The workings under the heading of are not required according to the requirement...

14

The workings under the heading of “Additional Working” are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.weebly.com 2014 Compiled and Solved by: Sameer Hussain XI – ACCOUNTING REGULAR

Transcript of The workings under the heading of are not required according to the requirement...

The workings under the heading of “Additional Working” are not required according to the requirement of the examiner. These are only for understanding the solutions. For more help, visit www.a4accounting.weebly.com

2014

Compiled and Solved by:

Sameer Hussain

XI – ACCOUNTING

REGULAR

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net [email protected]

X I – A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 2

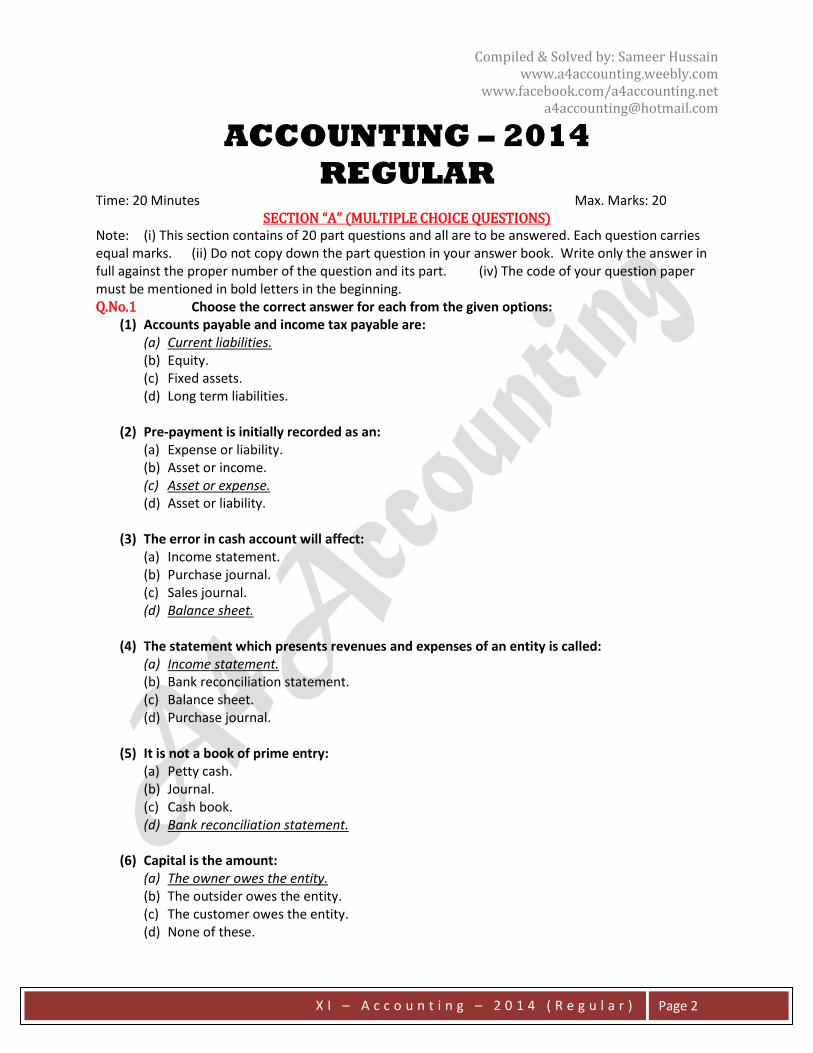

ACCOUNTING – 2014

REGULAR Time: 20 Minutes Max. Marks: 20

SECTION “A” (MULTIPLE CHOICE QUESTIONS) Note: (i) This section contains of 20 part questions and all are to be answered. Each question carries equal marks. (ii) Do not copy down the part question in your answer book. Write only the answer in full against the proper number of the question and its part. (iv) The code of your question paper must be mentioned in bold letters in the beginning. Q.No.1 Choose the correct answer for each from the given options:

(1) Accounts payable and income tax payable are: (a) Current liabilities. (b) Equity. (c) Fixed assets. (d) Long term liabilities.

(2) Pre-payment is initially recorded as an:

(a) Expense or liability. (b) Asset or income. (c) Asset or expense. (d) Asset or liability.

(3) The error in cash account will affect:

(a) Income statement. (b) Purchase journal. (c) Sales journal. (d) Balance sheet.

(4) The statement which presents revenues and expenses of an entity is called:

(a) Income statement. (b) Bank reconciliation statement. (c) Balance sheet. (d) Purchase journal.

(5) It is not a book of prime entry:

(a) Petty cash. (b) Journal. (c) Cash book. (d) Bank reconciliation statement.

(6) Capital is the amount:

(a) The owner owes the entity. (b) The outsider owes the entity. (c) The customer owes the entity. (d) None of these.

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net [email protected]

X I – A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 3

(7) Closing entries are prepared: (a) At the end of an accounting period. (b) During the year. (c) At the beginning of an accounting period. (d) None of these.

(8) Financial transactions are recorded in:

(a) Balance sheet. (b) Trial balance. (c) Ledger. (d) Journal.

(9) It is not included in the balance sheet:

(a) Cash. (b) Inventory. (c) Building. (d) Rent expense.

(10) Accrued income is:

(a) Asset. (b) Expense. (c) Liability. (d) Revenue.

(11) This one of the following is correct:

(a) Assets + Owner’s equity = Liabilities. (b) Assets = Owner’s equity – Liabilities. (c) Assets + Liabilities = Owner’s equity. (d) Assets – Liabilities = Owner’s equity.

(12) Sales is best described by:

(a) Only cash sale of merchandise. (b) Cash and credit sale of merchandise. (c) Any sale of any asset for cash. (d) Sale of any asset on credit.

(13) If cash sales are Rs.12,000 and credit sales are Rs.3,000 in the current month, the amount of

total revenue for the current month will be: (a) Rs.15,000. (b) Rs.9,000. (c) Rs.12,000. (d) Rs.3,000.

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net [email protected]

X I – A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 4

(14) If the company’s policy is to record advance payment as an asset, payment for insurance premium will be recorded as: (a) Prepaid insurance. (b) Insurance payable. (c) Insurance expense. (d) Unearned insurance.

(15) This one of the following is correct statement:

(a) Profit does not change owner’s equity. (b) Profit increases owner’s equity. (c) Profit decreases owner’s equity. (d) Profit increases both liabilities and owner’s equity.

(16) Posting means:

(a) Making an entry in general journal. (b) Making an entry in special journal. (c) Transferring an entry from a journal to ledger account. (d) Determining balance of an account.

(17) This normally has a debit balance:

(a) Accounts payable. (b) Supplies. (c) Unearned commission. (d) Capital account.

(18) The purpose of a trial balance is to:

(a) Determine the arithmetic accuracy of double entry. (b) Show financial position at a particular date. (c) Show performance of business. (d) None of these.

(19) If one entry has more than one debit or credit, it is called:

(a) Double entry. (b) Compound entry. (c) Contra entry. (d) None of these.

(20) If a seller reduces the price of goods after shipment, because of the goods supplied have

some defects, this reduction in price is called a: (a) Sales return and allowances. (b) Sales discount. (c) Quantity discount. (d) Purchase return and allowances.

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net [email protected]

X I – A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 5

ACCOUNTING – 2014

REGULAR Time: 2 Hours 40 Minutes Max. Marks: 80

SECTION “B” (SHORT – ANSWER QUESTIONS) (50) Note: Attempt any Four questions. All questions carry equal marks. The use of calculator is allowed. Q.No.2 GENERAL JOURNAL The following transactions were completed by Mr. Saad, a sole trader:

i) Invested Rs.500,000. ii) Opened a bank account with Rs.350,000. iii) Purchased goods from Mr. Ali on credit for Rs.45,000 and cash Rs.33,000. iv) Sold goods on account for Rs.55,000 and cash Rs.23,000. v) Paid for insurance Rs.26,000 through cheque. vi) Purchased computer for Rs.32,000. vii) Received commission in advance through a cheque of Rs.12,000. viii) Issued a cheque of Rs.44,500 to Mr. Ali in full settlement of his account of Rs.45,000.

REQUIRED Make entries in General Journal. SOLUTION 2

MR. SAAD GENERAL JOURANL

FOR THE MONTH OF _______

Date Particulars P/R Debit Credit

1 Cash 500,000 Saad Capital 500,000 (To record the cash invested by owner in the business)

2 Bank 350,000 Cash 350,000 (To record the cash deposited into bank)

3 Purchases 78,000 Accounts payable (Mr. Ali) 45,000 Cash 33,000 (To record the goods purchased for cash and on credit)

4 Accounts receivable 55,000 Cash 23,000 Sales 78,000 (To record the goods sold for cash and on account)

5 Insurance expense 26,000 Bank 26,000 (To record the insurance paid)

6 Equipment 32,000 Cash 32,000 (To record the equipment purchased)

7 Cash 12,000 Unearned commission 12,000 (To record the commission received in advance)

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net [email protected]

X I – A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 6

Date Particulars P/R Debit Credit

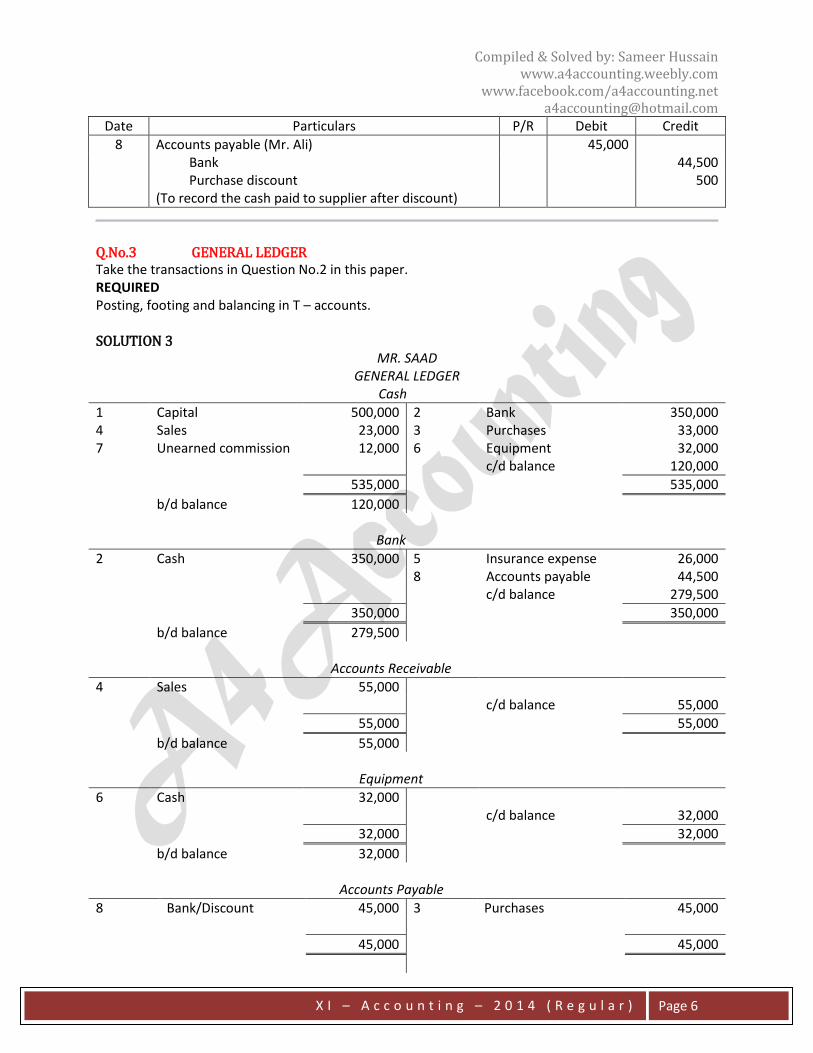

8 Accounts payable (Mr. Ali) 45,000 Bank 44,500 Purchase discount 500 (To record the cash paid to supplier after discount)

Q.No.3 GENERAL LEDGER Take the transactions in Question No.2 in this paper. REQUIRED Posting, footing and balancing in T – accounts. SOLUTION 3

MR. SAAD GENERAL LEDGER

Cash

1 Capital 500,000 2 Bank 350,000 4 Sales 23,000 3 Purchases 33,000 7 Unearned commission 12,000 6 Equipment 32,000 c/d balance 120,000

535,000 535,000

b/d balance 120,000 Bank

2 Cash 350,000 5 Insurance expense 26,000 8 Accounts payable 44,500 c/d balance 279,500

350,000 350,000

b/d balance 279,500 Accounts Receivable

4 Sales 55,000 c/d balance 55,000

55,000 55,000

b/d balance 55,000 Equipment

6 Cash 32,000 c/d balance 32,000

32,000 32,000

b/d balance 32,000 Accounts Payable

8 Bank/Discount 45,000 3 Purchases 45,000

45,000 45,000

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net [email protected]

X I – A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 7

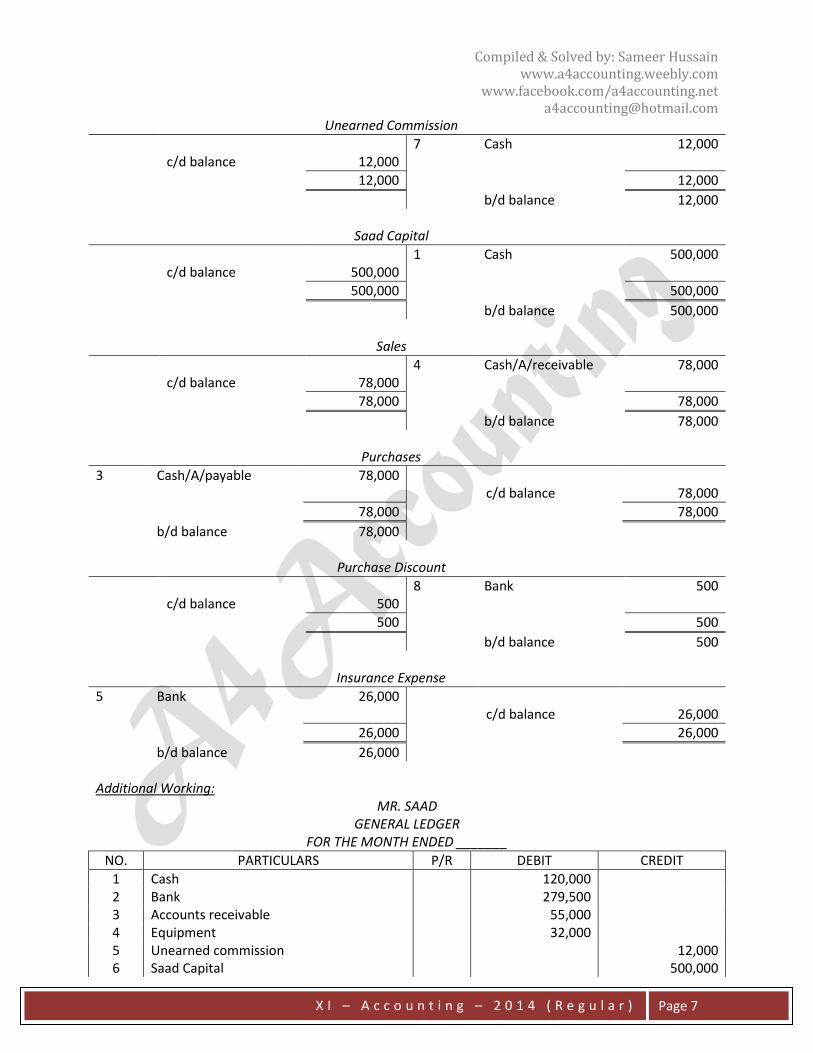

Unearned Commission

7 Cash 12,000 c/d balance 12,000

12,000 12,000

b/d balance 12,000 Saad Capital

1 Cash 500,000 c/d balance 500,000

500,000 500,000

b/d balance 500,000 Sales

4 Cash/A/receivable 78,000 c/d balance 78,000

78,000 78,000

b/d balance 78,000 Purchases

3 Cash/A/payable 78,000 c/d balance 78,000

78,000 78,000

b/d balance 78,000 Purchase Discount

8 Bank 500 c/d balance 500

500 500

b/d balance 500 Insurance Expense

5 Bank 26,000 c/d balance 26,000

26,000 26,000

b/d balance 26,000 Additional Working:

MR. SAAD GENERAL LEDGER

FOR THE MONTH ENDED _______

NO. PARTICULARS P/R DEBIT CREDIT

1 Cash 120,000 2 Bank 279,500 3 Accounts receivable 55,000 4 Equipment 32,000 5 Unearned commission 12,000 6 Saad Capital 500,000

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net [email protected]

X I – A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 8

7 Sales 78,000 8 Purchases 78,000 9 Purchases discount 500

10 Insurance expense 26,000

Total 590,500 590,500

Q.No.4 PETTY CASH BOOK

? ? ? ? ? ?

Stationary Postages &

Telegram

Cartage Entertainment Sundries

A/C No.

Amount

i) Established petty cash fund by Rs.5,000 on January 1, 2014. ii) Replenish the petty cash fund Rs.3,800.

REQUIRED Prepare entries in General Journal. SOLUTION 4

Cash (Dr.)

Date Voucher

No. Particular

Cash (Cr.)

Payments/Expenses

Stationary Postages

& Telegram

Cartage Entertainment Sundries

A/C No.

Amount

M/S. ____________ GENERAL JOURNAL

FOR THE MONTH OF JANUARY 2014

Date Particulars P/R Debit Credit

Jan. 1 Petty cash fund 5,000 Cash 5,000 (To record the establishment of petty cash fund)

Jan. 31 Petty cash fund 3,800 Cash 3,800 (To record the replenishment of petty cash fund)

Q.No.5 BANK RECONCILIATION STATEMENT A comparison of cash book and bank statement of Ather & Co. revealed the following information:

i) Cheques deposit of Rs.16,000 but not shown in bank statement. ii) Cheque issued of Rs.20,000 but not presented at the bank. iii) Direct deposit by customer Rs.14,000 in bank. iv) Dishonoured cheque Rs.8,500. v) Bank services charges Rs.1,000.

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net [email protected]

X I – A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 9

vi) Mark-up credited by bank Rs.500. vii) A cheque for Rs.4,050 issued to supplier was wrongly recorded in cash book as Rs.40,500. viii) A cheque for Rs.25,700 was deposited to bank entered in the company’s record as Rs.27,500.

REQUIRED A schedule of added to and deducted from cash book. SOLUTION 5

ATHER & CO. SCHEDULE OF ADDITION TO AND DEDUCTION FROM CASH BOOK

FOR THE MONTH ENDED _________

Particulars Cash Book

Add: Direct deposit by a customer (iii) 14,000 Less: Dishonoured cheque (iv) (8,500) Less: Bank service charges (v) (1,000) Add: Mark-up (vi) 500 Add: Accounts payable – error (vii) 36,450 Less: Cash deposit – error (viii) (1,800)

Q.No.6 CORRECTION OF ERRORS Give entries in General Journal to correct each of the following errors deducted before closing the books of Erma Stores:

i) Purchase return of Rs.185 was credited to purchase account. ii) Sales of office furniture of Rs.160 was credited to sales account. iii) Depreciation on furniture Rs.55 was overcharged. iv) Drawings of Rs.1,200 for personal use of the proprietor was debited to capital account. v) Cash Rs.40 received from Hamna was recorded as received from Yamna.

SOLUTION 6

ERMA STORES CORRECTING ENTRIES

Date Particulars P/R Debit Credit

1 Purchases 185 Purchase return and allowance 185 (To correct the goods return to supplier)

2 Sales 160 Office furniture 160 (To correct the sale of office furniture)

3 Allowance for depreciation 55 Depreciation expense 55 (To correct the depreciation expense)

4 Drawings 1,200 Capital 1,200 (To correct the withdrawn by owner for personal use)

5 Accounts receivable (Yamna) 40 Accounts receivable (Hamna) 40

(To correct the cash collected from Hamna)

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net [email protected]

X I – A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 10

Q.No.7 SPECIAL JOURNAL AND SUBSIDIARY LEDGER The following are the selected transactions completed by Asad Traders during March 2014: March 07: Purchased goods for resale, on account from Asim Sons for Rs.9,000. March 11: Purchased merchandise on account from Jamil Brothers for Rs.13,000. March 17: Purchased merchandise on credit from Sattar & Co. for Rs.4,000. March 26: Purchased merchandise on account from Asim Sons for Rs.6,000. March 27: Purchased merchandise for cash from Sattar Sons Rs.3,400. March 29: Purchased furniture for office use from Shamim Sons, Rs.34,800 paying cash. REQUIRED

a) Record the above transactions in the appropriate journals. b) Make postings to the accounts payable subsidiary ledger. Use three column ledger accounts.

SOLUTION 7 (a)

ASAD TRADERS PURCHASE JOURNAL

FOR THE MONTH OF MARCH 2014

Date Invoice No. Name of Customers P/R Amount

March 07 Asim Sons 9,000 March 11 Jamil Brothers 13,000 March 17 Sattar & Co. 4,000 March 26 Asim Sons 6,000

March 31 Purchases Dr. 32,000 Accounts payable Cr.

ASAD TRADERS

GENERAL JOURNAL FOR THE MONTH OF MARCH 2014

Date Particulars P/R Debit Credit

Mar.27 Purchases 3,400 Cash 3,400 (To record the goods purchased for cash)

Mar.29 Office furniture 34,800 Cash 34,800 (To record the purchase of furniture for cash)

SOLUTION 7 (b)

ASAD TRADERS SUBSIDIARY LEDGER – ACCOUNTS PAYABLE

FOR THE MONTH OF MARCH 2014

Asim Sons

Date Invoice No. Particulars P/R Debit Credit Balance

March 07, 2014 Purchases 9,000 9,000 March 26, 2014 Purchases 6,000 15,000

Jamil Brothers

Date Invoice No. Particulars P/R Debit Credit Balance

March 11, 2014 Purchases 13,000 13,000

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net [email protected]

X I – A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 11

Sattar & Co.

Date Invoice No. Particulars P/R Debit Credit Balance

March 17, 2014 Purchases 4,000 4,000

SECTION “C” (DETAILED – ANSWER QUESTIONS) (30) Instruction: Attempt the following question which is compulsory: Q.No.8 FINANCIAL STATEMENT (a) i) Merchandise inventory (opening) Rs.25,000 ii) Purchased merchandise Rs.133,000 iii) Merchandise inventory (ending) Rs.18,000 iv) Purchases returns Rs.500 v) Purchases discount Rs.1,000 vi) Transportation Rs.800 REQUIRED Compute cost of goods sold. (b) The following balances of Qasim & Co. on December 31, 2013 was as under:

ACCOUNT TITLE DEBIT CREDIT

Cash 40,000 Accounts receivable 60,000 Merchandise inventory ending 18,000 Prepaid insurance 20,000 Notes payable 20,000 Unearned commission 10,000 Capital – Qasim 150,000 Sales 120,000 Cost of goods sold ????? Salaries expense 11,000 Office supplies 8,000 Rent expenses 3,000

Supplementary Data for Adjustments for December 31, 2013: i) Office supplies used Rs.5,000. ii) Accrued salaries Rs.4,000. iii) Commission earned Rs.7,000. iv) Bad debt estimated 2% on sales. v) Insurance expired during the year Rs.6,000

REQUIRED a) Income statement for the year ended December 31, 2013. b) Balance sheet as of December 31, 2013. OR Prepare closing entries and post-closing trial

balance.

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net [email protected]

X I – A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 12

SOLUTION 8 (a) Computation of Cost of Goods Sold: Merchandise inventory (beginning) 25,000 Add: Net Purchases: Purchases 133,000 Add: Transportation 800

Delivered purchases 133,800 Less: Purchases returns (500) Less: Purchases discount (1,000)

Net purchases 132,300

Merchandise available for sale 157,300 Less: Merchandise inventory (ending) (18,000)

Cost of goods sold 139,300

SOLUTION 8 (b) Computation of Cost of Goods Sold: Total credits 300,000 Less: Total debits (160,000)

Cost of goods sold 140,000

QASIM & CO.

INCOME STATEMENT FOR THE PERIOD ENDED 31 DECEMBER 2013

Sales 120,000 Less: Cost of goods sold (140,000)

Gross loss (20,000) Less: Operating Expenses: Salaries expense (11,000 + 4,000) 15,000 Office supplies expense 5,000 Rent expenses 3,000 Bad debts expense 2,400 Insurance expense 6,000

Total operating expenses (31,400)

Loss from operation (51,400) Add: Other Income: Commission income 7,000

Net loss (44,400)

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net [email protected]

X I – A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 13

QASIM & CO. BALANCE SHEET

AS ON 31 DECEMBER 2013

ASSETS EQUITIES

Current Assets: Liabilities: Cash 40,000 Notes payable 20,000 Accounts receivable 60,000 Unearned commission 3,000 Less: All for bad debts (2,400) 57,600 Salaries payable 4,000

Merchandise inventory 18,000 Total liabilities 27,000 Prepaid insurance 14,000 Office supplies 3,000 Owner’s Equity:

Total current assets 132,600 Capital 150,000 Less: Net loss (44,400)

Total owner’s equity 105,600

Total assets 132,600 Total equities 132,600

Additional Working:

QASIM & CO. ADJUSTING ENTRIES

FOR THE PERIOD 31 DECEMBER 2013

Date Particulars P/R Debit Credit

1 Office supplies expense 5,000 Office supplies 5,000 (To adjust the office supplies expense)

2 Salaries expenses 4,000 Salaries payable 4,000 (To adjust the unpaid salaries)

3 Unearned commission 7,000 Commission income 7,000 (To adjust the unearned commission)

4 Bad dents expense 2,400 Allowance for bad debts 2,400 (To adjust the bad debts expense)

5 Insurance expense 6,000 Prepaid insurance 6,000 (To adjust the prepaid insurance)

Compiled & Solved by: Sameer Hussain www.a4accounting.weebly.com

www.facebook.com/a4accounting.net [email protected]

X I – A c c o u n t i n g – 2 0 1 4 ( R e g u l a r )

Page 14

QASIM & CO. CLOSING ENTRIES

FOR THE PERIOD ENDED 31 DECEMBER 2013

Date Particulars P/R Debit Credit

1 Expense and revenue summary 171,400 Cost of goods sold 140,000 Office supplies expenses 5,000 Salaries expenses 15,000 Rent expense 3,000 Bad debts expense 2,400 Insurance expenses 6,000 (To close the various expense accounts)

2 Sales 120,000 Commission income 7,000 Expense and revenue summary 127,000 (To close the revenue account)

3 Qasim’s Capital 44,400 Expense and revenue summary 44,400 (To close the expense and revenue summary account)

QASIM & CO.

POST – CLOSING TRIAL BALANCE FOR THE PERIOD ENDED 31 DECEMBER 2013

NO. PARTICULARS P/R DEBIT CREDIT

1 Cash 40,000 2 Accounts receivable 60,000 3 Allowance for bad debts 2,400 4 Merchandise inventory 18,000 5 Prepaid insurance 14,000 6 Office supplies 3,000 7 Notes payable 20,000 8 Unearned commission 3,000 9 Salaries payable 4,000

10 Qasim – Capital 105,600

Total 135,000 135,000