The World Bankdocuments.worldbank.org/curated/en/877131468277180362/pdf/698380... · ECA Europe and...

61

Document of The World Bank Report No: 69838-KZ PROJECT APPRAISAL DOCUMENT ON A PROPOSED GRANT IN THE AMOUNT OF US$ 21,763,000 TO THE REPUBLIC OF KAZAKHSTAN FOR AN ENERGY EFFICIENCY PROJECT MAY 17, 2013 This document is being made publicly available prior to Board consideration. This does not imply a presumed outcome. This document may be updated following Board consideration and the updated document will be made publicly available in accordance with the Bank’s policy on Access to Information. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of The World Bankdocuments.worldbank.org/curated/en/877131468277180362/pdf/698380... · ECA Europe and...

Document of

The World Bank

Report No: 69838-KZ

PROJECT APPRAISAL DOCUMENT

ON A

PROPOSED GRANT

IN THE AMOUNT OF US$ 21,763,000

TO THE

REPUBLIC OF KAZAKHSTAN

FOR AN

ENERGY EFFICIENCY PROJECT

MAY 17, 2013

This document is being made publicly available prior to Board consideration. This does not imply a presumed outcome. This document may be updated following Board consideration and the updated document will be made publicly available in accordance with the Bank’s policy on Access to Information.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

(Exchange Rate Effective – April 30, 2013)

Currency Unit = Kazakhstan Tenge KZT151.28 = US$1

US$1.51 = SDR 1

FISCAL YEAR January 1 – December 31

ABBREVIATIONS AND ACRONYMS

CPEE Comprehensive Program for Energy Efficiency

MINT Ministry of Industry and New Technologies

CPS Country Partnership Strategy MOU Memorandum of Understanding CO2 Carbon dioxide MW Mega Watt DC Direct Contracting NCB National Competitive Bidding EA Environmental Assessment NGO Non-Government Organization EBRD European Bank for Reconstruction and

Development

NOx Mono-Nitrogen Oxides

ECA Europe and Central Asia KEEP Kazakhstan Energy Efficiency Project EE Energy Efficiency OECD Organization for Economic Cooperation

and Development EMF Environmental Management Framework OM Operations Manual EMP Environmental Management Plan OP Operational Policy EIRR Economic Internal Rate of Return PEFA Public Expenditure and Financial

Accountability ESCO Energy Service Company PFM Public Financial Management ESMAP Energy Sector Management Assistance

Program

PFS Project Financial Statements

FIRR Financial Internal Rate of Return PPL Public Procurement Law FM Financial Management PIU Project Implementation Unit GAC Governance and Anti-Corruption Action Plan RE Renewable Energy GCal Gigacalorie SBD Standard Bidding Documents GDP Gross Domestic Product SDC Swiss Agency for Development and

Cooperation GHG Greenhouse Gases SOE Statement of Expenditure GOK Government of Kazakhstan SOx Sulfur Oxide GWh Giga Watt hours SSS Single Source Selection IEA International Energy Agency TA Technical Assistance IFR Interim Unaudited Financial Report TJ Terajoule ISA International Standards on Auditing toe Tons of oil equivalent JSC Joint Stock Company UNDB United Nations Development Business KazEE KazakhEnergoExpertiza UNDP United Nations Development Program

Regional Vice President: Philippe H. Le Houerou Country Director: Saroj Kumar Jha

Sector Director: Laszlo Lovei Sector Manager: Ranjit J. Lamech

Task Team Leader: Mirlan Aldayarov

ii

KAZAKHSTAN Energy Efficiency Project

TABLE OF CONTENTS

I. STRATEGIC CONTEXT .................................................................................................1

A. Country Context ............................................................................................................ 1

B. Sectoral and Institutional Context ................................................................................. 1

C. Higher Level Objectives to which the Project Contributes .......................................... 5

II. PROJECT DEVELOPMENT OBJECTIVES ................................................................5

A. Project Development Objectives................................................................................... 5

B. Project Beneficiaries ..................................................................................................... 5

C. PDO Level Results Indicators ....................................................................................... 6

III. PROJECT DESCRIPTION ..............................................................................................6

A. Project Parts .................................................................................................................. 6

B. Project Financing .......................................................................................................... 8

C. Lessons Learned and Reflected in the Project Design .................................................. 8

IV. IMPLEMENTATION .......................................................................................................9

A. Institutional and Implementation Arrangements .......................................................... 9

B. Results Monitoring and Evaluation .............................................................................. 9

C. Sustainability............................................................................................................... 10

V. KEY RISKS AND MITIGATION MEASURES ..........................................................11

A. Risk Ratings Summary Table ..................................................................................... 11

B. Overall Risk Rating Explanation ................................................................................ 11

VI. APPRAISAL SUMMARY ..............................................................................................12

A. Economic and Financial Analyses .............................................................................. 12

B. Technical ..................................................................................................................... 13

C. Financial Management ................................................................................................ 13

D. Procurement ................................................................................................................ 14

E. Social (including Safeguards) ..................................................................................... 15

F. Environment (including Safeguards) .......................................................................... 15

iii

Annex 1: Results Framework and Monitoring...................................................................... 21 Annex 2: Detailed Project Description ................................................................................. 22 Annex 3: Implementation Arrangements .............................................................................. 26 Annex 4: Operational Risk Assessment Framework (ORAF) .............................................. 39 Annex 5: Implementation Support Plan ................................................................................ 43 Annex 6: Economic and Financial Appraisal ....................................................................... 46

iv

.

PAD DATA SHEET Kazakhstan

Energy Efficiency Project (P130013) PROJECT APPRAISAL DOCUMENT

.

EUROPE AND CENTRAL ASIA ECSEG

Report No.: PAD176 .

Basic Information Project ID Lending Instrument EA Category Team Leader P130013 Specific Investment

Loan B - Partial Assessment Mirlan Aldayarov

Project Implementation Start Date Project Implementation End Date 01-July-2013 30-Jun-2017 Expected Effectiveness Date Expected Closing Date 01-July-2013 30-Jun-2017 Joint IFC No Sector Manager Sector Director Country Director Regional Vice President Ranjit J. Lamech Laszlo Lovei Saroj Kumar Jha Philippe H. Le Houerou .

Borrower: Republic of Kazakhstan Responsible Agency: Ministry of Industry and New Technologies Contact: Kanysh Tuleushin Title: Vice Minister Telephone No.:

0077172299010 Email: [email protected]

Responsible Agency: KazakhEnergoExpertiza Contact: Sungat Esimkhanov Title: President Telephone No.:

0077172968609 Email: [email protected]

.

Project Financing Data(US$M) [ ] Loan [ ] Grant [ X ] Other [ ] Credit [ ] Guarantee For Loans/Credits/Others Total Project Cost (US$M): 23.06

v

Total Bank Financing (US$M):

0.00

.

Financing Source Amount(US$M) Borrower 1.30 Free-standing TF for ECA 21.76 Total 23.06 .

Expected Disbursements (in USD Million) Fiscal Year

2013 2014 2015 2016 2017 0000 0000 0000 0000

Annual 2.50 6.00 8.30 4.70 0.26 0.00 0.00 0.00 0.00 Cumulative

2.50 8.50 16.80 21.50 21.76 0.00 0.00 0.00 0.00

.

Project Development Objective(s) The Development Objectives of the proposed project are to improve: (a) energy efficiency in public and social facilities; and (b) the enabling environment for sustainable energy financing. .

Components

Component Name Cost (USD Millions) Development and implementation of demonstration subprojects in public and social facilities

19.00

Technical assistance 4.06 .

Compliance Policy Does the project depart from the CAS in content or in other significant respects?

Yes [ ] No [ X ]

.

Does the project require any waivers of Bank policies? Yes [ ] No [ X ] Have these been approved by Bank management? Yes [ ] No [ X ]

Is approval for any policy waiver sought from the Board? Yes [ ] No [ X ] Does the project meet the Regional criteria for readiness for implementation? Yes [ X ] No [ ] .

Safeguard Policies Triggered by the Project Yes No Environmental Assessment OP/BP 4.01 X Natural Habitats OP/BP 4.04 X

Forests OP/BP 4.36 X

Pest Management OP 4.09 X

Physical Cultural Resources OP/BP 4.11 X

vi

Indigenous Peoples OP/BP 4.10 X

Involuntary Resettlement OP/BP 4.12 X

Safety of Dams OP/BP 4.37 X

Projects on International Waterways OP/BP 7.50 X

Projects in Disputed Areas OP/BP 7.60 X .

Legal Covenants Name Recurrent Due Date Frequency Project implementation in accordance with the Project Operational Manual (OM)

X Yearly

Description of Covenant The Recipient shall cause the Project Implementing Entity to carry out the Project, in accordance with the provisions of a manual satisfactory to the World Bank (“Project Operational Manual”).

Name Recurrent Due Date Frequency Staffing and Maintenance of Project Implementation Unit (PIU)

X Yearly

Description of Covenant The Recipient shall cause the Project Implementing Entity to establish and maintain, throughout Project implementation, a PIU with terms of reference, staffing and resources satisfactory to the World Bank, and which shall be responsible for the day-to-day execution, financial management, procurement, monitoring and evaluation of the Project.

Name Recurrent Due Date Frequency Maintenance of Steering Committee X Yearly

Description of Covenant he Recipient shall establish and thereafter maintain, until the completion of the Project, the Steering Committee, chaired by MINT and with representatives of MINT, the Project Implementing Entity and several representatives from other Ministries of the Recipient, with operating procedures and functions satisfactory to the World Bank and further detailed in the Project Operational Manual.

Name Recurrent Due Date Frequency Subsidiary Agreement X Yearly

Description of Covenant The Recipient shall exercise its rights and carry out its obligations under the Subsidiary Agreement in such manner as to protect the interests of the Recipient and the World Bank and to accomplish the purposes of the Grant. Except as the World Bank shall otherwise agree, the Recipient shall not assign, amend, abrogate, waive or fail to enforce the Subsidiary Agreement or any of its provisions.

Name Recurrent Due Date Frequency Implementation in accordance with Environmental Management Framework (EMF)

X Yearly

vii

Description of Covenant The Recipient shall cause the Project Implementing Entity to carry out the Project in accordance with the EMF and the Project Implementing Entity shall not assign, amend, repeal or waive any provision of any one thereof, without the prior written approval of the World Bank.

Name Recurrent Due Date Frequency Submission of Project Reports X Yearly

Description of Covenant The Recipient shall monitor and evaluate the progress of the Project and prepare Project Reports. Each Project Report shall cover the period of one calendar semester, and shall be furnished to the World Bank not later than forty five days after the end of the period covered by such report.

Name Recurrent Due Date Frequency Submission of Completion Report X Yearly

Description of Covenant The Recipient shall prepare the Completion Report in accordance with the provisions of Section 2.06 of the Standard Conditions. The Completion Report shall be furnished to the World Bank not later than six months after the Closing Date.

Name Recurrent Due Date Frequency Maintenance of Financial Management System

X Yearly

Description of Covenant The Recipient shall cause the Project Implementing Entity to maintain a financial management system, satisfactory to the World Bank.

Name Recurrent Due Date Frequency Carrying out Audit and Audit Reports X Yearly

Description of Covenant The Recipient shall have its Financial Statements for the Project. The Recipient shall ensure that interim unaudited financial reports for the Project are prepared and furnished to the World Bank not later than forty five days after the end of each calendar quarter, covering the quarter, in form and substance satisfactory to the World Bank.

Name Recurrent Due Date Frequency Procurement X Yearly

Description of Covenant All goods, works non-consulting-services and consultants’ services required for the Project and to be financed out of the proceeds of the Grant shall be procured in accordance with the requirements set forth or referred to in World Bank Procurement Guidelines.

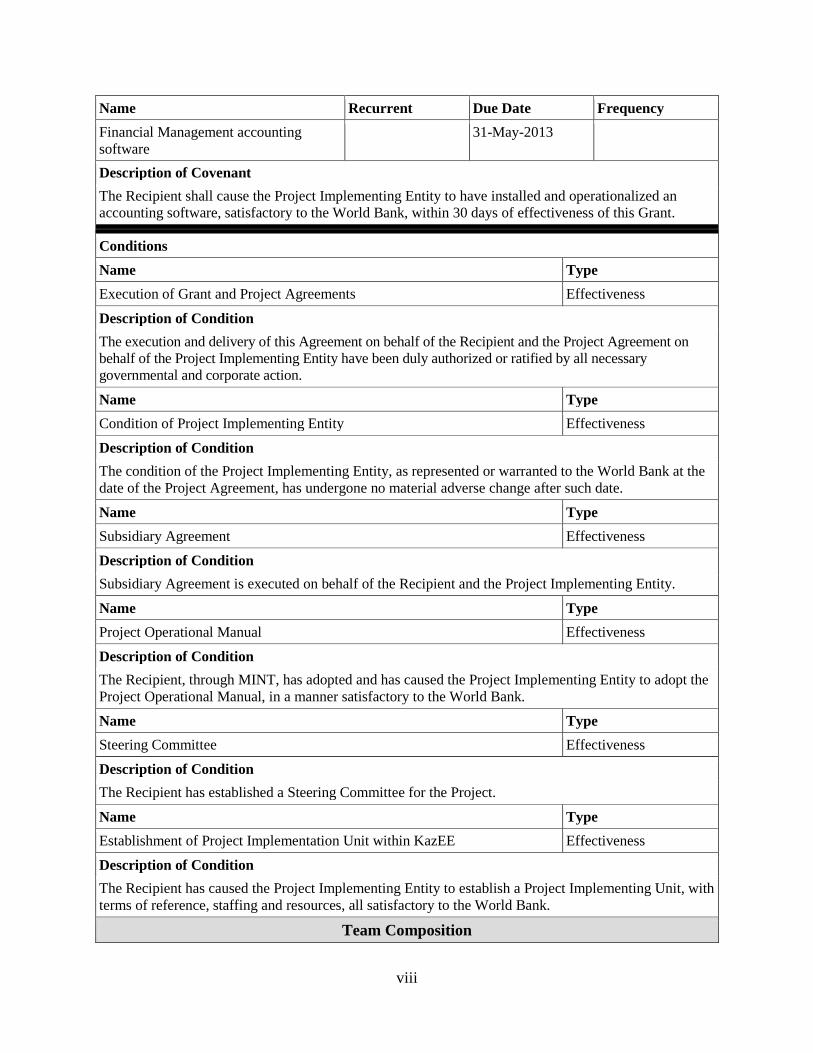

Name Recurrent Due Date Frequency Financial Management Specialist 30-June-2013 Description of Covenant The Recipient shall cause the Project Implementing Entity to hire a financial management specialist within 30 days of effectiveness of this Grant.

viii

Name Recurrent Due Date Frequency Financial Management accounting software

31-May-2013

Description of Covenant The Recipient shall cause the Project Implementing Entity to have installed and operationalized an accounting software, satisfactory to the World Bank, within 30 days of effectiveness of this Grant. .

Conditions Name Type Execution of Grant and Project Agreements Effectiveness

Description of Condition The execution and delivery of this Agreement on behalf of the Recipient and the Project Agreement on behalf of the Project Implementing Entity have been duly authorized or ratified by all necessary governmental and corporate action.

Name Type Condition of Project Implementing Entity Effectiveness

Description of Condition The condition of the Project Implementing Entity, as represented or warranted to the World Bank at the date of the Project Agreement, has undergone no material adverse change after such date.

Name Type Subsidiary Agreement Effectiveness

Description of Condition Subsidiary Agreement is executed on behalf of the Recipient and the Project Implementing Entity.

Name Type Project Operational Manual Effectiveness

Description of Condition The Recipient, through MINT, has adopted and has caused the Project Implementing Entity to adopt the Project Operational Manual, in a manner satisfactory to the World Bank.

Name Type Steering Committee Effectiveness

Description of Condition The Recipient has established a Steering Committee for the Project.

Name Type Establishment of Project Implementation Unit within KazEE Effectiveness

Description of Condition The Recipient has caused the Project Implementing Entity to establish a Project Implementing Unit, with terms of reference, staffing and resources, all satisfactory to the World Bank.

Team Composition

ix

Bank Staff Name Title Specialization Unit Joseph Paul Formoso Senior Finance Officer Finance CTRLA

Jasneet Singh Senior Energy Specialist Energy Efficiency ECSEG Sunil Kumar Khosla Lead Energy Specialist Energy ECSEG Roxanne Hakim Sr Anthropologist Social Safeguards ECSSO Aliya Kim Financial Management

Analyst Financial Management ECSO3

Anara Akhmetova Procurement Assistant Procurement ECCKZ Arcadii Capcelea Senior Environmental

Specialist Environmental Safeguards

ECSEN

Mirlan Aldayarov Energy Specialist Team Lead ECSEG Nurbek Kurmanaliev Procurement Specialist Procurement ECSO2 Artur Kochnakyan Energy Economist Economist ECSEG

Regina Oritshetemeyin Nesiama

Senior Program Assistant

Senior Program Assistant

ECSSD

Aliya Karakulova Operations Officer Operations ECSTR

Ma Dessirie Kalinski Finance Analyst Finance CTRLA Ramiro Ignacio Jauregui-Zabalaga

Counsel Legal LEGLE

Kathrin Hofer Jr Professional Officer Energy ECSEG

Sofia De Abreu Ferreira Legal Associate Legal LEGEN Yelena Yakovleva Team Assistant Team Assistant ECCKZ

Non Bank Staff Name Title Office Phone City

.

Locations Country First

Administrative Division

Location Planned Actual Comments

.

Institutional Data Sector Board Energy and Mining .

Sectors / Climate Change Sector (Maximum 5 and total % must equal 100)

x

Major Sector Sector % Adaptation Co-benefits %

Mitigation Co-benefits %

Energy and mining Energy efficiency in Heat and Power

100 100

Total 100

I certify that there is no Adaptation and Mitigation Climate Change Co-benefits information applicable to this project. .

Themes Theme (Maximum 5 and total % must equal 100) Major theme Theme % Financial and private sector development Infrastructure services for private sector

development 100

Total 100

1

I. STRATEGIC CONTEXT A. Country Context

1. The Republic of Kazakhstan is the largest economy in Central Asia. Two decades ago, emerging from the break-up of the Soviet Union, the Kazakh economy was half of its size today. Isolated from the world economy, it faced the immense challenge of economic transformation. Over the past decade, the country has made impressive policy strides, absorbed large natural resource-based earnings responsibly, progressed towards developing a rules-driven fiscal framework, strengthened public management and the business climate, and allocated resources for improved social services and critical infrastructure to sustain growth. Gross Domestic Product (GDP) per capita rose, in terms of constant 2011 dollars, from US$5,255 in 2000 to US$11,245 in 2011 and poverty incidence fell from 46 percent to below 6 percent over the same period.

2. Tightening liquidity in international financial markets in 2007 hit Kazakhstan’s financial sector. The second shock arose from the global financial crisis in 2008 and the associated sharp decline in commodity prices in 2009, which led to an economic slowdown. The authorities have taken a number of steps and supported output with stimulus programs directed at infrastructure and construction. The decisive approach to macroeconomic and financial sector management contributed to a quick recovery in output. Kazakhstan’s economy grew by 1.2 percent in 2009, 7.3 percent in 2010 and by 7.5 percent in 2011.

3. However, the economy remains highly natural resource-dependent, with minerals, oil and natural gas accounting for 73 percent of exports and 39 percent of GDP. Therefore, diversification of the economy and improved competitiveness are key development priorities. Development strategy of the Government of Kazakhstan (GOK) focuses on modernization, improved competitiveness and a shift towards growth based on non-oil sources. Increasing emphasis is also being put on strengthening governance, business-enabling environment and private sector enterprise. Following the Parliamentary elections of January 2012, the President of the country outlined the key government priorities within this overall strategy, including the renewed emphasis placed on regional development, diversification and improving energy efficiency of the national economy.

B. Sectoral and Institutional Context

4. Kazakhstan has abundant mineral and fuel resources and, with its proven oil, coal and uranium reserves, it ranks among the most energy-abundant countries in the world. Oil and natural gas output amounts to nearly a quarter of GDP and accounts for over two-thirds of exports.

5. In the electricity sector, the installed capacity is 19,400 MW, of which only 15,200 MW is available for generation. In 2011, coal-fired plants accounted for 84 percent of total generation, with hydro-power plants (10 percent) and gas-fired plants (6 percent) providing the balance. Total heat production is 390,963 TJ with 100 percent produced from coal.1 Industry is the largest consumer of electricity (about 75 percent), followed by households (11 percent) and transportation (2 percent). Kazakhstan’s rapid economic growth in the past decade has led to a sharp upswing in energy and electricity consumption. As a result, the earlier large surplus of 1 International Energy Agency (IEA), 2009

2

electricity generation is gradually disappearing and the supply-demand situation has become tight, causing occasional spot shortages during winter peak loads, especially in the booming southern part of the country. The International Energy Agency (IEA) projects Kazakhstan’s energy demand to increase at least 50 percent by 2035.

6. High Energy Intensity of the Economy. Energy is used very inefficiently in Kazakhstan, reflecting the legacy of the Soviet era. The economy is highly energy-intensive and is dominated by extractive industries and low level commodity processing. Moreover, dated and inefficient infrastructure, low energy prices mirroring the country’s rich fossil fuel endowments and distorted pricing, and the lack of targeted energy efficiency (EE) policies and enabling institutional framework contribute to inefficient use of energy.

7. Kazakhstan ranks among the top ten of the most energy-intensive economies in the world. It uses three times as much energy per unit of GDP (purchasing power parity-based) compared to the Organization for Economic Cooperation and Development (OECD) average. Mirroring the high energy intensity, the country is the fourth most carbon-intensive country in the world. With 1.4 kg CO2 per dollar of GDP emitted in 2008, Kazakhstan is more than twice as carbon intensive as the Europe and Central Asia (ECA) region on average and more than three times compared to the OECD average.

8. Adverse Impacts of High Energy Intensity. The high energy intensity incurs significant costs to the country in terms of economic competitiveness, public health and environment. International comparisons show that the industrial sector in Kazakhstan is significantly more energy intensive than in most countries. This negatively affects the competitive position of Kazakh semi-manufactured goods on international markets, especially in the energy-intensive metal product categories. Inefficient use of electricity contributes to power shortages, especially amid tightening supply-demand balance, and adversely impacts regional economic development

0

100

200

300

400

500

600

700

800

Turk

eyCr

oatia

Ger

man

yEu

rope

an U

nion

Japa

nFr

ance

OEC

D m

embe

rsHu

ngar

yU

nite

d St

ates

Tajik

istan

Czec

h Re

publ

icW

orld

Indi

aAr

ab W

orld

Paki

stan

Cana

daU

pper

mid

dle

inco

me

Indo

nesia

Bela

rus

Mol

dova

Kyrg

yz R

epub

licCh

ina

ECA

Sout

h Af

rica

Russ

ian

Fede

ratio

nKa

zakh

stan

Ukr

aine

Turk

men

istan

Uzb

ekist

an

Energy use (kg oil equivalent) per US$ 1,000 GDP - 2009 (constant 2005 PPP)

3

and social welfare. Energy-related pollution is one of the reasons for the existence of a number of environmental “hot spots” in the country with localized pollutants (e.g., NOx, SOx and particulate emissions) posing significant health risks.

9. Policy Context of Energy Efficiency. Historically, EE was not a high priority of the GOK. A “Law on Energy Saving” was adopted in 1997. However, it remained mainly declarative in nature due to the lack of specific national goals on EE improvements and implementable action plans. Recently, the GOK has devoted increasing attention to EE as a policy priority to prevent serious growth-slowing energy shortages, improve industrial competitiveness and environmental performance, and mitigate the social consequences of the recently rapid rise in domestic energy prices. In March 2010, the President of Kazakhstan set the goal to reduce energy intensity of the national economy by 10 percent by 2015 and 25 percent by 2020, making EE a top policy priority.

10. In January 2012, a new Energy Efficiency Law went into effect, which provides significantly more effective legal, regulatory and institutional framework for EE than the previous law. Among other things, the Law calls for mandatory energy audits of all business entities consuming 1,500 tons of oil equivalent (toe) or more per year. Public enterprises are mandated to prepare EE plans to ensure specified annual reductions in energy consumption. The Law provides for the allocation (of unspecified amounts) of state budget resources for the implementation of EE plans, audits, regional EE centers, training, etc.

11. For implementation support of the new Law, the GOK approved a Comprehensive Program for Energy Efficiency (CPEE), which is a time-bound action plan, containing 47 specific policies to be developed and measures with responsibilities assigned to various GOK agencies for implementation coordination and monitoring. The CPEE focuses on the most energy inefficient sectors of the economy, including industry and the municipal/residential sector. The aim is to tap the country’s vast energy saving potential, which is estimated at US$1.3 billion per year or 12 TWh of electricity, 2.5 million Gcal of heat and 7 million tons of coal. Mechanisms in the CPEE include fiscal incentives, standards and codes, awareness raising, state budget allocations with private sector leverage, and the creation of a National Energy Savings Fund.

12. Energy Savings Potential of Public and Residential Sectors. Under the CPEE, a sector-specific EE plan is to be drawn up for housing and social facilities. According to GOK estimates, the energy saving potential of public and residential sector is about 0.9 mtoe per year. The importance of these two sectors is underscored by the fact that they account for 55 percent of the country’s heat consumption and 20 percent of electricity consumption. The public sector uses about 4,100 GWh/year of electricity (5 percent of electricity generated) and about 59,000 TJ of heat (15 percent of heat consumption). About 70 percent of the public and residential buildings would require retrofitting in order to comply with applicable thermal efficiency standards of Kazakhstan. International experience shows that public office buildings in developing countries can readily achieve 20 to 40 percent energy savings through cost-effective retrofits. Among other things, the CPEE calls for mandatory energy audit of all public buildings and the application of EE performance criteria for major building renovations.

13. Institutional Framework for Energy Efficiency. The institutional structure related to EE was reorganized in 2010. The newly established Ministry of Industry and New Technologies (MINT) became responsible for energy policy setting, including EE and renewable energy. Before this reorganization, EE belonged to the Ministry of Energy and Mineral Resources, which

4

in 2010 was converted into Ministry of Oil and Gas. In addition to MINT a number of other state institutions, such as Agency of Construction and Communal Services and JSC Samruk-Energy, are involved in implementing EE initiatives. Furthermore, a separate dedicated EE agency, KazakhEnergyExpertise (KazEE), was established under MINT to implement EE initiatives, provide engineering and consultancy service and support MINT in developing the relevant EE primary and secondary legislation.

14. Specific Barriers to Energy Efficiency Investments. The abundance of opportunities for profitable EE investments is in sharp contrast with the limited number of successful EE projects and the low volume of actual investments, particularly in the public sector. Reasons for this disparity are informational, technical, financial, institutional and policy/procedural barriers constraining the promotion and market penetration of EE. These include:

(a) Energy pricing. Energy tariffs determine the financial viability of EE investments. Despite substantial recent increases, the GOK-regulated retail electricity and heat tariffs are still considered significantly below the full economic cost-recovery levels. Furthermore, in most cases, the heat services are billed based on regulated norms rather than on consumption, which does not encourage energy savings by end-users. This is a major factor in reducing the financial viability of EE projects.

(b) Financial barriers. The shortage of readily available and affordable debt financing is a key barrier to the uptake of EE projects in public facilities. Commercial banks are generally not familiar with financial and technical issues involved in EE projects and perceive the risks to lending to municipal and other public entities, as well as transaction costs of such projects, to be high. The excessively risk-averse bank behavior, high collateral requirements and lack of viable delivery mechanisms have also constrained EE financing. As with many post-Soviet states, a culture of municipal financing and credit is lacking, with many public entities reliant on state budget transfers to cover most if not all of their expenses and face borrowing restrictions. On the other hand, the state budget EE funding for municipal and public entities is potentially available but requires financing frameworks to be developed.

(c) Lack of information, weak technical capacities and high perceived risks. The lack of technical skills, information and awareness hampers the demand for EE products and services. Frequently, potential project sponsors lack the capacity to develop high quality bankable EE investment proposals, or are skeptical of the actual energy cost savings. Therefore, end users, particularly those in the public sector, are reluctant to undertake investments if they cannot be sure the operational savings will pay for the underlying investments. The EE market is currently underdeveloped due to weak technical capacity and lacking demand for EE services and goods. For instance, there are a number of energy audit companies, both local and subsidiaries of international companies, but almost no ESCO operating in the market.

(d) Institutional and regulatory barriers. Despite GOK’s recent considerable policy efforts, the institutional and regulatory framework for EE remains largely fragmented and most measures have yet to be fully implemented. While the main EE law was adopted, secondary legislation and regulations still need to be developed and enforced, including budgeting, procurement, certification schemes, audit and

5

benchmarking. Furthermore, the public sector suffers from a range of procedural barriers, from budgeting to procurement, which tend to be rigid in nature and prevent many EE improvements from being made.

15. Bilateral and multilateral support for EE. Various donors and multilateral institutions, such as GEF, UNDP and EBRD, are active in supporting the GOK to address the main barriers to EE. For instance, EBRD supported financing EE measures in the privately-owned industrial sector through a US$75 million credit line. The EE financing facility targeted medium and large private enterprises with typical investments ranging from US$ 250,000 to US$ 2,500,000. UNDP supported projects include activities to remove barriers to EE in municipal heat and hot water supply, including assistance to establish ESCOs, EE design and construction of residential buildings, as well as TA activities to strengthen the legal, regulatory and institutional frameworks. Aside from a few pilot audits, no donor has an investment-oriented program targeted at the public sector.

C. Higher Level Objectives to which the Project Contributes

16. The proposed project supports the GOK’s new policy focus to improve and promote EE. By providing much needed advisory policy and regulatory support, as well as hands-on capacity building related to the design, implementation and financing of EE initiatives, the project addresses existing barriers and responds to pressing economic and environmental needs of the country. Early implementation of a critical mass of projects will also help the institutions better understand the implementation realities, which can greatly help inform subsequent policies and regulatory measures.

17. Assisting Kazakhstan in improving EE is consistent with key objectives of the Bank’s new Country Partnership Strategy (CPS), specifically by: (i) supporting increased trade competitiveness by reducing the energy intensity of mineral-resource-based exportables; and (ii) safeguarding the environment by reducing pollution, including CO2 emissions caused by wasteful energy use.

II. PROJECT DEVELOPMENT OBJECTIVES A. Project Development Objectives

18. The Project Development Objectives of the proposed project are to improve: (a) energy efficiency in public and social facilities; and (b) the enabling environment for sustainable energy financing.

B. Project Beneficiaries

19. Expected beneficiaries of the project are:

(a) Clients in public facilities (school students, elderly people, hospital patients, etc.). Improvements in EE are expected to have positive impacts on living and working conditions in the targeted facilities by improving indoor comfort levels and healthier environments (e.g. better lighting and heating, improved indoor air quality).

6

(b) Municipal authorities: by supporting EE projects in public facilities with social benefits through improved building functionality and reduced absenteeism as well as energy cost savings.

(c) Ministry of Industry and New Technologies: by building technical, policy and institutional capacity related to EE.

(d) Commercial suppliers: by building demand for their EE goods and services, while building their capacity to implement projects.

C. PDO Level Results Indicators

20. Expected key PDO level results of the proposed project include: (i) quantified energy savings achieved from implementation of economically viable EE projects in public and social facilities; and (ii) improved policy and institutional framework for EE to allow sustainable energy financing mechanisms to be developed and launched.

III. PROJECT DESCRIPTION A. Project Components

21. The project will be supported by a US$21.76 million grant from the Government of Switzerland, Swiss Agency for Development and Cooperation (SDC), to be channeled through a Trust Fund to be set up with the World Bank, as well as an estimated US$1.3 million in possible co-financing from the participating institutions, utilities, and/or provinces/municipalities. The project consists of two Parts: an investment part and a technical assistance (TA) part, which are outlined below. More details are provided in Annex 2.

22. Part 1: Development and Implementation of Demonstration Subprojects in public and social facilities (estimated cost: US$19.0 million, including US$17.7 million from the World Bank grant and US$1.3 million from local co-financing). This Part will finance carrying out of eligible EE projects (“subprojects”) to support a reduction in energy use of public buildings, pursuant to criteria set forth in the Project Operational Manual. This part will finance EE projects (“subprojects”) in public and social facilities, such as schools, kindergartens, clinics/hospitals, and street lighting. These subprojects will generate demonstrable energy cost savings and social co-benefits (e.g., improved indoor temperature and comfort, reduced student sick days). Three annual batches of investment projects, selected through competitive proposals, will be developed and implemented. In Year 1, these investments will be fully grant financed to help build capacity within the PIU, MINT, service providers and others; in the subsequent years, some co-financing will be requested from the beneficiaries as selection criteria to help shift to a more sustainable model.

23. Target facilities will be competitively selected based on calls for proposals from the Project Implementation Unit (PIU). Eligible subprojects must meet basic eligibility criteria, to be reflected in the Project OM, which would include: (i) confirmation of public ownership; (ii) structural soundness of the facility; and (iii) absence of plans for closure, downsizing or privatization. Measures to be eligible for support will include upgrades to reduce the energy use of public buildings, including building envelop measures (insulation of walls, basements and attics, repair/replacement of external doors and windows), heating and cooling systems (boiler

7

upgrade/replacement, fuel switching, reflective surfacing of walls behind radiators, control systems, pipe insulation, chiller/AC replacement, heat pumps), lighting (compact fluorescent lamps, high pressure sodium vapor, light emitting diodes), power systems (following the requirements of EMF), and other energy-using systems (e.g., pumps and fans, solar water heating). All measures must be financially justified, i.e. having a simple payback period of less than eight years. A limited additional funding for EE measures with longer payback period may be provided to ensure reasonably full renovation.

24. The subprojects will be implemented in annual batches, so that construction can take place between heating seasons. Financing of public facilities will be demand-driven but subject to agreed ranking criteria. In Year 1, each of the 14 oblasts (administrative regions) and the cities of Astana and Almaty will be able to nominate facilities where energy use is high and an energy audit has already been conducted. The PIU will review the energy audit reports and rank the facilities based on potential energy savings (i.e., percentage of potential energy reduction with all eligible measures). With a budget of about US$4.5 million in Year 1, it is estimated that about 20 schools/kindergartens, 5 hospitals and one street lighting project can be implemented. MINT will then enter into a Memorandum of Understanding (MOU) with each facility’s oblast akimat (regional administration), and KazEE would enter into a subproject agreement with the local public authority and the Project Beneficiary (i.e., schools, hospitals or municipalities), and then conduct procurement of any supplemental energy audits and engineering designs, as well as construction works for selected subprojects. In order to ensure regional distribution, the annual allocation per oblast will not exceed US$1.5 million, and subprojects should not receive more than US$150,000 per school/kindergarten, US$250,000 per hospital and US$500,000 per street lighting subproject. No EE sub-project should cost less than US$50,000.

25. Based on experiences gained in Year 1, and results of EE market assessment studies, the selection and eligibility criteria for the subsequent years will be subject to modification to allow the testing of alternative business models, contracting and financing arrangements. For example, future phases are expected to include requirements for local co-financing, use of simplified ESCO contracts, and other mechanisms to help incrementally develop the EE market and capacity among the government and service providers towards commercially sustainable energy investments, which could then be scaled-up through a dedicated EE financing mechanism. About US$6 million will be allocated from the grant for Year 2 and US$7.2 million for Year 3.

26. Part 2: Technical assistance (US$4.06 million from the World Bank grant). TA will also be provided to MINT and KazEE to help ensure effective project implementation, as well as support the broader policy dialogue and institutional/market development to ensure project activities can be sustained. The TA part will include: (i) PIU project implementation support and capacity building (e.g., technical advisors, construction supervision, monitoring and reporting, project audit, staff training); (ii) technical studies, including EE market assessments, energy audits, and pilot oblast EE Master Plans for replication in the other regions; (iii) awareness, outreach and information campaigns; (iv) legal, institutional and regulatory reviews and workshops, with a focus on sustainable financing options, ESCOs and regulatory gaps/constraints to meeting GOK’s EE targets; (v) design of a sustainable energy financing mechanism (e.g., EE Fund) with detailed design and implementation plan; and (vi) other technical studies and TA as identified during project implementation to support the sustainable energy agenda of the GOK.

8

B. Project Financing

Lending Instrument

27. The IBRD instrument for KEEP is an Investment Project Financing (IPF), funded from a Free-Standing Trust Fund Grant. The IPF will be provided on a grant basis.

Project Cost and Financing 28. The total project cost is US$23,063,000. The project would be funded by a US$21,763,000 grant from SDC to be channeled through a Trust Fund to be set up with the World Bank. The Trust Fund will be managed and administered by the World Bank. An estimated US$1.3 million co-financing is expected to be provided from the participating institutions, utilities, and/or provinces/municipalities.

Project Parts Project cost (million US$)

IBRD Financing

(million US$)

% IBRD Financing

Local co-financing (million

US$)

% Local Co-Financing

1. Development and Implementation of Demonstration Subprojects in public and social facilities 2. TA Total Baseline Costs Physical contingencies Price contingencies

19.00 4.06 23.06 - -

17.70 4.06 21.76 - -

93% 100% 94% - -

1.3 - 1.3 - -

7% 6% - -

Total Project Costs Interest During

Implementation Front-End Fees

Total Financing Required

23.06 - - 23.06

21.76 - - 21.76

94% - - 94%

1.3 - - 1.3

6% - - 6%

C. Lessons Learned and Reflected in the Project Design

29. The design of the project draws upon experience and lessons learned from previous World Bank EE projects targeting the public sector within the ECA region, as well as other donors working in Kazakhstan: Armenia Energy Efficiency (2012), Montenegro Energy Efficiency (2008), Macedonia Sustainable Energy (2006), Bulgaria Energy Efficiency (2005), Croatia Energy Efficiency (2003), and Serbia Energy Efficiency (2004), as well as from recent World Bank and ESMAP publications. Key lessons include:

(a) Early successes and well-documented case studies are needed to establish program credibility and help demonstrate that EE can save money.

(b) There is a need to introduce market principles early on in a program (e.g., less than 8-10 year simple payback period, co-financing from beneficiaries) to transition to a more commercially sustainable system in outer years.

9

(c) When introducing innovative contracting mechanisms such as ESCOs, it is advisable to begin with simpler models and introduce more complex transactions as the market develops and supporting systems evolve. Developing partnerships with potential service providers, commercial financiers and other market actors also helps build program momentum.

(d) Strong technical energy diagnoses, clear and transparent eligibility and selection criteria, sound measurement and verification (M&V) procedures, and a strong initial pipeline are critical to ensure quick disbursements and achievement of desired outcomes. Building the pipeline through outreach and other mechanisms throughout the project, and maintaining some flexibility as the market continues to evolve, are also needed.

(e) Ongoing policy dialogue and TA is critical to overcome emerging obstacles during implementation and enhance the enabling environment for EE, sustainable energy financing, ESCO development, etc. Other donors’ efforts to help develop sustainable EE market players, such as ESCOs, produced mixed results. This experience reconfirms the importance of the issues related to public budgeting, procurement, municipal finance and other aspects to be a part of this dialogue to ensure long-term sustainability.

IV. IMPLEMENTATION A. Institutional and Implementation Arrangements

30. On behalf of the GOK, MINT will be responsible for the overall project coordination and oversight. MINT will need to: (i) approve the overall project framework, Operations Manual (OM), subproject criteria; and (ii) ensure intra-GOK coordination and communication. A Steering Committee, chaired by MINT, will be established to ensure coordination within GOK and would include representatives of MINT and KazEE, the Ministry of Finance, the Ministry of Economy and Budget Planning, the Ministry of Regional Development, the Ministry of Environmental Protection, and others. Day-to-day project implementation will be delegated to the PIU to be established within KazEE, a specialized EE entity under MINT. These roles and responsibilities will be reflected in a Subsidiary Agreement between MINT and KazEE, as well as in the OM.

31. The PIU will have primary responsibility for project implementation, including subproject ranking, signing MOUs with oblasts, consultant/contractor procurement, technical supervision, financial management, monitoring and reporting. The PIU will prepare Terms of Reference (TOR) for the TA activities, prepare and evaluate tenders and sign construction works contracts under Part 1. The PIU will process all payments and manage a Designated Account under the Project. The PIU will be staffed with experienced personnel to mitigate the risk in insufficient capacity. Further details on institutional and implementation arrangements are provided in Annex 3.

B. Results Monitoring and Evaluation

32. Results monitoring and evaluation activities will be carried out under the responsibility of the PIU, which will submit semi-annual implementation progress reports to the Bank. A simple

10

information management system for monitoring and evaluation will be developed by the PIU, based on the results indicators specified in Annex 1. The system will cover, inter alia, the project pipeline, disbursed, committed and invested amounts, co-financing by project beneficiaries, financial viability of EE subprojects, energy savings from implementation of EE measures, CO2 emission reductions, and gender-disaggregated numbers of project beneficiaries. The PIU will base its reporting on the commissioning and O&M reports provided by contractors. The PIU will verify the reports through a separate technical and field supervision. Emission reductions will be estimated based on the observed reduction in heating/energy intensity of retrofitted public and social facilities after implementation of EE measures.

33. For individual subprojects, pre- and post-project energy consumption will be estimated based on technical feasibility reports commissioned by end users and the PIU. As subprojects are implemented, commissioning will be carried out to document subproject performance and document actual energy savings. These data will be aggregated and reported in the implementation progress reports. The PIU has existing capacity to collect and process data required for monitoring and reporting of project results. In addition, regular monitoring and supervision activities of the Bank, in particular during the first two years of project implementation, are also expected to help increase the capacity of the PIU and improve the monitoring and reporting system within the implementing agency.

34. In addition, a mid-term review will be carried out to assess overall project progress and to inform on additional measures required to ensure that the project is successfully completed. A comprehensive impact assessment will be undertaken before the completion of the project in order to integrate experiences and lessons learnt into the development of future EE investments and, in particular, the dedicated EE financing mechanism to be designed under this project.

35. The cost of data collection, monitoring and evaluation will be covered by the incremental operating costs of the PIU. Further details on results monitoring and evaluation are provided in Annex 3.

C. Sustainability

36. Because the grant funds are limited and the need for investment in the public sector is large, sustainability is fundamental to the project design. The CPEE estimates that the immediate investment needs in the public sector are over US$2.7 billion. In Year 1, subprojects will be fully grant financed to help build capacity within the PIU, MINT, service providers and others. It will also yield valuable case studies and data for better understanding of the market needs and potential. In Year 2, the project would require modest co-financing from the provinces/municipalities, as selection criteria, to leverage the grant funds and introduce options for financing from service providers (e.g., ESCOs), commercial banks and other sources. Other contracting mechanisms may also be introduced, to allow for partial payments based on project performance (i.e., actual energy savings). In Year 3, it is expected that the co-financing criteria weighting will be increased and more complex financing and contracting mechanisms will be introduced. In order to ensure proper maintenance of retrofitted public and social facilities, a corresponding provision will be included in the Subproject Agreement with project beneficiaries. Under Part 2, EE market assessments will be conducted and financing mechanisms developed to help transition the program from a grant-funded to a more market oriented financing scheme, to allow for sustainability and scalability. Efforts will also be made to boost demand through

11

outreach campaigns while working with service providers and potential financiers to raise awareness and understanding of EE projects, their benefits, performance and risks.

37. The project, in collaboration with other donors, will help the GOK address the existing barriers by developing regulatory legislation and sustainable EE financing mechanisms, EE public outreach activities, strengthening technical capacities and providing trainings. Preliminary discussions with IFC and EBRD on key secondary legislation have already identified critical policy gaps that can be jointly discussed with MINT and other GOK agencies.

V. KEY RISKS AND MITIGATION MEASURES A. Risk Ratings Summary Table

Stakeholder Risk Rating Implementing Agency Risk - Capacity Moderate - Governance Substantial

Project Risk - Design Moderate - Social and Environmental Low - Program and Donor Low - Delivery Monitoring and Sustainability Moderate

Overall Implementation Risk Moderate

B. Overall Risk Rating Explanation

38. The risk related to the project preparation and implementation is rated Moderate before mitigation measures. The Moderate risk rating is based on the potential of delays in project implementation due to the limited experience of the PIU in managing similar projects, including in particular procurement and financial management, the need for substantial inter-ministerial consultations given complementary responsibilities but shared interests in improving EE in the target sectors among different Ministries, insufficient decision-making responsibilities by the PIU and/or insufficient ownership of the project at ministerial level, as well as the risks related to insufficient demand for EE investments in public and social facilities. These risks will be mitigated through a combination of measures, including the creation of a dedicated PIU with additional expert staff to support project implementation, provision of TA and training, close interaction between the Bank and the implementing agency, the establishment of a Steering Committee as a condition of effectiveness, and a detailed OM approved by MINT, clarifying roles, responsibilities and procedures for project implementation. The approved OM is also one of the conditions of effectiveness. Risks related to insufficient demand will be mitigated through timely pipeline development, outreach and awareness raising activities, structuring and packaging of services, as well as TA for issues related to public budgeting, public procurement and municipal finance in order to increase incentives for public and social facilities to invest in EE.

12

VI. APPRAISAL SUMMARY A. Economic and Financial Analyses

39. Economic and financial appraisal of the project was conducted through cost-benefit analysis. Economic costs and benefits were calculated at economic prices and exclusive of taxes and subsidies, and the assessment of financial costs and benefits was done at financial prices and inclusive of taxes and subsidies. The subprojects are considered economically and financially viable if the Net Present Value (NPV) of economic benefits and cash flows is positive and the Economic Internal Rate of Return (EIRR) and the Financial Internal Rate of Return (FIRR) are higher than the discount rate used.

40. Economic and financial appraisal was conducted for representative types of facilities to be financed under the project – healthcare and educational. The investment costs of energy efficiency measures and energy saving estimates are drawn from the energy audits prepared by two energy audit companies in the city of Shymkent. The reports were provided by KazEE. The assumptions and further details are presented in Annex 6.

41. Economic analysis. The main quantifiable economic benefit from EE investments in public and social facilities is the economic value of heat and electricity savings. Energy savings were valued at the estimated long-run average incremental cost of electricity and heat supply, depending on scope of EE measures planned. The main economic costs are the capital investment and incremental operating and maintenance (O&M) costs.

42. EE investments will also generate economic benefits that were not quantified in this analysis such as increased comfort level for occupants of the social and public facilities, improved quality of services provided by those facilities (e.g., improved indoor temperature and comfort, reduced student sick days) as well environmental externalities such as the reduction in GHG emissions, which were not quantified either.

43. Results of economic analysis suggest that EE investments have robust economic rates of return and simple pay-back periods in the range of 2-6 years. The details of the economic analysis are presented in the table below.

Table 1: Results of economic analysis of energy efficiency investments NPV (US$) EIRR (%) Payback (years) Healthcare facilities Regional Cancer Hospital 384,400 35 ≈3 Hospital N1 42,611 77 ≈2 Educational facilities School N20 103,429 17 ≈6 School N46 265,771 25 ≈4

44. Sensitivity analysis. The key parameters, which may significantly affect economic viability of EE investments, are the investment costs and the estimated energy savings. The impact of defined variation in those parameters is presented in Annex 6. The results of the sensitivity analysis suggest that even in case of significant and simultaneous deterioration of key input parameters, EE investments remain economically viable.

13

45. Financial analysis. The main financial benefit of energy efficiency investments is the reduction of energy bills of targeted facilities. The energy bill savings were valued at current heat and electricity tariffs. The main financial costs are the capital investments and incremental O&M costs. Results of financial analysis suggest that EE investments have robust financial rates of return and simple pay-back period in the range of 2-8 years. The details are presented in Table 2.

Table 2: Results of financial analysis of energy efficiency investments NPV (US$) FIRR (%) Payback (years) Healthcare facilities Shymkent City Regional Cancer Hospital 275,911 26 ≈4 Shymkent City Hospital N1 33,847 56 ≈2 Educational facilities Shymkent School N20 32,145 12 ≈8 Shymkent School N46 164,017 19 ≈6

46. Sensitivity analysis. The key parameters, which may significantly affect the financial viability of EE investments, are the investment costs and the estimated energy savings. The impact of defined variation in those parameters is presented in Annex 6The results of the sensitivity analysis suggest that EE investments in most of the sample facilities remain financially viable even in case of significant simultaneous deterioration of the key input parameters.

B. Technical

47. The typically small-sized subprojects to be funded by the Project involve standard, well proven technology for EE improvements in end-use applications of public facilities (e.g., schools, kindergartens, hospitals, street lighting) with demonstrable energy savings. No technology risk should be incurred. The Project will primarily finance EE improvements in building envelop (insulation of walls, basements and attics, repair/replacement of external doors and windows, window optimization), heating and cooling systems (boiler upgrade/replacement, reflective surfacing of walls behind radiators, automatic control systems, pipe insulation, chiller/air condition replacement, heat pumps), lighting (compact fluorescent lamps, high pressure sodium vapor, light emitting diodes), power systems (transformers, capacitors), other energy-using systems (e.g., pumps and fans, solar water heating), fuel switching (e.g., from fossil fuel to biomass or geothermal energy). The subproject design solutions will take into account the climatic parameters varying across the large country. Heating and ventilation systems will allow for programming of the ventilation regime and inside temperature by the occupants. The subprojects will have net positive environmental impacts.

C. Financial Management

48. The financial management (FM) arrangements of KazEE have been assessed and found to be overall satisfactory to the Bank. The Project FM assessment carried in May 2012 established that KazEE has generally acceptable FM arrangements in place. In particular: (i) KazEE has a functioning automated accounting system; (ii) a well-organized filing system; (iii) the internal control system is adequate; (iv) KazEE has experience of working with commercial

14

banks; and (v) its accounts are audited on an annual basis. A time-bound action plan has been agreed to bring the existing FM of the company into fully satisfactory status that includes: (i) development of the module on the basis of existing software to meet the project’s reporting and accounting requirements within 30 days after project effectiveness; and (ii) recruiting a dedicated FM Specialist to support KazEE’s Accounting Unit within 30 days after project effectiveness. As an interim arrangement KazEE will assign one staff from the Accounting Unit to the project.

49. While KazEE has an accounting policy that it follows, the project specific controls, accounting, budgeting, flow of funds, reporting, staffing and external auditing procedures will be documented in the FM section of the OM.

50. Annual audits of the project financial statements will be provided to the Bank within six months after the end of each fiscal year and at the project closing. The Recipient has agreed that it will publish (on the KazEE website) audit reports for the project within one month after receipt of these reports from auditors. The Bank will make them publically available according to the World Bank Policy on Access to Information. As part of project implementation support and implementation support missions, quarterly interim unaudited financial reports (IFRs) will be reviewed and regular risk-based FM missions conducted.

51. Under the Bank’s accountability assessment (PEFA), issued in May 2009, the overall fiduciary risk in Kazakhstan is assessed as substantial. According to the PEFA report, various key elements of the country’s public finance management (PFM) system, including accounting, internal audit, financial reporting and external audit are still weak. The country also scores poorly in the Transparency International’s Corruption Perception Index, which is an indication of high perceived corruption. The project will thus be implemented in an environment of weak PFM capacity and significant fiduciary risk due to high perceived corruption. Therefore, ring-fencing measures will be made, including requirements for additional reporting and independent audits of the project financial statements by auditors satisfactory to the Bank. The project will only rely on country systems in budgeting and partially internal controls. The overall FM risk of the project is Moderate after mitigation measures, with Inherent and Control Risks rated as Substantial before, and Moderate after mitigation measures.

D. Procurement

52. Procurement for the project will be carried out in accordance with World Bank procurement Guidelines. Specifically, procurement will be carried out in accordance with: (i) “Guidelines: Procurement of Goods, Works, and Non-Consulting Services under IBRD Loans and IDA Credits & Grants by World Bank Borrowers, dated January 2011; and (ii) “Guidelines: Selection and Employment of Consultants under IBRD Loans and IDA Credits & Grants by World Bank Borrowers’, dated January 2011; and (iii) the provisions stipulated in the Grant Agreement.

53. Public procurement reform in Kazakhstan began in 1996. The initial Public Procurement Law (PPL) was first enacted in June 1997. A new PPL was introduced on July 21, 2007 (No. 303-III) and put into force on January 1, 2008. Several amendments were introduced. The current/applicable PPL is dated July 2007 with amendments on January 13, 2012. The procurement system in Kazakhstan is highly decentralized, with some centralized planning and oversight. The GOK has been consistently adjusting the public procurement system to align it with the improvements and changes in the overall market economy system. However, the Bank’s

15

June 2009 PEFA report identified the following deficiencies in the implementation of the PPL: (a) excessive use of less competitive procurement methods and single-source procurement; and (c) perception of of the complaint handling system not being fully independent.

54. The overall procurement risk for the project is high. The risk rating is based on experience from past and ongoing Bank-financed projects in Kazakhstan, general public procurement environment and the current capacity of KazEE in administering procurement. To mitigate the risk, an experienced Procurement Specialist familiar with Bank procurement procedures will be hired by the PIU. The Bank’s procurement staff based in the country office will provide advice and assistance on a regular basis. The procurement packages will be carefully prepared in order to foster competition, wide and advance advertising will be carried out, and proactive search and contact of potential contractors, suppliers and consultants will be ensured. The procurement plan covering the initial 18 months of project implementation is being prepared by KazEE. Details on project procurement arrangements are presented in Annex 3.

E. Social (including Safeguards)

55. The project has substantial positive social impacts. By promoting EE in public facilities, with a focus on schools, hospitals and street lighting, subprojects in Part 1 will benefit a wide section of the economically weaker sections that cannot afford private facilities and rely heavily on these public services. By investing in energy saving measures, the public facilities will be able to reduce their operating costs and improve service in terms of more comfortable environment, without any economic burden being transferred upon the beneficiary.

56. Due to the selection and eligibility criteria of the subprojects, which focus on hospitals, schools and street lighting, the project will have a high proportion of the most vulnerable sections of society, i.e., women, children, sick and elderly in the beneficiary target group. Street lighting also results in higher safety levels, especially for women and children. Project monitoring and beneficiary assessment reports will also describe the specific impacts/benefits on some of the above mentioned vulnerable groups.

57. The project will consult stakeholders during preparation and implementation. The TA part includes awareness, outreach and information campaigns related to demonstration projects financed under Part 1. These case studies will analyze the impacts on the target vulnerable groups and draw lessons. The development of outreach materials to help increase awareness of the benefits and importance of EE will draw on the involvement of civil society actors such as NGOs, research bodies, etc. to the extent feasible.

58. Any subproject which would require land acquisition will be excluded from funding. This will be explicitly indicated in the OM. The implementing agency and the Bank’s project team will have the responsibility to ensure observance of this provision during implementation.

F. Environment (including Safeguards)

59. According to the World Bank safeguards policy on environmental assessment (EA, OP 4.01) the project is rated as Category B as it may generate some environmental and social impacts. While these impacts are expected to be mostly positive (reduced energy consumption and pollutant emissions, improved indoor temperature and comfort, reduced student sick days), the project might also generate some adverse impacts, which would be associated with air pollution, dust, noise, construction wastes, asbestos, occupational hazards, etc. All these adverse

16

impacts are minor, temporary, site specific, and can be easily avoided and/or mitigated during project implementation. To address these potential impacts, the PIU (KazEE) has prepared an Environmental Management Framework (EMF) including a sample Environmental Management Plan (EMP)/Checklist that provides mitigation measures for the noted adverse impacts. The EMP Checklist covers all typical mitigation approaches to common civil works contracts with localized impacts. These measures will be appropriately included in the design and technical specifications and their implementation in the respective contracts. The EMF contains: (i) rules and procedures for environmental screening; (ii) guidance for preparing subproject EMP Checklist; (iii) implementing responsibilities; and (iv) monitoring, supervision and reporting requirements on implementing EMP provisions. Project activities will not change boundaries, ownership or use rights in the project area and will work within the public buildings without any expansion or need of land and thus the Bank’s OP 4.12 is not triggered. Furthermore, it has been confirmed that there will be no impacts on Forests and Natural Habitats as all public and social buildings to be selected for project financing are located in existing settlements. The client also confirmed the project will not support any subprojects involving buildings which might be considered as Physical Cultural Resources and thus OP 4.11 is not triggered. In accordance with Bank requirements, the EMF has been disclosed and consulted in the country before appraisal.

17

Annex 1: Results Framework and Monitoring

.

Country: Kazakhstan Project Name: Energy Efficiency Project (P130013)

.

Results Framework .

Project Development Objectives .

PDO Statement The Development Objectives of the proposed project are to improve: (a) energy efficiency in public and social facilities; and (b) the enabling environment for sustainable energy financing. .

Project Development Objective Indicators

Cumulative Target Values Data Source/ Responsibility for

Indicator Name Core Unit of

Measure Baseline YR1 YR2 YR3 YR4 End Target Frequency Methodology Data Collection

Quantified energy savings achieved2

Gigawatt-hour (GWh)

0 0 195 500 825 825 Semi-annually

PIU implementation progress reports, based on commissioning reports

PIU

Development of sustainable energy financing mechanisms

Text 0

EE market assessment completed; financing options

Financing options selected; preparation of

Detailed arrangements for financing mechanism

New financing mechanisms adopted

New financing mechanisms launched

Semi-annually

PIU implementation progress reports

PIU

2 Cumulative energy savings over 15-years useful life of subprojects;

18

developed framework completed

s prepared

.

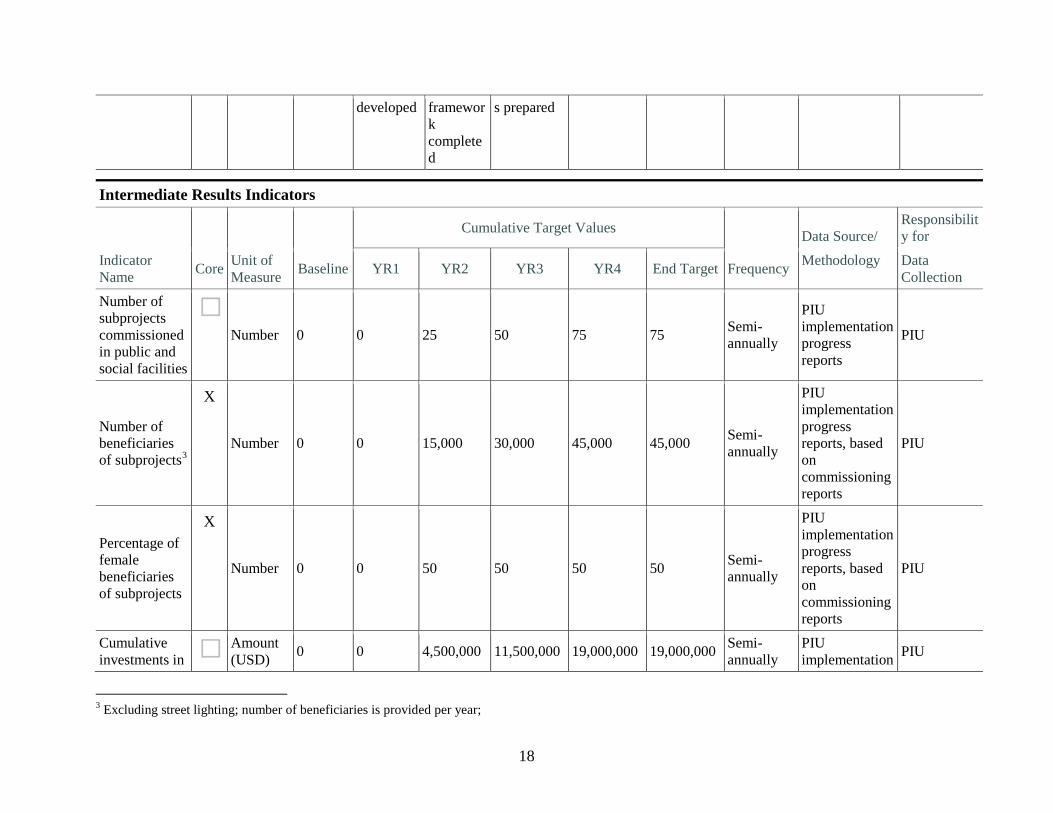

Intermediate Results Indicators

Cumulative Target Values Data Source/ Responsibility for

Indicator Name Core Unit of

Measure Baseline YR1 YR2 YR3 YR4 End Target Frequency Methodology Data Collection

Number of subprojects commissioned in public and social facilities

Number 0 0 25 50 75 75 Semi-

annually

PIU implementation progress reports

PIU

Number of beneficiaries of subprojects3

X

Number 0 0 15,000 30,000 45,000 45,000 Semi-annually

PIU implementation progress reports, based on commissioning reports

PIU

Percentage of female beneficiaries of subprojects

X

Number 0 0 50 50 50 50 Semi-annually

PIU implementation progress reports, based on commissioning reports

PIU

Cumulative investments in

Amount (USD) 0 0 4,500,000 11,500,000 19,000,000 19,000,000 Semi-

annually PIU implementation PIU

3 Excluding street lighting; number of beneficiaries is provided per year;

19

public and social facilities

progress reports, based on commissioning reports

CO2 emission reductions in retrofitted facilities through EE investments4

Metric ton (CO2) 0 0 95,000 240,000 400,000 400,000 Semi-

annually

PIU implementation progress reports, based on commissioning reports

PIU

Development of legal, institutional and regulatory basis for setting up EE financing mechanisms

Text

EE law, program in place; but no specific provisions on EE financing

EE policy gap assessment completed

Relevant EE package prepared

Package submitted for GOK approval

--

Package submitted for GOK approval

Semi-annually

PIU implementation progress reports

PIU

Number of local EE market institutions (including ESCOs and finance institutions) and co-financing arrangements involved

Number 0 0 3 5 7 7 Semi-annually

PIU implementation progress reports

PIU

4 Cumulative CO2 emission reductions over 15-years useful life of subprojects;

20

Number of trainings conducted to develop Oblast EE Master Plans

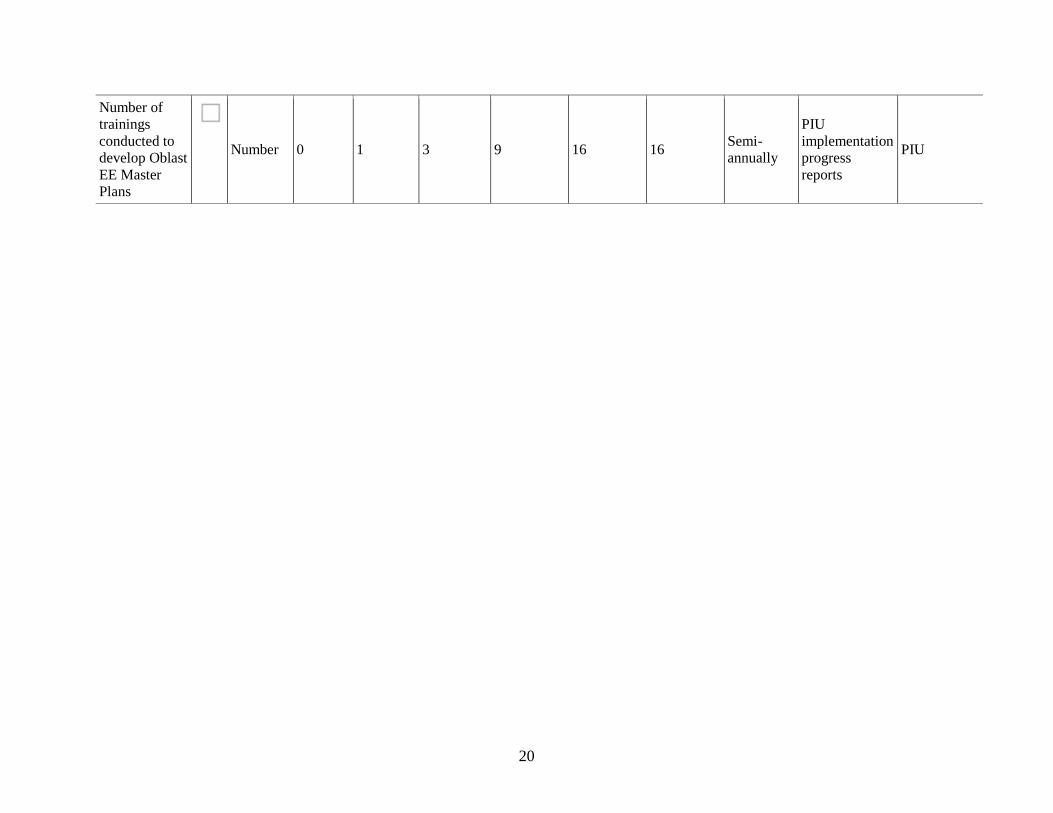

Number 0 1 3 9 16 16 Semi-annually

PIU implementation progress reports

PIU

.

21

Annex 1: Results Framework and Monitoring

Country: Kazakhstan Project Name: Energy Efficiency Project (P130013)

Results Framework .

Project Development Objective Indicators Indicator Name Description (indicator definition etc.) Quantified energy savings achieved Measures the EE improvements in public and social facilities Development of sustainable energy financing mechanisms

Assesses progress toward developing enabling environment for sustainable energy financing

.

Intermediate Results Indicators Indicator Name Description (indicator definition etc.) Number of subprojects commissioned in public and social facilities

Indicates progress with selection and implementation of EE subprojects

Number of male and female beneficiaries of subprojects Measures male and female population benefiting from the project Number of female beneficiaries of subprojects Measures female population benefiting from the project

Cumulative investments in public and social facilities Indicates progress with selection and implementation of EE subprojects CO2 emission reductions in retrofitted facilities through EE investments

Assesses environmental performance of retrofitted social and public facilities

Development of legal, institutional and regulatory basis for setting up EE financing mechanisms

Indicates progress with realization of financially viable EE potential

Number of local EE market institutions (including ESCOs and finance institutions) and co-financing arrangements involved

Indicates progress towards developing the national EE market and establishing a replicable and sustainable framework for EE

Number of trainings conducted to develop Oblast EE Master Plans

Indicates increase in capacity and interest by Oblasts to develop EE Master Plans

22

Annex 2: Detailed Project Description

KAZAKHSTAN: Energy Efficiency Project 1. The project development objectives are to improve: (i) EE in public and social facilities; and (ii) the enabling environment for sustainable energy financing. Expected key PDO level results of the proposed project include: (i) quantified energy savings achieved from implementation of economically viable EE projects in public and social facilities; and (ii) improved policy and institutional framework for EE to allow sustainable energy financing mechanisms to be developed and launched.

2. The project directly supports Kazakhstan’s recently passed Energy Efficiency Law (January 2012) and associated “Comprehensive Plan for Energy Efficiency Improvement in the Republic of Kazakhstan for 2012-2015” (2011). The GOK is now developing a suite of secondary legislation to establish a coherent EE policy framework. In addition, a dedicated EE financing mechanism is proposed to be developed by early 2013, possibly in the form of an EE Fund. This project can significantly help in preparing the grounds for sustainable EE financing mechanisms in terms of improving the methodology for energy audits, collection and analysis of market data, demonstration of financial returns on energy saving measures, raising awareness and understanding, developing an initial project pipeline and designing financing mechanisms reflecting international best practice. The policy and other TA activities can also assist GOK meet its EE targets and the strategic goals outlined in the Comprehensive Plan.

3. The project will be supported by a US$21.76 million grant from SDC, channeled through the World Bank, as well as an estimated US$1.3 million in co-financing from the participating institutions, utilities, and/or regions/municipalities. The project consists of two Parts: an investment Part and a TA Part, which are elaborated below.

4. Part 1: Development and Implementation of Demonstration Subprojects in the public and social facilities (estimated cost: US$19.0 million, including US$17.7 million from the grant and US$1.3 million from local co-financing). This part will finance EE projects (“subprojects”) in public and social facilities, such as schools, kindergartens, clinics/hospitals, and street lighting. These subprojects will generate demonstrable energy cost savings and social co-benefits (e.g., improved indoor temperature and comfort, reduced student sick days, better indoor air quality). Three annual batches of investment projects, selected through competitive proposals, will be developed and implemented. In the first year, these investments will be fully grant-financed in order to accelerate on-the-ground results and simplify contracting; in the subsequent years, some co-financing will be requested from the participating beneficiaries as selection criteria to help shift to a more sustainable model.

5. Target facilities will be competitively selected based on calls for proposals from the PIU. Eligible projects must meet basic eligibility criteria, to be reflected in the Project OM, which would include: (i) confirmation of public ownership; (ii) structural soundness of the facility; and (iii) absence of plans for closure, downsizing or privatization. Measures to be eligible for support will include upgrades to reduce the energy use of public buildings, including building envelop measures (insulation of walls, basements and attics, repair/replacement of external doors

23