The World Bank Sep 2001 Pension Fund Management “IBRD’s experience” Sudhir Krishnamurthi The...

30

The World Bank The World Bank Sep 2001 Sep 2001 Pension Fund Management “IBRD’s experience” Sudhir Krishnamurthi The World Bank Public Pension Fund Management, Washington, DC 24 September, 2001

-

Upload

alice-bridges -

Category

Documents

-

view

217 -

download

3

Transcript of The World Bank Sep 2001 Pension Fund Management “IBRD’s experience” Sudhir Krishnamurthi The...

The World BankThe World BankSep 2001Sep 2001

Pension Fund Management

“IBRD’s experience”

Sudhir KrishnamurthiThe World Bank

Public Pension Fund Management, Washington, DC

24 September, 2001

The World BankThe World BankSep 2001Sep 2001

Road Map

Introduction

Governance of Pension Plans

Strategic Asset Allocation

Middle Office Issues Performance and Risk Measurement

The World BankThe World BankSep 2001Sep 2001

IBRD (World Bank) Investments

IBRD $55 billion liquidity Managed internally Many instruments

Pensions $10 billion for Pension and others Managed externally Many asset classes

Provide Financial Technical Assistance

The World BankThe World BankSep 2001Sep 2001

Financial Instruments

Fostered innovation in supporting services

IBRD Pensions

• Futures & Forwards

• Swaps Interest Rate Currency Structured

• Other Synthetic Products

• Bonds - issuance &

trading(incl. EMG)

• Equities US Non-US EMG

• Other Hedge Funds

• Private Equities (EMG)

• Real Estate

• Fixed Income

Global High Yield EMG

The World BankThe World BankSep 2001Sep 2001

Fund Governance

Macro Governance Oversight Structure Responsibilities

Micro Governance Delegation of Authority Conflict of Interest

Cost of Governance

Governance of country systems

The World BankThe World BankSep 2001Sep 2001

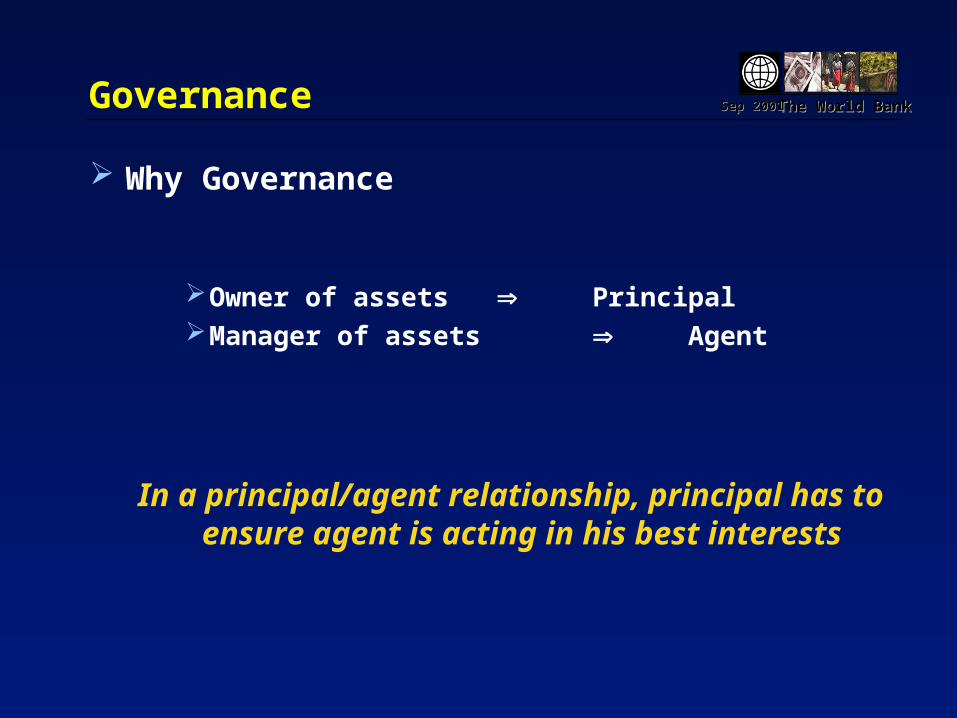

Governance Why Governance

Owner of assets PrincipalManager of assets Agent

In a principal/agent relationship, principal has to ensure agent is acting in his best interests

The World BankThe World BankSep 2001Sep 2001

Governance

Clear distinction between governing and governed bodies

Who needs to be Governed Pension investment groups, fund managers

Who does the Governing Ideally, the principals or pension beneficiaries Usually, a representative body like the oversight

committee or regulators

The World BankThe World BankSep 2001Sep 2001

Governance Organization Structure

The Regulators take role of Oversight Committee in DC plans

EquitiesEquities

oversight benchmark guidelinesmonitoring G

ove

rnin

g B

od

yG

ove

rned

Bo

dy

CurrencyCurrency Private EquitiesPrivate Equities

CashCash Real EstateReal Estate

Fixed Income

Oversight Committee

Investment Staff/External Managers

The World BankThe World BankSep 2001Sep 2001

Governance Macro Issues

Composition of Oversight Committee Selection method Size Representation Turnover Frequency of meeting

Responsibilities of Oversight Committee Select investment staff and external managers Set Investment Policy Oversee Investment Policy Implementation Monitor Investment Performance Overall Fiduciary Responsibilities

The World BankThe World BankSep 2001Sep 2001

Governance Macro Issues

Composition of Investment Staff Finance Professionals Accountants Quantitative Specialists Actuaries

Responsibility of Investment Staff Funding Recommendations Investment Management Risk Management Reporting

The World BankThe World BankSep 2001Sep 2001

Governance Micro Issues

Delegation of Authority Explicit and written Implementation of Investment Policy

Conflict of Interest Permissible and Non-permissible transaction Disclosures Code of Ethics

Responsibility for the Development of Investment Policy and its Implementation be separated

The World BankThe World BankSep 2001Sep 2001

Governance Cost of governance

Governance must be just right - not too little and not too much

Delays

False sense of comfort - especially if oversight committee is not paying attention.

Cost of providing adequate information to oversight committee/regulators.

Ensuring timely/appropriate feedback on decision to oversight committee/regulators.

The World BankThe World BankSep 2001Sep 2001

Governance Country Systems

Provident Fund (PF)

Individual

Provident Fund

Oversight Committee

NO

DefinedContributio

n(DC)

Individual

Fund Manager

Regulators

YES

DefinedBenefit

(DB)

Government

Government

Social Security Administration

YES

Agent

Oversight

Incentive compatibl

e

Principal

The World BankThe World BankSep 2001Sep 2001

Investment Decisions

Decision 1: Determining asset allocation policy mix

(Strategic Asset Allocation)

Portfolio construction &

manager selection

Tactical Asset

Allocation

Decision 2:

Decision 3:

The World BankThe World BankSep 2001Sep 2001

Importance Investment Decisions Sources of Long-Term Performance

As much as 91.5% of performance attributed to Strategic Asset Allocation

Source: Brinson, Hood & Beebower. “Determinants of Portfolio Performance” Financial Analysts Journal. May/June 1991.Note: Cross products account for 2.1% of the variance

Tactical Asset Allocation

1.80% Other Factors2.10%

Security Selection

4.60%

Strategic Asset Allocation

91.5%

The World BankThe World BankSep 2001Sep 2001

0

200

400

600

800

1000

1200

'80 '85 '90 '95

1980:$260 billion

0%

25%

50%

75%

100%

125%

150%

175%

'80 '85 '90 '95

1996: 104%($1.04 in assets for every $1 of liability)

1980: 123%($1.23 in assets for every $1 of liability)

1996:$1.13 trillion

Assets and Liabilities Liabilities are unique for every pension plan

Liabilities are the only reason for a pension plan to make investment choices

Pension fund assets,in $ billions, annually

Ratio of assets to liabilities,annually

Note: Figures include a majority of private pension plans (45,000)Source: Pension Benefit Guaranty Corp.

U.S. Pension Funds: 1980-1996

The World BankThe World BankSep 2001Sep 2001

Mean - Variance Efficient Frontier

Is standard deviation meaningful as risk tolerance measure for pension plans

6.00%

7.00%

8.00%

9.00%

10.00%

11.00%

5.00% 7.00% 9.00% 11.00% 13.00% 15.00% 17.00% 19.00% 21.00%

Risk - Standard Deviation

Ret

urn

- M

ean

Traditional approach to Strategic Asset Allocation

Market Portfolio

Capital Market Line

Asset Allocation

Risk Tolerance determines Asset Allocation

The World BankThe World BankSep 2001Sep 2001

The Pension Problem

Traditional asset allocation approach does not take liabilities into account

Asset and Liability matching problem

Yearly Outflows Current retirees

Future Outflows Future retirees

Yearly Inflows Contributions

Employees Employer

Return on Assets

Current Assets

LIABILITIES ASSETS

The World BankThe World BankSep 2001Sep 2001

Risk measures for Pension Plans

Pension Plan investors have many other risk measures besides standard deviation of expected returns.

The appropriate risk measures for pension plans depends on the parties that are involved in the decision making process.

The World BankThe World BankSep 2001Sep 2001

Different objectives Objectives of parties concerned with pension plans

Objectives dictates the risk measures and risk preference

PLAN SPONSOR

Low and stable contributions

PENSION FUND

REGULATING AUTHORITIES

Solvency requirements

EMPLOYEES

Maintaining pension scheme

CENTRAL GOVERNMENT

Reduction public pensions

RETIREES

Maintaining compensation cost of

living

Source: Ortec Consultant BV

The World BankThe World BankSep 2001Sep 2001

Objectives and Risk Measures

Risks: I. Low funded ratios II. High contribution rates

World Bank’s Pension Plan

Maximize Return(max. wealth of plan)

II.Avoid high

contribution rate levels

I.Avoid low

funded ratio levels

(ratio Asset to Liabilities)

The World BankThe World BankSep 2001Sep 2001

Mean - Variance Efficient Frontier

Risk

Ret

urn

- W

ea

lth

Asset Liability Management approach to Asset Allocation

Market Portfolio

Asset Allocation

Risk (as measured by st. dev.) determined by:

• Maximum Contribution Rate• Minimum Funded Ratio

Asset Allocation reflects risk bearing capacity of the pension plan

The World BankThe World BankSep 2001Sep 2001

Operationalize Risk Measures

5% Funded Ratio - at - Risk Minimum funded ratio that can occur in any year with a

5% probability

5% Contribution Rate - at - Risk Maximum contribution rate that can occur in any year

with a 5% probability

Variants of the value-at-risk concept

Use multiple years for calculation of these risks (in this example 10 years)

The World BankThe World BankSep 2001Sep 2001

Investment Decision Matrix Total allocation to risky assets

60% 60%60%

60% 70%70%

60% 80%80%

90% 80%85%

5% FUNDED RATIO - AT - RISK

19%

25%

22%

5% C

ON

TR

IBU

TIO

N R

AT

E -

AT

- R

ISK

Risk budget to these value-at-risk measures determines investment policy

The World BankThe World BankSep 2001Sep 2001

Investment Decision Example Budget: Funded Ratio-at-risk = 85% and Contribution Rate-at-risk = 22%

Shaded area shows investment policies which are conform with risk budget

5% Contribution Rate-at-risk

5% Funded Ratio-at-risk

92.5%14%

87.5%

82.5%

22% 30%18% 26%

90.0%

85.0%

60%

80%

70%

70% allocation to risky assets

The World BankThe World BankSep 2001Sep 2001

Middle Office Issues

For each external manager and entire portfolio

Contracts

standardized adequate protection

Guidelines

development compliance monitoring

Performance Measurement

frequency attribution

Accounting & Reporting

management internal Controls

risk management cash management local/global custody

The World BankThe World BankSep 2001Sep 2001

Why Risk Management and Performance attribution

Identify unsustainable downside risk.

Identify the sources of excess return

Support asset allocation by trading off risk and return.

The World BankThe World BankSep 2001Sep 2001

Sizes of Risks Value - At - Risk Tree

Asset Liability Risk is main risk and is taken by the oversight committee

Liabilities

Investment Benchmark

Extended Policy

1,809

128

168

192

1,776

Actual Portfolio

= -0.45

= -0.36

$, million

The World BankThe World BankSep 2001Sep 2001

TAA and Active Risk

Risk measured as tracking error against the strategic benchmark

177

TOTAL RISK

83

TAA - Risk

125

Active - Risk

40

Equity

45

Fixed Income

60

Others

100

Equity

20

Fixed Income

50

Others

10

US - Equity

120

Non US - Equity

15

High Yield

10

Global FI

0

Real Estate

50

Hedge funds

55

US - Equity

45

Non US - Equity

30

High Yield

7

Global FI

100

Hedge funds

15

Real Estate

The World BankThe World BankSep 2001Sep 2001

Monthly Performance Attribution

Performance in same format as risk enables evaluation of risk and returnof each investment decision

50

TOT. PERFORM

15

TAA-PERFORM

35

Active-PERFORM

20

Equity

5

Fixed Income

-10

Others

25

Equity

5

Fixed Income

5

Others

10

US - Equity

15

Non US - Equity

5

High Yield

0

Global FI

0

Real Estate

5

Hedge funds

15

US - Equity

5

Non US - Equity

0

High Yield

5

Global FI

-20

Hedge funds

10

Real Estate