The Solar Finance Revolution - WordPress.com

31

The Solar Finance Revolution: Beyond Tax Equity Travis Bradford President, Prometheus Institute

Transcript of The Solar Finance Revolution - WordPress.com

The Solar Finance Revolution: Beyond Tax Equity

Travis Bradford President, Prometheus Institute

The Opportunity…

Page 3

Issues in Innovating Energy Finance ! Which Technology?

! PV, Solar Thermal, Geothermal, Wind (even Efficiency?)

! Which size of installation? ! Distributed Residential and Commercial vs. Utility Scale

! Who is the ultimate customer? ! Utility (FiT, PPA, or RAM), Integrator, Distributed Customer ! Think about who provides revenue certainty

! Who provides capital? ! Corporations vs. individual investors

! Available incentives? ! Federal, State, Local, Utility ! Rebate, Tax Credits, Accelerated Depreciation

Conclusion: Start with distributed PV systems that offer the least risk and highest volume to build pools

Page 4

Substantial Portion of Sector Capital

4

Small distributed systems 1/3 of total project finance and growing rapidly

Strong deployment growth worldwide

! Distributed systems most diffuse, heterogeneous buyers ! US market driven by unique tax benefit elements

Page 5

Page 6

Falling System Prices drive demand

PV Installation Volumes Rising

! Tens of billions of dollars per year need to be allocated to solar installations across

! Represents hundreds of thousands of annual systems, thousands of commercial installations, and hundreds of utility scale systems.

Page 8

2015 with 1% annual rate hike ! Includes:

! ITC only ! Falling

system prices

! Two-thirds of market below grid parity

! 99% within 5 cents/ kWh

The Problem… [a.k.a. financing]

Page 10

Modeling inputs for fun and profit

Financial Costs drive LCOE

! Two-thirds of payments go for financial capital ! Only one-third is for physical capital

Page 11

Page 12

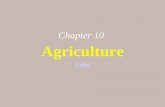

“Traditional” PV Project Finance

Page 13

! ITC and MACRS monetization are valuable benefits ! Since 2009, Section 1603 “Cash Grant” has allowed for

financial innovation to fall asleep at the switch

Current PPA Model driven by ITC

13

Tax Incentives Distort Financial Structures

Tax incentives can lead to complicated financial structures

Senior Lender

Tax Investor (99% of equity)

Developer (1% of equity)

Project Company (equity + PPA/cash debt)

Power (and REC) Sales

Cash Revenue ITC/Cash Grant

less Operating Expenses

less Debt Service

less Tax-Deductible Expenses

(including MACRS and interest on debt)

equals Taxable Losses/Income

(which result in Tax Benefits/Liabilities)

equals Distributable Cash

99% / 100% à

99% / 10% à ß 1% / 90%

ß 1% / 90% 99% / 10% à

ß 1% / 0%

Federal Incentive

Leveraged Partnership Flip Structure

Figure: NREL

WACC is high ! Equity

! 50% or more of the capital structure

! Introduces multiple counterparties

! Bottleneck drives rising rent allocation

! Debt ! Term gated by equity ! Very skeptical of tax

benefits and associated risks

! Hates multiple counterparties

! Needs scale to drive down costs

Page 16

.. If tax equity is even available

Page 16

What would a solution look like…

Page 18

Elements of Finance Solution 1. Mechanism for dealing with

tax incentives 2. Manage performance and

financial risks 3. Simplify transactions for

large aggregate volume 4. Access pools of capital with

correct risk/return profile and holding period

5. Create institutional structures to support dis-intermediation

Page 18

Page 19

1. Managing Tax Equity Bottleneck ! Master Limited Partnerships

! Requires Legislative Change

! Passive Tax Rules Change ! Requires Tax Code Overhaul

! Real Estate Investment Trust ! May be possible withExecutive Order

! Selling off Tax Equity Benefits ! Some analogs exist, rules unclear

! Self-liquidation ! Foregoing Tax Benefits

Access more pools of Tax Equity, but leave structure largely intact

Eliminate Third-Party Tax Equity within transaction

Page 20

2. Risk Characteristics to address ! Physical Performance

! Construction ! Maintenance ! Manufacturers Warranty

! Financial Performance ! Revenue Risk ! Off-taker Creditworthiness ! Lifetime Costs ! Policy Support (SRECs, etc.)

! Collateral Value ! Issues in collection ! Terminal Value

Page 21

Covering Transaction Risks

! Insuring Module Performance

! Insuring O&M Risks ! Off-taker Credit

Enhancements ! Establishing Secondary

Markets ! For Electricity Sales ! For Equipment

Page 22

3. Reducing Transaction Costs ! Sponsored Programs

! PACE Financing ! Warehousing ! Tradable Exchanges ! On-Bill Finance

! Securitization ! Pooling Requirements ! Pooling Classifications ! Strips

Page 23

Develop necessary program elements

! Each of these have analogs in existing securitization markets for mortgages and credit cards

Page 24

Securitization is well-trodden path

Page 25

4. Large Pools of Capital Available

Requirements of Available Capital

! Increase Term Duration (match asset life) ! Decrease WACC (simple, easy, repeatable) ! Improve Gearing Ratio (more in line with

mortgage structure)

Page 27

5. Institutional Structures Needed ! Standard Documentation –

Warehouser or Intermediary ! Loan Documentation ! O&M Agreements ! Etc.

! Quality Standards for Installations – ???

! Rating methodologies – Credit Agencies

! Legal and Tax Guidelines – FASB

Next Steps…

Page 29

Picking the correct order 1. First priority is determine the best “end game” for

securitization and larger pools of capital 2. Work backward to figure out structuring elements to allow

scale and standardization 3. Probably requires standardized method of tax equity

treatment for aggregation ! Most likely removing the tax credit from the transaction or baking it

into the transaction is the only standardized way of handling it, absent legislative rule changes

! Re-emergence of 1603 tax grant will disrupt the innovation cycle

! Creator of next-gen distributed solar finance will enable hundreds of billions of dollars of capital to flow into the industry on commercial mortgage terms

Questions?

Page 31

Loan Guarantee targets Asset Finance