The UK Logistics Confidence Index 2020 - Barclays Corporate

31

The UK Logistics Confidence Index 2020 Adapting to new realities

Transcript of The UK Logistics Confidence Index 2020 - Barclays Corporate

The UK Logistics Confidence Index 2020Adapting to new realities

⊳ Previous | 2 | Next page ⊲

Contents 3 Executivesummary

5 Asnapshotofcurrentmarketconditions

7 Businessoutlook

9 Covid-19impact

12 Challengesandopportunities

15 Brexit–nextsteps

17 Thetalentandskillsshortage

19 Technologyandinnovation

21 Greeninitiatives

22 Mergersandacquisitions

24 Industryinsight:WoodlandGroup

26 Industryinsight:AdvancedSupplyChainGroup

27 Keytakeaways

28 Aboutthisreport

29 Abouttheauthors

⊳ Previous | 3 | Next page ⊲

Executive summaryBarclaysandBDO,inconjunctionwithspecialistsectorresearchagencyAnalytiqa,haveundertakenthelatestinourseriesofsurveystoassessconfidenceandexpectationsintheUKlogisticssector.

Morethan100seniordecision-makers,includingchiefexecutiveofficers,managingdirectorsandchieffinancialofficers,providedtheirviewsandinsightsforthissurvey,conductedduringSeptemberandOctober2020.TheirresponseshavebeencompiledtocreatetheUKLogisticsConfidenceIndex2020.

Surveyrespondentsaredrawnfromallsectorsoftheindustry,coveringroad,airandsea,andinclude:freightforwarders,roadhauliers,alongwithoperatorsincontractlogistics,courierandexpressservices,ande-commerce/lastmiledeliveries.TrackingtheheadofficelocationsofourrespondentsshowsthathalfarebasedintheMidlandsandtheNorthofEngland,NorthernIreland,ScotlandandWales,withtheotherhalfbasedtowardstheSouthoftheUK.

Confidenceatlowesteverlevel

OuroverallConfidenceIndexhasfallenfrom49.7in2019to47.1thisyear.ThiscontinuesthedownwardtrendwehaveseeninrecentyearsandtakestheIndextoitslowestlevelsinceoursurveybeganin2012.

ThesetwoconsecutiveIndexscoresofbelow50indicatethat,overall,thesectorremainsmorepessimisticthanoptimisticaboutthestateofthemarket.GiventheunprecedentedimpactofCovid-19,perhapstheonlysurprisehereisthatthisyear’sfallinconfidencehasnotbeenmorepronounced.

Morethantwo-thirdsoflogisticscompanies(67.1%)saytradinghasbeentougherinthepastyearandalmosta

quarter(24.2%)saymarketconditionsaremuchmoredifficultthanlastyear–thehighestproportionsincethesecondhalfof2012.

However,logisticscontinuestobeastrongandresilientsectorandremainsamajorcontributortotheUKeconomy–totalcombinedUKrevenueforthe100+companiessurveyedis£16.4bn–and,evenunderthecurrenthighlychallenginganduncertaineconomicconditions,nearlyhalf(48.9%)ofthemsaytheystillexpecttoseeprofitsincreaseoverthenext12months.

ImpactofCovid-19

ThearrivalofCovid-19thisyear,anditsdramaticimpactonglobalandUKeconomicgrowth,hasaddedanothertotallyunexpectedlayerofchallengesfortheindustryontopoftheongoinguncertaintysurroundingtheUK’sfuturetradingrelationshipwiththeEU,andtheperennialissueofdrivershortages.

Covid-19hasclearlyhadadramaticanddistortingeffectonthesector,whichhasledtosomethingofanindustryreset.Ourresearchshows60.2%ofbusinesseshavebeennegativelyimpactedbythepandemic;itisworthnotingthatthisresponsewasrecordedbeforetheannouncementofthesecondnationallockdowninEnglandinNovember2020.

Yetthereisahighdegreeofpolarisationintheviewsofoperators,with35.5%sayingthepandemichashadapositiveimpactontheircompany’sperformance,despitetheeconomicdisruption.

Asinsomanyotherindustries,Covid-19hasshakenupthelogisticssectorbyrapidlyacceleratinganumberofexistingtrends–suchasthemovetoe-commerce,manufacturersincreasinglygoingdirecttoendconsumersandnewtechnologyadoption–andalsobyaddingunforeseenchallengesintothemix,likethepositiveornegativedisruptiveeffectsondemand,aswellasonsupplychains.Thishasleftsomeoperatorsinastrongposition,whileothershavestruggled,oftenlargelyasaresultofhowtheirend-usermarketshavebeenimpacted.

However,havingweatheredtheinitialimpactofthepandemic,thefocusisnowshiftingtoadaptingtothenewconstraintsandmarketconditions,andtheopportunitiesthatareemerging.Forexample,distributionoftherecentlyannouncedUSCovid-19vaccinepresentsbothalogisticalchallengeandagreatopportunityforthesectortoapplyandshowcaseitsexpertiseandabilitytodeliversolutions.Operatorswillneedtocontinuetoseeknewwaystoaddvalueacrossthesupplychain.It’slikelythatthemostagileandadaptablebusinesseswillemergestrongestfromthecrisis,buttheperiodofadjustmentfacingthesectormaybepainfulforsome.

⊳ Previous | 4 | Next page ⊲

Ongoingchallenges

AsidefromCovid-19,drivershortagesandBrexittransitionremainthemostpressingissuesforthecompaniesinoursurvey.

TheindustryseemstobeexperiencingamixtureofnervousnessandcalmtowardsBrexittransition.Whileoperators’attitudesareperhapsslightlymorerelaxedabout–orperhapssimplyresignedto–Brexitthanlastyear,possiblybecausetheyfeelmoreprepared,nearlyhalf(47.9%)stillfeartheywillbedoinglessbusinesswithEUcompaniesintheeventofnotradedealbeingagreed.

Meanwhile,theongoinglackofdriversinthesectorhasbeencompoundedbyanemergingshortageofskilledwarehousestaff.Toalleviatethesetalentshortages,operatorsareworkinghardtoattractmoreyoungpeopleintotheindustry,improvepayandconditionsandstrengthentraining.Inaddition,overhalfoffirmsthatrunwellnessprogrammesforemployeesareseeingimprovedstaffretention(55.2%),fallingabsenteeism(79.3%)andgreaterproductivity(56.9%)asaresult.

Morethaneverbefore,utilisingtechnologyisincreasinglyseenasthekeytoaddressingmanyofthesechallengesandtoenhancingvalue-addedserviceofferingstomeetnewservicelevelnorms.Inparticular,techisbeingdeployedtohelpalleviatethetalentshortage,with42.2%ofoperatorssayingthey’veinvestedinsomeformoftechnologytoreplacehumantalentinthelastyear.Butthereisalsoarealisationthatadifferentskillsetmayberequiredacrosstheworkforcetodrivechange.

However,whilecompaniesrecognisetheneedtoinvestinnewtechnology,automationandrobotics,themajorityoftechinvestmentcontinuestoinvolveupgradesofexistingsystems.

Lookingtothefuture

DespitetheimpactofCovid-19,morethansevenoutof10operators(72.2%)reportcontinuinginvestmentin‘green’projectsconnectedwithsustainabilityandtheenvironment.Thisprimarilyinvolvesintroducingalternative-fuelfleets,optimisingfuelusedbyexistingvehicles,recyclinginitiatives

andinstallingneweco-friendlywarehousinglightingsystems.Aswellasbringingworthyenvironmentalbenefits,manyoftheseprojectsalsodeliverlongtermcost-savingbenefits.

Finally,moresectorconsolidationlookstobeonthecards.Oursurveyshowsthat38.9%ofoperatorsareconsideringmakingacquisitionswithinthenext12months–thehighestlevelsince2017–mainlytoachieveeconomiesofscaleortoexpandtheirserviceoffering.Furthermore,theyarelikelytohavemoreopportunitiestoacquire,asstrugglingfirmsareforcedtogotomarketwhengovernmentCovid-19supportmeasuresarewithdrawn.

Wetrustyouwillfindthisreportinformativeandhelpful.

Ian CranidgeRelationshipDirector,HeadofTransportandLogistics,BarclaysUKCorporateBanking

Jason Whitworth Partner,M&AAdvisoryandLogistics&SupplyChainManagement,BDOLLP

Our overall Confidence Index has fallen from 49.7 in 2019 to 47.1 this year. This continues the downward trend we have seen in recent years and takes the Index to its lowest level since our survey began in 2012.

⊳ Previous | 5 | Next page ⊲

Foronlythesecondtimesinceoursurveybeganin2012theLogisticsConfidenceIndexisinnegativeterritorybelow50,at47.1.Thisisitslowestleveltodate,reflectingtheimpactoftheCovid-19pandemic,aswellasongoingchallengesfacingthesector.

Thefallfrom49.7lastyear,itselfthefirsttimetheindexfellbelow50,isacontinuationofadownwardtrendthatbeganin2017.

OursurveyalsoshowsaslightdifferenceintheConfidenceIndexnumberbetweentheNorthandSouthoftheUK,withtheNorthslightlylesspessimisticthantheSouth.WhiletheindexnumberforoperatorsintheSouthhasremainedconsistentwithlastyear,at45.8,forrespondentsintheNorthithasdeclinedslightly,from52.9to48.2.

Thefallinoverallconfidenceisunsurprising,giventhebackdropofunprecedenteddomesticandglobalupheavalcreatedbythepandemic,inadditiontoongoinguncertaintyovertheUK’sfuturerelationshipwiththeEU,andthecontinuingskillsshortages.

Indeed,withtheoverallimpactoftheCovid-19crisisontheUKeconomyleadingtoasharpcontractioninGDPandtheprospectofrisinglevelsofunemployment,weperhapsmighthaveexpectedanevenmorepessimisticresult.

A snapshot of current market conditionsOurLogisticsConfidenceIndexhasfallentoanewlowandnowstandsat47.1.

LogisticsConfidenceIndex

H2,

201

6

2017

2018

2019

2020

H1,

201

6

H2,

201

5

H1,

201

5

H2,

201

4

H2,

201

3

H1,

201

3

H2,

201

2

H1,

201

2

57.252.5

60.3

74.9 71.4 69.261.9

51.8 53.0 56.7 52.6 49.7 47.1

⊳ Previous | 6 | Next page ⊲

Challengingbusinessconditions

Two-thirds(67.1%)ofcompaniesinoursurveysaythatcurrentbusinessconditionshavebecomemoredifficultthan12monthsago,whileaquarter(24.2%)believetheyare“muchmoredifficult”,thehighestsuchresultsincethesecondhalfof2012.

Oursurveysuggeststhatlargercompanieshavegenerallyfoundthingsmoredifficultthansmallerones,despitebeingmorelikelytobenefitfromamorediversecustomerbase,astheymayhavefoundithardertoadaptquicklytothechangingmarket.

Lookingbacktolastyear,therewasageneralbeliefamongrespondentsthatoncegreaterclarityonBrexitwasachieved,confidencewouldstarttoimprove–buttheimpactofthepandemichasclearlyunderminedthesector’soptimism.

WhiletherewerebrightersignsoverthesummermonthsastheeconomybegantopickupaftertheinitialCovid-19shock,thishasclearlybeendampened,particularlyamongoperatorsinstrugglingend-usermarketssuchashospitalityandleisure,byrenewedrestrictionsoneconomicactivityasthecountrycopeswithasecondCovid-19wave.

GiventhatconcernsoverfutureEUtraderelationshavebeenresurfacingintherunuptotheendoftheBrexittransitionperiod,oursurveyresultsreflectawhollyunexpected‘doublewhammy’facingthesector.

Polarisingimpact

Oursurveyunderlineshowthechangesinthemarketasaresultoflockdownhavepolarisedtheviewsofoperators,dependingonhowthesectorstheyaremostexposedtohaverespondedtothepandemic.Unsurprisingly,thosefocusedone-commerceandlast-miledeliveriesoronpharmaceuticalsandhealthcareforexample,havefaredrelativelywell,whileothersoperatinginmanufacturingsectors,suchasautomotive,sawunprecedentedlevelsofdisruption.

Respondentcomment

“ Margins are tough, rates are low and payment terms are difficult.”

Much more favourable

7%

Somewhat more

favourable16%

The same10%

Somewhat more difficult

43%

Much more difficult

24%

Howdoyouviewcurrentbusinessconditionsvs12monthsago?

Changes in the market as a result of lockdown have polarised the views of operators, depending on how the sectors they are most exposed to have responded to the pandemic.

⊳ Previous | 7 | Next page ⊲

Lookingattheoutlookforthelogisticssectoroverthenext12months,half(50.6%)ofthosesurveyedsaybusinessconditionswillbecomemoredifficult.

Whilethisissignificantlylowerthanthe62.0%whosaidthislastyear,theshareofcompaniesexpectingfuturemarketconditionstobe“muchmoredifficult”isclosetoahistorichigh,withlargercompaniesgenerallyexpectingthingstobetougherinthenext12monthscomparedtosmalleroperators.

However,the30.8%ofrespondentswhothinkbusinessconditionswillbemorefavourableisafifthhigherthanin2019,reflectingthepolarisingimpactofthecurrentenvironmentonthesector.

Intermsoftheimpactonturnover,justoverhalf(50.5%)forecastanincrease.Thisisanall-timelowandsignificantlybelowlastyear.The42.9%ofrespondentspredictingtheirturnoverwillfallismorethanaquarterhigherthanlastyear.

Operatorsaremorecautiousaroundexpectedprofitabilitythanturnover.Overall,thenumberofcompaniesexpectingprofitstodecreaseisatanunprecedentedlevelcomparedtooursurveysoverthelasteightyears,likelyreflectingtheirexposuretostrugglingend-usermarketsasaresultoftheimpactofCovid-19.Incontrasttotheirmorepositiveviewsonfuturemarketconditions,smallercompaniesalsogenerallyexpectabiggernegativeimpactonprofitthanlargerbusinesses.

Business outlook Operators’viewsaremixedonhowtheywillrespondtoachallengingenvironment.

Howdoyouforeseebusinessconditionsin12months’time?

The 30.8% of respondents who think business conditions will be more favourable is a fifth higher than in 2019, reflecting the polarising impact of the current environment on the sector.

0

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Much more

favourable

Somewhat more

favourable

The same

Somewhat more

difficult

Much more

difficult

Smaller Companies

Larger Companies

0

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

IncreaseNo changeDecrease

Smaller Companies

Larger Companies

Doyouexpectanincreaseordecreaseinprofitabilityin12months’timecomparedtopre-Covid-19levels?

⊳ Previous | 8 | Next page ⊲

Ofthoseoperatorsexpectingincreasedprofits,themajorityonlyanticipateanincreaseof2%to5%,andthenumberexpectingtoseeprofitsincreaseby10%ormoreissignificantlydownonlastyear,suggestingthateventhemoreoptimisticwillseeslowergrowthinprofitabilityfollowingthechallengesthisyear.

Investmentandheadcount

Respondents’viewsonlikelycapitalexpenditurereflectagreaterdegreeofcaution,withthoselikelyorverylikelytoinvestdownby5.6%thisyear.

Meanwhile,thenumberofcompaniesthatsaytheyexpecttoreduceheadcountisatanunprecedentedlevel.Morethanfouroutoftenrespondents(43.0%)expecttocuttheirheadcountinthenext12months.However,itisnoteworthythatamajorityarepredictingasmalldecreaseinheadcountratherthanmassredundancies.

Thesefindingsmostlikelyreflectgenerallylowerbusinessvolumes,staffreductionsthroughnaturalwastageandrecruitmentfreezes,ratherthanproductivitygainsandmayalsoindicategreateruseofshort-termcontractsandself-employeddriversoperatinginthegigeconomy.

Perhapsunsurprisingly,changesinheadcountareexpectedtobefeltmorebylargercompanies,whethernegativeorpositive,andsomeofthelargeroperatorsarecertainlyactivelyrecruiting,especiallytosupportB2Crelatede-commerceactivities.

DespiterisingUKunemploymentasaresultofthepandemic,manyfirms,particularlyinthesouth,areanecdotallyfacingseveredrivershortages,especiallyforlast-milework,inpartduetoaperceivedlackofavailableEUworkers.

Respondentcomment

“ We face unknown changes in 2021 but reduced demand is the biggest challenge.”

Howlikelyisitthatyourcompanywillmakesignificantcapitalexpenditureoverthenext12months?

Doyouexpectanincreaseordecreaseinheadcountin12months’timecomparedtoPre-Covid-19levels?

Unlikely

31%

Likely

37%

Very likely

32%

0%

5%

10%

15%

20%

25%

30%

Increas

e 10%

+

Increas

e 8-10

%

Increas

e 5-8

%

Increas

e 2-5

%

No chan

ge

(-2%

to +2

%)

Decrea

se 2-

5%

Decrea

se 5-8

%

Decrea

se 8-10

%

Decrea

se 10

% +

⊳ Previous | 9 | Next page ⊲

TheCovid-19crisisisundoubtedlythesinglemostsignificantfactoraffectinghowoperatorsperformedin2020,inonewayoranother.

Aroundthree-fifths(60.2%)ofrespondentsbelieveithashadanegativeeffectontheirbusinesses,whilejustoverathird(35.5%)suggestthattheimpacthasbeenpositive.Onceagain,thesefindingsmostlikelyreflectthevaryingfortunesofoperators’end-usermarkets.

Thevastmajorityofourrespondents(94.4%)havetakenadvantageofgovernment-fundedjobretentionschemesandstafffurloughstohelpthemthroughtheCovid-19crisis,whilesomefouroutof10(43.8%)havemaderedundancies.

However,theyhavemaderelativelylimiteduseofthegovernment’sCBILSandCLBILsbusinesscontinuationloanscomparedtoothersectors,withmanycompaniesreluctanttotakeonadditionaldebt.

Halfofsurveyrespondents(49.4%)havemadeuseofVATdeferrals,underliningtheimportanceofpreservingcashduringthepandemic.

Thesinglegreatestchallengeraisedbythepandemic,identifiedbyeightoutof10companies(80.6%),hasbeenmanagingchanginglevelsofcustomerdemand.Asignificant71.0%havefacedchallengesindealingwithlabourandpersonnelissues,and47.3%hadtotacklethedisruptiontotheircustomer’ssupplychains,whilealmost

athird(32.3%)ofrespondentshighlighteddisruptiontoshippinglinesandairfreight.

Regardlessofanyfinancialsupporttheyhaveutilisedsofar,thesechallengesarelikelytobeexacerbatedwhenfurloughschemesareeventuallywounddownanditremainstobeseenthroughout2021howoperatorswilladapttothegovernment’srevisedsupportmeasures,raisingthespectreoffurtherredundanciesandpossiblebusinessclosures.

Covid-19 impact Businessesareadaptingrapidlytotheunprecedentedchallengescreatedbythepandemic.

TowhatextentisCovid-19likelytoimpactyourcompany’sperformancein2020?

Operators have made relatively limited use of the government’s CBILS and CLBILs business continuation loans compared to other sectors, with many companies reluctant to take on additional debt.

Significant negative impact

21%

Slight negative impact

39%

No impact4%

Slight positive impact23%

Significant positive impact

13%

⊳ Previous | 10 | Next page ⊲

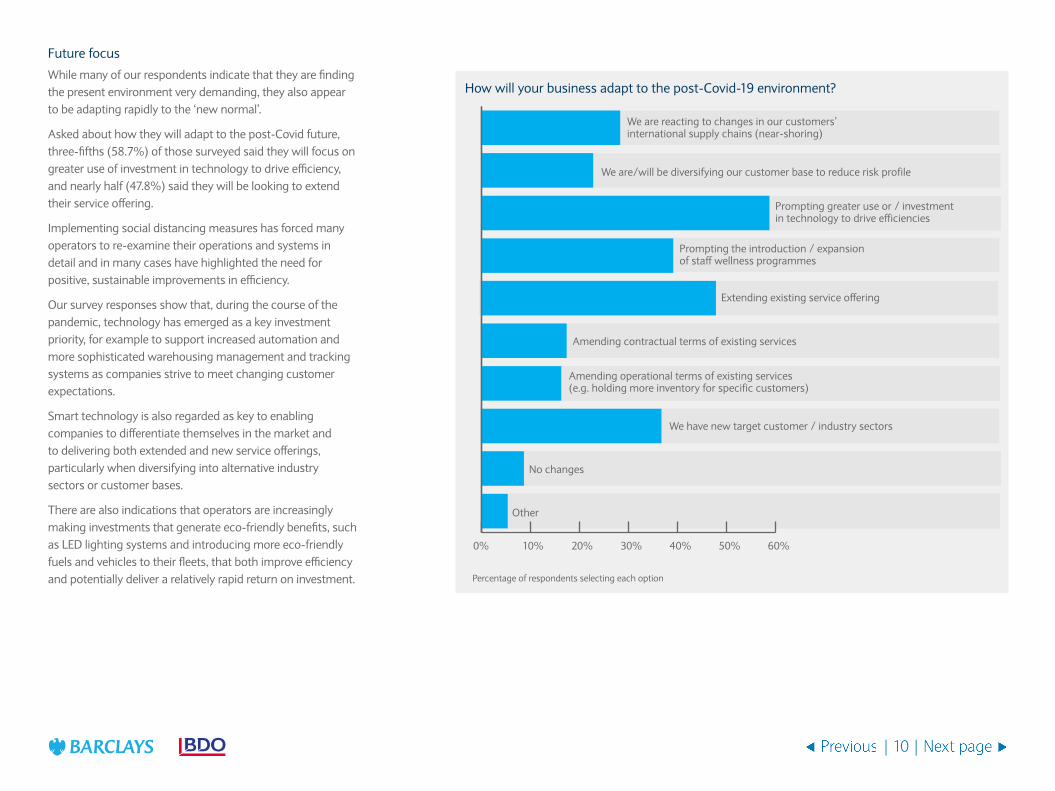

Futurefocus

Whilemanyofourrespondentsindicatethattheyarefindingthepresentenvironmentverydemanding,theyalsoappeartobeadaptingrapidlytothe‘newnormal’.

Askedabouthowtheywilladapttothepost-Covidfuture,three-fifths(58.7%)ofthosesurveyedsaidtheywillfocusongreateruseofinvestmentintechnologytodriveefficiency,andnearlyhalf(47.8%)saidtheywillbelookingtoextendtheirserviceoffering.

Implementingsocialdistancingmeasureshasforcedmanyoperatorstore-examinetheiroperationsandsystemsindetailandinmanycaseshavehighlightedtheneedforpositive,sustainableimprovementsinefficiency.

Oursurveyresponsesshowthat,duringthecourseofthepandemic,technologyhasemergedasakeyinvestmentpriority,forexampletosupportincreasedautomationandmoresophisticatedwarehousingmanagementandtrackingsystemsascompaniesstrivetomeetchangingcustomerexpectations.

Smarttechnologyisalsoregardedaskeytoenablingcompaniestodifferentiatethemselvesinthemarketandtodeliveringbothextendedandnewserviceofferings,particularlywhendiversifyingintoalternativeindustrysectorsorcustomerbases.

Therearealsoindicationsthatoperatorsareincreasinglymakinginvestmentsthatgenerateeco-friendlybenefits,suchasLEDlightingsystemsandintroducingmoreeco-friendlyfuelsandvehiclestotheirfleets,thatbothimproveefficiencyandpotentiallydeliverarelativelyrapidreturnoninvestment.

0% 10% 20% 30% 40% 50% 60%

Other

No changes

We have new target customer / industry sectors

Amending operational terms of existing services (e.g. holding more inventory for specific customers)

Amending contractual terms of existing services

Extending existing service offering

Prompting the introduction / expansion of staff wellness programmes

Prompting greater use or / investment in technology to drive efficiencies

We are/will be diversifying our customer base to reduce risk profile

We are reacting to changes in our customers’ international supply chains (near-shoring)

Howwillyourbusinessadapttothepost-Covid-19environment?

Percentageofrespondentsselectingeachoption

⊳ Previous | 11 | Next page ⊲

Respondentcomments

“ The biggest challenge is managing the costs and consequences of operating with safe social distancing and PPE.”

“ The Covid-19 crisis has had a significant impact on many sectors – automotive and aerospace have suffered, but pharmaceuticals are performing well and have a positive outlook.”

“ The supply chain is so fractured that demand for logistics solutions has increased.”

“ Business has grown as we were lucky enough to have a customer involved in PPE.”

Covid-19impactcontinued

⊳ Previous | 12 | Next page ⊲

Askedtoidentifythemostimportantissuefacingtheirbusinessinthenext12months,overaquarterofoperators(26.1%)saidtheimpactofBrexit,closelyfollowedbythe23.9%whoprioritiseddriverandskillsshortages,with19.6%mostconcernedovertheeconomicimpactontheirendcustomermarket.Ofcourse,itremainstobeseenwhatthelongertermimpactofthepandemicwillbeontheUKeconomyasgovernmentfinancialsupportforbusinessisgraduallywounddown,quiteapartfromhowthe

governmentrespondsinthefaceofmountingpublicborrowing.

Perhapssurprisingly,managinglengtheningpaymenttermsfromcustomerswasnotflaggedupasakeyconcern,althoughcopingwithcustomerpricepressurewasratedthebiggestissueby14.1%ofrespondents.ThismaysimplyreflecttherelativescaleoftheoverallCovid-19andBrexitchallengesfacingthesector.

Whatwillbethesinglemostimportantissuefacingyourbusinessinthenext12months?

Challenges and opportunities OperatorsarefocusingonBrexit,skillsshortagesandcostcontrol,whileeyeingnewopportunitiesemergingfromthepandemic.

Respondents’ priorities reflect the pressing need to tackle the ongoing threat of Covid-19, rather than business as usual concerns.

Perhaps surprisingly, managing lengthening payment terms from customers was not flagged up as a key concern.

Further industry consolidation

1%Shortage of warehouse

space4%

Investment in physical

infrastructure4%

Investment in technology

6%

Customer price pressure14%

Economic downturn

in your end customer

market20%

Driver/skills shortage

24%

Impact of Brexit26%

0%Other Lengthening payment terms from customersEmployee wage pressureCashflow/ Availability of finance

Percentagesgiventonearestwholenumber

⊳ Previous | 13 | Next page ⊲

Costcontrol

Lookingtothemoreimmediateareasoffocusforoperatorsoverthenextyear,respondents’prioritiesreflectthepressingneedtotackletheongoingthreatofCovid-19,ratherthanbusinessasusualconcerns.

Here,themajorityrankedcostcontrolastheirnumberonefocus,againreflectingtheneedtopreservecashflowintheshorttomediumterm,andtobuildtheirbusinessresilience.

Notably,maintainingtheexistingcustomerbasehasslippeddownthelistofoperators’prioritiesfromfirstplacelastyeartonumberfourthisyear,behindwinningnewcustomersandenteringnewindustrysectors,whichreflectsintentionsbymanyoperatorstodiversifytheircustomerbases.

Whatisthemainfocusforyourcompanyoverthenext12months?(Rankinorderofimportance,1=mostimportant,9=least)

21 3 4

5 6 7 8 9

Winningnewcustomers

Costcontrol Enteringnewindustrysectors

Maintainingexistingcustomerbase

Technologyinvestment

ManagingBrexit

Expansionofservices

Managingskillsshortage

Investinginsustainability

agenda

Maintaining the existing customer base has slipped down the list of operators’ priorities from first place last year to number four this year.

The majority ranked cost control as their number one focus.

⊳ Previous | 14 | Next page ⊲

Newbusinessopportunities

Morethanahalfofoperators(54.8%)saytheindustryofferingthebiggestbusinessopportunitiesin2021isonlineretail.Thisreflectsthecontinuingchangesinconsumerbuyinghabitsawayfrombricksandmortarstorestoonlinepurchasing,along-termtrendthathasbeenhugelyacceleratedbyCovid-19.Manyrespondentshighlightthesechanginge-commercetrendsanddemandfordeliveryofbasicnecessitiestohome-basedworkers,aswellasincreaseddemandforstoragespaceforonlinedeliveriesand,specifically,theroleofAmazon,askeydriversofnewbusinessopportunitiesinthesector.

Anotherkeyopportunityliesinthepharmaceutical/healthcaremarket,inpartbolsteredbyadditionaldemandformedicinesandmedicalequipmentduetothepandemic.AnumberofrespondentsidentifiedthedemandforPPEequipment,testingkitsandfuturevaccinationprogrammesasakeydriverfornewopportunitiesinthissector.

Foodretailisalsoseenasakeygrowthareabyrespondentsasitcontinuestobenefitfromstrengtheningdemandforhome-basedconsumptionoffoodanddrink,particularlyviaonlinechannels,andtheattractionsoftherelativelyrecession-proofperishablesmarket.

Manyrespondentshighlighttheneedforgreaterflexibilityintheirbusinessstrategiesandoperationsinordertocapitaliseonchangingend-usermarkets,althoughclearlythiswilloftenbeeasierforgeneralisthauliersand3PLs,thanforspecialistoperators.Atthesametime,whatonerespondentdescribesasa“fracturedsupplychain”,isincreasingdemandforinnovativelogisticssolutions.Managingthespeedofchangewillbeasignificanttestformany.

Respondentcomments

“ Customer buying habits have changed.”

“ High-yielding products that people cannot live without during Covid-19 are booming. Low-yielding products such as automotive are not.”

“ Building greater flexibility into business operations and capital exposure.”

“ Customers require higher levels of service, not just talk.”

“ Food has always been a more resilient sector that we continue to service. The growing trend of online retail and FMCG sectors we have seen continue.”

0

10%

20%

30%

40%

50%

60%

Food /

food retai

l

Foodse

rvice

/ HOREC

A

Bevera

ges

Tech

nology

Retail –

eCom

merc

e

Retail -

bricks

and m

ortar

FMCG

Pharmac

eutic

al / H

ealth

care

Industrial

/ M

anufac

turin

g

Constructi

on

Autom

otive

Whichindustriesprovidethegreatestnewbusinessopportunitiesforthelogisticsandtransportsectorin2021?

Percentageofrespondentsselectingeachoption

⊳ Previous | 15 | Next page ⊲

Unsurprisingly,concernsovertheimpactofUK/EUtradenegotiationsandtheendofthetransitionperiodremainfirmlyonoperators’minds,accordingtothisyear’sresearch,butappeartohavelessenedalittle,possiblybecausemoreoperatorsarebetterpreparedfornotradedeal.

Whilealmosthalf(47.9%)ofrespondentssaytheyexpecttodolessbusinesswithEUcustomersifthereisnotradedeal(seechartonthefollowingpage),thatissubstantiallyfewerthanthe62.4%whothoughtthatwouldbethecaselastyear.

Similarly,only17.8%oflogisticsfirmsbelievetheywilldomorebusinesswithEUcustomersifthereisnotradedeal,butthisfigureisstillanincreaseonthe10.6%ofrespondentswhofeltthatwouldbethecaselastyear.

Aroundathird(34.3%)felttherewouldbenochangeinEUbusiness,againmorethanthe27.1%whosaidthatin2019.

LookingatthepotentialforfacilitatingtradeoutsidetheEU,morethanaquarter(25.8%)ofrespondentsbelievetheywilldomorebusinesswithnon-EUcustomersunderano-dealscenario,3.1%morethanlastyear,while12.1%thinkbusinesswithnon-EUcustomerswilldecline,comparedtoafifth(19.7%)ofrespondentswhosharedthatviewayearago.

Inthescenariowhereatradedealisinplace,broadlyspeaking,themajorityofrespondentsfeelthatBrexitwillhavelessimpactontheirbusinesses,whethertradingwithEU,non-EUorUKcustomers.

Mixedresponses

CommentsfromoursurveyrespondentsreflectthetendencyofBrexittopolariseviews:rangingfrompredictionsofchaos,excessivepaperworkandhigherpricesforvehiclesandparts,topotentialnewopportunitiesasUKbusinessesadjusttheirsupplychainsandinventorylevelsandrequirenewlogisticsoperationstoservetheircustomers.

Anumberofrespondentsfocusontheincreasedpaperworkburdenthatwillimpactthesector,asbusinessestakestepstopreparefornewcustomsrequirements.

Again,itseemslikelythatoperators’responsesonBrexitareindicativeofthesectorstheyserve,butsomeseepotentialopportunitiesinofferingcustoms,advisoryandconsultancyservicesasaresultofchangestointernationaltradingagreements.

Brexit – next steps ContinueduncertaintyoverthetermsoftheUK’sfuturerelationshipwiththeEUisgeneratingbothoptimismandnervousness.

While almost half (47.9%) of respondents say they expect to do less business with EU customers if there is no trade deal, that is substantially fewer than the 62.4 % who thought that would be the case last year.

⊳ Previous | 16 | Next page ⊲

Respondentcomments

“ Customers struggling with understanding the impact on their business is creating a lot more work but also opportunities.”

“ There is still uncertainty among clients and hauliers as to what is expected from each party.”

“ It makes no difference. Only VAT/duty levels alter between the scenarios.”

“ We will lose deferment revenue but gain euro clearances.”

0% 20% 40% 60% 80% 100%

Less businessNo change

Impact on domestic business

Impact on non-EU/ROW business

Impact on EU business

More businees

Brexitimpact:whatwillbetheexpectedimpacttoyourcustomerbaseunderthefollowingend-of-transition-periodscenarios?

Deal is agreed

0% 20% 40% 60% 80% 100%

Less businessNo changeMore businees

Impact on domestic business

Impact on non-EU/ROW business

Impact on EU business

Leave transition with no deal

Brexit–nextstepscontinued

⊳ Previous | 17 | Next page ⊲

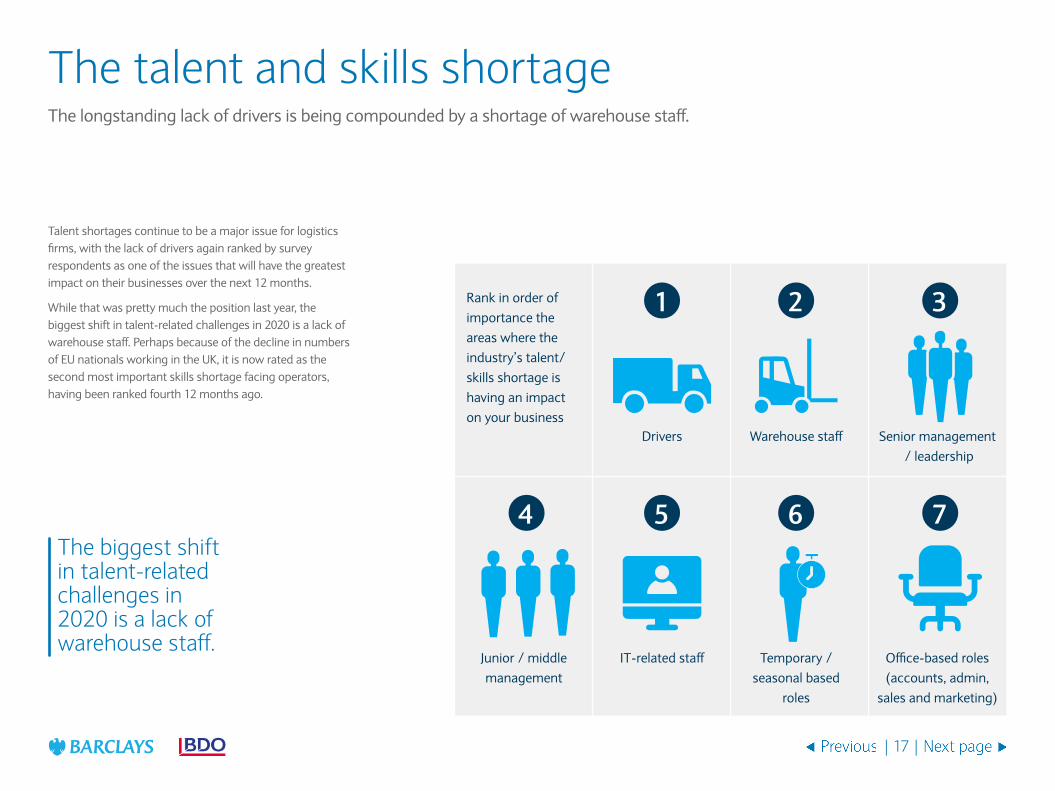

Talentshortagescontinuetobeamajorissueforlogisticsfirms,withthelackofdriversagainrankedbysurveyrespondentsasoneoftheissuesthatwillhavethegreatestimpactontheirbusinessesoverthenext12months.

Whilethatwasprettymuchthepositionlastyear,thebiggestshiftintalent-relatedchallengesin2020isalackofwarehousestaff.PerhapsbecauseofthedeclineinnumbersofEUnationalsworkingintheUK,itisnowratedasthesecondmostimportantskillsshortagefacingoperators,havingbeenrankedfourth12monthsago.

The talent and skills shortageThelongstandinglackofdriversisbeingcompoundedbyashortageofwarehousestaff.

The biggest shift in talent-related challenges in 2020 is a lack of warehouse staff.

1 2 3

4 5 6 7

Drivers Warehousestaff Seniormanagement/leadership

Junior/middlemanagement

IT-relatedstaff Temporary/seasonalbased

roles

Office-basedroles(accounts,admin,

salesandmarketing)

Rankinorderofimportancetheareaswheretheindustry’stalent/skillsshortageishavinganimpactonyourbusiness

⊳ Previous | 18 | Next page ⊲

Pluggingtheskillsgap

Themostpopularresponsetocounteracttheseshortages,accordingtoourrespondents,hasbeentoofferapprenticeshipsandtoworkwithyoungerpeopleinadrivetoaddresstheongoingproblemofattractingthemintothelogisticssector.However,despitenumerouseffortsbytheindustryandthegovernment’sapprenticeshipspush,therehasbeenalimitedtakeupofapprenticeshipstodate.

Thenextmostpopularcourseofactiontoresolveskillsshortagesamongrespondentsisimprovingpayandconditions,followedbyenhancingthequalityandleveloftraining.

Notably,justoverfouroutoftencompanies(42.2%)saytheyhaveusedsomeformoftechnologytoreplacehumantalent,asignificantjumpfromthe7.0%whosaidtheyhaddonethisin2019,whilearoundaquarter(25.6%)saytheyhavebeenusingmoretemporarystaffandsub-contractors.

Addressingthedrivershortagespecifically,somerespondentsindicatethattheyarediversifyingcareeropportunitiesforemployeesbytrainingtheirownnewdriversfor2021,ontopoftheadditionaldrivertrainingthatcertainoperatorsalreadyprovidetoimprovesafetyperformanceandreduceinsurancecosts.

Lookingatpotentialtechnologicalsolutions,18.0%ofrespondentssaytheyareactivelyexploringtheuseofdriverlesstrucks–orplatooning–asignificantincreaseonthe5.0%whosaidtheywerethinkingaboutthisin2019,eventhoughitappearsthetechnologyisstillsomewayfrompracticalapplication.

Despitenumerousattemptstoattractamorediversetalentpooltotheindustry,thisremainsastubbornlydifficultissuetocrackandonerespondentbemoansthefactthattheincreasedrecognitionforthesectorinkeepingsupermarketshelvesfilledduringthepandemic,andstaffbeingawarded‘keyworker’status,seemstohavebeenshort-lived.

Thewellnessfactor

Nearlytwo-thirdsofourrespondents(63.3%)saytheynowrunwellnessprogrammesforstaffand,encouragingly,theseappeartobeplayingsomepartinaddressingtheskillsandtalentshortage.

Ofthosewhoofferwellnessprogrammes79.3%saytheyhaveexperiencedreducedstaffabsenteeism,56.9%reporthigherproductivityandperformancefromemployees,andwelloverhalf(55.2%)sayithasledtopeoplestayingintheirjobsforlonger.

Thissuggeststhevalueofafocusonwellnessaspartofimprovingworkingconditionsinthesector,althoughitislesscleartowhatextentdriversmaybebenefitingfromtheseschemescomparedtootheremployees.

Respondentcomment

“ For a while, at the peak of the pandemic, the driver shortage was actually less of an issue but the situation deteriorated over the summer and is sluggish recovering.”

⊳ Previous | 19 | Next page ⊲

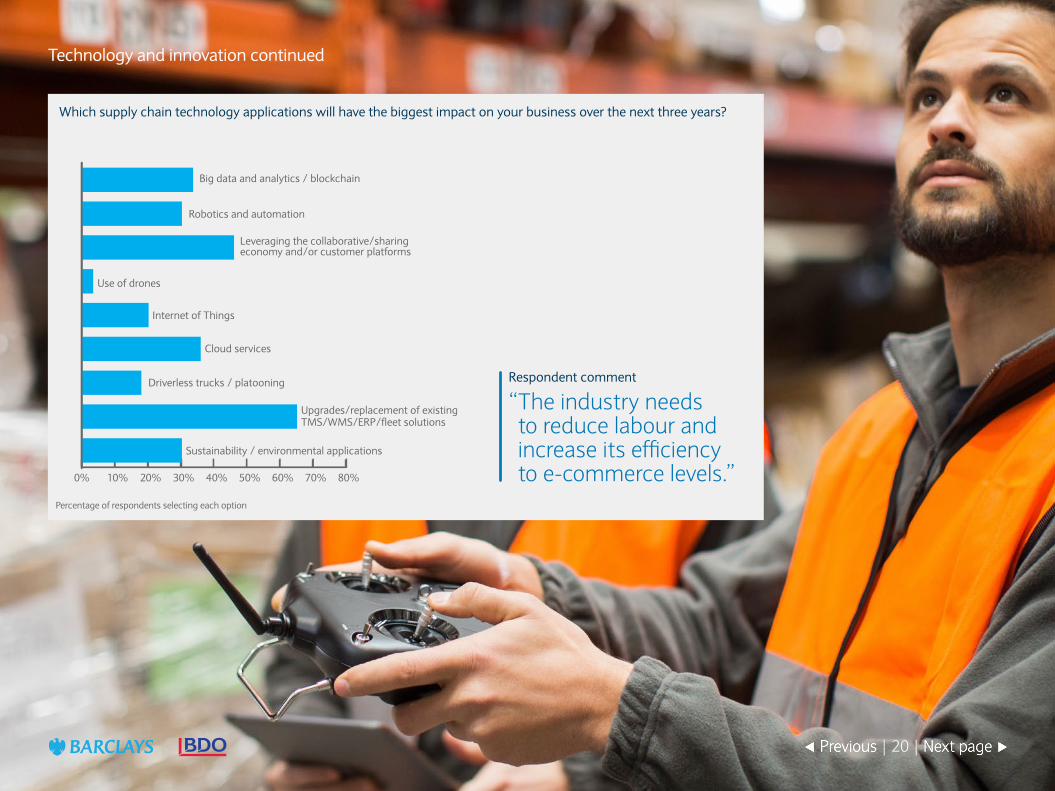

Whilenewtechnologycontinuestobeincreasinglyutilisedbythelogisticssector,updatingexistingsystemsandsolutionsisexpectedtobethepriorityforbusinessesoverthenextthreeyears.

Accordingtoourresearch,themainfocusofsometwo-thirdsofoperators(65.2%)isonreplacingandupgradingcurrentsystems,suchasthoseusedfortransportmanagement(TMS),warehousemanagement(WMS)andEnterpriseResourcePlanning(ERP),alongsideinvestinginnewapplications.However,overall,two-thirds(67.7%)ofrespondentssaytheywillconsiderinvestinginneworreplacementequipmentandtechnology,perhapsautomatingwarehousestotackleongoingskillsandlabourshortagesandincreaseefficiency,orcontinuingtoupgradevehiclefleets.

Nearlyhalfofrespondentssurveyed(46.1%)saytheyintendtoutilisethecollaborativeandsharingeconomyandcustomerrelationshipstointroducenewtechnologies.Thesecould,forexample,includeonlinefreightexchangesandotherplatformsthathelptomanagesub-contractorsanddeterminewhenandwhereloadsareavailable.

Almostathird(30.3%)ofoperatorssaytheyarelookingatroboticstechnologyandautomationduringthenextthreeyears,whichhasthepotentialtoreleaselower-skilledemployeestocarryouthigher-valuework.However,comparedto2019,slightlyfeweroperatorsexpecttousetechnologiestoreplaceoperationalwarehousestaffwithinthenextfiveyears,possiblyimplyingamorerealisticviewofthepaceofchange.

Therearesomesmallsignsofincreasinginterestintheuseofdronesinwarehouses,perhapstocarryoutinventoryworkusingscanningandbarcoding,whichisanticipatedtohaveanimpactbyjust3.4%ofoperators,butneverthelessanincreaseonthe1.0%predictingasignificantimpactlastyear.

Bigdata,analytics,blockchainandcloud-basedservicesareallexpectedtobeutilisedbymorethanathirdoffirms,whilethenumberofrespondentscitingthatsustainabilityandenvironmentalapplicationswillimpacttheirbusinesseshasrisenfromoneintenlastyearto30.3%in2020.

Technology and innovationInvestingintechandupgradingsystemsalreadyinuseremainsthepriorityformostfirms.

Compared to 2019, slightly fewer operators expect to use technologies to replace operational warehouse staff within the next five years.

⊳ Previous | 20 | Next page ⊲

Whichsupplychaintechnologyapplicationswillhavethebiggestimpactonyourbusinessoverthenextthreeyears?

3D printing 0%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Sustainability / environmental applications

Upgrades/replacement of existing TMS/WMS/ERP/fleet solutions

Driverless trucks / platooning

Cloud services

Internet of Things

Use of drones

Leveraging the collaborative/sharing economy and/or customer platforms

Robotics and automation

Big data and analytics / blockchain

Respondentcomment

“ The industry needs to reduce labour and increase its efficiency to e-commerce levels.”

Percentageofrespondentsselectingeachoption

Technologyandinnovationcontinued

⊳ Previous | 21 | Next page ⊲

Accordingtothisyear’sstudy,morethansevenoutoftencompanies(72.2%)willbeinvestingingreen-relatedprojectsconnectedwithsustainabilityandtheenvironmentoverthenext12months–roughlythesameaslastyear.

Thetop‘green’focusareasidentifiedbyrespondentsareoptimisingfuelusedbyexistingfleets,recyclinginitiatives,warehouse-relatedimprovementssuchasinstallingLEDlighting,andintroducingandexpandingalternativeenergyvehiclefleetsinresponsetoincreasingnumbersofcitycleanairzoneswhichimposeachargeonnon-compliantvehicles.

Eachoftheseinitiatives–withthepossibleexceptionofrecycling–hasthepotentialtobeacost-saverinthelongterm,illustratingthatsustainabilityprojectscanplayapartinhelpingcompaniestomanagetheircosts.Greeninitiativesarelikelytobeamajordriverofcapitalexpendituregoingforward.

Whiletherearerelativelysmallnumbersofsustainablevehiclesoperatinginfleetscurrently,changestovehicletaxation,thephasingoutofdieselenginesandintroductionofnewlow-emissionzonesarelikelytocontinuetoincentiviseoperatorstoreplaceolder,less-sustainablevehiclesbeforetheyeffectivelybecomeworthless.

TheCovidfactor

TurningtotheimpactofCovid-19ondeliveringenvironmentalinvestment,ourresearchshowsthatthepandemichasn’timpactedinvestmentingreenprojectsforthevastmajorityofcompanies.

Nevertheless,aroundathirdofrespondents(34.8%)saythepandemichasinterfered,negatively,withinvestmentintheirgreenagenda,asenvironmentalinitiativeshavebeendelayedorbudgetscut.Thismaybeperhapsduetodifficultiesinaccessingthenecessaryexpertiseandmaterialstoimplementenvironmentalprojectsduringthepandemic.

Respondentcomment

“ Availability of contractors to upgrade lighting etc has been challenging.”

Green initiativesCovidhasbeenadistractionbuthasnotdampenedinvestmentinsustainability.

Our research shows that the pandemic hasn’t impacted investment in green projects for the vast majority of companies.

Whatarethekeyfocusareasforyourcompany’senvironmentalinitiatives?

0 10 20 30 40 50 60 70 80

Other

Extending environmental initiatives to suppliers / sub-contractors

Meeting customer-enforced environmental targets

Utilising technology to drive environmental objectives

Procurement initiatives

Recycling initiatives

Warehouse initiatives (lighting, power etc)

Expanding number of alternative energy vehicles

Optimising fuel existing fleet

%

Percentageofrespondentsselectingeachoption

⊳ Previous | 22 | Next page ⊲

Thisyearthenumberofcompaniesexpectingtomakeacquisitionsisclosetotheall-timehighfortheindexin2017,with38.9%ofrespondentssayingtheyarelikelytomakeanacquisitionwithinthenext12months.

Reversingtheslightdipinpredictedacquisitionswesawin2019andtherecentmutedactivityduetoCovid-19andtheeconomicuncertainty,thisyear’sincreaseappearstoreflecttheambitionsofwell-financedcompaniesseekingeconomiesofscaleandthechancetomakeopportunisticbuysinatoughenvironment.

Asoperatorslooktoreducecostsanddriveupmargins,otherdriversfordealactivityincludeexpandingserviceofferingstoreflectthechangestobothconsumerspendingbehaviourandend-usermarketsthathavebeenacceleratedbyCovid-19.Companiesmaylooktoboltonmorevalue-addedservicestoimprovemargins,suchasproductassembly,processingreverselogistics,productreconditioningandend-of-lifewastemanagement.

Refinancingofover-leveragedoperatorsthatarestrugglinginthecurrenttoughenvironmentseemslikely,andthereisanexpectationthatmoredistressedassetswillcometomarket,givenmountingpressureasfurloughingandothergovernmentfinancialsupportends.

RecentexamplesofdealactivityincludeXPO’sproposedacquisitionofKuehne+NagelDrinksflowLogistics(subjecttoregulatoryapproval),Culina’sPurchaseofFowlerWelch,andthedisposalofTufnellsbyConnectgroupinH12020,allof

whichhighlightthevalueofconsolidation,scaleandmarketleadership.Meanwhile,theacquisitionofHermesParcelnetandHermesGermanybyAdventInternationalhighlightstheavailabilityandappetiteofinvestmentcapitaltoseekoutvalueandgrowth.

Mergers and acquisitionsWithpredictedM&Aactivityatitshighestlevelsince2017furtherconsolidationinthesectorlookslikely.

Companies may look to bolt on more value-added services to improve margins.

0%

10%

20%

30%

40%

50%

60%

70%

80% No, we are unlikely to make an acquisition(s)

Yes, we are likely to make an acquisition(s)

H2, 201

6201

7201

8201

9202

0

H1, 201

6

H2, 201

5

H2, 201

4

H1, 201

5

H2, 201

3

Areyoulikelytomakeanyacquisitionsoverthenext12monthsandwhatisthemaindrivebehindthis?

⊳ Previous | 23 | Next page ⊲

0% 5% 10% 15% 20% 25% 30% 35%

To achieve higher margins

Expansion of service offering

To achieve economies of scale

Gain access to specific customers

To enter a new sector

ForthoseundertakingM&Aactivity,whatarethedrivers?

Mergersandacquisitionscontinued This year’s increase appears to reflect the ambitions of well-financed companies seeking economies of scale and the chance to make opportunistic buys in a tough environment.

⊳ Previous | 24 | Next page ⊲

Thelogisticssectorisexperiencingasignificantshift:inhowbusinessisbeingdone,indemand,capacity,routingandmeansoftransportation.Tradelaneshavebeenshakenbytheextremepressuresplacedonthem,buttherearealsogreatopportunitiesforsupplychaincompanieswithvisiontoadapt,developandgrowinthisnewenvironment.

Weexpectcontinuedgrowthinfreightvolumesin2021asproductionofgoodscontinuestoimprove.Highdemandandlowcapacityislikelytodriveincreasedcosts,whileregulatoryissuesandthechallengessurroundingUK/EUandUS/Chinatradelaneswillremain.E-commerceandlastmileconsumerdeliveryexpectationswillcontinuetoimpactfreightcosts,availabilityanddrivedemandforlogisticsfacilities.Servicelevelswillbemoreandmoreimportant,withexpertise,localknowledge,globalreachandapersonalapproachbeingparamount.

Respondingtothepandemic

AtWoodlandGroupwe’veseenanumberofchallengesimpactthesupplychainindustryworldwideasaresultofthepandemic.

WithFCLshippinghavingprovedaconcerntobusinessesduetotheeconomicclimateoverthelast10months,we’veseenincreaseddemandforbespokeLCLsolutionsandhaveputinplaceanExpressLCLsolution.

We’vealsoseenahugeimpactonairfreight,puttingincreasedpressureonrates,andonfreightercapacitybetweenEuropeandtheUS,andoutboundfromChina.Asaresult,we’vereroutedsomeairfreighttoalternativeairportsorofferedair/sea(andrail)combinationoptionsfurtherafield.

Withwarehousingfacilitiesatornearfullutilisationlevelsduetolackofmovementoffreight,we’veprovidedservicessuchas“DelayInTransit”solutionsforgoodsatornearthepointofmanufacture,aswellasprovidingoverflowstoragearrangements.

ThisisontopofthechallengesofshortagesofdriversandessentialworkersduetoCOVID-19,especiallyintheUS;changestoimporttariffs;containershortagesandcongestionatportsacrosstheworld;theneedtoadjusttothevastarrayofnewguidelinesandregulationsglobally,particularlyaroundimportingPPE;andnewtradeagreementsandmodelscurrentlybeingimplementedand/orpreparedfor.

Staffwelfare

AtWoodlandGroup,wehavealsohadtoquicklyadaptourITsystemstoremoteworking,whilekeepingcustomerdataprotected,andimplementingnew‘Covid-19secure’workingpoliciesandprocedurestokeepourteamssafe.

We’vefocusedondevelopingalternativeinternalcommunicationtoolsandplatformstocounteractthelackofinteractionofteamsduetoremoteworking.Wenowhostregularcompany-widevideoconferencestobringallstafftogetherglobally,whichisakeylearningforthefutureintermsofinteractionandmotivationacrossthebusiness.

We’vealsoincreasedthenumberofin-housetrainingcoursestobetterpreparestafftocopewiththechallengesofthecurrentclimate,includingonmentalhealthawareness,andwe’reworkinghardtoputsupportstructuresinplacetoaidourstaffandtheirfamiliesthroughthesechallenges.

Industry insight: Finding the right solutions to adapt and growJohnStubbings,CompanySecretaryofWoodlandGroupandcurrentChairofBIFA,reflectsonarapidlychangingsupplychainindustry.

⊳ Previous | 25 | Next page ⊲

Futureopportunities

Digitisationiscontinuingtotransformthesupplychainindustry,whichhastraditionallybeenbuiltonpersonalinteractionandrelationships.WoodlandGrouphavebeeninvestinginanumberofdigitalsolutionsovertheyearstoprovideagile,trackableandcarbonconscioussolutionstoourclients.

Fromreducinginefficienciesandtheindustry’sundeniableenvironmentalimpacttohighlightingsupplychaindeficienciesandopportunities,deliveringabettercustomerexperience,communicationflowandincreasedtransparencyoftheentiresupplychain,ourdigitaldevelopmentandfocusondataanalysisarekey.Theyenableustobetterforecastandprotectourcustomers'supplychainsandsupportourexpertteamsinmeetingourclients’needs.

DealingwithBrexit

Weputalotofworkintopreparingforandquicklyadaptingtopoliticalandeconomicshiftsthatimpactthemovementofgoods,whethernationallyorinternationally.ThishasincludedimplementingstepstoprepareandguideourclientsthroughthenewregulationsthatneedtobeconsideredaroundtheUKtransition.

OurdedicatedcustomsspecialistsarepartofBIFA’sCustomsPolicyGroupandCustomsPractitionersGroupandhavebeenguidingourbusinessinprovidingsupportsolutionstoourclients.

We’vecreateddedicatedBrexitnewsreelscommunicatingtheinformationreceivedfromBIFA,thegovernmentandourcontactsinBrussels,includingsimplifiedliteraturetohelpcustomersbecomeBrexitready.ThroughourITsolutionswe’reabletoload-bearallourclearanceneedsacrossthecompanywithintheUKona24/7basis.

Wecontinuetoprovidetrainingforallstaffonchangesfrom1January2021onwardsandonhowtobestsupportourclients,andhavekeypartnersacrossEuropethatcanaidusandourclientswithanyproblemsthatmayarisewhilstintransitfrom1January2021onwards.

We’reworkingwithallofourhaulierstomakesurethey’reuptospeedwiththenewregulationsandprocessesfortravellingacrosstheUK/EUborderandtomakesurealldriverscarryingourgoodshavethecorrectpaperwork.

Widerchallenges

Ourindustryneedstobemoreinnovativeinaddressingthedrivershortage.Weneedtoconsidertrainingtalentfromwithinourexistingwarehouseteams–afterall,today’sFLToperatorcouldbetomorrow’sLGVorHGVdriver.Wealsoneedtoimprovethesector’simage,workinghoursandthequalityofdriverfacilities.

Theindustryundeniablyhasasignificantimpactontheenvironmentandisoneoftheleadingindustriesshapingtheuseoftechnologyanddigitaladvancement.Providingsolutionstoreduceenvironmentalimpacthasbeenakeyfocusforusandwillcontinuetogrowinimportanceinthefuture.

It’sfantastictoseethedevelopmentofgreenerandmorecarbonconscioussolutionsacrossports,somecarriersandfellowfreightforwarders.Thekeytothisisacollective,industry-wideapproachandagreementonsomeofthekeyissuesaffectingourenvironmentalimpactandwe’realreadyworkingwithanumberofourpartnersonthis.

Meanwhile,globalisationwillcontinuetodriveconsolidation.Demandforfullyintegratedserviceprovidersandglobalcoverage,andincreasingcompetition,willcontinuetopushorganisationstowardsconsolidation.

John StubbingsCompanySecretaryofWoodlandGroupwww.woodlandgroup.com

We put a lot of work into preparing for and quickly adapting to political and economic shifts that impact the movement of goods, whether nationally or internationally.

⊳ Previous | 26 | Next page ⊲

Industry insight: Opportunities opening up for agile operatorsClaireWebb,ManagingDirectorofgloballogisticssolutionsproviderAdvancedSupplyChainGroup(ASCG),discusseshowagilityiskeytothrivingintoday’sdemandingenvironment.

It’sfairtosaythatsupplychainmanagementhaschangedforeverthankstoCovid-19anditseffectonlogisticsoperatorsandtheircustomers.

EnsuringthewellbeingofemployeesandestablishingCovid-safeworkpracticeshasbeenapriorityofcourse,butsohasovercomingoperationalchallengestodeliverbusinesscontinuityforcustomers.

Thearrivalofthepandemicandanunrelentingshifttowardsonlinepurchasinghasbeenchallengingbutalsocreatedopportunities,particularlyine-commerceandmulti-channelmarkets.

Understandably,retailersarelookingtobuildresilience,flexibilityandintelligenceintotheirsupplychains.Thiscreatesopeningsforagilelogisticsoperatorswithafocusontechnologythatcangivecustomersreal-timevisibilityandinsightsintohowtheirsupplychainisworking,andenablethemtoscaleupordowninlinewithdemand.

Understandingchangingcustomer–andconsumer–needsandbeingnimbleenoughtorespondareabsolutelykeytothrivinginthishostileenvironment.Operatorswhoareheavilyautomated,withcumbersomelegacyinfrastructure,willstruggletoevolveagainstsuchafast-movingbackdrop.

Softwaresolutions

Asacompany,weofferacomprehensiverangeofspecialistsupplychainservices,atbothoriginanddestinationthroughaglobalnetworkofwhollyownedsitesintheUK,EuropeandAsia,andthroughestablishedpartnershipsinothergeographies.

Formorethanadecadewe’vebeeninvestingindesigninganddevelopingourownbespoke,technology-ledlogisticssolutionsthatprovedinvaluablewhenCovid-19hit.OurVectormodularwarehousemanagementsoftwaresystemconnectsallourUKsitesandanumberoverseastoofferseamlesslinkswithourcustomers’ownsystems,givingthema‘controltowerview’ofstockandendvisibilityoforders.

GiventheCovid-acceleratedchangestoshoppingbehaviours,investinginintelligenttechnologylikethispotentiallyoffersgreatopportunitiesforoperatorsandtheircustomers.

Understandingcustomerneeds

Ofcourse,withthepandemic,operatorshaveneededtotakestepstounderstandthechallengestheircustomersface,notleasttheheavyincreasesinfreightforwardingcharges.That’swhywerecentlycarriedoutasurveyof200seniorretailprofessionalsforawhitepaperlookingatthekeydriversofchangeforthesector.

Itrevealedthepandemiccausedstockmanagementissuesfor92%ofretailersandhasunderminedconfidenceinJustInTime(JIT)becauseitdoesn’tprovideenoughagilitytocopewithincreasingunpredictability.

Disruptionmeanttwothirdsofretailersreceivedstocklateandasimilarnumberexperiencedshortagesofgoods.Retailersidentifiedbalancingstockflowandstockpilingasthebiggestsupplychainchallengeasaresultofthepandemic,with57%investinginstockavailabilitysolutions,andasubstantialproportionrecognisingthatrealtimevisibilityplaysavitalpartinenhancingsupplychainresilience.

Takemanagingreturns,forexample;weknowconsumerswantreturnstobeaseffortlessandpainlessaspossible,whichmeansreverselogisticsisnowapivotalpartofthesupplychainandaninvestmentthatwillpayoff.

Logisticsoperatorsthereforeneedtobelookingtoutiliseuser-friendlytechnologies–suchaspaperlessreturns–thatprovideintelligentreturnsolutionswithgoodvisibilityofwhat’scomingintohelpcustomersmaximisetheiravailabilityofstock,keepwrite-offslowandgetproductsbackintoavailablestockasmarginscomeunderpressure.

⊳ Previous | 27 | Next page ⊲

Technologyandtalent

Investmentinnewtechacrossthesectorhastendedtofocusonincreasedautomation,whichmakessensefor‘bigbox’single-usesites,butoperatorsofmulti-usersitesactuallyneedpeople,ratherthanrigidautomation,toenablethemtoprovideretailersandsupplierswithmoreflexibleservicesandscaleupordownwithdemand.

Webelievethewaytoachievegreateragilityistouseintelligent,user-friendlytechnologythatenablespeopletobecomecompetentmorequickly,dotheirjobsfasterandmoreefficiently–ratherthanreplacethem.

Andwhileitseemsthesectorisfacingtalentshortages,particularlyinwarehouses,thishasn’tbeenourexperienceandit’sworthnotingthere’sagrowingleveloftalentemergingfromtroubledsectorslikehospitalityandleisureandlookingtoretrain.So,withastrongdevelopmentandtrainingplanitshouldbepossibletobridgeanygaps.

Thenearfuture

AsweneartheendoftheBrexittransitionperiod,it’sdifficulttoascertainwhatimpactthefinaloutcomewillhaveonthesector.

However,we’llbemakingtransitionthroughcustomsassimpleaspossibleforourcustomers,enablingthemto‘fast-track’throughthesystem.ThiswillbeachievedwiththeAuthorisedEconomicOperator(AEO)statuswealreadyhave,byintroducingCustomsFreightSimplifiedProcedures(CSFP)anddesignatingwarehouseswithExternalTemporaryStorageFacility(ETSF)statustoeffectivelyactasaportforcustomspurposes.WehavealsoestablishedoperationsintheCzechRepublicandMiddleEasttooffercustomersalternatesupplylines.

IrrespectiveofBrexit,itseemsfurtherconsolidationintheindustryisinevitable.Businesseswillneedtokeepaheadofthecurveandacquiretheexpertisetheydon’thavein-housetoenhancetheirflexibility,covermoresectorsandchannels,andpositionthemselvesforgrowth.

Thiscouldwellbethroughacquisition,astherewillbedistressedbusinessesupforsale,butalsojustaslikelythroughpartnershipsandcollaboration.

Overthecomingyearlogisticsisgoingtobeaveryinterestinganddemandingsectorthatwillundoubtedlyseeoperatorsinvestinginarangeofdifferentsolutionstogivetheircustomersacompetitiveadvantageaswealladapttotheevolvinglandscape.

Claire WebbManagingDirectorofgloballogisticssolutionsproviderAdvancedSupplyChainGroup(ASCG)

www.advancedsupplychain.com

It’s worth noting there’s a growing level of talent emerging from troubled sectors like hospitality and leisure and looking to retrain. So, with a strong development and training plan it should be possible to bridge any gaps.

⊳ Previous | 28 | Next page ⊲

( Our Confidence Index has fallen from 49.7 in 2019 to 47.1 this year, its lowest-ever level and the second year running it has dipped below 50.

( Two-thirds (67.1%) of respondents say current business conditions have become tougher in the past 12 months.

( While half of respondents (50.6%) think business conditions will get more difficult in the year ahead, and fewer than half (48.9%) think profits will be up, many still see opportunities to grow revenues by focusing on the changing supply chain, the growth of e-commerce and delivering value-added services.

( Three-fifths (60.2%) of those surveyed say Covid-19 had a negative effect on their business in 2020 – a dramatic and distorting factor as businesses enter a period of adjustment and adapt to new service lines and end markets.

( There is a high degree of polarisation in the views of operators, with 35.5% saying the pandemic has had a positive impact on their company’s performance, despite the economic disruption.

( In addition to the pandemic, operators think the biggest challenges over the next 12 months will be driver shortages, Brexit and cost control.

( The long-standing shortage of drivers is being compounded by a lack of warehouse staff but employers also report that their wellness programmes are having positive effects on overall staff productivity, retention and absenteeism.

( System upgrades remain the main technology focus, but the sector has a growing appetite for investing in automation and other enabling technologies.

( More than 7 out of 10 businesses (72.2%) say they will be investing in sustainable, environmental or ‘green’ projects in the next 12 months.

( Predicted M&A activity over the next 12 months is at a level only just below the all-time high for the index in 2017.

Key takeaways

⊳ Previous | 29 | Next page ⊲

About this reportAllfiguresanddatarelatingtotheUKLogisticsConfidenceIndexwithinthisreporthavebeenresearchedbyAnalytiqa.

Theindexcalculationisbasedontheproportionofrespondentsreportingeitheranimprovement,nochangeordeteriorationwithinthesector,scoredfrom0to100.Therefore,anumberover50indicatesanimprovement,whilebelow50suggestsadecline.Thefurtherawayfrom50theindexis,thestrongerthechangeovertheperiod.

Thetotalcombinedrevenueofthecompaniesincludedinoursurveythisyearis£16.4bn,accordingtothelatestcompanyaccountsavailable.

Wewouldliketothankour100-plussurveyrespondentsfortheirgreatlyvaluedinsightandloyalty.Halfofthemhavenowparticipatedin10ormoreofour13reports,providinguswithvaluableconsistencyofparticipation.

Analytiqa

⊳ Previous | 30 | Next page ⊲

JasonWhitworth

Partner, M&A Advisory and Logistics & Supply Chain Management, BDO LLP

JasonisaPartnerinBDO’sCorporateFinanceadvisoryteamandhasextensiveexperienceacrosstheLogisticsandSupplyChainManagementSector.

Hehasmorethan20years’experienceleadingcorporatefinancetransactionsandasuccessfultrackrecordincompletingnumerousmid-marketdeals,includingMBOs,salemandates,acquisitions,privateequity,debtfundraising,andstrategicadviceacrossawiderangeofendmarkets.

Jasonhasworkedwithabroadclientbase,bothUK-basedandglobal,acrossawiderangeofsectorbusinesses,includingroadhaulage,warehousing,fulfilment,palletisedfreight,freightforwarding,couriertransport,andlogisticstechnologyandautomation.

Jasonproducesregularupdatesandreportsforthesector,providinganalysisofthekeytrendsthataredrivingvalueinthemarket.

T:+44(0)1132041237E:[email protected]

IanCranidge

Relationship Director, Head of Transport and Logistics, Barclays UK Corporate Banking

IanheadsuptheTransportandLogisticsSectorforBarclays’UKCorporateBank,providingexpertisewhichhelpsshapethebank’soutlookonthesector.

Heprovidesclientswithaccesstothebank’sfullsuiteofproductsandsolutions,includingbutnotlimitedtocashmanagement,debtfinancing,foreignexchangeandinvestmentbanking.

IanhasbeenwithBarclayssince2002,joiningoriginallyasaLocalRelationshipmanagerinEastLondon.

Inhis18-plusyearswiththebankhiscareerhasincludedrolesinLargeCorporateBankingcoveringpowerutilitiesandinfrastructure,leveragedfinance,asset-basedlendingandoffshorebankinginLondonandNewYork.

T:+44(0)2071167204E:[email protected]

About the authors

IDEAS | PEOPLE | TRUST

barclayscorporate.com

@BarclaysCorp

Barclays Corporate Banking

www.bdo.co.uk

@bdoaccountant

BDO UK LLP

BarclaysBarclaysBankPLCisregisteredinEngland(CompanyNo.1026167)withitsregisteredofficeat1ChurchillPlace,LondonE145HP.BarclaysBankPLCisauthorisedbythePrudentialRegulationAuthority,andregulatedbytheFinancialConductAuthority(FinancialServicesRegisterNo.122702)andthePrudentialRegulationAuthority.BarclaysisatradingnameandtrademarkofBarclaysPLCanditssubsidiaries.

Theviewsexpressedinanyarticlesaretheviewsoftheauthoralone,anddonotnecessarilyreflecttheviewsoftheBarclaysBankPLCGroupnorshouldtheybetakenasstatementsofpolicyorintentoftheBarclaysBankPLCGroup.TheBarclaysBankPLCGrouptakesnoresponsibilityfortheveracityofinformationcontainedinthethirdpartyguidesorarticlesandnowarrantiesorundertakingsofanykind,whetherexpressorimplied,regardingtheaccuracyorcompletenessoftheinformationgiven.TheBarclaysBankPLCGrouptakesnoliabilityfortheimpactofanydecisionsmadebasedoninformationcontainedandviewsexpressed.

BDOThispublicationhasbeencarefullyprepared,butithasbeenwritteningeneraltermsandshouldbeseenascontainingbroadstatementsonly.Thispublicationshouldnotbeusedorreliedupontocoverspecificsituationsandyoushouldnotact,orrefrainfromacting,upontheinformationcontainedinthispublicationwithoutobtainingspecificprofessionaladvice.PleasecontactBDOLLPtodiscussthesemattersinthecontextofyourparticularcircumstances.BDOLLP,itspartners,employeesandagentsdonotacceptorassumeanyresponsibilityordutyofcareinrespectofanyuseoforrelianceonthispublication,andwilldenyanyliabilityforanylossarisingfromanyactiontakenornottakenordecisionmadebyanyoneinrelianceonthispublicationoranypartofit.Anyuseofthispublicationorrelianceonitforanypurposeorinanycontextisthereforeatyourownrisk,withoutanyrightofrecourseagainstBDOLLPoranyofitspartners,employeesoragents.

BDOLLP,aUKlimitedliabilitypartnershipregisteredinEnglandandWalesundernumberOC305127,isamemberofBDOInternationalLimited,aUKcompanylimitedbyguarantee,andformspartoftheinternationalBDOnetworkofindependentmemberfirms.Alistofmembers’namesisopentoinspectionatourregisteredoffice,55BakerStreet,LondonW1U7EU.BDOLLPisauthorisedandregulatedbytheFinancialConductAuthoritytoconductinvestmentbusiness.BDOisthebrandnameoftheBDOnetworkandforeachoftheBDOmemberfirms.BDONorthernIreland,apartnershipformedinandunderthelawsofNorthernIreland,islicensedtooperatewithintheinternationalBDOnetworkofindependentmemberfirms.

Copyright©November2020BDOLLP.Allrightsreserved.PublishedintheUK.