THE URGENCY WITH REVENUE RECOGNITION

9

Transcript of THE URGENCY WITH REVENUE RECOGNITION

THE URGENCY WITH REVENUE RECOGNITION

COPYRIGHT 2017 © TECHVENTIVE, INC. 2

UNAUTHORIZED REPRODUCTION, TRANSMISSION, STORAGE OR DISTRIBUTION PROHIBITED

Executive Summary

Compliance matters, like taxes, aren’t optional. You can’t defer their implementation like it’s some sort of budget line item (“Maybe we’ll get it done next year!”). You’re either in compliance or your not – it’s binary. The new revenue recognition rules aren’t just required - the due date is looming fast! For public companies, new revenue recognition rules must be implemented on January 1, 2018 (private firms must comply one year later). Unfortunately, meeting that deadline may not be a simple or easy matter for many companies. For companies that must comply with the new rules, the timeline may present significant challenges as:

- The amount of preliminary work to be compliant could be substantial - Material process changes may be required (or desired) in areas like commission payments,

mid-term contract adjustments, bundling of products, services and/or warranties into a single contract

- New or updated technology may be required - Stopgap solutions (e.g., spreadsheets) may be labor intensive, error-prone or ineffective - Businesses may not be able to locate (or locate in a timely fashion) critical source documents

(e.g., original sales contracts) What should businesses do? At a minimum, organizations should:

- Become acutely aware of the new accounting rules - Collect all of the relevant contracts, documents, etc. - Start testing the impact of the new rules on one or more business units within the

organization - Educate the executive team as to the potential impact to existing contracting, commission,

sales and other practices - Acquire new/updated revenue management technology - Line up expert resources to implement new technologies - Categorize contracts/deals into common types - Perform what-if scenario tests - Convert data - Inform shareholders as to pre-/post-rules change impact on earnings - Assess the need for new systems or updates when standalone spreadsheets no longer meet

internal control requirements, data volumes and audit needs

Failure to meet these new requirements could be difficult for financial executives whether or not they are with public or private firms. Executives at public companies may not want to sign off on non-compliant financials for fear of triggering a Sarbanes-Oxley violation. Private firms could meet resistance with banks and others if their financial reports are non-compliant. Is your financial accounting group up to the challenge?

THE URGENCY WITH REVENUE RECOGNITION

COPYRIGHT 2017 © TECHVENTIVE, INC. 3

UNAUTHORIZED REPRODUCTION, TRANSMISSION, STORAGE OR DISTRIBUTION PROHIBITED

Who is Impacted?

New revenue recognition rules go into effect on January 1, 2018 for public companies and January 1, 2019 for private firms. The new requirements can be found in the Accounting Standards Codification 606 (it supersedes ASC 605) and IFRS 15. While many companies will be affected, some firms will be heavily impacted. Those include firms that:

- Sell on a subscription or other time-based method - Create contracts with combinations of services, products and/or warranties - Permit mid-contract adjustments, additions or other changes - Allow customers to return products for refunds - Allow customers to make periodic payments over the life of the contract - Pay sales professionals commissions that may be earned over the life of the contract - Require deposits/advances - Offer long-term warranties - Deliver goods and/or services over a time period (not just at contract signing) - Offer buyback provisions in their contracts

Companies in the professional services industry, cable television/telephony industry, application software and other verticals may be impacted. Even traditional manufacturers who are offering ‘as-a-service’ capabilities will likely face new accounting rules.

The Timeline

The timeline to meet the new revenue recognition rules will be an aggressive one for many firms. Some firms will experience significant time compression to meet these deadlines. Those firms most adversely affected may be organizations with:

- Old financial software - No prior revenue management software - Multi-element arrangements contracts - Geographically dispersed operations - Broad and/or diverse product line - Complex sales - Complex contracts - Little commonality across deals, products and/or solutions - Numerous contracts and contract lines - Little or no electronic documentation re: deals - Multi-year contracts - Complex commission structures - Commission structures/plans that change frequently

Broadly speaking, the amount of time and effort required to meet the new compliance deadlines is broken up into several areas:

THE URGENCY WITH REVENUE RECOGNITION

COPYRIGHT 2017 © TECHVENTIVE, INC. 4

UNAUTHORIZED REPRODUCTION, TRANSMISSION, STORAGE OR DISTRIBUTION PROHIBITED

- Education (about the new rules and application of same) - Assessment (of effect of new rules on several operational matters, accounting policies,

contracts, financial statements, etc.) - Processing (of old and new contracts) - Acquisition (of necessary software)

Businesses may want to develop a detailed work plan to help them understand the level of effort and dependencies involved in implementing a functional solution by the January 1, 2018 deadline. Working backwards from the due date may actually help in the development of a viable plan. Getting the rules right will be important to those tasked with getting their firm compliant. Firms may want to review their understanding of the new rules with their external auditor and check-in with that auditor at major checkpoints along the way. This is especially important for firms that will be sharing financial results pre- and post- rules changes with affected stakeholders.

THE URGENCY WITH REVENUE RECOGNITION

COPYRIGHT 2017 © TECHVENTIVE, INC. 5

UNAUTHORIZED REPRODUCTION, TRANSMISSION, STORAGE OR DISTRIBUTION PROHIBITED

The timeline may actually be more acute for those firms with long-lived and/or complex contracts. According to accounting firm PriceWaterhouseCoopers:

“For companies choosing the retrospective option for adopting the new standard, the transition period has already begun. Companies are finding that circumstances such as tiered pricing, marketing offers (including volume discounts), contract modifications and a host of other potential contract terms are creating issues that require careful consideration under the new standards.”

1

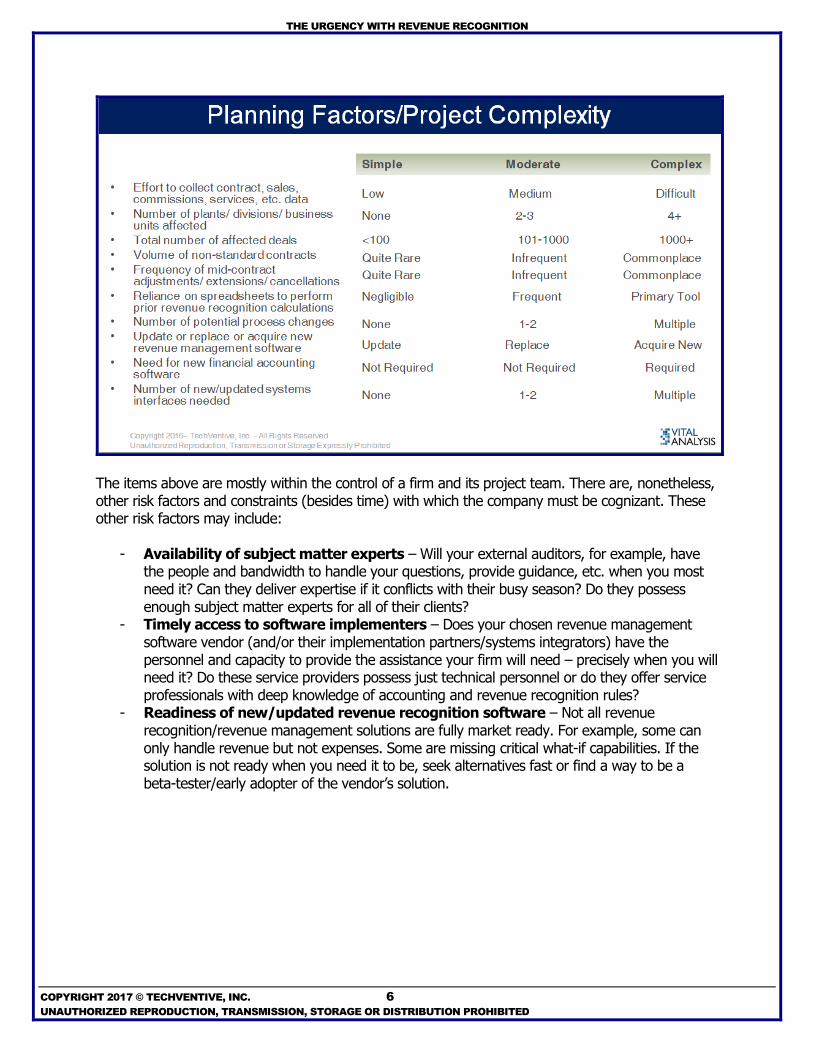

Planning Factors

How big an effort will your firm face in meeting new revenue recognition requirements? The following exhibit identifies a number of planning factors. These factors help project planners assess the enormity of the effort, the scope of the project and more. Firms just starting a revenue recognition compliance effort may find it difficult to plan such an exercise until they have acquired a sufficient education in the new rules and performed a minimal assessment of the new rules on, at least, a portion of the firm’s business. At that point, a better picture of the total project effort should become apparent.

1 Source: http://www.pwc.com/us/en/audit-assurance-services/accounting-advisory/revenue-recognition.html?WT.mc_id=CT3-PL300-DM1-

TR1-LS3-ND30-BPA30-CN_RevenueRecognition-2016-Search&eq=RevRecPaidSearch&gclid=CLW9ocyb088CFQKoaQodvUIBPw

THE URGENCY WITH REVENUE RECOGNITION

COPYRIGHT 2017 © TECHVENTIVE, INC. 6

UNAUTHORIZED REPRODUCTION, TRANSMISSION, STORAGE OR DISTRIBUTION PROHIBITED

The items above are mostly within the control of a firm and its project team. There are, nonetheless, other risk factors and constraints (besides time) with which the company must be cognizant. These other risk factors may include:

- Availability of subject matter experts – Will your external auditors, for example, have the people and bandwidth to handle your questions, provide guidance, etc. when you most need it? Can they deliver expertise if it conflicts with their busy season? Do they possess enough subject matter experts for all of their clients?

- Timely access to software implementers – Does your chosen revenue management software vendor (and/or their implementation partners/systems integrators) have the personnel and capacity to provide the assistance your firm will need – precisely when you will need it? Do these service providers possess just technical personnel or do they offer service professionals with deep knowledge of accounting and revenue recognition rules?

- Readiness of new/updated revenue recognition software – Not all revenue recognition/revenue management solutions are fully market ready. For example, some can only handle revenue but not expenses. Some are missing critical what-if capabilities. If the solution is not ready when you need it to be, seek alternatives fast or find a way to be a beta-tester/early adopter of the vendor’s solution.

THE URGENCY WITH REVENUE RECOGNITION

COPYRIGHT 2017 © TECHVENTIVE, INC. 7

UNAUTHORIZED REPRODUCTION, TRANSMISSION, STORAGE OR DISTRIBUTION PROHIBITED

Time for Data The data required to perform the revenue recognition calculations/allocations will likely come from a variety of sources and require a material amount of analysis. Businesses must allocate time to both collect and analyze this data. For some firms, just collecting this information could be a struggle as contracts may have originated in one legal entity or country with the delivery of the products and services occurring across multiple geographic areas over several different accounting periods. Where these specific order or contract documents exist could be anyone’s guess. Other complications can occur when:

- Contracts (e.g., master agreements) were crafted years or decades ago. Locating the source documents could be difficult.

- Contracts were frequently amended mid-term. The documentation for these mid-term adjustments may be in simple documents (e.g., emails), change orders, contract amendments, etc. Can all of these documents be located? Are all documents clear on the financial (and revenue recognition) implications of the adjustments?

- Sales commissions are calculated via spreadsheets not a formal sales tracking/management solution.

- Services information (e.g., work orders, change orders, time extensions, etc.) is stored in a separate system and may have deviated materially from the original contract specification.

- Product returns and credits are stored in a separate system. - Orders/contracts vary significantly in form and content across the firm’s numerous

divisions/business units.

Project teams should expect to pull together data from numerous systems (manual and automated) including:

- Project Billing - Order Management - Contract Accounting - Contract Documentation - Sales Order Fulfillment - Billing systems - Service and Subscription Management

Pulling together these views of contracts/orders may take time: Time that is quickly running out.

THE URGENCY WITH REVENUE RECOGNITION

COPYRIGHT 2017 © TECHVENTIVE, INC. 8

UNAUTHORIZED REPRODUCTION, TRANSMISSION, STORAGE OR DISTRIBUTION PROHIBITED

Summary

The deadline for complying with the new revenue recognition requirements is mandatory and is closing in on businesses fast! While many good-meaning corporate accounting leaders know of the new requirements and may have some idea of the changes required in their firm, they may have materially underestimated all of the effort, time and resources that will actually be required to become compliant on time. These executives may be in for an unpleasant surprise when future period closings are delayed or must be restated once the new requirements are fully implemented. Some of the challenges these accounting leaders may have to face could include:

- Inability to source the required data - Shortages of key subject matter experts - Time spent sourcing and implementing new revenue management software - Time lost negotiating changes to current commission practices, order change practices, etc. - Time spent building different what-if scenarios and getting approval for chosen allocation

approaches Shareholders will likely expect communications from finance leaders as to the bottom line impact of these new rules. Accurate guidance on this can only be given once finance leaders have the data, tools and processes to enable accurate processing of these transactions in a timely fashion. Will your firm be ready in time?

THE URGENCY WITH REVENUE RECOGNITION

COPYRIGHT 2017 © TECHVENTIVE, INC. 9

UNAUTHORIZED REPRODUCTION, TRANSMISSION, STORAGE OR DISTRIBUTION PROHIBITED

About Vital Analysis

Vital Analysis is a very different kind of technology research organization. We are the intersection set where exceptional technology market knowledge meets the executive suite. Where other ‘analysts’ replay vendor

press releases, we give you the:

Impact new technologies will have on your business.

Reasons why you should care about specific emerging solutions.

Business justifications why you may want specific solutions.

Vital Analysis was carved out of TechVentive, Inc. in 2007 as a new, but related, business. As designed, Vital Analysis is the publishing, research and analytical arm of that company.

Our reach, like our blog readership, is truly global. We’ve consulted with top technology executives across the globe and have been briefed by technology providers from virtually every corner of the planet.

About the Author Brian Sommer is the CEO of TechVentive, Inc. - a market-strategy and content firm. Brian closely follows what

C-level executives think, feel and need. Brian has won several ERP Writers Awards and many of his pieces can be found at www.diginomica.com and http://blogs.zdnet.com/sommer/). He welcomes your thoughts and

invites you to contact him at [email protected] .

Reproduction of any part of this publication in any form without prior written approval is forbidden. The information in this report has been obtained from sources believed to be reliable. TechVentive, Inc. disclaims all warranties as to the accuracy, completeness, or adequacy of such information and shall have no liability for errors, omissions, or inadequacies in the information contained herein or for interpretations thereof. The reader assumes sole responsibility for the selection of these materials to achieve its intended result. The opinions expressed herein are subject to change without notice. To purchase reprints of this document or to quote passages within, please email: [email protected]