The Three Pillars of FATCA

31

The Foreign Account Tax Compliance Act (FATCA) The Three Pillars of FATCA SESSION 3 Training Programme FATCA for LATAM Firms 23-24 February 2015 (Panama City), 25-26 February 2015 (Santo Domingo) Rodrigo Zepeda Independent Consultant

-

Upload

rodrigo-zepeda-llb-llm-acsi -

Category

Law

-

view

499 -

download

1

Transcript of The Three Pillars of FATCA

The Foreign Account Tax Compliance Act (FATCA)

The Three Pillars of FATCA

SESSION 3

Training ProgrammeFATCA for LATAM Firms

23-24 February 2015 (Panama City), 25 -26 February 2015 (Santo Domingo)

Rodrigo ZepedaIndependent Consultant

Section 1: FATCA Classification

Section 2: FATCA Reporting

Section 3: FATCA Withholding

FATCA ClassificationSE CT ION 1

3

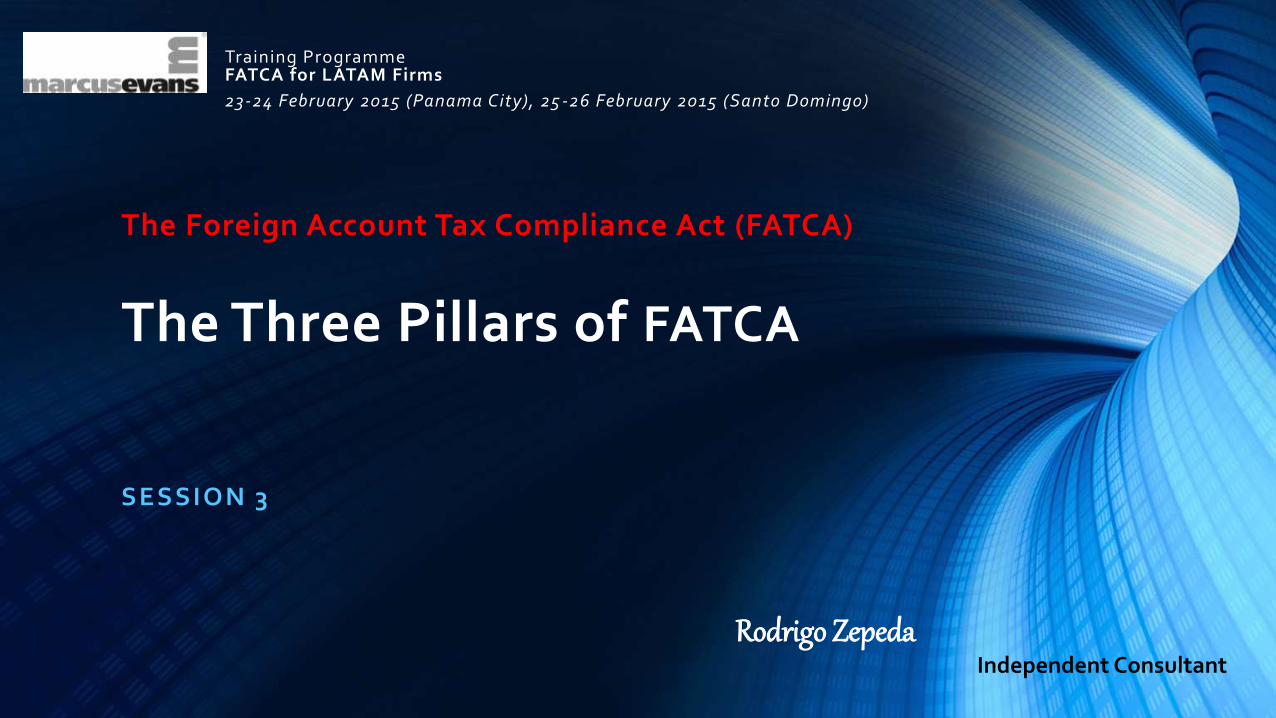

FATCA Classification

Three Types of Classification:

1. Own institution.• FFI (P-FFI, NP-FFI, RDC-FFI, CDC-FFI); NFFE (A-NFFE, P-NFFE); Excepted FFI; Exempted FFI.

2. Client institutions.• U.S. owned foreign entities (foreign entity with one or more Substantial U.S. Owners).

• A Substantial US Owner means: (1) corporations (any specified U.S. person that owns, directly or indirectly, more than 10%of corporate stock (by vote or value); (2) partnerships and trusts (comparable rules apply); (3) investment funds (the 10%ownership rule not applicable, any investment by a U.S. person below 10% is reportable).

3. Client individuals.• Classification of specified U.S. persons and foreign (non-U.S.) persons.

• Classification of High Value Accounts, Low Value Accounts, and Prima Facie Accounts.

• Classification of De Minimis (exempt) Accounts.

• Classification of Recalcitrant Account Holders (RAHs).

Prima Facie FFI is an entity that is designated in the WA’s electronic database (searchable) as an account holder, that is aQualified or Non-Qualified Intermediary, or documented or presumed to be, a foreign account holder, and assigned a set ofindustry codes indicating that the entity is a type of financial intermediary (for U.S. maintained accounts).

44

FFI FATCA General Classification Obligations

1. Search for U.S. indicia (U.S. persons) for individual pre-existing and new account holders.

2. Obtain additional “curing” information if U.S. indiciaexist (e.g., W-8BEN, W9).

3. Report to IRS as U.S. or recalcitrant account if no (non-U.S.) documentary proof.

4. Determine FATCA category classification for entityaccount holders.

5. Obtain withholding certificate (e.g. W-8BEN-E) + GIIN forP-FFIs, RDC-FFIs, CDC-FFIs, Excepted/Exempted FFIs.

6. Report and withhold on select payments to NP-FFIs.

53

U.S. indicia include:

(1) U.S. citizen or resident;

(2) U.S. place of birth;

(3) U.S. resident or mailingaddress;

(4) U.S. telephone number;

(5) standing instructions totransfer funds to a U.S.maintained account;

(6) Power of Attorney orSignatory Authority grantedto person with U.S. address;

(7) an “in care of” or “hold mail”address that is the soleaddress that the FFI has for theaccount holder.

Documentation Requirements

IS THE CLIENT A

U.S. PERSON?

Potential Problem Clients

• Residents of foreign (non-U.S.)

jurisdictions who have not revoked their

U.S. Green Card status (e.g. job or

employment based GC, student GC, or

‘other’ GC such as GC Lottery.

• Residents of foreign (non-U.S.)

jurisdictions with a U.S. born parent.

• Person who regularly travels in the U.S.

and meets the requirements of the

‘Substantial Presence Test’ for the

calendar year (i.e. Physically present 31

days during current year, and 183 days

during 3-year period which includes

current year and immediately preceding 2

years).*

* Must count (1) all the days person present

in the current year; (2) 1/3 of the days

person present in the first year before the

current year; (3) 1/6 of the days person

present in the second year before the

current year.

U.S. Citizenship or lawful permanent resident

U.S. Birth place

U.S. Address (residence, correspondence, or

P.O. Box)

Instructions to transfer funds to U.S.

Accounts or directions regularly received

from a U.S. address

Only address on file is “in care of” or “hold

mail” or U.S. P.O. Box

Notice 2011-34 excludes foreign P.O. Box as U.S. indicia

Power of Attorney or signatory authority granted to

person with U.S. address

Obtain W-9

1. Obtain W-9 or W-8BEN; and2. Non-U.S. Passport or similar documentation

establishing foreign citizenship; and3. Written explanation regarding U.S. citizenship

1. Obtain W-9 or W-8BEN; and2. Non-U.S. Passport or similar documentation

establishing foreign citizenship

1. Request W-9 or W-8BEN; and2. Documentary evidence establishing non-U.S.

status

Request W-9, W-8BEN; orDocumentary evidence establishing non-U.S. status

Request W-9, W-8BEN; orDocumentary evidence establishing non-U.S. status

The U.S. Persons Test

62

FATCA Account Classification

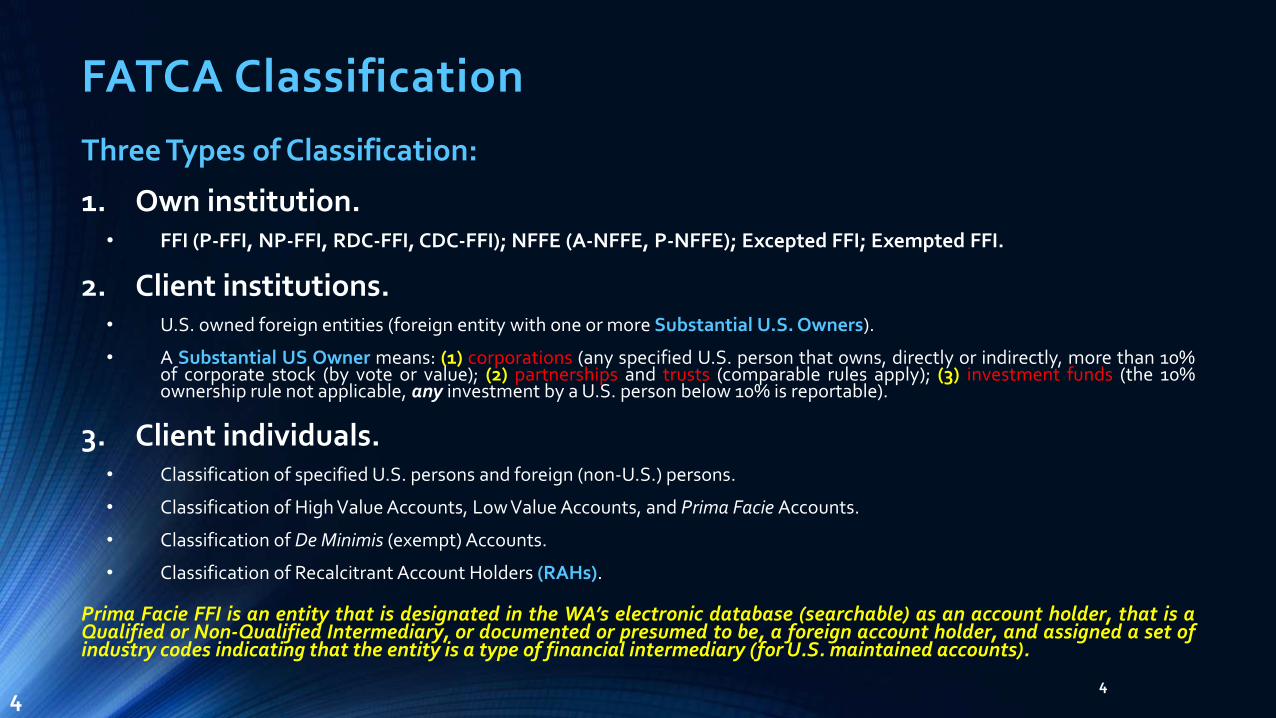

Types of Account Classification:

1. Individual Pre-Existing Account owned (0r controlled) by a Specified U.S. Person.

• (1) Low Value Account; or (2) High Value Account.

2. Individual New Account owned (or controlled) by a Specified U.S. Person.

• (1) Low Value Account; or (2) High Value Account.

3. Entity Pre-Existing Account.

• (1) FFI; (2) NFFE; (3) Exempt NFFE; or (4) Excepted NFFE.

4. Entity New Account.

• (1) FFI; (2) NFFE; (3) Exempt NFFE; or (4) Excepted NFFE.

Pre-Existing Accounts are U.S. Accounts Existing as of 31 December 2013.

New Accounts are U.S. Accounts Existing as from 1 January 2014.

72

Classification of AccountsDifferent Types of Accounts

• Direct U.S. Accounts: are those accounts that are maintained by an account holder which is a Specified U.S.Person, i.e. excludes those entities not listed within the exclusions to the definition of U.S. Person.

• Indirect U.S. Accounts: include any accounts held by a U.S. owned NFFE (held at a FFI or USFI). A U.S. ownedNFFE is a passive foreign entity that has one or more substantial U.S. owners.

• High Value Accounts: include any accounts with an aggregated balance or value in excess of U.S.$1,000,000.

• Low Value Accounts: include any accounts with an aggregated balance or value in excess of U.S.$50,000 up toand including U.S.$1,000,000.

• In Scope Accounts: include all FATCA defined Financial Accounts with a balance or value in excess ofU.S.$50,000.

• Out of Scope Accounts: Accounts which are not FATCA defined Financial Accounts, such as certain retirementfunds; non-retirement savings accounts; certain term life insurance contracts; individual accounts (with year-end aggregate value or balance of U.S.$50,000 or less); entity accounts (with year-end aggregated balance orvalue of U.S.$250,000 or less); and cash value insurance or annuity contracts (with an aggregated value ofU.S.$250,000 or less).

84

General FATCA Classification Observations

NFFE AML Risks

• Higher Risk: Passive NFFEs may be potentially used as a type of “shell company” for tax evasion or moneylaundering purposes.

• Lower Risk: Active NFFEs are Excepted NFFEs (e.g., non-financial active trade or business) but may now bespecifically targeted because they fall outside of FATCA obligations.

• Higher Risk: Passive NFEEs (balance or value of U.S.$1,000,000) FFI must obtain substantial U.S. ownershipinformation, or if no information is provided, account holder is deemed to be a RAH.

• Lower Risk: Passive NFFEs (aggregated balance or value of U.S.$250,000 to U.S.$1,000,000) FFI can rely onAML/KYC information to identify U.S. owners.

Certification of U.S. account holders

• IRS Form W-9: U.S. account holder can certify that he or she is a U.S. person.

• IRS Form W-8BEN: beneficial owner can certify that he or she is a foreign person.

93

FATCA CLASSIFICATION

U.S. Persons U.S. Entities Foreign (Non-U.S) Entities

FFIs Excepted NFFEs NFFEs

Active NFFEsPassive NFFEsDC-FFIsNP-FFIsP-FFIs

10

FATCA Classification

2

RDC-FFIsCDC-FFIs

Owned Documented

FFI

Exempt Beneficial

Owner

FATCA EXEMPTIONS

FFIs Active NFFEs Exempt Beneficial Owner

Low Value Accounts

Governmental organisations

Central bank

International organisations

Retirement funds

Active trade/business

A non-financial holding group service company

Registered charity or club, association , arrangement, or

non-profit organisation

Group financing company

A corporation with shares regularly trading on

established securities market

Registered-Deemed Compliance

Certified-Deemed Compliance

Local FFIs QIVsNon reporting

members of P-FFI groups

RFs

Retirement plans

Owner documented

FFIs

Non-profit organisations

FFIs with low value accounts

NRLBs

Depositary accounts held by individuals with an aggregate balance or

value of U.S.$50,000 or less are not treated as

U.S. accounts.

11

FATCA Exemptions

4

Out of Scope Accounts

Accounts which do not fall under the FATCA

definition of Financial Account, e.g. certain retirement funds, life insurance contracts.

U.S Territory Entity

In liquidation

Non-U.S government or international organisation

Start-up trading entity

Determining Active or Passive NFFE Status

12

NFEE

ACTIVE NFEE PASSIVE NFEE

ANY NON U.S. ENTITY THAT IS NOT A FINANCIAL

INSTITUTION.

ENTITY IS NOT INCORPORATED CREATED OR ORGANISED IN THE U.S, OR UNDER U.S.LAW, OR U.S.

STATE LAW (INCLUDING D.C.)

A corporation with shares that regularly trade on an established

securities market.

A non-U.S government or international organisation (or agency thereof).

A Start-Up Trading Entity.

Group Financing Company.

A U.S. Territory Entity.

Active Trade or Business.

A non-Financial Holding Group Service Company.

In liquidation.

A registered charity or club, association or arrangement or non-profit

organisation.

Without controlling persons that

are U.S. Persons.

Certify status and disclose name, address and U.S. TIN.

Passive income includes:• Dividends, including income equivalent to dividends;• Interest (including income equivalent to interest, certain returns from investments in insurance contracts;• Certain rents and royalties other than those derived from an active trade or business;• Net gains from transactions, e.g. forwards (similar transactions) relating to certain types of commodities transactions;• Certain foreign currency exchange gains;• Net income from notional principle contracts;• Amounts received under cash value insurance contracts or amounts earned by an insurance company in connection withits reserves for insurance and annuity contracts; and• Net gains from the sale of assets that give rise to certain of the above types of income.

Entity that operates an active trade or business other than that

of a financial business.

Entities, organisations or companies that are in receipt of passive income

or hold passive assets.

Passive income excludes:• Any income from interest, dividends, rents or royalties that is received or accrued from a related person to the extentsuch amount is properly allocable to income of such related person that is not passive income• Income generated by certain commodities dealers and securities dealers in the ordinary course of business.

With controlling persons that are

U.S. Persons.

Certify status.

3

Less than 50% of gross income for calendar year is passive

income AND less than 50% of assets passive assets.

FATCA ReportingSE CT ION 2

13

FATCA Reporting for USFIs and P-FFIs

• USFIs have different reporting requirements depending on payee type (i.e., U.S.Non-exempt Recipient; Owner-documented FFI; Substantial U.S. Owners of anNFFE; or Foreign Recipient.

• P-FFIs reporting on U.S. accounts must determine:

• Reporting framework, (1) Model 1 IGA; (2) Model 2 IGA; (3) No IGA.

• Reporting obligations, e.g., P-FFI, NP-FFI, A-NFFE, P-NFFE, etc.

• IRS registration, i.e. whether or not the institution must register with the IRS.

• Reporting on U.S. client accounts held (i.e., compliant, non-compliant, recalcitrant).

• Responsible Officer (RO), i.e. institutions must delegate a FATCA Responsible Officer.

143

FATCA IGAsFATCA IGA

Model 2 IGAModel 1 IGA

U.S. IRSU.S. IRS

FATCA Partner Government

FFI aggregates Information on U.S.

Accounts and NPFFI’s Accounts or Obligations

FFI client account specific information

FFIFFI FFIFFI

LATAM Model 1 IGAs:Brazil; Costa Rica; France (French Territories);Honduras; Mexico.

LATAM Model 2 IGAs:Chile.

LATAM Model 1 IGAs (AIS): Colombia; Dominican Republic; Haiti;Panama; Peru.

LATAM Model 2 IGAs (AIS):Nicaragua; Paraguay.

July 2012 November 2012

Consent granted Consent not granted

153

FATCA General IRS Reporting Obligations1. FFIs must obtain and report information on accounts held by one or more specified U.S. persons

or U.S. owned foreign entities.

2. P-FFI’s must REPORT for TaxYears 2013 and 2014 (reports due by 31 March):

• Account Number.

• Account Balance or Value (at year-end or closing date).

• Name, address, TIN of each specified U.S. account holder.

• Name, address, TIN of NFFE account holder.

• Name, address, TIN of each substantial U.S. owner of the NFFE.

3. P-FFIs must REPORT for TaxYears 2015 and 2016:

• 2015 Same + Gross U.S. and Foreign Source Income.

• 2016 Same + Gross Proceeds from sale or redemption of property.

4. USWAs must identify entity account holders as U.S. persons, FFIs, NFFEs, or excepted entities.

5. P-FFIs must REPORT recalcitrant accounts (aggregate number and total value) for recalcitrantaccounts that: (1) have U.S. indicia; (2) lack U.S. indicia; (3) are dormant.

163

FATCA IRS Certifications

• Responsible Officer (RO) Duties:

(1) sign the FFI Agreement;

(2) oversee compliance program;

(3) certify to the IRS;

(4) is personally legally liable for non-compliance (under IRS FFI Agreement and Model 2 IGA);

(5) may be personally liable dependent on domestic laws (Model 1 IGA).

• Initial FATCA IRS Certification (under penalty of perjury):

• 29 August 2016 (for FFIs, 30 June 2014) (or 2 years and 60 days after effective date of FFI Agreement).

• Diligence – RO electronically certifies that (to the best of the RO’s knowledge):• classification of pre-existing customers is complete;

• performed according to FFI Agreement Due Diligence procedures;

• accounts without required documentation are classified as non-participating or non-consenting;

• no formal or informal procedures are in place (from 6 August 2011) to assist in FATCA avoidance (afterconducting a reasonable inquiry).

173

Overview of FATCA IRS Certifications

• First (3Year) Periodical FATCA IRS Certification:

• June 2018 – covers 3.5 year period from effective date of FFI Agreement.

• RO must establish, manage, and periodically review a FATCA compliance program which includespolicies, procedures, and processes that satisfy FFI Agreement obligations.

• RO must certify that FATCA compliance program is in effect and subject to regular review.

• RO must certify there are no “material failures” or “events of default” for the certification period.

• If there were material failures, RO must list appropriate remedial actions taken to prevent re-occurrence, and for any failure to deposit, withhold, report, failure was corrected (e.g., by payingtaxes dues or filing/amending appropriate returns).

• RO makes a “qualified certification” where RO cannot make certifications and must list proposedcorrective actions.

• Material failures are failures of the P-FFI to fulfill obligations under FFI Agreement if failure arose because of: (1) an error attributable to afailure of P-FFI to implement sufficient controls; or (2) deliberate actions to avoid FFI Agreement obligations by one or more P-FFIemployees (or its agent, sponsor, or compliance financial institution).

• Event of default is when a P-FFI fails to perform material obligations of the FFI Agreement (due diligence, reporting, withholding), or if theIRS determines P-FFI has failed to substantially comply with the FFI Agreement obligations.

184

Overview of FATCA IRS CertificationsRO (or Designee) Initial Certifications

• P-FFI has completed a review of all High Value Accounts and identified RAHs (no required documentation for account holder ofaccount).

• P-FFI has completed the account identification procedures and documentation requirements for all other pre-existing accounts (or if norequired documentation recorded, treats such account according to the applicable FATCA rules).

• To the best of RO’s knowledge, after conducting a reasonable inquiry, P-FFI did not have any formal or informal practices orprocedures in place to assist account holders in the avoidance of FATCA (from 6 August 2011 to date of certification).

RO (or Designee) Periodical Certification

• The RO has established a compliance program in effect (at certification date) and subjected to review (FATCA Regulations).

• There are no material failures for certification period, or appropriate actions taken to remediate and prevent failures from reoccurring.

• If there has been any failure to withhold, deposit, or report any amount (under the FFI agreement), the FFI has corrected such failure bypaying any taxes due (including interest and penalties) and by filing or amending the appropriate return.

RO (or Designee) Qualified Certification

• Occurs when the FFI and/or RO identifies “material failure” of “event of default” that has not been remedied (at certification date).

• RO has identified an event of default, or determined (at certification date) that there are one or more material failures regarding P-FFI’s compliance with the FFI agreement, and appropriate actions will be taken to prevent such failures from reoccurring.

• RO, with regards to any failure to withhold, deposit, or report any amount (under the FFI agreement), certifies the FFI will correct suchfailure by paying any taxes due (including interest and penalties) and filing or amending the appropriate return.

• RO will respond to any default notice, or will provide to the IRS (upon request) a description and remedial plan for each material failure.

193

FATCA IRS Penalties

• RO Penalties:

• IRS has stated it will not penalise a FFI or RO if it makes a good faith effort to comply (2014/2015).

• FROs could end up having to pay the IRS the entire 30 percent withholding tax owed for eachaccount the firm cannot properly identify.

• e.g., documentation to obtain a GIIN must be filled out correctly, or individuals face IRS penaltiesfor willful perjury (U.S.$250,000, up to 3 years in jail, or both).

• A “…return, statement or other document…contains or is verified by a written declaration that itis made under penalties of perjury” (IRC, §7206) (criminal sanction).

• “Any person who willfully makes and subscribes any return, statement, or other document, whichcontains or is verified by a written declaration that is made under the penalties of perjury, and whichhe does not believe to be true and correct as to every material matter; shall be guilty of a felony and,upon conviction thereof: Shall be imprisoned not more than 3 years; Or fined not more than $250,000for individuals ($500,000 for corporations); Or both, together with cost of prosecution.”

203

FATCA WithholdingSE CT ION 3

21

Overview of FATCA Withholdable Payments

• FATCA imposes a 30% withholding tax on withholdable payments made to specified foreign persons.

• Includes FDAP “Fixed or Determinable Annual or Periodic” gains, profits and income.

•Withholdable payments will cover income that comes from U.S. sources, e.g.

• Interest paid on deposits at U.S. bank branches, or non-U.S. branches of U.S. banks.

• Dividends paid by a U.S. corporation

• Dividend equivalents (U.S. dividends converted through the use of swap contract payments pegged todividends on a U.S. equity, securities loan, or repurchase agreement of a U.S. equity).

• 1 January 2017: will include gross proceeds from the sale or other disposition of any U.S. sourceinterest or dividend producing property (even if there is no gain on sale), e.g. stock or debt issued byU.S. corporation or the U.S. government (sale of U.S. Treasury Bond).

• 1 January 2017: will include passthru payments and foreign passthru payments (payments made byforeign entities on debt or equity held is classified as foreign source, so could be used as a “FATCAblocker” to circumvent FATCA).

224

What is a Withholdable Payment?

A withholdable payment is any payment of interests, dividends, rents, salaries,wages, premiums, annuities, compensations, remunerations, emoluments, andother Fixed or Determinable Annual or Periodic (FDAP) gains, profits and income.

Requirements:

1. The payment must be from sources within the U.S. (U.S. source income).

2. From 1 January 2017 - will include “gross proceeds” (from the sale or other disposition of anyproperty of a type which can produce interest or dividends from sources within the U.S.),USWAs, WAs, P-FFIs must withhold on gross proceeds payments made to recalcitrantindividual and entity accounts.

3. Not before 1 January 2017 – will include “passthru payments” (any withholdable payment orother payment to the extent attributable to a withholdable payment) applicable to non-U.S.source income.

4. If source of payment is unknown, payment must be treated as withholdable payment but can be held inescrow (up to 1 year) pending determination of character or source of the payment.

233

Special rules on FATCA Withholding

Withholding Agents (WAs):

• Any person, U.S. or foreign, that has control, receipt, or custody of an amount subject to withholding, orwho can disburse or make payments of an amount subject to withholding.

• Applies to associations, corporations, individuals, partnerships, trusts, other entities.

Who does Withholding Apply to:

• P-FFIs (must withhold 0n payments made to NP-FFIs and their limited branches and affiliates).

• (1) Prima Facie FFIs; (2) Electing Participating FFIs; (3) Non-Compliant FFIs; (4) RAHs.

Exceptions, Exemptions, and Interpretation:

1. Withholding Exemptions and Withholding Exclusions.

2. Grandfathered Obligations.

3. Modified Grandfathered Obligations.

4. Passthrough (“passthru”) Payments.

243

Withholding Exemptions and Exclusions

EXEMPT from FATCA withholding:

• ECI - Income effectively connected with a U.S. trade or business included in a beneficial owner’s annual gross income.

• Short-term obligations - Interest on certain short-term debt obligations (i.e. debt with an original term of less than 183 days suchas Commercial Paper, Repurchase Agreements, certain Treasury Bills).

• Foreign source income – non-U.S. source income.

• Excluded non-financial payments.

EXCLUDED non-financial payments:

• Payments for services (including employee wages or other employee compensation like stock options).

• Payments for use of property.

• Payments for office and equipment leases and software licenses.

• Payments for transportation or freight.

• Payments for awards, prizes, gambling winnings, scholarships.

• Payments for interest on outstanding accounts payable (acquisition of goods or services).

• Payments for gross proceeds from sale of property giving rise to certain excluded non-financial payments.

• Bank custody fees, investment advisory fees, brokerage fees ARE NOT EXCLUDED.

253

Grandfathered Obligations

Grandfathered Obligations (GOs):• Obligations that are legally binding and outstanding as of 1 July 2014 that produces or could produce a

withholdable payment or foreign passthru payment, as well as the gross proceeds from the disposition ofsuch an obligation, but excludes:• Instruments treated as equity for U.S. tax purposes.

• Instruments that lack a stated expiration, term, or maturity date.

• Brokerage, custodial, or other similar agreements to hold financial assets for the account of others.

• Derivatives (ISDA) Master Agreements that set forth general terms (not individual MA Confirmations).

• Examples include: debt instruments; lines of credit; revolving credit agreements (fixed maturity andmaterial terms); term annuity contract; derivatives transaction

Modified GOs:• GO’s that are subject to “material modification” will be treated as newly issued on the date of

modification and will not benefit from FATCA exemptions any more.

• Material modification includes a significant amendment of terms of obligation, such as changesin the underlying obligor or security, timing of payments leading to a material deferral ofscheduled payments, the yield (by more than the greater of 5% annual yield or 25 basis points).

264

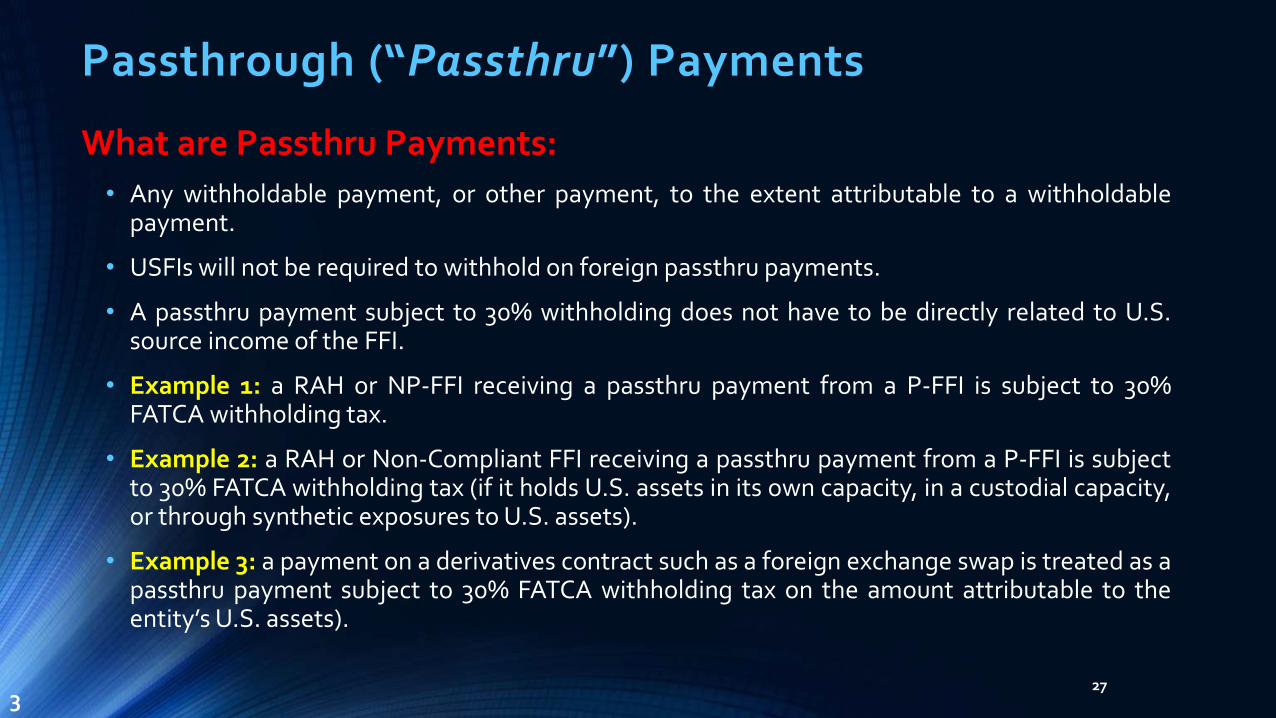

Passthrough (“Passthru”) Payments

What are Passthru Payments:

• Any withholdable payment, or other payment, to the extent attributable to a withholdablepayment.

• USFIs will not be required to withhold on foreign passthru payments.

• A passthru payment subject to 30% withholding does not have to be directly related to U.S.source income of the FFI.

• Example 1: a RAH or NP-FFI receiving a passthru payment from a P-FFI is subject to 30%FATCA withholding tax.

• Example 2: a RAH or Non-Compliant FFI receiving a passthru payment from a P-FFI is subjectto 30% FATCA withholding tax (if it holds U.S. assets in its own capacity, in a custodial capacity,or through synthetic exposures to U.S. assets).

• Example 3: a payment on a derivatives contract such as a foreign exchange swap is treated as apassthru payment subject to 30% FATCA withholding tax on the amount attributable to theentity’sU.S. assets).

273

Passthrough (“Passthru”) Payments

What we currently know about Passthru Payments:

• P-FFIs will not be obliged to trace passthru payments to NP-FFIs or RAHs (tracing method rejected by IRS).

• P-FFIs will be obliged to withhold 30% tax on passthru payments made to NP-FFIs or RAHs.

• This applies even on non-U.S. source payments.

• The amount of the passthru payment will likely be based on the FFI’s Passthru PaymentPercentage (PPP) (Notice 2011-34).

• PPP is a mathematical formula under which a % of non-U.S. source payments will be deemedattributable to U.S. sources, according to FFI’s ratio of (U.S. assets : non-U.S. assets).

• A FFI that does not calculate or publish their PPP will be deemed to have a PPP of 100%.

283

Sum of U.S. assets (held on each of last 4 quarterly testing dates)

Sum of total assets (held on each of last 4 quarterly testing dates)

29

30

Presentation Information

DECLARATION OF CONFLICTING INTERESTSThe author declares that to the best of his knowledge he has no potential conflicts of interest with respect to the research orauthorship of this presentation.

ABOUT THE PRESENTERRodrigo Zepeda is an independent consultant who specialises in derivatives and financial services law, regulation, andcompliance. He holds a LLM Masters degree in International and Comparative Business Law, has been an Associate of theChartered Institute for Securities and Investment since 2004, and has passed the New York Bar Examination. He has alsopublished widely in leading industry journals such as the Capco Institute’s Journal of Financial Transformation, the Journal ofInternational Banking Law and Regulation, as well as e-books on derivatives law. Noted publications include “Optimizing RiskAllocation for CCPs under the European Market Infrastructure Regulation”; “The ISDA Master Agreement 2012: A MissedOpportunity”; “The ISDA Master Agreement: The Derivatives Risk Management Tool of the 21st Century?”; and “To EU, or not toEU: that is the AIFMD question”.

CONTACT DETAILSEmail: [email protected]: http://www.linkedin.com/in/rodrigozepedaMobile: UK + (0)7592457373

The Foreign Account Tax Compliance Act (FATCA)

The Three Pillars of FATCA

SESSION 3

Training ProgrammeFATCA for LATAM Firms

23-24 February 2015 (Panama City), 25 -26 February 2015 (Santo Domingo)

Rodrigo ZepedaIndependent Consultant