Thomas Young, IRPA & OI Advisory Board Member

30

MARKET BRIEFING AND TRENDS www.outsourcing.com www.IRPAnetwork.com Thomas Young, IRPA & OI Advisory Board Member March 2014

Transcript of Thomas Young, IRPA & OI Advisory Board Member

MARKET BRIEFING AND TRENDS

www.outsourcing.com www.IRPAnetwork.com

Thomas Young, IRPA & OI Advisory Board Member

March 2014

PO

LAR S

HIFT IN

THE R

ELATIO

N O

F TEC

HN

OLO

GY &

LA

BO

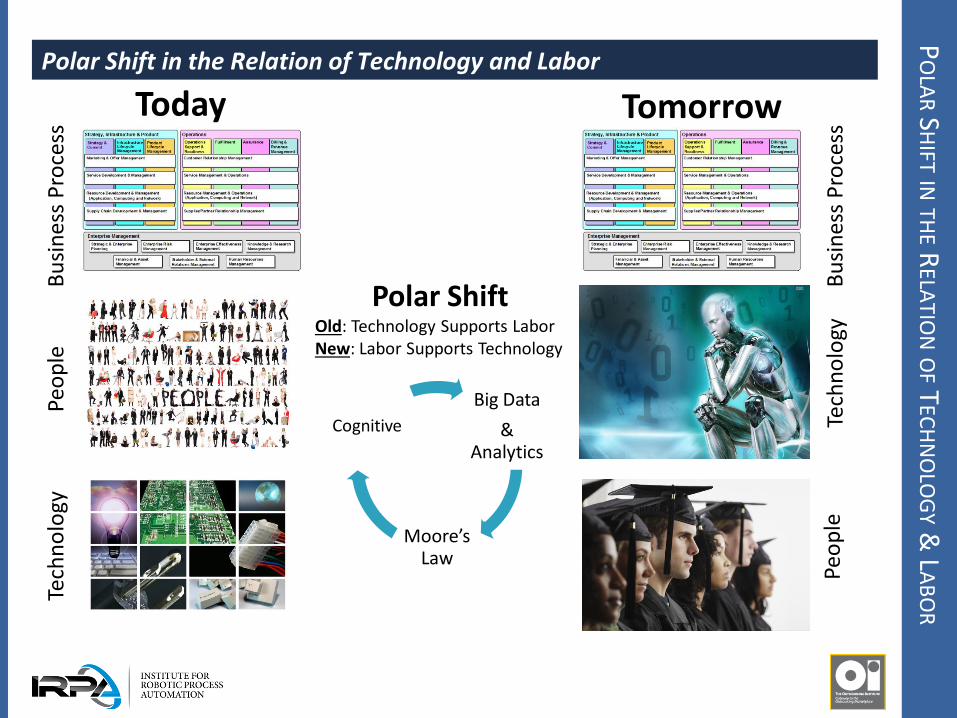

R Polar Shift in the Relation of Technology and Labor

Bu

sin

ess

Pro

cess

Te

chn

olo

gy

Peo

ple

Bu

sin

ess

Pro

cess

Te

chn

olo

gy

Peo

ple

Big Data

& Analytics

Moore’s Law

Cognitive

Polar Shift Old: Technology Supports Labor New: Labor Supports Technology

Today Tomorrow

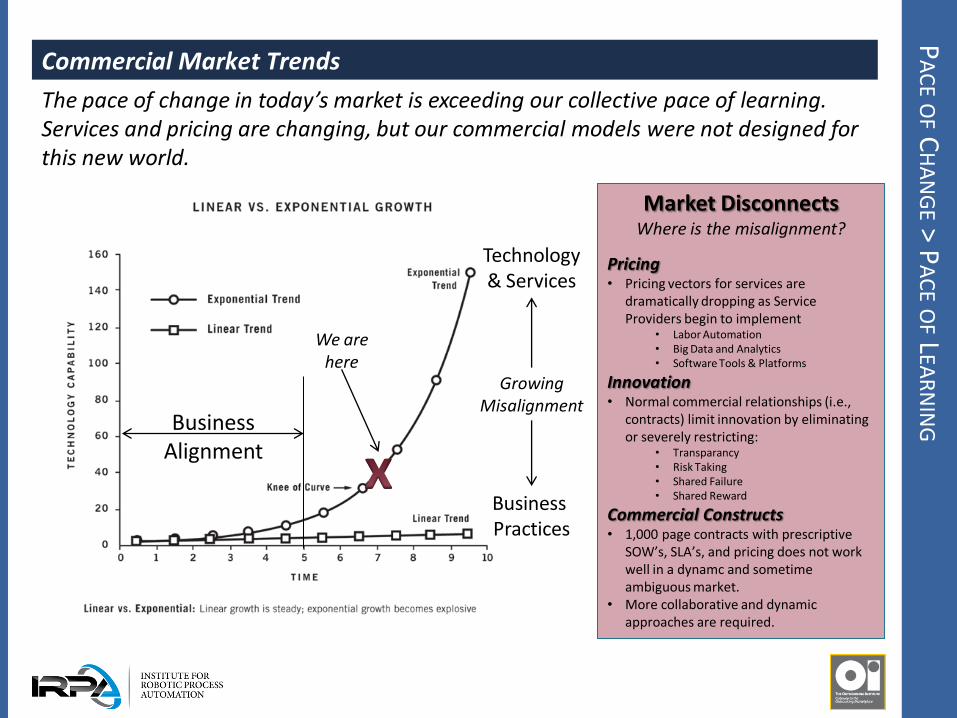

The pace of change in today’s market is exceeding our collective pace of learning. Services and pricing are changing, but our commercial models were not designed for this new world.

Business Alignment

Technology & Services

Business Practices

We are here

Growing Misalignment

Market Disconnects Where is the misalignment?

Pricing • Pricing vectors for services are

dramatically dropping as Service Providers begin to implement

• Labor Automation • Big Data and Analytics • Software Tools & Platforms

Innovation • Normal commercial relationships (i.e.,

contracts) limit innovation by eliminating or severely restricting:

• Transparancy • Risk Taking • Shared Failure • Shared Reward

Commercial Constructs • 1,000 page contracts with prescriptive

SOW’s, SLA’s, and pricing does not work well in a dynamc and sometime ambiguous market.

• More collaborative and dynamic approaches are required.

PA

CE O

F CH

AN

GE >

PA

CE O

F LEA

RN

ING

Commercial Market Trends

EV

OLU

TION

OF TH

E BU

YING E

CO

SYSTEM

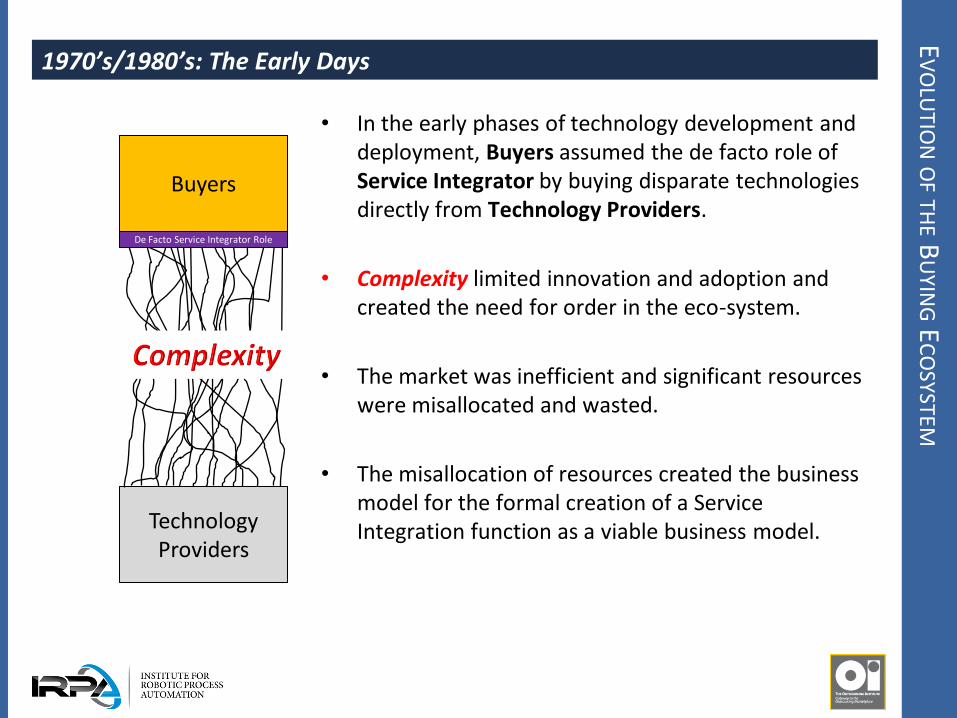

1970’s/1980’s: The Early Days

• In the early phases of technology development and deployment, Buyers assumed the de facto role of Service Integrator by buying disparate technologies directly from Technology Providers.

• Complexity limited innovation and adoption and created the need for order in the eco-system.

• The market was inefficient and significant resources were misallocated and wasted.

• The misallocation of resources created the business model for the formal creation of a Service Integration function as a viable business model.

Buyers

Technology Providers

De Facto Service Integrator Role

EV

OLU

TION

OF TH

E BU

YING E

CO

SYSTEM

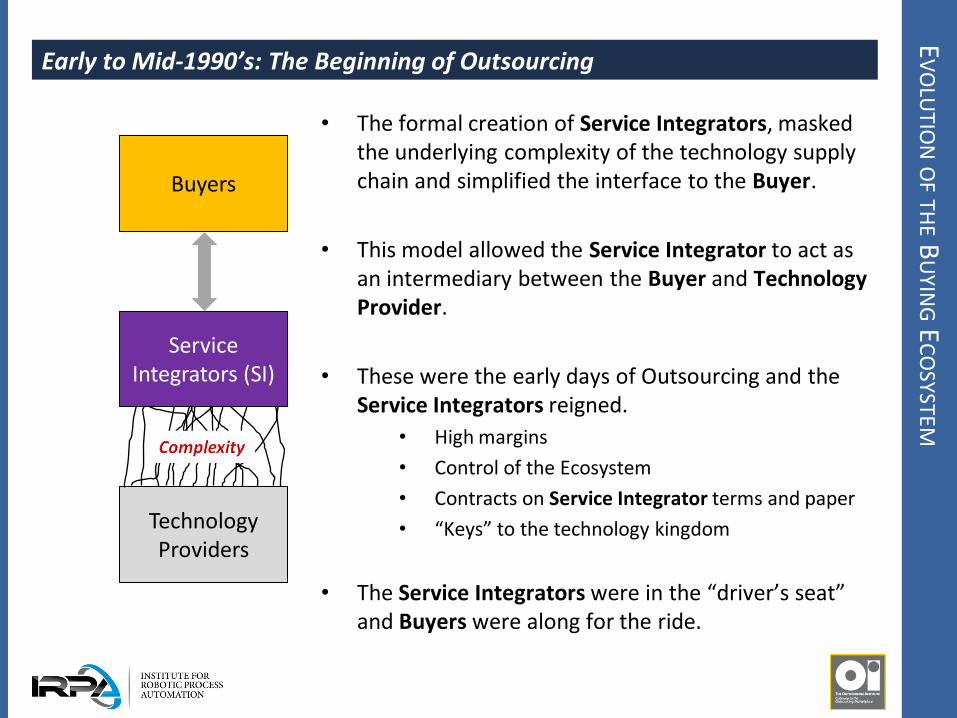

Early to Mid-1990’s: The Beginning of Outsourcing

• The formal creation of Service Integrators, masked the underlying complexity of the technology supply chain and simplified the interface to the Buyer.

• This model allowed the Service Integrator to act as an intermediary between the Buyer and Technology Provider.

• These were the early days of Outsourcing and the Service Integrators reigned.

• High margins

• Control of the Ecosystem

• Contracts on Service Integrator terms and paper

• “Keys” to the technology kingdom

• The Service Integrators were in the “driver’s seat” and Buyers were along for the ride.

Technology Providers

Buyers

Service Integrators (SI)

EV

OLU

TION

OF TH

E BU

YING E

CO

SYSTEM

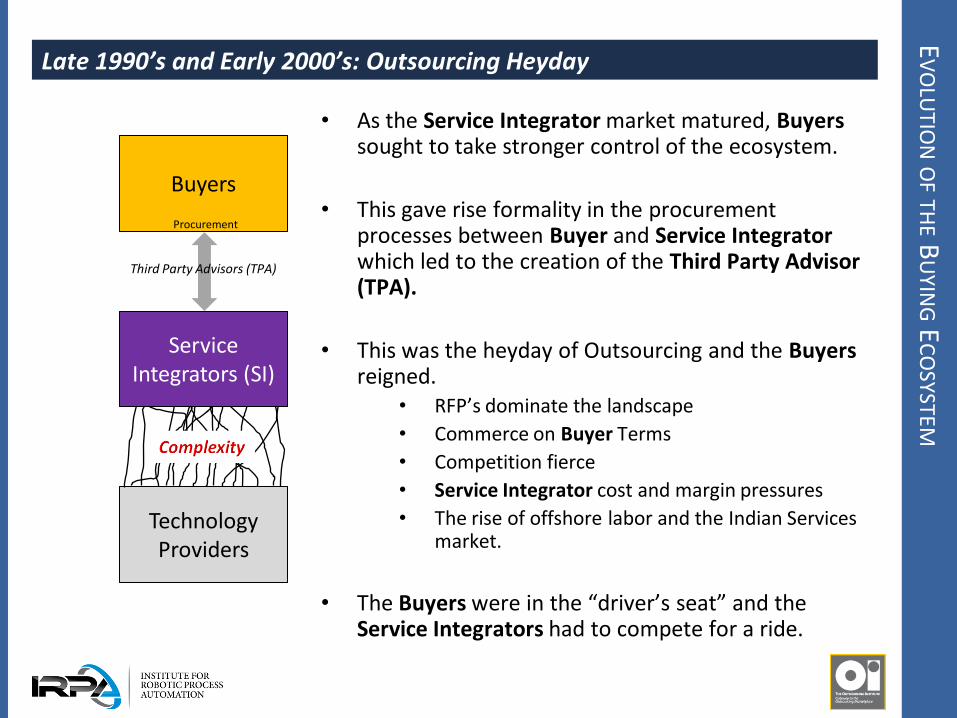

Late 1990’s and Early 2000’s: Outsourcing Heyday

• As the Service Integrator market matured, Buyers sought to take stronger control of the ecosystem.

• This gave rise formality in the procurement processes between Buyer and Service Integrator which led to the creation of the Third Party Advisor (TPA).

• This was the heyday of Outsourcing and the Buyers reigned.

• RFP’s dominate the landscape

• Commerce on Buyer Terms

• Competition fierce

• Service Integrator cost and margin pressures

• The rise of offshore labor and the Indian Services market.

• The Buyers were in the “driver’s seat” and the Service Integrators had to compete for a ride.

Technology Providers

Buyers

Service Integrators (SI)

Procurement

Third Party Advisors (TPA)

EV

OLU

TION

OF TH

E BU

YING E

CO

SYSTEM

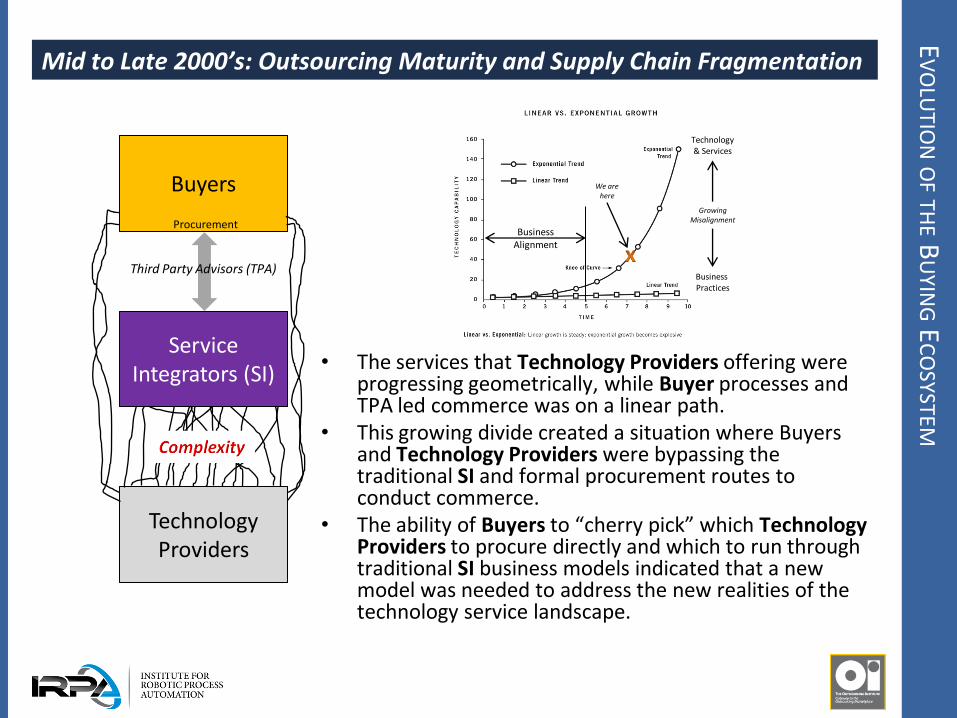

Mid to Late 2000’s: Outsourcing Maturity and Supply Chain Fragmentation

• The services that Technology Providers offering were

progressing geometrically, while Buyer processes and TPA led commerce was on a linear path.

• This growing divide created a situation where Buyers and Technology Providers were bypassing the traditional SI and formal procurement routes to conduct commerce.

• The ability of Buyers to “cherry pick” which Technology Providers to procure directly and which to run through traditional SI business models indicated that a new model was needed to address the new realities of the technology service landscape.

Technology Providers

Buyers

Service Integrators (SI)

Procurement

Third Party Advisors (TPA)

Business Alignment

Technology & Services

Business Practices

We are here

Growing Misalignment

EV

OLU

TION

OF TH

E BU

YING E

CO

SYSTEM

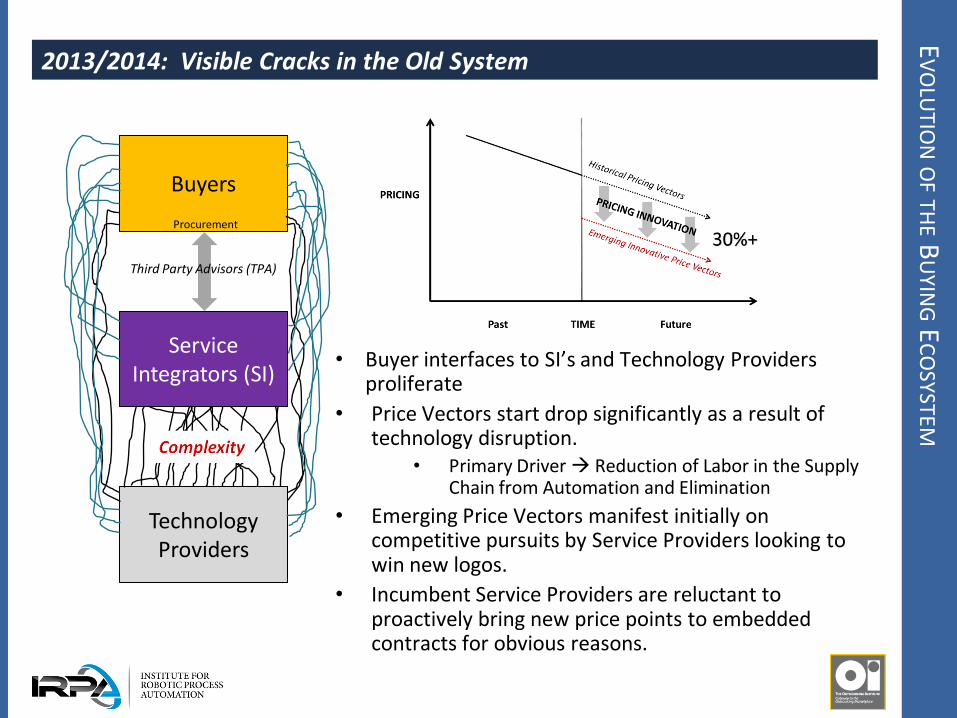

2013/2014: Visible Cracks in the Old System

Technology Providers

Buyers

Service Integrators (SI)

Procurement

Third Party Advisors (TPA)

• Buyer interfaces to SI’s and Technology Providers proliferate

• Price Vectors start drop significantly as a result of technology disruption.

• Primary Driver Reduction of Labor in the Supply Chain from Automation and Elimination

• Emerging Price Vectors manifest initially on competitive pursuits by Service Providers looking to win new logos.

• Incumbent Service Providers are reluctant to proactively bring new price points to embedded contracts for obvious reasons.

IBM

GLO

BA

L TEC

HN

OLO

GY S

ERV

ICES

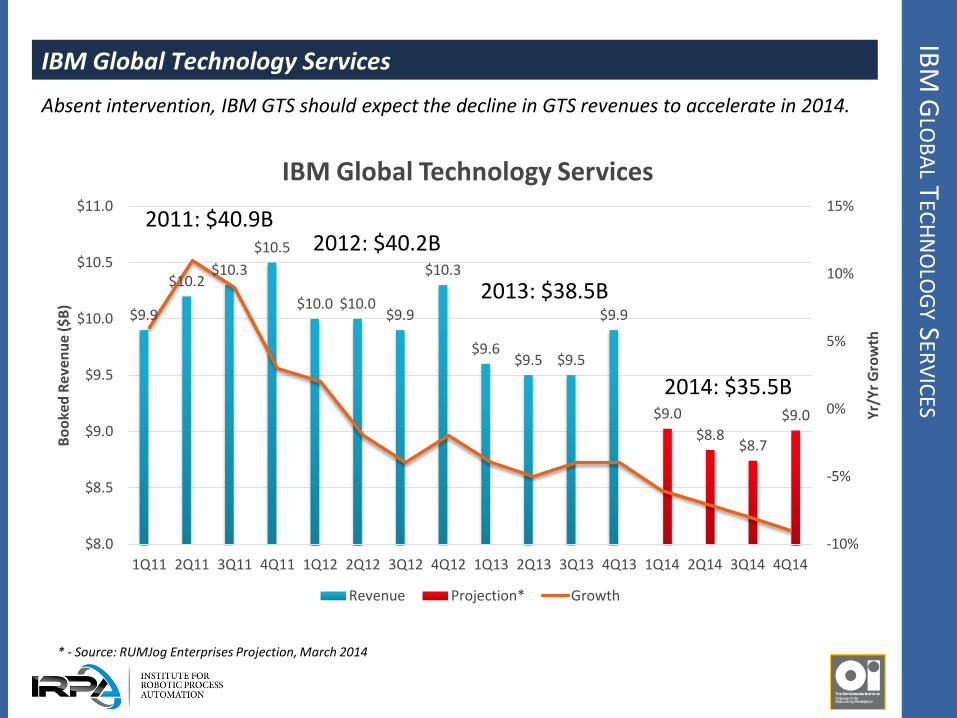

IBM Global Technology Services

Absent intervention, IBM GTS should expect the decline in GTS revenues to accelerate in 2014.

$9.9

$10.2 $10.3

$10.5

$10.0 $10.0 $9.9

$10.3

$9.6 $9.5 $9.5

$9.9

$9.0

$8.8 $8.7

$9.0

-10%

-5%

0%

5%

10%

15%

$8.0

$8.5

$9.0

$9.5

$10.0

$10.5

$11.0

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14

Yr/

Yr

Gro

wth

Bo

oke

d R

even

ue

($B

)

IBM Global Technology Services

Revenue Projection* Growth

2013: $38.5B

2014: $35.5B

* - Source: RUMJog Enterprises Projection, March 2014

2012: $40.2B 2011: $40.9B

HP

EN

TERP

RISE S

ERV

ICES

HP Enterprise Services

Absent intervention, HP Enterprise Services will decline to quarterly revenues below $5.0B starting in 3Q14 and incur and operating loss in 3Q and 4Q 2014.

$6.2

$6.6 $6.7

$6.8

$6.4

$6.6 $6.4 $6.4

$5.9 $6.0

$5.8 $5.8

$5.6

$5.3

$5.0

$4.6

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

$4.0

$4.5

$5.0

$5.5

$6.0

$6.5

$7.0

1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14

Yr/

Yr

Gro

wth

Bo

oke

d R

even

ue

($B

)

HP Enterprise Services

Revenue Projection* Growth

2013: $23.5B

2012: $25.7B 2011: $26.3B

2014: $20.6B

* - Source: RUMJog Enterprises Projection, March 2014

TR

END

S IN TH

E TEC

HN

OLO

GY S

OU

RC

ING M

AR

KET

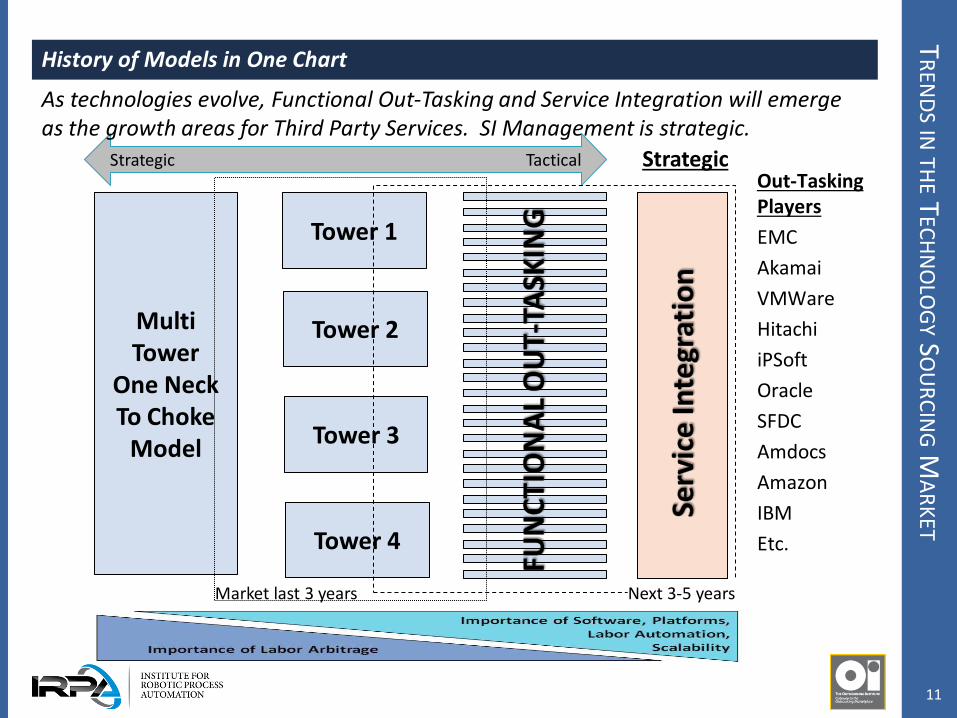

History of Models in One Chart

Out-Tasking Players

EMC

Akamai

VMWare

Hitachi

iPSoft

Oracle

SFDC

Amdocs

Amazon

IBM

Etc.

Multi Tower

One Neck To Choke

Model

Tower 2

Tower 3

Tower 4

Market last 3 years

Strategic Tactical

Tower 1

Next 3-5 years

Strategic

11

As technologies evolve, Functional Out-Tasking and Service Integration will emerge as the growth areas for Third Party Services. SI Management is strategic.

FU

NC

TION

AL O

UT-T

ASK

ING

: WH

AT’S TH

E BIG D

EAL

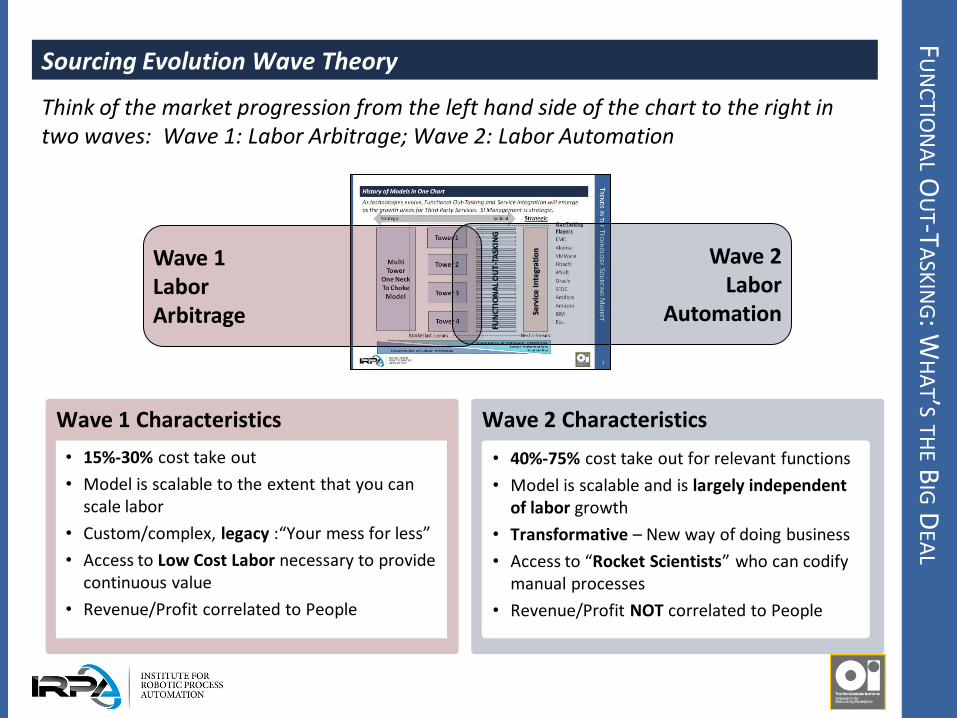

Sourcing Evolution Wave Theory

Think of the market progression from the left hand side of the chart to the right in two waves: Wave 1: Labor Arbitrage; Wave 2: Labor Automation

Wave 2 Characteristics Wave 1 Characteristics

• 15%-30% cost take out

• Model is scalable to the extent that you can scale labor

• Custom/complex, legacy :“Your mess for less”

• Access to Low Cost Labor necessary to provide continuous value

• Revenue/Profit correlated to People

• 40%-75% cost take out for relevant functions

• Model is scalable and is largely independent of labor growth

• Transformative – New way of doing business

• Access to “Rocket Scientists” who can codify manual processes

• Revenue/Profit NOT correlated to People

Wave 1 Labor Arbitrage

Wave 2 Labor

Automation

EC

ON

OM

ICS O

F THE F

UTU

RE

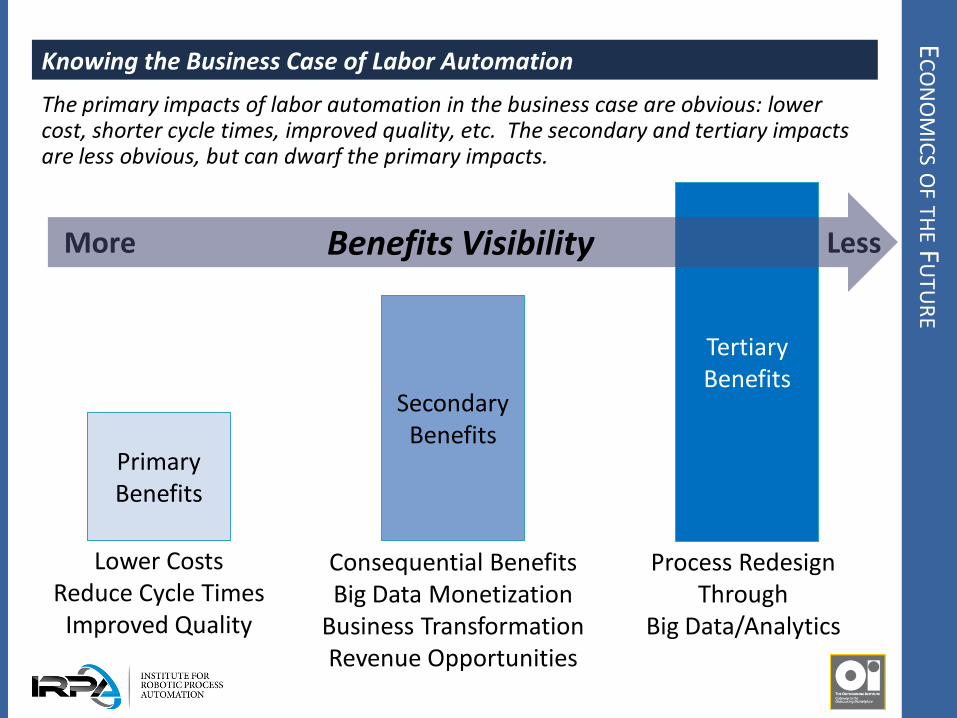

Knowing the Business Case of Labor Automation

Primary Benefits

Secondary Benefits

Lower Costs Reduce Cycle Times

Improved Quality

Consequential Benefits Big Data Monetization

Business Transformation Revenue Opportunities

Tertiary Benefits

Process Redesign Through

Big Data/Analytics

More Less Benefits Visibility

The primary impacts of labor automation in the business case are obvious: lower cost, shorter cycle times, improved quality, etc. The secondary and tertiary impacts are less obvious, but can dwarf the primary impacts.

EV

OLU

TION

OF TH

E BU

YING E

CO

SYSTEM

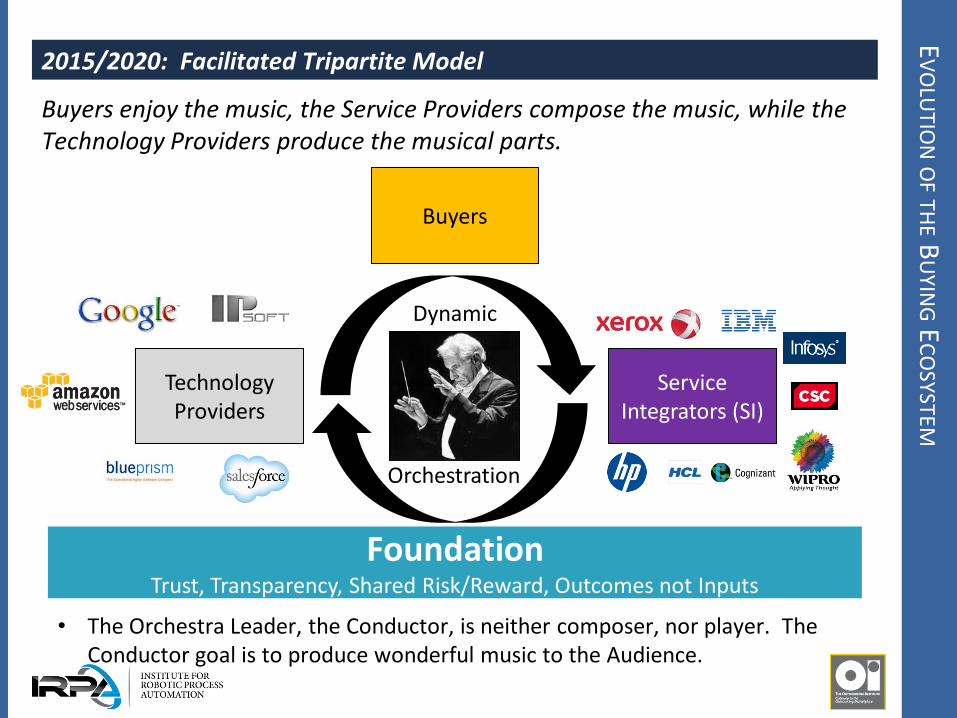

2015/2020: Facilitated Tripartite Model

Technology Providers

Buyers

Service Integrators (SI)

Foundation Trust, Transparency, Shared Risk/Reward, Outcomes not Inputs

Dynamic

Orchestration

• The Orchestra Leader, the Conductor, is neither composer, nor player. The Conductor goal is to produce wonderful music to the Audience.

Buyers enjoy the music, the Service Providers compose the music, while the Technology Providers produce the musical parts.

SO

UR

CIN

G SU

CC

ESS IN A D

YNA

MIC M

AR

KET

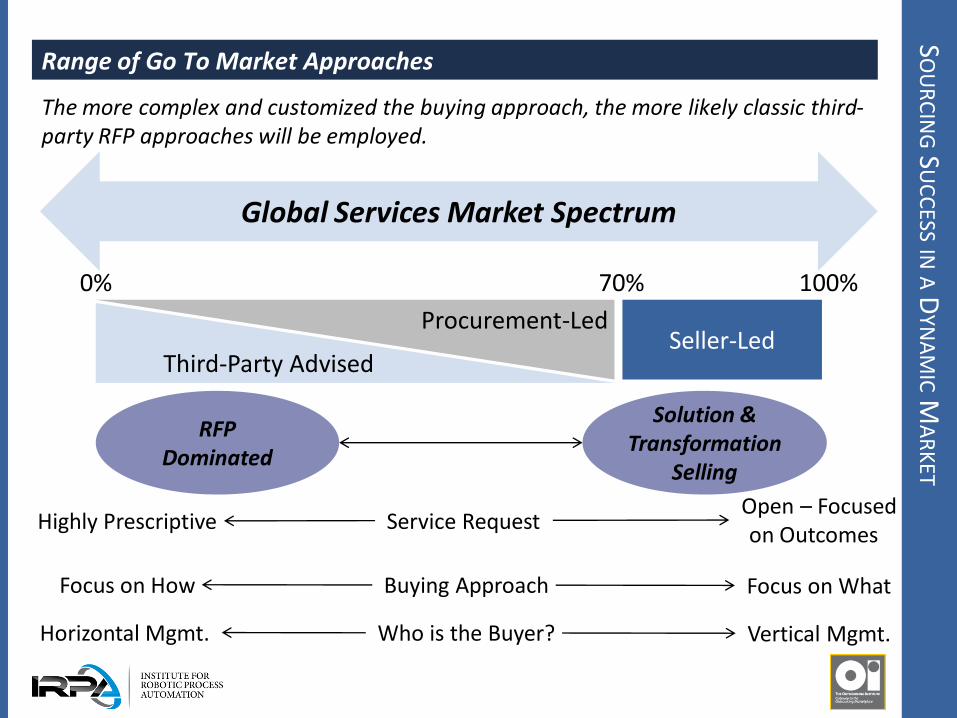

Range of Go To Market Approaches

The more complex and customized the buying approach, the more likely classic third-party RFP approaches will be employed.

Global Services Market Spectrum

Third-Party Advised Seller-Led

Procurement-Led

70% 0% 100%

RFP Dominated

Solution & Transformation

Selling

Highly Prescriptive Open – Focused

on Outcomes Service Request

Focus on How Focus on What Buying Approach

Horizontal Mgmt. Vertical Mgmt. Who is the Buyer?

SO

UR

CIN

G SU

CC

ESS IN A D

YNA

MIC M

AR

KET

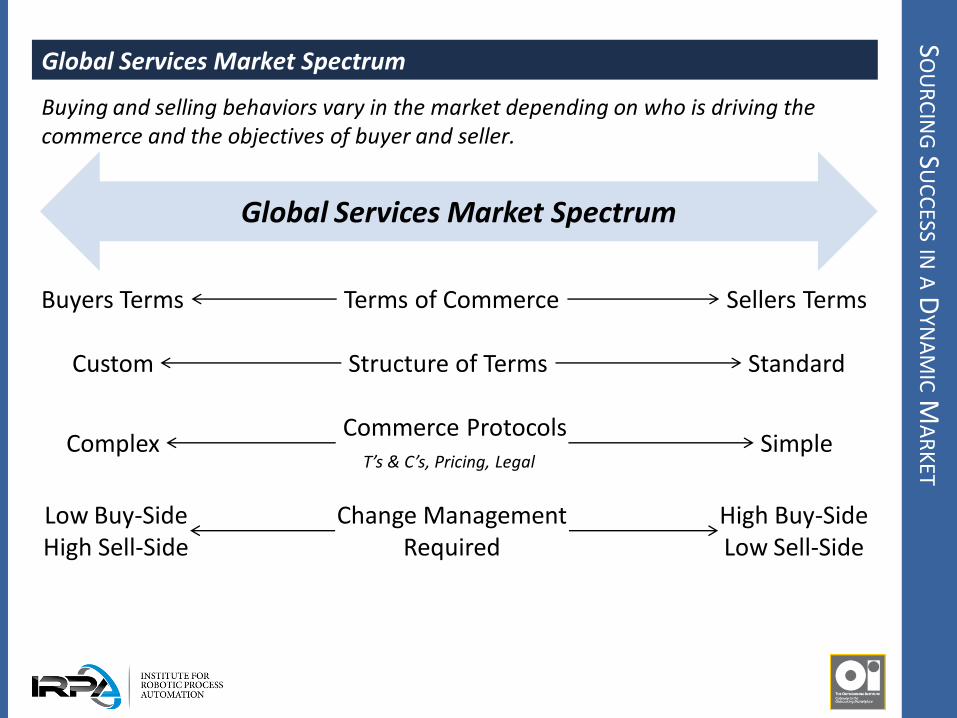

Global Services Market Spectrum

Buying and selling behaviors vary in the market depending on who is driving the commerce and the objectives of buyer and seller.

Global Services Market Spectrum

Buyers Terms Sellers Terms

Custom Standard

Complex Simple

Low Buy-Side High Sell-Side

High Buy-Side Low Sell-Side

Terms of Commerce

Structure of Terms

Commerce Protocols T’s & C’s, Pricing, Legal

Change Management Required

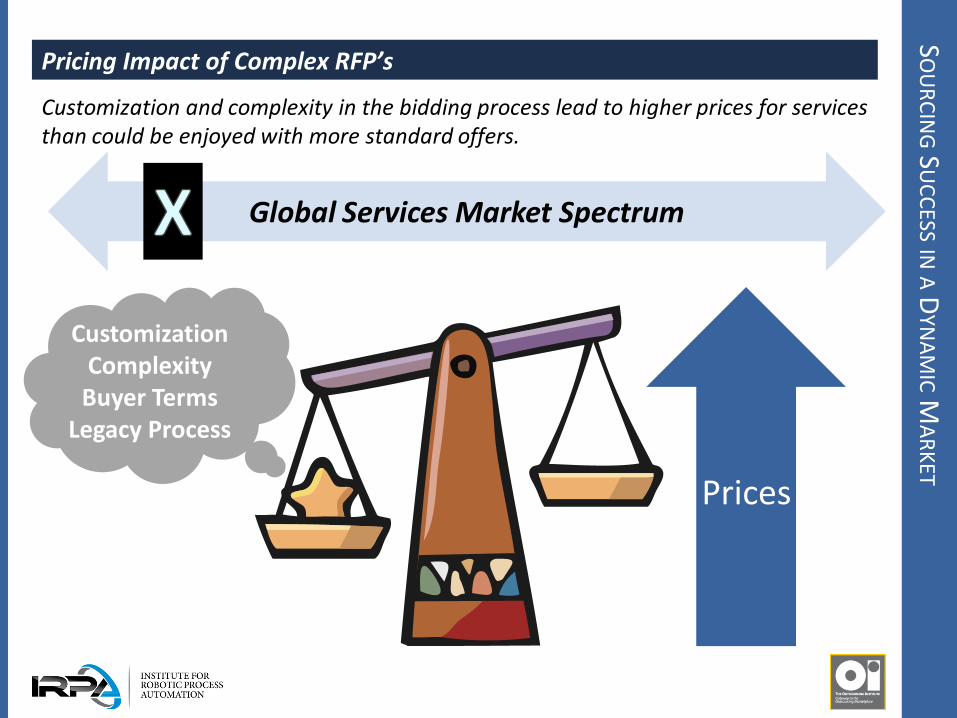

Pricing Impact of Complex RFP’s

Customization and complexity in the bidding process lead to higher prices for services than could be enjoyed with more standard offers.

SO

UR

CIN

G SU

CC

ESS IN A D

YNA

MIC M

AR

KET

Global Services Market Spectrum

Customization Complexity

Buyer Terms Legacy Process

Prices

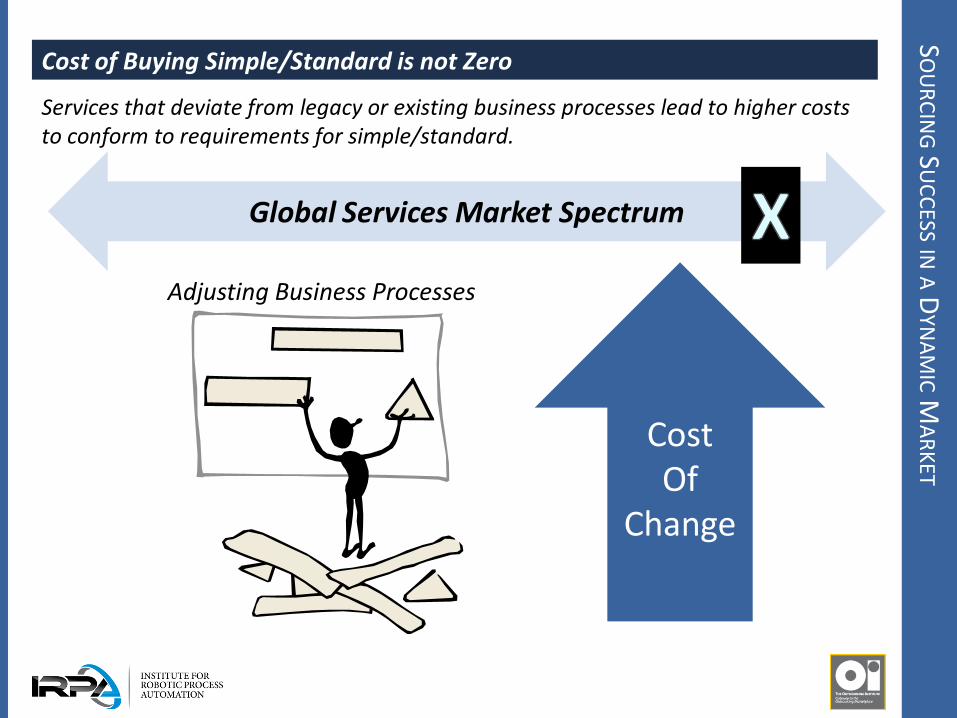

Cost of Buying Simple/Standard is not Zero

Services that deviate from legacy or existing business processes lead to higher costs to conform to requirements for simple/standard.

SO

UR

CIN

G SU

CC

ESS IN A D

YNA

MIC M

AR

KET

Global Services Market Spectrum

Cost Of

Change

Adjusting Business Processes

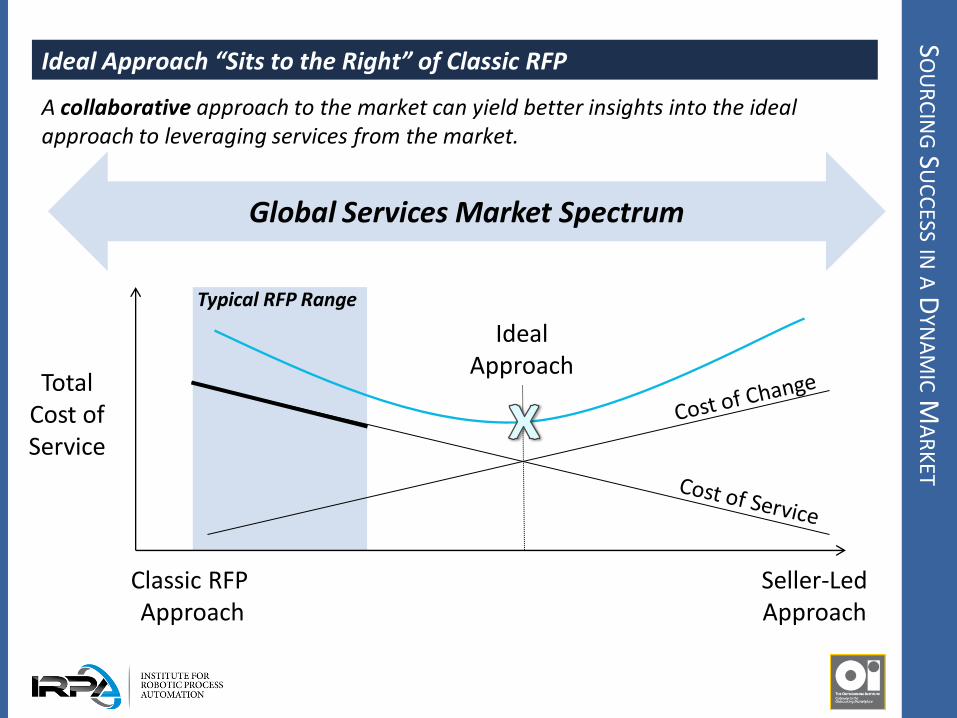

Ideal Approach “Sits to the Right” of Classic RFP

A collaborative approach to the market can yield better insights into the ideal approach to leveraging services from the market.

SO

UR

CIN

G SU

CC

ESS IN A D

YNA

MIC M

AR

KET

Global Services Market Spectrum

Total Cost of Service

Classic RFP Approach

Seller-Led Approach

Ideal Approach

Typical RFP Range

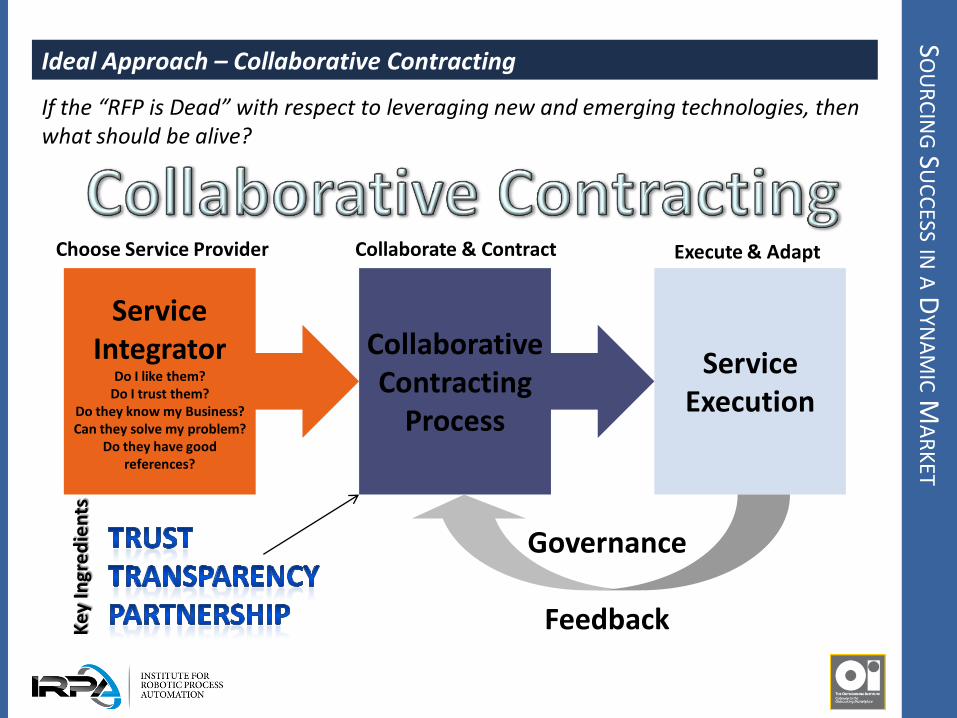

Ideal Approach – Collaborative Contracting

If the “RFP is Dead” with respect to leveraging new and emerging technologies, then what should be alive?

SO

UR

CIN

G SU

CC

ESS IN A D

YNA

MIC M

AR

KET

Service Integrator

Do I like them? Do I trust them?

Do they know my Business? Can they solve my problem?

Do they have good references?

Collaborative Contracting

Process

Service Execution

Governance

Feedback

Choose Service Provider Collaborate & Contract Execute & Adapt

Key

Ingr

ed

ien

ts

CO

LLAB

OR

ATIV

E CO

NTR

AC

TING

Collaborative Contracting: What are the Keys to Success

• Clients, primarily the Procurement and Finance organizations, need to be open to trying new ways of engaging the market for services. • Clients need to recognize the innovation requires both buyer and CSC to work

together in an open environment and be willing to: • Take Risk

• Share the Risk/Reward

• Service Providers needs to be transparent, reasonable, and be proactive driving the most innovative solutions – even if it is to the detriment of short term revenue. • Collaborative Contracting is not for commoditized or near commoditized services.

• Collaborative Contracting works ideally, when transformation is required and the path ahead undefined or untested.

• Technology Providers need to better understand how their technologies fit into the overall Services Ecosystem.

• You cannot have the trumpet playing off a different sheet of music.

• Advisors need to be more consultative and less process driven. • Ecosystem neutrality (orchestra leader) is key to help facilitate a commercial dialog

that achieves the commercial goals of: • Price optimization

• Innovation & Collaboration

• Trust and Transparency

CO

LLAB

OR

ATIV

E CO

NTR

AC

TING

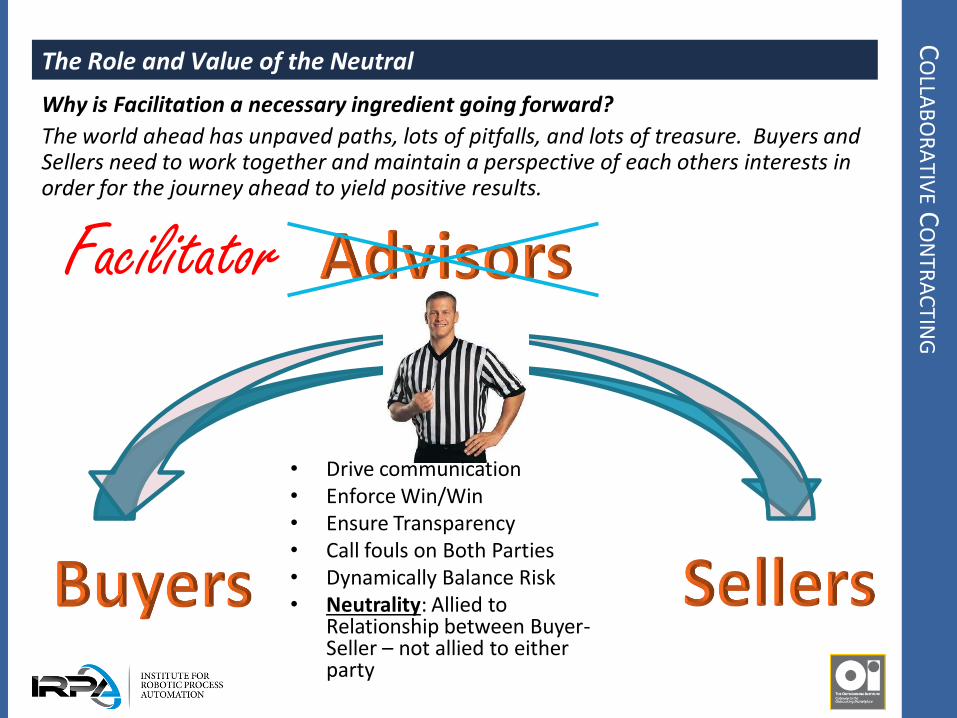

The Role and Value of the Neutral

• Drive communication • Enforce Win/Win • Ensure Transparency • Call fouls on Both Parties • Dynamically Balance Risk • Neutrality: Allied to

Relationship between Buyer-Seller – not allied to either party

Facilitator

Why is Facilitation a necessary ingredient going forward?

The world ahead has unpaved paths, lots of pitfalls, and lots of treasure. Buyers and Sellers need to work together and maintain a perspective of each others interests in order for the journey ahead to yield positive results.

TH

E RO

AD A

HEA

D

CO

GN

ITIVE T

ECH

NO

LOG

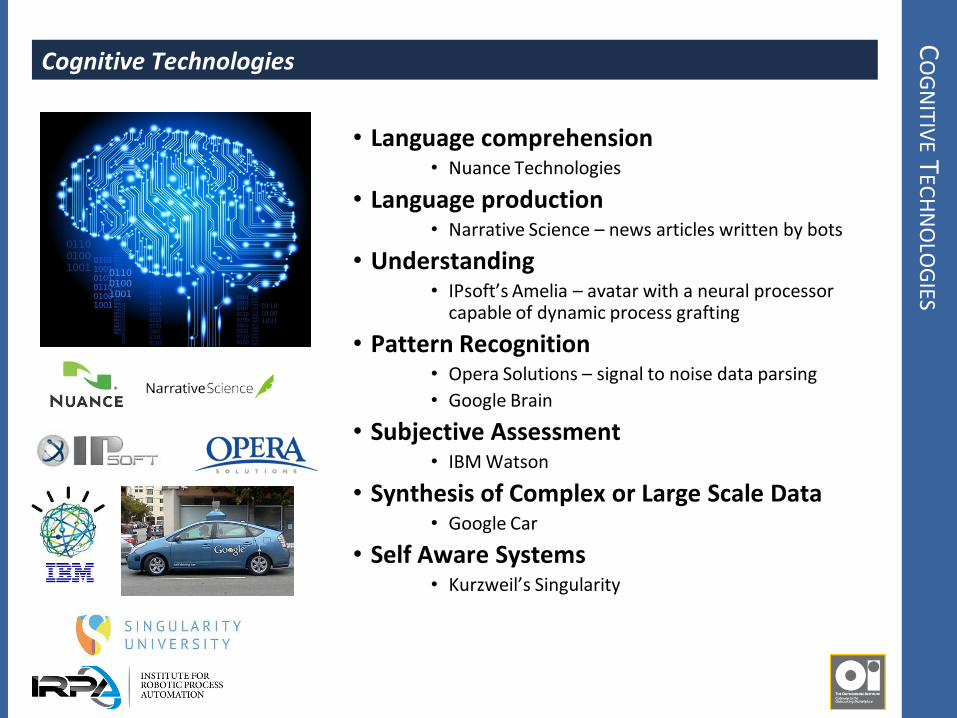

IES Cognitive Technologies

• Language comprehension • Nuance Technologies

• Language production • Narrative Science – news articles written by bots

• Understanding • IPsoft’s Amelia – avatar with a neural processor

capable of dynamic process grafting

• Pattern Recognition • Opera Solutions – signal to noise data parsing

• Google Brain

• Subjective Assessment • IBM Watson

• Synthesis of Complex or Large Scale Data • Google Car

• Self Aware Systems • Kurzweil’s Singularity

INN

OV

ATIO

N F

OR

MU

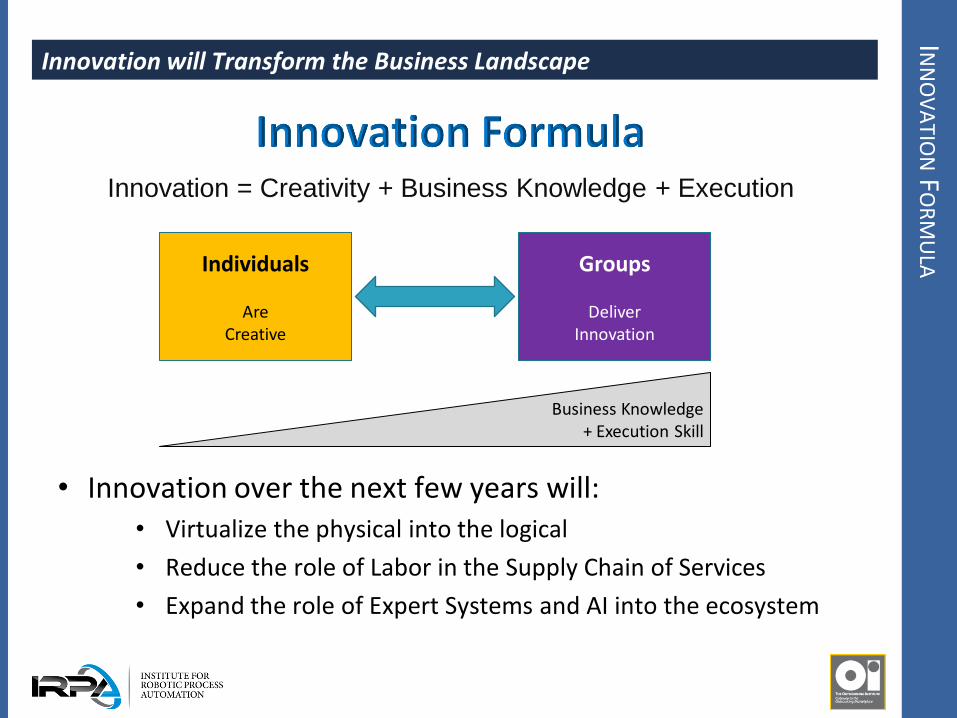

LA Innovation will Transform the Business Landscape

Individuals

Are Creative

Groups

Deliver Innovation

Business Knowledge + Execution Skill

Innovation = Creativity + Business Knowledge + Execution

• Innovation over the next few years will: • Virtualize the physical into the logical

• Reduce the role of Labor in the Supply Chain of Services

• Expand the role of Expert Systems and AI into the ecosystem

ZER

O C

ON

CEP

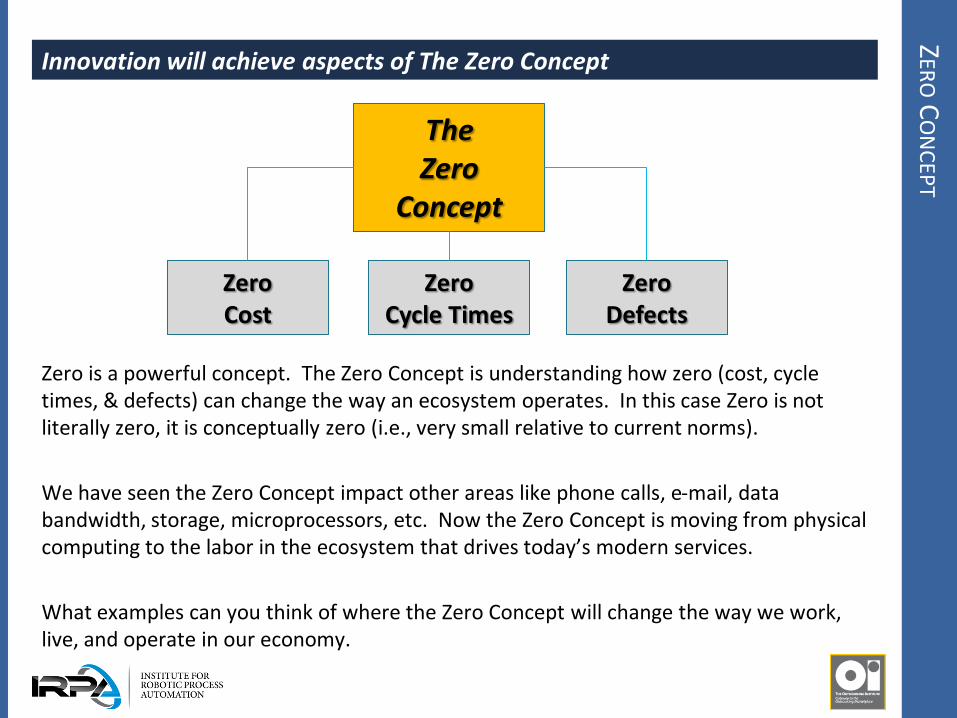

T Innovation will achieve aspects of The Zero Concept

Zero is a powerful concept. The Zero Concept is understanding how zero (cost, cycle times, & defects) can change the way an ecosystem operates. In this case Zero is not literally zero, it is conceptually zero (i.e., very small relative to current norms).

We have seen the Zero Concept impact other areas like phone calls, e-mail, data bandwidth, storage, microprocessors, etc. Now the Zero Concept is moving from physical computing to the labor in the ecosystem that drives today’s modern services.

What examples can you think of where the Zero Concept will change the way we work, live, and operate in our economy.

The Zero

Concept

Zero Cost

Zero Cycle Times

Zero Defects

AU

TOM

ATIO

N

Automation

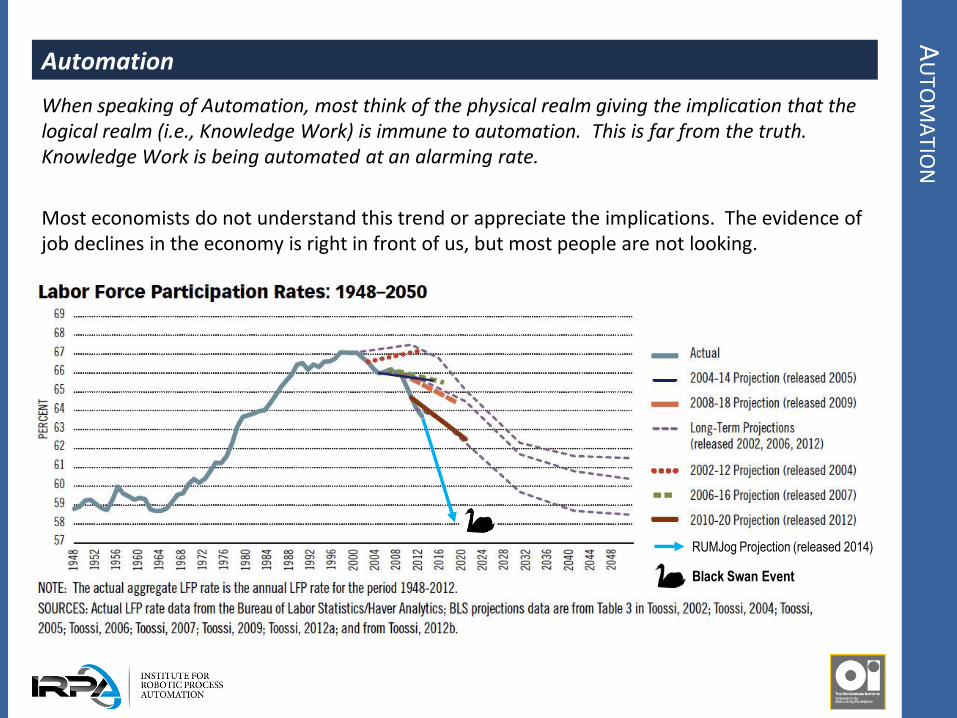

When speaking of Automation, most think of the physical realm giving the implication that the logical realm (i.e., Knowledge Work) is immune to automation. This is far from the truth. Knowledge Work is being automated at an alarming rate.

Most economists do not understand this trend or appreciate the implications. The evidence of job declines in the economy is right in front of us, but most people are not looking.

RUMJog Projection (released 2014)

Black Swan Event

CO

NC

LUSIO

N

Conclusion

• The changes that we have seen in the Technology Services markets has challenged our current business models and paradigms.

• Old playbooks are not yielding new results.

• The pace of change is accelerating, and gaps in our processes and knowledge will increase at an alarming rate.

• People need to end most of their sentences in question marks, not periods.

• All participants in the ecosystem need to be open to changing their approach to engaging in commerce.

• Collaboration, trust, and transparency are going to be foundational elements to success in an undefined future market.

• No ones knows for sure how the markets will progress, but it is safe to say that a status quo paradigm is wrong.

• Be open to change, take risk, accept failure, and ty again.

KEEP IN

FOR

MED –

STA

Y CO

NN

ECTED

Please Visit Us

www.IRPAnetwork.com

www.outsourcing.com

Tom Young [email protected]

30

Join the IRPA and OI networks to get the latest trends, expert interviews, best practices and commentary from thought leaders.

Frank Casale [email protected]

![IRPA guidance on implementation of eye dose …33FC6658-43C3-4DB4-B062...01 mai 2016 [Édition 1, volume 1] INTERNATIONAL RADIATION PROTECTION ASSOCIATION 4 IRPA GUIDANCE ON IMPLEMENTATION](https://static.fdocuments.us/doc/165x107/5ecd80276feee40e4273d82d/irpa-guidance-on-implementation-of-eye-dose-33fc6658-43c3-4db4-b062-01-mai-2016.jpg)