The Welfare Costs of Business Cycles in Robust Economies with Individual Consumption...

93

The Welfare Costs of Business Cycles in Robust Economies with Individual Consumption Risk Martin Ellison Thomas J Sargent University of Oxford New York University Martin Ellison and Thomas J. Sargent Robustness and Consumption Risk 1 / 23

Transcript of The Welfare Costs of Business Cycles in Robust Economies with Individual Consumption...

The Welfare Costs of Business Cycles in RobustEconomies with Individual Consumption Risk

Martin Ellison Thomas J SargentUniversity of Oxford New York University

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 1 / 23

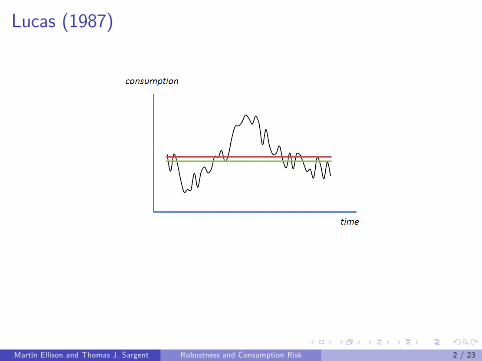

Lucas (1987)

Calculate welfare gain in simple model

≈ 0.1% of steady-state consumption

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 2 / 23

Lucas (1987)

Calculate welfare gain in simple model

≈ 0.1% of steady-state consumption

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 2 / 23

Lucas (1987)

Calculate welfare gain in simple model

≈ 0.1% of steady-state consumption

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 2 / 23

Lucas (1987)

Calculate welfare gain in simple model

≈ 0.1% of steady-state consumption

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 2 / 23

Increasing the welfare costs of business cycles

Increase persistence of consumption shocks

Increase risk aversion

Introduce aggregate and idiosyncratic risk

Introduce a preference for robustness

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 3 / 23

Increasing the welfare costs of business cycles

Increase persistence of consumption shocks

Increase risk aversion

Introduce aggregate and idiosyncratic risk

Introduce a preference for robustness

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 3 / 23

Increasing the welfare costs of business cycles

Increase persistence of consumption shocks

Increase risk aversion

Introduce aggregate and idiosyncratic risk

Introduce a preference for robustness

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 3 / 23

Increasing the welfare costs of business cycles

Increase persistence of consumption shocks

Increase risk aversion

Introduce aggregate and idiosyncratic risk

Introduce a preference for robustness

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 3 / 23

Increasing the welfare costs of business cycles

Increase persistence of consumption shocks

Increase risk aversion

Introduce aggregate and idiosyncratic risk

Introduce a preference for robustness

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 3 / 23

What we do

Introduce aggregate and idiosyncratic risk

I Consumption subject to aggregate and idiosyncratic shocksI De Santis (2007)I Heterogeneous agent model

Introduce a preference for robustness

I Tallarini (2000) uses Epstein-Zin preferences to separate risk aversionfrom intertemporal elasticity of substitution

I High risk aversion needed for business cycles to be costlyI Barillas, Hansen and Sargent (2009) reinterpret high risk aversion aspreference for robustness

We look at combined effect of idiosyncratic risk and robustness

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 4 / 23

What we do

Introduce aggregate and idiosyncratic risk

I Consumption subject to aggregate and idiosyncratic shocksI De Santis (2007)I Heterogeneous agent model

Introduce a preference for robustness

I Tallarini (2000) uses Epstein-Zin preferences to separate risk aversionfrom intertemporal elasticity of substitution

I High risk aversion needed for business cycles to be costlyI Barillas, Hansen and Sargent (2009) reinterpret high risk aversion aspreference for robustness

We look at combined effect of idiosyncratic risk and robustness

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 4 / 23

What we do

Introduce aggregate and idiosyncratic riskI Consumption subject to aggregate and idiosyncratic shocks

I De Santis (2007)I Heterogeneous agent model

Introduce a preference for robustness

I Tallarini (2000) uses Epstein-Zin preferences to separate risk aversionfrom intertemporal elasticity of substitution

I High risk aversion needed for business cycles to be costlyI Barillas, Hansen and Sargent (2009) reinterpret high risk aversion aspreference for robustness

We look at combined effect of idiosyncratic risk and robustness

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 4 / 23

What we do

Introduce aggregate and idiosyncratic riskI Consumption subject to aggregate and idiosyncratic shocksI De Santis (2007)

I Heterogeneous agent model

Introduce a preference for robustness

I Tallarini (2000) uses Epstein-Zin preferences to separate risk aversionfrom intertemporal elasticity of substitution

I High risk aversion needed for business cycles to be costlyI Barillas, Hansen and Sargent (2009) reinterpret high risk aversion aspreference for robustness

We look at combined effect of idiosyncratic risk and robustness

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 4 / 23

What we do

Introduce aggregate and idiosyncratic riskI Consumption subject to aggregate and idiosyncratic shocksI De Santis (2007)I Heterogeneous agent model

Introduce a preference for robustness

I Tallarini (2000) uses Epstein-Zin preferences to separate risk aversionfrom intertemporal elasticity of substitution

I High risk aversion needed for business cycles to be costlyI Barillas, Hansen and Sargent (2009) reinterpret high risk aversion aspreference for robustness

We look at combined effect of idiosyncratic risk and robustness

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 4 / 23

What we do

Introduce aggregate and idiosyncratic riskI Consumption subject to aggregate and idiosyncratic shocksI De Santis (2007)I Heterogeneous agent model

Introduce a preference for robustness

I Tallarini (2000) uses Epstein-Zin preferences to separate risk aversionfrom intertemporal elasticity of substitution

I High risk aversion needed for business cycles to be costlyI Barillas, Hansen and Sargent (2009) reinterpret high risk aversion aspreference for robustness

We look at combined effect of idiosyncratic risk and robustness

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 4 / 23

What we do

Introduce aggregate and idiosyncratic riskI Consumption subject to aggregate and idiosyncratic shocksI De Santis (2007)I Heterogeneous agent model

Introduce a preference for robustnessI Tallarini (2000) uses Epstein-Zin preferences to separate risk aversionfrom intertemporal elasticity of substitution

I High risk aversion needed for business cycles to be costlyI Barillas, Hansen and Sargent (2009) reinterpret high risk aversion aspreference for robustness

We look at combined effect of idiosyncratic risk and robustness

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 4 / 23

What we do

Introduce aggregate and idiosyncratic riskI Consumption subject to aggregate and idiosyncratic shocksI De Santis (2007)I Heterogeneous agent model

Introduce a preference for robustnessI Tallarini (2000) uses Epstein-Zin preferences to separate risk aversionfrom intertemporal elasticity of substitution

I High risk aversion needed for business cycles to be costly

I Barillas, Hansen and Sargent (2009) reinterpret high risk aversion aspreference for robustness

We look at combined effect of idiosyncratic risk and robustness

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 4 / 23

What we do

Introduce aggregate and idiosyncratic riskI Consumption subject to aggregate and idiosyncratic shocksI De Santis (2007)I Heterogeneous agent model

Introduce a preference for robustnessI Tallarini (2000) uses Epstein-Zin preferences to separate risk aversionfrom intertemporal elasticity of substitution

I High risk aversion needed for business cycles to be costlyI Barillas, Hansen and Sargent (2009) reinterpret high risk aversion aspreference for robustness

We look at combined effect of idiosyncratic risk and robustness

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 4 / 23

What we do

Introduce aggregate and idiosyncratic riskI Consumption subject to aggregate and idiosyncratic shocksI De Santis (2007)I Heterogeneous agent model

Introduce a preference for robustnessI Tallarini (2000) uses Epstein-Zin preferences to separate risk aversionfrom intertemporal elasticity of substitution

I High risk aversion needed for business cycles to be costlyI Barillas, Hansen and Sargent (2009) reinterpret high risk aversion aspreference for robustness

We look at combined effect of idiosyncratic risk and robustness

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 4 / 23

A preference for robustness

Agents fear model misspecification

Ut = (1− β)V (c it )−1σlog Et exp(−σβUt+1)

Recursive multiplier preferences of Hansen and Sargent (2001)

Preference for robustness σ > 0

σ ↑ → greater fear of misspecification

σ→ 0 means Ut = (1− β)V (c it ) + βEtUt+1

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 5 / 23

A preference for robustness

Agents fear model misspecification

Ut = (1− β)V (c it )−1σlog Et exp(−σβUt+1)

Recursive multiplier preferences of Hansen and Sargent (2001)

Preference for robustness σ > 0

σ ↑ → greater fear of misspecification

σ→ 0 means Ut = (1− β)V (c it ) + βEtUt+1

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 5 / 23

A preference for robustness

Agents fear model misspecification

Ut = (1− β)V (c it )−1σlog Et exp(−σβUt+1)

Recursive multiplier preferences of Hansen and Sargent (2001)

Preference for robustness σ > 0

σ ↑ → greater fear of misspecification

σ→ 0 means Ut = (1− β)V (c it ) + βEtUt+1

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 5 / 23

A preference for robustness

Agents fear model misspecification

Ut = (1− β)V (c it )−1σlog Et exp(−σβUt+1)

Recursive multiplier preferences of Hansen and Sargent (2001)

Preference for robustness σ > 0

σ ↑ → greater fear of misspecification

σ→ 0 means Ut = (1− β)V (c it ) + βEtUt+1

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 5 / 23

A preference for robustness

Agents fear model misspecification

Ut = (1− β)V (c it )−1σlog Et exp(−σβUt+1)

Recursive multiplier preferences of Hansen and Sargent (2001)

Preference for robustness σ > 0

σ ↑ → greater fear of misspecification

σ→ 0 means Ut = (1− β)V (c it ) + βEtUt+1

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 5 / 23

A preference for robustness

Agents fear model misspecification

Ut = (1− β)V (c it )−1σlog Et exp(−σβUt+1)

Recursive multiplier preferences of Hansen and Sargent (2001)

Preference for robustness σ > 0

σ ↑ → greater fear of misspecification

σ→ 0 means Ut = (1− β)V (c it ) + βEtUt+1

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 5 / 23

Aggregate and idiosyncratic risk

Consumption process

c it = ct + δit

∆ct+1 =√

εw1t+1∆δit+1 =

√εw2t+1

w1t+1 ∼ N(g − τ21/2, τ21) and w2t+1 ∼ N(−τ22/2, τ

22)

Result of aggregate and idiosyncratic shocks

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 6 / 23

Aggregate and idiosyncratic risk

Consumption process

c it = ct + δit

∆ct+1 =√

εw1t+1∆δit+1 =

√εw2t+1

w1t+1 ∼ N(g − τ21/2, τ21) and w2t+1 ∼ N(−τ22/2, τ

22)

Result of aggregate and idiosyncratic shocks

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 6 / 23

Aggregate and idiosyncratic risk

Consumption process

c it = ct + δit

∆ct+1 =√

εw1t+1∆δit+1 =

√εw2t+1

w1t+1 ∼ N(g − τ21/2, τ21) and w2t+1 ∼ N(−τ22/2, τ

22)

Result of aggregate and idiosyncratic shocks

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 6 / 23

Aggregate and idiosyncratic risk

Consumption process

c it = ct + δit

∆ct+1 =√

εw1t+1∆δit+1 =

√εw2t+1

w1t+1 ∼ N(g − τ21/2, τ21) and w2t+1 ∼ N(−τ22/2, τ

22)

Result of aggregate and idiosyncratic shocks

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 6 / 23

Solution

Solution satisfies value function:

W E (c it ) = (1− β)V (c it )−1σlog Et exp(−σβW E (c it+1))

c it+1 = c it +√

ε(w1t+1 + w2t+1)

Small noise approximation of Andersen, Hansen and Sargent (2011).

Solution of form W E (c it ) = W0(c it ) + h(c

it )

W 0(c it ) satisfies value function for√

ε = 0

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 7 / 23

Solution

Solution satisfies value function:

W E (c it ) = (1− β)V (c it )−1σlog Et exp(−σβW E (c it+1))

c it+1 = c it +√

ε(w1t+1 + w2t+1)

Small noise approximation of Andersen, Hansen and Sargent (2011).

Solution of form W E (c it ) = W0(c it ) + h(c

it )

W 0(c it ) satisfies value function for√

ε = 0

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 7 / 23

Solution

Solution satisfies value function:

W E (c it ) = (1− β)V (c it )−1σlog Et exp(−σβW E (c it+1))

c it+1 = c it +√

ε(w1t+1 + w2t+1)

Small noise approximation of Andersen, Hansen and Sargent (2011).

Solution of form W E (c it ) = W0(c it ) + h(c

it )

W 0(c it ) satisfies value function for√

ε = 0

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 7 / 23

Solution

Solution satisfies value function:

W E (c it ) = (1− β)V (c it )−1σlog Et exp(−σβW E (c it+1))

c it+1 = c it +√

ε(w1t+1 + w2t+1)

Small noise approximation of Andersen, Hansen and Sargent (2011).

Solution of form W E (c it ) = W0(c it ) + h(c

it )

W 0(c it ) satisfies value function for√

ε = 0

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 7 / 23

Solution

Solution satisfies value function:

W E (c it ) = (1− β)V (c it )−1σlog Et exp(−σβW E (c it+1))

c it+1 = c it +√

ε(w1t+1 + w2t+1)

Small noise approximation of Andersen, Hansen and Sargent (2011).

Solution of form W E (c it ) = W0(c it ) + h(c

it )

W 0(c it ) satisfies value function for√

ε = 0

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 7 / 23

Approximate solution

No noise solution W 0(c it ) = V (cit )

Small noise solution:

W 0(c it ) + h(cit ) = (1− β)V (c it )

− 1σlog Et exp

(−σβW E (W 0(c it+1)

+h(c it+1))

)c it+1 = c it +

√ε(w1t+1 + w2t+1)

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 8 / 23

Approximate solution

No noise solution W 0(c it ) = V (cit )

Small noise solution:

W 0(c it ) + h(cit ) = (1− β)V (c it )

− 1σlog Et exp

(−σβW E (W 0(c it+1)

+h(c it+1))

)c it+1 = c it +

√ε(w1t+1 + w2t+1)

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 8 / 23

Approximate solution

No noise solution W 0(c it ) = V (cit )

Small noise solution:

W 0(c it ) + h(cit ) = (1− β)V (c it )

− 1σlog Et exp

(−σβW E (W 0(c it+1)

+h(c it+1))

)c it+1 = c it +

√ε(w1t+1 + w2t+1)

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 8 / 23

Small noise expansion

Expansion for small√

ε:

e−σβ(W 0(c it+1)+h(cit+1)) = e−σβ(W 0(c it )+h(c

it ))

×(1+

∞

∑n=1

εn/2µ′nn!

(w1t+1 + w2t+1)n)

µ′n = κn +n−1∑m=1

(n− 1m− 1

)κmµ′n−m

κn = −σβDn(W 0(c it ) + h(cit ))

Take expectations, apply logarithm and expand

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 9 / 23

Small noise expansion

Expansion for small√

ε:

e−σβ(W 0(c it+1)+h(cit+1)) = e−σβ(W 0(c it )+h(c

it ))

×(1+

∞

∑n=1

εn/2µ′nn!

(w1t+1 + w2t+1)n)

µ′n = κn +n−1∑m=1

(n− 1m− 1

)κmµ′n−m

κn = −σβDn(W 0(c it ) + h(cit ))

Take expectations, apply logarithm and expand

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 9 / 23

Small noise expansion

Expansion for small√

ε:

e−σβ(W 0(c it+1)+h(cit+1)) = e−σβ(W 0(c it )+h(c

it ))

×(1+

∞

∑n=1

εn/2µ′nn!

(w1t+1 + w2t+1)n)

µ′n = κn +n−1∑m=1

(n− 1m− 1

)κmµ′n−m

κn = −σβDn(W 0(c it ) + h(cit ))

Take expectations, apply logarithm and expand

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 9 / 23

Undetermined coeffi cients

Solution satisfies:

(1− β)h(c it ) = −∞

∑k=1

(−1)k+1kσ(

∞

∑n=1

εn/2µ′nn!

Et (w1t+1 + w2t+1)n)k

Propose solution of form:

h(c it ) =∞

∑n=1

εn/2hn(c it )

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 10 / 23

Undetermined coeffi cients

Solution satisfies:

(1− β)h(c it ) = −∞

∑k=1

(−1)k+1kσ(

∞

∑n=1

εn/2µ′nn!

Et (w1t+1 + w2t+1)n)k

Propose solution of form:

h(c it ) =∞

∑n=1

εn/2hn(c it )

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 10 / 23

Undetermined coeffi cients

Solution satisfies:

(1− β)h(c it ) = −∞

∑k=1

(−1)k+1kσ(

∞

∑n=1

εn/2µ′nn!

Et (w1t+1 + w2t+1)n)k

Propose solution of form:

h(c it ) =∞

∑n=1

εn/2hn(c it )

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 10 / 23

Small noise solution

First order term:

h1(c it ) =Et (w1t+1 + w2t+1)

1− ββDW 0(c it )

Second order term:

h2(c it ) =Et (w1t+1 + w2t+1)

1− ββDh1(c it )

+Et (w1t+1 + w2t+1)2

2σ(1− β)

(σβD2W 0(c it )−(σβDW 0(c it )

)2 )

+(Et (w1t+1 + w2t+1))

2

2σ(1− β)

(σβDW 0(c it )

)2

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 11 / 23

Small noise solution

First order term:

h1(c it ) =Et (w1t+1 + w2t+1)

1− ββDW 0(c it )

Second order term:

h2(c it ) =Et (w1t+1 + w2t+1)

1− ββDh1(c it )

+Et (w1t+1 + w2t+1)2

2σ(1− β)

(σβD2W 0(c it )−(σβDW 0(c it )

)2 )

+(Et (w1t+1 + w2t+1))

2

2σ(1− β)

(σβDW 0(c it )

)2

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 11 / 23

Small noise solution

First order term:

h1(c it ) =Et (w1t+1 + w2t+1)

1− ββDW 0(c it )

Second order term:

h2(c it ) =Et (w1t+1 + w2t+1)

1− ββDh1(c it )

+Et (w1t+1 + w2t+1)2

2σ(1− β)

(σβD2W 0(c it )−(σβDW 0(c it )

)2 )

+(Et (w1t+1 + w2t+1))

2

2σ(1− β)

(σβDW 0(c it )

)2

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 11 / 23

Why second order?

Consumption process c it+1 = cit +√

ε(w1t+1 + w2t+1)

First order in ε has terms in Et (w1t+1 + w2t+1)2 = τ21 + τ22 + t.i .risk

Second order has terms inEt (w1t+1 + w2t+1)4 = 3τ41 + 2τ21τ

22 + 3τ42 + t.i .risk

Only second order approximation captures interaction betweenaggregate and idiosyncratic risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 12 / 23

Why second order?

Consumption process c it+1 = cit +√

ε(w1t+1 + w2t+1)

First order in ε has terms in Et (w1t+1 + w2t+1)2 = τ21 + τ22 + t.i .risk

Second order has terms inEt (w1t+1 + w2t+1)4 = 3τ41 + 2τ21τ

22 + 3τ42 + t.i .risk

Only second order approximation captures interaction betweenaggregate and idiosyncratic risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 12 / 23

Why second order?

Consumption process c it+1 = cit +√

ε(w1t+1 + w2t+1)

First order in ε has terms in Et (w1t+1 + w2t+1)2 = τ21 + τ22 + t.i .risk

Second order has terms inEt (w1t+1 + w2t+1)4 = 3τ41 + 2τ21τ

22 + 3τ42 + t.i .risk

Only second order approximation captures interaction betweenaggregate and idiosyncratic risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 12 / 23

Why second order?

Consumption process c it+1 = cit +√

ε(w1t+1 + w2t+1)

First order in ε has terms in Et (w1t+1 + w2t+1)2 = τ21 + τ22 + t.i .risk

Second order has terms inEt (w1t+1 + w2t+1)4 = 3τ41 + 2τ21τ

22 + 3τ42 + t.i .risk

Only second order approximation captures interaction betweenaggregate and idiosyncratic risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 12 / 23

Why second order?

Consumption process c it+1 = cit +√

ε(w1t+1 + w2t+1)

First order in ε has terms in Et (w1t+1 + w2t+1)2 = τ21 + τ22 + t.i .risk

Second order has terms inEt (w1t+1 + w2t+1)4 = 3τ41 + 2τ21τ

22 + 3τ42 + t.i .risk

Only second order approximation captures interaction betweenaggregate and idiosyncratic risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 12 / 23

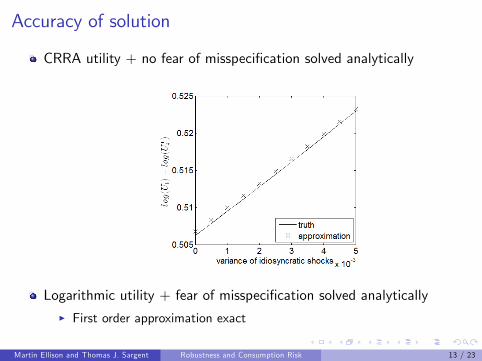

Accuracy of solution

CRRA utility + no fear of misspecification solved analytically

Logarithmic utility + fear of misspecification solved analytically

I First order approximation exact

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 13 / 23

Accuracy of solution

CRRA utility + no fear of misspecification solved analytically

Logarithmic utility + fear of misspecification solved analytically

I First order approximation exact

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 13 / 23

Accuracy of solution

CRRA utility + no fear of misspecification solved analytically

Logarithmic utility + fear of misspecification solved analytically

I First order approximation exact

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 13 / 23

Accuracy of solution

CRRA utility + no fear of misspecification solved analytically

Logarithmic utility + fear of misspecification solved analyticallyI First order approximation exact

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 13 / 23

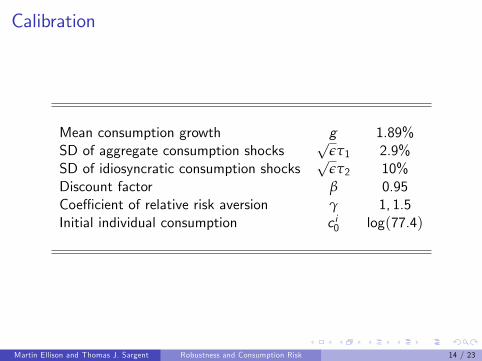

Calibration

Mean consumption growth g 1.89%SD of aggregate consumption shocks

√ετ1 2.9%

SD of idiosyncratic consumption shocks√

ετ2 10%Discount factor β 0.95Coeffi cient of relative risk aversion γ 1, 1.5Initial individual consumption c i0 log(77.4)

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 14 / 23

Calibration

Mean consumption growth g 1.89%SD of aggregate consumption shocks

√ετ1 2.9%

SD of idiosyncratic consumption shocks√

ετ2 10%Discount factor β 0.95Coeffi cient of relative risk aversion γ 1, 1.5Initial individual consumption c i0 log(77.4)

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 14 / 23

Calibrating the fear of misspecification

Detection error probability metric

Andersen, Hansen and Sargent (2003)

Agent fears models that are statistically similar in finite samples12 {P(accepting incorrect model) + P(rejecting correct model)}50%, 45%, 40%

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 15 / 23

Calibrating the fear of misspecification

Detection error probability metric

Andersen, Hansen and Sargent (2003)

Agent fears models that are statistically similar in finite samples12 {P(accepting incorrect model) + P(rejecting correct model)}50%, 45%, 40%

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 15 / 23

Calibrating the fear of misspecification

Detection error probability metric

Andersen, Hansen and Sargent (2003)

Agent fears models that are statistically similar in finite samples12 {P(accepting incorrect model) + P(rejecting correct model)}50%, 45%, 40%

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 15 / 23

Calibrating the fear of misspecification

Detection error probability metric

Andersen, Hansen and Sargent (2003)

Agent fears models that are statistically similar in finite samples

12 {P(accepting incorrect model) + P(rejecting correct model)}50%, 45%, 40%

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 15 / 23

Calibrating the fear of misspecification

Detection error probability metric

Andersen, Hansen and Sargent (2003)

Agent fears models that are statistically similar in finite samples12 {P(accepting incorrect model) + P(rejecting correct model)}

50%, 45%, 40%

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 15 / 23

Calibrating the fear of misspecification

Detection error probability metric

Andersen, Hansen and Sargent (2003)

Agent fears models that are statistically similar in finite samples12 {P(accepting incorrect model) + P(rejecting correct model)}50%, 45%, 40%

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 15 / 23

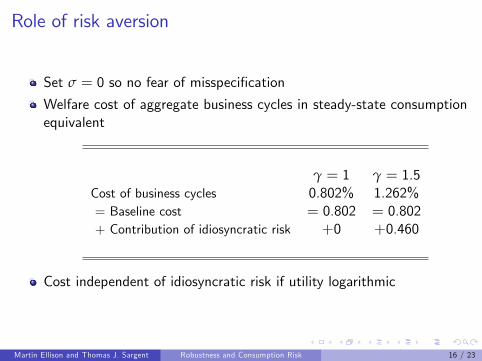

Role of risk aversion

Set σ = 0 so no fear of misspecification

Welfare cost of aggregate business cycles in steady-state consumptionequivalent

γ = 1 γ = 1.5Cost of business cycles 0.802% 1.262%= Baseline cost = 0.802 = 0.802+ Contribution of idiosyncratic risk +0 +0.460

Cost independent of idiosyncratic risk if utility logarithmic

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 16 / 23

Role of risk aversion

Set σ = 0 so no fear of misspecification

Welfare cost of aggregate business cycles in steady-state consumptionequivalent

γ = 1 γ = 1.5Cost of business cycles 0.802% 1.262%= Baseline cost = 0.802 = 0.802+ Contribution of idiosyncratic risk +0 +0.460

Cost independent of idiosyncratic risk if utility logarithmic

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 16 / 23

Role of risk aversion

Set σ = 0 so no fear of misspecification

Welfare cost of aggregate business cycles in steady-state consumptionequivalent

γ = 1 γ = 1.5Cost of business cycles 0.802% 1.262%= Baseline cost = 0.802 = 0.802+ Contribution of idiosyncratic risk +0 +0.460

Cost independent of idiosyncratic risk if utility logarithmic

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 16 / 23

Role of risk aversion

Set σ = 0 so no fear of misspecification

Welfare cost of aggregate business cycles in steady-state consumptionequivalent

γ = 1 γ = 1.5Cost of business cycles 0.802% 1.262%= Baseline cost = 0.802 = 0.802+ Contribution of idiosyncratic risk +0 +0.460

Cost independent of idiosyncratic risk if utility logarithmic

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 16 / 23

Add fear of misspecification

Set γ = 1.5 so mildly risk averse

detection error probability 50% 40%Cost of business cycles 1.088% 1.706%= Baseline cost = 1.020 = 1.020+ Contribution of idiosyncratic risk +0.068 +0.068+ Contribution of robustness +0 +0.402

+Joint contribution ofidiosyncratic risk and robustness

+0 +0.217

Interaction between robustness and idiosyncratic risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 17 / 23

Add fear of misspecification

Set γ = 1.5 so mildly risk averse

detection error probability 50% 40%Cost of business cycles 1.088% 1.706%= Baseline cost = 1.020 = 1.020+ Contribution of idiosyncratic risk +0.068 +0.068+ Contribution of robustness +0 +0.402

+Joint contribution ofidiosyncratic risk and robustness

+0 +0.217

Interaction between robustness and idiosyncratic risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 17 / 23

Add fear of misspecification

Set γ = 1.5 so mildly risk averse

detection error probability 50% 40%Cost of business cycles 1.088% 1.706%= Baseline cost = 1.020 = 1.020+ Contribution of idiosyncratic risk +0.068 +0.068+ Contribution of robustness +0 +0.402

+Joint contribution ofidiosyncratic risk and robustness

+0 +0.217

Interaction between robustness and idiosyncratic risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 17 / 23

Intuition

f (ct+1) conditional density of aggregate and idiosyncraticconsumption under approximating model

f (ct+1) = m(ct+1)f (ct+1) worst-case density to fear

mt+1 ∝ exp(−σβUt+1)

detection error p 50% 40%w1t 0 −0.532× 10−3w2t 0 −6.315× 10−3σ1 (2.9%)2 (2.90041%)2

σ2 10% 10.0171%ρw1,w2 0 0.995× 10−3

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 18 / 23

Intuition

f (ct+1) conditional density of aggregate and idiosyncraticconsumption under approximating model

f (ct+1) = m(ct+1)f (ct+1) worst-case density to fear

mt+1 ∝ exp(−σβUt+1)

detection error p 50% 40%w1t 0 −0.532× 10−3w2t 0 −6.315× 10−3σ1 (2.9%)2 (2.90041%)2

σ2 10% 10.0171%ρw1,w2 0 0.995× 10−3

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 18 / 23

Intuition

f (ct+1) conditional density of aggregate and idiosyncraticconsumption under approximating model

f (ct+1) = m(ct+1)f (ct+1) worst-case density to fear

mt+1 ∝ exp(−σβUt+1)

detection error p 50% 40%w1t 0 −0.532× 10−3w2t 0 −6.315× 10−3σ1 (2.9%)2 (2.90041%)2

σ2 10% 10.0171%ρw1,w2 0 0.995× 10−3

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 18 / 23

Intuition

f (ct+1) conditional density of aggregate and idiosyncraticconsumption under approximating model

f (ct+1) = m(ct+1)f (ct+1) worst-case density to fear

mt+1 ∝ exp(−σβUt+1)

detection error p 50% 40%w1t 0 −0.532× 10−3w2t 0 −6.315× 10−3σ1 (2.9%)2 (2.90041%)2

σ2 10% 10.0171%ρw1,w2 0 0.995× 10−3

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 18 / 23

Approximating and worst-case densities

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 19 / 23

Approximating and worst-case densities

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 19 / 23

Alternative consumption process

Idiosyncratic consumption process has cyclical job displacement risk:

w2t =

−dH with prob πpHpHdH1−pH with prob π(1− pH )−dL with prob (1− π)pLpLdL1−pL with prob (1− π)(1− pL)

.

Compare with acyclical job displacement risk process:

w2t =

{−d with prob ppd1−p with prob 1− p

Krebs (2007)

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 20 / 23

Alternative consumption process

Idiosyncratic consumption process has cyclical job displacement risk:

w2t =

−dH with prob πpHpHdH1−pH with prob π(1− pH )−dL with prob (1− π)pLpLdL1−pL with prob (1− π)(1− pL)

.

Compare with acyclical job displacement risk process:

w2t =

{−d with prob ppd1−p with prob 1− p

Krebs (2007)

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 20 / 23

Alternative consumption process

Idiosyncratic consumption process has cyclical job displacement risk:

w2t =

−dH with prob πpHpHdH1−pH with prob π(1− pH )−dL with prob (1− π)pLpLdL1−pL with prob (1− π)(1− pL)

.

Compare with acyclical job displacement risk process:

w2t =

{−d with prob ppd1−p with prob 1− p

Krebs (2007)

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 20 / 23

Alternative consumption process

Idiosyncratic consumption process has cyclical job displacement risk:

w2t =

−dH with prob πpHpHdH1−pH with prob π(1− pH )−dL with prob (1− π)pLpLdL1−pL with prob (1− π)(1− pL)

.

Compare with acyclical job displacement risk process:

w2t =

{−d with prob ppd1−p with prob 1− p

Krebs (2007)

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 20 / 23

Cost of business cycles

detection error probability 50% 40%

Cost of business cycles 1.175% 2.083%= Baseline cost = 1.022 = 1.022+ Contribution of cyclical displacement risk +0.153 +0.153+ Contribution of fear of model misspecification +0 +0.615+ Joint contribution +0 +0.293

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 21 / 23

Cost of business cycles

detection error probability 50% 40%

Cost of business cycles 1.175% 2.083%= Baseline cost = 1.022 = 1.022+ Contribution of cyclical displacement risk +0.153 +0.153+ Contribution of fear of model misspecification +0 +0.615+ Joint contribution +0 +0.293

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 21 / 23

Worst case density

detection error probability 50% 40%

π 0.5 0.49970pH 0.03 0.03002pL 0.05 0.05953

E (w1t |displaced in expansion ) 0 −0.699× 10−3E (w1t |displaced in contraction ) 0 −0.743× 10−3E (w1t |¬displaced in expansion ) 0 −0.666× 10−3E (w1t |¬displaced in contraction ) 0 −0.664× 10−3

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 22 / 23

Worst case density

detection error probability 50% 40%

π 0.5 0.49970pH 0.03 0.03002pL 0.05 0.05953

E (w1t |displaced in expansion ) 0 −0.699× 10−3E (w1t |displaced in contraction ) 0 −0.743× 10−3E (w1t |¬displaced in expansion ) 0 −0.666× 10−3E (w1t |¬displaced in contraction ) 0 −0.664× 10−3

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 22 / 23

Conclusions

Welfare cost of business cycles higher than previously thought

Worst-case scenario has:

I Lower mean aggregate and idiosyncratic consumption growthI Greater variance in aggregate and idiosyncratic consumption growthI + correlation between aggregate and idiosyncratic consumption shocks

Stabilising business cycle should be an important priority

Next up - implications for market price of risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 23 / 23

Conclusions

Welfare cost of business cycles higher than previously thought

Worst-case scenario has:

I Lower mean aggregate and idiosyncratic consumption growthI Greater variance in aggregate and idiosyncratic consumption growthI + correlation between aggregate and idiosyncratic consumption shocks

Stabilising business cycle should be an important priority

Next up - implications for market price of risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 23 / 23

Conclusions

Welfare cost of business cycles higher than previously thought

Worst-case scenario has:

I Lower mean aggregate and idiosyncratic consumption growthI Greater variance in aggregate and idiosyncratic consumption growthI + correlation between aggregate and idiosyncratic consumption shocks

Stabilising business cycle should be an important priority

Next up - implications for market price of risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 23 / 23

Conclusions

Welfare cost of business cycles higher than previously thought

Worst-case scenario has:I Lower mean aggregate and idiosyncratic consumption growth

I Greater variance in aggregate and idiosyncratic consumption growthI + correlation between aggregate and idiosyncratic consumption shocks

Stabilising business cycle should be an important priority

Next up - implications for market price of risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 23 / 23

Conclusions

Welfare cost of business cycles higher than previously thought

Worst-case scenario has:I Lower mean aggregate and idiosyncratic consumption growthI Greater variance in aggregate and idiosyncratic consumption growth

I + correlation between aggregate and idiosyncratic consumption shocks

Stabilising business cycle should be an important priority

Next up - implications for market price of risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 23 / 23

Conclusions

Welfare cost of business cycles higher than previously thought

Worst-case scenario has:I Lower mean aggregate and idiosyncratic consumption growthI Greater variance in aggregate and idiosyncratic consumption growthI + correlation between aggregate and idiosyncratic consumption shocks

Stabilising business cycle should be an important priority

Next up - implications for market price of risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 23 / 23

Conclusions

Welfare cost of business cycles higher than previously thought

Worst-case scenario has:I Lower mean aggregate and idiosyncratic consumption growthI Greater variance in aggregate and idiosyncratic consumption growthI + correlation between aggregate and idiosyncratic consumption shocks

Stabilising business cycle should be an important priority

Next up - implications for market price of risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 23 / 23

Conclusions

Welfare cost of business cycles higher than previously thought

Worst-case scenario has:I Lower mean aggregate and idiosyncratic consumption growthI Greater variance in aggregate and idiosyncratic consumption growthI + correlation between aggregate and idiosyncratic consumption shocks

Stabilising business cycle should be an important priority

Next up - implications for market price of risk

Martin Ellison and Thomas J. Sargent ()Robustness and Consumption Risk 23 / 23

![Robust Model Predictive Control - Carnegie Mellon …cepac.cheme.cmu.edu/.../Ronust_Control_Classnotes.pdf1 Robust Model Predictive Control Formulations of robust control [1] The robust](https://static.fdocuments.us/doc/165x107/5aab45707f8b9a2b4c8bd345/robust-model-predictive-control-carnegie-mellon-cepacchemecmueduronustcontrol.jpg)