The State of Rental Housing in Ontario - FRPOfrpo.lws1.com/wp-content/uploads/2015/04/Major... ·...

47

1 The State of Rental Housing in Ontario Mike Chopowick Federation of Rental-housing Providers of Ontario (FRPO) SpringFest Trade Show Toronto April 10, 2014

Transcript of The State of Rental Housing in Ontario - FRPOfrpo.lws1.com/wp-content/uploads/2015/04/Major... ·...

1

The State of Rental

Housing in Ontario

Mike Chopowick

Federation of Rental-housing Providers of Ontario (FRPO)

SpringFest Trade Show

Toronto

April 10, 2014

2

Overview

1. The Big Picture: Rental Housing’s

Economic Impact

2. Housing construction and supply/vacancy

3. Where should you invest? Ontario’s

Strongest Markets

4. Forget the Baby-Boomers

5. The Future: Low unemployment & low

inflation

3

Overview

6. Hydro and Gas Prices

7. Municipal Act Pitfalls

8. Poverty and Affordability

9. Immigration: The Great Exodus

10 .Renting is the New Normal

Fundamentals

Rental Housing: A Big Industry

4

Rental Housing by

Comparison (GDP 2012)

Manufacturing $76.1 billion

Finance and Insurance $51.8 billion

Construction (Total) $32.8 billion

Food and Beverage Industry $26.2 billion

Tourism Industry (Total) $19.5 billion

Rental Housing Industry $18.3 billion

Defence Industry $13.9 billion

Aeropace Industry $11.2 billion

Mining and oil and gas $6.5 billion

Agriculture, forestry, fishing & hunting $4.7 billion

Arts and Culture Industries $3.7 billion Source: Statistics Canada GDP CANSIM table 379-0030, 2013; KPMG 2013, Economic Impact Assessment Study – Federation of Rental Housing Providers of

Ontario; Ontario Ministry of Tourism, Culture and Sport, 2013; Ontario Arts Council, 2012.

5

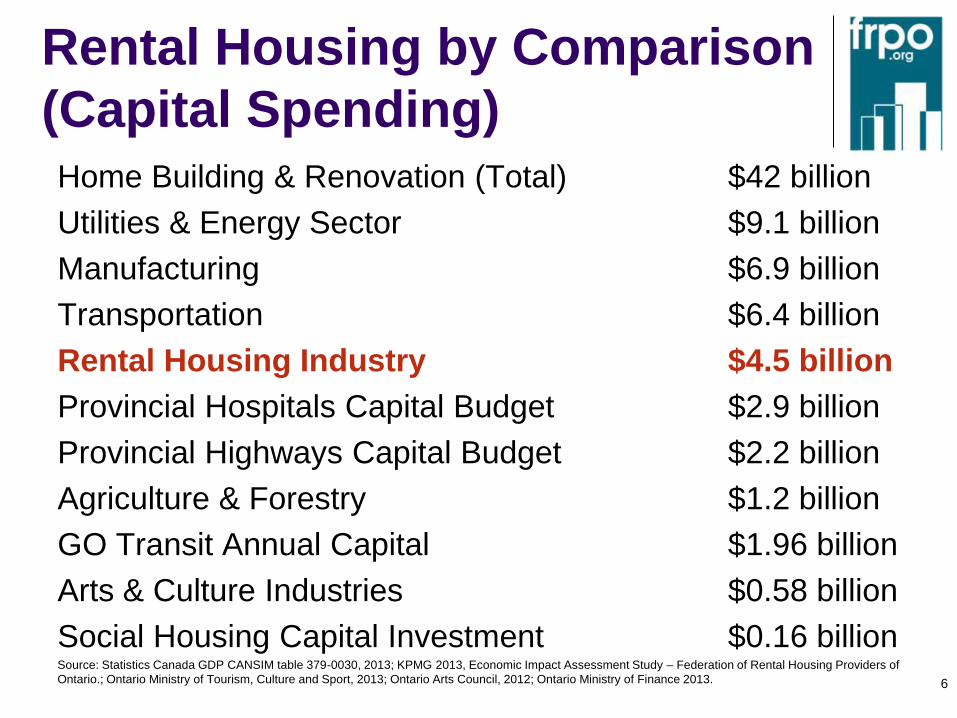

Rental Housing by Comparison

(Capital Spending) Home Building & Renovation (Total) $42 billion

Utilities & Energy Sector $9.1 billion

Manufacturing $6.9 billion

Transportation $6.4 billion

Rental Housing Industry $4.5 billion

Provincial Hospitals Capital Budget $2.9 billion

Provincial Highways Capital Budget $2.2 billion

Agriculture & Forestry $1.2 billion

GO Transit Annual Capital $1.96 billion

Arts & Culture Industries $0.58 billion

Social Housing Capital Investment $0.16 billion Source: Statistics Canada GDP CANSIM table 379-0030, 2013; KPMG 2013, Economic Impact Assessment Study – Federation of Rental Housing Providers of

Ontario.; Ontario Ministry of Tourism, Culture and Sport, 2013; Ontario Arts Council, 2012; Ontario Ministry of Finance 2013.

6

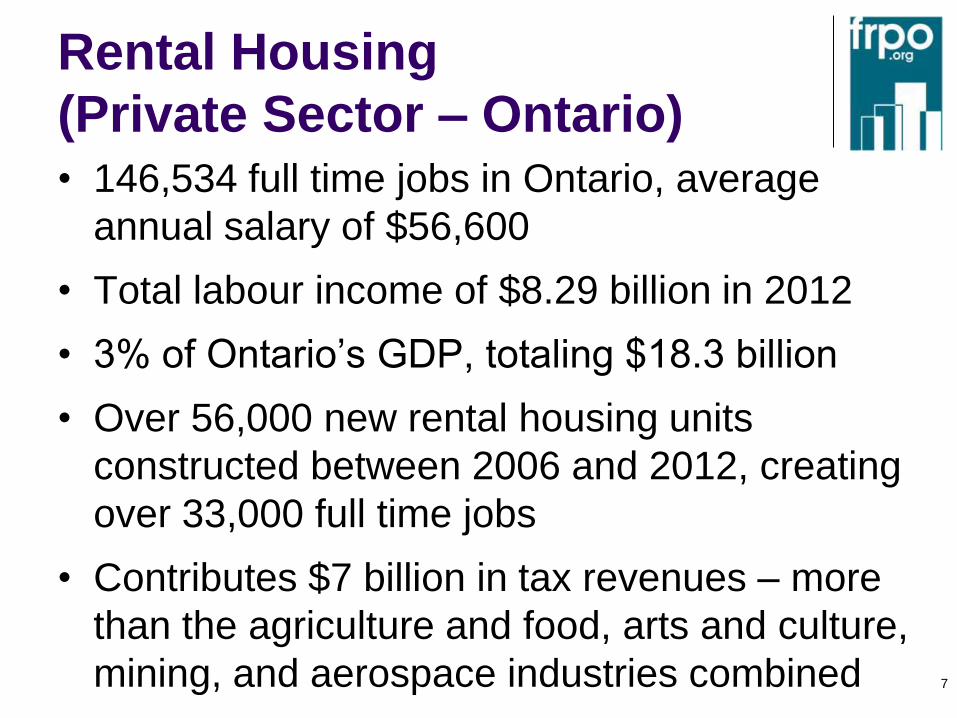

Rental Housing

(Private Sector – Ontario)

7

• 146,534 full time jobs in Ontario, average

annual salary of $56,600

• Total labour income of $8.29 billion in 2012

• 3% of Ontario’s GDP, totaling $18.3 billion

• Over 56,000 new rental housing units

constructed between 2006 and 2012, creating

over 33,000 full time jobs

• Contributes $7 billion in tax revenues – more

than the agriculture and food, arts and culture,

mining, and aerospace industries combined

Housing Construction

& Vacancy

8

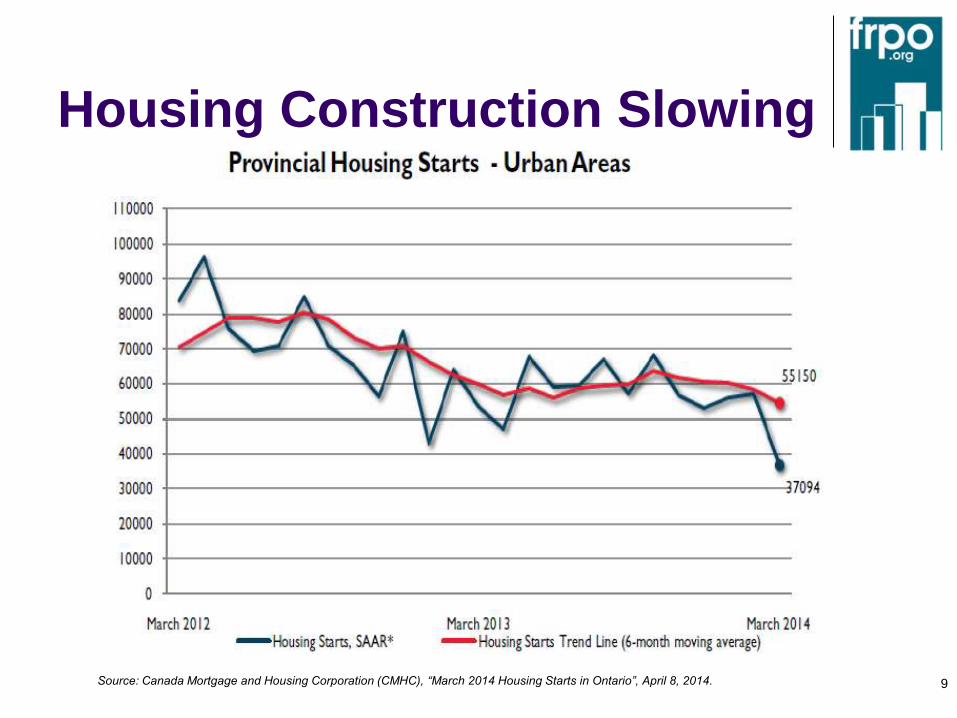

Housing Construction Slowing

9 Source: Canada Mortgage and Housing Corporation (CMHC), “March 2014 Housing Starts in Ontario”, April 8, 2014.

Vacancy Rates in Long-Term

Decline

10

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

2005 2006 2007 2008 2009 2010 2011 2012 2013

Source: CMHC Housing Observer 2013, Housing Market Indicator Data Tables

Average Vacancy Rates (Ontario)

Ontario’s strongest

markets

11

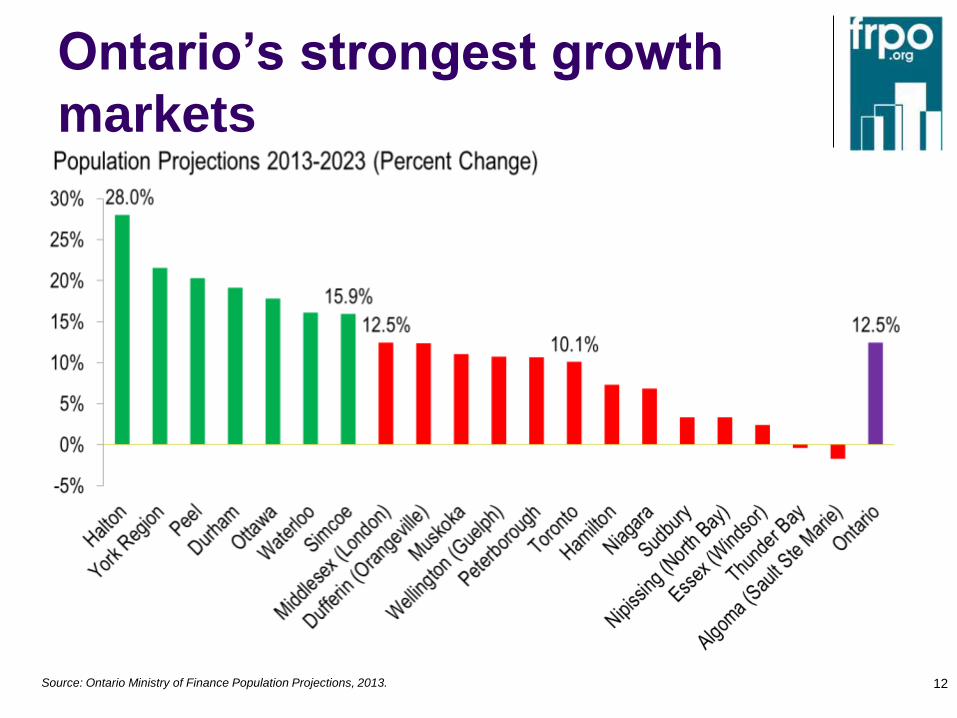

Ontario’s strongest growth

markets

12 Source: Ontario Ministry of Finance Population Projections, 2013.

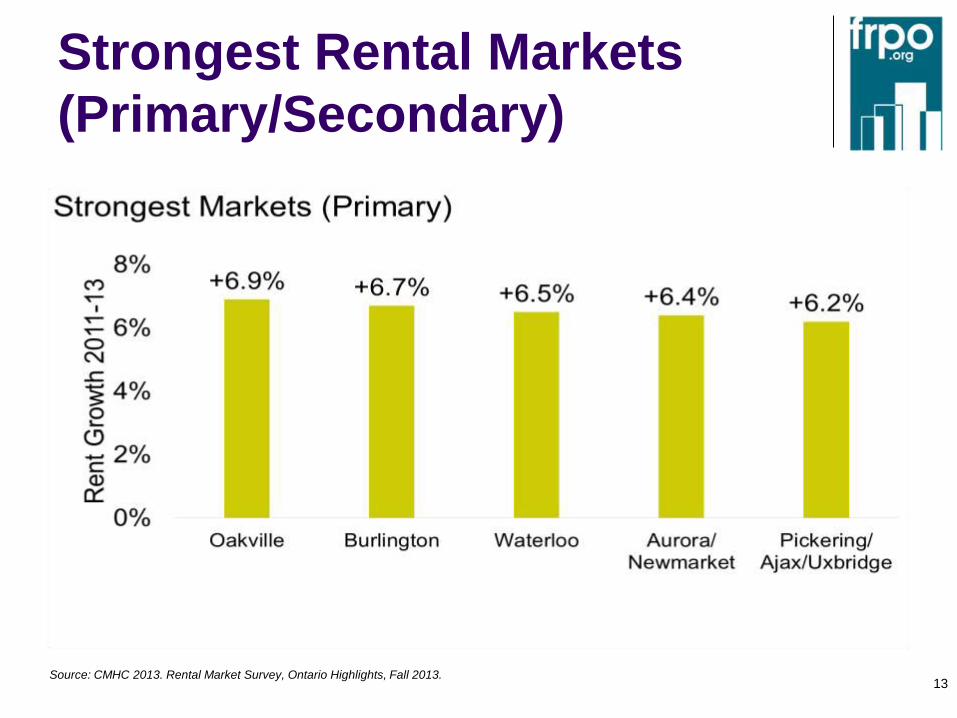

Strongest Rental Markets

(Primary/Secondary)

13 Source: CMHC 2013. Rental Market Survey, Ontario Highlights, Fall 2013.

Strongest Markets

(Secondary/Tertiary)

14 Source: CMHC 2013. Rental Market Survey, Ontario Highlights, Fall 2013.

Forget the Baby

Boomers

Meet the Millennials

15

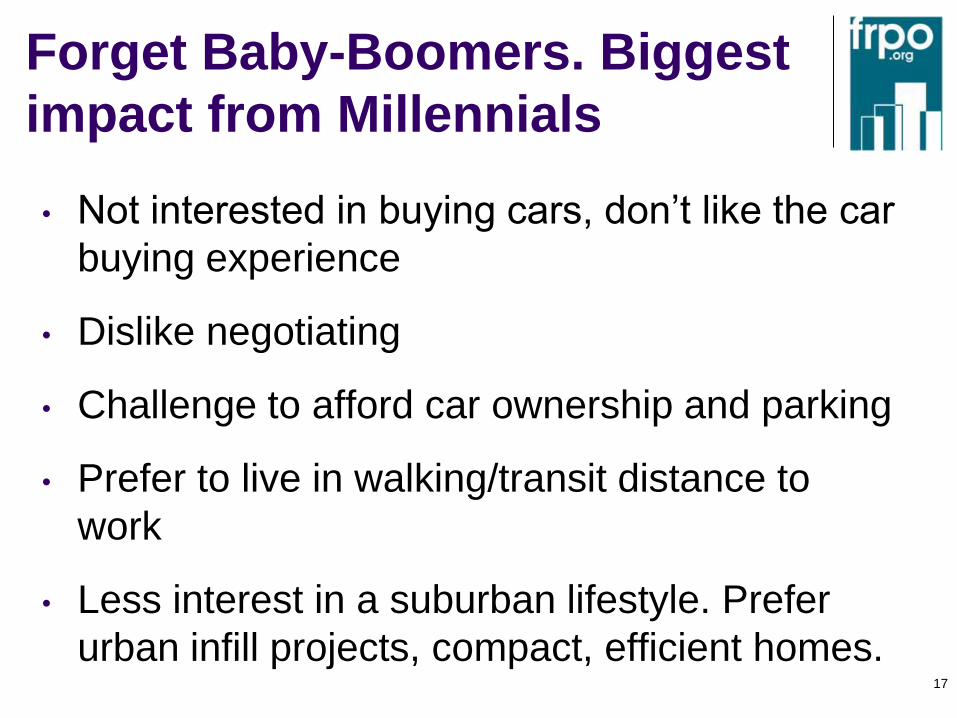

Forget Baby-Boomers. Biggest

Impact from Millennials • Born between 1980-2000

• Now in young-adulthood, teens (Ages 15-35)

• 8.9 million in Canada. 4.5 million live with heir

parents. 700,000 unemployed. $225 billion in

labour income.

• Characteristics: Helicopter Parents,

Boomerang Kids, Peter Pan Generation,

Trophy Kids, Technologically Dependent,

“Underemployed”, Mobile, on-the-move.

16

Forget Baby-Boomers. Biggest

impact from Millennials

• Not interested in buying cars, don’t like the car

buying experience

• Dislike negotiating

• Challenge to afford car ownership and parking

• Prefer to live in walking/transit distance to

work

• Less interest in a suburban lifestyle. Prefer

urban infill projects, compact, efficient homes. 17

Millennials: Housing

Preferences

“An energy-sapping, high maintenance

money pit in the middle of nowhere.”

18

Millennials: Housing

Preferences

“Affordable, functional, hip, close to

work and friends.”

19

Millennials (Ages 15-35):

Key Demographic for Renting

20 Source: CMHC Rental Market Report - Greater Toronto Area - Date Released - Fall 2013

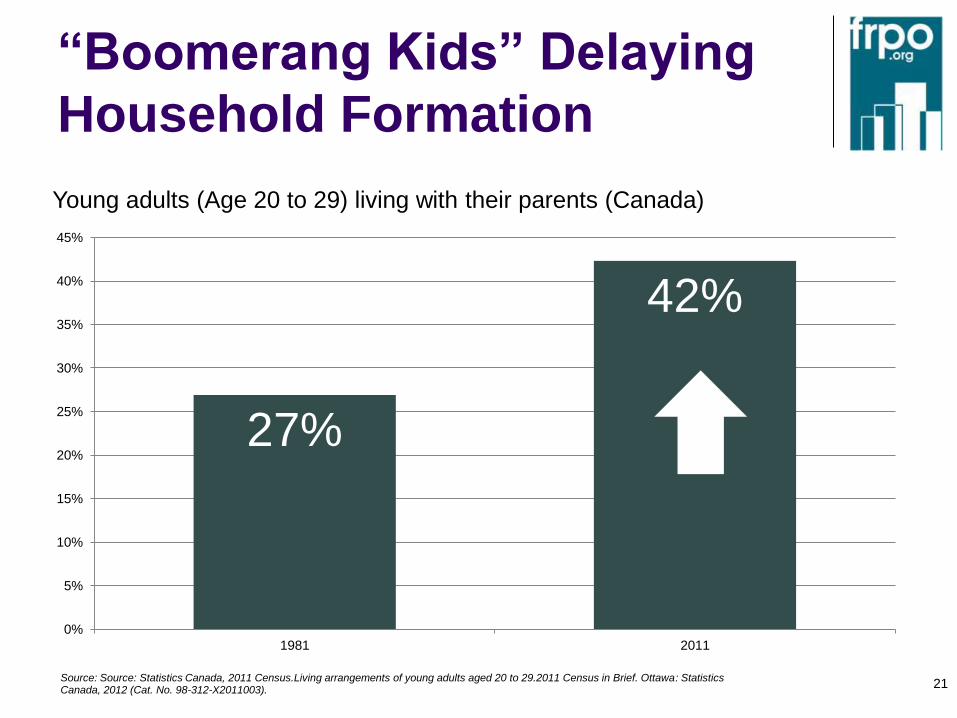

“Boomerang Kids” Delaying

Household Formation

21

27%

42%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1981 2011

Source: Source: Statistics Canada, 2011 Census.Living arrangements of young adults aged 20 to 29.2011 Census in Brief. Ottawa: Statistics Canada, 2012 (Cat. No. 98-312-X2011003).

Young adults (Age 20 to 29) living with their parents (Canada)

Low inflation & low

unemployment

22

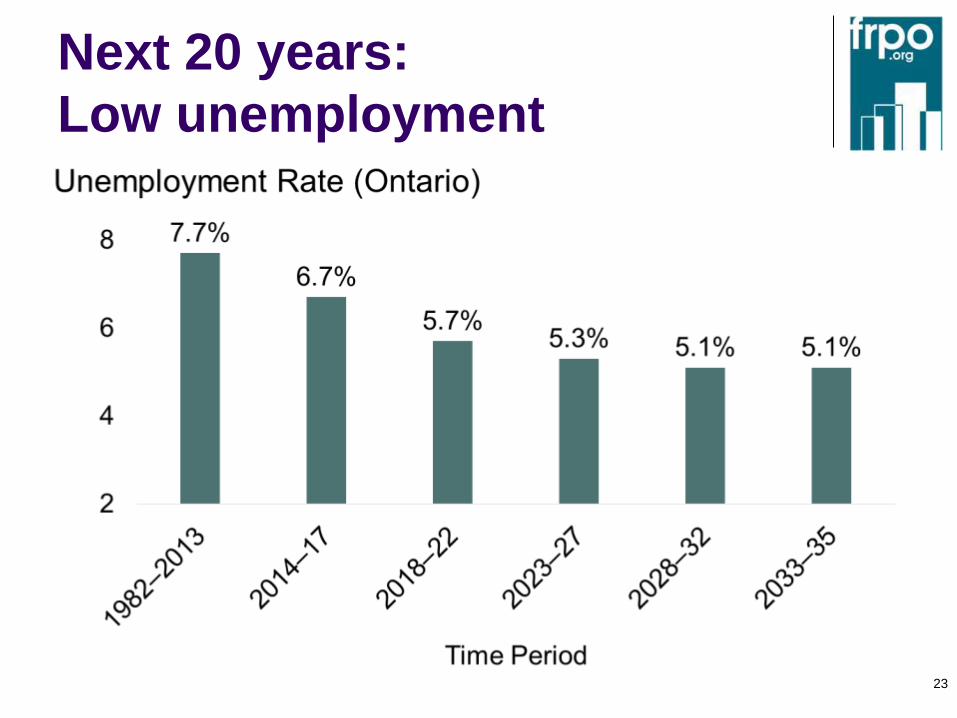

Next 20 years:

Low unemployment

23

Low unemployment

High unemployment is closely associated

with high levels of homeownership and vice

versa

High homeownership impairs the labour

market and mobility

Causes long commuting times and lowers

productivity

Homeowners oppose new development and

business investment in their neighbourhoods

24

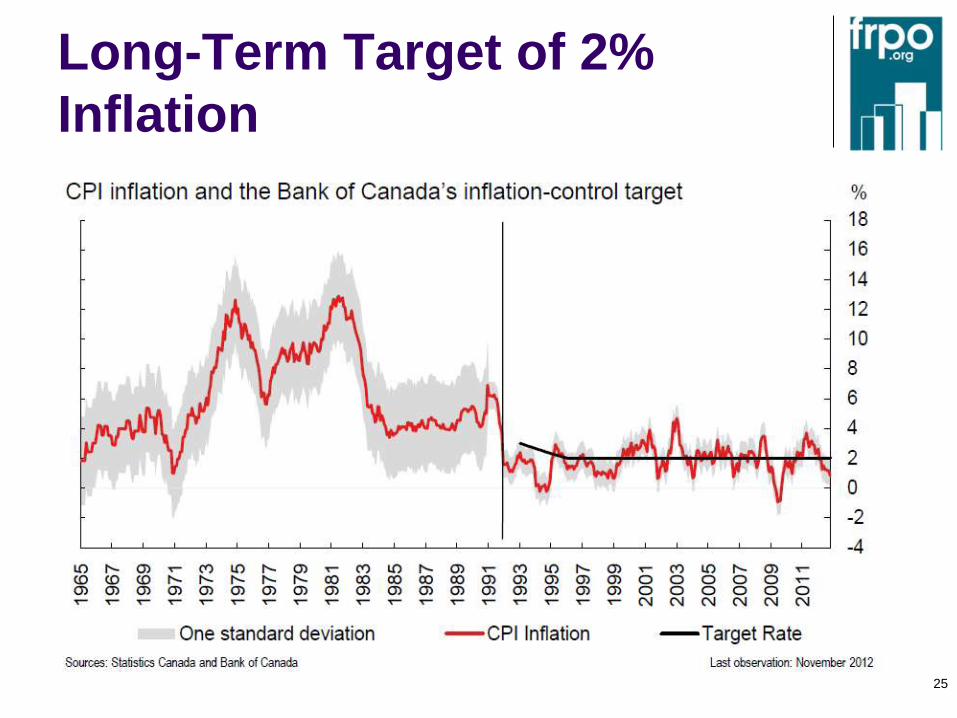

Long-Term Target of 2%

Inflation

25

Hydro and Gas Prices

Growing cost pressures

26

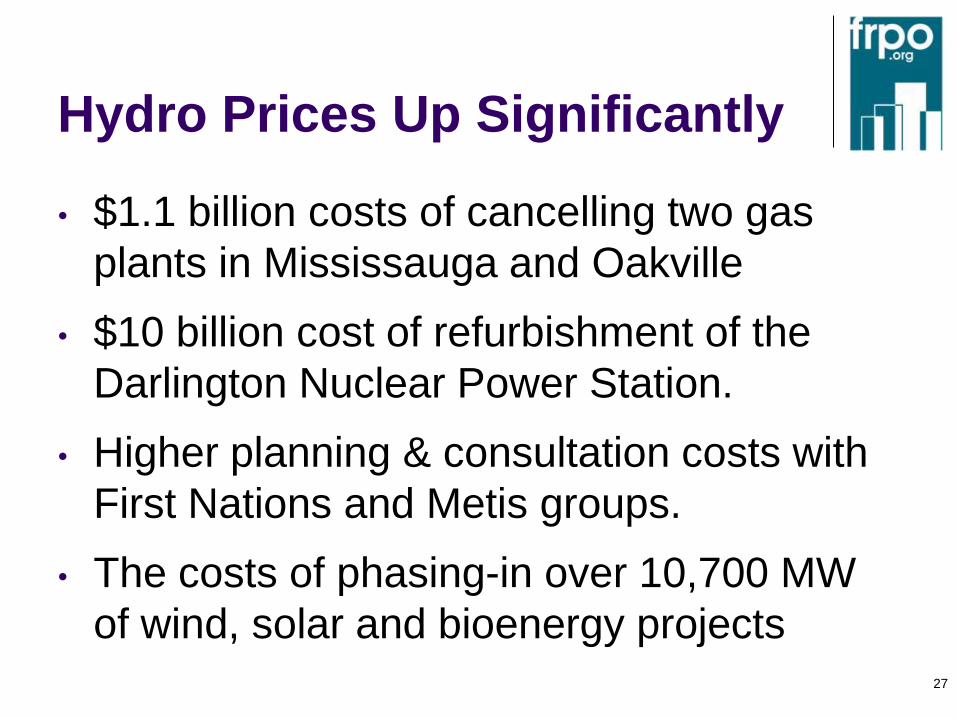

Hydro Prices Up Significantly

• $1.1 billion costs of cancelling two gas

plants in Mississauga and Oakville

• $10 billion cost of refurbishment of the

Darlington Nuclear Power Station.

• Higher planning & consultation costs with

First Nations and Metis groups.

• The costs of phasing-in over 10,700 MW

of wind, solar and bioenergy projects

27

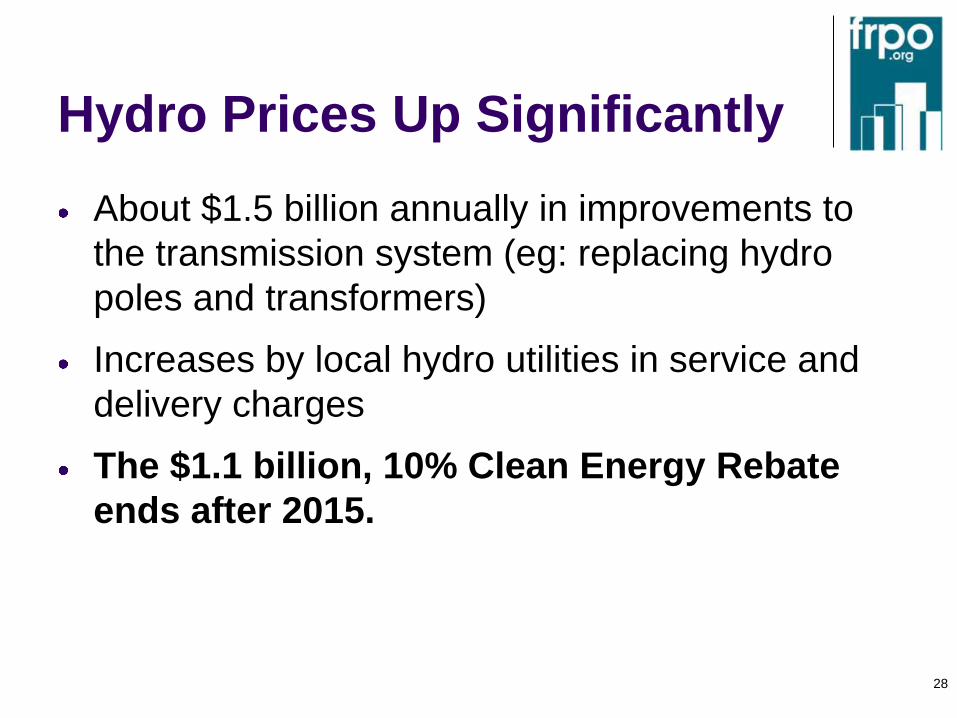

Hydro Prices Up Significantly

About $1.5 billion annually in improvements to

the transmission system (eg: replacing hydro

poles and transformers)

Increases by local hydro utilities in service and

delivery charges

The $1.1 billion, 10% Clean Energy Rebate

ends after 2015.

28

Future Hydro Price Hikes

29

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

An

nu

al In

crea

se (

%)

Typical Electricity Bill Forecast (10 Years) LTEP Forecast

"Realistic" Forecast

10%

OCEB

ends in

2016

Source: Ontario Ministry of Energy, 2013, Long Term Energy Plan; FRPO Calculations

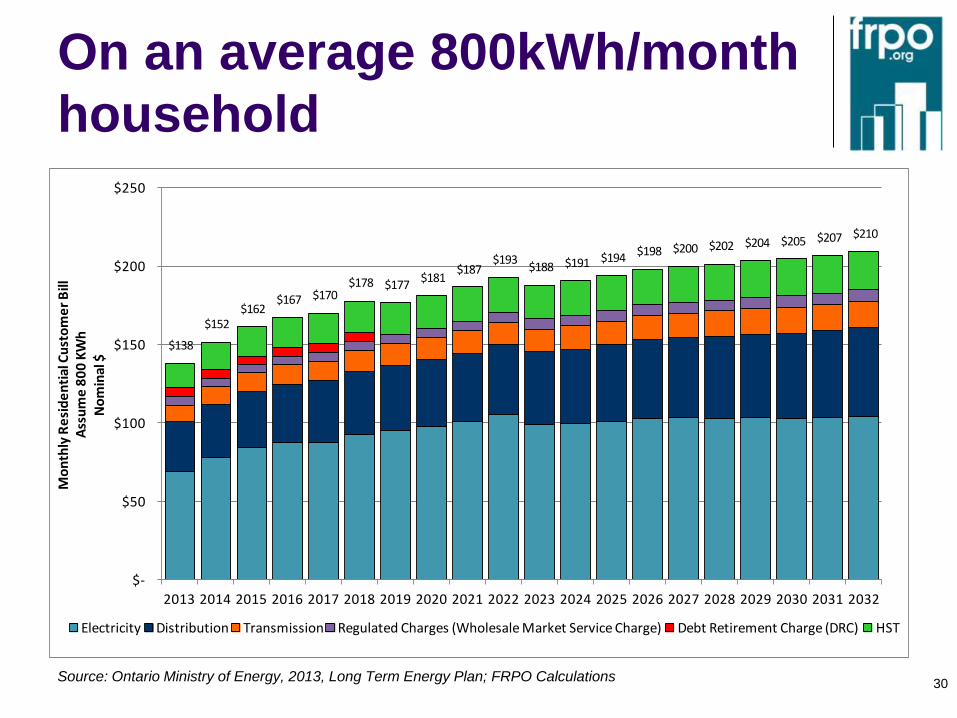

On an average 800kWh/month

household

30

$138

$152 $162

$167 $170 $178 $177

$181 $187

$193 $188 $191 $194

$198 $200 $202 $204 $205 $207 $210

$-

$50

$100

$150

$200

$250

2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032

Mo

nth

ly R

esi

de

nti

al C

ust

om

er

Bill

A

ssu

me

80

0 K

Wh

No

min

al $

Electricity Distribution Transmission Regulated Charges (Wholesale Market Service Charge) Debt Retirement Charge (DRC) HST

Source: Ontario Ministry of Energy, 2013, Long Term Energy Plan; FRPO Calculations

Hydro Prices Since 2002

31

Natural Gas: The Impact of

Cold • A long cold winter has dramatically impacted

natural gas prices

• NYMEX price increased 75% from Nov 2013

to Feb 2014

• Prices impacted by limited storage and

pipeline transmission capacity

• Hard to meet demand of long, cold winter

• Low inventory can impact supply for next

winter

• Storage levels at 10+ year lows 32

Natural Gas: The Impact of

Cold

33

$3.00

$3.25

$3.50

$3.75

$4.00

$4.25

$4.50

$4.75

$5.00

$5.25

$5.50

$5.75

$6.00

$6.25

1-A

pr-

13

15

-Ap

r-1

3

29

-Ap

r-1

3

13

-May

-13

27

-May

-13

10

-Ju

n-1

3

24

-Ju

n-1

3

8-J

ul-

13

22

-Ju

l-1

3

5-A

ug-

13

19

-Au

g-1

3

2-S

ep

-13

16

-Se

p-1

3

30

-Se

p-1

3

14

-Oct

-13

28

-Oct

-13

11

-No

v-1

3

25

-No

v-1

3

9-D

ec-

13

23

-Dec

-13

6-J

an-1

4

20

-Jan

-14

3-F

eb

-14

17

-Fe

b-1

4

3-M

ar-1

4

17

-Mar

-14

31

-Mar

-14

US$

/MM

Btu

Natural Gas Futures - Prompt Month(April 1, 2013 to March 31, 2014)

Gas prompt - NYMEX

Municipal Act Pitfalls

Licensing & Utility Arrears

34

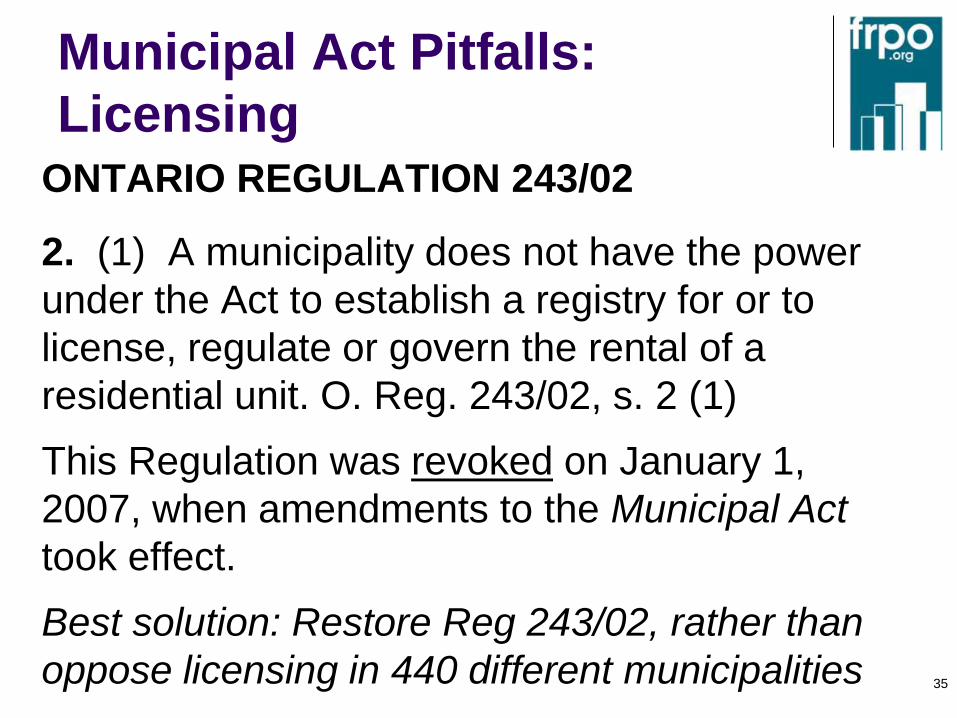

Municipal Act Pitfalls:

Licensing ONTARIO REGULATION 243/02

2. (1) A municipality does not have the power

under the Act to establish a registry for or to

license, regulate or govern the rental of a

residential unit. O. Reg. 243/02, s. 2 (1)

This Regulation was revoked on January 1,

2007, when amendments to the Municipal Act

took effect.

Best solution: Restore Reg 243/02, rather than

oppose licensing in 440 different municipalities 35

A big, new cost for landlords

and tenants – with no benefit

36

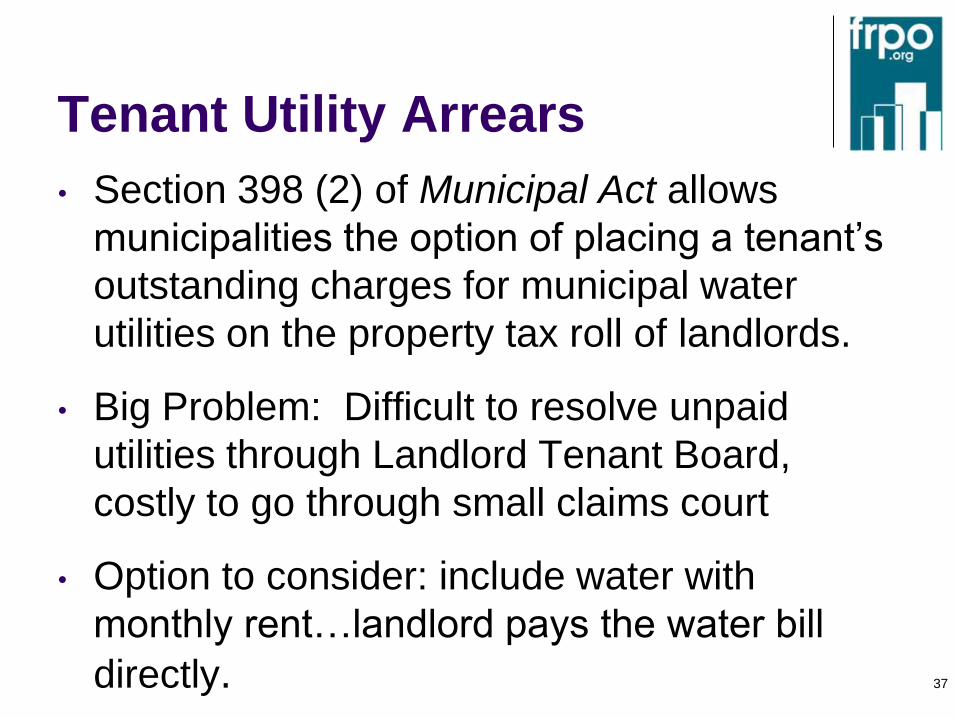

Tenant Utility Arrears

• Section 398 (2) of Municipal Act allows

municipalities the option of placing a tenant’s

outstanding charges for municipal water

utilities on the property tax roll of landlords.

• Big Problem: Difficult to resolve unpaid

utilities through Landlord Tenant Board,

costly to go through small claims court

• Option to consider: include water with

monthly rent…landlord pays the water bill

directly.

37

Poverty &

Affordability

38

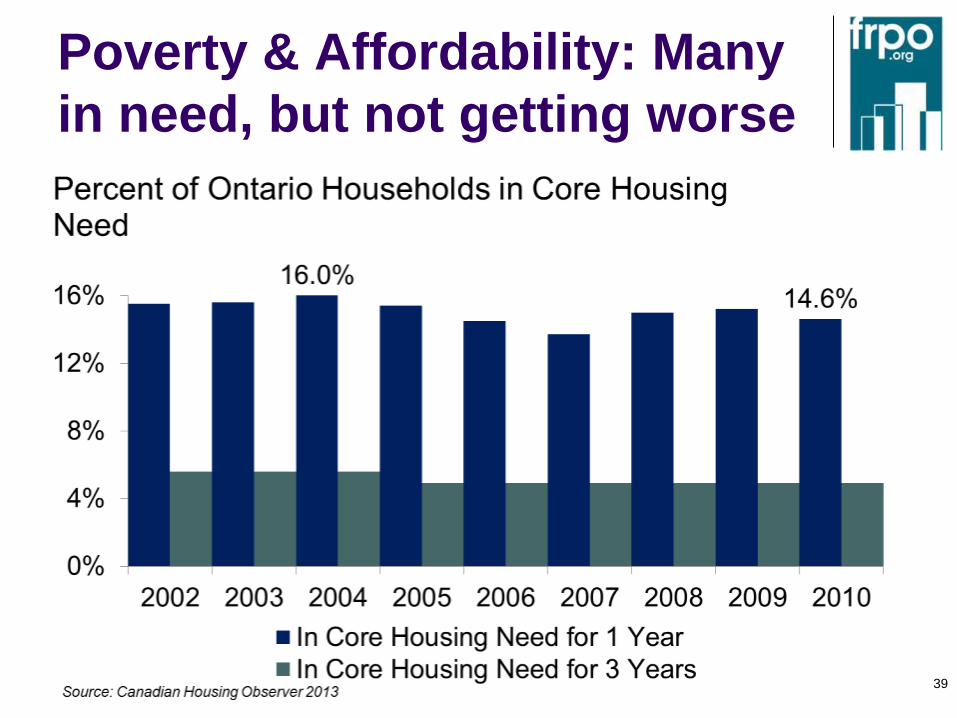

Poverty & Affordability: Many

in need, but not getting worse

39

Youth Unemployment:

Similar to previous recessions

40

Early 80’s

recession Early 90’s

recession

Late 00’s

recession

Immigration

41

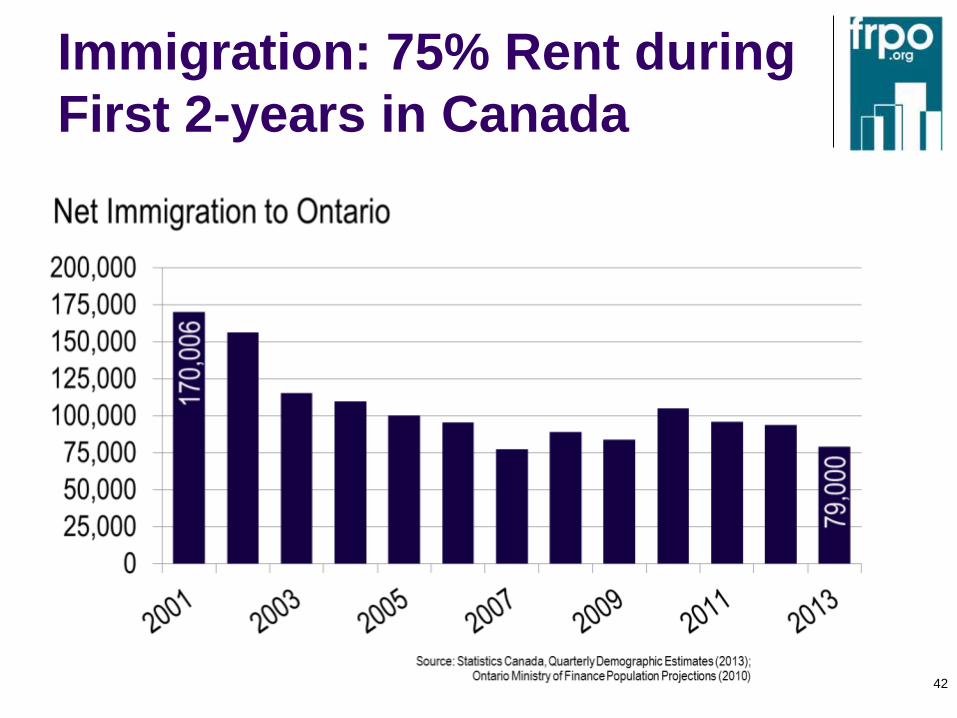

Immigration: 75% Rent during

First 2-years in Canada

42

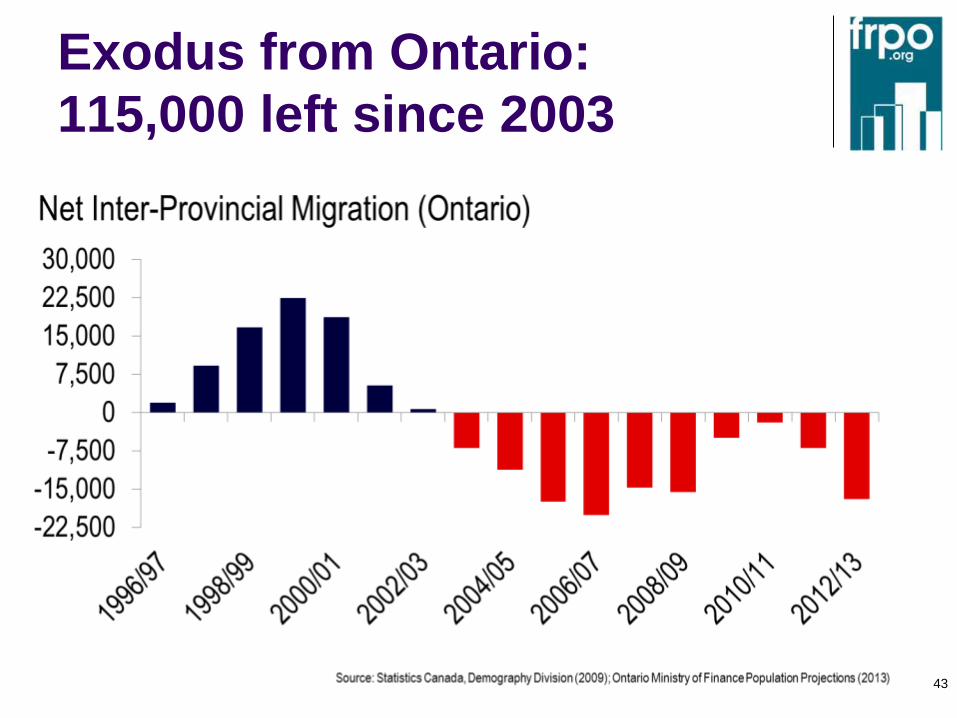

Exodus from Ontario:

115,000 left since 2003

43

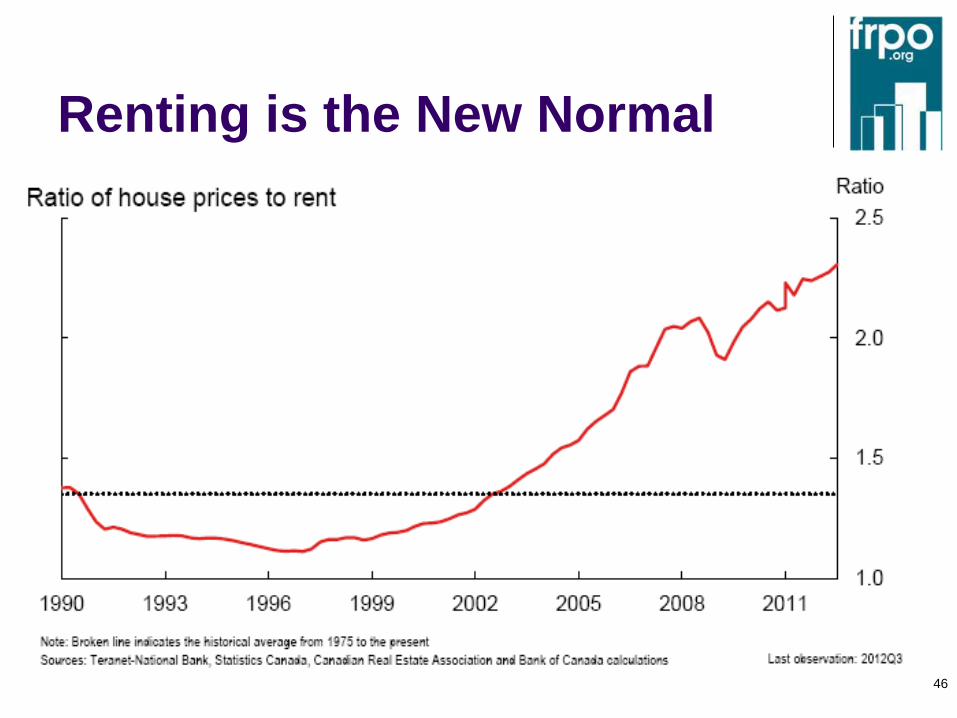

Renting is the New

Normal

44

Renting is the New Normal

45

Renting is the New Normal

46