The Willis Index€¦ · Mergers and Acquisitions Newsletter The specialist divisions of Willis...

6

The Willis Index `çåíÉåíë Introduction 1 Regional M&A Growth 1 Globalisation in Reverse? 2 Airport Transactions 3 EU Environmental Liability Directive 4 Case Study 5 Meet the Team 5 Mergers and Acquisitions Newsletter The specialist divisions of Willis produce regular publications on the relevant issues affecting the insurance industry and the effect they have on various business sectors. To request editions of The Willis Index including Financial Institutions, Professional Indemnity, Directors' & Officers' Liability, Environmental Liability or Political Risks, please contact Amy Dawson at [email protected]. bÇáíáçå=N=OMMT It is almost a year since we were the first insurance broker to be formally recognised as a leading provider of specialist due diligence services by winning the BVCA / Real Deals Specialist Adviser of the Year Award 2006. Since that time I am proud to say that we have continued to go from strength to strength. During the past 12 months we have: - acted on more than 1000 transaction assignments globally - responded to our clients’ needs by launching dedicated Willis M&A practices in Japan, Greater China, Australia, India and Eastern Europe. - continued to selectively recruit some of the best talent in our industry such as Richard Worker, former MD of Heath Lambert M&A. We have also been at the forefront of developing more advanced bespoke solutions in a wider number of jurisdictions including tax liability placements in Germany and Spain. Our continued focus on the development of a sector-leading insurance due diligence service has also seen the value of our reports increase in the eyes of a number of our clients. This has allowed us to continue to increase our penetration of the due diligence market despite seeing the traditional driver of deal flow – the debt providers insurance appropriateness CP – being increasingly waived in the highly liquid and competitive debt finance market. I hope that you find the contents of this newsletter to be of interest and we look forward to being of assistance to you in the near future. ^äáëí~áê=iÉëíÉê International Practice Leader Mergers & Acquisitions qÜÉ=nì~êíÉêäó=kÉïëäÉííÉê=çÑ=íÜÉ=fåíÉêå~íáçå~ä=jÉêÖÉêë=~åÇ=^Åèìáëáíáçåë=mê~ÅíáÅÉ Regional M&A Growth The UK operations of the International Mergers & Acquisitions practice have recently expanded into the UK regions. With a strong London and international framework the regional resource will be led by Heulwen Samuel in Leeds, reporting to Simon Dodsworth in London, responsible for UK M&A advisory services. Heulwen has recently been working on secondment with the UK M&A practice in London prior to the expansion into the regions. Regional Private Equity growth has been steadily on the increase in 2006 with over 55% of employees within Private Equity backed companies in businesses based outside of London and the South-East. Deals of increasing size and complexity are now being carried out by regional offices drawing on the skills and expertise of local advisers. New Private Equity houses are opening in the regions, those who retracted a few years ago are opening new branches, continued on page 2 råáíÉÇ=háåÖÇçã Alistair Lester Richard Worker Ten Trinity Square London EC3P 3AX Tel: +44 (0)20 7488 8111 dÉêã~åó Albert Höyng Gruneburgweg 102 Frankfurt am Main 60323 Tel: +49 69 95931-0 fí~äó Sebastiano Doria Via Tortona 33 20144 Milan Tel: +39 02 47787301 cê~åÅÉ Jean-Luc Delcros Gras Savoye 2 a 8 rue Ancellle Neuilly Sur Seine, Paris 92202 Tel: +33 141 43 50 00 pïÉÇÉå Johan Forsgärd Sergelgatan 1 S- 111 57 Stockholm Tel +46 8 463 89 78 pé~áå Jose Carlos Marcos Paseo de la Castellana 36-38 4a Planta, Edificio Castellana Madrid 28046 Tel: +34 91 423 3400 kÉíÜÉêä~åÇë Simon Cross De Ruyterkade 7 Amsterdam 1013 AA Tel: +31 20 531 2525 _ÉäÖáìã Bart Smets Gras Savoye Belgium Zuiderlaan 91 1731 Zellik, Brussels Tel: +32 2 481 1927 rp^= Mark Rusas One World Financial Centre 200 Liberty Street New York, 10281 Tel: +1 212 344 8888 g~é~å= Nobuto Ota Ohtemachi Tatemono Toranomon Bldg. 10F 6-12 Toranomon 1-chome Minato-ku, Tokyo 105-0001, Tel: +81 3 3500 2523 mçêíìÖ~ä Crispin Stillwell Ed.Liberdade Av.Da Liberdade Lisbon 49-41250 Tel: +351 21 346 9621 ^ìëíê~äá~ Josh Roach Level 8 2 Market Street Sydney 2000 Tel: +61 292 854 0000 fåÇá~ B Rammohan 111, Free Press House, Free Press Journal Marg, Nariman Point, Mumbai 400 021 dêÉ~íÉê=`Üáå~ Jason Wang 3502 The Lee Gardens 33 Hysan Avenue Causeway Bay +852 2830 0111 táååÉê=çÑ=píê~íÉÖáÅofph ã~Ö~òáåÉDë=_Éëí=~åÇ=jçëí fååçî~íáîÉ=_êçâÉê=çÑ=íÜÉ=vÉ~ê=OMMS Ñçê=íÜÉ=ëÉÅçåÇ=ÅçåëÉÅìíáîÉ=óÉ~ê táååÉê=çÑ=oÉ~Åíáçåë=j~Ö~òáåÉDë bìêçéÉ~å=`çããÉêÅá~ä=_êçâÉê=çÑ=íÜÉ vÉ~ê=Ñçê=íÜÉ=ëÉÅçåÇ=ÅçåëÉÅìíáîÉ=óÉ~ê táååÉê=çÑ=fåëìê~åÅÉ=qáãÉë k~íáçå~ä=_êçâÉê=çÑ=íÜÉ=óÉ~ê=OMMS Ñçê=íÜÉ=ëÉÅçåÇ=ÅçåëÉÅìíáîÉ=óÉ~ê

Transcript of The Willis Index€¦ · Mergers and Acquisitions Newsletter The specialist divisions of Willis...

The Willis Index

`çåíÉåíë

Introduction 1

Regional M&A Growth 1

Globalisation in Reverse? 2

Airport Transactions 3

EU Environmental Liability Directive 4

Case Study 5

Meet the Team 5

Mergers and Acquisitions Newsletter

The specialist divisions of Willisproduce regular publications on therelevant issues affecting the insuranceindustry and the effect they have onvarious business sectors. To requesteditions of The Willis Index includingFinancial Institutions, ProfessionalIndemnity, Directors' & Officers'Liability, Environmental Liability orPolitical Risks, please contact AmyDawson at [email protected].

bÇáíáçå=N=OMMT

It is almost a year since we were the first insurancebroker to be formally recognised as a leading provider ofspecialist due diligence services by winning the BVCA /Real Deals Specialist Adviser of the Year Award 2006.

Since that time I am proud to say that we havecontinued to go from strength to strength. During thepast 12 months we have:- acted on more than 1000 transaction assignments

globally- responded to our clients’ needs by launching

dedicated Willis M&A practices in Japan, GreaterChina, Australia, India and Eastern Europe.

- continued to selectively recruit some of the besttalent in our industry such as Richard Worker,former MD of Heath Lambert M&A.

We have also been at the forefront of developing moreadvanced bespoke solutions in a wider number of

jurisdictions including tax liability placements inGermany and Spain. Our continued focus on thedevelopment of a sector-leading insurance duediligence service has also seen the value of our reportsincrease in the eyes of a number of our clients. This hasallowed us to continue to increase our penetration ofthe due diligence market despite seeing the traditionaldriver of deal flow – the debt providers insuranceappropriateness CP – being increasingly waived in thehighly liquid and competitive debt finance market.

I hope that you find the contents of this newsletterto be of interest and we look forward to being ofassistance to you in the near future.

^äáëí~áê=iÉëíÉêInternational Practice Leader Mergers & Acquisitions

qÜÉ=nì~êíÉêäó=kÉïëäÉííÉê=çÑ=íÜÉ=fåíÉêå~íáçå~ä=jÉêÖÉêë=~åÇ=̂ Åèìáëáíáçåë=mê~ÅíáÅÉ

Regional M&A GrowthThe UK operations of the International Mergers &Acquisitions practice have recently expanded into theUK regions. With a strong London and internationalframework the regional resource will be led byHeulwen Samuel in Leeds, reporting to SimonDodsworth in London, responsible for UK M&Aadvisory services. Heulwen has recently been workingon secondment with the UK M&A practice in Londonprior to the expansion into the regions.

Regional Private Equity growth has been steadilyon the increase in 2006 with over 55% of employeeswithin Private Equity backed companies in businessesbased outside of London and the South-East.

Deals of increasing size and complexity are nowbeing carried out by regional offices drawing on theskills and expertise of local advisers. New PrivateEquity houses are opening in the regions, those whoretracted a few years ago are opening new branches,

continued on page 2

råáíÉÇ=háåÖÇçãAlistair Lester

Richard Worker

Ten Trinity Square

London EC3P 3AX

Tel: +44 (0)20 7488 8111

dÉêã~åóAlbert Höyng

Gruneburgweg 102

Frankfurt am Main 60323

Tel: +49 69 95931-0

fí~äóSebastiano Doria

Via Tortona 33

20144 Milan

Tel: +39 02 47787301

cê~åÅÉJean-Luc Delcros

Gras Savoye

2 a 8 rue Ancellle

Neuilly Sur Seine, Paris 92202

Tel: +33 141 43 50 00

pïÉÇÉåJohan Forsgärd

Sergelgatan 1

S- 111 57 Stockholm

Tel +46 8 463 89 78

pé~áåJose Carlos Marcos

Paseo de la Castellana 36-38

4a Planta, Edificio Castellana

Madrid 28046

Tel: +34 91 423 3400

kÉíÜÉêä~åÇëSimon Cross

De Ruyterkade 7

Amsterdam 1013 AA

Tel: +31 20 531 2525

_ÉäÖáìãBart Smets

Gras Savoye Belgium

Zuiderlaan 91

1731 Zellik, Brussels

Tel: +32 2 481 1927

rp^=Mark Rusas

One World Financial Centre

200 Liberty Street

New York, 10281

Tel: +1 212 344 8888

g~é~å=Nobuto Ota

Ohtemachi Tatemono Toranomon

Bldg.10F

6-12 Toranomon 1-chome

Minato-ku, Tokyo 105-0001,

Tel: +81 3 3500 2523

mçêíìÖ~äCrispin Stillwell

Ed.Liberdade

Av.Da Liberdade

Lisbon 49-41250

Tel: +351 21 346 9621

^ìëíê~äá~Josh Roach

Level 8

2 Market Street

Sydney 2000

Tel: +61 292 854 0000

fåÇá~B Rammohan

111, Free Press House,

Free Press Journal Marg,

Nariman Point,

Mumbai 400 021

dêÉ~íÉê=`Üáå~Jason Wang

3502 The Lee Gardens

33 Hysan Avenue

Causeway Bay

+852 2830 0111

táååÉê=çÑ=píê~íÉÖáÅofphã~Ö~òáåÉDë=_Éëí=~åÇ=jçëífååçî~íáîÉ=_êçâÉê=çÑ=íÜÉ=vÉ~ê=OMMSÑçê=íÜÉ=ëÉÅçåÇ=ÅçåëÉÅìíáîÉ=óÉ~ê

táååÉê=çÑ=oÉ~Åíáçåë=j~Ö~òáåÉDëbìêçéÉ~å=`çããÉêÅá~ä=_êçâÉê=çÑ=íÜÉvÉ~ê=Ñçê=íÜÉ=ëÉÅçåÇ=ÅçåëÉÅìíáîÉ=óÉ~ê

táååÉê=çÑ=fåëìê~åÅÉ=qáãÉëk~íáçå~ä=_êçâÉê=çÑ=íÜÉ=óÉ~ê=OMMSÑçê=íÜÉ=ëÉÅçåÇ=ÅçåëÉÅìíáîÉ=óÉ~ê

Globalisation in Reverse?

We have again, this quarter, included an exert from theWillis Political Risk Index. The Political Risk Practicespecialises in structuring insurance products to mitigatethe risk of trading with, or investing in, volatile emergingmarkets. The Index was developed in conjunction withinternational consulting firm Oxford Analytica, andincludes expert contribution from political and economicanalysts based at universities and research institutesranging from Oxford University and the University ofLondon’s School of Oriental and African Studies to theUniversity of Natal in South Africa, and the Institute ofSouth East Asian Studies in Singapore.

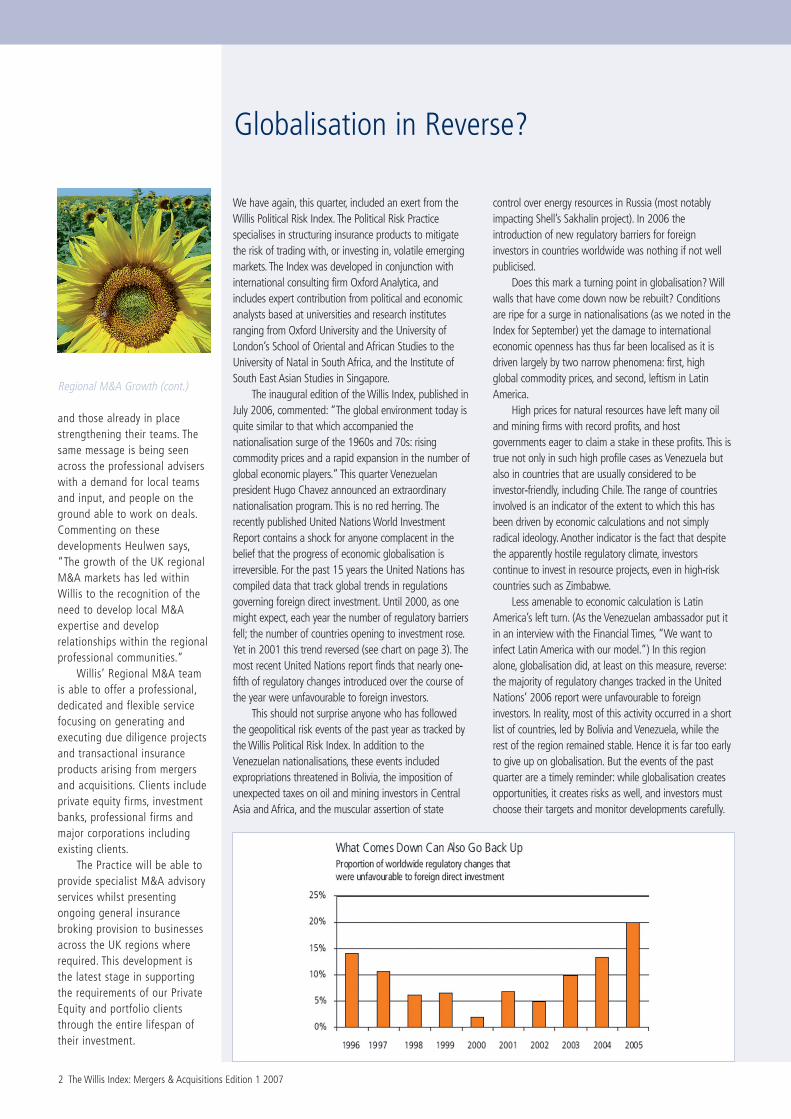

The inaugural edition of the Willis Index, published inJuly 2006, commented: “The global environment today isquite similar to that which accompanied thenationalisation surge of the 1960s and 70s: risingcommodity prices and a rapid expansion in the number ofglobal economic players.” This quarter Venezuelanpresident Hugo Chavez announced an extraordinarynationalisation program. This is no red herring. Therecently published United Nations World InvestmentReport contains a shock for anyone complacent in thebelief that the progress of economic globalisation isirreversible. For the past 15 years the United Nations hascompiled data that track global trends in regulationsgoverning foreign direct investment. Until 2000, as onemight expect, each year the number of regulatory barriersfell; the number of countries opening to investment rose.Yet in 2001 this trend reversed (see chart on page 3). Themost recent United Nations report finds that nearly one-fifth of regulatory changes introduced over the course ofthe year were unfavourable to foreign investors.

This should not surprise anyone who has followedthe geopolitical risk events of the past year as tracked bythe Willis Political Risk Index. In addition to theVenezuelan nationalisations, these events includedexpropriations threatened in Bolivia, the imposition ofunexpected taxes on oil and mining investors in CentralAsia and Africa, and the muscular assertion of state

control over energy resources in Russia (most notablyimpacting Shell’s Sakhalin project). In 2006 theintroduction of new regulatory barriers for foreigninvestors in countries worldwide was nothing if not wellpublicised.

Does this mark a turning point in globalisation? Willwalls that have come down now be rebuilt? Conditionsare ripe for a surge in nationalisations (as we noted in theIndex for September) yet the damage to internationaleconomic openness has thus far been localised as it isdriven largely by two narrow phenomena: first, highglobal commodity prices, and second, leftism in LatinAmerica.

High prices for natural resources have left many oiland mining firms with record profits, and hostgovernments eager to claim a stake in these profits. This istrue not only in such high profile cases as Venezuela butalso in countries that are usually considered to beinvestor-friendly, including Chile. The range of countriesinvolved is an indicator of the extent to which this hasbeen driven by economic calculations and not simplyradical ideology. Another indicator is the fact that despitethe apparently hostile regulatory climate, investorscontinue to invest in resource projects, even in high-riskcountries such as Zimbabwe.

Less amenable to economic calculation is LatinAmerica’s left turn. (As the Venezuelan ambassador put itin an interview with the Financial Times, “We want toinfect Latin America with our model.”) In this regionalone, globalisation did, at least on this measure, reverse:the majority of regulatory changes tracked in the UnitedNations’ 2006 report were unfavourable to foreigninvestors. In reality, most of this activity occurred in a shortlist of countries, led by Bolivia and Venezuela, while therest of the region remained stable. Hence it is far too earlyto give up on globalisation. But the events of the pastquarter are a timely reminder: while globalisation createsopportunities, it creates risks as well, and investors mustchoose their targets and monitor developments carefully.

2 The Willis Index: Mergers & Acquisitions Edition 1 2007

Regional M&A Growth (cont.)

and those already in placestrengthening their teams. Thesame message is being seenacross the professional adviserswith a demand for local teamsand input, and people on theground able to work on deals.Commenting on thesedevelopments Heulwen says,“The growth of the UK regionalM&A markets has led withinWillis to the recognition of theneed to develop local M&Aexpertise and developrelationships within the regionalprofessional communities.”

Willis’ Regional M&A teamis able to offer a professional,dedicated and flexible servicefocusing on generating andexecuting due diligence projectsand transactional insuranceproducts arising from mergersand acquisitions. Clients includeprivate equity firms, investmentbanks, professional firms andmajor corporations includingexisting clients.

The Practice will be able toprovide specialist M&A advisoryservices whilst presentingongoing general insurancebroking provision to businessesacross the UK regions whererequired. This development isthe latest stage in supportingthe requirements of our PrivateEquity and portfolio clientsthrough the entire lifespan oftheir investment.

táääáë The Willis Index: Mergers & Acquisitions Edition 1 2007 3

Airport Transactions

aÉîÉäçéãÉåíë=qÜáë=nì~êíÉêVenezuela’s shocking nationalisation program hasstolen the headlines. Last quarter we raised thetemperature on expropriation risk in Venezuela andwrote: “Risks are quite high as national policy in thisarea has become politicised and the administration ispursuing a model of state-led development. Anincreased state presence in sectors such as mining andhydrocarbons is likely.” This quarter we have raised therisk temperature still further.

Also in the headlines was Ethiopia, whose militaryaction against Islamists in Somalia may (some argue)be a positive development for Somalia, but is likely tomake Ethiopia more of a target for terrorism, leadingus to raise the risk temperature by two points. AfterVenezuela, the largest rating change occurred in theDemocratic Republic of Congo, which was upgraded,after the return of some degree of normalcy followinganother round of post-civil-war elections, which unlikethe first round was not marred by violence. The DRCwas not alone in achieving improvements: worldwide,upgrades once again surpassed downgrades thisquarter, 15 against 11, with 14 countries unchanged.

The most significant downgrades occurred inVenezuela and Ecuador. In Ecuador, pro-Chavezcandidate Rafael Correa achieved the presidency.Correa had supported the expulsion of US oil companyOccidental and mentioned the possibility ofsuspending debt repayments. Other downgradesincluded Iran, with international tension on the rise;Saudi Arabia, facing potential spill-over effects fromregional conflict; and Turkmenistan, which this quartersaw the death in office of its colourful and repressivedictatorial leader. Additional upgrades includedVietnam, continuing to integrate into the worldeconomy; the Philippines, regaining stability; Gabon,with continued good political and economicconditions; and Colombia, which is seeing results in itsongoing struggle against political violence, despitesome significant risks surrounding the demobilisationof right-wing paramilitary forces, a trend to bemonitored in the quarters ahead.

Over the last 12 months the Willis Mergers &Acquisitions Practice has been appointed to providedue diligence on a number of Private Equity backedshare purchase transactions for regional andinternational airports around the world. The complexityof the transactions may differ according to the often-intricate ownership structure of the target, but the duediligence focus remains the same, ensuring the currentand future operational aspects of the airports businessare adequately protected.

Due diligence requirements for airports extendfurther than simply a review of the insurance portfolioand the accompanying claims. Typically, the standardscope is extended to specifically include the following:- a thorough review of the specialised Aviation

sector insurance market.- benchmarking of the operators liability limit and

cost against peers.- investigation into previous or future

environmental issues with a risk transfer costproposal.

- future insurance costs analysis based on marketconditions and business plan.

- review of traditional and bespoke businessinterruption insurance solutions ranging fromrevenue protection to adverse weather andhurricane cover.

qÜÉ=fåëìê~åÅÉ=j~êâÉíDuring the course of 2006 there wasan increase in capacity in theaviation sector as a result of thearrival of CV Starr/Marlborough andQBE Limit in the Lloyd’s aviationunderwriting market. Between themthey can theoretically provide 30%capacity on a US$1.5bn limit,although this has yet to be seen. Ithas been enough, however, to causesignificant softening in airlineinsurance rates and, towards the end of 2006, had started to influence prices in the airportsector.

The theoretical maximumcapacity for this class at the endof 2006 is now estimated to bemore than 200% for a US$1.5bnlimit (see chart on page 4).However, it should be appreciatedthat these maximum theoreticalshares would only be deployedwhere the insurers were socomfortable with premium levelthat they wished to underwrite as

Willis M&A Firmly on the Radar

The Willis Index: Mergers & Acquisitions Edition 1 2007 4

large a share as possible. The mark of a competitiveplacement is one where it has only just been possibleto support the risk at the price being offered and inpractice the maximum limit currently sold to an airportoperator is approximately US$2bn and such a limittests the market’s appetite.

mêÉãáìã=jçîÉãÉåíë=aìêáåÖ=OMMSDuring the first quarter of 2006, the upwards trend of2005 continued with most policies seeing increases ofaround 5%, but by the end of the year the capacitychanges had brought about a softening with 10%reductions being achieved. This is the first softening inthis sector to be seen since 2001.

The above chart tracks the percentage premiumchanges in the airport sector for each quarter for alarge percentage of the global portfolio.

OMMS=fåÅáÇÉåíëAgainst the background of a general reduction in thenumber of aircraft accidents around the world, insurersare conscious of a disturbing incidence of near misses,either in the air or on the ground, often as a result ofrunway incursion. In many cases it is too early to tellwhether those losses which resulted in death or injurywill impact upon the Airport /ATC sector of the market,but what is making insurers especially nervous is thegrowing incidence of events at airports, some of whichmay not have resulted in accidents but came close todoing so.

Examples during only four months of 2006:

NSíÜ=gìäó=– rhWExcel Airways B737 near miss on take-off with vehiclesworking at the end of the runway.

OPêÇ=gìäó=– rp^WUnited B737 has near miss with Atlas Air B747

OTíÜ=^ìÖìëí=– rp^WComair CRJ 100 mistakenly took off from the generalaviation runway which was half the length the aircraftneeded, crashed killing 49. FAA sued by Comair.

OSíÜ=pÉéíÉãÄÉê=– hóêÖóëí~åWKyrgystan Airways TU154 collideswith US Military KC135 on therunway as it takes off.

OVíÜ=pÉéíÉãÄÉê=– _ê~òáäWGOL B737-800 and EmbraerLegacy executive jet collide mid-air. 154 dead.

PMíÜ=lÅíçÄÉê=– rp^WContinental B757 mistakenly tookoff from a runway for which it hadnot been cleared.

Despite the above incidents thepremiums in the sector aresoftening, but the incidence ofanother major loss could result ina sharp response from insurers.

aáäáÖÉåÅÉ=cçÅìëTypically the key insurances underreview are:- Airport Owners & Operators

Liability- Property Damage and

Business Interruption- Motor Airside Liability- Construction Insurances- Local Statutory Insurances

táääáë=bñéÉêíáëÉWillis Mergers & Acquisitionspractice is fully supported by adedicated Willis Aviation teamwho are able to providefocused guidance at eachstage of the transaction withfocus on all the key aspectsrequired for the particulardiligence and scope.

rh=`çåëìäí~íáçåAs reported in our Summer 2006 Willis Index, the ECDirective 2004/35 on Environmental Liability (the“Environmental Liability Directive”) must have beenimplemented by Member States by 30 April 2004. TheDirective was intended to prevent damage occurringto water, protected species, natural habitats and land,and to increase the responsibility of operators tomitigate such damage when it does occur.

In November 2006, the UK government released along awaited consultation document on options forimplementing the Environmental Liability Directive inEngland, Wales and Northern Ireland. A separateconsultation is being undertaken in Scotland. Many ofthe requirements of the Directive are mandatory, leavingMember States with little or no flexibility as to how suchmeasures are implemented. Certain aspects are,however, subject to the discretion and choice ofindividual Member States; it is these aspects on whichthe government is seeking opinion by raising specificquestions.

For a number of aspects, the government sets outits own proposals for implementation. For example, itis proposed that the threshold for land damage forthe purposes of the Environmental Liability Directivewill be the same as for Contaminated Land under Part2A of the Environmental Protection Act 1990 (i.e. atleast a “significant possibility” of “significant harm”being caused). Unlike a number of other MemberStates, the UK government does not propose toimplement compulsory financial security (such asEnvironmental Insurance), relying instead on the EC’splanned review of the uptake of such provisions in2010 to determine the need for such a requirement.

The deadline for responses to the consultation was 16 February 2007. The government plans tohold a second consultation on the draft legislation when issued.

EU EnvironmentalLiability Directive

5 The Willis Index: Mergers & Acquisitions Edition 1 2007

A significant UK-based propertyportfolio was being prepared forsale via a limited auctionprocess. A US propertyinvestment fund (PIF) identifiedthe portfolio as an attractivetarget and approached the Sellerwith a pre-emptive bid.

The Seller agreed tonegotiate exclusively with PIF fora period of 10 days, after whichthey would revert to the originalplan to sell by auction. A numberof potential bidders had alreadyindicated an interest inparticipating in the auction.

The holding structure for theportfolio was complex (to fit it all in it was necessary to printthe structure diagram on A3paper!) however a substantivecertificate as to property title was available.

PIF took a cautious approachto the investment and were keento see substantive recourse forthe seller warranties in relationto the holding vehicles in theregion of 15% of the acquisitioncost.

Seller was not willing toentertain this request during thepre-emptive bid negotiations.Their position was strong as theyhad a number of bidders liningup and they considered that theywould be unlikely to be requiredto give such recourse to thesuccessful bidder if theyconducted the auction process.

On approximately day threeof the 10-day exclusivity period,Willis were instructed by thelawyers on behalf of PIF toinvestigate the options for aWarranty & Indemnity policy toprotect the buyers from lossarising from breach of warranty.Willis provided quick preliminaryfeedback and commenceddiscussions with the insurancemarket to identify a lead insurer.

Meet the TeamCase Study

On day six, preliminary dealdocumentation was received forreview and initial market termswere released for client reviewlater that day. On day seven,Willis were instructed to proceedto full underwriting process withthe proposed lead insurer and toco-ordinate following insurers toprovide the full level of coverrequired.

The information flowcontinued apace on day eightand towards the end of the daylawyers for PIF advised that theinsurance placement was nowcrucial to the deal being agreedbetween the parties. Willis wereasked to negotiate the lowestpossible attachment point for theinsurance and were able tosecure terms based upon anexcess level of just 0.375% ofthe transaction value (standardexcess levels for W&I policieswould be in the region of 1%-2% of the transaction value).

Ongoing negotiationsregarding the policy terms andconditions continued on day nineand by the end of the day theexcess wording had been agreed,with just a few outstandingissues on the primary wordingremaining. On day 10, Insurersreviewed the final drafttransaction documentation andthe policy wording was finalised.Willis provided a final quotearound 5pm. The parties werefinally in a position to sign thetransaction documentation at4am, at which time Willis wereon hand to confirm the insurancecover was in place.

The strategic use of W&Iinsurance enabled PIF toconclude their pre-emptive bidwithin the required timeframe onterms that were acceptable tothe Seller, but still provided PIFwith the requisite security.

^äÑçåëç=`çåÇÉI táääáë=j~ÇêáÇAlfonso leads the Spanish M&A Practice for Willis. Priorto joining Willis, Alfonso spent nine years working in theRisk Management Department of another broker. He hasspecialised in the Oil & Gas and Technology &Communications sectors. Recently Alfonso has assisted in

a number of key global transactions, transferring his skill and localknowledge to maximise delivery. During this period, his involvement in riskmanagement for the main players of the Spanish market has resulted innumerous due diligence processes and involvement in W&I.

New JoinersoáÅÜ~êÇ=tçêâÉêmê~ÅíáÅÉ=iÉ~ÇÉê=– `äáÉåí=oÉä~íáçåëÜáéëRichard Worker has been recruited joined Willis Mergers & Acquisitions (M&A)Practice in 2006. As Practice Leader – Client Relationships he has responsibilityfor developing and managing the client relationship structure for Willis M&A.

Richard was previously Joint Managing Director of the Heath LambertM&A Practice, providing risk and insurance advisory services on entry and exitstrategy to mid-market and large international private equity investment fundsand corporates. He is a Chartered Insurance Practitioner and studied CorporateFinance at London Business School.

As a deal specialist he is widely regarded as one of the leading UKinsurance corporate advisors on transaction insurance and risk issues to thePrivate Equity community and its portfolio companies, having advised on asignificant number transactions in his 15 years’ involvement in the sector.

Richard is a member of the M&A executive committee working withAlistair Lester, International Practice Leader, Sebastiano Doria, Practice Leader –Continental Europe and Doug Smith, Non Executive Deputy Chairman (anotherrecent high profile Willis M&A recruit), and the wider Willis team of specialistM&A associates.

f~å=hÉååÉííI _^=EeçåëF^`ff=– mêçàÉÅí=aáêÉÅíçêIan has worked in the insurance industry since 1986. He gained 15 yearsexperience in underwriting Property business for a number of insurancecompanies across a diverse range of industry sectors including PrivateEquity investments. Latterly he has specialised in global Mergers &Acquisitions due diligence for a range of Private Equity led transactions.

oáÅÜ~=pÜìâä~I ii_qÉ~ã=pçäáÅáíçêRicha joined the M&A, Transaction Solutions team at Willis in November2006. Having completed her Bachelors degrees in History and Law, Richaqualified as an Advocate of Bar Council of India in 1997 and as a Solicitorof Supreme Court of England & Wales in 2002. Richa has practised in thearea of company/commercial law with law firms in Delhi and London.

As part of the Transaction Solutions team, Richa focuses on providinglegal and technical solutions for the transfer of risks involved in mergerand acquisition transactions.

Transaction Solution Productsassist in Property Deal

Willis Mergers & Acquisitions Practice performed theinsurance due diligence on the

on behalf of

aÉÅÉãÄÉê=OMMSThis announcement appears as a matter of record only

FIN/5268/0407

Willis Limited, Registered number: 181116 England and Wales.Registered address: Ten Trinity Square, London EC3P 3AX.

A Lloyd's Broker. Authorised and regulated by the Financial Services Authority.

Willis Mergers & Acquisitions Practice performed insurance due diligence on the

£60,000,000acquisition of

by

g~åì~êó=OMMTThis announcement appears as a matter of record only

Willis Mergers & Acquisitions Practice performed insurance due diligence on the

acquisition of

by

cÉÄêì~êó=OMMTThis announcement appears as a matter of record only

Willis Mergers & Acquisitions Practice performed theinsurance due diligence on the

£32,000,000investment in

by

kçîÉãÄÉê=OMMSThis announcement appears as a matter of record only

Willis Mergers & Acquisitions Practice performed insurance due diligence on the

acquisition of

`~ääáÖ~êáë=pé~

by

aÉÅÉãÄÉê==OMMSThis announcement appears as a matter of record only

Willis Mergers & Acquisitions Practice performed insurance due diligence on the

acquisition of

by

backed by

g~åì~êó=OMMTThis announcement appears as a matter of record only

Willis Mergers & Acquisitions Practice performed insurancedue diligence on the joint venture transaction between

and

pÉîÉå=kÉíïçêâ=iáãáíÉÇto form

pÉîÉå=jÉÇá~=dêçìé

kçîÉãÄÉê=OMMSThis announcement appears as a matter of record only

Willis Mergers & Acquisitions Practice performed insurance due diligence on the

acquisition of

by

aÉÅÉãÄÉê=OMMSThis announcement appears as a matter of record only

Gras Savoye (a Willis Partner) Mergers & AcquisitionsPractice performed insurance due diligence on the

acquisition of

by

g~åì~êó=OMMTThis announcement appears as a matter of record only

Willis Mergers & Acquisitions Practice performed vendorinsurance due diligence on the

£588,000,000disposal of

by

j~êÅÜ=OMMTThis announcement appears as a matter of record only

Willis Mergers & Acquisitions Practice performed insurance due diligence on the

accquisition of

by

and

aÉÅÉãÄÉê=OMMSThis announcement appears as a matter of record only

Willis Mergers & Acquisitions Practice performed insurance due diligence on the

acquisition of

by

aÉÅÉãÄÉê=OMMSThis announcement appears as a matter of record only

Willis Mergers & Acquisitions Practice performed insurance due diligence on the

acquisition of

by

kçîÉãÄÉê=OMMSThis announcement appears as a matter of record only

Willis Mergers & Acquisitions Practice performed insurancedue diligence on the

1,725,000,000acquisition of

by

kçîÉãÄÉê==OMMSThis announcement appears as a matter of record only

Willis Mergers & Acquisitions Practice performed theinsurance due diligence on the

management buy-out of

on behalf of

aÉÅÉãÄÉê=OMMSThis announcement appears as a matter of record only

Willis Mergers & Acquisitions Practice performed theinsurance due diligence for the

$275,000,000simultaneous acquisition of the majority stake in General

Electric Commercial Aviation Training (“GECAT”) from GE’sCommercial Aviation Services business (“GECAS”); and the

entire share capital of SAS Flight Academy (“FlightAcademy”) from SAS AB (“SAS”)

by

j~êÅÜ=OMMTThis announcement appears as a matter of record only