Tianjin Plastics FIN 570 Irvine1

22

Tianjin Plastics Brian Hider Brian Kopan Ernest Lew Juan Villa A case study in international project finance. October 8, 2008 Cal State Fullerton, MBA Program 人人人

Transcript of Tianjin Plastics FIN 570 Irvine1

Tianjin Plastics

Brian Hider

Brian Kopan

Ernest Lew

Juan Villa

A case study in international project finance.

October 8, 2008

Cal State Fullerton, MBA Program

人民币

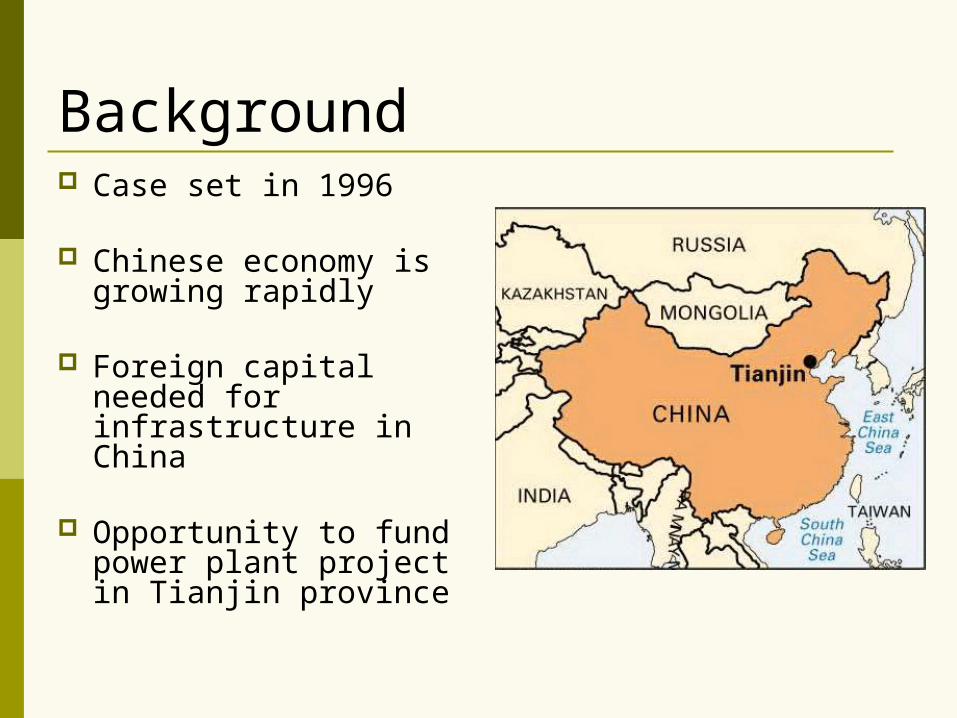

Background Case set in 1996

Chinese economy is growing rapidly

Foreign capital needed for infrastructure in China

Opportunity to fund power plant project in Tianjin province

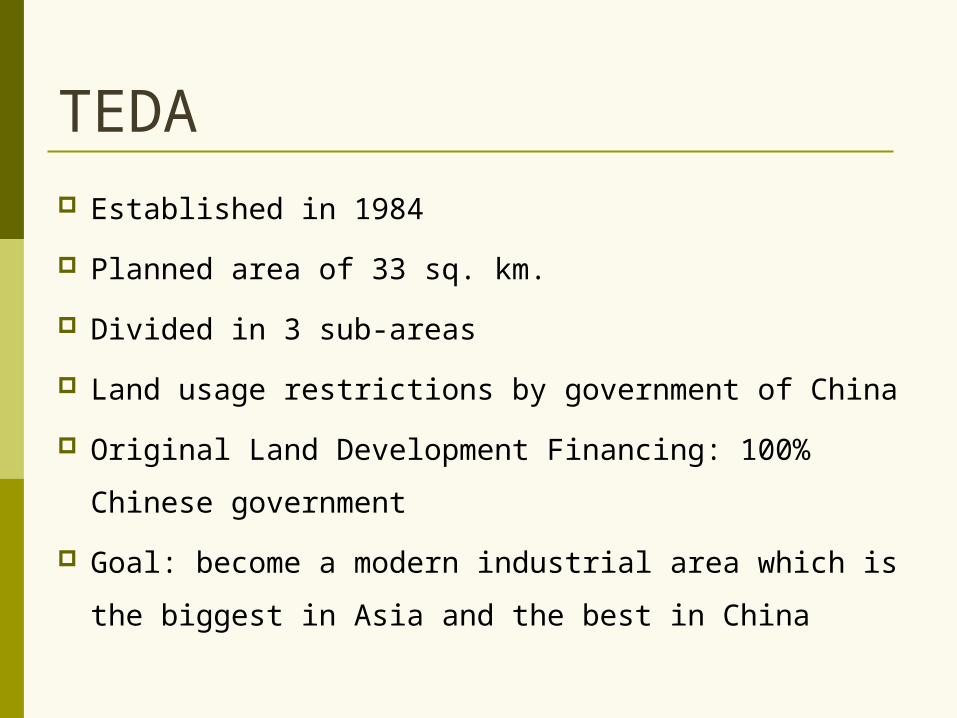

TEDA Established in 1984

Planned area of 33 sq. km.

Divided in 3 sub-areas

Land usage restrictions by government of China

Original Land Development Financing: 100%

Chinese government

Goal: become a modern industrial area which is the

biggest in Asia and the best in China

TEDA In 1992, TEDA FDI increased-needed for

development

New Land Development Financing: combination

of China’s government & MNCs.

Wholly foreign-owned companies and joint

ventures were created to develop of land

MNC’s investment in the area has lead to strong

economic growth in the TEDA region.

Project Structure: The Players Maple Energy (49% Equity)

US Based company, since 1989 Subsidiary of Northern States Utility Power plant projects in four countries Specialize in turnkey projects

Tianjin Plastics (46% Equity) Government run factory Specialty is energy intensive extrusion process

MOPI (5% Equity) Chinese Ministry of Power Industry

Wintel Had Rmb that could not be repatriated

Project Structure: Fundamentals Project life-4 year construction, 20 year operation

Operating costs fixed, paid in Rmb

20yr contract for free coal feedstock

Selling price of energy guaranteed (Rmb)

Profits virtually guaranteed as long as debt, equity and final

profit are in Rmb

Project financed with 85% debt

Forecast shows China requiring 21GW of additional power

annually for a decade (150 plants of this size)

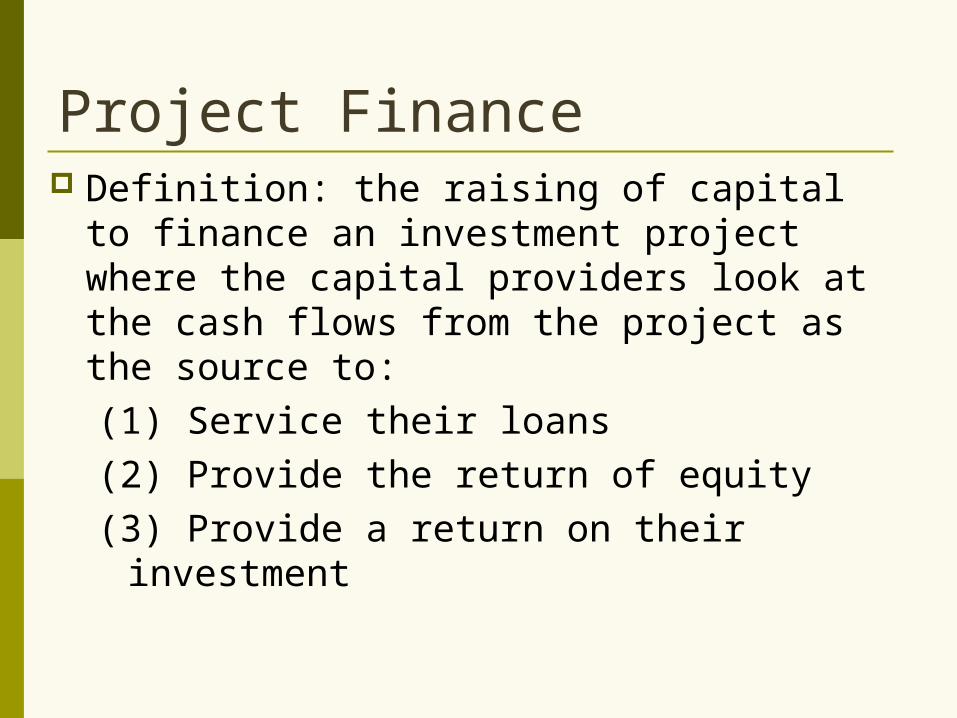

Project Finance Definition: the raising of capital to finance

an investment project where the capital providers look at the cash flows from the project as the source to:(1) Service their loans(2) Provide the return of equity (3) Provide a return on their investment

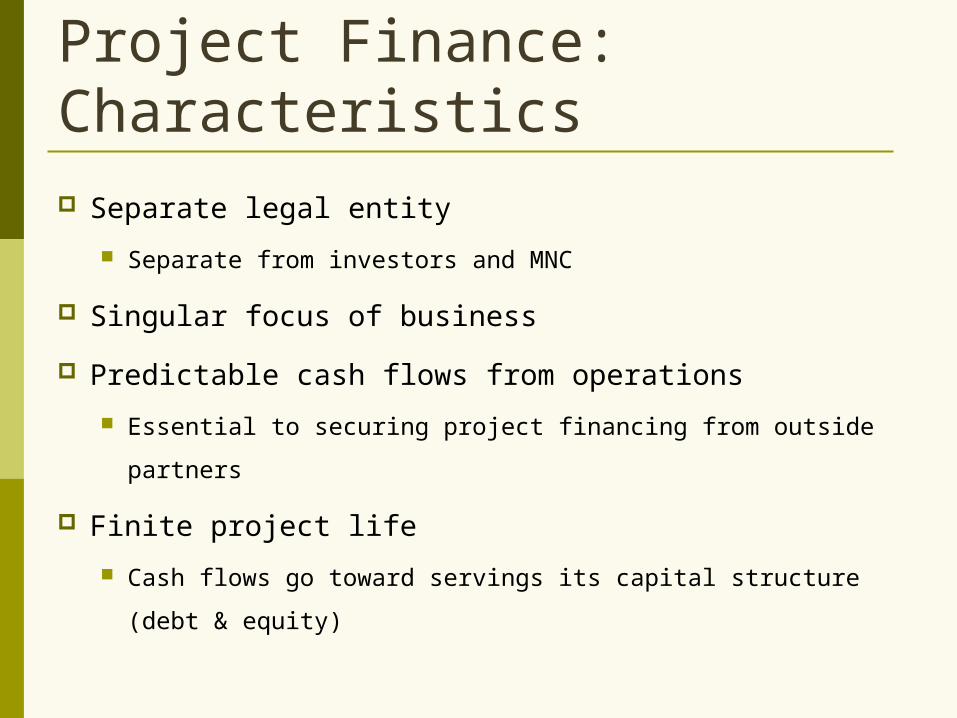

Project Finance: Characteristics Separate legal entity

Separate from investors and MNC

Singular focus of business

Predictable cash flows from operations

Essential to securing project financing from outside partners

Finite project life

Cash flows go toward servings its capital structure (debt &

equity)

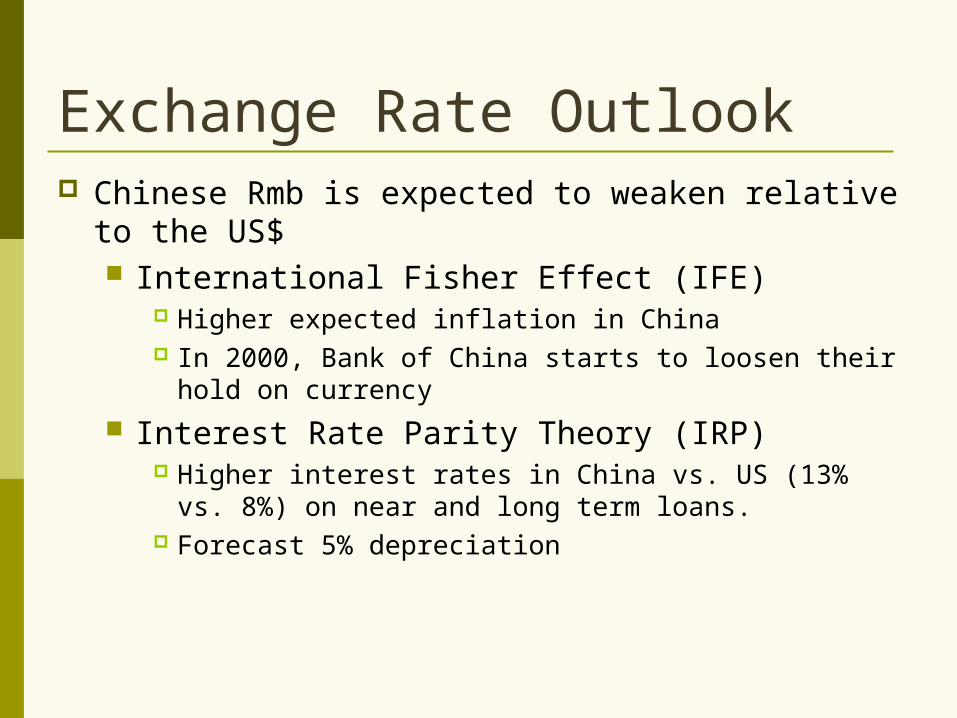

Exchange Rate Outlook Chinese Rmb is expected to weaken relative to

the US$ International Fisher Effect (IFE)

Higher expected inflation in China In 2000, Bank of China starts to loosen their hold on

currency Interest Rate Parity Theory (IRP)

Higher interest rates in China vs. US (13% vs. 8%) on near and long term loans.

Forecast 5% depreciation

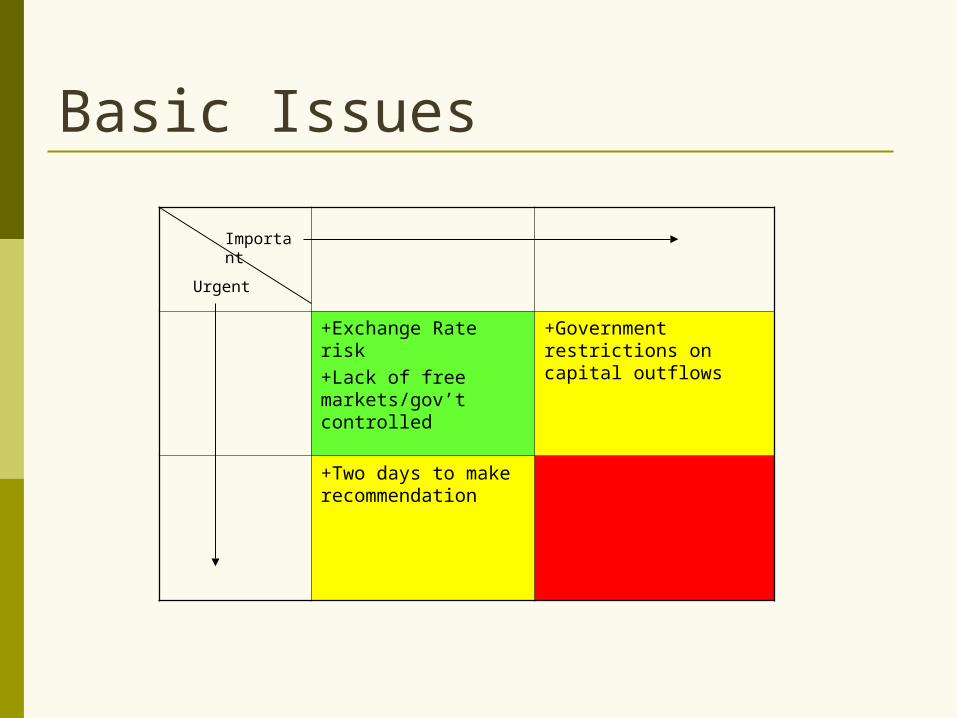

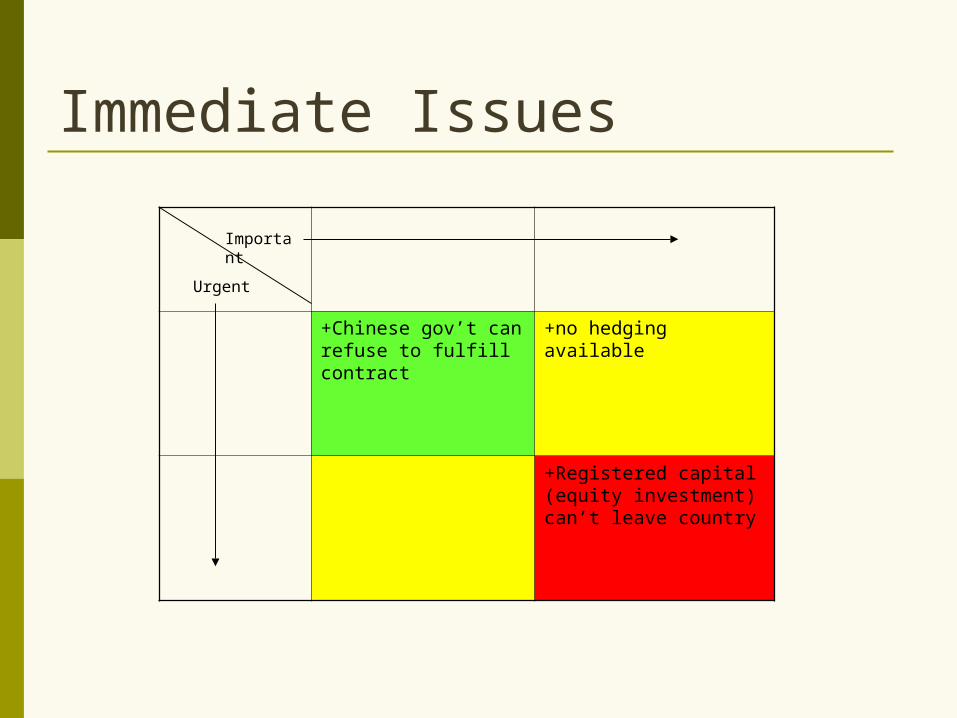

Basic Issues

+Exchange Rate risk+Lack of free markets/gov’t controlled

+Government restrictions on capital outflows

+Two days to make recommendation

Important

Urgent

Immediate Issues

+Chinese gov’t can refuse to fulfill contract

+no hedging available

+Registered capital (equity investment) can’t leave country

Important

Urgent

Cause/Effect

Unpredictability of project

profitability

Political instability Equity repatriation constraints

Lack of hedging options and forecast data

Partially convertible Rmb

Lack of EX/IM financing help

Decision Criteria Quantitative:

Highest likely NPV Sensitivity to currency exposure Must have positive NPV

Shortest payback period

Qualitative Overall company growth strategy in TEDA

NPV and Payback Period Model

1996 2020

+Operating Margin-Interest Expense-Taxes=Net Income+75% of Depr-Principal Pmt=Project Cash Flow

17% ROI Project Restriction

Maple (49%) CF in Rmb

Maple/Wintel Rmb Loan Net CF

Bal Available to Repatriate

+ Repatriated $'s

+ Maple/Wintel $ Loan Net CF

= Maple $ Cash Flow

NPV @ 18% Disc

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

3% Projected GrowthConstruction Phase

Option 1 Maple Energy invests directly with US$

Maple leaves US$ in project and can’t pull them out = lose equity investment.

Debt obligations are in US$ and will be exposed to exchange rate risk.

Currency Exposures: Firm Profitability

Dollar based debt (almost 90% of debt) Profit Magnitude

Profits converted to dollars

Const. Loan + Syndicate Loans NPVRenminbi Depreciation Rate -10% -5% 0% 5%Probability 20% 70% 5% 5%1996 NPV 3.3 7.4 13.5 23.1Weighted NPV 0.7 5.2 0.7 1.2 7.7Payback Period 5 5 5 5Weighted Payback Period 1 4 0 0 5

Option 2Back-to-Back loans

Maple Energy does US$/Rmb loan with another US firm doing business in China, Wintel

Currency Exposures: Firm Profitability

Dollar based debt (almost 90% of debt) Profit Magnitude

Profits converted to dollars

Back to Back Loan NPVRenminbi Depreciation Rate -10% -5% 0% 5%Probability 20% 70% 5% 5%1996 NPV 4.1 7.5 12.8 21.2Weighted NPV 0.8 5.2 0.6 1.1 7.8Payback Period 4 4 4 4Weighted Payback Period 1 3 0 0 4

Option 2 (continued)Back-to-Back loans

Mechanics: Wintel has generated profits in Rmb (can’t repatriate

earnings) Wintel loans Rmb70.018 to Maple for 6 years Maple loans $8.415 to Wintel for 6 years Maple: instead of converting their US$ and making

the equity investment IN China, Maple BORROWS the Rmb from Wintel for the equity investment

Maple pays loan with Rmb from cash flows Wintel pays loan with US$

Option 3Have power price paid by Tianjin Plastics indexed to dollar

Tianjin has already contracted to purchase most of the power from the plant.

This guarantees earnings would maintain their US$ value.

Not allowed by MOPI due to concerns over negative impact it might have on their Rmb invested in project.

Currency Exposures: Profit Magnitude

Profits converted to dollars

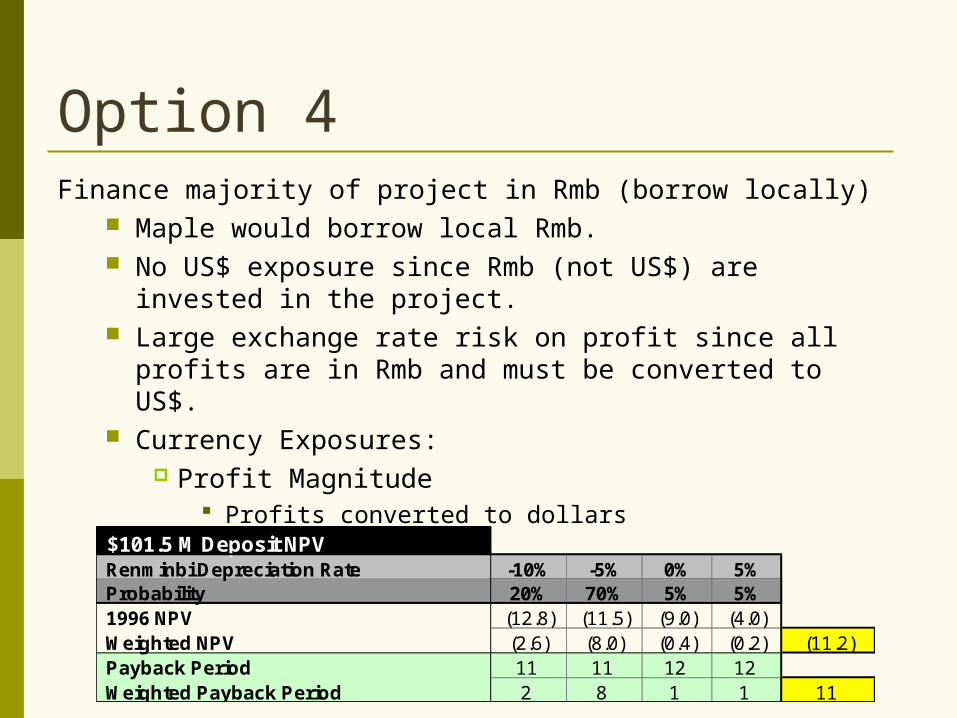

Option 4Finance majority of project in Rmb (borrow locally)

Maple would borrow local Rmb. No US$ exposure since Rmb (not US$) are invested in

the project. Large exchange rate risk on profit since all profits are in

Rmb and must be converted to US$. Currency Exposures:

Profit Magnitude Profits converted to dollars

$101.5 M Deposit NPVRenminbi Depreciation Rate -10% -5% 0% 5%Probability 20% 70% 5% 5%1996 NPV (12.8) (11.5) (9.0) (4.0)Weighted NPV (2.6) (8.0) (0.4) (0.2) (11.2)Payback Period 11 11 12 12Weighted Payback Period 2 8 1 1 11

Selected Option Option 2: Back-to-Back loans

Maple Energy

(China)

Maple Energy

(USA)

Wintel

(USA)

Wintel-China

(China)

Loan of Rmb 70.018m

Loan of US $8.415m

Selected Option1996 NPV & Payback PeriodRenminbi Depreciation Rate -10% -5% 0% 5%

Const. Loan then Syndicate Loans NPV 3.3 7.4 13.5 23.1 Payback Period 5 5 5 5

Back to Back Loan NPV 4.1 7.5 12.8 21.2 Payback Period 4 4 4 4

$101.5 M Deposit NPV (12.8) (11.5) (9.0) (4.0) Payback Period 11 11 12 12

Probability 20% 70% 5% 5%Expected

NPV

Const. Loan then Syndicate Loans NPV 0.7 5.2 0.7 1.2 7.7 Payback Period 1 4 0 0 5

Back to Back Loan NPV 0.8 5.2 0.6 1.1 7.8 Payback Period 1 3 0 0 4

$101.5 M Deposit NPV (2.6) (8.0) (0.4) (0.2) (11.2) Payback Period 2 8 1 1 11

Questions?