010-20 2020-30

Energy Outlook 2030

Gas trade and market integration

20%80

Bcf/dLNG exports LNG diversification

10

15%

20%

60

80

% f t t l

8

10 Suppliers per importerCustomers per exporter

10%40

% of total consumption

(RHS)4

6

0%

5%

0

20LNG

0

2

© BP 2013Energy Outlook 2030

0%01990 2000 2010 2020 2030 1991 1996 2001 2006 2011

Tight oil and shale gas uncertaintiesShare of global supply growthRange of tight oil forecasts

(excludes NGLs)Mb/d Bcf/d

Range of shale gas forecasts

8

10 RangeBP

50%

75% Shale gasTight oil

80

100

120 RangeBP

4

6

25%

50%

40

60

80

0

2

0%

25%

0

20

40

© BP 2013

02010 2020 2030

Energy Outlook 2030

0%2000-10 2010-20 2020-30

02010 2020 2030

Oil and gas: reserves and production

EuropeN. America

FSU

Middle East

Asia Pacific

50%% share of global totalKey:

S. & C. America Africa

Asia Pacific

0%

2011 reserves2030 output

Africa

Net importers 2011

© BP 2013Energy Outlook 2030

Net exporters 2011Net importers 2011

Energy imbalances: import profiles

60

Energy imbalances to GDP ratioEnergy imbalancesChina EU US

300

Mtoe Toe per $Mln GDP PPP

20

40

60 ChinaUSEU

0

300

-20

0-600

-300

OilG

-80

-60

-40

-1,200

-900

90 10 30 90 10 30 90 10 30GasCoal

© BP 2013

1990 2000 2010 2020 2030

Energy Outlook 2030

199

20 203

199

20 203

199

20 203

Energy imbalances: export profilesEnergy imbalances to GDP ratioEnergy imbalances

Saudi Arabia Africa RussiaMtoe Toe per $Mln GDP PPP

1000

1200Saudi Arabia

Russia600

800OilGas

400

600

800 Africa400

Coal

0

200

400

0

200

0 0 0 0 0 0 0 0 0

© BP 2013

01990 2000 2010 2020 2030

Energy Outlook 2030

199

201

203

199

201

203

199

201

203

Energy and carbon emissionsCO2 emissions and primary energy

Billion tonnes CO2

Growth of CO2 emissions % p.a.Billion toe

15

18

40

50 Emissions from energy use

Primary energy (RHS)

6%

8%1970-1990

1990-2010

2010 2030

Gas6

9

12

20

30 (RHS)

2%

4%2010-2030

Oil

Gas

0

3

6

0

10

2%

0%

© BP 2013Energy Outlook 2030

001970 1990 2010 2030

-2%China EU US

Conclusion

4%% p.a. Economic growth needs

energy

3%Income

per

gy

Competition and innovation are the key to meeting this

1%

2%

Popul

capita need

− energy efficiency

0%

Population

Economic Efficiency New supply

− new supplies

Wide ranging implications

© BP 2013

growthy

gainspp y

Energy Outlook 2030

January 2013

Energy: prices demand growth

2000

Energy and GDPBillion toe Trillion $2011

Energy prices$2011/boe

150

200

40

50

80

100

120 Oil - BrentGas - basketCoal - basket

10020

30

GDP (RHS)40

60

80

0

50

0

10

Energy0

20

40

© BP 201323

1970 1990 2010 20301965 1980 1995 2010

The power sector leads primary energy growthGrowth by sector and fuel,

2011-2030Growth by sector and region,

2011-2030Billion toe Billion toe

2

3 HydroNuclearRenew.

2

3RoW

Middl E t

0

1 ElectricityGasBiofuels0

1Middle East

China & India

-1

Tran

spor

t

Indu

stry

Oth

er

Pow

er OilCoal-1

Tran

spor

t

Indu

stry

Oth

er

Pow

er

d aOECD

© BP 2013

Final energy use Inputs to powerFinal energy use Inputs to power

Energy Outlook 2030

Emerging economies dominate energy production

18FSU

Billion toe18

Billion toe

12

15FSU

S&C America

N. America12

15

6

9 Middle East

EuropeNon-OECD6

9

Non-OECD

0

3 Asia Pacific

AfricaOECD

0

3OECD

© BP 2013

01990 2000 2010 2020 2030

Energy Outlook 2030

01990 2000 2010 2020 2030

Energy: prices demand growth

2000

Energy and GDPBillion toe Trillion $2011

Energy prices$2011/boe

150

200

40

50

80

100

120 Oil - BrentGas - basketCoal - basket

10020

30

GDP (RHS)40

60

80

0

50

0

10

Energy0

20

40

© BP 201326

1970 1990 2010 20301965 1980 1995 2010

Shale gas: regional growth

120

Bcf/d ChinaBcf/d N. America Bcf/d EU

Sources of gas supply, by region

80

100

120 Net pipeline importsNet LNG importsShale gas production80

100

120

80

100

120

40

60Other domestic production

40

60

40

60

-20

0

20

-20

0

20

-20

0

20

© BP 2013Energy Outlook 2030

201990 2010 2030

Energy Outlook 2030

201990 2010 2030

201990 2010 2030

Global gas balance

500

Bcf/dDemand Supply

450

500

Other non-OECD

2030 levelOECD

350

400

Other OECDMiddle East

Chinanon OECD

Non-OECD

OECD

250

300N. America

Other OECD

© BP 2013Energy Outlook 2030

2011 OECD Non-OECD 2011 Non-shale Shale

Energy Outlook 2030

Coal consumption

O

Coal demand by regionBillion toe

5

Billion toeCoal demand by sector

5 Oil

IndustryChina China Chi

4

5

China China4

5

Industry

Other

y

India India

China

India

China

India2

3China

India

China

India2

3y

Power

OECD

India

OECD

Other Non-OECD

OECD0

1OECD

Other non-OECD

OECD0

1Power

© BP 2013Energy Outlook 2030

1990 2000 2010 2020 203001990 2000 2010 2020 2030

Non-fossil fuels

2 0

Billion toeOECD

2 0

Non-OECDBillion toe

1.5

2.0RenewablesBiofuelsHydro

1.5

2.0

1.0

HydroNuclear

Renewables in power

1.0

0.0

0.5Renewables in power

Biofuels0.0

0.5

© BP 2013

0.01990 2000 2010 2020 2030

0.01990 2000 2010 2020 2030

Energy Outlook 2030

Growth of renewables in powerRenewable power

% p.a.% share

Share of power generationGrowth 2011-30, and share of power

15%

20%Nuclear

1970-2000 12%

15%

20%

25% Growth (RHS)Share 2011Share 2030

Non-OECD5%

10%

R bl

6%

9%

10%

15%

OECD0%

5%

2000 2010 2020 2030

Renewables2000-2030

0%

3%

0%

5%

OECD Other Non OECD

© BP 2013

2000 2010 2020 20301970 1980 1990 2000

OECD Europe

Other OECD

Non-OECD

Energy Outlook 2030

Power generation and electricity useElectricity share of final consumption

50%

Shares of power output

100%

40%

50%

Other 80%

100%

NuclearOil

20%

30%Industry

40%

60% HydroGas

0%

10%Transport

0%

20%

Renew.

Coal

© BP 2013Energy Outlook 2030

0%1990 2010 2030 1970 1990 2010 2030

High oil prices are reducing oil’s share of primary energy

100%

Oil share in sector

12

Fuel economy of new carsLitres per 100 km

75%

100%

PowerOther

8

10

12 EUUS light vehiclesChina

50%IndustryTransport

4

6

8

0%

25%

0

2

4

© BP 2013

1965 1978 1991 2004 2017 2030

Energy Outlook 2030

01995 2005 2015 2025