The Trend of Cargo and Container Movements Between · PDF filein ASEAN Countries and Pacific...

30

Soteri Gatera Senior Economic Affairs Officer [email protected] Seminar on Development of an Integrated Transport and Logistics System in ASEAN Countries and Pacific Sub-region. Bangkok, 21 – 23 November 2012 The Trend of Cargo and Container Movements Between ASEAN Countries and Africa: An overview

Transcript of The Trend of Cargo and Container Movements Between · PDF filein ASEAN Countries and Pacific...

Soteri GateraSenior Economic Affairs Officer

Seminar on Development of an Integrated Transport and Logistics System in ASEAN Countries and Pacific Sub-region.

Bangkok, 21 – 23 November 2012

The Trend of Cargo and Container Movements Between ASEAN Countries and Africa:

An overview

Presentation Outline

• SSA’s Macroeconomic Conditions• Asia – Africa Trade Trends• World Seaborne Trade: Forecast Trend• Shipping Containers in Africa• Eastern & Southern Africa: Ports and

Market coverage• Regional approach to Challenges

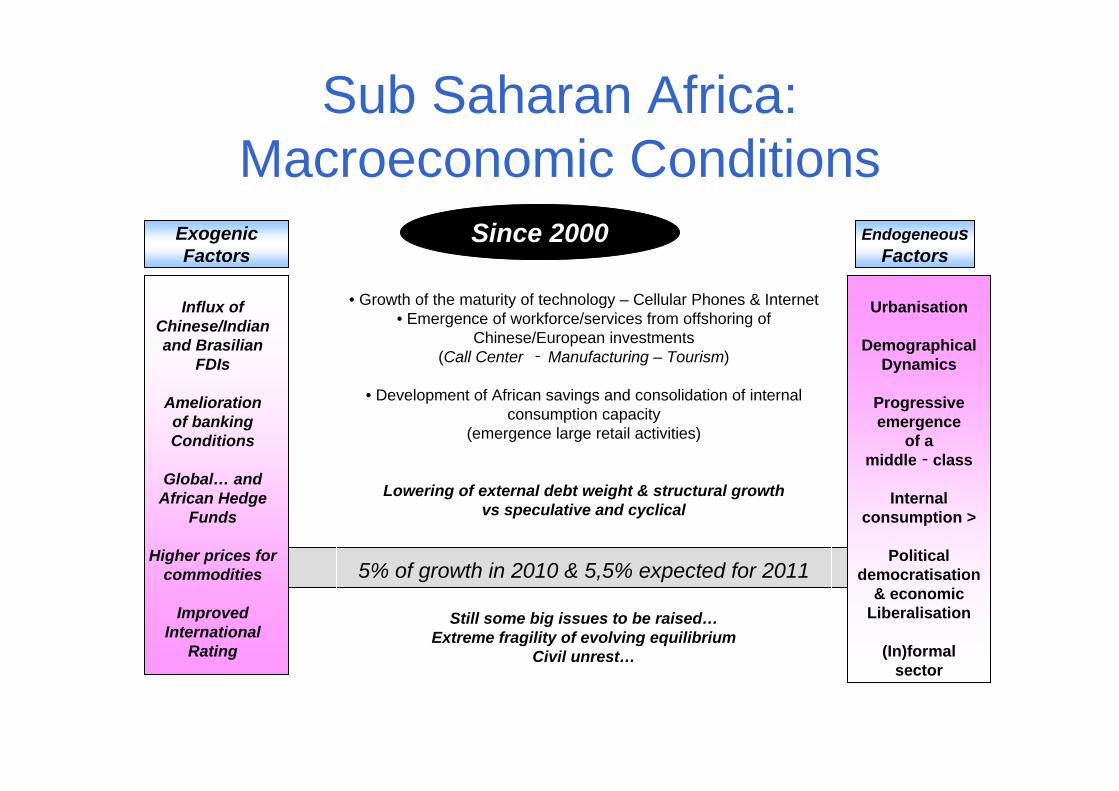

Sub Saharan Africa: Macroeconomic Conditions

EndogeneousFactors

Influx ofChinese/Indianand Brasilian

FDIs

Ameliorationof bankingConditions

Global… andAfrican Hedge

Funds

Higher prices forcommodities

ImprovedInternational

Rating

• Growth of the maturity of technology – Cellular Phones & Internet • Emergence of workforce/services from offshoring of

Chinese/European investments(Call Center ‐ Manufacturing – Tourism)

• Development of African savings and consolidation of internalconsumption capacity

(emergence large retail activities)

Lowering of external debt weight & structural growthvs speculative and cyclical

5% of growth in 2010 & 5,5% expected for 2011

Still some big issues to be raised…Extreme fragility of evolving equilibrium

Civil unrest…

Urbanisation

DemographicalDynamics

Progressiveemergence

of a middle‐class

Internalconsumption >

Politicaldemocratisation

& economicLiberalisation

(In)formalsector

ExogenicFactors

Since 2000

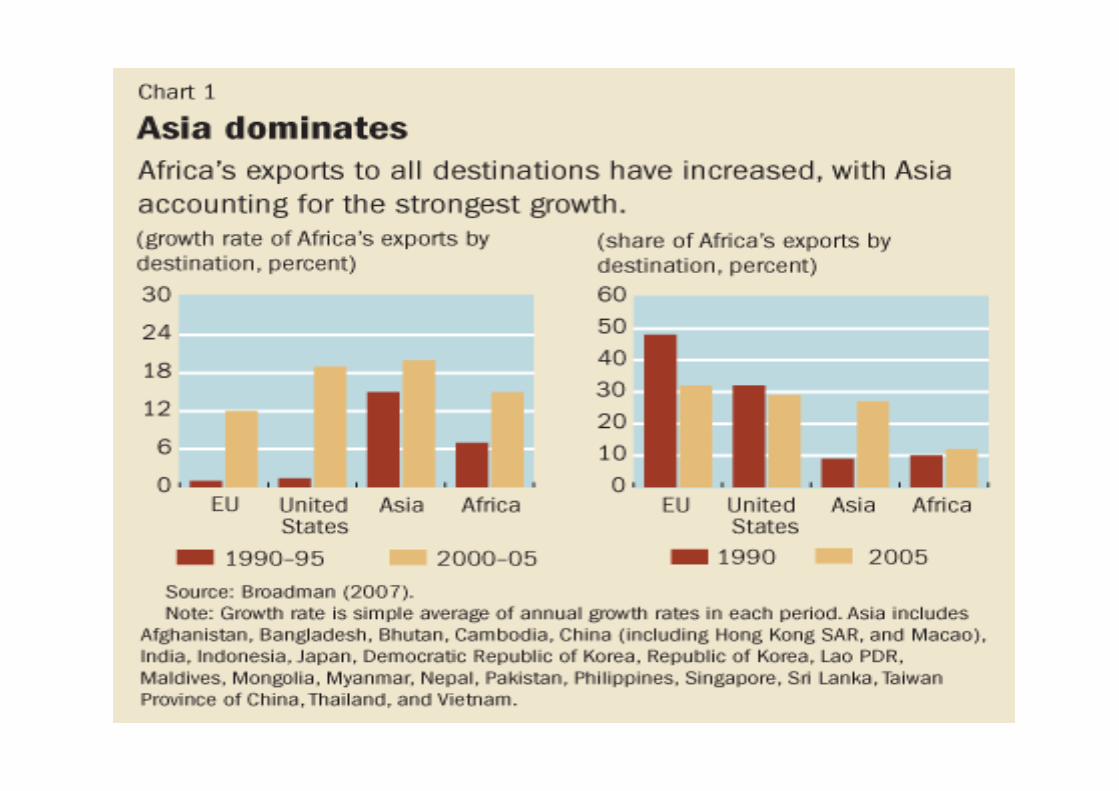

• The recent boom in commerce between Africa and Asia epitomizes the explosion of South-South trade:

Burgeoning middle classes in ASEANRising Economic growth in SSASSA’s increasing demand for ASEAN manufactured goods

• The traditional Africa’s N-S commerce with EU and USA: Preferential Arrangements

• S-S complementarities between developing nations – likely sustainability

SSA’s trade record remains poor• Africa’s numerous small, landlocked

countries and high degree of geographic segmentation

• Largest number of countries per square area of any developing region

• Heterogeneous Africa: GDP per capital range from less than $200 to $ 7000

• One third of resource-dependent economies are in Africa

• Small and shallow markets due to high inland transport costs

Asia – Africa trade patterns• Increased trade flows: the hallmark of South-

South cooperation and trade• Asia is Africa’s third most important export

destination after EU and US• Commodities accounts for 86 % of SSA’s

exports to Asia• Manufactured goods accounts for 80% of SSA’s

imports from Asia• Africa’s exports to China and India accounts for

half of SSA’s exports to Asia

Exports of merchandise products of world and regions by destination, 2011 (Note: Value ranges differ by region.)

Exports of merchandise products of world and regions by destination, 2011 (Note: Value ranges differ by region.)

Exports of merchandise products of world and regions by destination, 2011 (Note: Value ranges differ by region.)

Value of World Seaborne Trade (US$)

• 52% Container

• 22% Tanker

• 20% General Cargo

• 6% Dry Bulk

• Liner Shipping is the most efficient mode of Transportation

• Shipping is the most carbon-efficient mode of Transportation

• The Value of the liner shipping industry to Global economy exceeds 400 bn a year

• A large container ship can carry 11,000 containers of cargo == 77 km or 44 miles long train

• Source: Lloyd’s Maritime Intelligence Unit

Container Port Volume: World and ESCAP Region

• Study Forecast: Total volume of world container handling to increase to 795 million TEU by 2015, implying 7.9 %/ annual growth

• Total volume of international container handling in ESCAP Ports to increase from 152 million TEU in 2005 to 383 in 2015 ….9.7 % annual average growth

• China’s share of total port throughput will account for 44% of total ESCAP Ports throughput in 2015

Total Container Throughput of ESCAP Economies – 2015 (million TEU)

Total Container Throughput Annual Growth of ESCAP Economies (2005 – 2015)

Shipping containers handled in Ports by Country in 2008(prior to the global crisis)

0

2 000 000

4 000 000

6 000 000

8 000 000

10 000 000

12 000 000

14 000 000

16 000 000

18 000 000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

Gatew ay Transhipment

Shipping containers handled in Africa

1980 ‐ 2008 (prior to the global crisis)

KENYA UGANDA

MOZAMBIQUE

MADAGASCAR

COMOROS

TANZANIA

REUNION

MAURITIUS

ZAMBIA

NAMIBIA

SOUTH AFRICA

BOTSWANA

ZIMBABWE

RWANDA

BURUNDI

SEYCHELLES

Mombasa

Dar‐es‐Salaam

Nacala

Toamasina

Port Reunion

Port Louis

Maputo

Durban

East London Ngqura

Port Elizabeth Cape Town

WalvisBay

Dr. Yann ALIX & Jean‐François PELLETIER

Nov 2011

Eastern & Southern Countries & major ports Market coverage

Shipping Lines Connectivity& Capacity deployed on Eastern & Southern Ports

Situation reported Sept 2011

3,800,000Teu’s Trade Capacity

350 Vessels

50 Weeklyservices

20 Portsweeklycalled

Source : Dynam

ar2011, D

rewry

2011, Con

tainerisation Internationa

l 2011, Alpha

liner

2011

2222

Shipping Lines Connectivity& Capacity deployed on Eastern & Southern Ports

Situation reported Sept 2011

3,800,000Teu’s Trade Capacity

350 Vessels

50 Weeklyservices

20 Portsweeklycalled

Source : Dynam

ar2011, D

rewry

2011, Con

tainerisation Internationa

l 2011, Alpha

liner

2011

2222

Annual Trade Capacity deployed by Major areas of marketsSituation reported Sept 2011

In TEU’s

Southern, Eastern& Indian OceanMarkets

Far EastAsia

MidEast& India

Europe & Med

Africa

NorthAmerica

100,000

250,000

500,000

1,000,000

Source : Dynam

ar2011, D

rewry

2011, Con

tainerisation Internationa

l 2011,

Alpha

liner

2011, Port A

utho

ritie

s 45 %

25 %

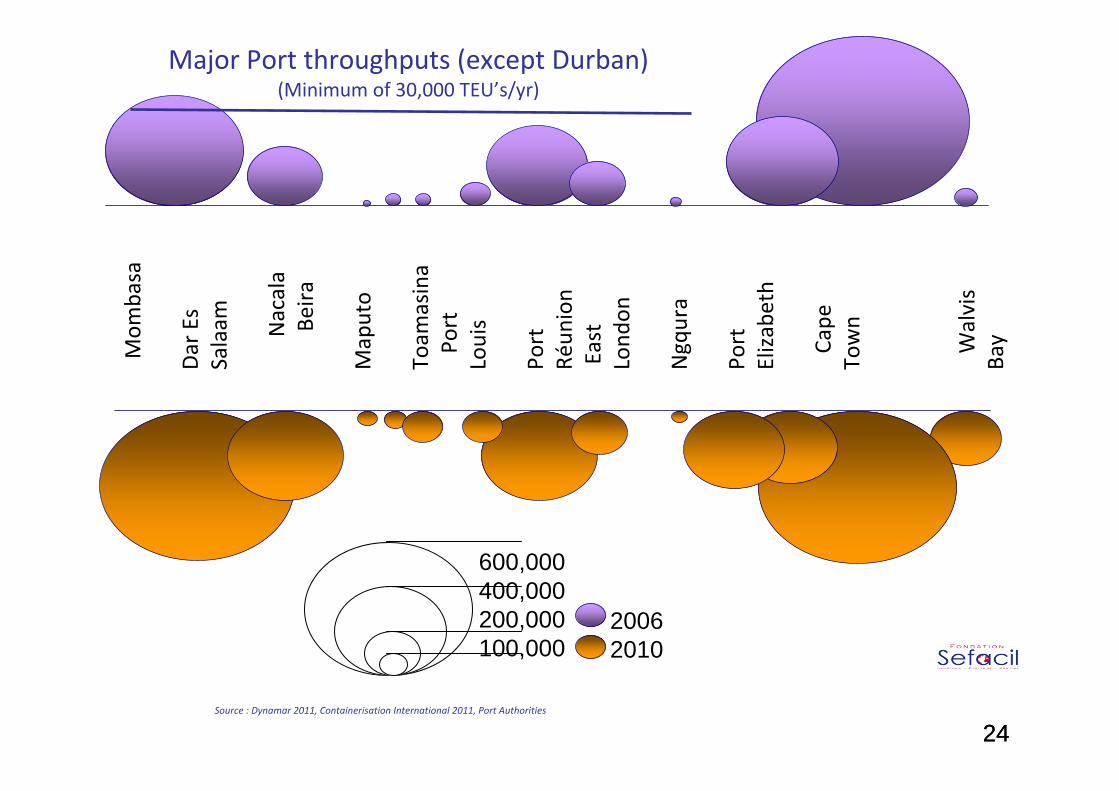

Major Port throughputs (except Durban) (Minimum of 30,000 TEU’s/yr)

Mom

basa

Dar Es

Salaam Nacala

Beira

Maputo

Toam

asina

Port

Louis

Port

Réun

ion

East

Lond

on

Ngqura

Port

Elizabeth

Cape

Town

Walvis

Bay

Source : Dynamar 2011, Containerisation International 2011, Port Authorities

600,000 400,000 200,000100,000

20062010

2424

Sketch on Ports configuration ‐ Yesterday ! •Milk Run System with« national single port gateway »serving mainly « domestic markets »

• Cross‐trading liner system based on interlinking Regional & Intercontinental loops

• Feedering network not enough reliable(size of the markets, productivityof handling activities, terminal costsfor thanshipments, dwell time for small ships, etc.)

• Economies of scale not sufficient• Lack of Regional Customs facilitation & integration

• Very few transnational freight railwayopportunities

• Few paved roads connecting gateway• Very few Logistic value added services

on Imp/Exp products(FTZ & services added)

South‐AfricanRange

SouthW

est

Range

SouthEastRange

Land

locked

markets

Inland boundaries

National Port Gateway & hinterland

Transcontinental direct call services

National direct call services

Regional feedering services Regional Hub

Toward a new subregionalPort hierarchy based on :

• Forecasted increase of Imp/Exp volumes • New generation of motherships(6,000 and +) & feederships (1500 and +)

• Hub & Spoke opportunities• Improvment of Terminal global performances

• Trades imbalances & empty strategicmanagement

• Regional Port Reform& GTO investments• Inland investments & Multimodal Corridors solutions

• Overlapping of hinterland coverage& competitiveness to control landlocked markets stimulated

Sketch on Ports configuration ‐ tomorrow ?

South‐AfricanRange

SouthW

est

Rang

e

SouthEastRange

Land

locked

markets

Inland boundaries

National Port Gateway & hinterland

Transcontinental direct call services

National direct call services

Regional feedering services

Inland multimodal corridors

Regional Hub

Hub & Spoke terminal

The African Port System: Fundamental Challenges

Major Traffic Growth• Port Container traffic demand is expected to quadruple by 2020 and

has already triggered the need for substantive Terminal Development

Capacity Limitations• The rapid growth is already putting pressure on the port system• Shipping lines have serious concerns about condition, capability

and future reliability of ports, road and rail services and infrastructure

• What are the Infrastructure priorities and how can African portsattract private sector funding?

Port Customers Demand Competitive Services and Prices

• Strong competition exists among global supply chains

Facilitating African Ports to Responding to opportunities/Challenges

• Increase inter/intra African Trade

• Regional economic integration through Transport Corridor

Development

• Intermodal harmonisation to improve regional Supply Chain and

reduce logistics costs

• Capacity Expansion: scale-up infrastructure and inland networks in

place to meet growth opportunities

• Patnerships between developed and developing ports – a regional

approach is required to build economies of scale and drive transport

system efficiencies

Thank you for your attention!