Theshape of your super - Public Sector Superannuation ... 2011-2012 Annual... · competitive...

22

Annual Report 2011/12 of your shape The super

Transcript of Theshape of your super - Public Sector Superannuation ... 2011-2012 Annual... · competitive...

Annual Report 2011/12

of your shapeThe

super

Important note about this Annual Report

This document was prepared on 1 November 2012 by Commonwealth Superannuation Corporation (CSC).

Any financial product advice in this document is general advice only and has been prepared without taking account of your personal objectives, financial situation or needs. Before acting on any such general advice, you should consider the appropriateness of the advice, having regard to your own objectives, financial situation or needs.

You may wish to consult a licensed financial advisor.

Commonwealth Superannuation Corporation (CSC) ABN: 48 882 817 243 AFSL: 238069 RSEL: L0001397

Trustee of the Public Sector Superannuation accumulation plan (PSSap) ABN: 65 127 917 725 RSE: R1004601

The shape of your super 2011/12 3

2011/12 was CSC’s first year as trustee of the Australian Government’s nine superannuation schemes for public sector employees and Australian Defence Force personnel.

The objective of implementing the merger of the ARIA and the military (MSB) Schemes in accordance with the legislation passed by Parliament in June 2011 has been completed. A new board was established to replace the previous ARIA and MSB boards.

Significant achievements in 2011/12 included:

> a smooth transition of responsibilities to the new Board

> the establishment of Board Committees, including an Audit and Risk Management Committee and an HR Committee

> an equitable integration of the Military Super assets with those of the ARIA funds into one pooled investment trust

> the transfer of the custody of all ARIA and MSF assets now managed by CSC to a new custodian, Northern Trust

> the appointment of Peter Carrigy-Ryan as the inaugural Chief Executive Officer of CSC

> continuing work on superannuation reforms, including preparation of a MySuper product

> working with our scheme administrators on implementation of the government’s decision to transition PSSap administration from ComSuper to Pillar Administration

> preparing for the introduction of pension and salary sacrifice enhancements to the PSSap.

All of these ‘merger’ and other targets were achieved within the first twelve months, with minimum disruption to everyday business activities.

The CSC board of directors has a depth of skill, knowledge and experience that has underpinned this year of achievement. The commitment and contribution from all directors in 2011/12 has been outstanding. It is a privilege to work with such capable people. I acknowledge and thank CSC employees for their hard work and dedication during this year of change. Our major service providers, including custodians, fund managers and scheme administrators, have made a valuable contribution.

CSC now manages and invests approximately $25 billion in super on behalf of more than 600,000 members and pensioners. We expect that the scale created by the merger will enable CSC to improve long-term investment performance, reduce cost, strengthen already strong governance practices, and enhance services to members.

CSC operates in an increasingly sophisticated, regulated and competitive superannuation market. To meet these challenges, the Board has embarked on a major planning exercise, the results of which will define our key success targets and govern our priorities. Amongst other activities, the Board is reviewing CSC’s investment and member service offerings, and all governance policies and practices, with the aim of achieving the highest possible standards.

Tony Hyams AM Chairman, Commonwealth Superannuation Corporation

I am pleased to present Commonwealth Superannuation Corporation’s (CSC) Annual Report to PSSap members for the year ending 30 June 2012.

Chairman’s report

The shape of your super 2011/12 4

Member servicesDuring 2011/12, the Government’s policy decision was implemented to move the administration of member services to Pillar Administration. The changeover from ComSuper to Pillar occurred in February, and although most members experienced a smooth transition of member services, some members were adversely affected due to some data-related issues. Pillar is working to resolve these matters so as to provide full service delivery to all PSSap members.

New products for PSSap membersAs mentioned in the Chairman’s report, we will be working on changes to the PSSap to enable members to purchase an allocated pension.

MySuper update‘MySuper’ is designed to make sure that all working Australians have access to a simple, low-cost, default superannuation product. Key ‘MySuper’ details are currently being debated in government and discussed with the broader superannuation industry.

CSC will be implementing a ‘MySuper’ option in the PSSap. We will keep you up to date with any changes and what they may mean for you.

What’s happening

Changes to superannuation in the Federal Budget 2012The following changes were announced in the 2012/13 Budget delivered by the Treasurer, The Hon. Wayne Swan.

Higher tax for very high income earnersFrom 1 July 2012, individuals with an income greater than $300,000 will effectively be paying tax on their concessional superannuation contributions at 30% rather than the current 15%. The definition of ‘income’ for the purpose of this measure will include taxable income, concessional superannuation contributions, adjusted fringe benefits, total net investment loss, target foreign income, tax-free government pensions and benefits (less child support). We will provide further information on the PSSap website on the detail of this measure when it becomes available.

Contribution caps have changedFrom 1 July 2012, the concessional contribution cap for all Australians will be $25,000 per annum. For PSSap members, this includes the 15.4% employer contributions made on your behalf and any contributions made via salary sacrifice. For PSSap members with a salary for superannuation purposes of $162,338 or more, the PSSap employer contributions would exceed the concessional cap, and you may wish to contact your employer about strategies to stay within the cap.

The shape of your super 2011/12 5

The PSSap is an accumulation fund. The money that you and your employer contribute to your super earns investment returns and accumulates over time. This means the more you can contribute now, the more you should have to enjoy life after work.

How do I benefit from the PSSap?The PSSap is a competitive super fund. We offer members:

> at least 15.4% employer contributions

> competitive returns

> comprehensive insurance cover

> competitive fees, which your employer also helps with

> access to low-cost home loans and banking services through ME Bank.

In addition to these benefits, the PSSap is a smart choice, because all benefits after fees, expenses and taxes are returned to members and we don’t pay any commissions to financial advisors.

How is my PSSap super invested?We pool your super with that of other PSSap members as well as members of the CSS, PSS and MSBS. It goes into a pooled superannuation trust, and we then invest it according to the investment options you choose.

Your super in focus

The shape of your super 2011/12 6

What are my investment options?The PSSap offers a range of investment choices, and you can mix and match these to find a balance that is right for you. You can also switch investment strategies at any time. Just visit the Product Disclosure Statement and the Investment & performance sections at www.pssap.gov.au.

If you haven’t made an investment choice, your super will be invested in the PSSap’s Trustee Choice option. The investment strategy for this option is to spread investments over a number of asset classes, to maximise the long-term real return on contributions while reducing short-term risks to a level we consider prudent.

How is my PSSap super valued?Your PSSap super is valued in units. We use your employer and personal contributions, along with any other amounts you transfer in, to buy units in the investment options you choose.

We keep a record of all the units you hold, and call this your super account. You can estimate the value of your account on any business day by multiplying the number of units you hold in each investment option on that day, by the relevant ‘sell’ unit price for that day. Alternatively, you can view your up-to-date withdrawal benefit using Member Online services.

You’ll need an access number to use this service. If you don’t have one or you’ve misplaced it, call us on 1300 725 171 and we can give you one over the phone.

Unit prices fluctuate in line with investment returns, and the net earnings of the fund are reflected in the price of your units. Generally, unit prices are available on our website each business day.

Fees, expenses, costs and taxes are usually deducted before we calculate the unit price. Some fees, such as insurance premiums and switching fees, need to be paid out of your account, so we sell units to cover the cost of these fees as they arise.

How are unit prices calculated?To work out the unit price for an investment option, we take the total value of assets in the investment option (less fees not deducted directly from your super account, as well as taxes and costs) and divide it by the number of units issued in the investment option. The costs associated with buying or selling fund investments are reflected in the unit price for the relevant investment option through a ‘buy-sell’ spread.

Generally, we base our calculation of the value of assets in each investment option on the latest available market value at the end of each business day. Using these values, we will generally calculate the unit price for a given business day on the next business day. For example, we will generally calculate the unit price for 1 September (if a business day) and make it available on 2 September (if also a business day).

If we can’t determine a unit price for a business day on the following business day due to an unforeseeable event (such as a trading suspension in relevant markets), we take all reasonable steps to make a determination as soon as possible after that day.

The shape of your super 2011/12 7

For more information about AUSfund, including a copy of its product disclosure statement, call 1300 361 798, visit www.unclaimedsuper.com.au or write to:

AUSfund PO Box 2468 Kent Town SA 5071

In accordance with superannuation law, we’ll pass on any personal information required by AUSFund to establish your account.

Eligible rollover fundIf you become a lost member, we may move your super to an eligible rollover fund (ERF).

To be considered a lost member, you must have joined the PSSap more than two years ago, and:

> had no contributions or transfers made to your account in the last five years (meaning that you are an inactive member), or

> have changed address without telling us or we have been unable to contact you.

If you become a lost member, we may move your super to an ERF. The fund we use is AUSfund, Australia’s Unclaimed Super Fund. If your super is moved to AUSfund, a number of things will happen:

> your PSSap membership and insurance cover will cease

> you’ll become a member of AUSfund and be subject to its governing rules

> you’ll need to apply directly to AUSfund to access your benefit

> you won’t be able to make contributions to AUSfund

> you’ll have no investment choice, and the trustee of AUSfund will nominate your investment strategy

> AUSfund will attempt to ensure your benefit isn’t eroded by fees and charges, but some fees and charges may apply.

The shape of your super 2011/12 8

2011/12 investment performance summaryIn the 2011/12 financial year, the PSSap Trustee Choice option posted a net return of 2.4%. The fund’s diversified exposures to real assets, active strategies and fixed income preserved capital in an environment of flat to falling listed equity markets. This return represented first quartile performance versus peer superannuation funds over the financial year.

Weaker global demand, continued default risk in Europe, and particular concerns about low Chinese demand for Australia’s raw materials, drove declines in listed equity markets around the world. The listed Australian equity market fell by 7%; international developed-world markets fell 1.5% (on a hedged basis), with significant dispersion in country performance; and emerging-region equity indices fell by over 12%.

These same factors contributed to capital gains on yield assets. CSC holds Australian government bonds, which returned 13% over the financial year; corporate credit, which returned 12%; and unlisted property, which rose 8.8%. CSC’s active investment strategies returned between 5% and 16% over the same period. These gains helped to offset the material drag from listed equity markets.

The Conservative and Balanced investment options returned 5.3% and 5.0%, respectively, over the financial year. This performance was driven by these funds’ higher exposure to yield assets and lower exposure to listed equity markets. By comparison, the Aggressive investment option, which has a higher allocation to equity markets, for their potential longer-term capital growth, rose by just 0.9% over the shorter, financial year term.

The best single asset class option performance in 2011/12 was achieved by the Government Bonds option (previously ‘Fixed Interest’), which rose by 12.9%. The Property option recorded a solid gain of 8.8%, while the Cash option gained 3.9%.

The Australian Shares and Sustainable options recorded significant negative returns of -6.9% and -7.9%, respectively, while the two international share options declined by 1.5% (unhedged) and 2.0% (hedged). In the seven years since inception, the highest single asset class option return was achieved by the Property option, which rose by 8.2% per annum.

Investments

The shape of your super 2011/12 9

PSSap’s comparison to SuperRatings all-fund median

Funds under investment management for the total fund ($m)

30 June 2011 30 June 2012

2,761 3,549

Investment option performance summary

Investment option 1 year to 30 June 2012 5 years to 30 June 2012

Trustee Choice 2.4% 0.2%

Conservative 5.3% 3.2%

Balanced 5.0% 2.3%

Aggressive 0.9% -1.0%

Cash 3.9% 4.4%

Government bonds 12.9% 4.5%

Australian shares -6.9% -3.2%

International shares (unhedged) -1.5% -5.7%

International shares -2.0% -5.7%

Property 8.8% 5.6%

Sustainable -7.9% -4.2%

All returns are calculated as the compound average rate of earnings after fees and taxes. Be aware that long-term performance figures outlined above are for the investment options as a whole, and are not your personalised investment returns in PSSap.

Note: Super is a long-term investment, and past performance is no indication of future performance – investment markets are volatile, and it is not possible to predict when they will go up or down, or how quickly it will happen.

PSSap Trustee Choice

SuperRatings SR50 Balanced

Difference

The rate of return is annualised, both for the three years and five years ending June 2012.

0.07%

0.06%

0.05%

0.04%

0.03%

0.02%

0.01%

0.0%

-0.01%5 Year Rolling3 Year Rolling

The shape of your super 2011/12 10

Before you changeTake the time to understand your options, taking your personal objectives, financial situation and needs into account. See Investment option performance on page 14 where you’ll find information on the investment objectives, strategies, investor suitability, investment timeframes and risk levels for all of these investment options. In addition to reviewing this information, you may wish to consider:

1. What is your investment timeframe? How long do you plan to invest your money before withdrawing it for retirement?

2. What level of investment performance are you hoping for? If you’re looking for a higher return, you’ll need to be willing to accept a greater degree of volatility.

3. What level of risk are you willing to tolerate? Different investment options carry different levels of risk, and you’ll need to decide which level you’re comfortable with.

Higher-risk investment options can potentially deliver a higher return for your investment over the long term, but you will need to be comfortable with higher levels of volatility and periods of negative returns. If you are this type of investor, you will tend to have a long investment time horizon.

Moderate-risk investment options can potentially deliver a higher return on your investment over the medium term, but you will need to be comfortable with moderate levels of volatility and some negative returns.

Low-risk investment options may be suitable if you don’t like risk or are planning to access your super in the near future.

The PSSap Product Disclosure Statement available at www.pssap.gov.au outlines further information on the investment options and the risk measures used to describe these options. You may also wish to get advice from a licensed financial advisor.

Changing investment strategies: making the right choiceYou can choose how your super is invested by selecting from one of the PSSap’s 11 investment options listed below, or you can choose to mix and match them. You can even invest your existing balance one way, and have all your future contributions invested another. The right investment strategy for you will depend upon your personal goals, financial situation and plans for the future.

Pre-mixed options – we take care of the investment mix for you

Individual asset classes – you choose the right mix

We invest these options across a range of different asset classes, such as Australian shares, fixed interest and property. Each option carries a different level of risk.

If you want to choose your own mix of investments, then these single-sector options may suit you best.

Trustee Choice Cash

Conservative Government bonds

Balanced Australian shares

Aggressive International shares (unhedged)

International shares

Property

Sustainable

The shape of your super 2011/12 11

Making the switch If you decide you’d like to change your investment strategy, you can log on to Member Online, download an Investment choice form at www.pssap.gov.au, or call 1300 725 171.

You can make two free investment choice switches in each financial year; a fee of $20 will apply for each additional switch.

Once you’ve changed your investment strategy, you should keep a close eye on your investments to see if you have made the right choice for you, particularly if you’ve created your own portfolio using individual asset-class options.

The shape of your super 2011/12 12

CSC works with leading investment managers to make sure that your super is well managed.Our policy on derivativesInvestment managers who enter into an investment management agreement with CSC may use derivative securities (known as derivatives) to facilitate increases or decreases in the fund’s exposure to different investment markets. Derivatives are financial instruments whose value changes in response to the changes in underlying variables. Examples include futures, options and forward exchange contracts.

Derivatives within investment mandates are mainly used to reduce risk for you. Our investment managers are not permitted to use derivative securities for gearing the fund or any part of the fund, or for placing the fund in a position where it is short an asset class.

The investment mandates we grant to our investment managers, allowing them to use derivatives, reflect the policy for the fund as a whole. If CSC’s investment managers are permitted to use derivative securities, the limits will be clearly set out in the mandate. CSC’s internal investment team (and custodian) monitor whether derivative use is consistent with CSC’s policy.

If you would like more information about our derivatives policy, call CSC on 02 6263 6999.

PSSap Trustee Choice investment managers 2011/12:

> Alleron Investment Management Limited

> Anchorage Capital Offshore Fund Limited

> Arcadia Funds Management Limited

> Aurora Investment Management LLC

> Balanced Equity Management Pty Limited

> Bridgewater Associates, Inc

> Brigade Leveraged Capital Structures Offshore

> Colchester Global Investors Limited

> Dexus Property Group Limited

> Eureka Funds Management Company

> GMO Australia Limited

> Graham Global Investment Fund Limited

> Gruss Global Investors Limited

> Integrity Investment Management Limited

> JCP Investment Partners Limited

> Lend Lease Real Estate Investments Limited

> Loomis Sayles & Company LP

> Luxor Capital Partners Offshore Limited

Investment managers

The shape of your super 2011/12 13

> Macquarie Investment Management Limited

> Marathon Asset Management Limited

> Marvin & Palmer Associates Inc

> Orbis Investment Management Limited

> Paradice Investment Management Limited

> Pharo Macro Fund Limited

> PIMCO Australia Pty Ltd

> Platinum Asset Management

> Rogge Global Partners PLC

> Schroder Investment Management Australia Limited

> Solaris Investment Management Limited

> State Street Global Advisors Limited

> Steadfast International Limited

> Stone Harbor International Partners LP

> Vanguard Investments Australia Limited

> Wellington International Management Company Pte Limited

> Winton Futures Fund Limited

The shape of your super 2011/12 14

Trustee Choice

Investment objective

To outperform the Consumer Price Index (CPI) by 4.5% per annum over the medium to long term.

Investment strategy

The strategic asset allocation of the Trustee Choice option is designed to invest in different types of investments that tend to perform independently of each other. By embracing the benefits of diversification, the default fund tries to reduce its reliance on equity market returns and therefore provide a smoother pattern of long-term returns.

Fund performance The Trustee Choice investment option returned 2.4% after tax and fees in 2011/12.

Investment return (after tax and fees)

2007/08 -2.0%

2008/09 -13.8%

2009/10 8.9%

2010/11 7.3%

2011/12 2.4%

Five year compound annual return: 0.2%

Trustee Choice (cont.)

Minimum time frame

Five to seven years

Risk level Medium to high (band five)

Investor suitability It may be suitable for those prepared to take more risk in exchange for potentially higher returns on their investment over the medium to long term, and who are comfortable with moderate to high levels of volatility and periods of negative return.

Asset allocation Asset 30 June 11 30 June 12

Australian equity 26.5% 23.0%

International equity 28.6% 28.6%

Long/short equity funds 1.8% –

Real assets 12.8% 14.6%

Alternatives 13.9% 16.0%

Fixed income 11.6% 14.0%

Cash 4.8% 3.8%

Pre-mixed investment options

Investment option performance

The shape of your super 2011/12 15

Balanced

Investment objective

To outperform the Consumer Price Index (CPI) by 4% per annum over the medium-to-long term.

Investment strategy

The strategic asset allocation of the Balanced investment option is designed to maximise the benefits of diversification within the constraint of having a balance between growth and defensive assets.

Fund performance

The Balanced investment option returned 5.0% after tax and fees in 2011/12.

Investment return (after tax and fees)

2007/08 0.6%

2008/09 –8.6%

2009/10 9.0%

2010/11 6.7%

2011/12 5.0%

Five year compound annual return: 2.3%

Minimum time frame

Five to seven years

Risk level Medium (band four)

Investor suitability

It may be suitable for those prepared to take more risk in exchange for potentially higher returns on their investment over the medium term, and who are comfortable with moderate levels of volatility and periods of negative return.

Asset allocation Asset 30 June 11 30 June 12

Australian equity 15.8% 15.8%

International equity 14.7% 18.5%

Long/short equity funds 4.0% –

Real assets 11.9% 12.0%

Alternatives 19.9% 19.7%

Fixed income 23.8% 24.0%

Cash 9.9% 10.0%

Conservative

Investment objective

To outperform the Consumer Price Index (CPI) by 3% per annum over the medium-to-long term.

Investment strategy

The strategic asset allocation of the Conservative investment option is designed to maximise the benefits of diversification within the constraint of having a range of 20–30% exposure to growth assets and having no exposure to alternative strategies considered inappropriate for a conservative strategy.

Fund performance

The Conservative investment option returned 5.3% after tax and fees in 2011/12.

Investment return (after tax and fees)

2007/08 0.8%

2008/09 –4.2%

2009/10 8.3%

2010/11 6.4%

2011/12 5.3%

Five year compound annual return: 3.2%

Minimum time frame

Three years

Risk level Low to medium (band three)

Investor suitability

It may be suitable for those who prefer to take less risk and/or need to access their super in the near future.

Asset allocation Asset 30 June 11 30 June 12

Australian equity 12.2% 12.1%

International equity 9.2% 9.0%

Long/short equity funds – –

Real assets 6.0% 6.0%

Alternatives – –

Fixed income 42.7% 42.9%

Cash 29.9% 30.0%

The shape of your super 2011/12 16

Cash

Investment objective

Before the payment of tax, to match the return from the UBS Australian Bank Bill Index.

Investment strategy

The Cash option offers you the ability to invest your super in a diversified portfolio of cash investments, including bank deposits, Australian-dollar-denominated money market securities, and interest rate futures and options traded on the Australian Securities Exchange. This allows the Cash option to capture the returns generated by the Australian cash market.

Fund performance

The Cash investment option returned 3.9% after tax and fees in 2011/12.

Investment return (after tax and fees)

2007/08 5.9%

2008/09 4.5%

2009/10 3.4%

2010/11 4.2%

2011/12 3.9%

Five year compound annual return: 4.4%

Minimum time frame

One year

Risk level Very low (band one)

Investor suitability

It may be suitable for those who prefer to take less risk and/or need to access their super in the near future.

Asset allocation 100% cash

Aggressive

Investment objective

To outperform the Consumer Price Index (CPI) by 5% per annum over the medium to long term.

Investment strategy

The strategic asset allocation of the Aggressive investment option is designed to maximise the benefits of diversification within the constraint of having a range of 75–85% exposure to growth assets.

Fund performance

The Aggressive investment option returned 0.9% after tax and fees in 2011/12.

Investment return (after tax and fees)

2007/08 –5.2%

2008/09 –16.8%

2009/10 11.0%

2010/11 7.9%

2011/12 0.9%

Five year compound annual return: –1.0%

Minimum time frame

Six years

Risk level High (band six)

Investor suitability

It may be suitable for those prepared to take more risk in exchange for potentially higher returns on their investment over the long term, and who are comfortable with higher levels of volatility and periods of negative return.

Asset allocation Asset 30 June 11 30 June 12

Australian equity 37.5% 37.6%

International equity 30.9% 30.7%

Long/short equity funds – –

Real assets 14.8% 14.9%

Alternatives 7.9% 7.8%

Fixed income 5.9% 6.0%

Cash 3.0% 3.0%

Individual asset class investment options

The shape of your super 2011/12 17

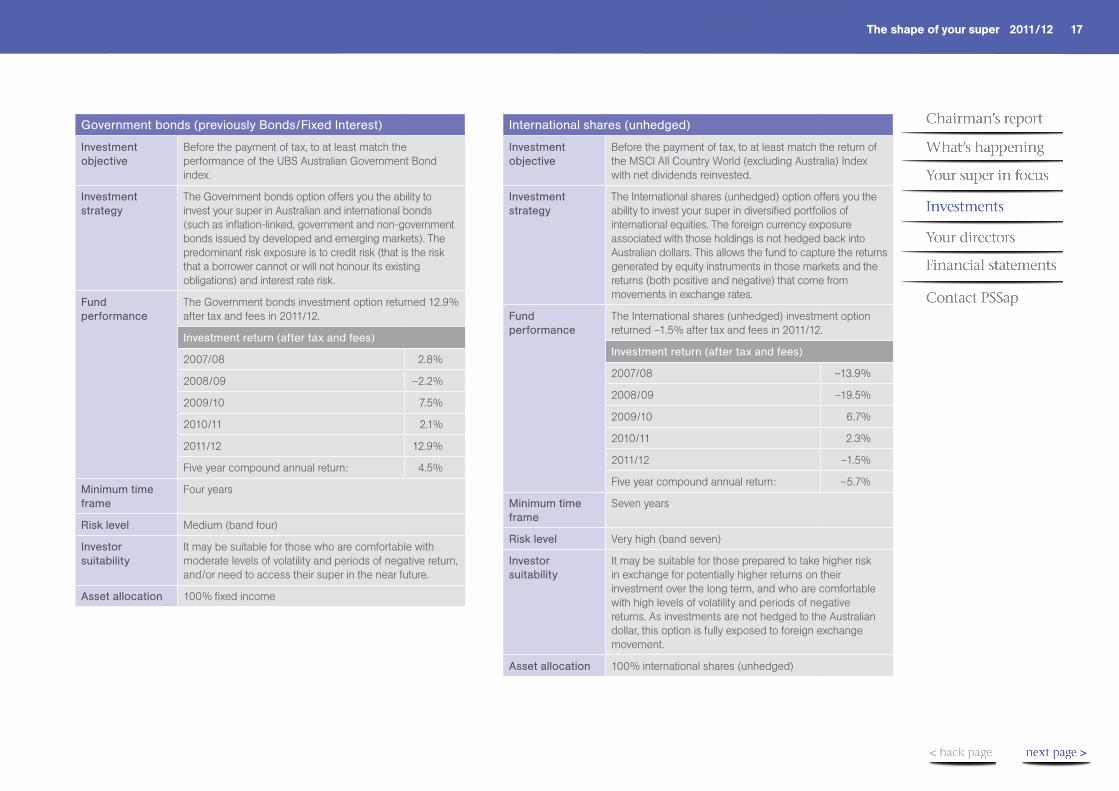

International shares (unhedged)

Investment objective

Before the payment of tax, to at least match the return of the MSCI All Country World (excluding Australia) Index with net dividends reinvested.

Investment strategy

The International shares (unhedged) option offers you the ability to invest your super in diversified portfolios of international equities. The foreign currency exposure associated with those holdings is not hedged back into Australian dollars. This allows the fund to capture the returns generated by equity instruments in those markets and the returns (both positive and negative) that come from movements in exchange rates.

Fund performance

The International shares (unhedged) investment option returned –1.5% after tax and fees in 2011/12.

Investment return (after tax and fees)

2007/08 –13.9%

2008/09 –19.5%

2009/10 6.7%

2010/11 2.3%

2011/12 –1.5%

Five year compound annual return: –5.7%

Minimum time frame

Seven years

Risk level Very high (band seven)

Investor suitability

It may be suitable for those prepared to take higher risk in exchange for potentially higher returns on their investment over the long term, and who are comfortable with high levels of volatility and periods of negative returns. As investments are not hedged to the Australian dollar, this option is fully exposed to foreign exchange movement.

Asset allocation 100% international shares (unhedged)

Government bonds (previously Bonds/Fixed Interest)

Investment objective

Before the payment of tax, to at least match the performance of the UBS Australian Government Bond index.

Investment strategy

The Government bonds option offers you the ability to invest your super in Australian and international bonds (such as inflation-linked, government and non-government bonds issued by developed and emerging markets). The predominant risk exposure is to credit risk (that is the risk that a borrower cannot or will not honour its existing obligations) and interest rate risk.

Fund performance

The Government bonds investment option returned 12.9% after tax and fees in 2011/12.

Investment return (after tax and fees)

2007/08 2.8%

2008/09 –2.2%

2009/10 7.5%

2010/11 2.1%

2011/12 12.9%

Five year compound annual return: 4.5%

Minimum time frame

Four years

Risk level Medium (band four)

Investor suitability

It may be suitable for those who are comfortable with moderate levels of volatility and periods of negative return, and/or need to access their super in the near future.

Asset allocation 100% fixed income

The shape of your super 2011/12 18

Australian shares

Investment objective

Before the payment of tax, to at least match the performance of the ASX 300 Accumulation Index.

Investment strategy

The Australian shares option offers you the ability to invest your super in diversified portfolios of Australian equities. This allows the fund to capture the returns generated by Australian companies listed on the Australian Securities Exchange.

Fund performance

The Australian shares investment option returned –6.9% after tax and fees in 2011/12.

Investment return (after tax and fees)

2007/08 –14.5%

2008/09 –14.6%

2009/10 13.1%

2010/11 10.3%

2011/12 –6.9%

Five year compound annual return: –3.2%

Minimum time frame

Seven years

Risk level Very high (band seven)

Investor suitability

It may be suitable for those prepared to take higher risk in exchange for potentially higher returns on their investment over the long term, and who are comfortable with high levels of volatility and periods of negative returns.

Asset allocation 100% Australian shares

International shares

Investment objective

Before the payment of tax, to at least match the return of the MSCI All Country World (excluding Australia) Index with net dividends reinvested and a currency hedging ratio determined by the Trustee.

Investment strategy

The International shares option offers you the ability to invest your super in diversified portfolios of international equities. The foreign currency exposure associated with those holdings is hedged back into Australian dollars, based on a currency hedging ratio determined by the Trustee. This allows the fund to capture the returns generated by equity instruments in those markets. This option will usually be less exposed to currency fluctuations than the International shares (unhedged) option, although a portion of your investment will still be subject to currency risk.

Fund performance

The International shares investment option returned –2.0% after tax and fees in 2011/12.

Investment return (after tax and fees)

2007/08 –9.7%

2008/09 –30.5%

2009/10 11.1%

2010/11 9.4%

2011/12 –2.0%

Five year compound annual return: –5.7%

Minimum time frame

Seven years

Risk level Very high (band seven)

Investor suitability

It may be suitable for those prepared to take higher risk in exchange for potentially higher return on their investment over the long term, and who are comfortable with high levels of volatility and periods of negative returns. This option will usually be less exposed to currency fluctuations than the International shares (unhedged) option, although a portion of your investment will still be subject to currency risk.

Asset allocation 100% international shares

The shape of your super 2011/12 19

Sustainable

Investment objective

The Sustainable option is passively managed and represents a well-diversified portfolio that has expected risk and total return characteristics similar to the broader Australian share market (as represented by the S&P/ASX 200 Index).

Investment strategy

The Sustainable option is the only option investing in the Sustainable asset class. Investing in the Sustainable asset class/option means you are investing in companies that lead their industry peers in terms of sustainable business practice (‘Australian Sustainable Leaders’). The option seeks to capture the performance of Australia’s Sustainability Leaders with a well-diversified portfolio that has expected risk and total return characteristics similar to the broader Australian share market (as represented by the S&P/ASX 200 Index).

The portfolio holds securities included in the Australian Sustainable Asset Management (SAM) Sustainability Index (the AuSSI). SAM selects approximately 70 stocks for inclusion in the AuSSI from a universe of 200 of Australia’s largest listed companies. Most of these companies have a primary listing on the Australian Securities Exchange (ASX). This universe may also include other selected stocks that are well traded, with adequate liquidity on the ASX, and have a significant part of their business operations in Australia.

Fund performance The Sustainable investment option returned –7.9% after tax and fees in 2011/12.

Investment return (after tax and fees)

2007/08 –12.1%

2008/09 –17.4%

2009/10 11.3%

2010/11 8.2%

2011/12 –7.9%

Five year compound annual return: –4.2%

Min. time frame Seven years

Risk level Very high (band seven)

Investor suitability It may be suitable for those prepared to take higher risk in exchange for potentially higher returns on their investment over the long term, and who are comfortable with high levels of volatility and periods of negative returns.

Asset allocation 100% sustainable

Property

Investment objective

Before the payment of tax, to outperform the Consumer Price Index (CPI) by 5% per annum over the medium to long term.

Investment strategy

The Property option offers you the ability to invest your super in diversified portfolios of primarily industrial office and retail properties in Australia. This allows the property option to capture the returns generated by the Australian property market.

Fund performance

The Property investment option returned 8.8% after tax and fees in 2011/12.

Investment return (after tax and fees)

2007/08 13.1%

2008/09 –1.8%

2009/10 1.6%

2010/11 7.1%

2011/12 8.8%

Five year compound annual return: 5.6%

Minimum time frame

Five years

Risk level Medium (band four)

Investor suitability

It may be suitable for those who are comfortable with moderate levels of volatility and periods of negative return.

Asset allocation 100% property

The shape of your super 2011/12 20

Full biographies for each of the directors can be found at www.csc.gov.au

For more information on director appointments, terminations, responsibilities, risk management and corporate responsibility, visit www.csc.gov.au

Our directors manage the PSSap and invest the funds in accordance with the law and relevant regulatory requirements. All directors are appointed in writing by the Minister for Finance and Deregulation.

CSC and individual directors are covered by indemnity insurance to protect themselves and the PSSap from losses arising from certain claims against them. To date, there has never been a claim against CSC or a director that has resulted in the loss of members’ monies, nor have any regulatory penalties been imposed.

1. Tony Hyams AM, Chairman (Independent), App. 1/7/11 to 30/6/14.2. Tony Cole AO, Director, App. 1/7/11 to 30/6/13.3. General Peter Cosgrove, AC, MC, CNZM, Director, (CDF nominated), App. 1/7/11 to 30/6/14.4. Peter Feltham, Director, (ACTU nominated), App. 1/7/11 to 30/6/15.5. Nadine Flood, Director, (ACTU nominated), App. 1/7/11 to 30/6/14.6. Lyn Gearing, Director, App. 13/9/11 to 12/9/13.

7. Peggy Haines, Director, App. 1/7/11 to 30/6/14.8. Winsome Hall, Director, (ACTU nominated), App. 1/7/11 to 30/6/13.9. John McCullagh, Director, (CDF nominated), App. 1/7/11 to 30/6/13.10. Gabriel Szondy, Director, App. 1/7/11 to 30/6/14.11. Dr Michael John Vertigan AC, Director, App. 1/7/11 to 30/6/13.

1.

5.

9.

2.

6.

10.

3.

7.

11.

4.

8.

Your directors 2011/12

The shape of your super 2011/12 21

PSSap unaudited financial statements for 2011/12

Operating Statement for the year ended 30 June 20122012 $000

Revenue

Interest on cash at bank 5,657

Changes in net market value of investments 58,501

Employer contributions 809,001

Member contributions 12,380

Transfer from other funds 148,739

Government co-contributions 1,261

Insurance proceeds and other revenue 10,704

Total revenue 1,046,243

Insurance premium expense (28,342)

Income tax expense (120,047)

Benefits accrued for the year as a result of operations 897,854

Less: benefits and transfers paid (124,177)

Net increase in net assets available to pay benefits 773,677

Net assets available to pay benefits 30 June 2011 2,774,103

Net assets available to pay benefits as at 20 June 2012 3,547,780

Assets and liabilities as at 30 June 20122012 $000

Assets

Investments 3,529,416

Cash at bank 142,666

Other assets 679

Total assets 3,672,761

Liabilities

Benefits payable (2,649)

Sundry creditors (2,260)

Provision for tax (120,072)

Total liabilities (124,981)

Net assets available to pay benefits 3,547,780

Notes:The assets of the PSSap are invested in the ARIA Investments Trust (AIT), where they are pooled with the investments of the other CSC managed funds – the Commonwealth Superannuation Scheme (CSS), the Public Sector Superannuation Scheme (PSS) and the Military Superannuation Benefit Scheme (MSBS) – in order to deliver a cost-efficient investment process. The AIT invests in multiple specialist investment funds and portfolios. The AIT receives income such as dividends, interest, trust distributions and gains and losses on sales, and incurs administration and management expenses including expenses that would otherwise be incurred by the PSSap.The operating surplus or deficit generated by the AIT is reflected in daily unit prices provided by the AIT for its unitholders, including the PSSap, and the unit prices are published on the PSSap website. If you would like to see a copy of the PSSap audited financial statements for this year and the reports from the auditor, please refer to our Annual Report to Parliament (which is published and tabled in the Parliament in October) at www.csc.gov.au, send an email to [email protected], call us on 1300 725 171 or write to PSSap, Locked Bag 9300 Wollongong BC NSW 2500.

Financial statements

The shape of your super 2011/12 22

For all the information you need to make smart choices about your super, visit www.pssap.gov.au

On our website you’ll find:

> the PSSap Product Disclosure Statement

> a handy glossary of terms

> forms and publications to change your investments or learn more about your options

> news and information

> Member Services Online, where you can:

– check your balance and transaction history – make additional contributions via BPAY – select your investment options – view your nominated beneficiaries – update your address and contact details – use calculators to help keep your super investment on track – register for an online Member Statement – view and print your Member Statement.

If you have lost or forgotten your secure access number, you can use your secret questions and answers to re-set it. If you need help to do this, please don’t hesitate to contact us.

Web: www.pssap.gov.auEmail: [email protected]: 1300 725 171TTY: 02 6272 9827Fax: 1300 662 406Post: PSSap Locked Bag 9300

Wollongong BC NSW 2500

If you would like more information about your fund’s investments and governance, you can also contact CSC in one of the following ways:

Web: www.csc.gov.auEmail: [email protected]: 02 6263 6999Fax: 02 6263 6900Post: CSC

GPO Box 1907 Canberra ACT 2601

Contact PSSap