The Train is Leaving the Station Estate Planning in 2012 October 10, 2012 William L. Montague Frost...

24

The Train is Leaving the Station Estate Planning in 2012 October 10, 2012 William L. Montague Frost Brown Todd LLC [email protected] 3300 Great American Tower 301 East Fourth Street Cincinnati, Ohio 45202 (513) 651-6920 7310 Turfway Road Suite 210 Florence, Kentucky 41042 (859) 517-5920

Transcript of The Train is Leaving the Station Estate Planning in 2012 October 10, 2012 William L. Montague Frost...

The Train is Leaving the Station

Estate Planning in 2012October 10, 2012

William L. MontagueFrost Brown Todd LLC

3300 Great American Tower301 East Fourth StreetCincinnati, Ohio 45202(513) 651-6920

7310 Turfway RoadSuite 210

Florence, Kentucky 41042(859) 517-5920

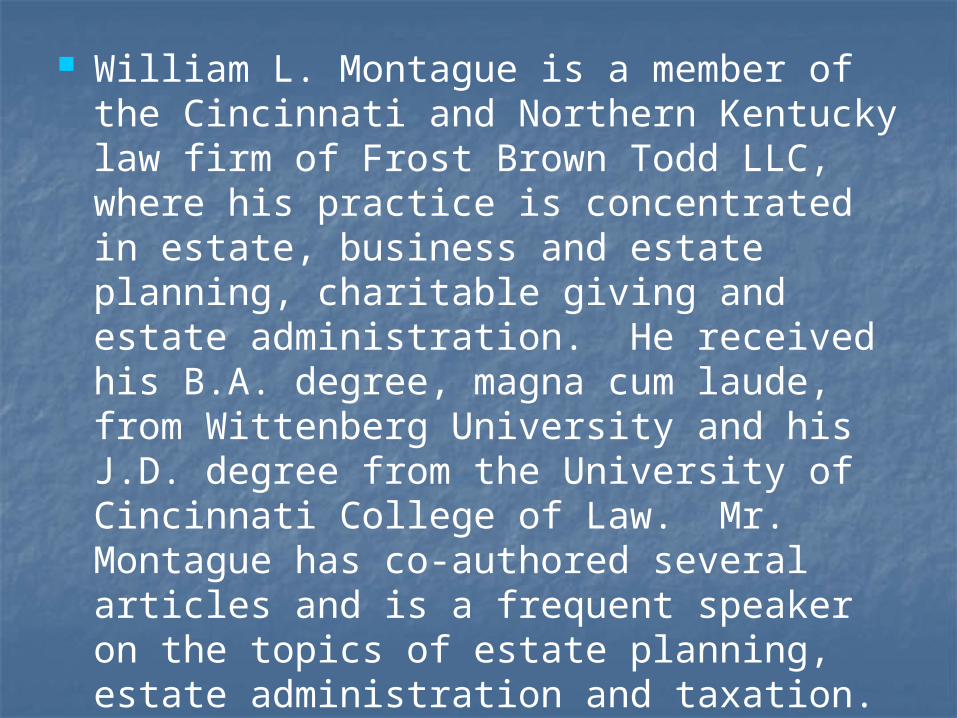

William L. Montague is a member of the Cincinnati and Northern Kentucky law firm of Frost Brown Todd LLC, where his practice is concentrated in estate, business and estate planning, charitable giving and estate administration. He received his B.A. degree, magna cum laude, from Wittenberg University and his J.D. degree from the University of Cincinnati College of Law. Mr. Montague has co-authored several articles and is a frequent speaker on the topics of estate planning, estate administration and taxation. He has been repeatedly recognized as a Best Lawyer in America and Ohio Super Lawyer.

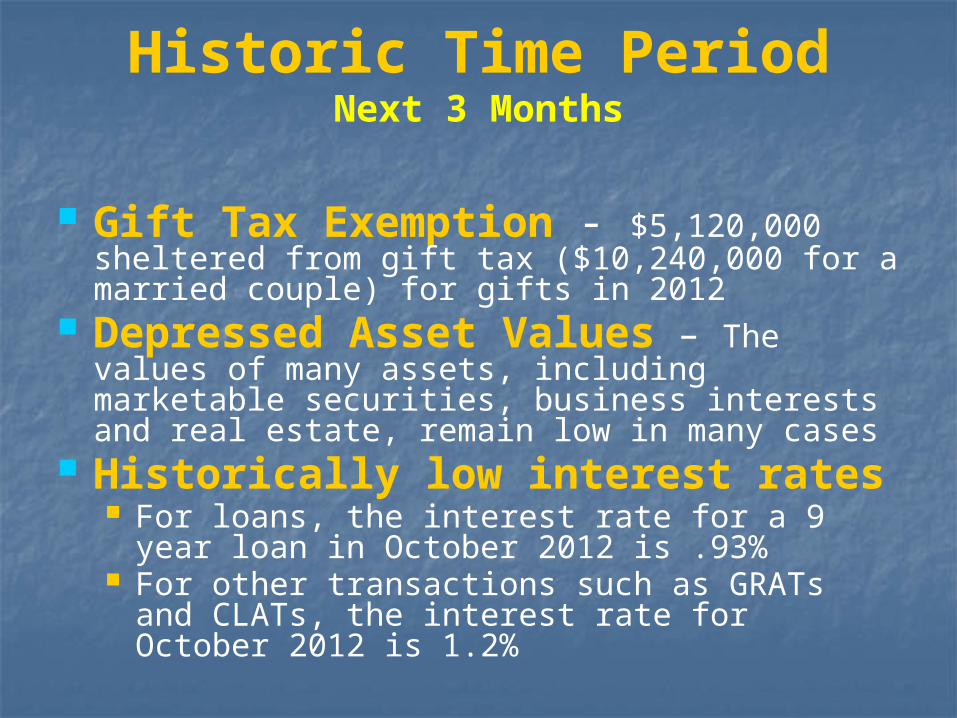

Historic Time PeriodNext 3 Months

Gift Tax Exemption - $5,120,000 sheltered from gift tax ($10,240,000 for a married couple) for gifts in 2012

Depressed Asset Values – The values of many assets, including marketable securities, business interests and real estate, remain low in many cases

Historically low interest rates For loans, the interest rate for a 9 year loan in

October 2012 is .93% For other transactions such as GRATs and

CLATs, the interest rate for October 2012 is 1.2%

Take Advantage of Larger Gift Tax

ExemptionNext 3 Months

Direct Gifts to Children – simple, but not as much protection for the children

Direct Gift to Irrevocable Trust for Children– Protects the gifted assets from estate taxation at the children’s deaths, from the children’s creditors, and from the divorce of a child. Can also provide asset management, if needed

Direct Gift by One Spouse to Irrevocable Trust for Other Spouse and Children – Provides same protections for children, but provides the additional benefit of making assets available to the other spouse if living needs require in the future

Take Advantage of Larger Gift Tax

ExemptionNext 3 Months

Leveraged Gift to Irrevocable Trust for Children– Protects the gifted assets from estate taxation at the children’s deaths, from the children’s creditors, and from the divorce of a child. Can also provide asset management, if needed

Leveraged Gift by One Spouse to Irrevocable Trust for Other Spouse and Children – Provides same protections for children, but provides the additional benefit of making assets available to the other spouse if living needs require in the future

Take Advantage of Low Interest Rates

Next 3 Months

Direct Loan to Children – simple, but not as much protection for the children

Direct Loan to Irrevocable Trust for Children– Protects the gifted assets from estate taxation at the children’s deaths, from the children’s creditors, and from the divorce of a child. Can also provide asset management, if needed

Direct Loan by One Spouse to Irrevocable Trust for Other Spouse and Children – Provides same protections for children, but provides the additional benefit of making assets available to the other spouse if living needs require in the future

Loan to Lifetime

Trust

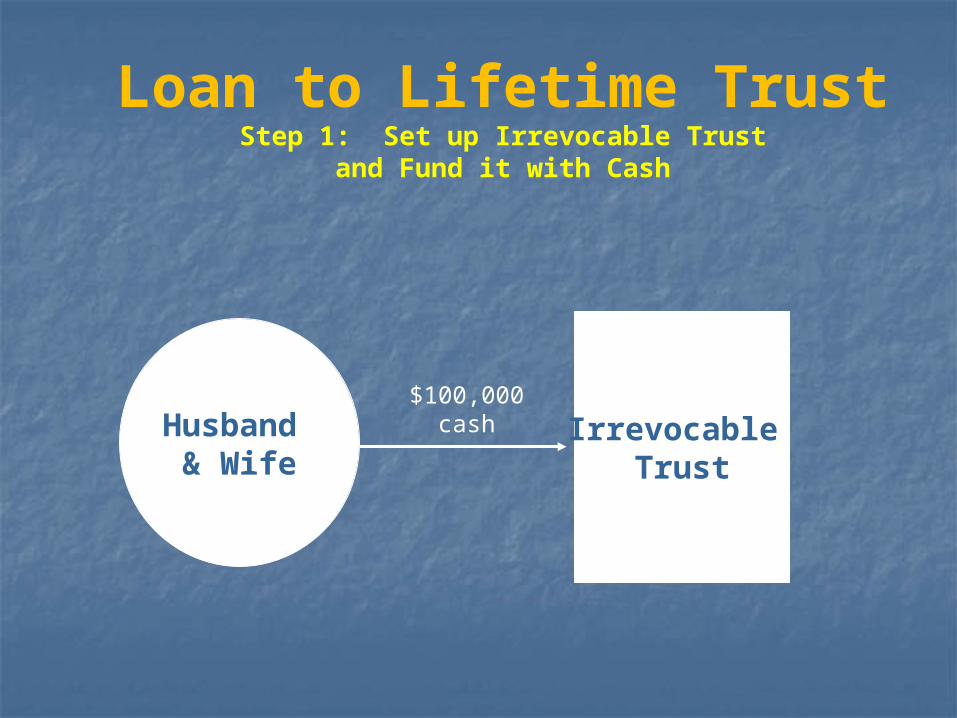

Loan to Lifetime TrustStep 1: Set up Irrevocable Trust

and Fund it with Cash

Husband & Wife

Irrevocable Trust

$100,000cash

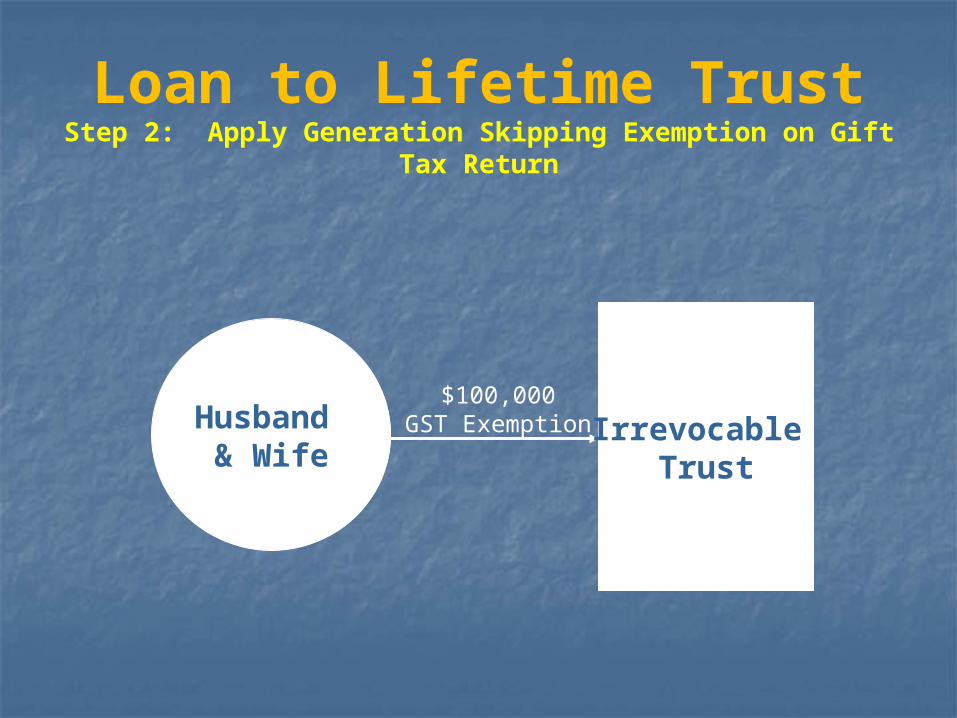

Loan to Lifetime TrustStep 2: Apply Generation Skipping Exemption on Gift

Tax Return

Husband & Wife

Irrevocable Trust

$100,000GST Exemption

Loan to Lifetime TrustStep 3: Loan Money to Irrevocable Trust

Husband & Wife

Irrevocable Trust

$900,000loan

(9 years at .93% interest)

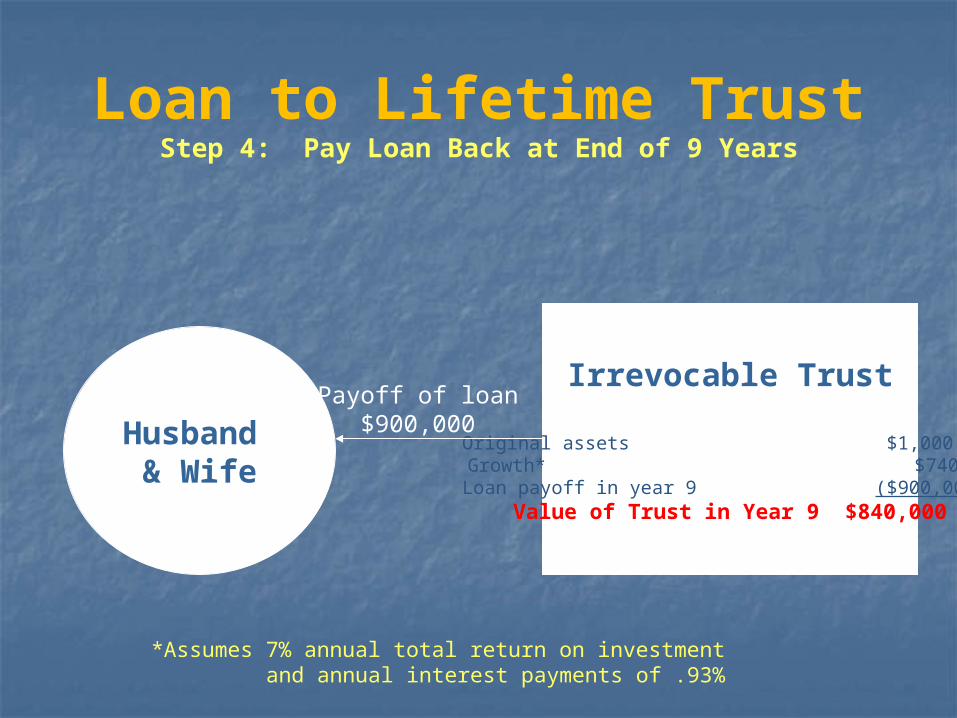

Loan to Lifetime TrustStep 4: Pay Loan Back at End of 9 Years

Husband & Wife

Irrevocable Trust

Original assets $1,000,000 Growth* $740,000

Loan payoff in year 9 ($900,000) Value of Trust in Year 9 $840,000

Payoff of loan$900,000

*Assumes 7% annual total return on investment and annual interest payments of .93%

Leveraged Gift to

Lifetime Trust

Installment Sale to Grantor TrustOriginal Scenario

SteveXYZ

Manufacturing $15,000,000

100 shares100% ownership

$1,200,000 annual distribution

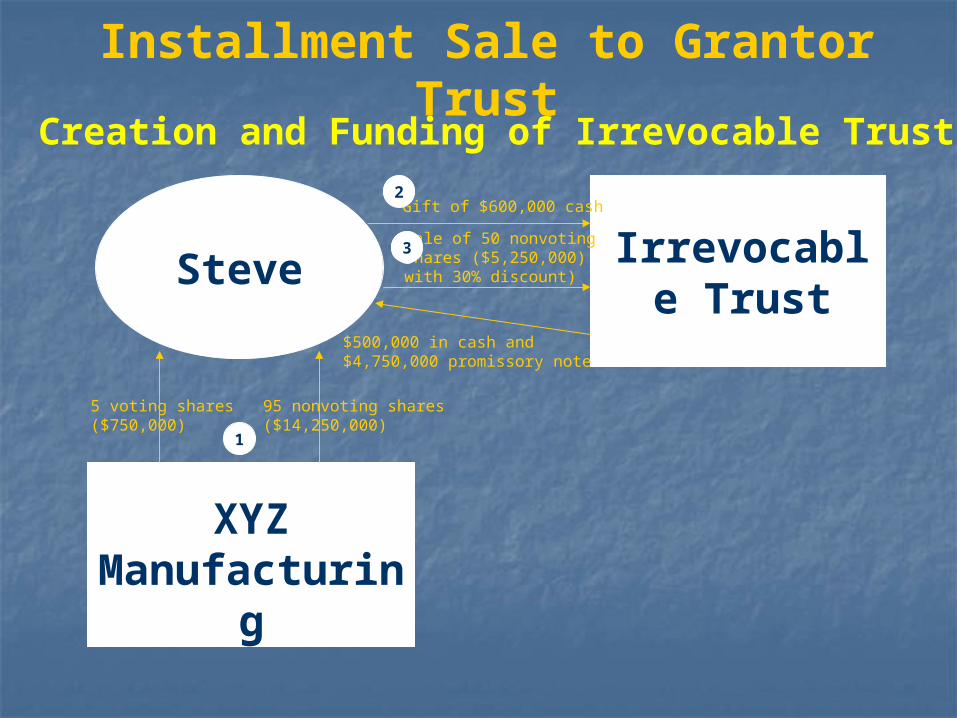

Installment Sale to Grantor Trust

Creation and Funding of Irrevocable Trust

Steve Irrevocable Trust

XYZ Manufacturing

Sale of 50 nonvotingshares ($5,250,000)with 30% discount)

Gift of $600,000 cash

$500,000 in cash and$4,750,000 promissory note

95 nonvoting shares($14,250,000)

5 voting shares($750,000)

3

2

1

Cash Flow(Year 1)

IrrevocableTrust Steve

XYZManufacturing

50% of profitdistributions($600,000) 50% of profit

distributions($600,000)

$600,000note payment

IRS

Taxes($526,000)

Installment Sale to Grantor Trust

LifeInsurance

premiumpayments

Installment Sale to Grantor TrustStep Four: Sale of XYZ Manufacturing in 2017 for $30,000,000

Steve Irrevocable Trust

XYZManufacturin

gCash $30,000,000

$882,000promissory

notebalance

50 nonvoting shares

management control

BuyerBuyer assets

Cash $30,000,000

Installment Sale to Grantor TrustStep Five: Distribution of Sale Proceeds

SteveIrrevocabl

e TrustCash $15,000,000

XYZManufacturin

gCash $30,000,000

$882,000promissory

note

50 nonvoting shares

management control

$15,000,000cash distribution 50 voting and

nonvoting shares

$15,000,000cash distribution

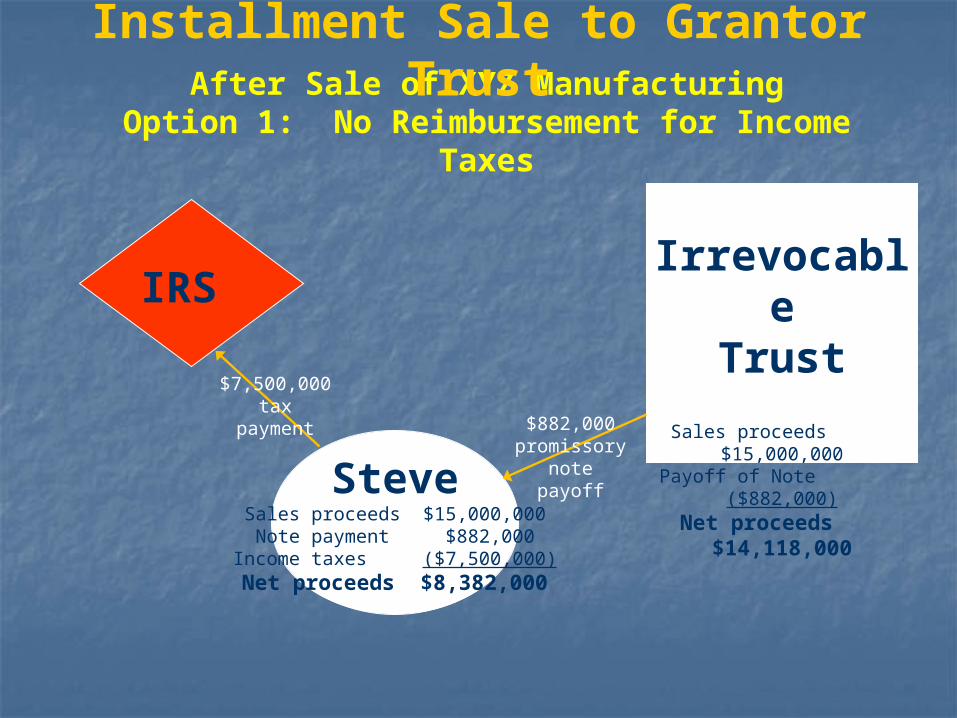

After Sale of XYZ ManufacturingOption 1: No Reimbursement for Income

Taxes

IrrevocableTrust

Sales proceeds $15,000,000Payoff of Note ($882,000)

Net proceeds $14,118,000

SteveSales proceeds $15,000,000Note payment $882,000

Income taxes ($7,500,000)Net proceeds $8,382,000

IRS

Installment Sale to Grantor Trust

$882,000promissory

notepayoff

$7,500,000tax

payment

After Sale of XYZ ManufacturingOption 2: Reimbursement for Income Taxes

IrrevocableTrust

Sales proceeds $15,000,000Tax reimbursement ($3,750,000)Payoff of Note ($882,000)

Net proceeds $10,368,000

SteveSales proceeds $15,000,000Tax reimbursement $3,750,000Note payment $882,000

Income taxes ($7,500,000)Net proceeds $12,132,000

IRS

Installment Sale to Grantor Trust

$882,000promissory

notepayoff

$7,500,000tax

payment

$3,750,000tax

reimbursement

Installment Sale to Grantor TrustBottom Line

$14,118,000* is sheltered from estate tax inside the Irrevocable

Trust at a gift tax cost of $600,000, which is leverage of

more than 23 to 1!

*Assumes Steve will not request reimbursement for income taxes paid on behalf of Irrevocable Trust.

Installment Sale to Grantor Trust

Step One: Recapitalize company into voting and nonvoting shares

Step Two: Seed the irrevocable trust with gifted assets so that the purchaser of nonvoting stock will be a “creditworthy” purchaser

Step Three: Steve sells nonvoting stock to the Irrevocable Trust, free of capital gain taxes, in exchange for an installment promissory note

Step Four: Make note payments back to Steve with cash flow generated by corporate distributions paid to the Irrevocable Trust

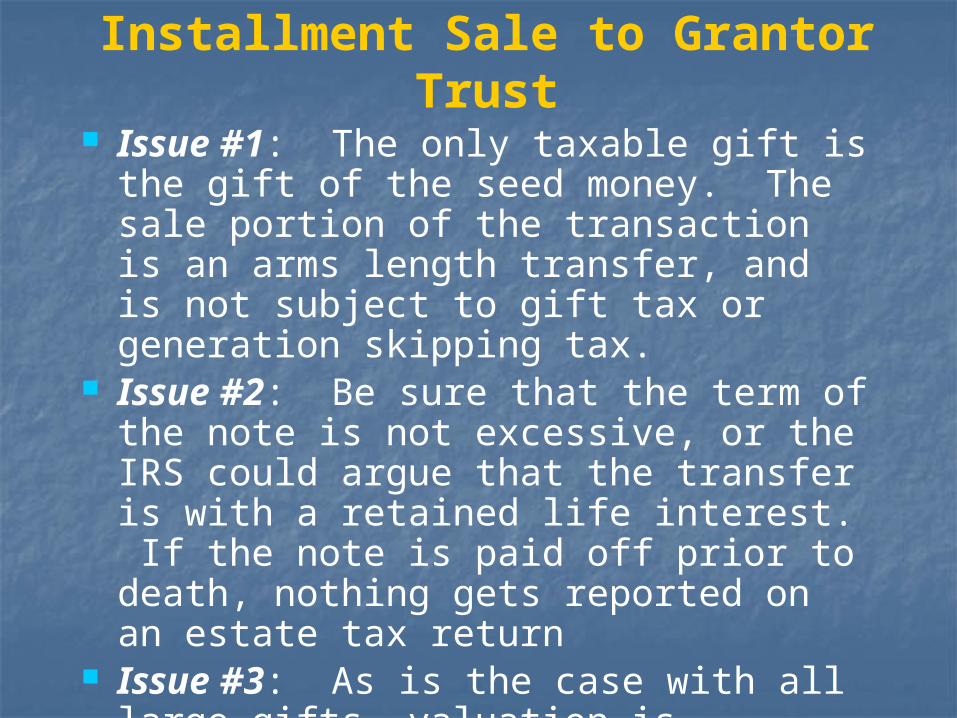

Installment Sale to Grantor Trust

Issue #1: The only taxable gift is the gift of the seed money. The sale portion of the transaction is an arms length transfer, and is not subject to gift tax or generation skipping tax.

Issue #2: Be sure that the term of the note is not excessive, or the IRS could argue that the transfer is with a retained life interest. If the note is paid off prior to death, nothing gets reported on an estate tax return

Issue #3: As is the case with all large gifts, valuation is critical!!

Installment Sale to Grantor Trust

Advantages No gain recognized by grantor on sale Payment of income taxes by grantor rather

than by irrevocable trust (reducing the size of grantor’s estate)

Favorable interest rates Payment flexibility / refinancing Protected from estate taxation in multiple

generations Partial disclosure on gift tax return / no

disclosure on income tax return

Installment Sale to Grantor Trust

IRS attack in Karamazin It is preferable to have the trust own

assets other than interests in the entity being sold

If personal guarantees would be required by a commercial lender, they should be used here

There should be sufficient entity income to assure repayment of the note