Theoretical Framework for Analyzing Accounting...

26

Theoretical Framework for Analyzing Accounting Developments: In case of Local Government Accounting in Japan Kiyoshi Yamamoto, Graduate School of Education, The University of Tokyo Email: [email protected] Abstract This article provides an analysis on accounting developments of Japanese local government in past five decades. The study examines the development arenas in terms of scope and time: micro and macro perspectives, and processes and outcomes. We adopt a segmented approach depending on stage analyzed. The single or integrated approach is not used taking into account of research findings by historical institutionalism. By using the approach, this paper shows that the accounting developments of local government were the outcomes of interactions among related actors in vertical and horizontal ways: local government and national government, and central ministries in national government. Although the introduction and diffusion were to some extent explained by new institutional sociology (NIS), it is shown NIS could not explain why particular local government adopted an accrual financial reporting at particular time compared to policy window model. This study also indicates that in improving decision making management policy shall be matched with accounting information from rational perspective. Keywords accounting developments, local government, Japan, institutional theory, rational theory, policy window model 1

Transcript of Theoretical Framework for Analyzing Accounting...

Theoretical Framework for Analyzing Accounting Developments: In case of Local Government Accounting in Japan Kiyoshi Yamamoto, Graduate School of Education, The University of Tokyo Email: [email protected] Abstract This article provides an analysis on accounting developments of Japanese local government in past five decades. The study examines the development arenas in terms of scope and time: micro and macro perspectives, and processes and outcomes. We adopt a segmented approach depending on stage analyzed. The single or integrated approach is not used taking into account of research findings by historical institutionalism. By using the approach, this paper shows that the accounting developments of local government were the outcomes of interactions among related actors in vertical and horizontal ways: local government and national government, and central ministries in national government. Although the introduction and diffusion were to some extent explained by new institutional sociology (NIS), it is shown NIS could not explain why particular local government adopted an accrual financial reporting at particular time compared to policy window model. This study also indicates that in improving decision making management policy shall be matched with accounting information from rational perspective. Keywords accounting developments, local government, Japan, institutional theory, rational theory, policy window model

1

Introduction Since the 1980s, accounting change from cash to accrual basis has diffused in the public sector across the countries (Olson et al., 1998; Jackson and Lapsley, 2003; Khan and Mayes, 2009). The change is considered a movement in financial management adopting new public management (NPM) which is a coupling of institutional economics and management thoughts (Hood, 1991). In practice, Sargiacomo and Gomes (2011) showed that there were very little publications prior to the 1980s by reviewing articles of historical research in the public sector. They also indicated ‘only a few articles’ adopted a theoretical framework, in addition major research focused on Anglophone countries and specific periods. Most public sector accounting research highlight the changing or transformation process in recent time while increasing studies on comparative accounting systems and practices through comparative international governmental accounting research (CIGAR) network (Jones, 1991; Jorge et al., 2011). Besides, as the theoretical perspective, institutional theory and rational (choice) theory have been used in investigating the adoption, use and institutionalization of accounting system, especially for accrual accounting. It looks that the situation in current research has been steadily coping with the problems. Despite that, reforming or changing processes and outcomes differ from country to country, and even in the same country and the same period. While both approaches have contributed to explain the accounting choices and implementation practices, they cannot fully explain why the organizations in similar conditions adopt different strategies and result in different outcomes by using the same approach. From a micro-perspective, institutional economics to some extent answer the problem through the concept of ‘path dependence’ (David, 1985; Arthur, 1989). It is however unable to explain why the organization adopted accrual accounting at the particular time. Therefore we have to develop a new theoretical perspective other than those in current public sector (historical) accounting research. Also, introducing or implementing accrual accounting system itself is just a means, not the objective of reform: accrual information is a crucial tool of NPM. There still is few research on the impacts or outcomes by implementing accrual accounting (and budgeting) system in the public sector. Some research investigated the utility or contribution to improving financial performance (Bogt, 2004; Paulsson, 2006; Campos and Pradham, 1996: Marti, 2007). However, there are limitations in case studies (Yin, 1994) or cross-national data analysis (Tella and Schargrods, 2003), in addition the results are inconsistent. Further, there is ‘much to learn about the use of accounting and accountability in LG (local government) in non-Anglophone scenarios’ (Sargiacomo and Gomes, 2011, p.273). There might be

2

significant differences in the reality and actual practices from the West to the East or Anglophone and non-Anglophone, even though using the same word like accrual accounting and financial management. The historical development in local government of Japan is quite appropriate to explore the new frontier in public sector accounting research. It took 40 years for most local governments to adopt an accrual based financial reporting system since the starting discussion on introduction in 1962. However, once the responsible ministry, the Ministry of Internal Affairs and Communications (MIC) in 2001 published a guideline for preparing financial statements for local government, it promptly diffused around the nation in a short time, despite a voluntary adoption, not regulations or laws. The sudden policy change by MIC responded to the change by the Ministry of Finance (MOF) and was influenced by some local governments adopting international innovations. This means that Japan’s case will contribute to investigate why the specific public entity adopted or determined to adopt a new accounting system at particular time after long discussion, but also examine the outcomes by using and experiencing the new system for one decade. Consequently we are able to examine how the central government and local government interacted with each other in addition to those between related ministries in the central government. In order to analyze the above interactions, we divide the research period into two phases, 1962-1999 and 2000-2012. The former composes of ‘talk and decision’, and the latter ‘practice and results’ (Pollitt, 2002). For the first period, we will use the policy windows model as an alternative approach from the perspective of a policy process: the model can specify the time and reasons for determining to introduce a new system. On the other hand, for the second period, a segmented approach from institutional theory and rational theory will be adopted due to taking into consideration of Japan’s institutional and cultural elements. The paper is organized as follows. The next section reviews previous research on accounting developments in the public sector. The third section describes the theoretical framework for accounting development ranging from talking to results. In the fourth section, the local government system of Japan is presented and the accounting development is explained. Then discussions and conclusions are offered. Literature Review Before explaining the development of the new theoretical framework proposed here, we will review previous research on accounting developments in the public sector. As mentioned earlier, there are several approaches to the research.

Firstly, in historical research, as mentioned earlier, Sargiacomo and Gomes (2011)

3

reviewed 33 historical/longitudinal articles on public sector accounting in 8 countries (UK, USA, Italy, France, Germany, Russia, Spain and Sweden). They found that most research adopted a descriptive study and their focus was on “the technical aspects of accounting practices” (p.268) despite the character of public sector accounting for social, political and economic functioning. The review is very insightful and generally accommodates to other nations, however, some interesting and thoughtful approaches are missing. For example, Ryan (1998) analyzed the policy process of introducing accrual reporting from 1976 to 1996 in Australian public sector using the concept of agenda setting or policy window by Kingdon (1984). He showed transforming into accrual accounting was not just a technical change but a political and policy process interacting among related actors like Treasury, Auditor General, and accounting professions.

In Japan, there were few modern historical studies on public sector accounting like in Anglophone countries. However, owing to the specific nature in Meiji Constitution enacted in 1889, for a long while, the concept and scope of public finance has involved accounting rules and practices for the government sector. The chapter on “Accounting” corresponded to the content of “Public Finance”. New constitution after the Second World War replaced “Accounting” with “Public Finance”. This change was understood by the democratic control by the parliament to the administration or cabinet in new constitution, which was set up under the strong influence by the United States of America occupying Japan in a short period. Under the former constitution, the administration dominated over the parliament given the delegation principles in executions from the Emperor (Yamamoto, 1989). The concept of public finance necessarily includes budgeting other than its execution and reporting. Accordingly, using the technical term of “accounting”, the administration fairly obtained a predominant (discretionary) power against the parliament. The interpretation was excellently political. It is a suitable example which “accounting” played a political function in controlling public money.

Second, in modern accounting reform in the government sector, theoretical and empirical research has been developed since the 1980s. From an innovative perspective, Lüder (1992) developed a contingency model in which the accounting innovation in the government sector was sparked by the stimuli like financial scandals and crises. Lüder’s model has been often used in an academic network of the Comparative International Governmental Accounting Research (CIGAR). Likewise, Hussein (1981) proposed the process approach that change in financial accounting standards was a social process that approximates a diffusion and adoption of innovation process. Mattisson et al. (2004)

4

explored the accrual accounting reform processes in Swedish and Finish local governments by using the Hussein’s model.

On the other hand, to explain and investigate the accounting choice for public institutions, there are mainly two theories: institutional theory (Meyer and Rowan, 1977; DiMaggio and Powell, 1983, 1991) and positive accounting theory. The latter is based on self-interest and rational theory (Zimmerman, 1977; Watts and Zimmerman, 1979). It is assumed that accounting is part of the contract between a principal and an agent. The former intends to explain the diffusion of accrual accounting in the public sector from the perspective of institutional practices in which organizations adopt an accounting model to acquire legitimacy confirming to rules. Carpenter and Feroz (2001) explained how institutional pressures influenced the decision of state governments in the United States to adopt or resist the use of generally accepted accounting standards. Lande (2006) and Bogt (2008) also used social institutional theory into the accounting reform processes in France central government and Dutch municipalities respectively. Recently a mixed approach of positive accounting theory and institutional theory has been proposed and adopted by Falkmand and Tagesson (2008), Collin et al. (2009) for the Swedish public sector accounting and Pina et al. (2009) for EU local government. However, despite of insisting integrated approach, they do not develop an eclectic theory that mixes economic and institutional theories.

Further, from the perspective of political dimensions and interplay of competing interests, Ryan et al. (2007) analyzed the public sector accounting standard setting and development processes in Australia by using the framework of Puxty et al.(1987). Whether in the private sector or public sector, accounting standards as an accounting regulation have somewhat the historical and politico-economic context rather than merely a technical matter. Puxty et al. (1987, p.275) also indicate that the accounting regulation is constructed within a nexus of market forces, bureaucratic control and communitarian ideals. Their framework is based on three principles of social order composed of Market, State and Community (Streeck and Schmitter, 1985). Puxty et al. identify several modes of regulation, liberalism mode where market determines; legalism that state exclusively sets up; associationism is the mixed mode of three principles, where significantly depends on market principle; corporatism where the state incorporates the organized interest groups. Using these principles, Ryan et al. showed Australian public sector accounting standard setting moved from liberalism to associationism to corporatism and finally reached into legalism.

The above approaches surely have contributed to government accounting research, especially in explaining the accounting system reform in the public sector. However,

5

these models have some limitations and disadvantages. While process model expands the scope from initiation to outcomes in accounting change, outcomes are not just to adopt, reject or pre-empt new accounting system or standards, rather a political resolution or reconciled results by interactions of stakeholders. Hussein (1981, p.36) himself mentions that it should avoid sacrificing the complexity and the need to facilitate relational and dynamic analysis.

For analyzing the accounting choice, neither institutional theory nor positive accounting theory can fully explain and predict the actual results. In fact, as Kasperskaya (2008) indicated, new institutional sociology is unable to explain why organizations under similar environment adopted different approaches. Also it cannot account for why the organization among similar organs introduced a new accounting system at the particular time. In addition, the emerging approach insisting an integrated theory so far does not develop clear alternative model, while institutional theory and resource dependency theory are complementary as indicated by Carpenter and Feroz (2001). However, few studies investigate the outcomes by reforming accounting system whether the intended results like improving performance or accountability have been caused or not. Most research have focused on changing process and its utility. Accordingly, in order to analyze the interactions in the reforming process, we must identify the principal actors interacting with each other in the public domain (Stewart and Stewart, 1994). Especially in case of local government, the interrelations between national and local government are a crucial factor in reforming. This means that the new approach for government accounting research needs to consider the dynamic and interrelated character of reforming processes. In addition, we have to examine the actual figures in terms of intended outcomes or objectives of the reform. Theoretical framework Policy Window Model for Introduction Policy window model by Kingdon (1984) is appropriate in analyzing the changing process, since introducing accrual accounting into the local government might be considered a policy change in public financial management, not a technical issue. Contingency theory of course contributes to explain the accounting transformation from innovation perspective, however, it somewhat assumes a straight progress on transforming from cash to accrual given the same conditions. Policy window model comes from garbage can model (Cohen, March and Olsen, 1972) in which contrasts with rational or incremental model in decision making. Kingdon develops the model

6

through interviewing and questionaries for politicians and other actors which has a great advantage in our research aim to explain ‘why and how particular issues come to dominant the government and decision agenda’ (Kingdon, 1984). In his model, policy change occurs when three separate streams come together. Firstly, there is the problem stream, which consists of perceived problems with particular attributes. Second, there is the policy stream which indicates solutions, waiting to attach themselves to problems. Third, there is the political stream, which encompasses the current political balance and the state of public opinion. When three streams are coupled together, the policy window is open. At the time, a policy entrepreneur has to be ready to tie all three streams together to push the issue to the decision agenda. Accordingly, the timing and role of entrepreneur are critical for change. Models for Implementation and Results Kingdon’s model is quite useful for analyzing the policy process. However, the policy window model focuses on decisions of policy change, not the outcomes by change. Consequently we have to expand the analytical scope into adoption and its influence on practices after decisions of introducing new system. New institutional sociology, especially the concepts of isomorphism and decoupling are applicable to this aim. The political and bureaucratic culture in Japanese local government still has been dominated by centralism, i.e. highly affected by the power of national government despite of being provided local autonomy by constitution. Therefore, the guidelines or standards published by the national government, specially by MIC, might work as a coercive isomorphism for local government. Of course the implementation can be as a decoupling (Meyer and Rowan, 1979) which new accounting system has been used in ceremonial way owing to conflict with traditional practices in cash basis. In this case, the implementing new accrual accounting or financial reporting system will have little impact on practices and outcomes. However, the influence could differ by local government due to the extent of fiscal independence from the national government. Also, as previous studies showed, some cases indicated successful outcomes while other cases unsuccessful.

Therefore we have to consider other factors other than institutional isomorphism on studying the outcomes. NIS is a macro-perspective theory and insists uniformity or similarity; a micro-theoretical approach is rather required. While the concept of organization routines by Burns and Scapens (2000) is useful, there might be conflict with system design and rules or routines through new system, in addition to that between existing and new routines. Besides, each local government will be facing its individual path-dependency and take into consideration of costs and benefits using the

7

new system. Consequently, rational approach complements the institutional theory. In this regard, policy window model is a kind of approach exploring particular process which is not inconsistent of old institutional economics. Above reviews indicates that it is impossible to analyze or explain the total figures composing “talk”, “decision”, “practice” and “results” (Pollitt, 2002) from the perspectives of micro and macro dimensions with which actors are interacted. Institutional approach is suitable in explaining macro perspective from collective action in accounting developments, while rational approach has advantage in examining the driving forces for accounting choice from individual action or micro perspective. In addition, the concept of path dependency from institutional economics or institutional sociology is useful in analyzing the change process. The concept has similarity with policy process theory like policy window model in focusing on a particular time and space, although new institutional sociology (NIS) emphasizes the persistence or continuity. Therefore, as Thelen (1999) indicated, NIS is “not particularly helpful in talking about change”(p.387).

The aim of this article is however to analyze the developments of local governmental accounting in terms of processes and outcomes, rather than changing itself. Also the scope ranges from individual local government level to national level including related central ministries. This might lead to the conclusion that we need to adopt a synthesized approach integrating these different theories and models. However, it is too high to hurdle in realizing the approach, rather we will adopt another strategy for creative combinations. As Zysman (1994) elaborates, issues shall be segmented to make most appropriate use of perspective. Figure 1 shows how the different theories are segmented by scope and time. At the same time, we must acknowledge that even the most appropriate approach will be adopted, its scope will be limited and certain subsets could be represented and explained. From this perspective, we will use different approaches by analyzing scope and time, neither adopting a single theory nor developing an integrated or a global model. Data and Method We studied two levels of accounting policy in the public sector of Japan owing to interactions between local governments and national government, i.e. in local government and in national government. In case of local government, the developments in Tokyo Metro Government are focused from the micro perspective. On the hand, MOF and MIC are main actors examined in national government. We adopted a segmented approach which the different theory was used by stage on accounting developments. The data used in this study was collected from formal documents, informal talks with

8

senior bureaucrats in local and national government, and internal documents. I was involved in accounting development as an academic adviser for Tokyo Metropolitan Government and MOF in the early 2000s, however, the role was limited to just make an advice on technical issues, did not reach to policy decision making which financial reporting model should be adopted or whether transformed into accrual accounting. In addition, the survey results on utility of accrual information which we implemented for all Japanese municipalities in other research project are complementary used.

Figure 1. Segmentation of theories Time Process Outcomes

Micro policy window model OIE*, PAT**

Scope path dependence

Macro contingency theory NIS, NIE***

*: old institutional economics

**: positive accounting theory

***: new institutional economics

Accounting developments Local Government System The Constitution designates the Parliament (Diet) as the highest organ of state power. Parliament consists of a lower house and an upper house. The postwar constitution accords extensive authority to local government which consists of prefectures and municipalities. As of October 2011, the number of prefectures is 47 and municipalities are 1720. The autonomy contrasts strikingly with the prewar period when governors were appointed by the national government. Local government is a kind of “presidential system” or “chief system”, affording residents the rights to elect local assemblies and directly elect the chief officer. Governors are also directly elected. However, in practice, the national government is able to exert considerable control over the local governments through the financial distribution system from the national government (Yamamoto,

9

2000). Besides, the national government sets up guidance of reforming management for local government and promotes it through laws and regulations.

Financial management in the public sector is regulated by laws and their related rules. The fiscal rules have been greatly influenced by German and French Law or the European Continental System of law. While in the early times of Meiji Era (the modernizing period in Japan) from 1880 to 1899, the government sector (national government, local government and central bank) adopted a double-entry bookkeeping in accounting under the guidance by Braga, a former senior official of Hong Kong Branch of the British Empire. It is notable that in that period, bookkeeping was an examination subject for recruiting civil servants. However, after the Meiji Constitution (Constitution of the Empire of Japan) was enacted in 1889, the double-entry system was abandoned and returned to a single-entry cash based system. Many bureaucrats and scholars1 went to Prussia (present Germany) and France to study their legal and governance system. Hence, the Japanese government system has been greatly influenced by the continental culture, while in the postwar, an Anglo-Saxon System was also imported in part.

Consequently accounting standards and financial reporting are prescribed in laws, and basically in a cash basis. The senior bureaucrats are dominated by the graduates from law. The fiscal management system in particular has changed little since the Meiji Era. As a result, for a long time, government accounting had been separated from business or corporate accounting. Introduction Period This period ranges from talking to decision making in introducing accrual based financial reporting. Following policy window model, the coupling of three streams did not occur until the late 1990s, whether local government level or national government level as the responsible ministry.

The problems and limitations of traditional cash accounting were already acknowledged in the 1960s by the government. In 1962, the Research Board of Financial Accounting System for Local Government, an organ of the responsible minister (MIC, then the Minister of Home Affairs) published the report on reforming financial accounting system. The report indicated that current system was in short of managing assets and liabilities by contrast to cash control. Also it indicated since final account was disregarded, local government was not accountable to the citizens or residents. From this perspective, the Board recommended to set up accrual based final account in addition to the current cash based account contrasting to the budget. It is a dual system using cash and accrual based system in accounting. However, at that point, the report did not suggest the accounting standards, just mentioned the general scheme

10

toward improving. Besides, the technical character of accounting in financial management did not attract public interest. Accordingly, among three streams, policy and political streams were quite weak while problem stream could be slightly found.

The break occurred in 1987 when the Association of Local Authorities, a think tank related to the Ministry of Home Affairs, developed an accrual based financial reporting system prepared by fiscal statistics in cash basis which every local government was required and submitted to the government (MIC). The system does not use a double-entry bookkeeping in daily transactions, as a result, for local government it was the feasible alternative to cope with the problems identified: the policy stream for accounting reform definitely appeared. The Governor of Kumamoto Prefecture, Mr. Hosokawa noticed the system and firstly prepared the balance sheet of the prefecture in Japan. He was the national leader in local government reform. However, in the late 1990s, fiscal scandals and corruptions were found in many local governments, especially prefecture level. Closed management system and asymmetry in information between citizens and public administration were identified as the major problem. Accrual based reporting used in the private sector was considered a more transparent and accountable system, which include information of assets and liabilities current accounting system could not provide with. At the same time, several governors eagering in government reform were elected. They have common specific features compared to traditional governors in experiencing the Member of Parliament, strong leadership, and active learning from public sector reforms in other nations (NPM). Governor of Mie Prefecture, Mr. Kitagawa was the pioneer in public management reform, especially adopting NPM. He introduced performance measurement system into all projects of prefecture from the perspective of result-orientation or changing budget-dominant culture in 1996. Then financial reporting composed of operating statement and balance sheet in accrual basis was also prepared in 1998, although double-entry bookkeeping was not introduced.

On the other hand, in 1999 Tokyo Metropolitan Government led by Governor, Mr. Ishihara determined to introduce an accrual based financial management system through using double-entry bookkeeping in daily transactions. It was remarkable in adopting full accrual accounting system by contrast to previous financial reporting which adjusted cash based final accounts into accrual basis at the end of fiscal year. These innovations are explained by coupling problem and policy streams through political leadership of governors themselves with political streams: they played a role of policy entrepreneur. At the moment, there were just several local governments introducing an accrual based financial reporting. However, the responsible ministry MIC (MOH at that time) was

11

also forced with the three streams. First, as the problem stream, public finance of local government had been more and more worse in the 1990s (the ratio of long term debts to GDP was 14.8 % in 1990 to 32.3% in 1998). The fiscal stress drove MIC to encourage local government to improve financial management alongside of enhancing more accountability and transparency in local government public finance. At the same time, MOF started to develop financial reporting model in corporate accounting or in response to the report by the Economic Strategy Council chaired by a leading business executive and established as an ad hoc Cabinet Committee. The recommendation in 1999 stated that the governmental accounting should transform from cash to accrual accounting through using a double-entry bookkeeping. The council mentioned that the national government should prepare the business type financial statements from the perspective of transparency and information disclosure, and as well that local governments should prepare and publish their accounts in accordance with the national standards. MIC (former Ministry of Home Affairs) has competed with MOF since the Meiji-Era. Financial transfer or support to local government by the national government is the second largest item of national budget. The influential power of MIC over local government significantly depends on the financial supporting system. Consequently MIC also had to take appropriate actions against MOF. The leading role in developing accrual based financial statements was necessary to keep influential position as the competent ministry to local government, because some innovative local authorities already prepared accrual financial reporting in their own ways. The political streams pushed MIC to develop a model of preparing balance sheet for local government in March 2000. MIC preceded MOF in publishing on a balance sheet, since MOF published a tentative model of balance sheet for national government in October 2000, adjusting final accounts into accrual financial reporting through statistical approach like in local government. Diffusion Period Following the recommendation of the Economic Strategy Council, Prime Minister Koizumi, whose administration lasted from April 2001 to September 2006, strongly promoted public sector reform from a new liberalism perspective. In June 2001, the Economic and Fiscal Council chaired by the Prime Minister announced a more forward to introduce the accrual based approach into public financial management. This signified a sea change in public policy after the war; it was the firstly official acknowledge by the national government of taking on accrual based approach.

Just three months before the announcement, MIC published the accrual financial reporting model composed of balance sheet and operating cost statement using fiscal

12

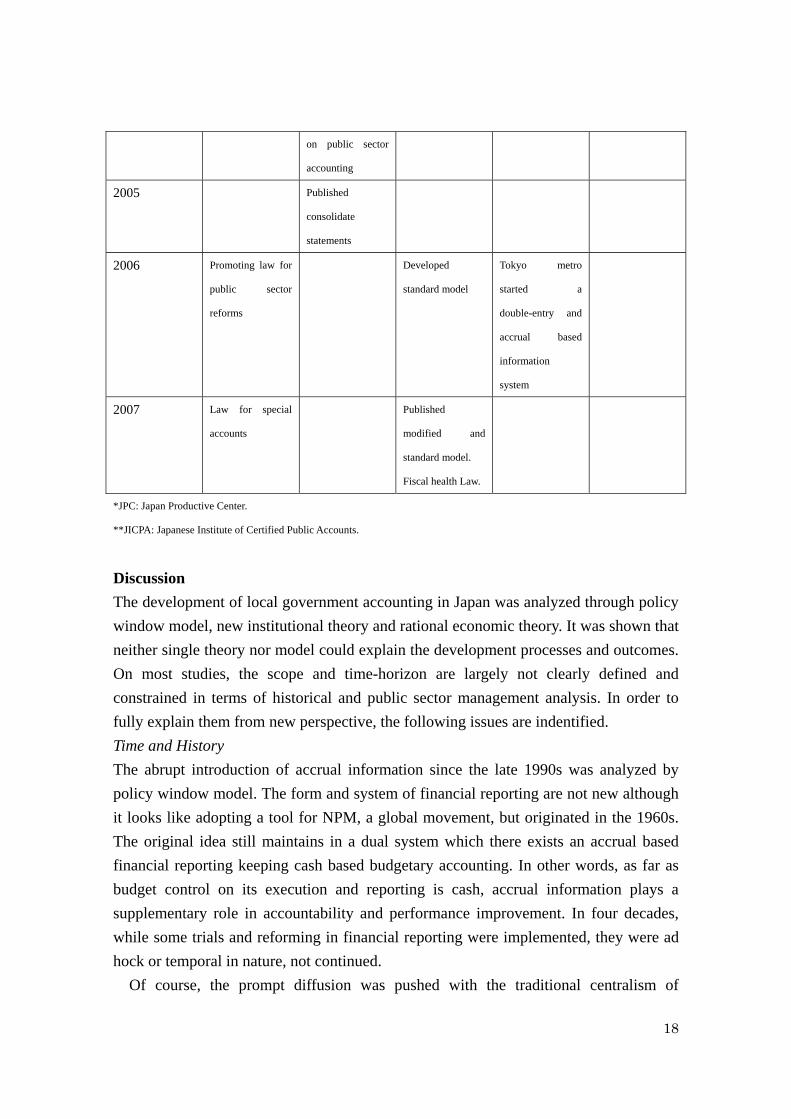

statistics. Many local governments adopted the MIC’s model in the next few years despite of some exceptions like in Tokyo Metropolitan. However, in 2006 the Administration determined that the national government would ask local government to develop a standardized accounting model based on the financial reporting rules for the national government; in September 2005 MOF firstly prepared consolidated financial statements composed of balance sheet, operating cost statement, statement of change in difference between assets and liabilities, and cash flow statement, while the statements were not required by law, but just supplementary documents of the final accounts. The intent was to measure the value of assets and debts for the government sector as a whole. Koizumi Administration aimed to improve public finance by downsizing assets and debts through setting up a program act called the Law for Promoting Public Sector Reform in June 2006. The Law stipulates that the national government shall take necessary actions in promoting financial reporting system referring to the generally accepted accounting principles (Article 60) and provide local authorities with information, advice and support in establishing financial reporting system (Article 62).

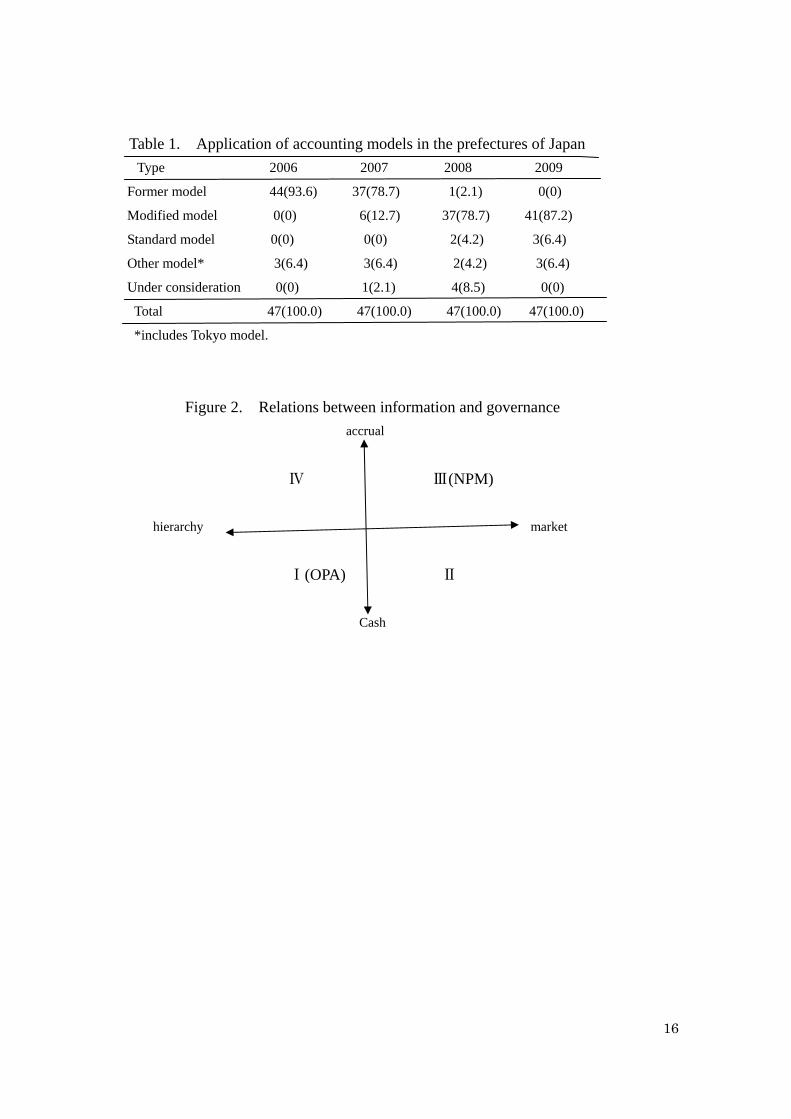

Accordingly, MIC began to harmonize local government accounting model with the national government model. In October 2007, MIC proposed two accounting models for local government comparable to the national model: one was a modified approach (revised version of former MIC model) based on cash accounting, and the other is on an accrual basis through double-entry bookkeeping called ‘standard model’. At the same time, MIC encouraged local government to introduce either model within five years. These models are not mandatory in preparing financial reporting as prescribed in the promotion law. Whether using the model or not is left to the local government discretion. Despite of being voluntary, after publishing the models in 2006, former model was fast replaced by the modified and standard models. Especially for modified model, just 6 among 47 prefectures adopted it for FY 2007, for FY 2008 and 2009, 37 and 41 prefectures used the model respectively (see Table 1).

It can therefore be said that MIC succeeded in leading the reform of financial reporting for local government. Strictly speaking, since two models are just recommended by MIC, local government is not enforced to adopt them. This means that there are some limitations in explaining the diffusion from the concept of coercive isomorphism. Rather it is more appropriate to interpret it in terms of decoupling or loose-coupling from the NIS. Many local governments have prepared accrual based financial reporting just to confirm MIC’s recommendation. In practice, a survey to financial officials of municipalities by Kobayashi et al. (2011) showed that approximately 70 percent of respondents indicated MIC as the most influential actor in

13

introducing accrual financial reporting; most local governments do not prepare financial statements by their own will for improving accountability or performance. The fact might be explained by the perspective of OIE: modified and former MIC models are common in using a statistical approach, not adopting double-entry bookkeeping like the standard model. Therefore there is no change in daily transactions and practices whether modified or former model. According to the concepts of ‘rules, routines and institutions’ by Burns and Scapens (2000), who developed OIE in accounting change, local authorities are more likely to accept new rules which are consistent with existing routines. In this case, new rules are the modified MIC model, and existing routines are accounting practices in cash based traditional system. The transaction costs from former MIC model to new model are evidently lower in case of the modified model than in case of the standard model. Despite the prompt diffusion, Tokyo Metropolitan Government has pushed forward the different approach which basically adopts IPSAS in a full accrual accounting system through double-entry bookkeeping. The financial reporting system started in 2006 (see Table 2). In 2011, Osaka Prefecture followed the Tokyo Metro model. It is notable in intergovernmental politics in which the local governments having the first and second largest economy adopt different approach from the national government in financial reporting, while seemingly technical issues in public finance. Both governments were led by strong political leadership of Ishihara and Hashimoto, who turned into the Mayor of Osaka in 2012 preserving his powerful influence on the Osaka Prefecture Government. Consequently at present three different models coexist for local government financial reporting. The competitive situation is partly caused by the supplementary position of financial reporting itself separated from formal cash based accounting system, although the diffusion of modified model can be explained by NIS and OIE from the perspective of uniformity and path dependency. MIC so far does not have the mandate to set up accounting standards for local government by law. Institutional theory predicts that the decoupling of actual and formal practices or ceremonial adoption would not cause successful results. Kobayashi et al. (2011) found that less than 20 percent of local governments (municipalities) used accrual based financial reporting in operational management, by contrast more than 90 percent used information of budget and accounts in traditional cash basis (current system). In other words, it might be explained that actual practices in accrual financial reporting are not yet transformed from rules to routines. However we can indicate other scenarios. The one is the approach by NIS. Several local governments introduced accrual financial reporting as a reforming tool,

14

because they thought that such accounting information in Anglo Saxon countries, especially in the UK and New Zealand, was a crucial tool in successful reform. The adoption of accrual system was driven by mimetic isomorphism. In practice, the recommendations by MIC led many local governments to prepare financial reporting in just conforming to MIC’s models. The motivation or intention was not to reform local government management but a reactive response to the national government. Accordingly accrual based financial information for most local authorities was little linked to budgeting, evaluation, assets and liability management (Kobayashi et al., 2011).

The other comes from the rational perspective of system design. As mentioned before, NPM aims at increasing efficiency and effectiveness. Accrual accounting is the strategic tool for NPM: “without double-entry bookkeeping or accruals accounting, it is hard to make either global or specific links between expenditure and cost, and between cost and performance” (Pollitt and Bouckaert, 2011, p.85). These links work in a competitive condition where cost and quality of services are comparable among (possible) providers whether public or private. Costing in the private sector is accrual basis in compliance with corporate accounting or generally accepted accounting principles, therefore, changing cash basis into accrual basis in the public sector is required to compare costs in the same rule. Following the Figure 2, traditional (old) public administration (OPA) is located in CellⅠcomposing hierarchy control and cash information, while NPM is located in Cell Ⅲ composing market mechanism and accrual information. However, market mechanism like market testing and internal market was little adopted in Japanese local government even in the innovative municipalities. Rather a lot of local authorities sought to use cost information in budgeting or management control through performance measurement for improving efficiency. The actual figure in Japan is located in Cell Ⅳ with hierarchy control and accrual information. Consequently the transition was fromⅠto Ⅳ where there is a conflict between governance system and financial information, not Ⅰto Ⅲ.

15

Table 1. Application of accounting models in the prefectures of Japan Type 2006 2007 2008 2009

Former model 44(93.6) 37(78.7) 1(2.1) 0(0)

Modified model 0(0) 6(12.7) 37(78.7) 41(87.2)

Standard model 0(0) 0(0) 2(4.2) 3(6.4)

Other model* 3(6.4) 3(6.4) 2(4.2) 3(6.4)

Under consideration 0(0) 1(2.1) 4(8.5) 0(0)

Total 47(100.0) 47(100.0) 47(100.0) 47(100.0)

*includes Tokyo model.

Figure 2. Relations between information and governance accrual

Ⅳ Ⅲ(NPM) hierarchy market Ⅰ(OPA) Ⅱ

Cash

16

Table 2. Historical developments in accounting for local authorities

Year Cabinet MOF MIC Local

Government

Think-tank

1962 Report by

Research

Committee

1963 Report by special

group of Ad hoc

Council

Report on

double-entry

bookkeeping

1964 Report by Ad hoc

Council

1987 Kumamoto

Prefecture

prepared BS

Association for

Local Authorities

developed a BS

model

1997 JPC* developed

accrual financial

reporting model.

JICPA** published

a draft for public

sector accounting

standards.

1998 Mie Prefecture

prepared accrual

financial reporting

1999 Report by

Economic Strategy

Council

7 prefectures

prepared accrual

financial reporting.

2000 Published a

tentative BS of

national

government

Published a model

for preparing BS

2001 Report by

Economic and

Fiscal Council

Published accrual

financial reporting

model

2003 Fundamental view

17

on public sector

accounting

2005 Published

consolidate

statements

2006 Promoting law for

public sector

reforms

Developed

standard model

Tokyo metro

started a

double-entry and

accrual based

information

system

2007 Law for special

accounts

Published

modified and

standard model.

Fiscal health Law.

*JPC: Japan Productive Center.

**JICPA: Japanese Institute of Certified Public Accounts.

Discussion The development of local government accounting in Japan was analyzed through policy window model, new institutional theory and rational economic theory. It was shown that neither single theory nor model could explain the development processes and outcomes. On most studies, the scope and time-horizon are largely not clearly defined and constrained in terms of historical and public sector management analysis. In order to fully explain them from new perspective, the following issues are indentified. Time and History The abrupt introduction of accrual information since the late 1990s was analyzed by policy window model. The form and system of financial reporting are not new although it looks like adopting a tool for NPM, a global movement, but originated in the 1960s. The original idea still maintains in a dual system which there exists an accrual based financial reporting keeping cash based budgetary accounting. In other words, as far as budget control on its execution and reporting is cash, accrual information plays a supplementary role in accountability and performance improvement. In four decades, while some trials and reforming in financial reporting were implemented, they were ad hock or temporal in nature, not continued. Of course, the prompt diffusion was pushed with the traditional centralism of

18

intergovernmental relationships. The process is considered the interactions and intersections between institutions and actors: arena at particular time and space. The innovative adoption of accrual financial reporting by some local authorities in the 1990s and sea change in 2000 by MIC to promoting financial reporting occurred in the specific arena. Accordingly, time and history are a crucial determinant of the accounting development. However, the policy window model does not explain why many local governments do not adopt the standard model by the national government and some authorities have developed another model. Institutions The diffusion of modified MIC model can be partly explained by transaction costs from former MIC model to new model: whether new or old model, it is not necessary to introduce double-entry bookkeeping. The financial reporting is prepared by adjusting final accounts in cash into accrual basis at the end of fiscal year. If local authorities will introduce the standard model or develop their own model, they have to bear the costs for changing or developing. The choice by many local governments is quite rational in cost saving. In addition, the national government never intends to change the financial management system into accrual basis like in the UK, Australia and New Zealand. The public reform promotion act aims to recognize and measure the assets and liability in more correct and comprehensive way. In practice, the Law of Fiscal Health for Local Authorities in 2007 monitors the financial conditions of local authorities in terms of flow-type and stock-type indicators. However, actual indicators are thoroughly measured in cash basis even in the stock-type. This means that financial control by the national government does not change but be kept in cash basis. Consequently the relationships between budgetary accounting and financial reporting are decoupled or separated as institutional theory suggests. Although the new rules in accrual based reporting are adopted in many local governments, no routines and institutions on financial management practices in actual basis are established.

The background lies in the preferences of politicians and bureaucrats, which is a part of the institution as norms and culture. As Ball (2012, p.38) indicates, “in many cases they (politicians) are working within highly idiosyncratic cash-based budget and accounting systems. A move to accrual based accounting and budgeting would force them outside their area of expertise”. The current accounting practices are embedded in the financial institution on cash basis. Accordingly the transformation from current single-entry and cash budgetary system into double-entry and accrual financial management system is a political institutional change. It requires a strong political power against the current institutions. We need to have another scenario other than

19

institutional theory in examining the development process. Politics The drastic change by MIC on financial reporting system was caused by its political strategy for primary actors in leading the policy/maintaining power. On the other hand, Tokyo Metropolitan Government clearly chose another approach from the national government including MIC and MOF. The financial reporting basically adopts IPSAS and is seeking to use the accrual information in financial management in parallel with institutional cash based budgetary accounting, not in de-coupling or loose-coupling between accrual and budgetary accounting. Governor Ishihara’s stance is definitely different from other former innovators in establishing an accrual based financial information in daily transactions. He rather wishes to write off traditional cash based culture and norms, and set up new institution with political power. The strategy is effective in politics and supported by fiscal independence, because MIC does not have power to enforce local government to adopt a specific model or system, also Tokyo receives no financial transfer payments from the national government.

While political behavior of MIC promoted local government to prepare an accrual based financial reporting, the prompt diffusion partly repressed innovations in local government management. The reporting model was given by MIC, therefore, local government does not need to develop the model and strive to use accrual information in management. It leads to misunderstanding for local government in the objectives and backgrounds of accrual based financial reporting. Consequently we further have to investigate the relation between politics and institutions in addition to influence by principal political actors. Conclusion This article provided an analysis of accounting developments of Japanese local government in past five decades. The study analyzed the development arenas in terms of scope and time: micro and macro perspective, and processes and outcomes. We adopted a segmented approach depending on stage analyzed; a single or integrated approach was not used taking into consideration of research findings by historical institutionalism (Thelen, 1999; Zysman, 1994). The theories used at different stages were policy window model from political science, positive accounting theory or rational theory and path dependency from new institutional economics, contingency theory from management, new institutional sociology from sociology. The historical analysis showed that institutional theory, especially new institutional sociology (NIS) could explain the diffusion process of accrual financial reporting in

20

local governments. Also NIS was generally legitimate in analyzing lower utility of accrual financial reporting in managing local government through the concept of loose-coupling or de-coupling. While adopting accrual financial reporting is in compliance with the recommendation by MIC, there is little linkage between accrual information prepared and decision making in use. Even in the similar conditions, some local authorities adopted accrual information system before the diffusion, while the other local authorities did not. Besides, the extent in using accrual reporting differs by local government. Policy window model focused on processes interacting among actors and explained why at the particular time and entity the introduction of or transforming to accrual based financial reporting occurred. In fact, earlier adoptions of accrual financial reporting in Japan were led by governor’s strong leadership in coupling with problem (corruptions in financial issues) and policy streams (tools for preparing accrual based reporting). In addition, it was shown that the accounting developments were the results of interactions among related actors in two levels. The one was the relationships between local government and national government: that is which player does take a dominant position in setting up financial reporting model after the opening of policy window. The other was the relationships between central ministries in the national government. MOF is responsible for national government finance while MIC is the competent ministry in controlling local government finance. The competition between the two ministries promoted to develop the financial reporting standards. On the other hands, the different outcomes by local government were found by our survey. It is unable to explain the differences from the perspective of new institutional sociology, rather might be caused by the mismatch between policy design and its assumed information from rational perspective. The segmented approach was basically supported by our analysis. Our study to some extent answered the call for extensional historical research on local government by Sargiacomo and Gomes (2011). However, there remain three issues. First, there might be another theoretical approach to establish an integrated or a synthesized theory rather than segmented or combination model like in this article. Second, there need to investigate the interactive processes in accounting developments through interviews and analyzing internal documents. Third, comparative international governmental accounting history research has to be explored. Comparative studies among Asian countries or the West and the East are potential fields.

21

References Arthur, W.B. (1989). “Competing Technologies, Increasing Returns, and Lock-in by

Historical Events”, Economic Journal, Vol.99, No.394, pp.116-131. Ball, I. (2012). “New Development: Transparency in the Public Sector”, Public Money

and Management, Vol.32, No.1, pp.35-40. Bogt, ter, H.J. (2004), ‘Politicians in Search of Performance Information? –Survey

Research on Dutch Aldermen’s Use of Performance Information’ Financial Accountability and Management, Vol.20, No.3, pp.221-252.

--- (2008), ‘Management Accounting Change and New Public Management in Local Government’ Financial Accountability and Management, Vol.24, No.3, pp.209-241.

Boyne, G., C. Farrell, J. Law, M. Powell and R. Walker (2003), Evaluating Public Management Reforms, Buckingham, Open University Press.

Burns, J. and R.W. Scapens (2000). “Conceptualizing Management Accounting Change: An Institutional Framework”, Management Accounting Research, Vol.11, No.1, pp.3-25.

Carlin, T.M. (2006), ‘Victoria’s Accrual Output Based Budgeting System-Delivering as Promised? Some Empirical Evidence’ Financial Accountability and Management, Vol.22, No.1, pp.1-20.

Campos, E. and S. Pradhan (1996), ‘Budgetary Institutions and Expenditure Outcomes’ Policy Research Working Paper 1646, Washington, World Bank.

Carpenter, V.L. and E.H. Feroz (2001). “Institutional Theory and Accounting Rule Choice: An analysis for US state governments’ decisions to adopt generally accepted accounting principles” Accounting, Organizations and Society, Vol.26, No.7/8, pp.565-596.

Cohen, M.D., J.G. March and J.P. Olsen (1972). “A Garbage Can Model of Organizational Choice”, Administrative Science Quarterly, Vol.17, No.1, pp.1-25.

Collin, S-O, Y., T. Tagesson, A. Andersson, J. Cato and K. Hansson (2009). “Explaining the Choice of Accounting Standards in Municipal Corporations: Positive accounting theory and institutional theory as competitive or concurrent theories” Critical Perspective on Accounting, Vol.20, No.2, pp.141-174.

David, P. A. (1985). “Clio and the Economics of QWERTY”, American Economic Review, Vol.75, No.2, pp.332-337.

DiMaggio, P. and W. Powell (1983), ‘The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields’ American Sociological Review, Vol.48, No.2, pp.147-160.

Falkman, P. and T.Tagesson (2008). “Accrual accounting does not necessary mean

22

accrual accounting: Factors that counteract compliance with accounting standards in Swedish municipal accounting” Scandinavian Journal of Management, Vol.24, No.3, pp.271-283.

Godfrey, A.D., P.J. Delvin and M. C. Merrouche. (2001), ‘A Diffusion-Contingency Model for Government Accounting Innovations’ in A. Bac (ed.), International Comparative Issues in Government Accounting, Boston: Kluwer.

Heinrich, C. and L.E. Lynn (2000). Governance and Performance-New Perspectives, Washington: Georgetown University Press.

Hood, C. (1983). The Tools of Government, London: Macmillan. --- (1991), ‘A Public Management for All Seasons?’ Public Administration, Vol.69, No.1,

pp.3-19. Hussein, M.E. (1981). “The Innovative Process in Financial Accounting Standards

Setting” Accounting, Organizations and Society, Vol.6, No.1, pp.27-37. Jackson, A. and I. Lapsley (2003). “The Diffusion of Accounting Practices in the New

“Mnagerial” Public Sector”, The International Journal of Public Sector Management, Vol.16, No.4/5, pp.359-372.

Jones, R. (1991). “Comparative Governmental Accounting Research”, Staatswissenschaften und Staatpraxis, Vol.4, No.2, pp.548-552.

Jorge, S., E. Caperchione and R. Jones (2011). “Introduction: Comparative International Governmental Accounting Research (CIGAR): Bridging Researching and Networking” in R. Jones (ed.). Public Sector Accounting, Vol.4, Los Angeles: Sage.

Kasperskaya, Y. (2008). “Implementing the Balanced Scorecard: A Comparative Study of Two Spanish City Councils – An Institutional Perspective”, Financial Accountability and Management, Vol.24, No.4, pp.363-384.

Khan, A. and S. Mayes (2009). Transition to Accrual Accounting, Washington, DC:IMF. Kingdon, J.W. (1984). Agendas, Alternatives, and Public Policies, Boston: Little Brown

and Co. Kobayashi, M., K.Yamamoto, and K. Ishikawa (2011). “Usefulness of Accrual

Information in Non-mandatory Environment: the case of Japanese Local Government”, working paper.

Lande, E. (2006), ‘Accrual Accounting in the Public Sector: Between Institutional Competitiveness and the Search for Legitimacy’ in E. Lande and J-C, Scheid (eds.), Accounting Reform in the Public Sector: Mimicry, fad or Necessity, Paris: Experts Comptables Media.

Lüder, K. (1992), ‘A Contingency Model of Government Accounting Innovations in the Political-Administrative Environment’ Research in Governmental and Nonprofit

23

Accounting, Vol.7, pp.99-127. --- (1994), ‘The “Contingency Model” Reconsidered: Experiences from Italy, Japan and

Spain’ in E. Buschor and K. Schedler (eds.), Perspectives on Performance Measurement, Berne: Haupt.

--- (2002), ‘Research in Comparative Governmental Accounting over the Last Decade- Achievements and Problems’ in V. Montesinos and J. M. Vela (eds.), Innovations in Governmental Accounting, Boston: Kluwer.

Luft, J. and M.D. Shields (2002). “Zimmerman’s Contentious Conjectures: Describing the Present and Prescribing the Future of Empirical Management Accounting Research” The European Accounting Review, Vol.11, No.4, pp.795-803.

Marti, C. (2007), ‘Accrual Accounting, Fiscal Decentralisation and Governance: An Empirical Study in OECD Countries’ paper prepared for EGPA Conference.

Mattisson, O., S.Näsi and T. Tagesson (2004). “Accounting Innovations in the Public Sector” paper prepared for the 27th Annual Congress of the European Accounting Associations, Prague.

Meyer, J.W. and B. Rowan (1977). “Institutionalized Environments: Formal Structure as Myth and Ceremony”, American Journal of Sociology, Vol.83, No.2, pp.340-363.

Olson, O., J. Guthrie and C. Humphrey (1998). Global Warning: Debating International Developments in New Public Financial Management, Oslo: Cappelen Akademisk Forlag.

Paulsson, G. (2006), ‘Accrual Accounting in the Public Sector: Experiences from the Central Government in Sweden’ Financial Accountability and Management, Vol.22, No.2, pp.47-62.

Pierre, J. (1995), Bureaucracy in the Modern State: An Introduction to Comparative Public Administration , Aldershot: Edward Elgar.

Pina, V., L. Torres and A. Yetano (2009). “Accrual Accounting in EU Local Governments: One Method, Several Approaches” European Accounting Review, Vol.18, No.4, pp.765-807.

Pollitt, C. (2002). “Clarifying Convergence: Striking Similarities and Durable Differences in Public Management Reform”, Public Management Review, Vol.4, No.1, pp.471-492.

Pollitt, C. and G. Bouckaert (2011), Public Management Reform: A Comparative Analysis, 3rd edition, New York: Oxford University Press.

Powell, W.W. and DiMaggio, P. (1991). The New Institutionalism in Organizational Analysis, Chicago: Univ. Chicago Press.

Puxty, A.G., D.J. Cooper and T. Lowe (1987). “Nodes of Regulation in Advanced

24

Capitalism: Locating Accountancy in Four Countries” Accounting, Organizations and Society, Vol.12, No.3, pp.273-291.

Ryan, C., J. Guthrie and R. Day (2007). “Politics of Financial Reporting and the Consequences for the Public Sector” ABACUS, Vol.43, No.4, pp.474-487.

Ryan, C. (1998). “The Introduction of Accrual Reporting Policy in the Australian Public Sector: An Agenda Setting Explanation”, Accounting, Auditing and Accountability Journal, Vol.11, No.5, pp.518-539.

Sargiacomo, M. and D. Gomes (2011). “Accounting and Accountability in Local Government: Contributions from Accounting History Research”, Accounting History, Vol.16, No.3, pp.253-290.

Scharpf, F.W. (1997). Games Real Actors Play, Boulder, CO: Westview. Scott, R.W. (2001), Institutions and Organizations, 2nd edition, Thousand Oaks: Sage

Publications. Stewart, R. and J. Stewart (1994), Management for the Public Domain: Enabling the

Learning Society, London: St. Martin’s Press. Streeck, W. and P.C. Schmitter (1985). “Community, Market, State – and Associations?”

in Streeck, W. and P.C. Schmitter (eds.). Private Interest Government and Public Policy, London: Sage.

Tella, R.D. and E. Schargrosky (2003). “The Role of Wages and Auditing: During a Crackdown on Corruption in the City of Buenos Aires”, Journal of Law and Economics, Vol.46, No.1, pp.269-292.

Thelen, K. (1999). “Historical Institutionalism in Comparative Politics”, Annual Review of Political Science, Vol.2, No.1, pp.369-404.

Watt, R.L. and J. L. Zimmerman (1979). “The Demand for and Supply of Accounting Theories: the market for excuses” The Accounting Review, Vol.54, No.2, pp.273-305.

Yamamoto, K. (2000), ‘Accounting System Reform and Management in the Japanese Local Government’ in E. Caperchione and R. Mussari (eds.), Comparative Local Government Accounting , Boston:Kluwer.

--- (2004), ‘Agencification in Japan: Renaming or revolution?’ in C. Pollitt and C. Talbot (eds.), Unbundled Government, London: Routledge.

--- (2008). ‘What Matters in Legislator’s Information Use for Financial Reporting? – The Case of Japan’ in S. Jorge (ed.), Implementing Reforms in Public Sector Accounting, Coimbra: Coimbra University Press.

Yamamoto, K. (1989). “History of Public Sector Accounting in Japan”, Journal of Urban Management Review, Vol.5, No.1, pp.1-13 (in Japanese).

25

Yin, R. (1994), Case Study Research: Design and Methods, 2nd edition, London: Sage. Zimmerman, J.L. (1977). “The Municipal Accounting Maze: An Analysis of Political

Incentives” Journal of Accounting Review, Vol.15, Supplement, pp.107-144. Zysman, J. (1994). “How Institutions Create Historically Rooted Trajectories of

Growth”, Industrial and Corporate Change, Vol.3, No.2, pp.243-283.

26