Thought leadership Oilfield services in Asia Emergence of a new business model

24

Oilfield services in Asia: Emergence of a new business model

-

Upload

jaishankar-krishnamurthy -

Category

Documents

-

view

691 -

download

0

Transcript of Thought leadership Oilfield services in Asia Emergence of a new business model

Oilfield services in Asia: Emergence of a new business model

1. Introduction

2. Asia: Growing demand, but some uncertainty around production

3. Outlook for oilfield services (OFS) in Asia

4. Spotlight on China: Opportunities in conventional and unconventional resources

5. Spotlight on Indonesia: CBM now, shale later

6. Spotlight on Malaysia: Boosting domestic output

7. Spotlight on Singapore: A financial hub for OFS companies in Southeast Asia

8. Growing influence of regional OFS: Emergence of a new business model

Contents

1

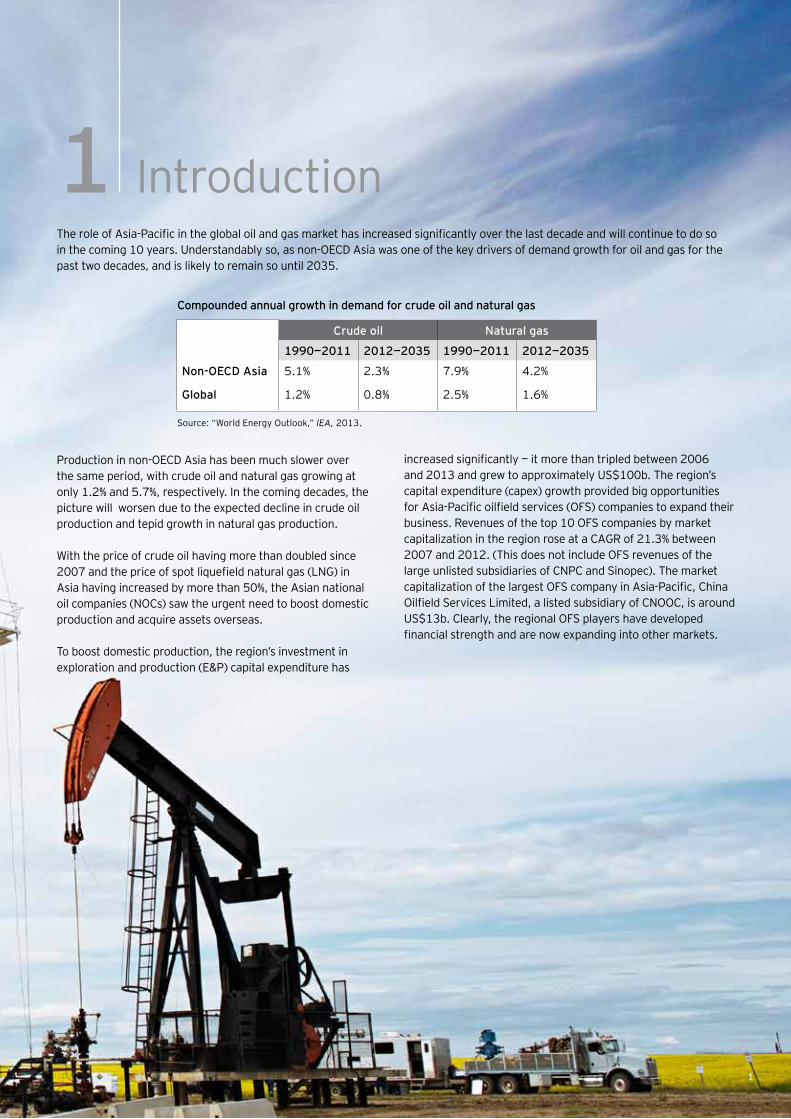

The role of Asia-Pacific in the global oil and gas market has increased significantly over the last decade and will continue to do so in the coming 10 years. Understandably so, as non-OECD Asia was one of the key drivers of demand growth for oil and gas for the past two decades, and is likely to remain so until 2035.

Production in non-OECD Asia has been much slower over the same period, with crude oil and natural gas growing at only 1.2% and 5.7%, respectively. In the coming decades, the picture will worsen due to the expected decline in crude oil production and tepid growth in natural gas production.

With the price of crude oil having more than doubled since 2007 and the price of spot liquefield natural gas (LNG) in Asia having increased by more than 50%, the Asian national oil companies (NOCs) saw the urgent need to boost domestic production and acquire assets overseas.

To boost domestic production, the region’s investment in exploration and production (E&P) capital expenditure has

Crude oil Natural gas

1990—2011 2012—2035 1990—2011 2012—2035

Non-OECD Asia

Global

5.1%

1.2%

2.3%

0.8%

7.9%

2.5%

4.2%

1.6%

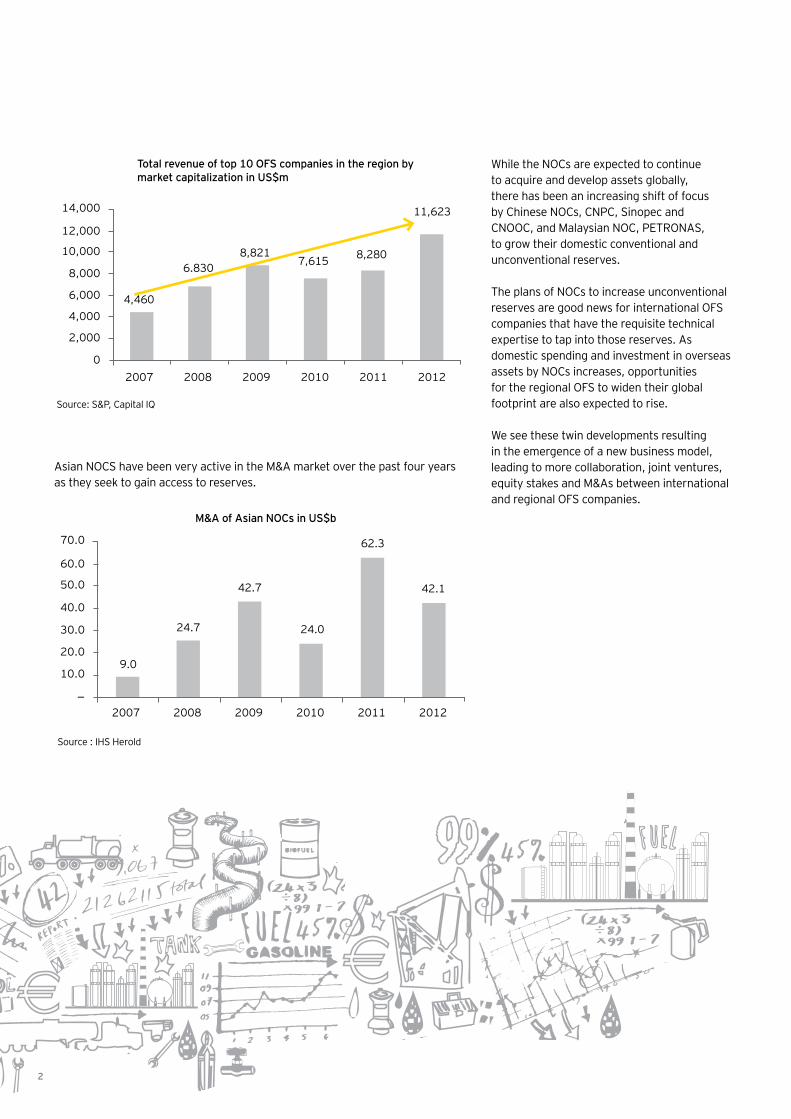

increased significantly — it more than tripled between 2006 and 2013 and grew to approximately US$100b. The region’s capital expenditure (capex) growth provided big opportunities for Asia-Pacific oilfield services (OFS) companies to expand their business. Revenues of the top 10 OFS companies by market capitalization in the region rose at a CAGR of 21.3% between 2007 and 2012. (This does not include OFS revenues of the large unlisted subsidiaries of CNPC and Sinopec). The market capitalization of the largest OFS company in Asia-Pacific, China Oilfield Services Limited, a listed subsidiary of CNOOC, is around US$13b. Clearly, the regional OFS players have developed financial strength and are now expanding into other markets.

Source: “World Energy Outlook,” IEA, 2013.

Compounded annual growth in demand for crude oil and natural gas

1 Introduction

1

2

Total revenue of top 10 OFS companies in the region by market capitalization in US$m

Asian NOCS have been very active in the M&A market over the past four years as they seek to gain access to reserves.

Source : IHS Herold

Source: S&P, Capital IQ

While the NOCs are expected to continue to acquire and develop assets globally, there has been an increasing shift of focus by Chinese NOCs, CNPC, Sinopec and CNOOC, and Malaysian NOC, PETRONAS, to grow their domestic conventional and unconventional reserves.

The plans of NOCs to increase unconventional reserves are good news for international OFS companies that have the requisite technical expertise to tap into those reserves. As domestic spending and investment in overseas assets by NOCs increases, opportunities for the regional OFS to widen their global footprint are also expected to rise.

We see these twin developments resulting in the emergence of a new business model, leading to more collaboration, joint ventures, equity stakes and M&As between international and regional OFS companies.

14,000

12,000

10,000

8,000

6,000

4,000

2,000

2007

4,460

6.8308,821

7,615 8,280

11,623

2008 2009 2010 2011 20120

M&A of Asian NOCs in US$b

70.0

60.0

50.0

40.0

30.0

20.0

10.0

2007

9.0

24.7

42.7

24.0

62.3

42.1

2008 2009 2010 2011 2012—

3

Non-OECD Asia will hold the largest share of global energy demand growth at 65% between 2012 and 2035. China will be the main driver of increasing energy demand in the current decade, but India will take over as the principal source of growth in the 2020s1.

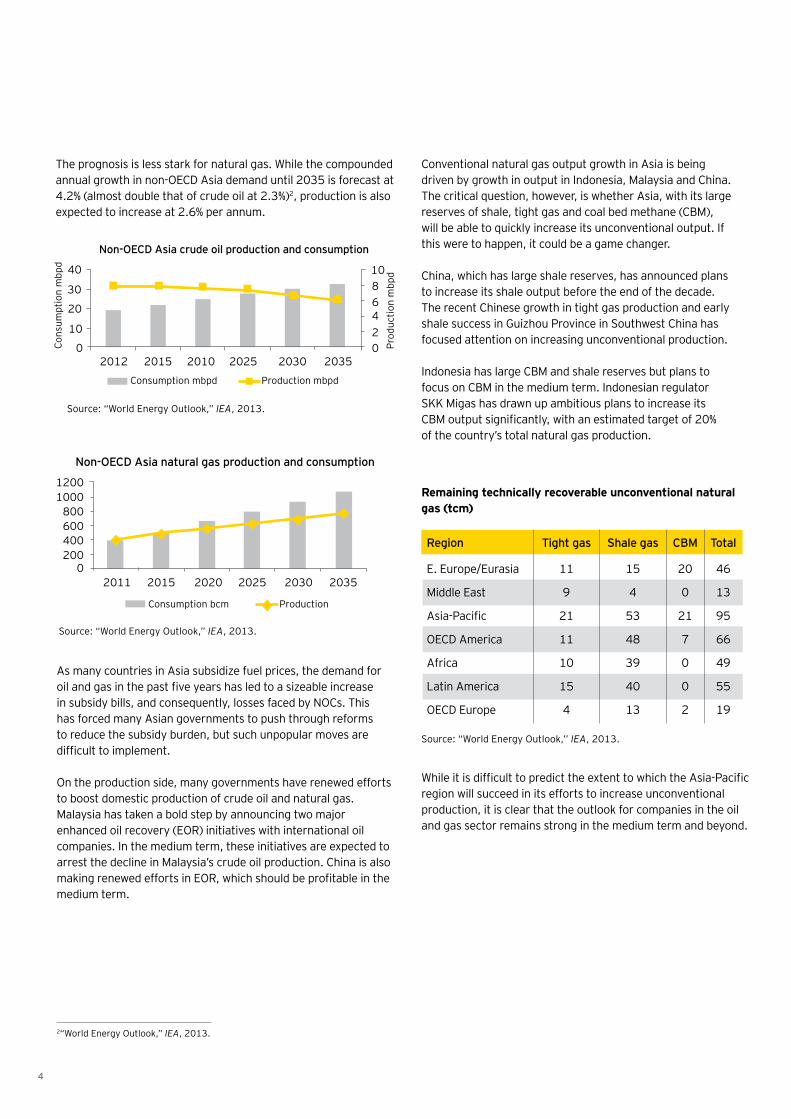

Crude oil demand of non-OECD Asia by 2035 will be almost equal to that of the entire OECD. Forecasts indicate that demand from the former will continue to increase, whereas demand from the latter is likely to experience negative growth during the same period. This represents a major shift as energy–hungry Asia (excluding Japan and Australia) will consume 31% of the global crude output. At the same time, Asian production is forecast to come down by 13% by 2025, driven largely by two factors — lack of major crude oil discoveries in Asia during the last 10 years and depletion of existing fields. The twin effect of increased consumption and decreased production will lead to a substantial increase in imports into Asia, which is already a significant net importer of crude oil.

1“World Energy Outlook,” IEA, 2013.

2 Asia: Growing demand, but some uncertainty around production

3

4

The prognosis is less stark for natural gas. While the compounded annual growth in non-OECD Asia demand until 2035 is forecast at 4.2% (almost double that of crude oil at 2.3%)2, production is also expected to increase at 2.6% per annum.

Source: “World Energy Outlook,’’ IEA, 2013.

Source: “World Energy Outlook,” IEA, 2013.

2“World Energy Outlook,” IEA, 2013.

As many countries in Asia subsidize fuel prices, the demand for oil and gas in the past five years has led to a sizeable increase in subsidy bills, and consequently, losses faced by NOCs. This has forced many Asian governments to push through reforms to reduce the subsidy burden, but such unpopular moves are difficult to implement.

On the production side, many governments have renewed efforts to boost domestic production of crude oil and natural gas. Malaysia has taken a bold step by announcing two major enhanced oil recovery (EOR) initiatives with international oil companies. In the medium term, these initiatives are expected to arrest the decline in Malaysia’s crude oil production. China is also making renewed efforts in EOR, which should be profitable in the medium term.

Conventional natural gas output growth in Asia is being driven by growth in output in Indonesia, Malaysia and China. The critical question, however, is whether Asia, with its large reserves of shale, tight gas and coal bed methane (CBM), will be able to quickly increase its unconventional output. If this were to happen, it could be a game changer.

China, which has large shale reserves, has announced plans to increase its shale output before the end of the decade. The recent Chinese growth in tight gas production and early shale success in Guizhou Province in Southwest China has focused attention on increasing unconventional production.

Indonesia has large CBM and shale reserves but plans to focus on CBM in the medium term. Indonesian regulator SKK Migas has drawn up ambitious plans to increase its CBM output significantly, with an estimated target of 20% of the country’s total natural gas production.

While it is difficult to predict the extent to which the Asia-Pacific region will succeed in its efforts to increase unconventional production, it is clear that the outlook for companies in the oil and gas sector remains strong in the medium term and beyond.

Region Tight gas Shale gas CBM Total

E. Europe/Eurasia

Middle East

Asia-Pacific

OECD America

Africa

Latin America

OECD Europe

11

9

21

11

10

15

4

15

4

53

48

39

40

13

20

0

21

7

0

0

2

46

13

95

66

49

55

19

Remaining technically recoverable unconventional natural gas (tcm)

Source: “World Energy Outlook,” IEA, 2013.

Non-OECD Asia crude oil production and consumption

40

30

20

10

02012 2015 2010 2025 2030 2035

1086420

Consumption mbpd Production mbpd

Cons

umpt

ion

mbp

d

Prod

uctio

n m

bpd

Non-OECD Asia natural gas production and consumption

12001000

800600400200

02011 2015 2020 2025 2030 2035

Consumption bcm Production

55

3 Outlook for OFS in Asia

6

3 “Asset report Natuna D Alpha,” Wood Mackenzie, 1 May 2013.

E&P spending is forecast to remain robust in Asia. According to IHS Herold, Asia will record high growth in E&P spending during 2012 to 2017. This is positive news for both international and domestic OFS companies in the region.

Once again, Malaysia is leading the way by launching an ambitious capex program to boost the country’s oil and natural gas output. PETRONAS has announced that the group, along with its partners, will incur capex of MYR300b (US$91.4b) on various initiatives to boost domestic output of crude and natural gas. According to Standard Chartered, spending on oilfield services in China will increase by 85% between 2012 and 2020. Furthermore, Indonesia has announced several large-scale plans that will result in increasing the country’s gas output by 50% by 2020. This does not include the development of the East Natuna project (Natuna D Alpha), with estimated reserves of 46 tcf, forecast to commence production in 20253. The estimated investment in Natuna, in which Exxon, Pertamina, Total and PTT are partners, is expected to cost in excess of US$40b.

A significant proportion of the increase in Asian E&P spending will be on deepwater and unconventional resources. This augurs well for international OFS companies that have the requisite

expertise to tap these resources. With several deepwater projects already in planning or implementation stages in Malaysia and Indonesia, Asia’s production from deepwater resources is set to increase.

A new development to be aware of is the planned offshore projects in Myanmar. While estimated reserves held by the country vary significantly, the Asian Development Bank estimates 3P reserves to be 14 bboe. Therefore, several international majors have targeted Myanmar as a highly prospective region for future exploration, development and production. The results of the recent licensing round are likely to be announced by the second quarter of 2014. Myanmar Oil & Gas Enterprise (MOGE), the country’s oil and gas regulator, has projected a jump in the natural gas output from 13.1 bcm per year in 2012 to 24 bcm per year by 2020.

Spending on unconventional resources will receive a boost as China and Indonesia plan to increase output of shale gas, tight gas and CBM. According to Wood Mackenzie, China has ramped up spending in shale with Sinopec planning to drill 30 wells in 2014. Several IOCs are also planning to spud about a dozen wells during 2014 in order to appraise their acreage.

77

4 Spotlight on China

8

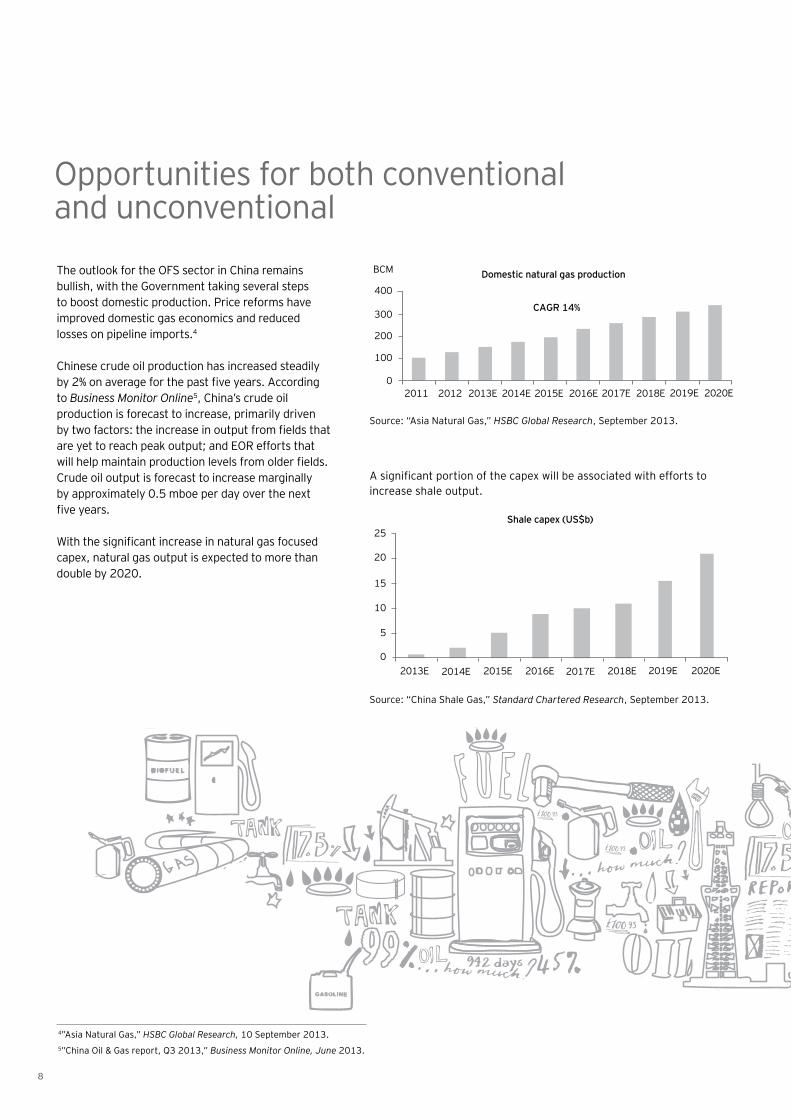

The outlook for the OFS sector in China remains bullish, with the Government taking several steps to boost domestic production. Price reforms have improved domestic gas economics and reduced losses on pipeline imports.4

Chinese crude oil production has increased steadily by 2% on average for the past five years. According to Business Monitor Online5, China’s crude oil production is forecast to increase, primarily driven by two factors: the increase in output from fields that are yet to reach peak output; and EOR efforts that will help maintain production levels from older fields. Crude oil output is forecast to increase marginally by approximately 0.5 mboe per day over the next five years.

With the significant increase in natural gas focused capex, natural gas output is expected to more than double by 2020.

A significant portion of the capex will be associated with efforts to increase shale output.

4”Asia Natural Gas,” HSBC Global Research, 10 September 2013.5”China Oil & Gas report, Q3 2013,” Business Monitor Online, June 2013.

Opportunities for both conventional and unconventional

Source: “Asia Natural Gas,” HSBC Global Research, September 2013.

2020E

Domestic natural gas production

CAGR 14%

BCM

400

300

200

100

02011 2012 2013E 2014E 2015E 2016E 2017E 2018E 2019E

Source: “China Shale Gas,” Standard Chartered Research, September 2013.

Shale capex (US$b)25

20

15

10

5

02013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

9

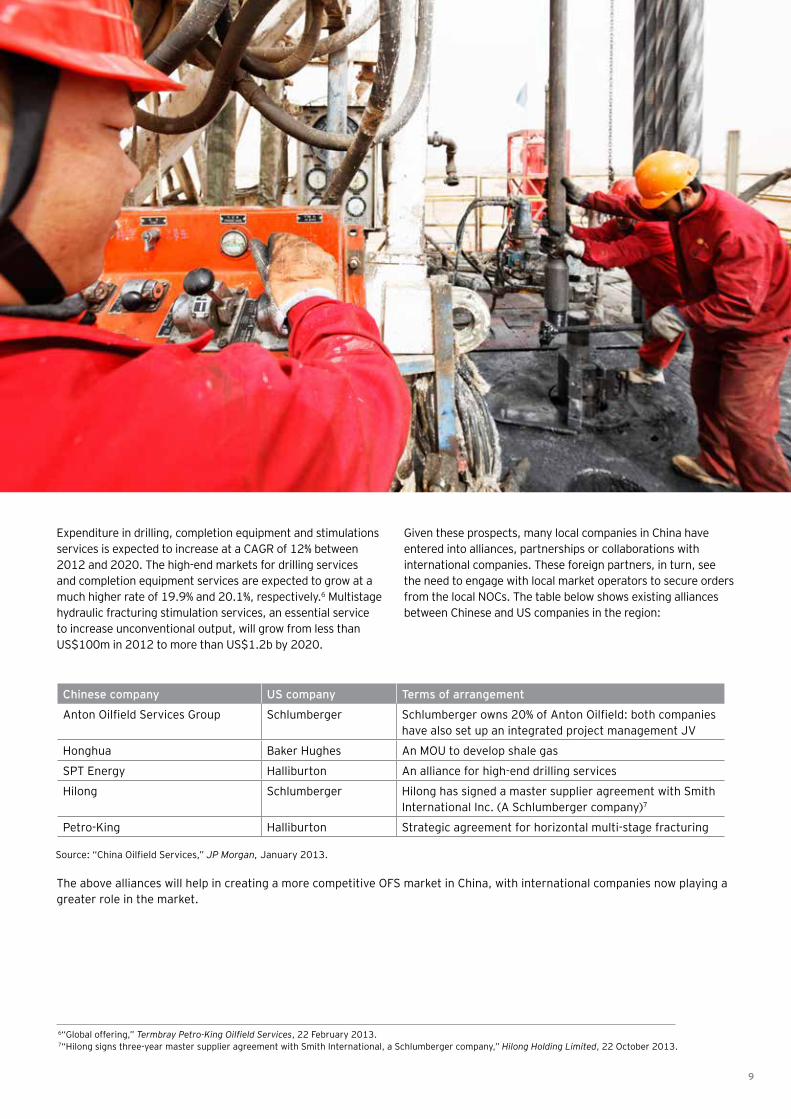

Expenditure in drilling, completion equipment and stimulations services is expected to increase at a CAGR of 12% between 2012 and 2020. The high-end markets for drilling services and completion equipment services are expected to grow at a much higher rate of 19.9% and 20.1%, respectively.6 Multistage hydraulic fracturing stimulation services, an essential service to increase unconventional output, will grow from less than US$100m in 2012 to more than US$1.2b by 2020.

6“Global offering,” Termbray Petro-King Oilfield Services, 22 February 2013.7“Hilong signs three-year master supplier agreement with Smith International, a Schlumberger company,” Hilong Holding Limited, 22 October 2013.

Chinese company US company Terms of arrangement

Anton Oilfield Services Group Schlumberger Schlumberger owns 20% of Anton Oilfield: both companies have also set up an integrated project management JV

Honghua Baker Hughes An MOU to develop shale gas

SPT Energy Halliburton An alliance for high-end drilling services

Hilong Schlumberger Hilong has signed a master supplier agreement with Smith International Inc. (A Schlumberger company)7

Petro-King Halliburton Strategic agreement for horizontal multi-stage fracturing

Source: “China Oilfield Services,” JP Morgan, January 2013.

The above alliances will help in creating a more competitive OFS market in China, with international companies now playing a greater role in the market.

Given these prospects, many local companies in China have entered into alliances, partnerships or collaborations with international companies. These foreign partners, in turn, see the need to engage with local market operators to secure orders from the local NOCs. The table below shows existing alliances between Chinese and US companies in the region:

1010

5 Spotlight on Indonesia

11

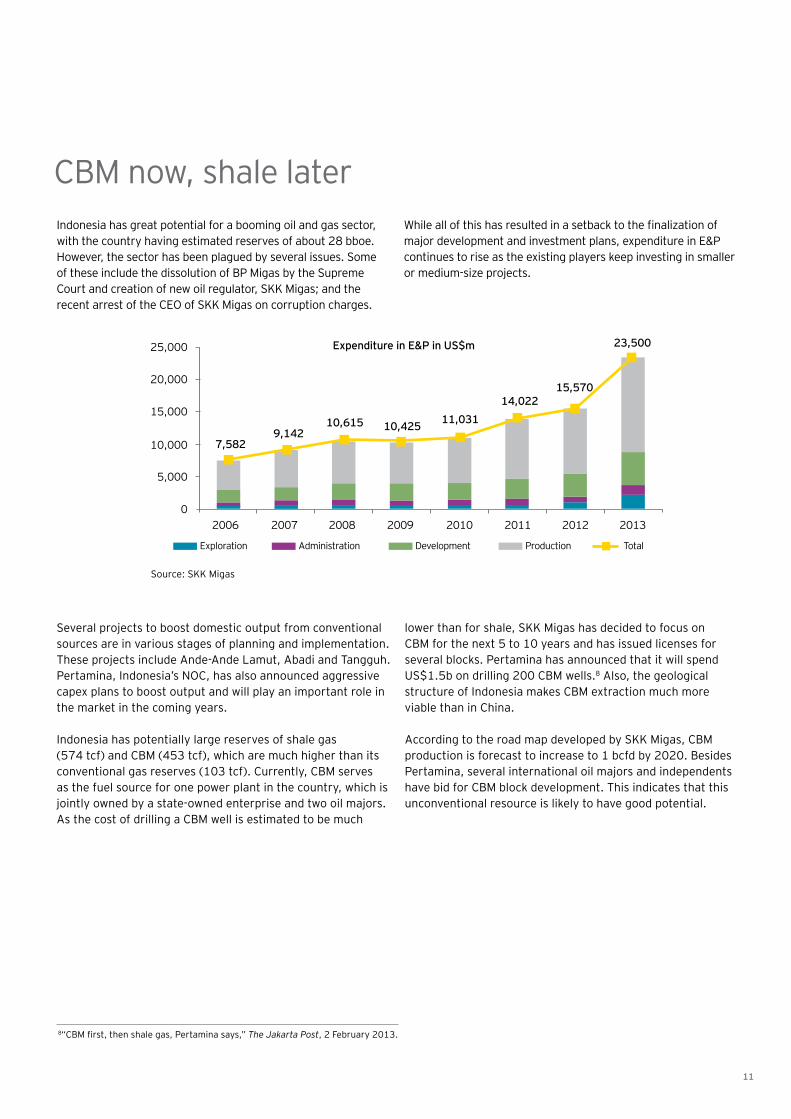

Indonesia has great potential for a booming oil and gas sector, with the country having estimated reserves of about 28 bboe. However, the sector has been plagued by several issues. Some of these include the dissolution of BP Migas by the Supreme Court and creation of new oil regulator, SKK Migas; and the recent arrest of the CEO of SKK Migas on corruption charges.

CBM now, shale later

Source: SKK Migas

Several projects to boost domestic output from conventional sources are in various stages of planning and implementation. These projects include Ande-Ande Lamut, Abadi and Tangguh. Pertamina, Indonesia’s NOC, has also announced aggressive capex plans to boost output and will play an important role in the market in the coming years. Indonesia has potentially large reserves of shale gas (574 tcf) and CBM (453 tcf), which are much higher than its conventional gas reserves (103 tcf). Currently, CBM serves as the fuel source for one power plant in the country, which is jointly owned by a state-owned enterprise and two oil majors. As the cost of drilling a CBM well is estimated to be much

While all of this has resulted in a setback to the finalization of major development and investment plans, expenditure in E&P continues to rise as the existing players keep investing in smaller or medium-size projects.

lower than for shale, SKK Migas has decided to focus on CBM for the next 5 to 10 years and has issued licenses for several blocks. Pertamina has announced that it will spend US$1.5b on drilling 200 CBM wells.8 Also, the geological structure of Indonesia makes CBM extraction much more viable than in China.

According to the road map developed by SKK Migas, CBM production is forecast to increase to 1 bcfd by 2020. Besides Pertamina, several international oil majors and independents have bid for CBM block development. This indicates that this unconventional resource is likely to have good potential.

Expenditure in E&P in US$m

7,5829,142

10,615 10,425 11,03114,022

15,570

23,50025,000

20,000

15,000

10,000

5,000

02006

Exploration Administration Development Production Total

2007 2008 2009 2010 2011 2012 2013

8“CBM first, then shale gas, Pertamina says,” The Jakarta Post, 2 February 2013.

12

6 Spotlight on Malaysia

12

13

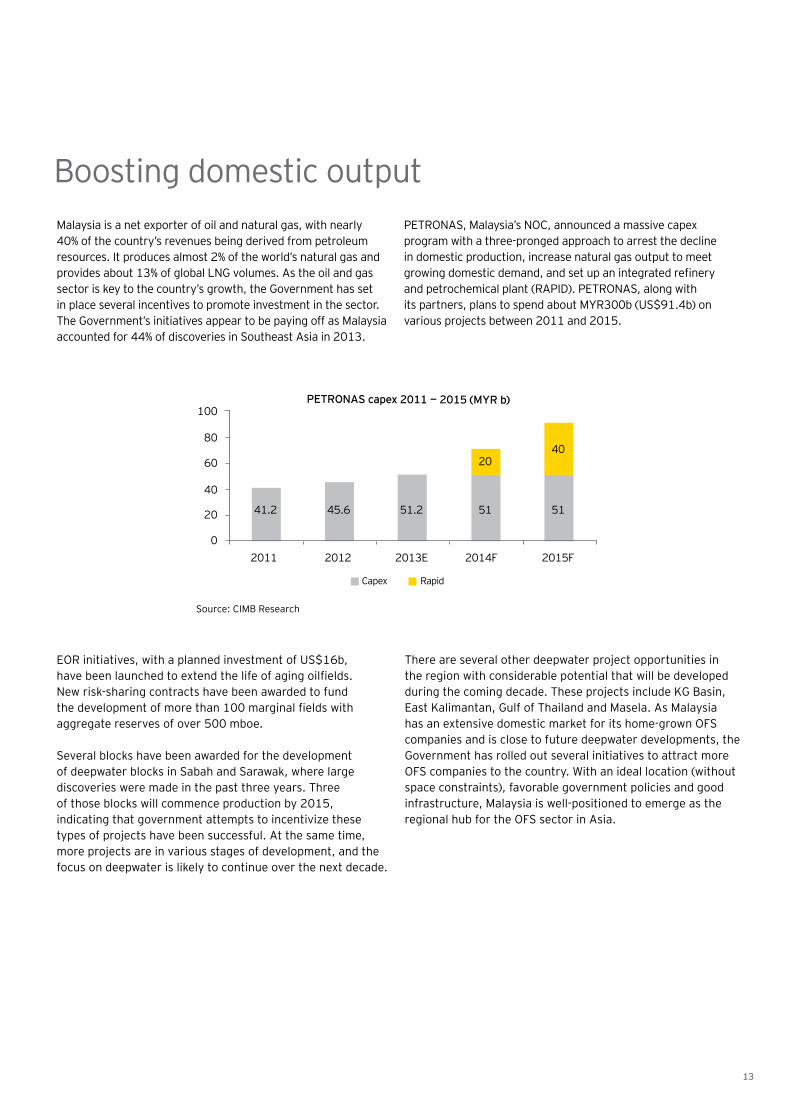

Malaysia is a net exporter of oil and natural gas, with nearly 40% of the country’s revenues being derived from petroleum resources. It produces almost 2% of the world’s natural gas and provides about 13% of global LNG volumes. As the oil and gas sector is key to the country’s growth, the Government has set in place several incentives to promote investment in the sector. The Government’s initiatives appear to be paying off as Malaysia accounted for 44% of discoveries in Southeast Asia in 2013.

Boosting domestic output

EOR initiatives, with a planned investment of US$16b, have been launched to extend the life of aging oilfields. New risk-sharing contracts have been awarded to fund the development of more than 100 marginal fields with aggregate reserves of over 500 mboe.

Several blocks have been awarded for the development of deepwater blocks in Sabah and Sarawak, where large discoveries were made in the past three years. Three of those blocks will commence production by 2015, indicating that government attempts to incentivize these types of projects have been successful. At the same time, more projects are in various stages of development, and the focus on deepwater is likely to continue over the next decade.

PETRONAS, Malaysia’s NOC, announced a massive capex program with a three-pronged approach to arrest the decline in domestic production, increase natural gas output to meet growing domestic demand, and set up an integrated refinery and petrochemical plant (RAPID). PETRONAS, along with its partners, plans to spend about MYR300b (US$91.4b) on various projects between 2011 and 2015.

There are several other deepwater project opportunities in the region with considerable potential that will be developed during the coming decade. These projects include KG Basin, East Kalimantan, Gulf of Thailand and Masela. As Malaysia has an extensive domestic market for its home-grown OFS companies and is close to future deepwater developments, the Government has rolled out several initiatives to attract more OFS companies to the country. With an ideal location (without space constraints), favorable government policies and good infrastructure, Malaysia is well-positioned to emerge as the regional hub for the OFS sector in Asia.

Source: CIMB Research

PETRONAS capex 2011 — 2015 (MYR b)100

80

60

40

20

02011 2012

Capex Rapid

2013E 2014F 2015F

41.2 45.6 51.2 51 51

2040

14

7 Spotlight on Singapore

14

15

Despite having no oil and natural gas reserves, Singapore has positioned itself to play a key role in the global market. The country’s efforts have paid off as it is currently the Asian hub for crude oil and is likely emerge as a significant player in natural gas or LNG trading in the region. On oilfield services, besides being a global leader in the construction of jack-up rigs and semi-submersibles, Singapore’s robust financial stock market has played a pivotal role in raising equity and debt for over thirty companies whose total enterprise value is around US$11.0b. (the enterprise value excludes Keppel and Sembcorp Marine)

In spite of facing challenges from the emergence of new players from China, Keppel and Sembcorp, have managed to develop their businesses through investing in research and technology and moving up the value chain.

Keppel has taken two bold initiatives, which reveal the company’s vision to maintain its competitive edge in the global market:

• Without having any confirmed order, Keppel is designing and building a state-of-the-art drill ship that will hit the market in 2016. Based on the company’s track record, Keppel will not face issues in marketing the drill ships, particularly as the exploration and development of oil and gas reserves moves into deepwater, the market for advanced drill ships is forecast to grow. With the proposed investment, Keppel has outlined its growth strategy.

• Keppel is negotiating with Golar LNG for the conversion of an LNG carrier into a floating storage liquefaction vessel (FSLV). Keppel was awarded front-end engineering and design (FEED) for the project in 2012, which it completed in August, 2013. Once Keppel demonstrates success in this project, there will be no shortage of orders for conversion of LNG tankers into FSLV.

The presence of leading private equity players in Singapore, with an appetite for investment in OFS companies, provides necessary capital for OFS companies of all sizes. While leading OFS companies will have manufacturing hubs in other countries, they continue to use Singapore as the financial hub which ensures the long-term viability of the country’s role in the OFS segment.

A financial hub for OFS companies in Southeast Asia

16

8 Growing influence of regional OFS

16

17

The regional scenarios described in the previous sections shows three significant trends: increased spending power of the Asian NOCs; increased influence of regional OFS players; and increased reliance on global OFS players for accessing reserves in the region. These trends are likely to reconfigure sector arrangements in the region and globally. This, in turn, will necessitate the creation of new approaches and business models.

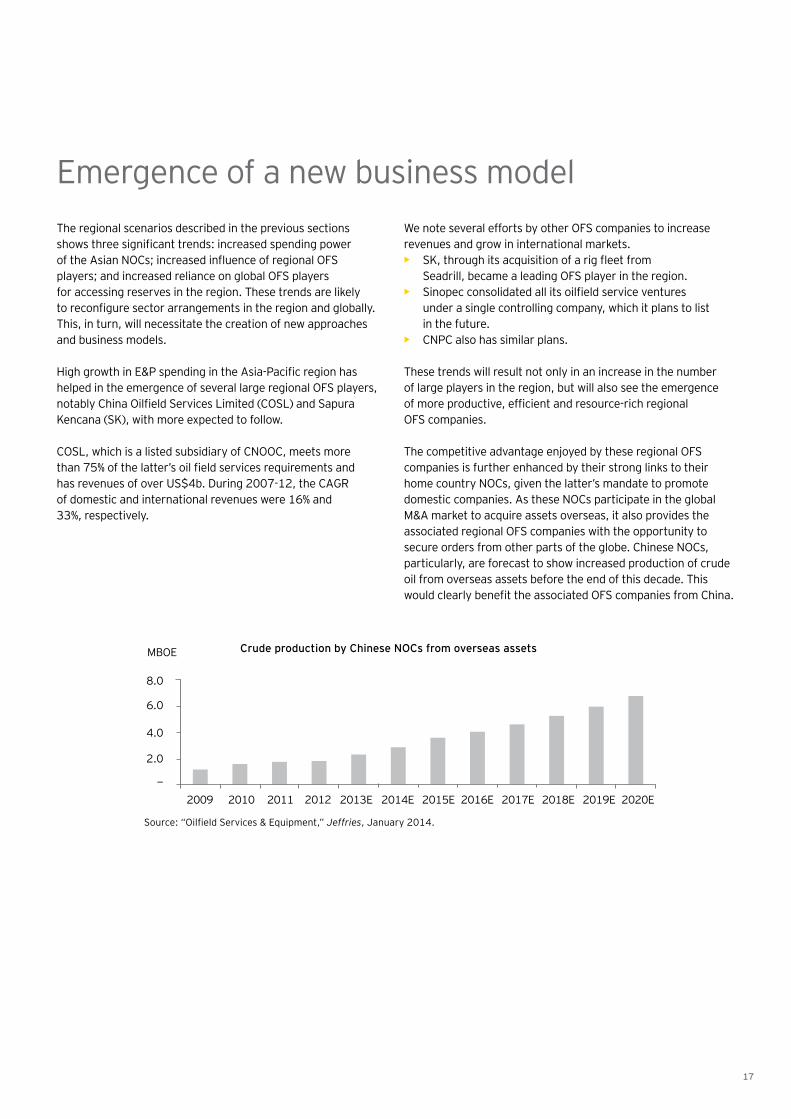

High growth in E&P spending in the Asia-Pacific region has helped in the emergence of several large regional OFS players, notably China Oilfield Services Limited (COSL) and Sapura Kencana (SK), with more expected to follow.

COSL, which is a listed subsidiary of CNOOC, meets more than 75% of the latter’s oil field services requirements and has revenues of over US$4b. During 2007-12, the CAGR of domestic and international revenues were 16% and 33%, respectively.

We note several efforts by other OFS companies to increase revenues and grow in international markets.• SK, through its acquisition of a rig fleet from

Seadrill, became a leading OFS player in the region. • Sinopec consolidated all its oilfield service ventures

under a single controlling company, which it plans to list in the future.

• CNPC also has similar plans.

These trends will result not only in an increase in the number of large players in the region, but will also see the emergence of more productive, efficient and resource-rich regional OFS companies.

The competitive advantage enjoyed by these regional OFS companies is further enhanced by their strong links to their home country NOCs, given the latter’s mandate to promote domestic companies. As these NOCs participate in the global M&A market to acquire assets overseas, it also provides the associated regional OFS companies with the opportunity to secure orders from other parts of the globe. Chinese NOCs, particularly, are forecast to show increased production of crude oil from overseas assets before the end of this decade. This would clearly benefit the associated OFS companies from China.

Emergence of a new business model

Crude production by Chinese NOCs from overseas assets

Source: “Oilfield Services & Equipment,” Jeffries, January 2014.

MBOE

8.0

6.0

4.0

2.0

—2009 2010 2011 2012 2013E 2014E 2015E 2016E 2017E 2018E 2019E 2020E

18

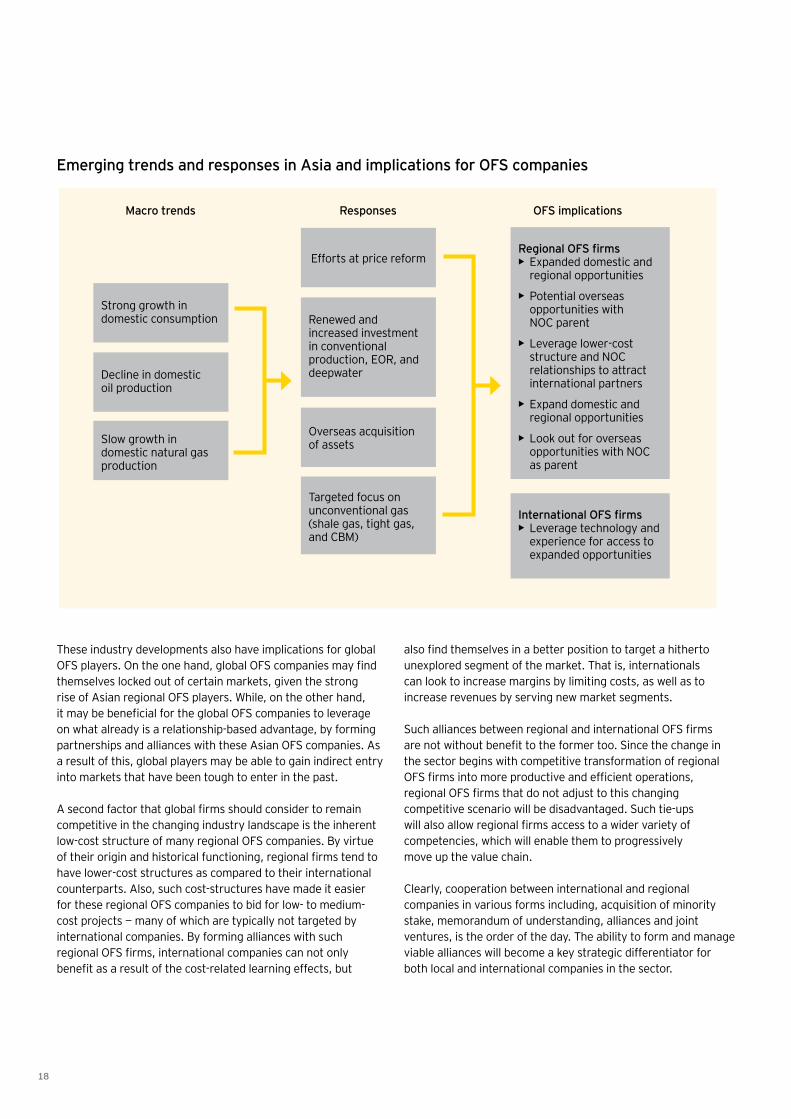

These industry developments also have implications for global OFS players. On the one hand, global OFS companies may find themselves locked out of certain markets, given the strong rise of Asian regional OFS players. While, on the other hand, it may be beneficial for the global OFS companies to leverage on what already is a relationship-based advantage, by forming partnerships and alliances with these Asian OFS companies. As a result of this, global players may be able to gain indirect entry into markets that have been tough to enter in the past.

A second factor that global firms should consider to remain competitive in the changing industry landscape is the inherent low-cost structure of many regional OFS companies. By virtue of their origin and historical functioning, regional firms tend to have lower-cost structures as compared to their international counterparts. Also, such cost-structures have made it easier for these regional OFS companies to bid for low- to medium- cost projects — many of which are typically not targeted by international companies. By forming alliances with such regional OFS firms, international companies can not only benefit as a result of the cost-related learning effects, but

also find themselves in a better position to target a hitherto unexplored segment of the market. That is, internationals can look to increase margins by limiting costs, as well as to increase revenues by serving new market segments.

Such alliances between regional and international OFS firms are not without benefit to the former too. Since the change in the sector begins with competitive transformation of regional OFS firms into more productive and efficient operations, regional OFS firms that do not adjust to this changing competitive scenario will be disadvantaged. Such tie-ups will also allow regional firms access to a wider variety of competencies, which will enable them to progressively move up the value chain.

Clearly, cooperation between international and regional companies in various forms including, acquisition of minority stake, memorandum of understanding, alliances and joint ventures, is the order of the day. The ability to form and manage viable alliances will become a key strategic differentiator for both local and international companies in the sector.

Emerging trends and responses in Asia and implications for OFS companies

Macro trends Responses OFS implications

Strong growth in domestic consumption

Efforts at price reformRegional OFS firms• Expanded domestic and

regional opportunities

• Potential overseas opportunities with NOC parent

• Leverage lower-cost structure and NOC relationships to attract international partners

• Expand domestic and regional opportunities

• Look out for overseas opportunities with NOC as parent

International OFS firms• Leverage technology and

experience for access to expanded opportunities

Decline in domestic oil production

Renewed and increased investment in conventional production, EOR, and deepwater

Slow growth in domestic natural gas production

Overseas acquisition of assets

Targeted focus on unconventional gas (shale gas, tight gas, and CBM)

19

EY’s global oil and gas team

Calgary

Houston

Rio de Janeiro

Global Hub CenterRegional Hub Center

Stavanger

Moscow

Beijing

Singapore

Perth

Aberdeen

Lagos

London

Bahrain

BrisbaneJohannesburg

Cape Town

Europe, Middle East, India and Africa4,800 professionals

Americas3,300 professionals

Asia-Pacific and Japan1, 500 professionals

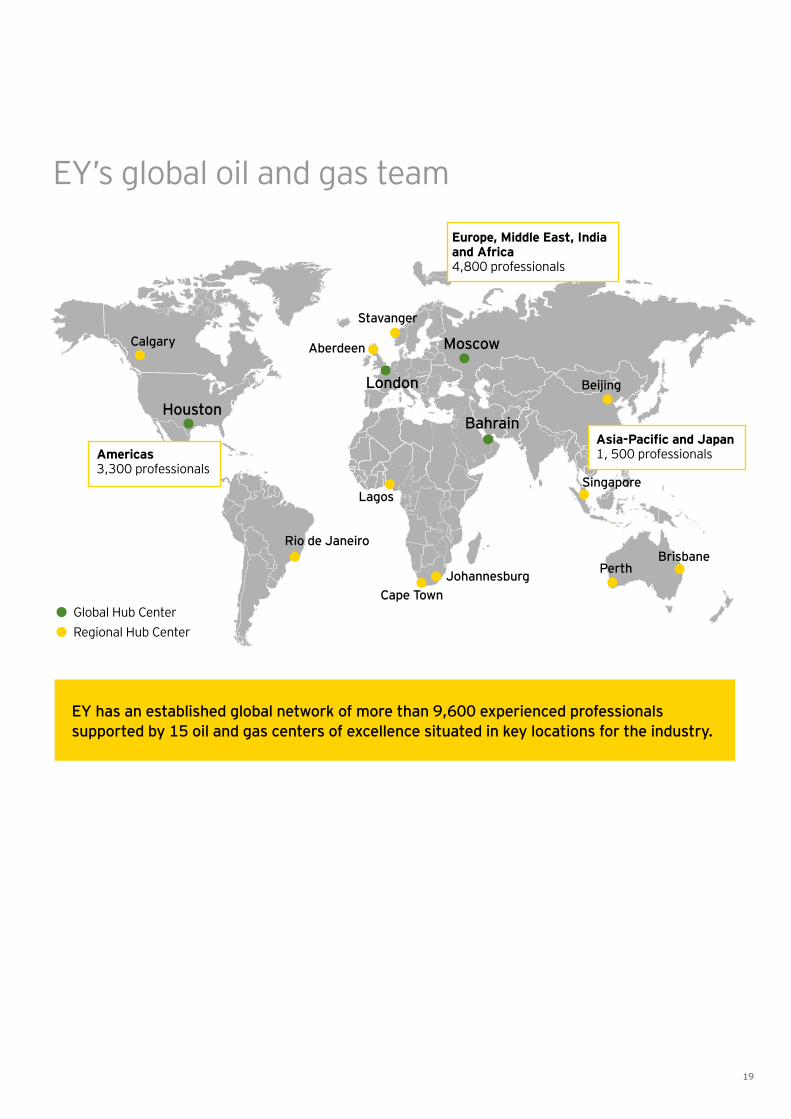

EY has an established global network of more than 9,600 experienced professionals supported by 15 oil and gas centers of excellence situated in key locations for the industry.

Regional Oil & Gas teamKC YauGreater China O&G Assurance LeaderBeijingTel: +86 10 58153339Email: [email protected]

Xiaoping ZhangGreater China O&G Advisory LeaderShanghaiTel: +86 21 2228 2660Email: [email protected]

Alan LanTax PartnerBeijingTel: +86 10 58153389Email: [email protected]

Andy ChenGreater China O&G Tax LeaderBeijingTel: +86 10 5815 3381Email: [email protected]

August ZhaoAssurance PartnerBeijingTel: +86 10 58152829Email: [email protected]

Rebecca MakTax PartnerBeijingTel: +86 10 58152910Email: [email protected]

Chauon ChokGreater China O&G TAS LeaderBeijingTel: +86 10 5815 2838Email: [email protected]

Libby ZhongAssurance PartnerBeijingTel: +86 10 58153541Email: [email protected]

Lucy WangTax PartnerBeijingTel: +86 10 58153809Email: [email protected]

Global Oil & Gas CenterDale Nijoka Global Oil & Gas LeaderHoustonTel: +1 713 750 1551Email: [email protected]

Alexey KondrashovGlobal Oil & Gas Tax LeaderMoscowTel: +7 495 662 9394Email: [email protected]

Alexandre OliveiraGlobal Oil & Gas Emerging Markets LeaderDubaiTel: +971 4 7010750Email: [email protected]

Andy BroganGlobal Oil & Gas Transaction LeaderLondonTel: +44 20 7951 7009Email: [email protected]

Gary DonaldGlobal Oil & Gas Assurance LeaderLondonTel: +44 20 7951 7518Email: [email protected]

Axel PreissGlobal Oil & Gas Advisory LeaderFrankfurt Tel: +49 619 699 96 17589Email: [email protected]

Contacts

20

21

Notes

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

How EY’s Global Oil & Gas Center can help your businessThe oil and gas sector is constantly changing. Increasingly uncertain energy policies, geopolitical complexities, cost management and climate change all present significant challenges. EY’s Global Oil & Gas Center supports a global network of more than 9,600 oil and gas professionals with extensive experience in providing assurance, tax, transaction and advisory services across the upstream, midstream, downstream and oilfield service sub-sectors. The Center works to anticipate market trends, execute the mobility of our global resources and articulate points of view on relevant key sector issues. With our deep sector focus, we can help your organization drive down costs and compete more effectively.

© 2014 EYGM Limited.All Rights Reserved.

EYG no. DW0373ED 0115

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

www.ey.com