Third Quarter 2014 Global ISG Outsourcing Index

26

© 2014 Information Services Group, Inc. All Rights Reserved isg-one.com *Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase® 1 Hosted by: Moshe Katri, Cowen and Company 14 October 2014 The Global ISG Outsourcing Index Third Quarter 2014 Market Data and Insights

-

Upload

information-services-group-isg -

Category

Business

-

view

788 -

download

0

Transcript of Third Quarter 2014 Global ISG Outsourcing Index

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

1

Hosted by:

Moshe Katri,

Cowen and Company

14 October 2014

The Global ISG Outsourcing Index

Third Quarter 2014

Market Data and Insights

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

2

Covering the state of the outsourcing industry for global, commercial contracts.*

Welcome to the 48th Quarterly Outsourcing Index Review

Esteban Herrera Partner

John Keppel Partner & President

Dr. David Howie Partner

Paul Reynolds Chief Research Officer

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

3

At a Glance

Scorecard 3Q14 3Q Y/Y 3Q Q/Q ACV ($B)* Change Change

Global Market $ 4.6 -21% -28%

New Scope $ 3.0 -10% -27%

Restructurings $ 1.6 -36% -31%

Mega-relationships $ 1.1 -12% -32%

ITO $ 3.4 -23% -31%

BPO $ 1.2 -17% -18%

Americas $ 1.9 11% -17%

EMEA $ 2.4 -36% -26%

Asia Pacific $ 0.3 -27% -64%

YTD YTD ACV ($B)* Change

$ 17.1 13%

$ 10.8 22%

$ 6.3 0%

$ 4.5 24%

$ 13.0 22%

$ 4.1 -9%

$ 6.2 18%

$ 8.7 3%

$ 2.2 59%

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

4

Broader Market Quarterly ACV is down 21% Y/Y on slower contracting activity. YTD, ACV is still at the second-highest level ever, up 13% against 2013.

Year-to-date Broader Market ($B)*

Year-to-date Contracting Counts

Broader Market Contract Award Trends

660 511

631 631 528 518 408 343 332 329

239 352 252 295

235 221 227

163 141 142

-

250

500

750

1,000

201413121110090807062005

1H Counts 3Q Counts

$12.5 $9.3

$12.5 $10.2 $12.5 $10.2 $11.1 $8.7 $8.9 $9.2

$4.6 $5.9

$5.7 $6.1

$4.4 $4.3 $4.5

$3.1 $2.8 $3.9

$4.6

$5.4 $7.1 $5.6 $7.1 $4.9

$6.1 $4.5 $5.5

201413121110090807062005

$0

$5

$10

$15

$20

$25

1H ACV 3Q ACV 4Q ACV

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

5

Both ITO and BPO quarterly ACV down Y/Y. Year-to-date, ITO ACV stands at all-time high while BPO ACV has trended lower, down 9% from 2013.

BPO Year-to-date ACV ($B)*

ITO and BPO Contract Award Trends

ITO Year-to-date ACV ($B)*

BPO Year-to-date Counts

$9.6 $6.2

$7.8 $6.7 $9.5

$7.4 $7.8 $6.3 $6.6 $6.7

$3.4

$4.4 $3.7

$4.4

$3.1

$3.1 $3.1

$2.1 $1.8 $2.7

201413121110090807062005

$0

$5

$10

$151H ACV 3Q ACV

ITO Year-to-date Counts

176 184 235 231 192

154 137 115 130 105

66 104

91 110 96

75 87 55 60

50

-

100

200

300

400

201413121110090807062005

1H Counts 3Q Counts

484

327 396 400 336

364 271 228 202 224

173

248 161 185

139 146

140

108 81

92

-

100

200

300

400

500

600

700

201413121110090807062005

1H Counts 3Q Counts

$2.9 $3.0 $4.7

$3.5 $3.0 $2.8 $3.2 $2.4 $2.3 $2.4

$1.2 $1.4

$2.0 $1.7

$1.2 $1.1 $1.4 $1.0 $1.0 $1.2

201413121110090807062005

$0

$2

$4

$6

$8

1H ACV 3Q ACV

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

6

Americas quarterly ACV was up 11% Y/Y even as the number of contract awards fell back. Year-to-date, ACV is up 18% from 2013 with New Scope ACV growing 30%.

Americas Year-to-date ACV ($B)*

Americas YTD Segment Details ACV ($B)*

Americas Contract Award Trends

Americas Year-to-date Counts

265 195

278 259 239

219 168 142 149 130

97 137

104 119 101 83

84 61 49 57

-

100

200

300

400

500

201413121110090807062005

1H Counts 3Q Counts

$4.3 $3.5 $5.0

$3.7 $5.6

$4.2 $3.1 $3.4

$4.6 $3.8

$1.9 $1.7

$1.9 $2.0

$1.9

$1.9

$1.3 $0.9 $1.1 $1.8

$1.5

$1.9 $2.3

$1.1 $2.3

$1.8 $2.7 $1.7 $2.0

201413121110090807062005

$0

$2

$4

$6

$8

$10

1H ACV 3Q ACV 4Q ACV

$3.9

$2.3

$3.7

$2.5

$1

$2

$3

$4

$5

$6

New Scope Restructuring ITO BPO

Range of Prior 4 YTDs Avg of Prior 4 YTDsYTD 3Q13 YTD 3Q14

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

7

Year-to-date, U.S. ACV has risen 17% against 2013. Both Canada and Brazil ACV have advanced as a result of some larger contract awards.

Americas Contract Award Trends Detail

Americas Sub-regions Year-to-date ACV ($B)* Americas Industry YTD ACV ($B)*

$0.41

$0.27

$0.06 $0.03

$-

$0.1

$0.2

$0.3

$0.4

$0.5

$0.6

Canada Brazil Other LatAm Mexico

Range of Prior 4 YTDs Avg of Prior 4 YTDs YTD 3Q13 YTD 3Q14

$5.38

$-

$1.0

$2.0

$3.0

$4.0

$5.0

$6.0

$7.0

$8.0

U.S.

$0.91

$1.71

$0.66

$0.71

$0.46

$0.41

$0.41

$0.73

$0.16

$- $1.0 $2.0

Manufacturing

Financial Services

Telecom & Media

Healthcare & Pharma

Business Services

Retail

Consumer Products &Goods

Energy

Travel, Transport &Leisure

Avg of Prior 4 YTDs YTD 3Q14

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

8

Co. Revenues < $2 B Co. Revenues $2 -10 B

ISG Sourcing Market Standouts in the Americas Americas-based providers head up the Big 10 Sourcing Standouts. Providers with substantial offshore profiles lead in both the Building and Breakthrough tiers.

1Top 10 in region across all company sizes Placements based on ACV of commercial contract awards in the past 12 months sourced from ISG Contracts Knowledgebase®. Service providers in alphabetical order; no rankings implied. Revenues sourced from Hoovers and individual company financial fillings

The Building 10

Sourcing Standouts

The Breakthrough 10

Sourcing Standouts

CBRE Group CGI

Cognizant1 CompuCom

Genpact HCL1

Infosys1 Tech Mahindra

Teleperformance Wipro

Accenture1

BT Capgemini1

CSC1 Dell IBM1 ISS

RR Donnelley TCS1

Xerox1

Allscripts Healthcare Solutions EXL

Garda World iGATE1

KPIT Technologies Minacs Neoris

NIIT Sitel

Syntel

SOURCING STANDOUTS BY COMPANY SIZE

The Big 10

Sourcing Standouts

Co. Revenues > $10B

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

9

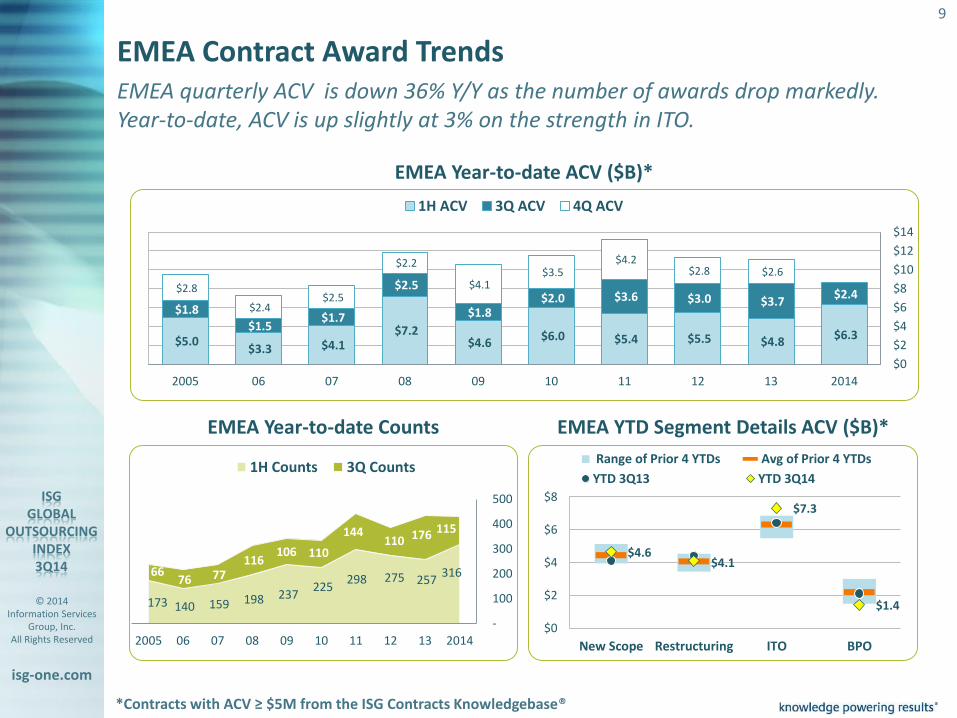

EMEA quarterly ACV is down 36% Y/Y as the number of awards drop markedly. Year-to-date, ACV is up slightly at 3% on the strength in ITO.

EMEA Year-to-date ACV ($B)*

EMEA YTD Segment Details ACV ($B)*

EMEA Contract Award Trends

EMEA Year-to-date Counts

316 257 275 298

225 237 198 159 140 173

115 176 110 144

110 106 116

77 76 66

-

100

200

300

400

500

201413121110090807062005

1H Counts 3Q Counts

$4.6 $4.1

$7.3

$1.4

$0

$2

$4

$6

$8

New Scope Restructuring ITO BPO

Range of Prior 4 YTDs Avg of Prior 4 YTDs

YTD 3Q13 YTD 3Q14

$6.3 $4.8 $5.5 $5.4 $6.0

$4.6 $7.2

$4.1 $3.3 $5.0

$2.4 $3.7 $3.0 $3.6 $2.0

$1.8

$2.5

$1.7 $1.5

$1.8

$2.6 $2.8 $4.2

$3.5 $4.1

$2.2

$2.5 $2.4

$2.8

201413121110090807062005

$0

$2

$4

$6

$8

$10

$12

$14

1H ACV 3Q ACV 4Q ACV

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

10

France and Southern Europe help support year-to-date gains in EMEA while the more mature markets of the U.K., DACH and the Nordics pull back from 2013.

EMEA Contract Award Trends Detail

EMEA Sub-regions Year-to-date ACV ($B)* EMEA Industries YTD ACV ($B)*

$2.8

$1.5 $1.3 $1.3

$0.3

$0.9

$0.4 $0.2

$-

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

U.K. &Ireland

DACH Nordics France Benelux SouthernEurope

Africa &Middle

East

E. Europe& Russia

Range of Prior 4 YTDs Avg of Prior 4 YTDs

YTD 3Q13 YTD 3Q14

$1.6

$1.9

$1.4

$1.4

$1.0

$0.5

$0.3

$0.4

$0.2

$- $1.0 $2.0 $3.0

Financial Services

Manufacturing

Travel, Transport &Leisure

Energy

Telecom & Media

Business Services

Retail

Consumer Products& Goods

Healthcare & Pharma

Avg of Prior 4 YTDs YTD 3Q14

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

11

Co. Revenues < $2 B Co. Revenues $2 -10 B

ISG Sourcing Market Standouts in EMEA Large multinationals and providers with strong local “home market” profiles head up both the Big 10 and Building 10 tiers.

1Top 10 in region across all company sizes Placements based on ACV of commercial contract awards in the past 12 months sourced from ISG Contracts Knowledgebase®. Service providers in alphabetical order; no rankings implied. Revenues sourced from Hoovers and individual company financial fillings

SOURCING STANDOUTS BY COMPANY SIZE

Co. Revenues > $10B

Capita Carillion1

Cognizant1 EVRY HCL1

Infosys1 Mitie Group

Orange Business Services Tech Mahindra

Tieto

Accenture1 Atos1 BT1

Capgemini1 CSC

Fujitsu HP

IBM1 TCS1

T-Systems

HH Global

iGATE

Innovation Group

Kelway

MAYKOR

NGA Human Resources

NNIT A/S

Quindell

Sitel

The Building 10

Sourcing Standouts

The Breakthrough 10

Sourcing Standouts

The Big 10

Sourcing Standouts

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

12

Asia Pacific quarterly ACV is down 27% Y/Y on the absence of large contract awards. Year-to-date ACV is up almost 60% on substantial contracting activity.

Asia Pacific Year-to-date ACV ($B)*

Asia Pacific YTD Segment Details ACV ($B)*

Asia Pacific Contract Award Trends

Asia Pacific Year-to-date Counts

79 59

78 74 64 62

42 42 43 26

27 39

38 32

24 32

27 25 16 19

-

20

40

60

80

100

120

140

201413121110090807062005

1H Counts 3Q Counts

$1.4

$0.8

$2.1

$0.1 $0.0

$0.5

$1.0

$1.5

$2.0

$2.5

New Scope Restructuring ITO BPO

Range of Prior 4 YTDs Avg of Prior 4 YTDs

YTD 3Q13 YTD 3Q14

$1.9 $0.9

$2.0 $1.1 $0.8

$1.4 $0.7

$1.2 $1.0 $0.4

$0.3

$0.5

$0.8

$0.5 $0.4

$0.6

$0.7 $0.5

$0.2

$0.3

$0.5

$0.6

$0.5 $1.0

$0.7

$0.9 $0.8

$0.4 $0.8

201413121110090807062005

$0

$1

$2

$3

$41H ACV 3Q ACV 4Q ACV

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

13

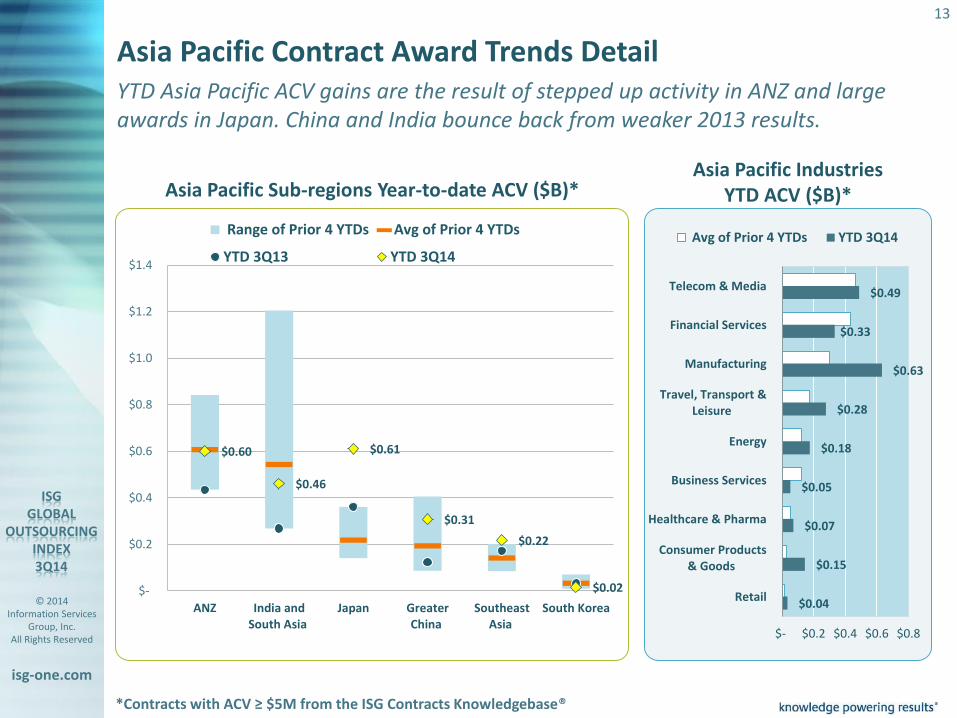

YTD Asia Pacific ACV gains are the result of stepped up activity in ANZ and large awards in Japan. China and India bounce back from weaker 2013 results.

Asia Pacific Contract Award Trends Detail

$0.60

$0.46

$0.61

$0.31

$0.22

$0.02 $-

$0.2

$0.4

$0.6

$0.8

$1.0

$1.2

$1.4

ANZ India andSouth Asia

Japan GreaterChina

SoutheastAsia

South Korea

Range of Prior 4 YTDs Avg of Prior 4 YTDs

YTD 3Q13 YTD 3Q14

Asia Pacific Sub-regions Year-to-date ACV ($B)*

$0.49

$0.33

$0.63

$0.28

$0.18

$0.05

$0.07

$0.15

$0.04

$- $0.2 $0.4 $0.6 $0.8

Telecom & Media

Financial Services

Manufacturing

Travel, Transport &Leisure

Energy

Business Services

Healthcare & Pharma

Consumer Products& Goods

Retail

Avg of Prior 4 YTDs YTD 3Q14

Asia Pacific Industries YTD ACV ($B)*

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

14

Co. Revenues < $2 B Co. Revenues $2 -10 B

ISG Sourcing Market Standouts in Asia Pacific Japanese providers join large multinationals in the Big 10 Sourcing Standouts list. Australian and India-based providers contribute greatly to the two smaller tiers.

1Top 10 in region across all company sizes Placements based on ACV of commercial contract awards in the past 12 months sourced from ISG Contracts Knowledgebase®. Service providers in alphabetical order; no rankings implied. Revenues sourced from Hoovers and individual company financial fillings

SOURCING STANDOUTS BY COMPANY SIZE

Co. Revenues > $10B

Cognizant1

HCL

Infosys1

Orange Business Services

Singtel Optus

Tech Mahindra

UGL Limited

Unisys

Wipro1

Accenture1 AT&T

Capgemini CSC1

Fujitsu1

Hitachi IBM1

NTT

TCS1

Telstra1

Aegis ChinaSoft1

Hollysys Automation Itron

Kratos Defense & Security

NGA Human Resources Pactera

Ramco

Redknee Solutions

SITA

The Building 10

Sourcing Standouts

The Breakthrough 10

Sourcing Standouts

The Big 10

Sourcing Standouts

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

15

Relative to the Commercial Sector, Public Sector ACV has grown steadily since 2009. Most ACV is generated by ITO awards, although it varies by geographic market.

Public Sector Trailing 12 Months Counts

Global Public Sector Award Trends

1,198 1,143 1,201 1,181 1,061

1,213

1,043 954 852 745

4Q13 -3Q14

4Q12 -3Q13

4Q11 -3Q12

4Q10 -3Q11

4Q09 -3Q10

Commercial Sector Public Sector

Public Sector Trailing 12 Months ACV ($B)*

$21.7

$38.8 $33.7

$30.1 $25.4 $23.4

4Q13 -3Q14

4Q12 -3Q13

4Q11 -3Q12

4Q10 -3Q11

4Q09 -3Q10

Commercial Sector Public Sector

$30.1 $26.3

$22.0 $18.4 $18.1

$8.7 $7.5 $8.1 $7.0 $5.3

4Q13 -3Q14

4Q12 -3Q13

4Q11 -3Q12

4Q10 -3Q11

4Q09 -3Q10

Public Sector ITO ACV Public Sector BPO ACV

Public Sector ITO vs. BPO TTM ACV ($B)* Public Sector Regional ITO vs. BPO % TTM ACV

86%

47%

93%

37%

14%

53%

7%

63%

U.S. & Canada U.K. ContinentalEurope

Australia

ITO BPO

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

16

$18.1 $22.6

$32.0 $31.4

4Q13 - 3Q144Q12 - 3Q134Q11 - 3Q124Q10 -3Q114Q09 - 3Q10

Commercial Sector Public Sector

4.05 4.36

3.20 4.10

69%

11% 6% 9%

4%

U.S. &Canada

U.K. ContinentalEurope

Australia Other

North America, led by U.S. Dept. of Defense, accounts for a large share of Public Sector sourcing activity followed by the U.K., Australia and Continental Europe.

Share of Public Sector ACV for Trailing 12 Months Top Public Sector Providers in Recent 12 Months*

Global Public Sector Award Trends Continued

*Service providers in alphabetical order; no rankings implied. Placements based on ACV of public sector contract awards sourced from ISG Contracts Knowledgebase ®.

BT

Capita

Carillion

CGI

HP

Interserve

Serco

Accenture

Atea

Atos

Capgemini

HP

IBM

T-Systems

Accenture

Boeing

CSC

Data#3

Fujitsu

IBM

Serco

Global Average Deal Size and Duration Compare

Avg. Duration in Yrs.

Avg. Contract Value ($K)

U.S. & Canada Australia

U.K. Continental

Europe

BAE Systems

CACI

General Dynamics

Leidos

Lockheed Martin

Northrop Grumman

SAIC

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

17

Special Topic for 3Q14

ISG MOMENTUM® METHODOLOGY FOR SOURCING OPPORTUNITIES ASSESSMENT

Paul Reynolds

Chief Research Officer

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

18

Historic vs. Potential Industry Characterization

Historical Activity Frames an Industry

$0

$1

$2

$3

2014YTD

'13'12'112010

Chemicals Oil & Gas Ops Utilities

Energy Industry ACV ($B)*

But more information is needed to Characterize the Industry Potential Momentum® Vertical Reports gauge a market’s maturity and momentum

Amount of industry business available but not yet captured

by service providers

vs U FARMING HUNTING Amount of industry growth that can be cultivated from outsourcing relationships in place

Utilities Historical Frame exhibits consistency — over $1B in ACV for past five years — within Energy, a consistent performer on pace for a record high 2014 ACV

1

Utilities Potential ISG’s 2014 Momentum Vertical Report rates Utilities as Medium Hunting and High Farming

2

WHY?

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

19

Industry Challenges local hiring requirements, heavy regulation and M&A activity impact service standardization and flexibility

Medium Hunting: Recent Growth Is Highest of 27 Verticals

$1,395 $1,612

$1,746 $1,695 $1,613

$1,824

$2,006

$3,078

$3,411 $3,340

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

US

$ M

illio

ns

Growth: 5% 16% 8% -3% -5% 13% 10% 53% 11% -2%

Utilities Market Spend (ACV)

18.5 % compound annual growth rate for outsourcing spending by Utilities clients is highest among the 27 verticals Momentum tracks

1

2

2014 Vertical Industry Report

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

20

Innovative solutions abound due to deregulation, smart grid technologies, and ongoing service efficiency needs

High Farming: Low Per-company ACV Leaves Room for Growth

2013 Utilities Average Market Spend

$66.8 $99.8

Utilities

Market Average

50 58

Outsourcing

Not Outsourcing

108 Companies

2013 Utilities Market Composition

46% Penetration Rate is in line with 47% G2000 average

1

Below Average Spend compared to G2000 in 2013

2

3

2014 Vertical Industry Report

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

21

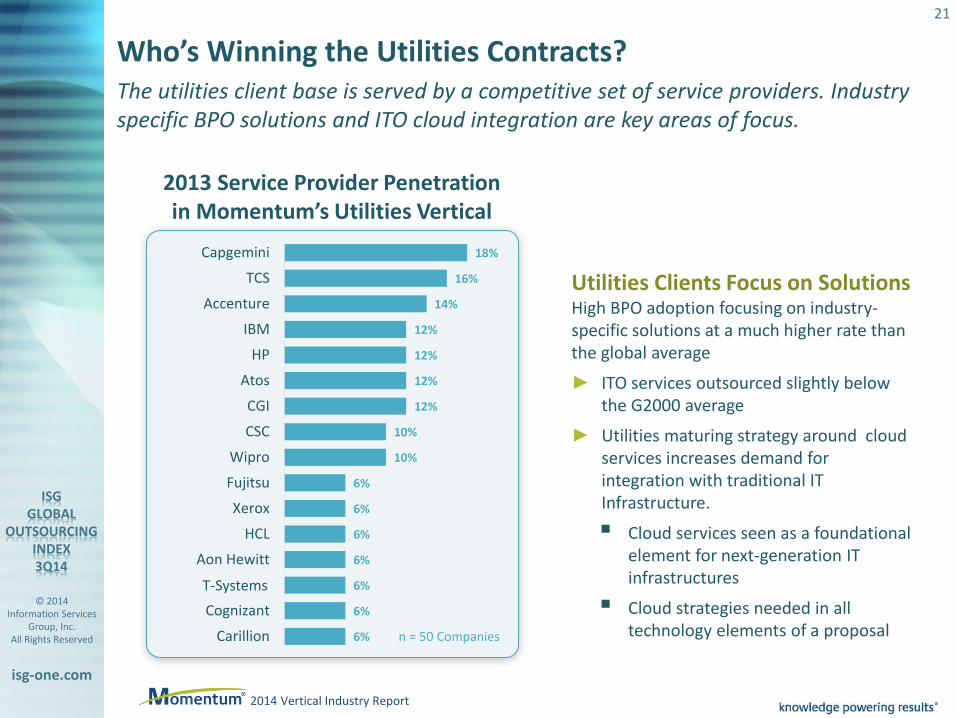

Who’s Winning the Utilities Contracts? The utilities client base is served by a competitive set of service providers. Industry specific BPO solutions and ITO cloud integration are key areas of focus.

18%

16%

14%

12%

12%

12%

12%

10%

10%

6%

6%

6%

6%

6%

6%

6%

Capgemini

TCS

Accenture

IBM

HP

Atos

CGI

CSC

Wipro

Fujitsu

Xerox

HCL

Aon Hewitt

TSystems

Cognizant

Carillion

Utilities Clients Focus on Solutions High BPO adoption focusing on industry-specific solutions at a much higher rate than the global average

► ITO services outsourced slightly below the G2000 average

► Utilities maturing strategy around cloud services increases demand for integration with traditional IT Infrastructure.

Cloud services seen as a foundational element for next-generation IT infrastructures

Cloud strategies needed in all technology elements of a proposal

2013 Service Provider Penetration in Momentum’s Utilities Vertical

n = 50 Companies

2014 Vertical Industry Report

T-Systems

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

22

As ISG forecast, Broader Market ACV lagged Y/Y on lower contract counts

Weakness across both the ITO and BPO markets, although ITO will likely surpass 2013’s results but BPO continues to yield patchy results

All regions are ahead of 2013’s pace

Americas ACV was up Y/Y as large awards in Canada and Brazil supported growth in the region

EMEA 3Q slipped as its key geographic markets pulled back; YTD sourcing activity continues to spread geographically in the continent, especially in France and Southern Europe

Asia Pacific slowed from record 1H14 as large awards were absent; YTD Australia rebounded and Japan becomes noteworthy

Expect a pickup in activity in 4Q14 as we have noticed a buildup of transaction activity likely to be awarded in next few quarters

Expect 2014 ACV to exceed 2013 by double digits, although tepid 3Q14 performance may suppress comparisons against more robust periods like the years 2010-12

3Q14 ISG Outsourcing Index Summary and Outlook

summary market

outlook market

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

23

Please contact us with your questions and comments.

Learn More

Paul Reynolds Chief Research Officer

+1 508 625 2194 [email protected]

ISG insights serving providers and market analysts

www.isg-one.com John Keppel

Partner and President +44 (0)7879 432 212

Will Thoretz Americas Media Contact

+1 203 517 3119 [email protected]

Denise Colgan EMEA and AP Media Contact

+44 1737 371523 [email protected]

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

24

Third Quarter 2014

APPENDIX: SCORE CARD FOR TCV

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

25

The ISG Outsourcing Index has moved to ACV as the primary measure of the Broader Market. In transition, we will continue to provide a high-level TCV view of the market via a Scorecard analysis.

3Q14 TCV Scorecard

*Contracts with TCV ≥ $25M from the ISG Contracts Knowledgebase®

Scorecard 3Q14 3Q Y/Y 3Q Q/Q YTD YTD

TCV ($B)* Change Change TCV ($B)* Change

Global Market $ 22.7 -9% -17% $ 76.3 15%

New Scope $ 15.7 1% -14% $ 51.1 23%

Restructurings $ 7.0 -26% -24% $ 25.3 1%

Mega-deals $ 4.9 20% -30% $ 15.1 26%

ITO $ 16.4 -12% -21% $ 56.4 27%

BPO $ 6.3 -2% -6% $ 20.0 -11%

Americas $ 10.3 66% 15% $ 27.6 32%

EMEA $ 10.9 -35% -24% $ 38.6 -1%

Asia Pacific $ 1.5 -26% -64% $ 10.1 54%

© 2014 Information Services

Group, Inc. All Rights Reserved

isg-one.com

*Contracts with ACV ≥ $5M from the ISG Contracts Knowledgebase®

26

Information Services Group is a leading technology insights, market intelligence and advisory services company, serving more than 500 clients around the world to help them achieve operational excellence. ISG supports private and public sector organizations to transform and optimize their operational environments through research, benchmarking, consulting and managed services, with a focus on information technology, business process transformation, program management services and enterprise resource planning. Clients look to ISG for unique insights and innovative solutions for leveraging technology, the deepest data source in the industry, and more than five decades of experience of global leadership in information and advisory services. Based in Stamford, Conn., the company has more than 850 employees and operates in 21 countries.

knowledge powering results®

www.isg-one.com

![ISG-600 0.37 470 0.49 790 ü]fiEñ (kWh) ISG-400 29 …...ISG-600 0.37 470 0.49 790 ü]fiEñ (kWh) ISG-400 29 ISG-600 49 DAITOËtff± 2020 TEL (022) 253 -7445 TEL (047) 395- 3335 TEL](https://static.fdocuments.us/doc/165x107/5e5d97d3470c0964465f340b/isg-600-037-470-049-790-fie-kwh-isg-400-29-isg-600-037-470-049-790.jpg)