Thiel Logistik AG - logwin-logistics.com · 2 Company Profile Business: As an external partner,...

25

Thiel Logistik AG Investor Meetings Frankfurt – August 31, 2007

-

Upload

hoangxuyen -

Category

Documents

-

view

222 -

download

0

Transcript of Thiel Logistik AG - logwin-logistics.com · 2 Company Profile Business: As an external partner,...

Thiel Logistik AGInvestor Meetings Frankfurt –August 31, 2007

1

Agenda

New Management Structure

Market and Business Profile

Financial Review and Outlook –Half-Year Results 2007

2

Company ProfileBusiness: As an external partner, Thiel Logistik AG, develops holistic logistics and service solutions for

trade and industry. Its business segments are Solutions (customer-orientated contract logisticssolutions), Air & Ocean (global air and ocean freight forwarding activities) and Road & Rail(land and special transportation activities in Central, Western and Eastern Europe).

Founded: 1985 in Luxembourg

Revenue: 1,891.4 mn. €in 2006 (+2.8% vs. 2005)

Employees: 8,500 worldwide at more than 350 sites in 43 countries

Listing: Frankfurt Stock Exchange (ISIN: LU0106198319, German SIN: 931705, TGH)

Major Shareholder: DELTON AG, Bad Homburg (50.26%)

MarketCap: Approx. 300 mn. €

Key Developments 2007§ Increase of net sales in all three business segments

§ Further improvement in operating earnings

§ With the start of the new management structure on July 1, Thiel Logistik has become an integrated logistics group

§ Targets for management teams: to enlarge strengths, resolve weaknesses, improve efficiency

3

126b

n U

S$721bn US$

209bn US$

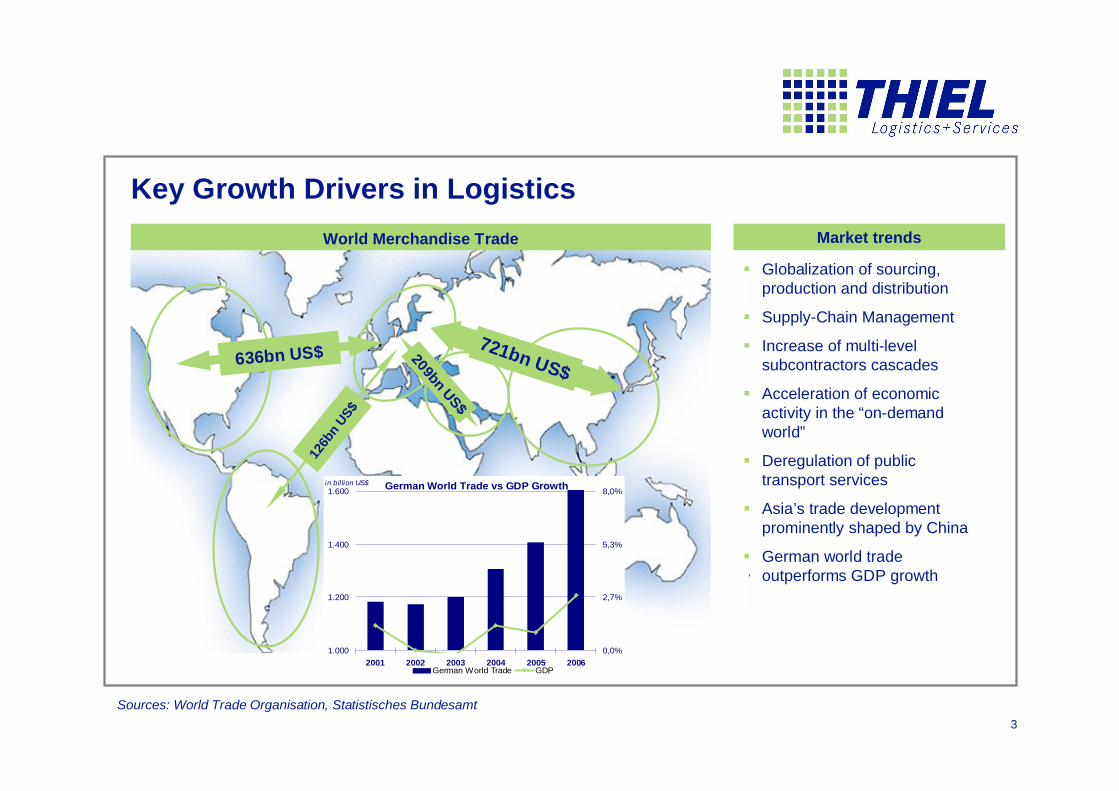

Key Growth Drivers in Logistics

Sources: World Trade Organisation, Statistisches Bundesamt

German World Trade vs GDP Growth

1.000

1.200

1.400

1.600

2001 2002 2003 2004 2005 2006

in bil lion US$

0,0%

2,7%

5,3%

8,0%

German World Trade GDP

636bn US$

World Merchandise Trade

§ Globalization of sourcing, production and distribution

§ Supply-Chain Management

§ Increase of multi-level subcontractors cascades

§ Acceleration of economic activity in the “on-demand world”

§ Deregulation of public transport services

§ Asia’s trade development prominently shaped by China

§ German world trade outperforms GDP growth

Market trends

4

Focus on Air & Ocean Expansion of Network and Growth

Key Trends Thiel Market Position

§ Organization of inter-continental air and ocean transports combined with value-added services and freight management solutions generates operating margins above 3 percent

§ Global network with 88 offices plus partner-ships

§ Member of purchasing alliances to bundle purchasing power (FUTURE, Group 99)

§ Globalization of sourcing activities continues and will increasingly be supplemented by increasing demand from emerging markets

§ Importance of and demand for intercontinental management of supply chains will increase and generate significant efficiency gains

§ High importance of container shipping for international cargo and increasing importance of air-freight market due to specific performance characteristics (e.g. short lead-times)

Thiel Strengths

§ Highly advanced IT solutions allow integrated handling of processes

§ Long-standing presence in East Asia has been developed in a lasting competitive advantage

§ Focus on medium-sized business customers mirrors own strong corporate culture with high degree of loyalty

5

Focus on SolutionsExtension and Growth

Key Trends Thiel Market Position

§ Strong market positions and expertise in selected industries based on special networks (Media, Fashion, Steel, Food)

§ Range of customer-specific solutions with highly innovative solutions (Red Bull, Subway, ZF etc.)

§ High share of asset-light business models with high level of integration into customer processes and conceptual logic

§ Specialized demand for logistics services resulting from individualization of customer needs

§ Complex solutions require high degree of reliability, reactivity and also cost efficiency

§ Co-ordination activities across the supply chains of market participants will generate significant benefits

§ Long-standing customer relations, partially resulting from successful spin-offs

§ High level of industry-specific knowledge and tools which allow back-/forward-integration in supply chains of customers

§ Special equipment and infrastructure creating additional barriers of entry (e.g. garment on hanger transportation)

§ Global link via Air & Ocean network

Seed

Raw materialTransport optimization

to manufacturerQuality control

Transport optimization

Combination of components

Deliveryto POS

Disposal

• Broker of Supply Chain• Quality control, compliance, fashion logistics• Inventory control system, POTrack, SC simulation

Manufacturer/ Producer

Processedmaterials

Thiel Strengths

6

ThielHome

regions

Sales Orientation

§ Shift of production towards Eastern Europe will continue

§ Economic growth in emerging markets will outpace Western

European growth rates

§ Demand for sophisticated logistics services and

transport connection will rise significantly

§ Thiel general network activities in Eastern Europe with unique standards and wide coverage (Top 3)

§ Long-standing Eastern European expertise with 57 sites in 14 countries

§ Establishment of an Intra-Eastern Europe network

Focus on Road & RailIntegration of Network based on strength in Eastern Europe

Key Trends Thiel Market Position

Thiel Strengths

§ Network activities serve as platform for solutions currently performed in Western Europe mainly

§ Entering new markets in former GUS

§ Cost leadership by standardization

§ Activities provide strong link in East-West traffic (road and inter-modal)

7

Agenda

New Management Structure

Market and Business Profile

Financial Review and Outlook –Half-Year Results 2007

8

Evolution of Management and Organizational Structure

until 2002 2003-2005 starting July 2007

Numerous

acquisitions in

contract logistics

and freight

forwarding

Formation of

segments based

on legal entities

Re-Organization of

segments based on

business

processes

Addition of

Centers of

Competence and

shared services

2006

9

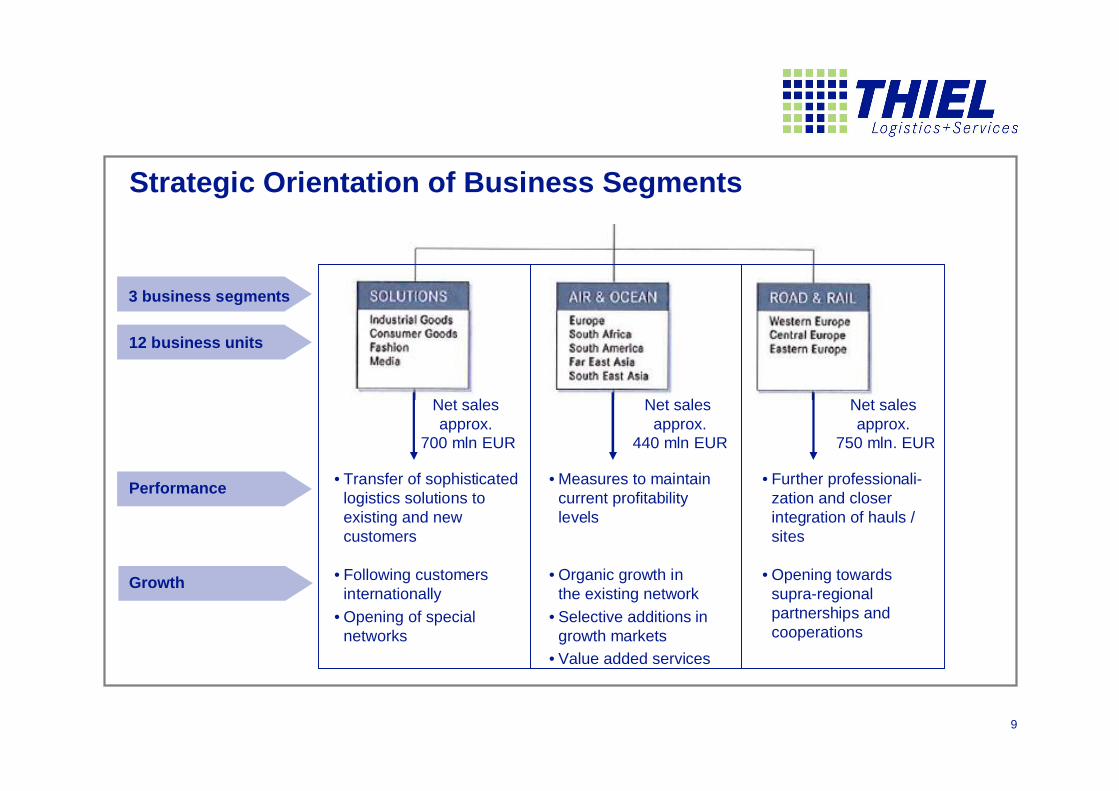

Strategic Orientation of Business Segments

•Transfer of sophisticated logistics solutions to existing and new customers

•Following customers internationally

•Opening of special networks

•Further professionali-zation and closer integration of hauls / sites

•Opening towards supra-regional partnerships and cooperations

•Measures to maintain current profitability levels

•Organic growth inthe existing network

•Selective additions ingrowth markets

•Value added services

Performance

Growth

Net sales approx.

700 mln EUR

Net sales approx.

440 mln EUR

Net sales approx.

750 mln. EUR

12 business units

3 business segments

10

Efficient and Effective Division of Tasks and Responsibilities

Responsibility to manage the Thiel Group

•Bundling of similar business processesin business segments

•Integration of alike regional and industry-oriented logistics, IT and pur-chasing processes in the business segments

Logistics services provision, innovation and professional approach towards customer solutions and land transportation

Bundling of administrative functions

11

Thiel Executive Committee

*1954

Chairman of Thiel Board of Directors since 2002;CEO of DELTON AG since 1999

Previously:Managing Director atLafarge Group and Mast-Jägermeister AG

Berndt-Michael Winter

CEO

Dr. Antonius Wagner

CFO

* 1961

Vice-Chairman of ThielBoard of Directors since 2002;CFO of DELTON AGsince 2002

Previously:Management Positions atBosch Group and LafargeGroup

Klaus Hrazdira

COO Solutions

* 1963

Executive Member ofThiel Board of Directorssince 2006;CEO of QuehenbergerGroup since 2003;

Previously:Managing Director at US Logistics GroupExpeditors

*1965

CEO of Birkart Globistics air + ocean since 2007

Previously:Regional Director Kühne + Nagel;Executive Vice President Oceanfreight Schenker

Helmut Kaspers

COO Air & Ocean

*1961

CEO of Thiel FashionLifestyle since 2006

Previously:Managing Director Birkart Globistics;Managing Director System Alliance

Detlef Kükenshöner

COO Road & Rail

12

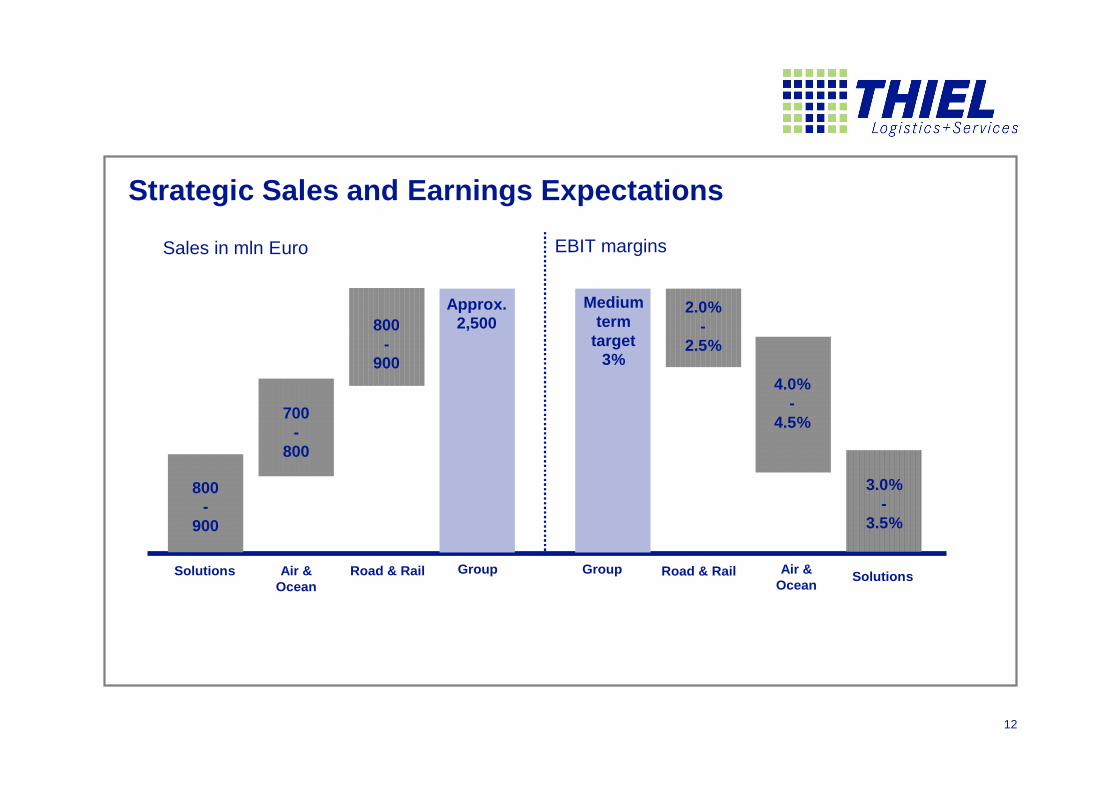

Strategic Sales and Earnings Expectations

Solutions Air & Ocean

Road & Rail Group

700-

800

Sales in mln Euro

SolutionsAir &

OceanRoad & RailGroup

4.0%-

4.5%

2.0%-

2.5%

3.0%-3.5%

EBIT margins

800-

900

800-

900

Approx.2,500

Medium term

target 3%

3.0%-

3.5%

13

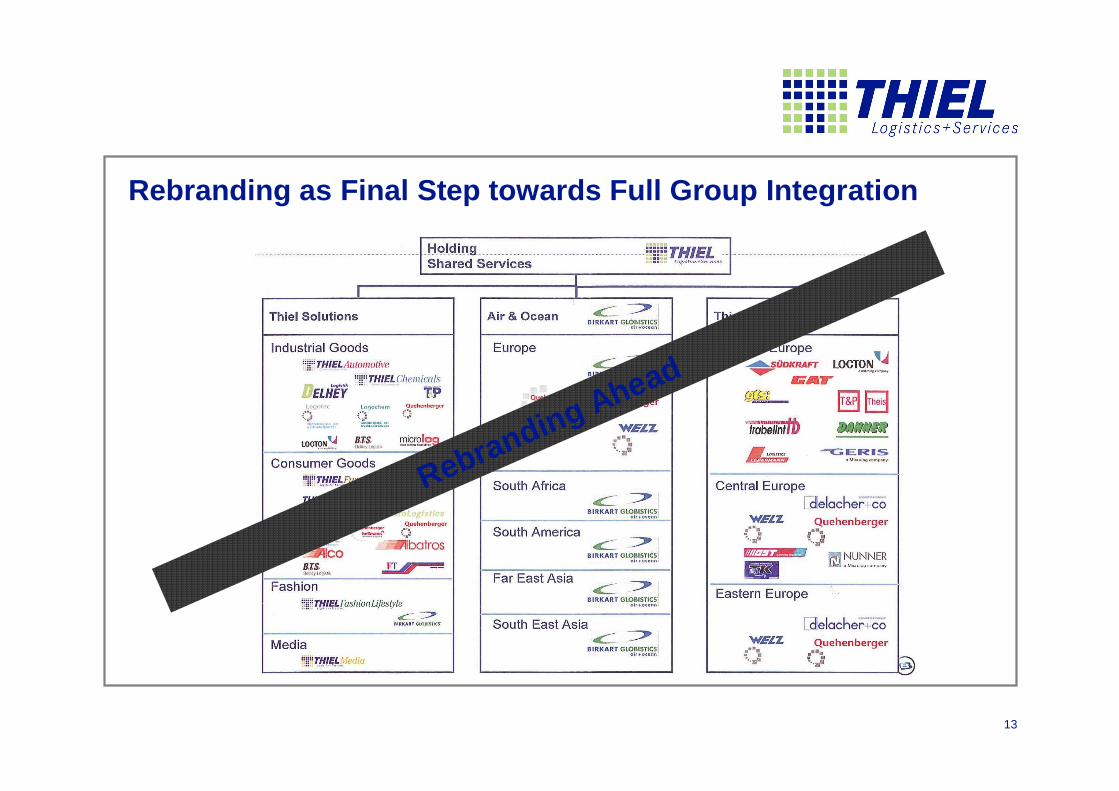

Rebranding as Final Step towards Full Group Integration

Rebranding Ahead

14

Agenda

Financial Review and Outlook –Half-Year Results 2007

Market and Business Profile

New Management Structure

15

HY 2007 –Key Financials

(EUR in million)

n/a2.7-5.1n/a6.0-9.7Operating Cash Flow

2.7

0.9

6.0

6.0 1.4%

445.1

2006

n/a-8.2n/a2.5-22.8Net Cash Flow

Cash Flow

n/a0.012.1%4.24.7Net Result

-26.3%4.5-0.1%16.416.4EBIT

-17.9%5.01.0%

9.4%16.41.8%

18.01.8%

EBIT before Restructuring CostsEBIT-Margin

Earnings

10.8%493.48.5%922.51,000.9Net Sales

Δin %2007

Δin % 20062007

Half-Year 2nd Quarter

16

HY 2007 –Sales Analysis

(EUR in million)

Net salesHY 2006

SignificantCustomer

Project Lossese.g. FAG/INA

AcquisitionsConsolidations

Additional Growth

Net salesHY 2007

-20.3

1,000.9

17.2

85.0

-3.5

Exchange Rate Effects

~~

922.5

9.2 %

17

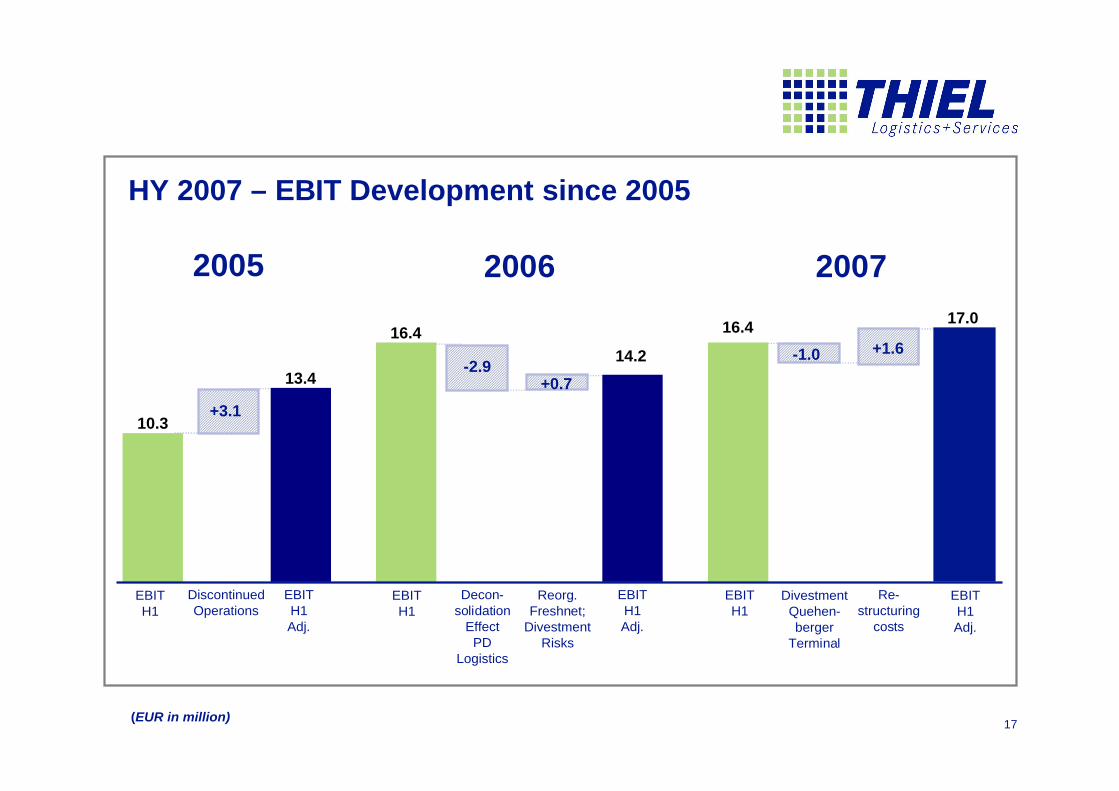

HY 2007 –EBIT Development since 2005

(EUR in million)

2005 2006 2007

EBIT H1

Decon-solidation

EffectPD

Logistics

EBIT H1 Adj.

16.4

EBIT H1

DivestmentQuehen-berger

Terminal

EBIT H1 Adj.

16.417.0

EBIT H1

EBIT H1 Adj.

10.3

DiscontinuedOperations

13.4

+3.1

-2.9+0.7

14.2

Reorg. Freshnet;

DivestmentRisks

Re-structuring

costs

-1.0 +1.6

18

HY 2007 –Segment ReportingIndustry

Solutions Air & Ocean Regional Logistics Services

(EUR in million) Proceeds from the disposal of PD Logistics (3.1 million euros)

Sales

203.7197.3

206.9

178.7

589.9546.5

500

12

10

8

6

4

Segment Result

2006 2007

4.42.5

8.06.4

8.9

11.6

2006 2007 2006 2007

20072006 2007 2006 20072006

400

300

200

100

2

600

+3.3%+15.7%

+7.9%

195.1159.5

528.8

2.34.3

9.4

2005 2005 2005

2005 2005 2005

19

HY 2007 –Income Statement

(EUR in million)

10.3%-3.9-4.38.9%-7.9-8.6Interest Expenses, net

-87.4%-1.2-0.2-26.2%-4.2-3.1Income Taxes

n/a--0.5n/a--1.6Restructuring Costs

0.9

6.01.4%

-30.2

34.2

-109.4

-301.567.7%

445.1

2006

n/a0.012.1%4.24.7Net Result

-17.9%5.01.0%

9.4%16.41.8%

18.01.8%

EBIT before Restructuring Costs% of Net Sales

7.9%-32.63.7%-61.4-63.6SG&A

6.3%36.46.6%73.878.7Gross Profit

2.8%-112.5-3.8%-233.9-224.9Other Cost of Sales

14.3%-344.569.8%

13.4%-614.866.6%

-697.369.7%

Purchased Services% of Net Sales

10.8%493.48.5%922.51,000.9Net Sales

Δin %2007

Δin % 20062007

Half-Year 2nd Quarter

20

HY 2007 –Balance Sheet

76.883.7Other Assets

278.5285.7Goodwill

223.9220.4Intangible and Fixed Assets

913.1939.2Total

270.1310.4Trade Accounts Receivable

63.839.0Cash and Cash Equivalents

FY

2006

HY

2007Assets

126.1126.3Bonds Payable

321.1325.6Shareholders’Equity

138.8149.2Other Liabilities, Provisions

238.5248.6Trade Accounts Payable

43.7

44.9

47.0

42.5

Financial LiabilitiesLeasing Liabilities

913.1939.2Total

FY

2006

HY

2007

Liabilities and

Shareholders’Equity

(EUR in million)

21

HY 2007 –Working Capital Development*

(EUR in million)

27.3

Change in Accounts

Receivable

40.3

Change in Accounts Payable

Change inInventories

Change in Other Assets

Change in Working Capital

-10.1

-6.33.4

Growth Effects

- Change in IT-Systems- Invoicing Backlogs- Reorganization

(Early Payments)

Change in Customer

Projects and in Supplier Base

* as against December 31, 2006

22

HY 2007 –Cashflow Statement

-2.4%-6.6-6.42.9%-7.1-7.3Interest Payments

-2.8

-7.9

-3.7

2.5

-3.4

-0.2

3.6

-8.7

6.0

-11.3

-4.5

33.2

2006

n/a

-73.8%

n/a

n/a

n/a

n/a

-52.7%

16.1%

n/a

n/a

29.7%

-0.6%

Δin %

-7.9

-1.5

1.7

-8.2

-3.1

-1.3

1.3

-2.8

-5.1

-7.6

-4.1

12.5

2007

-2.0

-2.1

0.1

2.7

0.0

1.1

2.6

-4.7

2.7

-0.7

-2.2

14.4

2006

n/a-22.8Net Cash Flow1)

n/a-19.9Free Cash Flow2)

-25.2%-2.1Cash Flow from Financing Activities

n/a2.8Changes in Bank Borrowings

n/a-13.1Cash Flow from Investing Activities

-4.5

1.7

-10.2

-9.7

-27.9

-5.8

33.0

2007

n/aAcquisitions

n/aOperating Cash Flow

n/aChanges in Working Capital

-50.5%Divestments

-39.6%Capital Expenditure

-89.2%Income Tax Payments

-13.2%EBITDA

Δin %

1) Net Cash Flow = Operating Cash Flow –Cash Flow from Investing Activities2) Free Cash Flow = Operating Cash Flow –Capital Expenditure

(EUR in million)

Half-Year 2nd Quarter

23

Outlook

n Continued growth trend strengthened by organic revenue increase

n Continuous EBIT improvement targeted with margin goal of three percent:

n Elimination of remaining weaknesses / restructuring (mainly Road & Rail)

n Efficient organisation and lean processes

n Shift of sales mix towards Solutions and Air & Ocean business

n Main risk to improvement in net result 2007 is the insolvency of Thiel Furniture‘s main customer Schieder Group

Thiel Logistik AGInvestor Meetings –August 31, 2007