The Unholy Trinity of Financial Contagion - Homepages at WMU

24

The Unholy Trinity of Financial Contagion Graciela L. Kaminsky, Carmen M. Reinhart and Carlos A. Ve ´gh F or reasons that are not always evident at the time, some nancial events, like the devaluation of a currency or an announcement of default on sovereign debt obligations, trigger an immediate and startling adverse chain reaction among countries within a region and in some cases across regions. This phenom- enon, which we dub “fast and furious” contagion, was manifest after the oatation of the Thai baht on July 2, 1997, as it quickly triggered nancial turmoil across east Asia. Indonesia, Korea, Malaysia and the Philippines were hit the hardest—by December 1997, their currencies had depreciated (on average) by about 75 per- cent. Similarly, when Russia defaulted on its sovereign bonds on August 18, 1998, the effects were felt not only in several of the former Soviet republics, but also in Hong Kong, Brazil, Mexico, many other emerging markets and the riskier segments of developed markets. 1 The economic impact of these shocks on the countries unfortunate enough to be affected included declines in equity prices, spikes in the cost of borrowing, scarcity in the availability of international capital, declines in the value of their currencies and falls in economic output. 1 The international nancial turmoil that followed Russia’s default was compounded in a signi cant manner by another negative surprise announcement: on September 2, 1998, it became public knowl- edge that the prominent hedge fund Long Term Capital Management (LTCM) had gone bankrupt owing to its large exposure to Russia and other high-yield, high-risk assets. y Graciela L. Kaminsky is Professor of Economics, George Washington University, Washing- ton, D.C. Carmen M. Reinhart is Professor of Economics at University of Maryland, College Park, Maryland. Carlos A. Ve ´gh is Professor of Economics, University of California, Los Angeles, California. All three authors are Research Associates, National Bureau of Economic Research, Cambridge, Massachusetts. Their e-mail addresses are ^[email protected]&, ^[email protected]& and ^[email protected]&, respectively. Journal of Economic Perspectives—Volume 17, Number 4—Fall 2003—Pages 51–74

Transcript of The Unholy Trinity of Financial Contagion - Homepages at WMU

The Unholy Trinity of FinancialContagion

Graciela L Kaminsky Carmen M Reinhartand Carlos A Vegh

F or reasons that are not always evident at the time some nancial events likethe devaluation of a currency or an announcement of default on sovereigndebt obligations trigger an immediate and startling adverse chain reaction

among countries within a region and in some cases across regions This phenom-enon which we dub ldquofast and furiousrdquo contagion was manifest after the oatationof the Thai baht on July 2 1997 as it quickly triggered nancial turmoil across eastAsia Indonesia Korea Malaysia and the Philippines were hit the hardestmdashbyDecember 1997 their currencies had depreciated (on average) by about 75 per-cent Similarly when Russia defaulted on its sovereign bonds on August 18 1998the effects were felt not only in several of the former Soviet republics but also inHong Kong Brazil Mexico many other emerging markets and the riskier segmentsof developed markets1 The economic impact of these shocks on the countriesunfortunate enough to be affected included declines in equity prices spikes in thecost of borrowing scarcity in the availability of international capital declines in thevalue of their currencies and falls in economic output

1 The international nancial turmoil that followed Russiarsquos default was compounded in a signi cantmanner by another negative surprise announcement on September 2 1998 it became public knowl-edge that the prominent hedge fund Long Term Capital Management (LTCM) had gone bankruptowing to its large exposure to Russia and other high-yield high-risk assets

y Graciela L Kaminsky is Professor of Economics George Washington University Washing-ton DC Carmen M Reinhart is Professor of Economics at University of Maryland CollegePark Maryland Carlos A Vegh is Professor of Economics University of California LosAngeles California All three authors are Research Associates National Bureau of EconomicResearch Cambridge Massachusetts Their e-mail addresses are ^gracielagwueduamp^creinharumdeduamp and ^cveghuclaeduamp respectively

Journal of Economic PerspectivesmdashVolume 17 Number 4mdashFall 2003mdashPages 51ndash74

Table 1 presents summary material for recent contagion episodes The rstcolumn lists the country the date that marks the beginning of the episode thenature of the shock and currency market developments in the crisis country Theremaining columns include information on the existence and nature of commonexternal shocks the suspected main mechanism for propagation across nationalborders and the countries that were most affected

The challenge for economic researchers is to explain why the number of nancial crises that did not have signi cant international consequences is fargreater than those that did It is no surprise that a domestic crisis (no matter howdeep) in countries that are approximately autarkic (either voluntarily or otherwise)will not likely have immediate repercussions in world capital markets The countriesmay be large (like China or India) or comparatively small (like Bolivia or Guinea-Bissau) More intriguing cases of ldquocontagion that never happenedrdquo are thosewhere the crisis country is relatively large (at least by emerging market standards)and is reasonably well integrated to the rest of the world through trade or nanceAlong with the fast and furious contagion episodes these cases are the focus of thispaper

Some recent nancial crises with limited immediate consequences includethese examples Brazilrsquos devaluation of the real on January 13 1999 andeventual otation on February 1 1999 the Argentine default and abandon-ment of the Convertibility Plan in December 2001 and Turkeyrsquos devaluation ofthe lira on February 22 2001 Given that Brazil Turkey and Argentina arerelatively large emerging markets these episodes could have beenmdashat leastpotentiallymdashas highly ldquocontagiousrdquo as the Thai and Russian crises Nonetheless nancial markets shrugged off these events despite the fact that it was evidentat the time that some of these shocks would have trade and real sector reper-cussions on neighboring countries over the medium term For example be-cause Brazil is Argentinarsquos largest trading partner the sharp depreciation of thereal (about 70 percent between January and the end of February) clearly left theArgentine peso overvalued Table 2 presents some summary material for theseepisodes in a format parallel to Table 1

This paper seeks to address the central question of why nancial contagionacross borders occurs in some cases but not others2 Throughout the paper westress that there are three key elements that distinguish the cases where contagion

2 Of course there are historical examples of fast and furious contagion before the last few decadesCommonly cited examples of contagion include the rst Latin American debt crisismdashwhich began withPerursquos default in April 1826 mdashand the international nancial crisis of 1873 Going back even further intime Neal and Weidenmeir (2002) also discuss the ldquocontagionrdquo dimension of the Tulip Mania of the1630s and the Mississippi and South Sea Bubbles of 1719ndash1720 Two leading examples of nancial crisesthat did not lead to contagion include the well-documented Argentina-Baring crisis of 1890 and theUnited States nancial crisis of 1907 For detailed accounts of historical episodes of nancial crises seeBordo and Eichengreen (1999) Bordo and Murshid (2000) Kindleberger (1997) and Neal andWeidenmier (2002)

52 Journal of Economic Perspectives

Table 1Financial Crises with Immediate International Repercussions 1980ndash2000

Origin of the shock countryand date

Nature of common externalshock if any Contagion mechanisms Countries affected

On August 12 1982Mexico defaults on itsexternal bank debt ByDecember the pesohad depreciated by100 percent

Between 1980 and 1985commodity prices fellby about 31 percentUS short-term realinterest rates rise toabout 7 percent thehighest levels sincethe depression

US banks heavilyexposed to Mexicoretrenched fromemerging markets

With the exception ofChile Colombia andCosta Rica allcountries in LatinAmerica defaulted

On September 8 1992the Finnish markka is oated and theExchange RateMechanism (ERM)crisis unfolds

High interest rates inGermany Rejectionby Danish voters ofthe Maastricht treaty

Hedge funds All the countries in theEuropean MonetarySystem exceptGermany

On December 20 1994Mexico announced a15 percent devaluationof the peso It sparkeda con dence crisisand by March 1995the pesorsquos value haddeclined by about100 percent

From January 1994 toDecember theFederal Reserve raisedthe federal funds rateby about 25percentage points

Mutual funds sell offother Latin Americancountries notablyArgentina and BrazilMassive bank runsand capital ight inArgentina

Argentina suffered themost losing about20 percent ofdeposits in early1995 Brazil wasnext while losses inother countries inthe region limited todeclines in equityprices

On July 2 1997Thailand announcesthat the baht will beallowed to oat ByJanuary 1998 the bahthad depreciated byabout 113 percent

The yen depreciated byabout 51 percentagainst the US dollarduring April 1995 andApril 1997 Given theAsian currencies linkto the US dollar thistranslated into asigni cantappreciation for theircurrencies as well

Japanese banksexposed to Thailandretrenched fromemerging Asia AsKorea is affectedEuropean banks alsowithdraw

Indonesia KoreaMalaysia and thePhilippines were hithardest Financialmarkets in Singaporeand Hong Kong alsoexperienced someturbulence

On August 18 1998Russia defaults on itsdomestic bond debtBetween July 1998 andJanuary 1999 theruble depreciated by262 percent OnSeptember 2 1998 itbecame publicknowledge that LTCMhad gone bankrupt

With heavy exposure toRussia and otherhigh-yieldinstruments LTCM isrevealed to bebankrupt

Margin calls andleveraged hedgefunds fueled the selloff in other emergingand high yieldmarkets It is dif cultto distinguishcontagion fromRussia and fear ofanother LTCM

Apart from several ofthe former Sovietrepublics HongKong Brazil andMexico were hithardest But mostemerging anddeveloped marketswere affected

Sources International Monetary Fund International Financial Statistics dates of the default or restruc-turings are taken from Reinhart Rogoff and Savasteno (2003)

Graciela L Kaminsky Carmen M Reinhart and Carlos A Vegh 53

occurs from those where it does not We call them the ldquounholy trinityrdquo an abruptreversal in capital in ows surprise announcements and a leveraged commoncreditor First contagion usually followed on the heels of a surge in in ows ofinternational capital and more often than not the initial shock or announcementpricked the capital ow bubble at least temporarily The capacity for a swift and

Table 2Selected Financial Crises without Immediate International Repercussions1999ndash2001

Origin of the shockcountry and date

Background on therun-up to the shock Spillover mechanisms Countries affected

On January 131999 Brazildevalues the realand eventually oats on February1 Between earlyJanuary and end-February the realdepreciates by70 percent

The crawling pegexchange ratepolicy (the RealPlan) that wasadopted in July1994 to stabilizein ation isabandoned

There is an increasein volatility insome of largerequity marketsand Argentinaspreads widenedEquity markets inArgentina andChile ralliedThese effectslasted only a fewdays

Signi cant and protractedeffect on Argentina asBrazil is Argentinarsquoslargest trading partner

On February 222001 Turkeydevalues and oats the lira

Facing substantialexternal nancingneeds in lateNovember 2000rumors of thewithdrawal ofexternal credit linesto Turkish bankstriggered a foreignexchange out owsand overnight ratessoared to close to2000 percent

There has been someconjecture that theTurkish crisis may haveexacerbated thewithdrawal of investorsfrom Argentina butgiven the weakness inArgentinarsquosfundamentals at thetime it is dif cult tosuggest developmentsowed to contagion

On December 232001 thepresident ofArgentinaannouncesintentions todefault

Following severalwaves of capital ight and runs onbank deposits onDecember 1st

capital controls areintroduced

Bank deposits fallby more than30 percent inUruguay asArgentineswithdraw depositsfrom Uruguayanbanks Signi canteffects oneconomic (tradeand tourism)activity inUruguay

Uruguay and to a muchlesser extent Brazil

54 Journal of Economic Perspectives

drastic reversal of capital owsmdashthe so-called ldquosudden stoprdquo problemmdashplayed asigni cant role3 Second the announcements that set off the chain reactions cameas a surprise to nancial markets The distinction between anticipated and unantic-ipated events appears critical as forewarning allows investors to adjust their port-folios in anticipation of the event Third in all cases where there were signi -cant immediate international repercussions a leveraged common creditor wasinvolvedmdashbe it commercial banks hedge funds mutual funds or bondholdersmdashwho helped to propagate the contagion across national borders

Before turning to the question of what elements distinguish the cases wherecontagion occurs from those where it does not however we provide a brief tour ofthe main theoretical explanations for contagion and the most salient empirical ndings on the channels of propagation

What is Contagion

Since the term ldquocontagionrdquo has been used liberally and has taken on multiplemeanings it is useful to clarify what it will mean in this paper We refer to contagionas an episode in which there are signi cant immediate effects in a number ofcountries following an eventmdashthat is when the consequences are fast and furiousand evolve over a matter of hours or days This ldquofast and furiousrdquo reaction is acontrast to cases in which the initial international reaction to the news is mutedThe latter cases do not preclude the emergence of gradual and protracted effectsthat may cumulatively have major economic consequences We refer to thesegradual cases as spillovers Common external shocks such as changes in interna-tional interest rates or oil prices are also not automatically included in our workingde nition of contagion Only if there is ldquoexcess comovementrdquo in nancial andeconomic variables across countries in response to a common shock do we considerit contagion

Theories of Contagion

Through what channels does a nancial crisis in one country spread acrossinternational borders Some models have emphasized investor behavior that givesrise to the possibility of herding and fads It is no doubt possible (if not appealingto many economists) that such ldquoirrational exuberancerdquo to quote Federal ReserveChairman Alan Greenspan can in uence the behavior of capital ows and nan-cial markets and exacerbate the booms as well as the busts Other models stresseconomic linkages through trade or nance This section provides a selective

3 See Calvo and Reinhart (2000) for an empirical analysis of sudden stop episodes and Caballero andKrishnamurthy (2003) for a model that traces out the economic consequences of sudden stops

The Unholy Trinity of Financial Contagion 55

discussion of theories of contagion The main message conveyed here is that nancial linkagesmdash cross-border capital ows and common creditorsmdashand investorbehavior gure the most prominently in the theoretical explanations of contagion

HerdingBikhchandani Hirshleifer and Welch (1992) model the fragility of mass

behavior as a consequence of informational cascades4 An information cascadeoccurs when it is optimal for an individual after observing the actions of thoseahead of him to follow the behavior of the preceding individual without regard tothe individualrsquos own information Under relatively mild conditions cascades willalmost surely start and often they will be wrong In those circumstances a few earlyindividuals can have a disproportionate effect Changes in the underlying value ofalternative decisions can lead to ldquofadsrdquomdashthat is drastic and seemingly whimsicalswings in mass behavior without obvious external stimulus

Banerjee (1992) also develops a model to examine the implications of deci-sions that are in uenced by what others are doing The decisions of others mayre ect potentially important information in their possession that is not in thepublic domain With sequential decision making people paying attention to whatothers are doing before them end up doing what everyone else is doing (that isherding behavior) even when onersquos own private information suggests doing some-thing different The herd externality is of the positive feedback type If we join thecrowd we induce others to do the same The signals perceived by the rst fewdecision makersmdashrandom and not necessarily correctmdash determine where the rstcrowd forms and from then on everybody joins the crowd This characteristic ofthe model captures to some extent the phenomena of ldquoexcess volatilityrdquo in assetmarkets or the frequent and unpredictable changes in fashions

Another story suggests that the channels of transmission arise from the globaldiversi cation of nancial portfolios in the presence of information asymmetriesCalvo and Mendoza (2000) for instance present a model where the xed costs ofgathering and processing country-speci c information give rise to herding behav-ior even when investors are rational Because of information costs equilibria arisein which the marginal cost exceeds the marginal gain of gathering information Insuch instances it is rational for investors to mimic market portfolios When a rumorfavors a different portfolio all investors ldquofollow the herdrdquo

Trade LinkagesSome recent models have revived Nurksersquos (1944) classic story of competitive

devaluations (Gerlach and Smets 1996) Nurkse argued that since a devaluation inone country makes its goods cheaper internationally it will pressure other coun-tries that have lost competitiveness to devalue as well In this setting a devaluation

4 See Bikhchandani Hirshleifer and Welch (1998) in this journal for a thoughtful discussion of thisliterature

56 Journal of Economic Perspectives

in a second country is a policy decision whose effect on output is expected to besalutary as it reduces imports increases exports and improves the current accountAn empirical implication of this type of model is that we should observe a highvolume of trade among the ldquosynchronizedrdquo devaluers As a story of voluntarycontagion this explanation does not square with the fact that central banks oftengo to great lengths to avoid a devaluation in the rst placemdash often by engaging inan active interest rate defense of the existing exchange rate (as in Lahiri and Vegh2003) or by enduring massive losses of foreign exchange reservesmdashnor that deval-uations have often been contractionary

Financial LinkagesOther studies have emphasized the important role of common creditors and

nancial linkages in contagion The ldquotyperdquo of the common creditor may differacross models but the story tends to remain consistent

In Shleifer and Vishny (1997) arbitrage is conducted by relatively few special-ized and leveraged investors who combine their knowledge with resources thatcome from outside investors to take large positions Funds under managementbecome responsive to past performance The authors call this Performance BasedArbitrage In extreme circumstances when prices are signi cantly out of line andarbitrageurs are fully invested Performance Based Arbitrage is particularly ineffec-tive In these instances arbitrageurs might bail out of the market when theirparticipation is most needed That is arbitrageurs face fund withdrawals and arenot very effective in betting against the mispricing Risk-averse arbitrageurs mightchose to liquidate even when they do not have to for fear that a possible furtheradverse price movement may cause a drastic out ow of funds later on While themodel is not explicitly focused on contagion one could see how an adverse shockthat lowers returns (say like the Mexican peso crisis) may lead arbitrageurs toliquidate their positions in other countries that are part of their portfolio (likeArgentina and Brazil) as they fear future withdrawals

Similarly Calvo (1998) has stressed the role of liquidity A leveraged investorfacing margin calls needs to sell asset holdings Because of the information asym-metries a ldquolemons problemrdquo arises and the asset can only be sold at a low re-saleprice For this reason the strategy will not be to sell the asset whose price hasalready collapsed but other assets in the portfolio In doing so however other assetprices fall and the original disturbance spreads across markets

Kodres and Pritsker (2002) develop a rational expectations model of assetprices to explain nancial market contagion In their model assetsrsquo long-run valuesare determined by macroeconomic risk factors which are shared across countriesand by country-speci c factors Contagion occurs when ldquoinformedrdquo investors re-spond to private information on a country-speci c factor by optimally rebalancingtheir portfoliorsquos exposures to the shared macroeconomic risk factors in othercountriesrsquo markets When there is asymmetric information in the countries hit bythe rebalancing ldquouninformedrdquo investors cannot fully identify the source of the

Graciela L Kaminsky Carmen M Reinhart and Carlos A Vegh 57

change in asset demand they therefore respond as if the rebalancing is related toinformation on their own country (even though it is not) As a result an idiosyn-cratic shock generates excess comovementmdash contagionmdashacross countriesrsquo assetmarkets A key insight from the model is that contagion can occur between twocountries even when contagion via correlated information shocks correlated li-quidity shocks and via wealth effects are ruled out by assumption and even when thecountries do not share common macroeconomic factors provided that both coun-tries share at least one underlying macroeconomic risk factor with a third countrythrough which portfolio rebalancing can take place Their model like the rationalherding model of Calvo and Mendoza (1998) has the empirical implication thatcountries with more internationally traded nancial assets and more liquid marketsshould be more vulnerable to contagion Small highly illiquid markets are likely tobe underrepresented in international portfolios to begin with and as suchshielded from this type of contagion

Kaminsky and Reinhart (2000) focus on the role of commercial banks inspreading the initial shock The behavior of foreign banks can exacerbate theoriginal crisis by calling loans and drying up credit lines but can also propagatecrises by calling loans elsewhere The need to rebalance the overall risk of thebankrsquos asset portfolio and to recapitalize following the initial losses can lead to amarked reversal in commercial bank credit across markets where the bank hasexposure

Other ExplanationsThe so-called ldquowake-up call hypothesisrdquo (a term coined by Morris Goldstein

1998) relies on either investor irrationality or a xed cost in acquiring informationabout emerging markets In this story once investors ldquowake uprdquo to the weaknessesthat were revealed in the crisis country they will proceed to avoid and move out ofcountries that share some characteristics with the crisis country So for instance ifthe original crisis country had a large current account de cit and a relatively ldquorigidrdquoexchange rate then other countries showing similar features will be vulnerable tosimilar pressures (Basu 1998 offers a formal model)

Channels of Propagation The Empirical Evidence

Some of the theoretical models just discussed emphasized trade linkages asa channel for the cross-border propagation of shocks but most models havelooked to nancial markets for an explanation However perhaps because tradein goods and services has a longer history in the postndashWorld War II period thantrade in nancial assets or because of far better data availability trade linkshave received the most attention in the empirical literature on channels ofcontagion Eichengreen Rose and Wyplosz (1996) nd evidence that tradelinks help explain the pattern of contagion in 20 industrial countries over

58 Journal of Economic Perspectives

1959 ndash1993 Glick and Rose (1999) who examine this issue for a sample of161 countries come to the same conclusion Glick and Rose (1999) andKaminsky and Reinhart (2000) also study trade linkages that involve competi-tion in a common third market

While sharing a third party is a necessary condition for the competitivedevaluation story Kaminsky and Reinhart (2000) argue it is clearly not a sufcientone If a country that exports wool to the United States devalues it is not obviouswhy this step would have any detrimental effect on a country that exports semicon-ductors to the United States Their study shows that trade links through a thirdparty is a plausible transmission channel in some cases but not for the majority ofcountries recently battered by contagion For example at the time of the Asiancrisis Thailand exported many of the same goods to the same third parties asMalaysia This connection however does not explain all the other Asian crisiscountries Bilateral or third-party trade also does not appear to carry any weight inexplaining the effects of Mexico (1994) on Argentina and Brazil At the time ofMexicorsquos 1994 devaluation only about 2 percent of Argentinarsquos and Brazilrsquos totalexports went to Mexico Similarly Brazil hardly trades with Russia as only02 percent of its exports are destined for Russian markets yet in the weeksfollowing the Russian default Brazilrsquos interest rate spreads doubled and its equityprices fell by more than 20 percent

Kaminsky and Reinhart (2000) compare countries clustered along the lines oftrade links versus countries with common bank creditors and conclude that com-mon nancial linkages better explain the observed pattern of contagion Mody andTaylor (2002) who seek to explain the comovement in an exchange marketpressures index by bilateral and third-party trade and other factors also cast doubton the importance of trade linkages in explaining the propagation of shocks

Conversely many cases of crises without contagion have strong trade linksAbout 30 percent of Argentinarsquos exports are destined for Brazil yet in the weekfollowing Brazilrsquos devaluation the Argentine equity market increased 12 percentSimilarly nearly 13 percent of Uruguayrsquos exports are bound for the Argentinemarket Yet the main reason why the crisis in Argentina ultimately affected Uru-guay was the tight nancial linkages between the two countries Uruguayan bankshave (for many years) been host to Argentinean depositors who thought theirdeposits safer when these were denominated in US dollars and kept across the Racuteode la Plata At rst as the crisis deepened in Argentina many deposits ed fromArgentine banks and found their way to Uruguay But when the Argentine author-ities declared a freeze on bank deposits in December 2001 Argentine rms andhouseholds began to draw down the deposits they kept at Uruguayan banks Thewithdrawals escalated and became a run on deposits amid fears that the Uruguayancentral bank would either run out of international reserves or (like Argentina)con scate the deposits

Other studies focused primarily on nancial channels of transmission Frankeland Schmukler (1998) and Kaminsky Lyons and Schmukler (2000) show evidence

The Unholy Trinity of Financial Contagion 59

to support the idea that US-based mutual funds have played an important role inspreading shocks throughout Latin America by selling assets from one countrywhen prices fall in anothermdashwith Mexicorsquos 1994 crisis being a prime exampleCaramazza Ricci and Salgado (2000) Kaminsky and Reinhart (2000) and VanRijckeghem and Weder (2000) focus on the role played by commercial banks inspreading shocks and inducing a sudden stop in capital ows in the form of banklending especially in the debt crisis of 1982 and the crisis in Asia in 1997 Mody andTaylor (2002) link contagion to developments in the US high yield or ldquojunkrdquo bondmarket The common thread in these papers is that without the nancial sectorlinkages contagion of the fast and furious variety would be unlikely

Summing UpTable 3 summarizes the arguments about propagation of contagion among the

ve fast and furious cases emphasized earlier Mexico in 1982 the EuropeanExchange Rate Mechanism crises of 1992 Mexicorsquos currency devaluation in 1994Thailandrsquos devaluation in 1997 and Russiarsquos devaluation in 19985 In each case weconsider the possible trade channel whether the affected countries shared similarcharacteristics with the crisis country and with each other and whether a commoncreditor was present with the possible nancial channel Indeed Table 3 lays thefoundation for our unholy trinity of nancial contagion proposition which thenext section discusses in greater detail Several features summarized in Table 3 areworth highlighting In all ve cases a common leveraged creditor was presentmaking it consistent with the explanations offered by Schleifer and Vishny (1997)Calvo (1998) and discussed in Kaminsky and Reinhart (2000) In three of the vecases the scope for propagation via trade links is virtually nonexistent and in oneof the two remaining cases (Thailand) the extent of third party competition is withMalaysia not the other affected Asian countries Lastly with the exception of thecountries that suffered most from RussiaLTCM fallout the affected countriestended to have large capital in ows and relatively xed exchange rates

The Unholy Trinity Capital In ows Surprises andCommon Creditors

Having summarized some of the key ndings of the literature on contagion wenow return to our central question of why contagion occurs in some instances butnot in others

5 For a detailed discussion of the evolution of these contagion episodes the interested reader is referredto IMF World Economic Outlook (January 1993) for the ERM crisis IMF International Capital Markets(August 1995) for the more recent Mexican crisis Nouriel Roubinirsquos home page ^httppagessternnyuedunroubiniamp for an excellent chronology of the Asian crisis and IMF World EconomicOutlook and International Capital Markets Interim Assessment (December 1998) for Russiarsquos defaultand LTCM crisis Diaz-Alejandro (1984) provides a compelling discussion of the debt crisis of the early1980s

60 Journal of Economic Perspectives

Table 3Propagation Mechanisms in Episodes of Contagion

Episode TradeCommon characteristicacross affected countries Common creditor

Mexico August 1982 As the entire regionwas affected tradelinks are signi canteven though thereare low levels ofbilateral tradeamong most of theaffected countries

Large scal de citsweak bankingsectorsdependence oncommodity pricesand heavy externalborrowing

US commercial banks

Finland September 81992mdashERM crisis

While bilateral exportsto Finland from theaffected countriesare small there aresubstantial tradelinks among all theaffected countries

Large capital in owscommon exchangerate policy as partof the EuropeanMonetary System

Hedge funds

Mexico December 211994

No signi cant tradelinks Bilateral tradewith Argentina andBrazil was minimalOnly 2 percent ofArgentinarsquos andBrazilrsquos exports weredestined to MexicoLittle scope forthird-party tradestory Mexicorsquosexports to theUnited States werevery different fromArgentine andBrazilian exports

Exchange rate basedin ationstabilization plansSigni cantappreciation of thereal exchange rateand concernsaboutovervaluationLarge capitalin ows in the run-up to the crisis

Primarily USbondholdersincluding mutualfunds

Thailand July 2 1997 Bilateral trade withother affectedcountries was verylimited Malaysiaexported similarproducts to some ofthe same thirdmarkets

Heavily managedexchange ratesand large increasein the stock ofshort-term foreigncurrency debt

European and Japanesecommercial bankslending to ThailandKorea Indonesia andMalaysia Mutualfunds sell off HongKong and Singapore

RussiaLTCM August18 1998

Virtually no trade withthe most affectedcountries (bilateralor third party)Exports from BrazilMexico and HongKong to Russiaaccounted for 1percent or less oftotal exports forthese countries

The most liquidemerging marketsBrazil Hong Kongand Mexico weremost affectedThese threecountriesaccounted for thelargest shares ofmutual fundholdings

Mutual funds andhedge funds

Sources Direction of Trade International Monetary Fund Bank of International Settlements Interna-tional Finance Corporation

Graciela L Kaminsky Carmen M Reinhart and Carlos A Vegh 61

The Capital Flow CycleFast and furious contagion episodes are typically preceded by a surge in capital

in ows which more often than not come to an abrupt halt or sudden stop in thewake of a crisis The in ow of capital may come from banks other nancialinstitutions or bondholders The debt contracts typically have short maturitieswhich means that the investors and nancial institutions will have to make decisionsabout rolling over their debts or not doing so With fast and furious contagioninvestors and nancial institutions who are often highly leveraged are exposed tothe crisis country Such investors can be viewed as halfway through the door readyto back out on short notice

This rising nancial exposure to emerging markets is not present to nearly thesame extent in the crises without major external consequences Financial crises thathave not set off major international dominos have usually unfolded against lowvolumes of international capital ows Given lower levels of exposure investors andinstitutions in the nancial sector have a much lower need to adjust their portfolios

Figure 1Net Private Capital Flows 1985ndash2003(billions of US dollars)

a Includes Argentina and Mexicob Includes Indonesia Malaysia Philippines South Korea and ThailandSource IMF World Economic OutlookNote If the crisis occurred in the second half of the year the vertical line is inserted in the followingyear

62 Journal of Economic Perspectives

Table 4Capital Flows and Capital Flight on the Eve of Crises

Episode Capital ow background in crisis countryCapital ow background in other

relevant countries

Fast and furious episodes

Exchange ratemechanism crisisFinland September 81992

Net capital ows to Finland had risenfrom less than $2 billion in 1998 to$9 billion at their peak in 1990Portfolio ows which were about$3 billion in 1988 however hit theirpeak prior to the crisis in 1992 at$8 billion

In 1989 private net capital ows to the European Union(EU) were about $11 billion(US dollars) in 1992 onthe eve of the crisis thesehad risen to $174 billion

Tequila crisisMexico December21 1994

In 1990 private net capital ows wereless than $10 billion (US dollars) by1993 ows had risen to $35 billionEstimates of capital ight showed arepatriation through 1994

Net ows to the other majorLatin American countrieshad also risen sharply forwestern hemisphere as awhole it went from netout ows in 1989 to in owsof $47 billion in 1994

Asian crisisThailand July 2 1997

From 1993 to 1996 net capital ows toThailand doubled to about $20 billion(US dollars) in 1997 capital out owsamounted to about $14 billion

Flows to emerging Asia hadrisen from less than$10 billion (US dollars) toalmost $80 billion in 1996

Russian crisis August18 1998

While total ows into Russia peaked in1996 foreign direct investment peakedin 1998 rising from about $01 billionin 1992 to $22 billion in 1998

Excluding Asia whichwitnessed a sharp capital owreversal in 1997 capital owsto other emerging marketsremained buoyant through1997 and early 1998 havingrisen from about $9 billionin 1990 to $125 billion in1997

Cases without immediate international consequences

Brazil devalues and oats February 11999

Repatriation of capital ight amountedto about 3 percent of GDP in 1996 Byearly 1998 it had reversed into capital ight Yet net capital ows did notchange much between 1997 and 1999currency crisis notwithstanding

At about $54 billion (USdollars) in 1999 capital owsto western hemisphere wellbelow their peak ($85billion) in 1997

Turkey oats the liraFebruary 22 2001

While repatriation amounted to about2 percent of GDP during 1997ndash1999capital ight began in earnest in 2000

Following the successive crisesin Asia (1997) and Russia(1998) private capital owsto emerging markets had allbut dried up by 2001 At ameager $20 billion in 2001 ows were $200 billion offtheir peak in 1996

Argentina defaultsDecember 23 2001

Until 1998 capital abroad was beingrepatriated By 1999 however capital ight amounted to 5 percent of GDPAfter several waves of bank runscapital ight was estimated at6 percent of GDP in 2001

(See Turkey commentary)

Sources International Monetary Fund World Economic Outlook and authorsrsquo calculations

The Unholy Trinity of Financial Contagion 63

when the shock occurs In many instances because the shock is anticipatedportfolios were adjusted prior to the event

In all ve of the examples from Table 1 the capital ow cycle has also playeda key role in determining whether the effects of a crisis have signi cant interna-tional rami cations For example in the late 1970s soaring commodity prices lowand sometimes negative real interest rates (as late as 1978 real interest ratesoscillated between minus 2 percent and zero) and weak loan demand in the UnitedStates made it very attractive for US banks to lend to Latin America and otheremerging marketsmdashand lend they did Capital ows by way of bank lendingsurged during this period as shown in Figure 1 By the early 1980s the prospectsfor repayment had signi cantly changed for the worse US short-term interestrates had risen markedly in nominal terms (the federal funds rate went from below7 percent in mid-1978 to a peak of about 20 percent in mid-1981) and in real terms(by mid-1981 real short-term interest rates were around 10 percent the highestlevel since the 1930s) Since most of the existing loans had either short maturitiesor variable interest rates the effects were passed on to the borrower relativelyquickly Commodity prices had fallen almost 30 percent between 1980 and 1982and many governments in Latin America were engaged in spending sprees thatwould seal their fate and render them incapable of repaying their debts In 1981Argentinarsquos public sector de cit as a percentage of GDP was about 13 percentwhile Mexicorsquos was 14 percent during 1979ndash1980 Brazilrsquos de cit was of a compa-rable order of magnitude Prior to Mexicorsquos default in August 1982 one afteranother of these countries had already experienced currency crises banking crises

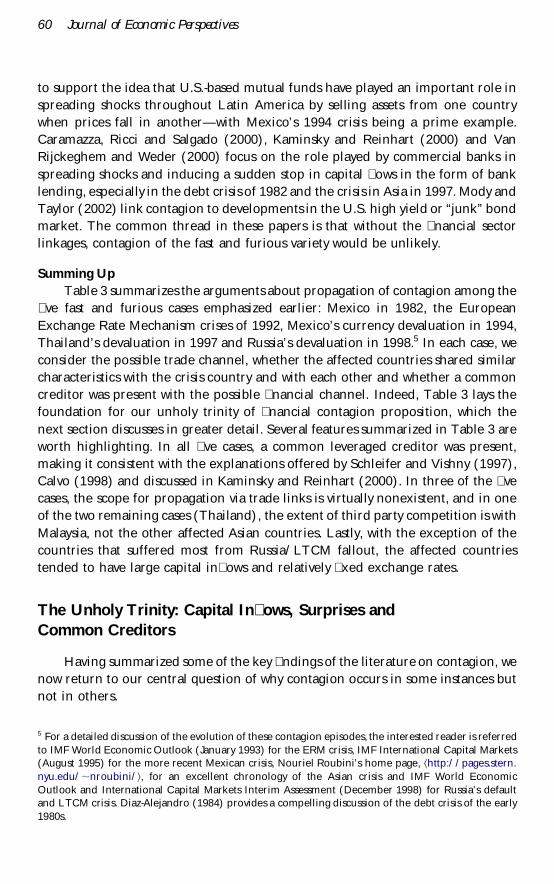

Figure 2Emerging Market Bond Market Issuance Around Crises(in billions of US dollars weekly data centered three-week moving average)

00 1 2 3 4 5 6 7 8 9 10 11 12 13 14 152122232425

04

08

12

16

2

24

28

32

36

Weeks Relative to Crisis Week (Week 0)

After Brazilian devaluation

After unilateral Russiandebt restructuring

Note Data prior to Russian default exclude the July 1998 Russian debt exchangeSource IMF staff calculations based on data from Capital Data

64 Journal of Economic Perspectives

or both When Mexico ultimately defaulted the highly exposed and leveragedbanks retrenched from emerging markets in general and Latin America inparticular

During the decade that followed Latin America experienced numerous crisesincluding some severe hyperin ations (Bolivia in 1985 and Peru Argentina andBrazil in 1990) and other defaults Yet these crises had minimal internationalrepercussions as most of the region was shut out of international capital marketsThe drought in capital ows lasted until 1990

Figure 1 shows net private capital ows for the contagion episodes of the 1990swhile Table 4 provides complementary information on capital ows and capital ight for the crisis country and those affected by it Again notice the commonpattern of a run-up in borrowing followed by a crash at the time of the initial shockand lower in ows of capital thereafter Net private capital ows to Europe had risenmarkedly and peaked in 1992 before coming to a sudden stop after the collapse ofthe Exchange Rate Mechanism crisis in which the attempt to hold exchange rateswithin preset bands fell apart under pressure from international arbitrageurs Thecrisis in the European Monetary System in 1992ndash1993 showed that emergingmarkets do not have a monopoly on vulnerability to contagion although theycertainly tend to be more prone to crisis

In the case of Mexico as the devaluation of the peso loomed close latein 1994 capital ows were close to their 1992 peak after surging considerably(As late as 1989 Mexico had recorded net large capital out ows) The rise incapital ows to the east Asian countries of Indonesia Korea Malaysia thePhilippines and Thailand (shown in Figure 1) was no less dramaticmdash especiallyafter 1995 when Japanese and European bank lending to emerging Asiaescalates

The bottom right panel of Figure 1 shows the evolution of capital ows to allemerging markets and the progression of crises The halcyon days of capital owsto emerging markets took place during the rst half of the 1990s and held up atleast for a short time after the Mexican crisis and its contagious effects on Argen-tina But the east Asian crisis brings another wave of contagion along the markeddecline in capital ows in 1997 The Russian crisis of August 1998 delivers anotherblow from which emerging market ows never fully recover in the 1990s As shownin the right bottom panel of Figure 1 this crisis is associated with the second majorleg of decline in private capital ows to emerging markets Since Figure 1 is basedon annual capital ow data it signi cantly blurs the stark differences in capital ows during the pre- and post-Russian crisis Figure 2 plots weekly data on emerg-ing market bond issuance before (negative numbers) and after (positive numbers)the Russian default (dashed line) and for contrast the Brazilian devaluation onJanuary 1999 (solid line) The vertical line marks the week of the crisis Bondissuance collapses following the Russian crisis and remains for over two monthsfollowing the event by contrast the Brazilian devaluation had no discernibleimpact on issuance which actually increases following the devaluation

Graciela L Kaminsky Carmen M Reinhart and Carlos A Vegh 65

As Figure 1 highlights the next three crisesmdashthe Brazilian devaluation ofJanuary 1999 the Turkish devaluation of February 2001 and the Argentine defaultat the end of 2001mdashtake place during the downturn of the cycle and at levels of netcapital in ows that were barely above the levels of the 1980s drought Indeed theestimates of capital ows to emerging markets in recent years shown in Figure 1may actually be overstated because total net ows include foreign direct investmentwhich held up better than portfolio bond and equity ows

Surprise Crises and Anticipated CatastrophesFast and furious crises and contagion cases have a high degree of surprise

associated with them while their quieter counterparts are more broadly antici-pated This distinction appears to be critical when ldquopotentially affected countriesrdquohave a common lender If the common lender is surprised by the shock in theinitial crisis country there is no time ahead of the impending crisis to rebalanceportfolios and scale back from the affected country In contrast if the crisis isanticipated investors have time to limit the damage by scaling back exposure orhedging their positions

Evidence that quieter episodes were more anticipated than the fast and furiouscases is presented in Table 5 Standard and Poorrsquos credit ratings had remainedunchanged during the twelve months prior to the Mexican and Thai currencycrises In the case of Russia the credit rating is actually upgraded as late as June1998 when the broader de nition that includes Credit Watch (CW) status is usedThe CW list lists the names of credits whose Moodyrsquos ratings have a likelihood ofchanging These names are actively under review because of developing trends orevents that warrant a more extensive examination Two downgrades eventually takeplace prior to the crises on August 13 1998 and again on August 17 the day beforethe default By contrast Argentina has a string ( ve) of downgrades as it marchedtoward default with the rst one taking place in October 2000 over a year beforethe eventual default Likewise Brazil and Turkey suffered downgrades well beforethe eventual currency crisis

As further evidence that markets anticipated some of the shocks and notothers Figure 3 plots of the domestic-international interest rate differential for theEmerging Market Bond Index (EMBI) and the EMBI1 for two of the contagiousepisodes (Mexico and Russia top panels) and for two crises without immediateinternational repercussions (Argentina and Brazil bottom panels)6 The patternsshown in these four panels are representative of the behavior of spreads ahead of

6 The Emerging Market Bond Index Plus (EMBI1) tracks total returns for traded external debtinstruments in the emerging markets While the EMBI covers only Brady sovereign debt bonds theEMBI1 expands upon the EMBI covering three additional markets 1) Eurobonds 2) US dollar localmarket instruments and 3) performing and nonperforming loans The country coverage of the EMBI1varies over time currently including 19 members Current members are Argentina Brazil BulgariaColombia Ecuador Egypt Mexico Malaysia Morocco Nigeria Panama Peru Philippines PolandRussia Turkey Ukraine Venezuela and South Africa

66 Journal of Economic Perspectives

anticipated and unanticipated crises (The vertical axis is measured in basis pointsso a measure of 1000 means a gap of 10 percentage points between the domesticborrowing rate and the international benchmark) If bad things are expected tohappen risk increases and spreads should widen The overall message is that fastand furious episodes are accompanied by sharp spikes in yield differentialsmdashre ecting the unanticipated nature of the newsmdashwhereas other episodes havetended to be anticipated by nancial markets

The top left panel of Figure 3 which shows the evolution of Mexicorsquos spreadin the precrisis period is striking In Mexico spreads are stable at around 500 basispoints in the months and weeks prior to the December 21 1994 devaluationIndeed Mexicorsquos spreads remained below 1000 basis points until the week ofJanuary 6 1995 Russian spreads illustrated in the top right panel of Figure 3 showremarkable stability until a couple of weeks prior to the announcement and defaultIn the case of Russia the devaluation of the ruble appears to have been widelyexpected by the markets as evident on the spreads on ruble-denominated debtOne can conjecture that it was either the actual default or the absence of an IMFbailout (following on the heels of historically large bailout packages for Mexico andKorea) that took markets by surprise

Table 5Expected and Unexpected Crises Standard and Poorrsquos Sovereign Credit RatingsBefore and After Crises

Country Crisis date

Change in rating(including Credit Watch)12 months prior to the

crisisChange in rating after

the crisis

Fast and furious contagion episodes

Mexico December 21 1994 None Downgraded two daysafter the crisisDecember 23 1994

Thailand July 2 1997 None Downgraded in AugustRussia August 18 1998 1 upgrade and 2

downgrades (thelatter on the weekof the crisis)

1 further downgrade

Crises with limited external consequences

Brazil February 1 1999 2 downgrades No immediate changeTurkey February 22 2001 1 upgrade and 2

downgrades1 further downgrade

the day after thecrisis

Argentina December 23 2001 5 downgrades betweenOctober 2000 andJuly 2001

Source Standard and Poorrsquos Sovereign Rating History Since 1975

The Unholy Trinity of Financial Contagion 67

The data presented in the bottom panels of Figure 3 illustrate the fact thatmarkets foreshadowed turbulence in the cases of Argentina (2001) and Brazil(1999) The left bottom panel of Figure 3 presents evidence for interest ratespreads for Argentina and shows that the cost of borrowing began to rise steadilyand markedly well before its default on December 23 2001 In effect since theweek of April 22 spreads began to settle above 1000 and after July 20 they neverfell below 1500 The bottom right panel of Figure 3 shows Brazilian spreads Thereis a run-up in spreads well before Brazil oats the real on February 1 1999 Thischart also reveals that Brazilmdashmore so than Argentinamdashwas quickly and markedlyaffected by the Russian crisis

In sum we have provided suggestive evidence that anticipated crises arepreceded by credit ratings downgrades and widening interest spreads before thecrisis while for unanticipated crises the downgrades and widening of spreads comeduring the crisis or after the fact

Common CreditorsAs noted international banks played an important role in the transmission of

some of the crises of the 1980s and the 1990s In the 1980s it was US banks

Figure 3Emerging Market Bond Yield Spreads 1992ndash2002

0

500

93

Mexico

94

Mexicancrisis

Russiancrisis

Brazildevaluation

Argentinacrisis

95 9692

1000

1500

2000

2500

0

2000

1000

99

Russia

00 01 0298

3000

5000

4000

6000

7000

0

2000

1000

99

Argentina

00 01 0298

3000

4000

5000

7000

6000

8000

0

500

99

Brazil

00 01 0298

1000

1500

2000

2500

Note Emerging market bond index plus (EMBI1) spreads are plottedSource JP Morgan Chase

68 Journal of Economic Perspectives

lending heavily to Latin America while in the 1990s it was European and Japanesebanks lending to Asia the transition economies and in the case of Spanish banksLatin America Here we discuss the role that commercial banks and mutual andhedge funds have played in the recent contagion episodes

International bank lending to the Asian crisis countries grew at a 25 percentannual rate from 1994 to 1997 (or at a pace of about $40 billion in ow per year)At the onset of the crisis European and Japanese banksrsquo lending to Asia was at itspeak at $165 billion and $124 billion respectively while the exposure of US bankswas much more limited Japanese banks had the highest exposure to Thailandwhich also accounted for 26 percent of their total lending to emerging markets (thelargest representation of any emerging market country in their portfolio) Collec-tively the Asian crisis countries (excluding the Philippines which did not borrowmuch from Japanese banks) accounted for 65 percent of the emerging marketloan portfolio of Japanese banks For European banks the comparable share was23 percent Following the oatation of the Thai baht on July 2 1997 the exposedbanks retrenched quickly and cut credit lines to emerging Asia The bank in owsquickly became out ows of about $47 billion

As with Asia lending to transition economies had accelerated in the mid-1990s In the three years before the Russian crisis international bank lending to theregion grew at 14 percent per annum German banks were more heavily exposedto Russia with lending to Russia averaging about 20 percent of all their lending toemerging economies As with earlier fast and furious contagion episodes bank ows to the region which oscillated around $28 billion per year in the years beforethe crisis turned into a $14 billion dollar out ow in the year following the crisisThis retrenchment in lending helps explain why other transition economies wereaffected by the Russian crisis However it fails to explain why Brazil Hong Kongand Mexico come under signi cant pressures at this time To understand these andother cases we need to turn our attention to nonbank common creditors

Equity and bond ows also declined sharply in the aftermath of the fast andfurious crises of the 1990s For example US-based mutual funds specialized inLatin America withdrew massively from the region following the Mexican crisis in1994 As discussed in Kaminsky Lyons and Schmukler (2002) withdrawals fromLatin America oscillated around 40 percent in the immediate aftermath of thecrisis The countries most affected were Argentina Brazil and (of course) Mexicowhich were the countries to which the mutual funds were most heavily exposed toin Latin America at the time of the crisis For example if one examines the LatinAmerican portfolio of mutual funds specialized in emerging markets at around thetime of the crisis Brazil Mexico and Argentina account for 37 26 and 14 percentof their portfolio respectively (that is three countries accounted for 77 percent ofthe Latin American portfolio)

The Thai crisis in 1997 also triggered equity out ows through mutual fundsfrom Asia The countries most affected by abnormal withdrawals were Hong KongSingapore and Taiwan the countries with the most liquid nancial markets in the

Graciela L Kaminsky Carmen M Reinhart and Carlos A Vegh 69

region Mutual funds were heavily exposed to these countries Of the portfolioallocated to Asia 30 percent was directed to Hong Kong 7 percent to Singaporeand 13 percent to Taiwan Kaminsky Lyons and Schmukler (2002) estimate thatabnormal withdrawals (relative to the mean ow during the whole sample) oscil-lated at around 10 percent for the three economies

Similarly highly leveraged funds seem to have had an important role in thespeculative attack against the Hong Kong dollar in August of 1998 following theRussian crisis (Corsetti Pesenti and Roubini 2001) According to a report from theFinancial Stability Forum (2000) large macro hedge funds appear to have detectedfundamental weaknesses early and started to build large short positions against theHong Kong dollar According to available estimates hedge fundsrsquo short positions inthe Hong Kong market were close to $10 billion US (6 percent of Hong KongrsquosGDP) but some observers believe that the correct gure was much higher Severallarge hedge funds also took very large short positions in the equity markets andthese positions were correlated over time As reported in the Financial StabilityForum study among those taking short positions in the equity market were fourlarge hedge funds whose futures and options positions were equivalent to around40 percent of all outstanding equity futures contracts as of early August prior to theHong Kong Monetary Authority intervention Position data suggest a correlationalbeit far from perfect in the timing of the establishment of the short positionsTwo hedge funds substantially increased their positions during the period of theHong Kong Monetary Authority intervention At the end of August four hedgedfunds accounted for 50500 contracts or 49 percent of the total open interestnetdelta position one fund accounted for one third The grouprsquos meetings suggestedthat some large highly leveraged institutions had large short positions in both theequity and currency markets

Concluding Re ections

To date what has distinguished the contagion episodes that happened fromthose that could have happened seems to have had little to do with more ldquojudiciousrdquoand ldquodiscriminatingrdquo investorsmdashnor with any improvements to boast of in the stateof the international nancial architecture If investors behaved in a more discrim-inating manner in the recent crises where contagion could have happened but didnot it is because i) those crises tended to unfold in slow motion and were thuswidely anticipated ii) the capital ow bubble had been pricked at an earlier stagewhen those same investors were more ldquoexuberantrdquo and hence iii) the ldquocommoncreditorrdquo we have stressed in our discussion was less leveraged in these episodesWhen looking back into history one is struck by an overwhelming sense of deja vuIt certainly seems a mystery why episodes of nancial crises and contagion recur inspite of the major costs associated with crises that would seem to provide a suf cientmotivation for avoiding them But based on historical experience there appears to

70 Journal of Economic Perspectives

be little hope that during the good times future generations of sovereign borrow-ers or investors will remember that the four most expensive words in nancialhistory are ldquothis time itrsquos differentrdquo

If history is any guide nancial crises will not be eliminatedmdashas Kindleberger(1977) noted they are hardy perennials But it should be possible based on theunderstanding of what causes contagion and what does not for countries to takesteps to reduce their vulnerability to international contagion

Contagion appears to be linked to a substantial in ow of capital to a countryOf course the prospect of nancial autarky as a way of avoiding fast and furiouscontagion is not particularly attractive as a long-run solution It may not even befeasible when countries have already liberalized the nancial sector and the capitalaccount But before turning to the issue of capital account restrictions it is criticalto remember that in many crises (most of those discussed here and many others)the lead and largest borrower in international capital markets during the boomperiods are the sovereign governments themselves As Reinhart Rogoff and Savas-tano (2003) observe it is the most debt-intolerant countries with a history of serialdefault that can least afford to borrow that usually borrow the most Often theoutcome is default

So as a rst important step the risk of contagion would be reduced if policy-makers in countries that are integrated with world capital markets remember thatmany a surge in capital in ows often ends in a sudden stopmdashwhether owing tohome-grown problems or contagion from abroad As a consequence prudentpolicymaking would at a minimum ensure that the government does not overspendand overborrow when international capital markets are all too willing to lend asthose episodes can often end in tears In contrast scal policy in emerging marketscurrently tends to be markedly procyclical with countries engaging in expansionary scal policy in good times and contractionary scal policy in bad times (Talvi andVegh 2000) Fiscal reforms aimed at designing institutional mechanisms thatwould discourage such procyclical behavior (particularly on the part of ldquoprovincesrdquoor other autonomous entities) appear as an essential ingredient in preventingfuture crises from building up However such consistent self-discipline on the partof governments has historically proved elusive

As regards to curbing private borrowing from abroad the issues are even morecomplex The best case for restrictions on international nancial in ows wouldseem to focus on debt contracts with short maturities that are denominated in aforeign currency the kind of capital ows that have been the trigger in manymodern contagion episodes But although such policies may help in tilting thecomposition of capital ows toward longer maturities their overall long-termeffectiveness is unclear Curbing capital out ows once contagion and the ensuingsudden stop has occurred is even more problematic Experience has shown thatcapital ight has been an endemic problem for countries that have tried to turn theclock back and reintroduce tight capital account and nancial restrictions amidst

The Unholy Trinity of Financial Contagion 71

economic turmoil More fundamentally pervasive capital controls hardly seemlikely to be the solution in the medium and long run to the contagion and suddenstop problem

As to new mechanisms in nancial centers that could curb these periodic boutsof lending and ldquoirrational exuberancerdquo and lessen the likelihood of unpleasantfuture surprises we remain very skeptical that there are easy or obvious solutionsAccess to more information may not lessen surprises when borrowers and lendershave often shown themselves willing to downplay worrisome fundamentals that arein the public domain in the late 1990s under the guise of having superior infor-mation The economic historian Max Winkler wrote in the New York Tribune ofMarch 17 1927

The over-abundance of funds together with the dif culty of nding the mostpro table employment therefore at home has contributed greatly to thepronounced demand for and the ready absorption of large foreign issuesirrespective of quality While high yield on a foreign bond does notnecessarily indicate inferior quality great care must be exercised in theselection of foreign bonds especially today when anything foreign seems to nd a ready market Promiscuous buying however is destined to provedisastrous

In 1929 a wave of currency crises swept through Latin Americamdashit was quicklyfollowed by a string of defaults on sovereign external debt obligations At the timeof this writing with investors searching for high yields quickly snapping up emerg-ing market bonds Winklerrsquos warning rings as true now as it did then

y The authors wish to thank Laura Kodres Vincent Reinhart and Miguel Savastano for veryuseful comments and suggestions and Kenichi Kashiwase for excellent research assistance

72 Journal of Economic Perspectives

References

Banerjee Abhijit 1992 ldquoA Simple Model ofHerd Behaviorrdquo Quarterly Journal of EconomicsAugust 1073 pp 797ndash817

Basu Ritu 1998 ldquoContagion Crises The In-vestorrsquos Logicrdquo Mimeograph University of Cali-fornia Los Angeles

Bikhchandani Sushil David Hirshleifer andIvo Welch 1992 ldquoA Theory of Fads FashionCustom and Cultural Change as InformationalCascadesrdquo Journal of Political Economy 1005 pp992ndash1026

Bikhchandani Sushil David Hirshleifer andIvo Welch 1998 ldquoLearning from the Behavior ofOthers Conformity Fads and InformationalCascadesrdquo Journal of Economic Perspectives Sum-mer 123 pp 151ndash70

Bordo Michael and Barry Eichengreen 1999ldquoIs Our Current International Economic Envi-ronment Unusually Crisis Pronerdquo in CapitalFlows and the International Financial System DavidGruen and Luke Gower eds Sydney ReserveBank of Australia pp 50ndash 69

Bordo Michael and Antu P Murshid 2000ldquoThe International Transmission of FinancialCrises before World War II Was there Conta-gionrdquo Mimeograph

Caballero Ricardo and Arvind Krishnamur-thy 2003 ldquoSmoothing Sudden Stopsrdquo Journal ofEconomic Theory Forthcoming

Calvo Guillermo 1998 ldquoCapital Market Con-tagion and Recession An Explanation of theRussian Virusrdquo Mimeograph

Calvo Guillermo and Enrique Mendoza2000 ldquoRational Contagion and the Globaliza-tion of Securities Marketsrdquo Journal of Interna-tional Economics June 511 pp 79 ndash113

Calvo Guillermo and Carmen Reinhart2000 ldquoWhen Capital In ows Come to a Sud-den Stop Consequences and Policy Optionsrdquoin Reforming the International Monetary and Fi-nancial System P Kenen and A Swoboda edsWashington DC International MonetaryFund pp 175ndash201

Caramazza Franceso Luca Ricci and RanilSalgado 2000 ldquoTrade and Financial Contagionin Currency Crisesrdquo IMF Working Paper WP0055

Corsetti Giancarlo Paolo Pesenti andNouriel Roubini 2001 ldquoThe Role of Large Play-ers in Currency Crisesrdquo NBER Working Paper8303 May

Dawson Frank G 1990 The First Latin Ameri-

can Debt Crisis New Haven and London YaleUniversity Press

Diaz-Alejandro Carlos 1984 ldquoLatin AmericanDebt I Donrsquot Think We are in Kansas AnymorerdquoBrookings Papers on Economic Activity 2 pp 335ndash403

Doukas John 1989 ldquoContagion Effect on Sov-ereign Interest Rate Spreadsrdquo Economic LettersMay 29 pp 237ndash41

EichengreenBarry Andrew Rose and CharlesWyplosz 1996 ldquoContagious Currency CrisesFirst Testsrdquo Scandinavian Journal of Economics984 pp 463ndash84

Financial Stability Forum 2000 ldquoWorkingGroup on Highly Leveraged Institutions(HLIs)rdquo April

Frankel Jeffrey and Sergio Schmukler1998 ldquoCrises Contagion and Country FundsEffects on East Asia and Latin Americardquo inManaging Capital Flows and Exchange Rates Per-spectives from the Pacic Basin Reuven Glick edNew York Cambridge University Press pp232ndash 66

Gerlach S and Frank Smets 1996 ldquoConta-gious Speculative Attacksrdquo CEPR Discussion Pa-per No 1055

Glick Reuven and Andrew Rose 1999 ldquoCon-tagion and Trade Why are Currency Crises Re-gionalrdquo Journal of International Money and Fi-nance August 184 pp 603ndash17

Goldstein Morris 1998 The Asian FinancialCrisis Washington DC Institute for Interna-tional Economics

International Monetary Fund Various IssuesCapital Markets Report

International Monetary Fund Various IssuesWorld Economic Outlook

Kaminsky Graciela and Carmen Reinhart2000 ldquoOn Crises Contagion and ConfusionrdquoJournal of International Economics June 511 pp145ndash 68

Kaminsky Graciela and Sergio Schmuk-ler 1999 ldquoWhat Triggers Market Jitters AChronicle of the Asian Crisisrdquo Journal of Inter-national Money and Finance August184 pp537ndash 60

Kaminsky Graciela Richard Lyons and Ser-gio Schmukler 2000 ldquoManagers Investorsand Crises Mutual Fund Strategies in Emerg-ing Marketsrdquo NBER Working Paper No7855

Kaminsky Graciela Richard Lyons and SergioSchmukler 2002 ldquoLiquidity Fragility and Risk

Graciela L Kaminsky Carmen M Reinhart and Carlos A Vegh 73

The Behavior of Mutual Funds During CrisesrdquoMimeograph

KindlebergerCharles P 1977 Manias Panicsand Crashes New York John Wiley amp Sons

Kodres Laura and Matthew Pritsker 2002 ldquoARational Expectations Model of Financial Conta-gionrdquo Journal of Finance April 572 pp 769ndash800

Lahiri Amartya and Carlos A Vegh 2003ldquoDelaying the Inevitable Optimal Interest RateDefense and BOP Crisesrdquo Journal of Political Econ-omy Spring 1 pp 1ndash62

Mody Ashok and Mark Taylor 2002 ldquoCom-mon Vulnerabilitiesrdquo Mimeograph

Neal Larry and Marc Weidenmeir 2002 ldquoCri-ses in the Global Economy from Tulips to TodayContagion and Consequencesrdquo NBER WorkingPaper 9147 September

Nurkse Ragnar 1944 International CurrencyExperience Lessons of the Interwar Period GenevaLeague of Nations

Reinhart Carmen M Kenneth S Rogoff andMiguel A Savastano 2003 ldquoDebt IntolerancerdquoBrookings Papers on Economic Activity Forthcoming

Shleifer Andrei and Robert W Vishny 1997ldquoThe Limits of Arbitragerdquo Journal of FinanceMarch 521 pp 35ndash55

Talvi Ernesto and Carlos A Vegh 2000 ldquoTaxBase Variability and Procyclical Fiscal PolicyrdquoNBER Working Paper No 7499

Van Rijckeghem Caroline and BeatriceWeder 2000 ldquoFinancial Contagion Spilloversthrough Banking Centersrdquo Mimeograph

Winkler Max 1933 Foreign Bonds An AutopsyPhiladelphia Roland Swain Company

74 Journal of Economic Perspectives

Table 1 presents summary material for recent contagion episodes The rstcolumn lists the country the date that marks the beginning of the episode thenature of the shock and currency market developments in the crisis country Theremaining columns include information on the existence and nature of commonexternal shocks the suspected main mechanism for propagation across nationalborders and the countries that were most affected

The challenge for economic researchers is to explain why the number of nancial crises that did not have signi cant international consequences is fargreater than those that did It is no surprise that a domestic crisis (no matter howdeep) in countries that are approximately autarkic (either voluntarily or otherwise)will not likely have immediate repercussions in world capital markets The countriesmay be large (like China or India) or comparatively small (like Bolivia or Guinea-Bissau) More intriguing cases of ldquocontagion that never happenedrdquo are thosewhere the crisis country is relatively large (at least by emerging market standards)and is reasonably well integrated to the rest of the world through trade or nanceAlong with the fast and furious contagion episodes these cases are the focus of thispaper

Some recent nancial crises with limited immediate consequences includethese examples Brazilrsquos devaluation of the real on January 13 1999 andeventual otation on February 1 1999 the Argentine default and abandon-ment of the Convertibility Plan in December 2001 and Turkeyrsquos devaluation ofthe lira on February 22 2001 Given that Brazil Turkey and Argentina arerelatively large emerging markets these episodes could have beenmdashat leastpotentiallymdashas highly ldquocontagiousrdquo as the Thai and Russian crises Nonetheless nancial markets shrugged off these events despite the fact that it was evidentat the time that some of these shocks would have trade and real sector reper-cussions on neighboring countries over the medium term For example be-cause Brazil is Argentinarsquos largest trading partner the sharp depreciation of thereal (about 70 percent between January and the end of February) clearly left theArgentine peso overvalued Table 2 presents some summary material for theseepisodes in a format parallel to Table 1

This paper seeks to address the central question of why nancial contagionacross borders occurs in some cases but not others2 Throughout the paper westress that there are three key elements that distinguish the cases where contagion

2 Of course there are historical examples of fast and furious contagion before the last few decadesCommonly cited examples of contagion include the rst Latin American debt crisismdashwhich began withPerursquos default in April 1826 mdashand the international nancial crisis of 1873 Going back even further intime Neal and Weidenmeir (2002) also discuss the ldquocontagionrdquo dimension of the Tulip Mania of the1630s and the Mississippi and South Sea Bubbles of 1719ndash1720 Two leading examples of nancial crisesthat did not lead to contagion include the well-documented Argentina-Baring crisis of 1890 and theUnited States nancial crisis of 1907 For detailed accounts of historical episodes of nancial crises seeBordo and Eichengreen (1999) Bordo and Murshid (2000) Kindleberger (1997) and Neal andWeidenmier (2002)

52 Journal of Economic Perspectives

Table 1Financial Crises with Immediate International Repercussions 1980ndash2000

Origin of the shock countryand date

Nature of common externalshock if any Contagion mechanisms Countries affected

On August 12 1982Mexico defaults on itsexternal bank debt ByDecember the pesohad depreciated by100 percent

Between 1980 and 1985commodity prices fellby about 31 percentUS short-term realinterest rates rise toabout 7 percent thehighest levels sincethe depression

US banks heavilyexposed to Mexicoretrenched fromemerging markets

With the exception ofChile Colombia andCosta Rica allcountries in LatinAmerica defaulted

On September 8 1992the Finnish markka is oated and theExchange RateMechanism (ERM)crisis unfolds

High interest rates inGermany Rejectionby Danish voters ofthe Maastricht treaty

Hedge funds All the countries in theEuropean MonetarySystem exceptGermany

On December 20 1994Mexico announced a15 percent devaluationof the peso It sparkeda con dence crisisand by March 1995the pesorsquos value haddeclined by about100 percent

From January 1994 toDecember theFederal Reserve raisedthe federal funds rateby about 25percentage points

Mutual funds sell offother Latin Americancountries notablyArgentina and BrazilMassive bank runsand capital ight inArgentina

Argentina suffered themost losing about20 percent ofdeposits in early1995 Brazil wasnext while losses inother countries inthe region limited todeclines in equityprices

On July 2 1997Thailand announcesthat the baht will beallowed to oat ByJanuary 1998 the bahthad depreciated byabout 113 percent

The yen depreciated byabout 51 percentagainst the US dollarduring April 1995 andApril 1997 Given theAsian currencies linkto the US dollar thistranslated into asigni cantappreciation for theircurrencies as well

Japanese banksexposed to Thailandretrenched fromemerging Asia AsKorea is affectedEuropean banks alsowithdraw

Indonesia KoreaMalaysia and thePhilippines were hithardest Financialmarkets in Singaporeand Hong Kong alsoexperienced someturbulence

On August 18 1998Russia defaults on itsdomestic bond debtBetween July 1998 andJanuary 1999 theruble depreciated by262 percent OnSeptember 2 1998 itbecame publicknowledge that LTCMhad gone bankrupt

With heavy exposure toRussia and otherhigh-yieldinstruments LTCM isrevealed to bebankrupt

Margin calls andleveraged hedgefunds fueled the selloff in other emergingand high yieldmarkets It is dif cultto distinguishcontagion fromRussia and fear ofanother LTCM

Apart from several ofthe former Sovietrepublics HongKong Brazil andMexico were hithardest But mostemerging anddeveloped marketswere affected

Sources International Monetary Fund International Financial Statistics dates of the default or restruc-turings are taken from Reinhart Rogoff and Savasteno (2003)

Graciela L Kaminsky Carmen M Reinhart and Carlos A Vegh 53

occurs from those where it does not We call them the ldquounholy trinityrdquo an abruptreversal in capital in ows surprise announcements and a leveraged commoncreditor First contagion usually followed on the heels of a surge in in ows ofinternational capital and more often than not the initial shock or announcementpricked the capital ow bubble at least temporarily The capacity for a swift and

Table 2Selected Financial Crises without Immediate International Repercussions1999ndash2001

Origin of the shockcountry and date

Background on therun-up to the shock Spillover mechanisms Countries affected

On January 131999 Brazildevalues the realand eventually oats on February1 Between earlyJanuary and end-February the realdepreciates by70 percent

The crawling pegexchange ratepolicy (the RealPlan) that wasadopted in July1994 to stabilizein ation isabandoned

There is an increasein volatility insome of largerequity marketsand Argentinaspreads widenedEquity markets inArgentina andChile ralliedThese effectslasted only a fewdays

Signi cant and protractedeffect on Argentina asBrazil is Argentinarsquoslargest trading partner

On February 222001 Turkeydevalues and oats the lira

Facing substantialexternal nancingneeds in lateNovember 2000rumors of thewithdrawal ofexternal credit linesto Turkish bankstriggered a foreignexchange out owsand overnight ratessoared to close to2000 percent

There has been someconjecture that theTurkish crisis may haveexacerbated thewithdrawal of investorsfrom Argentina butgiven the weakness inArgentinarsquosfundamentals at thetime it is dif cult tosuggest developmentsowed to contagion

On December 232001 thepresident ofArgentinaannouncesintentions todefault

Following severalwaves of capital ight and runs onbank deposits onDecember 1st

capital controls areintroduced

Bank deposits fallby more than30 percent inUruguay asArgentineswithdraw depositsfrom Uruguayanbanks Signi canteffects oneconomic (tradeand tourism)activity inUruguay

Uruguay and to a muchlesser extent Brazil

54 Journal of Economic Perspectives

drastic reversal of capital owsmdashthe so-called ldquosudden stoprdquo problemmdashplayed asigni cant role3 Second the announcements that set off the chain reactions cameas a surprise to nancial markets The distinction between anticipated and unantic-ipated events appears critical as forewarning allows investors to adjust their port-folios in anticipation of the event Third in all cases where there were signi -cant immediate international repercussions a leveraged common creditor wasinvolvedmdashbe it commercial banks hedge funds mutual funds or bondholdersmdashwho helped to propagate the contagion across national borders

Before turning to the question of what elements distinguish the cases wherecontagion occurs from those where it does not however we provide a brief tour ofthe main theoretical explanations for contagion and the most salient empirical ndings on the channels of propagation

What is Contagion

Since the term ldquocontagionrdquo has been used liberally and has taken on multiplemeanings it is useful to clarify what it will mean in this paper We refer to contagionas an episode in which there are signi cant immediate effects in a number ofcountries following an eventmdashthat is when the consequences are fast and furiousand evolve over a matter of hours or days This ldquofast and furiousrdquo reaction is acontrast to cases in which the initial international reaction to the news is mutedThe latter cases do not preclude the emergence of gradual and protracted effectsthat may cumulatively have major economic consequences We refer to thesegradual cases as spillovers Common external shocks such as changes in interna-tional interest rates or oil prices are also not automatically included in our workingde nition of contagion Only if there is ldquoexcess comovementrdquo in nancial andeconomic variables across countries in response to a common shock do we considerit contagion

Theories of Contagion

Through what channels does a nancial crisis in one country spread acrossinternational borders Some models have emphasized investor behavior that givesrise to the possibility of herding and fads It is no doubt possible (if not appealingto many economists) that such ldquoirrational exuberancerdquo to quote Federal ReserveChairman Alan Greenspan can in uence the behavior of capital ows and nan-cial markets and exacerbate the booms as well as the busts Other models stresseconomic linkages through trade or nance This section provides a selective

3 See Calvo and Reinhart (2000) for an empirical analysis of sudden stop episodes and Caballero andKrishnamurthy (2003) for a model that traces out the economic consequences of sudden stops

The Unholy Trinity of Financial Contagion 55