The State of Facilities at Midwestern Institutions

17

Center University of Missouri – Columbia University of Missouri – Kansas City University of Missouri – St. Louis University of Nebraska at Kearney University of Nebraska at Lincoln University of Nebraska Medical Center University of Nebraska Omaha University of New Brunswick University of New Hampshire University of New Haven University of New Mexico University of North Texas University of Northern Iowa University of Notre Dame University of Oregon University of Ottawa University of Pennsylvania University of Redlands University of Rhode Island University of Rochester University of San Diego University of San Francisco University of Southern Maine University of Southern Mississippi University of St. Thomas University of Tennessee Health Science Center University of Tennessee, Knoxville University of Texas at Dallas University of the Sciences in Philadelphia University of Toledo University of Vermont University of Washington Vanderbilt University Virginia Commonwealth University Virginia Department of General Services Wagner College Wake Forest University Washburn University Washington University in St. Louis Wellesley College Wesleyan University West Chester University State of Facilities in Higher Education: 2015 Benchmarks, Best Practices, & Trends Midwestern Institutions

-

Upload

sightlines -

Category

Education

-

view

162 -

download

5

Transcript of The State of Facilities at Midwestern Institutions

University of Mississippi Medical

Center

University of Missouri – Columbia

University of Missouri – Kansas City

University of Missouri – St. Louis

University of Nebraska at Kearney

University of Nebraska at Lincoln

University of Nebraska Medical Center

University of Nebraska Omaha

University of New Brunswick

University of New Hampshire

University of New Haven

University of New Mexico

University of North Texas

University of Northern Iowa

University of Notre Dame

University of Oregon

University of Ottawa

University of Pennsylvania

University of Redlands

University of Rhode Island

University of Rochester

University of San Diego

University of San Francisco

University of Southern Maine

University of Southern Mississippi

University of St. Thomas

University of Tennessee Health

Science Center

University of Tennessee, Knoxville

University of Texas at Dallas

University of the Sciences in

Philadelphia

University of Toledo

University of Vermont

University of Washington

Vanderbilt University

Virginia Commonwealth University

Virginia Department of General

Services

Wagner College

Wake Forest University

Washburn University

Washington University in St. Louis

Wellesley College

Wesleyan University

West Chester University

State of Facilities in Higher Education: 2015 Benchmarks, Best Practices, & Trends

Midwestern Institutions

16%

24%

33%

27%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Midwest Region

% o

f S

pa

ce

2015 Age Profile

Under 10 10 to 25 25 to 50 Over 50

High Risk

% of Space Over 25 Years Old Continues to Rise

2

Roughly 60% of space is over 25 years old, which is a critical age threshold that threatens the reliability of program delivery. While

some Midwestern institutions have been able to renovate their 25 to 50 year old space, others have had to watch their facilities age

without significant renovation and are now crossing over into the over 50 year old category, significantly compounding the challenge

of finding money to address the preponderance of needs coming due.

10-25

25-50

Focus on PM:

Significant need for PM in

young systems.

Low Risk:

“Honeymoon” period –

little need for capital

reinvestment.

Medium Risk:

Lower cost space

renewal updates needed.

Higher Risk:

Life Cycles coming due in

core building

components.

React as Needed:

Issues in components

past the end of their

lifecycles will demand

reactive maintenance.

Highest Risk:

Life cycles of major components past due –end of building life cycle

approaching.

Operational

Demands:Capital Risk:

Under

10

Over

50

Balance PM and Reactive

Maintenance:

Younger components still

require PM.

Aging components require

reactive maintenance.

0%

2%

4%

6%

8%

10%

12%

14%

16%

Space Growth Enrollment Growth

Declining Enrollment Adds to Challenge of Managing Density

3

In addition to older space, Midwestern institutions are dealing with flat enrollment rates while experiencing some of the highest

percentage increases in space since 2008. To the point where the increase in space is practically double the increase in

enrollment. As a result, Midwestern campuses are experiencing steady declines in student density (22% decrease since

2008), which raises questions about how space will be managed with fewer students. With future enrollment projections

difficult to determine, managing campus density will be a critical strategy in the future as rightsizing decisions may become a

reality.

Central Eastern Midwest Rocky Mountain Southern Pacific Coast

Capital Funding Slow to Recover; Hitting Highs in 2013

4

0.00

1.00

2.00

3.00

4.00

5.00

6.00

2008 2009 2010 2011 2012 2013 2014 2015

Annual Capital One-Time Capital

$/G

SF

Midwestern institutions took a sizable cut in capital funding in 2010 and it took until 2013 for these institutions to make

a full recovery. While facing several years of stagnant investment levels, Midwestern institutions realized that they had

to reexamine their funding strategies. Although total capital spending was slow to recover, annual capital spending has

been on the rise since 2011 as campuses have begun to look at institutional sources of funding more seriously in

recent years. This funding type enables leaders to be proactive about pending critical needs and flexibly apply

appropriations to preserve physical assets. This becomes increasingly important when institutions are unable to rely

on large one-time infusions of capital to address major needs.

Mix of Capital Spending on the Right Track

5

42% 39% 38% 38% 38% 37%41% 38%

40%43%

49% 48% 46% 46% 41% 44%

18% 18%13% 14% 16% 17% 18% 18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014 2015

Space Renewal & Safety Code Envelope & Building Systems Infrastructure

In addition to total spending and funding sources, project selection must also be taken into account to fully understand the

impact of historical investment patterns. To counteract the limited capital dollars available, Midwestern institutions have

recently made strong efforts to invest a greater portion of their capital into high priority project needs that affect building

reliability (envelope and mechanical systems) rather than space upgrades. Sightlines has found that space renewal

projects last about 12 years while envelope and buildings systems investment last 30 years or more. So, while

funding remains limited, the shift of that funding to more durable, high ROI investments is an important strategy.

Facilities Operating Budgets Slowly Rising

6

3.53 3.64 3.58 3.53 3.56 3.65 3.67 3.7

0.25 0.27 0.27 0.28 0.30 0.32 0.31 0.34

0.00

1.00

2.00

3.00

4.00

5.00

2008 2009 2010 2011 2012 2013 2014 2015

Daily Service Planned Maintenance

Facilities operating budgets are starting to grow at Midwestern institutions, but at very modest rates. When

compared to steady state adjusted levels, campuses are funding their facilities operations approx. 13% less than

the rate of inflation. This is forcing campuses to try to do more with less.

$/G

SF

3.5

3.6

3.7

3.8

3.9

4

4.1

4.2

0

20,000

40,000

60,000

80,000

100,000

120,000

To

tal G

SF

/FT

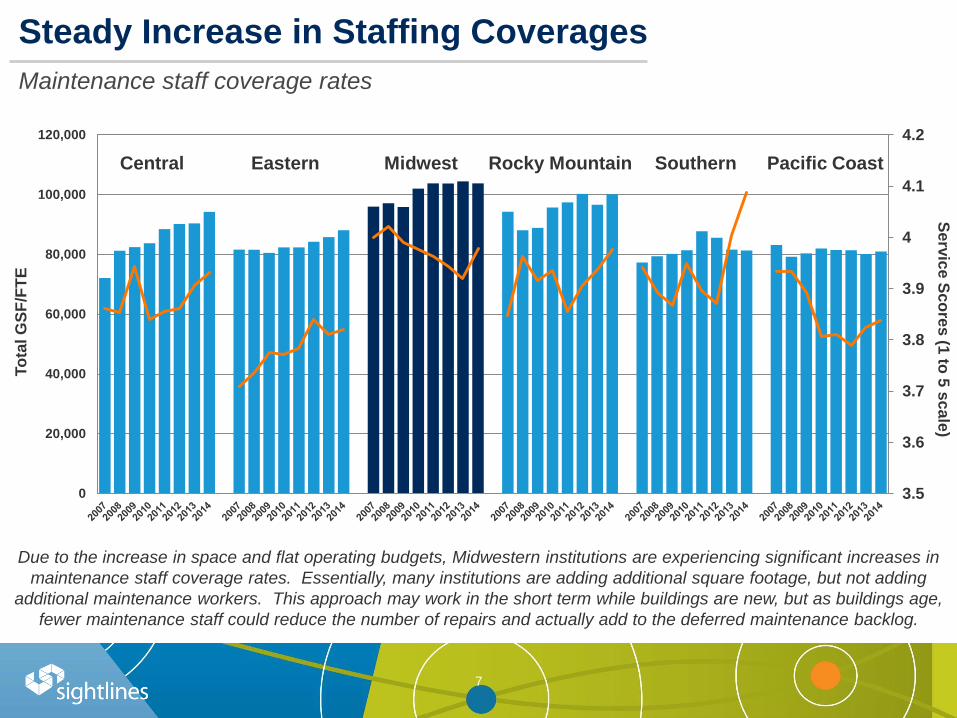

ESteady Increase in Staffing Coverages

Maintenance staff coverage rates

7

Central Eastern Midwest Rocky Mountain Southern Pacific Coast

Due to the increase in space and flat operating budgets, Midwestern institutions are experiencing significant increases in

maintenance staff coverage rates. Essentially, many institutions are adding additional square footage, but not adding

additional maintenance workers. This approach may work in the short term while buildings are new, but as buildings age,

fewer maintenance staff could reduce the number of repairs and actually add to the deferred maintenance backlog.

Se

rvic

e S

co

res

(1 to

5 s

ca

le)

Facilities Asset Reinvestment Needs Continue to Grow

8

60

65

70

75

80

85

90

95

100

2008 2009 2010 2011 2012 2013 2014 2015

While funding shifts to more durable, high ROI investments have helped to mitigate some risk, overall funding

reductions have caused facilities backlogs to increase by almost 21% since 2008. Finance and Facilities leaders

at Midwestern institutions will need to look into implementing strategies that make the problem smaller and more

manageable, which will help build confidence among decision makers and lead to a greater commitment of capital

and operational resources for facilities.

$/G

SF

9

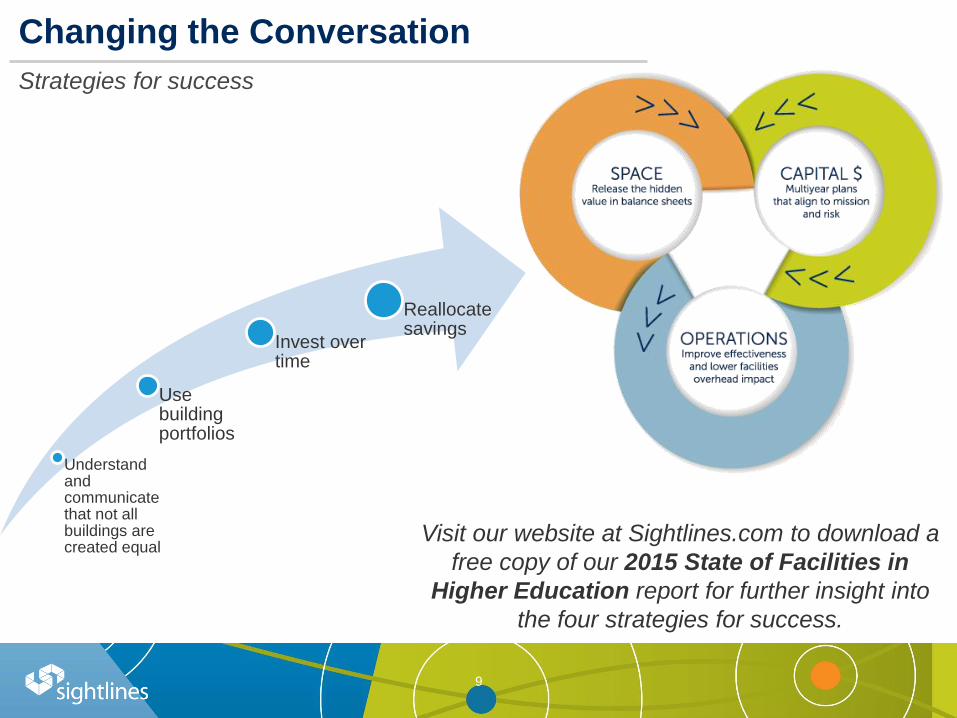

Changing the Conversation

Strategies for success

Understand and communicate that not all buildings are created equal

Use building portfolios

Invest over time

Reallocate savings

Visit our website at Sightlines.com to download a

free copy of our 2015 State of Facilities in

Higher Education report for further insight into

the four strategies for success.

About Sightlines

10

What Does Sightlines Do?

We Connect the Boiler Room

to the Boardroom.

Who Partners with Sightlines?

Robust membership includes colleges, universities, consortiums, and state systems

12

* U.S. News 2016 Rankings

Sightlines is proud to

announce that:

• 450 colleges and

universities are

Sightlines clients

including over 350

ROPA members.

• Consistently over 90%

member retention rate

• We have clients in

over 40 states, the

District of Columbia

and five Canadian

provinces

• More than 125 new

institutions became

Sightlines members

since 2013

Sightlines advises state

systems in:

• Alaska

• California

• Florida

• Hawaii

• Maine

• Massachusetts

• Minnesota

• Mississippi

• Missouri

• Nebraska

• New Hampshire

• New Jersey

• Pennsylvania

• Texas

Serving the Nation’s Leading Institutions:

• 70% of the Top 20 Colleges*

• 75% of the Top 20 Universities*

• 34 Flagship State Universities

• 14 of the 14 Big 10 Institutions

• 12 of the 14 SEC Institutions

• 9 of the 12 Ivy Plus Institutions

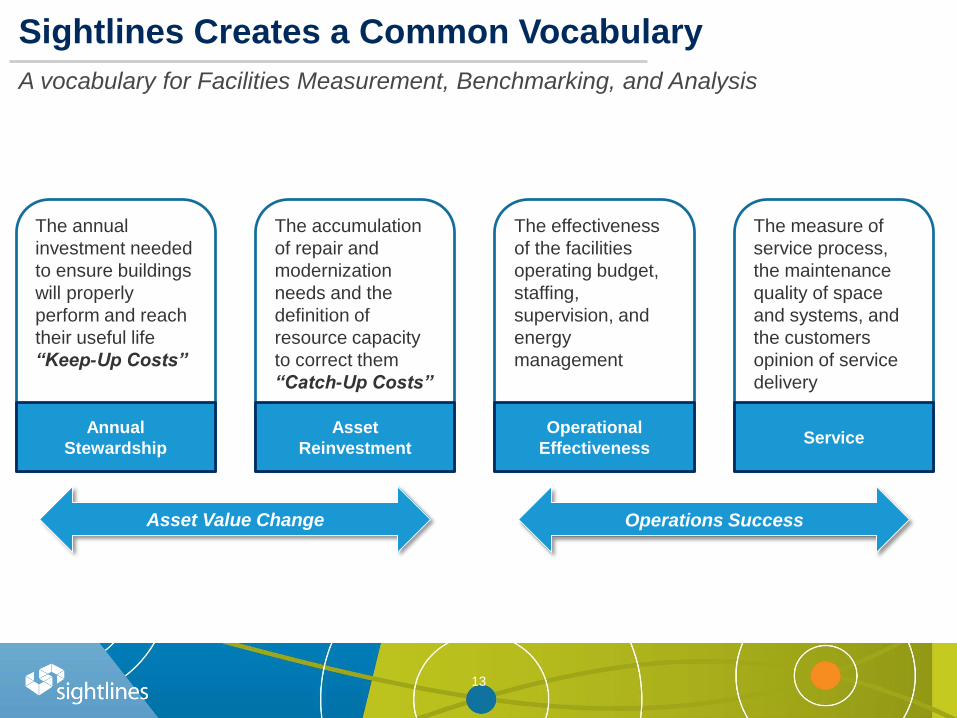

Sightlines Creates a Common Vocabulary

A vocabulary for Facilities Measurement, Benchmarking, and Analysis

13

Asset Value Change

The annual

investment needed

to ensure buildings

will properly

perform and reach

their useful life

“Keep-Up Costs”

Annual

Stewardship

The accumulation

of repair and

modernization

needs and the

definition of

resource capacity

to correct them

“Catch-Up Costs”

Asset

Reinvestment

The effectiveness

of the facilities

operating budget,

staffing,

supervision, and

energy

management

Operational

Effectiveness

The measure of

service process,

the maintenance

quality of space

and systems, and

the customers

opinion of service

delivery

Service

Operations Success

Sightlines Drives a New Conversation

Facilities intelligence toolkit that connects the dots between space, capital, and operating policies

14

A new conversation around facilities management…

• Treats physical plant like a core business

• Uses concepts of endowment management to contextualize investment decisions;

• Aligns facilities operations and capital investment with institutional mission and finance;

• Uses predictive analysis to focus on outcomes and not inputs.

• Lets you tell your “facilities story” as effective as possible.

Three Phases for Continuous Improvement

15

ROPA+ model

16

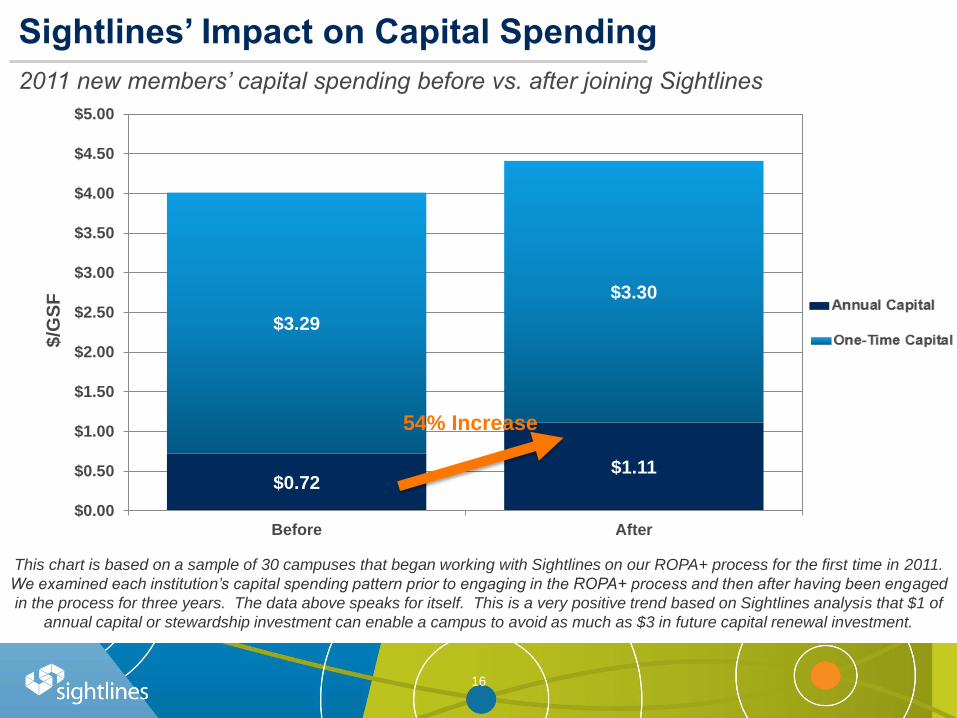

Sightlines’ Impact on Capital Spending

2011 new members’ capital spending before vs. after joining Sightlines

$0.72$1.11

$3.29

$3.30

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

Before After

$/G

SF

54% Increase

This chart is based on a sample of 30 campuses that began working with Sightlines on our ROPA+ process for the first time in 2011.

We examined each institution’s capital spending pattern prior to engaging in the ROPA+ process and then after having been engaged

in the process for three years. The data above speaks for itself. This is a very positive trend based on Sightlines analysis that $1 of

annual capital or stewardship investment can enable a campus to avoid as much as $3 in future capital renewal investment.

Connect with Sightlines

Get in touch with us to start a new facilities conversation on campus

17

We’re eager to discuss your needs and answer any questions you may have

about our Facilities Intelligence Solutions or these latest trends.

Call us at

(203) 682-4950

Email us at

Website:

www.sightlines.com/

contact-us