The U.S. Solar Energy Industry: Powering America Resch SEIA... · The U.S. Solar Energy Industry:...

24

Rhone Resch Solar Energy Industries Association President & CEO January 21 st , 2015 The U.S. Solar Energy Industry: Powering America

Transcript of The U.S. Solar Energy Industry: Powering America Resch SEIA... · The U.S. Solar Energy Industry:...

Rhone Resch

Solar Energy Industries Association

President & CEO

January 21st, 2015

The U.S. Solar Energy Industry:

Powering America

About SEIA

• Founded in 1974

• U.S. National Trade Association for Solar Energy

• 1,000 member companies from around the world

• Members from across 50 states

• Largest companies in the world as well as small

installers

• Our Mission: Build a strong solar industry to power

America

• Our Goal: 10 gigawatts (GW) of annual installed solar

capacity in the U.S. by 2015

January 26, 2015 © 2014 Solar Energy Industries Association® 2

Residential Solar Photovoltaic (PV)

• Typically rooftop installations on single or multi family

residential properties

• Capacity: 1-15 kW (average 6 kW)

– Sized to account for majority of yearly household electricity use (but not

more than)

• Normally grid-connected

– Uses net energy metering (NEM)

• Average cost: $3.60/watt

– Average system cost: $20,000

• Finance Options

– Third Party Ownership (Lease)

– Debt Financing through installer

– Self-financed

• 19% Market Share in 2014

January 26, 2015 © 2014 Solar Energy Industries Association® 3

Non-Residential Solar Photovoltaic

January 26, 2015 © 2014 Solar Energy Industries Association® 4

• Roof or ground-mounted installations on commercial,

industrial, government or non-profit properties

• Capacity: 1-5000+ kW (average 100 kW)

– Sizes vary widely depending on project objectives

• Normally grid-connected

– Uses net energy metering (NEM)

– Commercial entity is electricity off-taker

• Average cost: $2.27/watt

– Average system cost: ranges widely

• Finance Options

– Third Party Ownership (PPA)

– Debt Financing through installer

– Self-financed

• 17% Market Share in 2014

Utility-Scale Solar Photovoltaic

January 26, 2015 © 2014 Solar Energy Industries Association® 5

• Typically ground-mounted installations in a variety of open

spaces (desert, brownfield, grassland, other reclaimed land)

• Capacity: 1+ MW (average 12 MW)

– Can be as large as 500 MW

• Sells electricity on wholesale market

– Utility or Independent Power Producer-owned

– Utility is electricity off-taker

• Average cost: $1.71/watt

– Average system cost: ranges widely

• Finance Options

– Multi-party arrangements

– Debt, Equity, Tax Equity, Loan

Guarantee

• 64% Market Share in 2014

Concentrating Solar Power

January 26, 2015 © 2014 Solar Energy Industries Association® 6

• Generates electricity using heat from the sun

• Systems located in areas with exceptional solar resources

• Capacity: 75 MW+

– Experimental systems can be smaller

• Sells electricity on wholesale market

– Utility or Independent Power Producer-owned

– Utility is electricity off-taker

• 767 MW installed in 2014

– 1,685 MW installed cumulatively

• Finance Options

– Multi-party arrangements

– Debt, Equity, Tax Equity, Loan

Guarantee

Solar in America: Strong and Getting Stronger

January 26, 2015 © 2014 Solar Energy Industries Association® 7

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E

Yearl

y I

nsta

lled

So

lar

Cap

acit

y (

MW

)

Yearly U.S. Solar Installations

Residential (PV) Non-residential (PV) Utility (PV) Concentrating Solar Power (CSP)

Source: SEIA/GTM Research U.S. Solar Market Insight Q3 2014

greentechmedia.com/research/ussmi

Solar as an Economic Engine

• Nearly 174,000 American workers in solar – more than

double the number in 2009 – at 6,100 companies across

the country

January 26, 2015 © 2014 Solar Energy Industries Association® 8

Investment in Solar has increased 10x since 2006

January 26, 2015 © 2014 Solar Energy Industries Association® 9

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

2006 2007 2008 2009 2010 2011 2012 2013 2014E

Mil

lio

ns

Yearly U.S. Solar Investment Source: SEIA/GTM Research U.S. Solar Market Insight Q3 2014

greentechmedia.com/research/ussmi

Growth in Solar led by Falling Prices

January 26, 2015 © 2014 Solar Energy Industries Association® 10

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

$-

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014E

So

lar

PV

In

sta

lla

tio

ns

(M

Wd

c)

Ble

nd

ed

Ave

rag

e S

ola

r P

V P

ric

e (

$/w

att

)

Solar PV Installations Solar PV PricesSource: SEIA/GTM Research U.S. Solar Market Insight Q3 2014

greentechmedia.com/research/ussmi

Lawrence Berkeley National Laboratory, Tracking the Sun

Prices in all market segments near Sunshot Goals

January 26, 2015 © 2014 Solar Energy Industries Association® 11

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

2010 2011 2012 2013 2014

Insta

lled C

ost ($

/wa

tt)

Residential Commercial Utility

SunShot Goal: Residential SunShot Goal: Commercial SunShot Goal: Utility

Source: SEIA/GTM Research U.S. Solar Market Insight Q3 2014

greentechmedia.com/research/ussmi

Residential PV: Near Retail Rate Parity in Some States…

January 26, 2015 © 2014 Solar Energy Industries Association® 12

90% 77% 84% 78%

51% 37% 42%

28% 13%

10% 23% 16% 22%

49% 63% 58%

72% 87%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

% o

f R

esid

en

tial

Insta

lls

California Residential Installations

With State Incentives Without State Incentives

100% 100% 99% 99% 99% 86%

48% 34%

48%

0% 0% 10% 10% 10% 14%

52% 66%

52%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

% o

f R

esid

en

tial

Insta

lls

Arizona Residential Installations

With State Incentives Without State Incentives

Source: SEIA/GTM Research U.S. Solar Market Insight Q3 2014

greentechmedia.com/research/ussmi

…Still Work to do in Others

January 26, 2015 © 2014 Solar Energy Industries Association® 13

39% 41% 42% 38%

47% 50% 54% 55% 55% 55% 53%

45% 46% 46%

50%

43% 42% 35%

38% 38% 39% 40%

16% 13% 12% 12% 10% 8% 11% 7% 7% 6% 7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

Market Share of Residential Installations

California Remaining Top 10 States Rest of the U.S.

Source: SEIA/GTM Research U.S. Solar Market Insight Q3 2014

greentechmedia.com/research/ussmi

Third-Party Ownership plateaus, but with large market share

January 26, 2015 © 2014 Solar Energy Industries Association® 14

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q1-2011 Q2 2011 Q3 2011 Q4 2011 Q1 2012 Q2 2012 Q3 2012 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Q3 2014

Percentage of New Residential Installations Third-Party Owned

California Arizona Colorado Massachusetts New Jersey New York

Source: SEIA/GTM Research U.S. Solar Market Insight Q3 2014

greentechmedia.com/research/ussmi

Non-Residential Market: Crossing the Financing Gap

January 26, 2015 © 2014 Solar Energy Industries Association® 15

0

50

100

150

200

250

300

350

400

450

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Insta

lla

tio

ns

(M

Wd

c)

U.S. PV Installations by Market Segment, Q1 2010 – Q3 2014

Residential Non-Residential

Source: SEIA/GTM Research U.S. Solar Market Insight Q3 2014

greentechmedia.com/research/ussmi

Utility PV Market: Pipeline Replenishing

January 26, 2015 © 2014 Solar Energy Industries Association® 16

8,137 9,967

27,503

4,526

0

5,000

10,000

15,000

20,000

25,000

30,000

Operating Contracted (PPA Signed) Announced (Pre Contract

So

lar

PV

Ca

pa

cit

y (

MW

dc)

Utility PV Pipeline

In Construction

Source: SEIA/GTM Research U.S. Solar Market Insight Q3 2014

greentechmedia.com/research/ussmi

Concentrating Solar Power: Recent Surge

January 26, 2015 © 2014 Solar Energy Industries Association® 17

Source: SEIA/GTM Research U.S. Solar Market Insight Q3 2014

greentechmedia.com/research/ussmi

Another Strong Year Expected in 2015

• Over 8.5 GW of solar installations in 2015

– 8.4 GW Photovoltaics

– 112 MW Concentrating Solar Power

– 18% growth over last year (30% growth in PV market)

– A new installation every 2.5 minutes

• By years end, over 28 GW of solar in U.S.

– Nearing 1 million cumulative solar installations

– Enough solar in U.S. to power 5.5 million+ homes

– Displace CO2 equivalent to 8 coal power plants,

emissions from 6.3 million vehicles

January 26, 2015 © 2014 Solar Energy Industries Association® 18

Source: SEIA/GTM Research U.S. Solar Market Insight Q3 2014

greentechmedia.com/research/ussmi

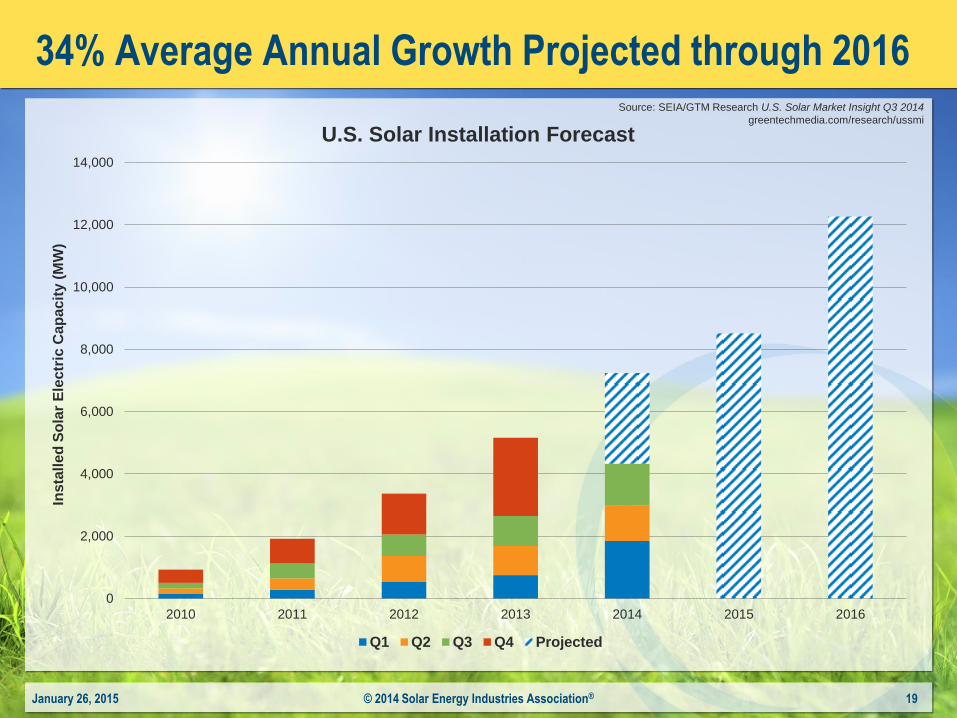

34% Average Annual Growth Projected through 2016

January 26, 2015 © 2014 Solar Energy Industries Association® 19

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

2010 2011 2012 2013 2014 2015 2016

Insta

lle

d S

ola

r E

lectr

ic C

ap

acit

y (

MW

)

U.S. Solar Installation Forecast

Q1 Q2 Q3 Q4 Projected

Source: SEIA/GTM Research U.S. Solar Market Insight Q3 2014

greentechmedia.com/research/ussmi

Continued Growth Across All Market Segments

January 26, 2015 © 2014 Solar Energy Industries Association® 20

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2010 2011 2012 2013 2014E 2015E 2016E

Insta

lle

d P

ho

tovo

lta

ic C

ap

acit

y (

MW

dc)

Installed PV Capacity by Market Segment

Residential Non-Residential Utility

Source: SEIA/GTM Research U.S. Solar Market Insight Q3 2014

greentechmedia.com/research/ussmi

36% of Electric Capacity Installed in 2014 through Q3 from Solar

January 26, 2015 © 2014 Solar Energy Industries Association® 21

10%

29% 36%

31%

46%

47%

16%

10% 0%

41%

7% 15%

4% 8%

2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 2013 Q1-Q3 2014

New U.S. Generating Capacity by Fuel Type

Solar Natural Gas Coal Wind Other

Source: SEIA/GTM Research U.S. Solar Market Insight Q3 2014

greentechmedia.com/research/ussmi

Solar Increasingly Important Part of Generation Mix

January 26, 2015 © 2014 Solar Energy Industries Association® 22

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2010 2011 2012 2013 2014E 2015E 2016E

Perc

en

tag

e o

f T

ota

l G

en

era

tio

n

Insta

lled

Cap

acit

y (

MW

)

Cumulative Solar Electric Installations Solar as % of Total Electric Generation

Source: SEIA/GTM Research U.S. Solar Market Insight Q3 2014

greentechmedia.com/research/ussmi

SEIA estimate from EIA data

SEIA Policy Priorities: Federal & Trade

• Investment Tax Credit

– Preserve and Extend at 30% Beyond 2016

– Modify to include Commence Construction

• Preserve MACRS

• Project Finance

– Increase tax equity pool through PWI authority and CRA

– Expand MLPs to include renewable energy

• Lead effort to resolve U.S.-China trade conflict

• Solar codes and safety standards

• EPA 111d

January 26, 2015 © 2013 Solar Energy Industries Association® 23

SEIA Policy Priorities: State

• Renewable Portfolio Standards

– Defend and Expand; advocate for SHC

• NEM, rate design and incentives in key states:

– CA, AZ, CO, NY, NV, MA, NJ & mid-Atlantic, TX, GA &

southeast

• Expand policies to support DG

• Grid Integration

– Outreach & education to key policymakers

– Research and address key issues

January 26, 2015 © 2013 Solar Energy Industries Association® 24