“The Strategy of REpower and expectations to subcontractors” · “The Strategy of REpower and...

27

SOURCE: REpower Systems SE “The Strategy of REpower and expectations to subcontractors” Lars Rytter, COO Hamburg December 2 nd , 2013

Transcript of “The Strategy of REpower and expectations to subcontractors” · “The Strategy of REpower and...

SOURCE: REpower Systems SE 1

“The Strategy of REpower and expectations to subcontractors” Lars Rytter, COO Hamburg December 2nd, 2013

SOURCE: REpower Systems SE 2

Agenda

- Introduction

- REpower in a “Nutshell”

“ The Market

- REpower Strategy 2013-2018

- Expectations to Subcontractors

- Q & A

1

2

3

4

5

6

SOURCE: REpower Systems SE 3

Introduction

Lived and worked in China, India, the Netherlands and in

Hamburg; Germany since 2008 18 years of experience in the wind turbine industry 1995-2005 Vice President Strategic Purchasing and Logistics

at Vestas Wind Systems A/S 2006-2008 Chief Supply Chain Officer for Suzlon 2008-2010 Chief Supply Chain Officer for REpower Systems 2011-2013 Chief Procurement Officer of Nordex SE 2013, August Chief Operating Officer for REpower Systems COO at REpower; 1400 employees, 8 factories in 3 continents

Lars Rytter Chief Operating Officer (COO) of REpower Systems SE

SOURCE: REpower Systems SE 4

Agenda

- Introduction

- REpower in a “Nutshell”

“ The Market

- REpower Strategy 2013-2018

- Expectations to Subcontractors

- Q & A

1

2

3

4

5

6

SOURCE: REpower Systems SE 5

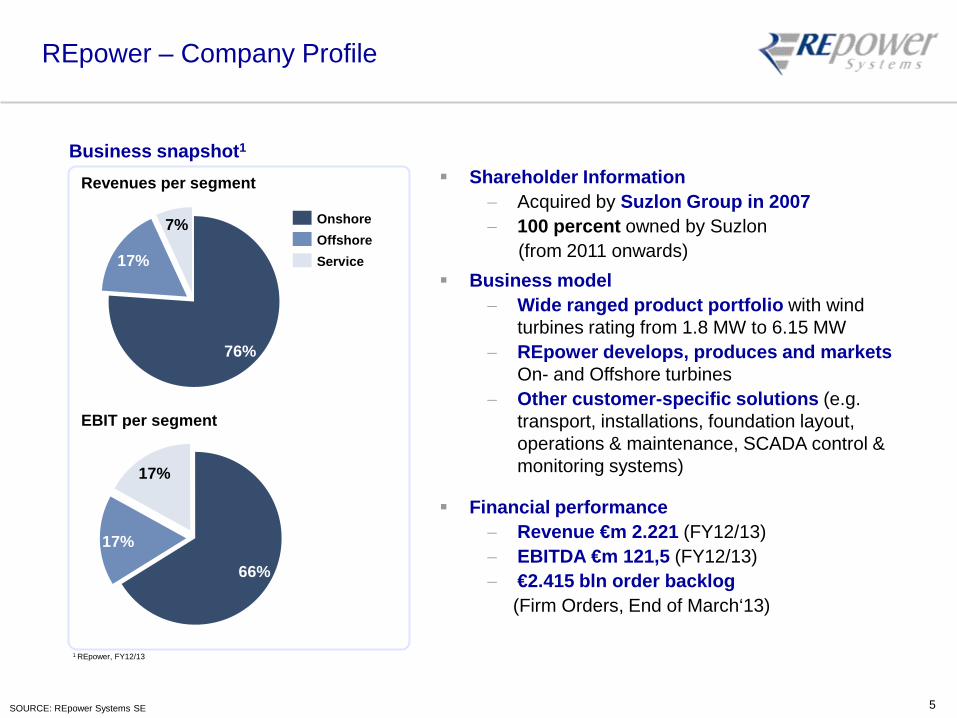

REpower – Company Profile

Shareholder Information − Acquired by Suzlon Group in 2007 − 100 percent owned by Suzlon (from 2011 onwards)

Business model − Wide ranged product portfolio with wind

turbines rating from 1.8 MW to 6.15 MW − REpower develops, produces and markets

On- and Offshore turbines − Other customer-specific solutions (e.g.

transport, installations, foundation layout, operations & maintenance, SCADA control & monitoring systems)

Financial performance − Revenue €m 2.221 (FY12/13) − EBITDA €m 121,5 (FY12/13) − €2.415 bln order backlog (Firm Orders, End of March‘13)

7%

17%

76%

Service Offshore Onshore

Revenues per segment

17%

17%

66%

EBIT per segment

Business snapshot1

1 REpower, FY12/13

SOURCE: REpower Systems SE 6

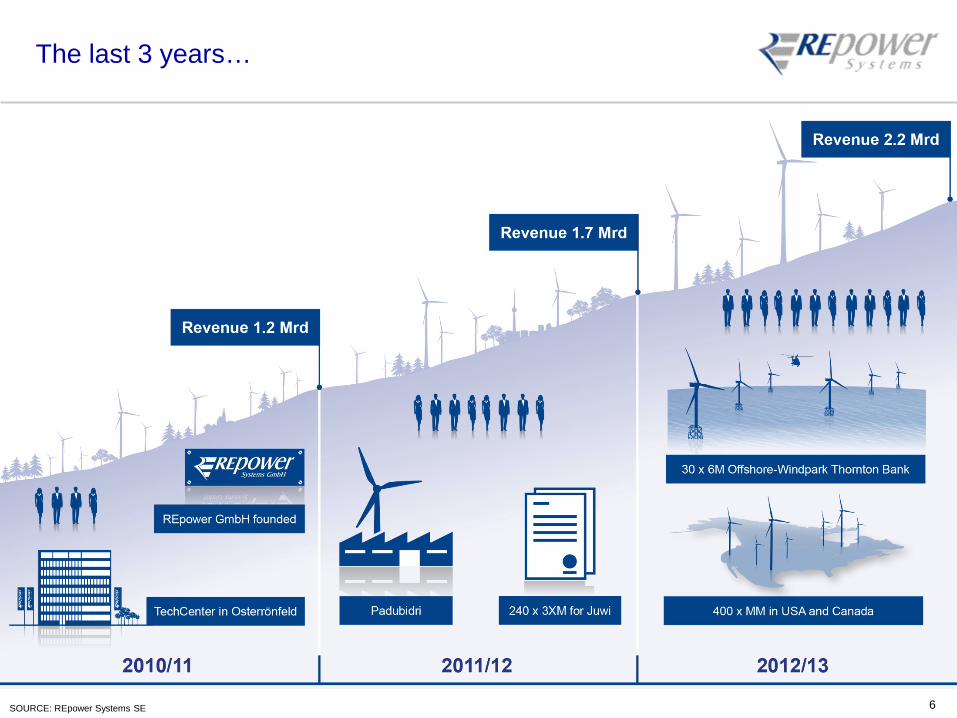

The last 3 years…

SOURCE: REpower Systems SE 7

6 Months with “POWER“

SOURCE: REpower Systems SE 8

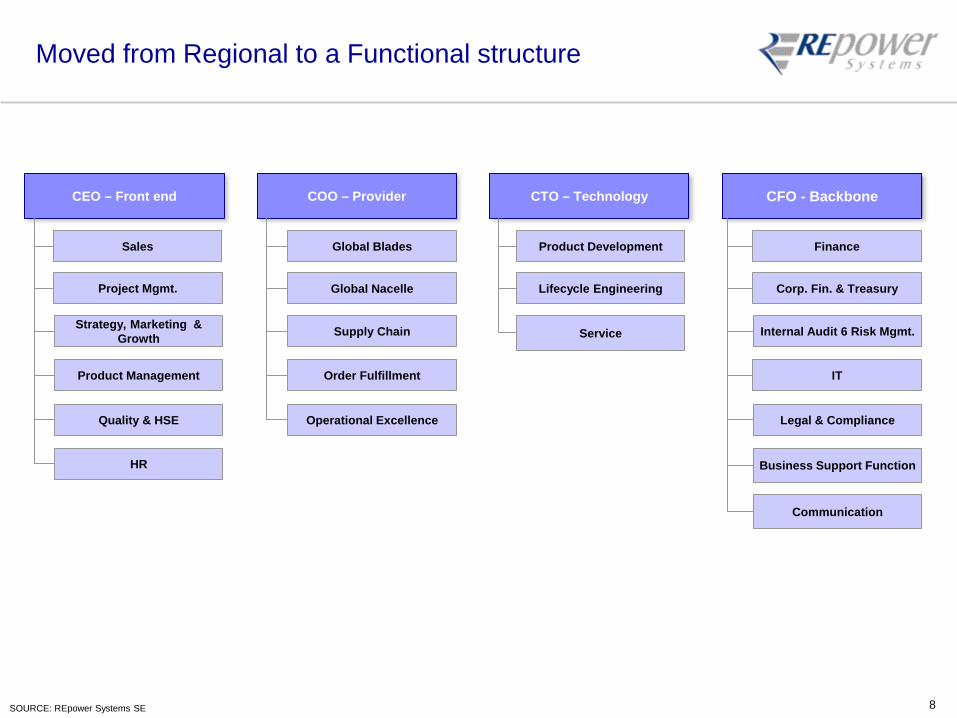

Moved from Regional to a Functional structure

CEO – Front end

Sales

Strategy, Marketing & Growth

HR

Quality & HSE

Product Management

Project Mgmt.

COO – Provider

Global Blades

Global Nacelle

Supply Chain

Order Fulfillment

Operational Excellence

CTO – Technology

Lifecycle Engineering

Service

Product Development Finance

IT

Legal & Compliance

CFO - Backbone

Corp. Fin. & Treasury

Internal Audit 6 Risk Mgmt.

Business Support Function

Communication

SOURCE: REpower Systems SE 9

REpower footprint based in Europe and in key emerging markets

REpower Systems Inc. SBU: Montreal Blade production: Ontario

Current footprint

REpower France SBU: La Défense

REpower USA Corp SBU: Denver REpower Portugal

SBU: Oliveira de Frades Nacelle assembly: Oliveira de Frades Blade production: Vagos

REpower Germany HQ: Hamburg Nacelle assembly: Trampe, Husum, Bremerhaven Blade production: Bremerhaven R&D: Osterroenfeld, Buedelsdorf, Osnabrück

REpower Italy SBU: Milano

REpower North (China) Nacelle assembly: Baotou

REpower Beijing Office Sourcing: Beijing

REpower Australia SBU: Melbourne

India Contract manufacturing

REpower UK SBU: Edinburgh

SOURCE: REpower Systems SE 10

Technology - Product Portfolio An introduction - Evolution of REpower turbines

MD 70

1998 2000

MD 77

2002

MM 70

MM 82

2003 2004

5M

MM 92

2005

MM100

2008

6.2M126

2009 2011

3.2M114

3.4M104

3.0M122

2013 2015

6.2M152

Vorführender

Präsentationsnotizen

Zweck: Produktstrategie erläutern

SOURCE: REpower Systems SE 11

Markets Around 9.4 GW installed across the world

Germany

Italy, Austria, Hungary

& Switzerland

France

UK

Belgium & Netherland

Canada

China

India

Japan

N. America Canada 564 USA 1,264 Total 1,828

Portugal & Spain

Europe

Germany 2,446

France 1,492 UK 1104 Italy 774 Others 1251 Total 7,067

Asia China 234 Japan 118 India 23 Total 375

Australia Total 159

Czech Republic

Poland

Australia

USA

REpower Global Installations in MW1

1As of Oct 2013; Includes all installed and SCADA connected systems; 2. REpower installation from 1987 onwards

Sweden

SOURCE: REpower Systems SE 12

REpower current production footprint has facilities in Europe and Asia to supply key markets

5

8

4

3 1 2

6

Location Type Current Capacity Ownership

Nacelle/hub [MW] Husum GER MM-Series 1000 100% REpower Trampe GER 3.XM 340 100% REpower Bremerhaven GER 3.XM, 5/6M 900 100% REpower

Oliveira de Frades POR MM-Series 300 Owned by Ventinveste, 100% controlled and operated by REpower

Padubidri IND MM-Series 800 “Job Order Contract” with Suzlon Baotou CHN MM-Series 0 Joint Venture / Exit done

Total hub & nacelle 3,340 Own Blade Production [Sets of 3 blades]

Bremerhaven GER RE 51/61 650 100% REpower, PowerBlades Vagos POR RE 45/51 700 100% REpower, RiaBlades Ontario CAN RE45 125 100% REpower

Total blade sets 1,475

7

1 2 3

4

5 6

7 8 9

9

SOURCE: REpower Systems SE 13

Manufacturing footprint Manufacturing & logistics center - Bremerhaven (Germany)

REpower production hall 3.XM / 5M / 6M

PowerBlades rotor blade factory

SOURCE: REpower Systems SE 14

Agenda

- Introduction

- REpower in a “Nutshell”

“ The Market

- REpower Strategy 2013-2018

- Expectations to Subcontractors

- Q & A

1

2

3

4

5

6

SOURCE: REpower Systems SE 15

There is a lot of juice in the global wind market

+4% p.a.

20181

6.8

4.1

2.2

0.5

2010

5.2

3.4

1.4 0.4

Fossil Renewables Nuclear

Renewables will grow their share ... ... with wind as 2nd largest source

1. Interpolated from 2010/2020 numbers 2. Includes solar and bio energy Note: Hydro energy is counted as renewable energy source Source: REpower market model for wind energy forecast; IEA 2012 World Energy Outlook (new policies scenario) for other generating technologies;

Global electricity generation (TW)

+6% p.a.

20181

2.2

1,2

0.6

0.4

2010

1.4

1.0

0.2 0.1

Global renewable electricity generation (TW)

Hydro Wind Other2

SOURCE: REpower Systems SE 16

Outlook wind turbine market: After the record year 2012 macro headwinds imposed strong challenges in 2013

Global market shrinking for the first time in 2013 (due to policy implications)

Policy deterioration in major parts of Europe (Germany, Spain, and Italy)

Global new order intake slowed in Q2 2012 but in 2013 a small improvement has been registered

Macro trends

21 20 21 22 2326

10 1011

1113

14

0

20

40

60 CAGR +10%

-1% +9%

Installations in GW

2016

58

6

12

2015

52

5

11

2014

48

4

11

2013

44

3

9

2012

45

2

13

2011

41

1

9

Offshore Asia/Pacific EMEA Americas

Expected global installations of wind turbines

Note: 2011 EMEA installation based on EWEA; Americas, Asia, and Offshore installation based on GWEC; 2012–2016 based on market model (mean of most recent studies: MAKE (11/12), BTM (03/12), SAT (09/12) Source: REpower 2013

SOURCE: REpower Systems SE 17

Agenda

- Introduction

- REpower in a “Nutshell”

“ The Market

- REpower Strategy 2013-2018

- Expectations to Subcontractors

- Q & A

1

2

3

4

5

6

SOURCE: REpower Systems SE 18

Offshore – REpower projects Beatrice – alpha ventus – Ormonde – Thornton Bank

Vorführender

Präsentationsnotizen

Zum Schluss einige Impressionen der bisher durch uns realisierten Offshore Parks Beatrice, Thornton Bank, Alpha Ventus und Ormonde.

SOURCE: REpower Systems SE 19

Agenda

- Introduction

- REpower in a “Nutshell”

“ The Market

- REpower Strategy 2013-2018

- Expectations to Subcontractors

- Q & A

1

2

3

4

5

6

SOURCE: REpower Systems SE 20

Current development state of wind industry impacts

Global network required with local manufacturing hubs, content & suppliers

Shorter lead times / order fulfillment cycle required

Efficient inventory management, working capital reduction required

Wider reach and availability of service and spares required

Quality, Time & Cost matters…

Scale − Move to industrialization phase

Reliability − Product quality to ensure better

value proposition to end-customer

Cost − Improving margins through efficient

operations and asset utilization

Implications for supply chain Key success factors in current industry situation

SOURCE: REpower Systems SE 21

Customer`s perspective

Customers in the past

Investment approx. 1-5 Mio.$

Turbines out of the shelf

Product functionality

Current Customers

Investment > 1 Mrd. $ Powerplant approach Product-/ Process Quality

- Manufacturing procedures - Quality procedures

Risk Management -comprehensive, professional

Documentation - proof of product Quality - proof of process Quality

Fundamental Paradigm Change in Customer Requirements

Preventive Quality Approach is essential !

to

SOURCE: REpower Systems SE 22

Cost of Quality: Rule of 10‘s

Failures to be avoided at suppliers in order to minimize total Cost of Quality.

@ Supplier

€ / 1.000

@ REpower GM

€ / 10.000 € / 100.000 € / 1.000.000

On-shore WTG Off-shore WTG

10x 10x 10x

SOURCE: REpower Systems SE 23

REpower requirements to our supply partners

Commercial requirements: Continuous effort required to support declining market prices

o Value Engineering o Globalization of Supply Chain o Improvement of productivity o Payment term extension

Performance requirements; Excellent execution: o OTD (on-time delivery) - and increased flexibility to changing market needs o High level quality / zero failure culture / preventive quality approach o Implementation of APQP-requirements (Advanced Product Quality Planning) o QAA (Quality Assurance Agreement)

Responsiveness o Fast reaction times & handling of non-conformities o Close cooperation with REpower o Improved reliability

Service support: Availability of spare parts, 24/7 hotline

SOURCE: REpower Systems SE 24

Agenda

- Introduction

- REpower in a “Nutshell”

“ The Market

- REpower Strategy 2013-2018

- Expectations to Subcontractors

- Q & A

1

2

3

4

5

6

SOURCE: REpower Systems SE 25

Time for your questions…

SOURCE: REpower Systems SE 26

New name as of January 20th, 2014…

SOURCE: REpower Systems SE 27