THIS YEAR NEXT YEAR 2018 INDIA REPORT - …bestmediainfo.in/mailer/nl/nl/TYNY_2018.pdf ·...

14

THIS YEAR NEXT YEAR 2018 INDIA REPORT

-

Upload

vuongduong -

Category

Documents

-

view

213 -

download

0

Transcript of THIS YEAR NEXT YEAR 2018 INDIA REPORT - …bestmediainfo.in/mailer/nl/nl/TYNY_2018.pdf ·...

THIS YEAR NEXT YEAR

2018 INDIA REPORT

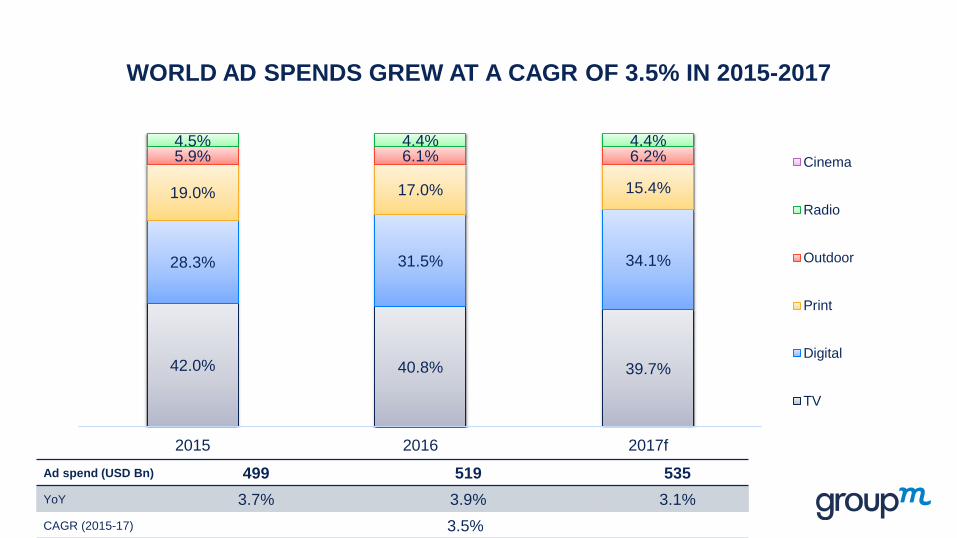

WORLD AD SPENDS GREW AT A CAGR OF 3.5% IN 2015-2017

42.0% 40.8% 39.7%

28.3% 31.5% 34.1%

19.0% 17.0% 15.4%

5.9% 6.1% 6.2% 4.5% 4.4% 4.4%

2015 2016 2017f

Cinema

Radio

Outdoor

Digital

TV

Ad spend (USD Bn) 499 519 535

YoY 3.7% 3.9% 3.1%

CAGR (2015-17) 3.5%

ASIA PACIFIC BRIDGING THE GAP WITH NORTH AMERICA

36.7% 36.5% 36.1%

32.8% 33.3% 33.6%

18.9% 18.9% 18.8%

6.7% 6.4% 6.6% 2.6% 2.7% 2.9% 2.3% 2.2% 2.0%

2015 2016 2017f

Share of World Ad Spends

MIDDLE EAST & AFRICA

CENTRAL & EASTERNEUROPE

LATIN AMERICA

WESTERN EUROPE

ASIA-PACIFIC

NORTH AMERICA

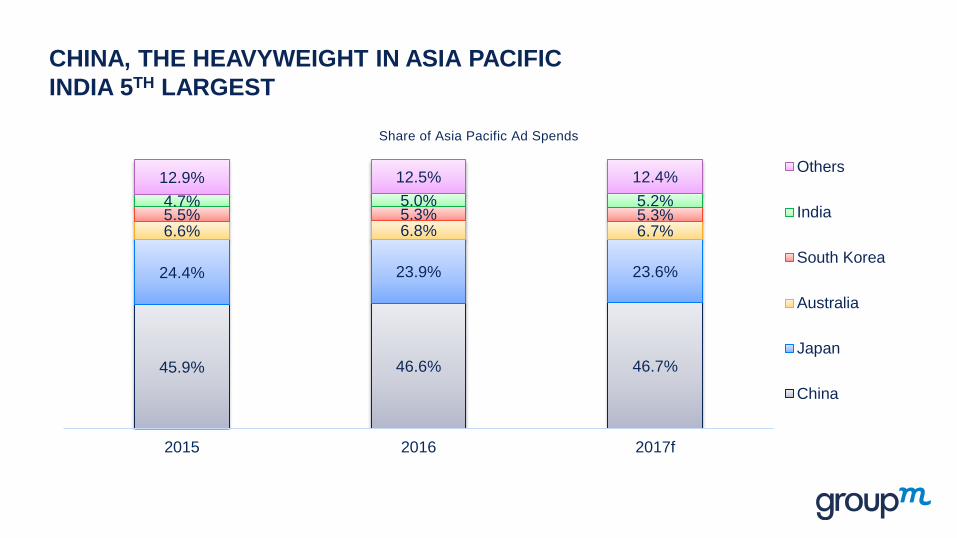

CHINA, THE HEAVYWEIGHT IN ASIA PACIFIC

INDIA 5TH LARGEST

45.9% 46.6% 46.7%

24.4% 23.9% 23.6%

6.6% 6.8% 6.7% 5.5% 5.3% 5.3% 4.7% 5.0% 5.2%

12.9% 12.5% 12.4%

2015 2016 2017f

Share of Asia Pacific Ad Spends

Others

India

South Korea

Australia

Japan

China

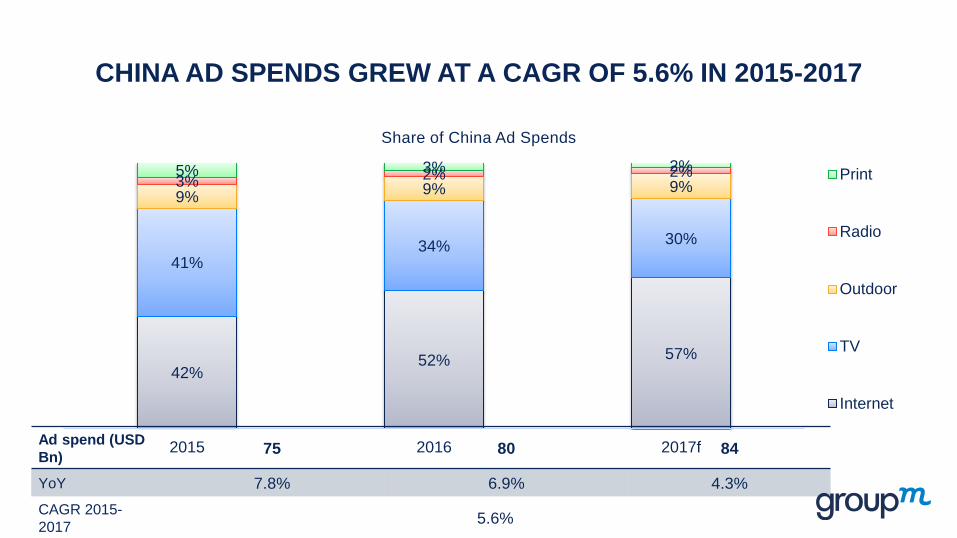

CHINA AD SPENDS GREW AT A CAGR OF 5.6% IN 2015-2017

42% 52% 57%

41% 34% 30%

9% 9% 9% 3% 2% 2% 5% 3% 2%

2015 2016 2017f

Share of China Ad Spends

Radio

Outdoor

TV

Internet

Ad spend (USD

Bn) 75 80 84

YoY 7.8% 6.9% 4.3%

CAGR 2015-

2017 5.6%

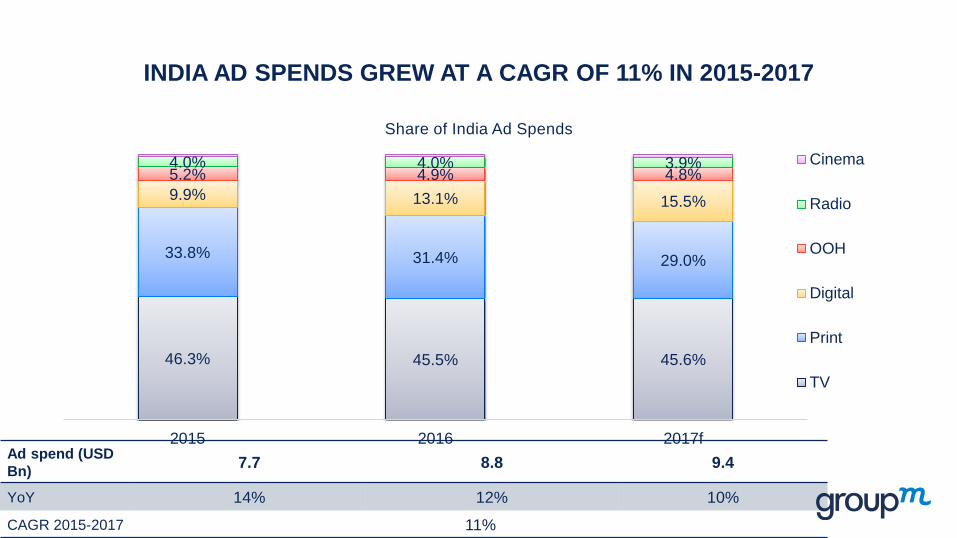

INDIA AD SPENDS GREW AT A CAGR OF 11% IN 2015-2017

46.3% 45.5% 45.6%

33.8% 31.4% 29.0%

9.9% 13.1% 15.5%

5.2% 4.9% 4.8% 4.0% 4.0% 3.9%

2015 2016 2017f

Share of India Ad Spends

Cinema

Radio

OOH

Digital

TV

Ad spend (USD

Bn) 7.7 8.8 9.4

YoY 14% 12% 10%

CAGR 2015-2017 11%

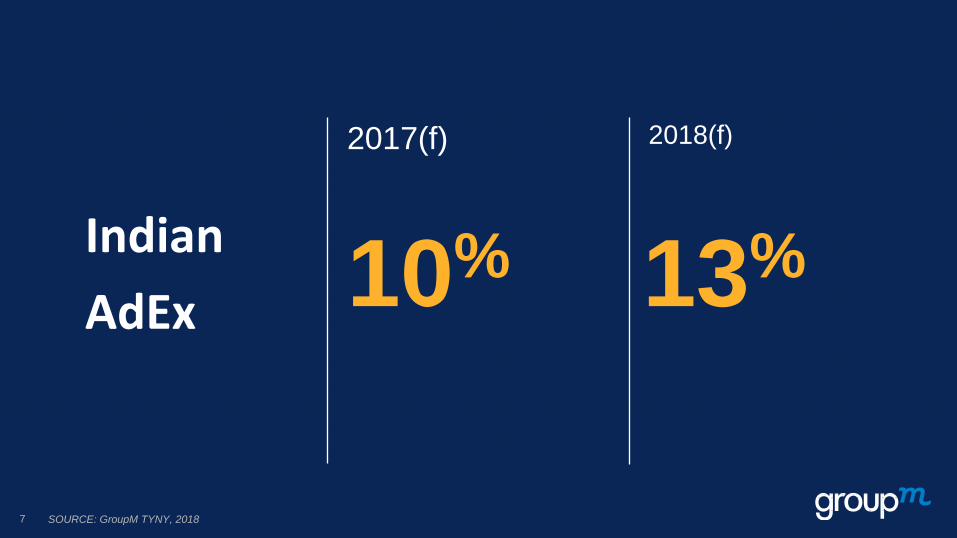

Indian

AdEx

2018(f) 2017(f)

7

10% 13%

SOURCE: GroupM TYNY, 2018

INDIAN ADEX ESTIMATED TO GROW AT 13% IN 2018

Medium 2016 2017f 2018f 17f vs 16 18f vs 17f

TV 25,350 27,961 31,596 10% 13%

Print 17,472 17,779 18,437 2% 4%

Digital 7,300 9,490 12,337 30% 30%

OOH 2,750 2,942 3,389 7% 15%

Radio 2,240 2,419 2,782 8% 15%

Cinema 560 672 806 20% 20%

All media 55,671 61,263 69,347 10% 13%

INDIA, 11TH LARGEST AD SPENDS MARKET IN 2017

SET TO BECOME 10TH LARGEST IN 2018

Medium 2017 rank 2018 rank

TV 9 8

Digital 15 15

Print 5 4

Outdoor 11 11

Radio 13 13

INDIA AMONG TOP 5 CONTRIBUTORS OF

INCREMENTAL ADEX IN 2018

Country Incremental ad spend (USD mn) Share

USA 6,274 27%

China 4,330 19%

Argentina 1,392 6%

Japan 1,292 6%

India 1,243 5%

Others (65) 8,703 37%

Total 23,234

DIGITAL SHARE OF ADEX ESTIMATED TO BE ~18% IN 2018

45.5% 45.6% 45.6%

31.4% 29.0% 26.6%

13.1% 15.5% 17.8%

4.9% 4.8% 4.9% 4.0% 3.9% 4.0%

2016 2017f 2018f

Cinema

Radio

OOH

Digital

TV

Ad spends (INR,Crs) 55,671 61,263 69,347

Ad spend (USD Bn) 8.6 9.4 10.7

YoY 12% 10% 13%

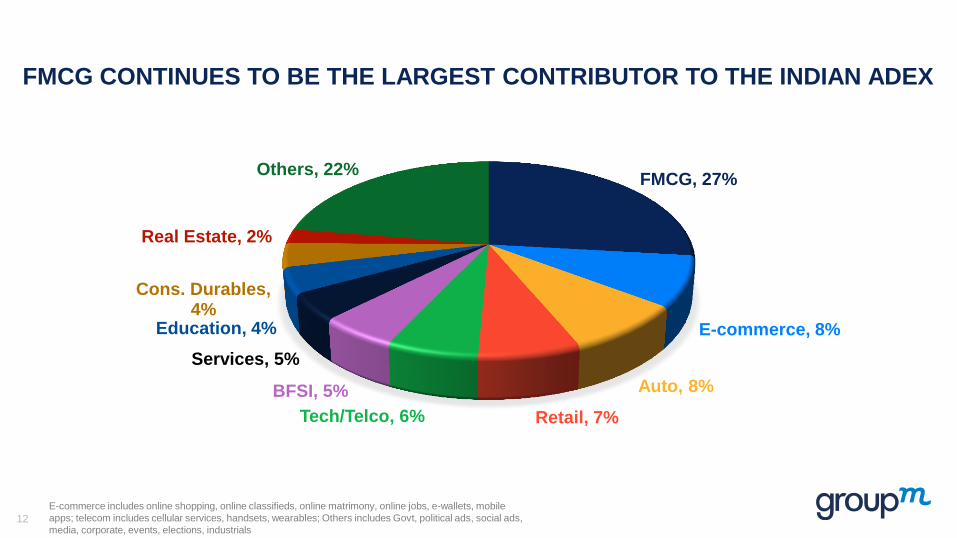

FMCG CONTINUES TO BE THE LARGEST CONTRIBUTOR TO THE INDIAN ADEX

FMCG, 27%

E-commerce, 8%

Auto, 8%

Retail, 7% Tech/Telco, 6%

BFSI, 5%

Services, 5%

Education, 4%

Cons. Durables, 4%

Real Estate, 2%

Others, 22%

E-commerce includes online shopping, online classifieds, online matrimony, online jobs, e-wallets, mobile

apps; telecom includes cellular services, handsets, wearables; Others includes Govt, political ads, social ads,

media, corporate, events, elections, industrials 12

KEY HIGHLIGHTS

• The overall ADEX in 2018 will grow by

13%

• Digital will lead the growth with a 30%

growth rate

• Besides FMCG - E-commerce, Tech/

Telcos, Auto and BFSI will be the

growth drivers in 2018

• India is a unique market where all

media have headroom to grow

• India is the fastest growing ad market

in APAC and among the fastest

growing markets in the world

13

EXCLUSIONS AND DISCLAIMERS

Media ADEX reported excludes:

• Print - tender notices, appointments, classifieds/ matrimonial

• Radio - activation spends

• Digital - ad spends by SME segment

• Outdoor - wall painting

DISCLAIMER:

All rights reserved. This publication is protected by copyright. No part of it may be reproduced, stored in a retrieval

system, or transmitted in any form, or by any means, electronic, mechanical, photocopying or otherwise, without

written permission from the copyright owners.

Every effort has been made to ensure the accuracy of the contents, but the publishers and copyright owners cannot

accept liability in respect of errors or omissions. Readers will appreciate that the data are as up-to-date only to the extent

that their availability, compilation and printed schedules will allow and are subject to change.

14