The Six Major Puzzles in International Macroeconomics: Is ...sewonhur/teaching/lecture1.pdf · The...

33

Transcript of The Six Major Puzzles in International Macroeconomics: Is ...sewonhur/teaching/lecture1.pdf · The...

The Six Major Puzzles in International

Macroeconomics: Is There a Common Cause?

Maurice Obstfeld and Kenneth Rogo�

International Finance

International Finance (Sewon Hur) Lecture 1 0 / 32

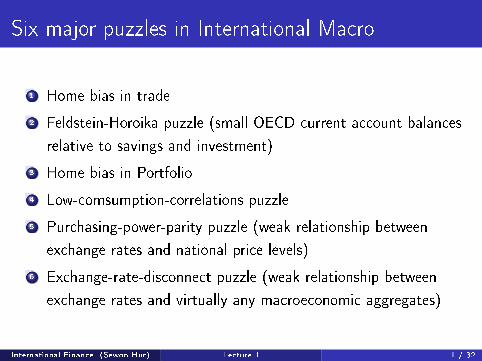

Six major puzzles in International Macro

1 Home bias in trade

2 Feldstein-Horoika puzzle (small OECD current account balances

relative to savings and investment)

3 Home bias in Portfolio

4 Low-comsumption-correlations puzzle

5 Purchasing-power-parity puzzle (weak relationship between

exchange rates and national price levels)

6 Exchange-rate-disconnect puzzle (weak relationship between

exchange rates and virtually any macroeconomic aggregates)

International Finance (Sewon Hur) Lecture 1 1 / 32

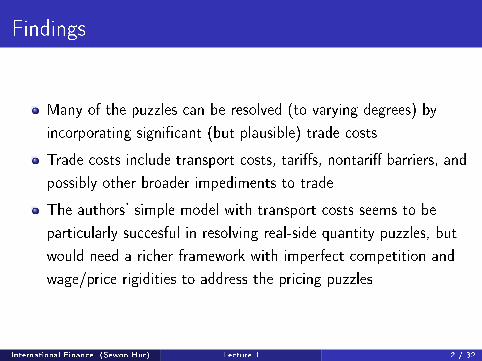

Findings

Many of the puzzles can be resolved (to varying degrees) by

incorporating signi�cant (but plausible) trade costs

Trade costs include transport costs, tari�s, nontari� barriers, and

possibly other broader impediments to trade

The authors' simple model with transport costs seems to be

particularly succesful in resolving real-side quantity puzzles, but

would need a richer framework with imperfect competition and

wage/price rigidities to address the pricing puzzles

International Finance (Sewon Hur) Lecture 1 2 / 32

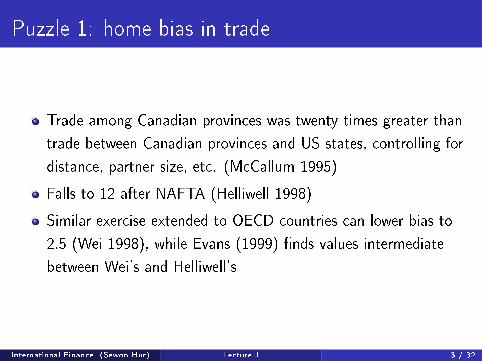

Puzzle 1: home bias in trade

Trade among Canadian provinces was twenty times greater than

trade between Canadian provinces and US states, controlling for

distance, partner size, etc. (McCallum 1995)

Falls to 12 after NAFTA (Helliwell 1998)

Similar exercise extended to OECD countries can lower bias to

2.5 (Wei 1998), while Evans (1999) �nds values intermediate

between Wei's and Helliwell's

International Finance (Sewon Hur) Lecture 1 3 / 32

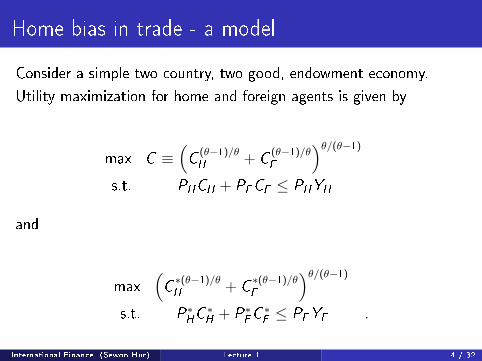

Home bias in trade - a model

Consider a simple two country, two good, endowment economy.

Utility maximization for home and foreign agents is given by

max C ≡(C

(θ−1)/θH

+ C(θ−1)/θF

)θ/(θ−1)

s.t. PHCH + PFCF ≤ PHYH

and

max(C

∗(θ−1)/θH

+ C∗(θ−1)/θF

)θ/(θ−1)

s.t. P∗HC ∗H+ P∗

FC ∗F≤ PFYF .

International Finance (Sewon Hur) Lecture 1 4 / 32

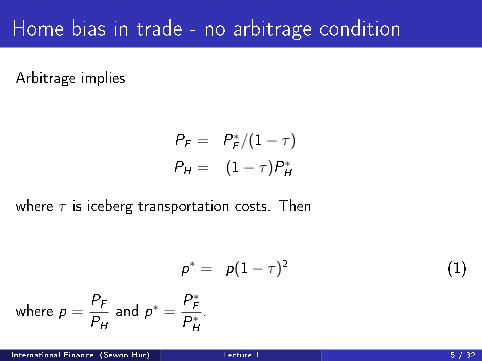

Home bias in trade - no arbitrage condition

Arbitrage implies

PF = P∗F/(1− τ)

PH = (1− τ)P∗H

where τ is iceberg transportation costs. Then

p∗ = p(1− τ)2 (1)

where p =PF

PH

and p∗ =P∗F

P∗H

.

International Finance (Sewon Hur) Lecture 1 5 / 32

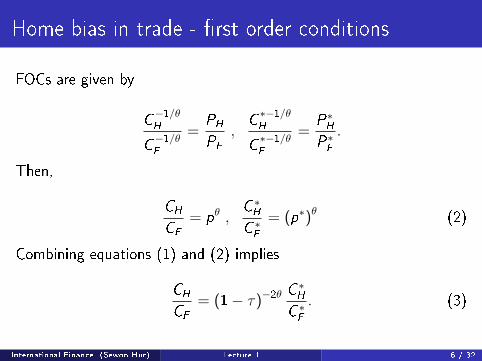

Home bias in trade - �rst order conditions

FOCs are given by

C−1/θH

C−1/θF

=PH

PF

,C

∗−1/θH

C∗−1/θF

=P∗H

P∗F

.

Then,

CH

CF

= pθ ,C ∗H

C ∗F

= (p∗)θ (2)

Combining equations (1) and (2) implies

CH

CF

= (1− τ)−2θ C∗H

C ∗F

. (3)

International Finance (Sewon Hur) Lecture 1 6 / 32

Home bias in trade

Consider the symmetric case where YH = YF . Then,CH

CF

=C ∗F

C ∗H

.

Then equation (3) reduces to

CH

CF

=C ∗F

C ∗H

= (1− τ)−θ = pθ.

Then

PHCH

PFCF

=CH

pCF

= pθ−1 = (1− τ)1−θ

and

P∗FC ∗F

P∗HC ∗H

=p∗C ∗

F

C ∗H

= pθp∗ = pθ+1(1− τ)2 = (1− τ)1−θ .

International Finance (Sewon Hur) Lecture 1 7 / 32

Home bias in trade - numerical results

If τ = 0, thenCH

pCF

= 1.

If τ = 0.25 and θ = 6, thenCH

pCF

= 4.2.

International Finance (Sewon Hur) Lecture 1 8 / 32

Home bias in trade - preferences

Now consider home bias ω < 1 in preferences

U ≡(C

(θ−1)/θH

+ ωC(θ−1)/θF

)θ/(θ−1)

and

U ≡(ωC

∗(θ−1)/θH

+ C∗(θ−1)/θF

)θ/(θ−1)

Example

Show that the e�ects of home bias in preferences (ω < 1) can be

isomorphic to the e�ects of trade costs τ .

International Finance (Sewon Hur) Lecture 1 9 / 32

Puzzle 2: Feldstein-Horoika puzzle

Theory:

savings �ow to countries with the most productive investment

opportunities

domestic saving rates would be uncorrelated with domestic

investment rates

Feldstein and Horoika (1980) documented that national savings

rates are highly correlated with domestic investment rates (long

period averages)

International Finance (Sewon Hur) Lecture 1 10 / 32

Puzzle 2: Feldstein-Horoika puzzle

Feldstein and Horoika regressions:����� �

&��������'����(� ,����������� .//CP.//G@

�

�� �� �

#$

�� %

8�� �� %����.� � � 52

: ���������K 4A C�.4 C�5. C�11�C�C;� �C�C0�

$�������� ���� E<?7��� � .CCC 50 C�.1 C�50 C�1/�C�C;� �C�C/�

$�������� ���� E<?7��� � ;CCC 5. C�CG C�GC C�A;�C�C;� �C�C/�

"#$% ���������S ;5 C�C0 C�AC C�A0�C�C;� �C�C/�

@"D3 ������������ 3������� ������ �� ������������K����� �� ������� ��� � ����������� �� ���� ����� �� ����� �� ����� ��

��� ����� �� ���� �4A� 50� 5.�� ��� �������� �� � ��� �C�1/� C�54� C�A1��S�� ��� ���� N���� �� ��� "#$% ����� ��� ������� ��� � ����� �� C�GA�

N���� �� ������� �� ��� ����� ������

4A

International Finance (Sewon Hur) Lecture 1 11 / 32

Feldstein-Horoika puzzle - a model

Consider a two-period, two-good, small-country endowment model.

The utility function of a representative home resident is

u(C1) + δu(C2)

where

C ≡(C

(θ−1)/θH

+ C(θ−1)/θF

)θ/(θ−1)

.

International Finance (Sewon Hur) Lecture 1 12 / 32

Feldstein-Horoika puzzle - budget constraints

The small country is endowed with YH,1 in period 1, and YH,2 in

period 2. It takes as given world prices P∗H, P∗

F, r ∗. The �rst and

second period budget constraints are given by

PH,1CH,1 + PF ,1CF ,1 ≤ PH,1YH,1 + D

PH,2CH,2 + PF ,2CF ,2 ≤ PH,2YH,2 − (1+ r ∗) D

International Finance (Sewon Hur) Lecture 1 13 / 32

Feldstein-Horoika puzzle - �rst order conditions

FOCs are given by

(CH,1)−1/θ

C 1/θ = PH,1λ1 (4)

(CF ,1)−1/θ

C 1/θ = PF ,1λ1 (5)

International Finance (Sewon Hur) Lecture 1 14 / 32

Feldstein-Horoika puzzle

Combine equations (4) and (5),

(C

(θ−1)/θH,1 + C

(θ−1)/θF ,1

)C (1−θ)/θ =

(P1−θH,1 + P1−θ

F ,1

)λ1−θ1(

C(θ−1)/θH,1 + C

(θ−1)/θF ,1

)θ/(θ−1)

C−1 =(P1−θH,1 + P1−θ

F ,1

)θ/(θ−1)λ−θ1

λ1 = P−1

1

where

P1 =(P1−θH,1 + P1−θ

F ,1

)1/(1−θ)(6)

International Finance (Sewon Hur) Lecture 1 15 / 32

Feldstein-Horoika puzzle

Therefore the consumption of home and foreign goods are

CH,t =

(PH,t

Pt

)−θ

Ct , CF ,t =

(PF ,t

Pt

)−θ

Ct t = 1, 2 (7)

The �rst period budget constraint can be written as

PH,1CH,1 + PF ,1CF ,1 = P1−θH,1 P

θ1C1 + P1−θ

F ,1 Pθ1C1

=(P1−θH,1 + P1−θ

F ,1

)Pθ

1C1

= P1C1

≤ PH,1YH,1 + D

International Finance (Sewon Hur) Lecture 1 16 / 32

Feldstein-Horoika puzzle

Similarly, the second period budget constraint is

P2C2 ≤ PH,2YH,2 − (1+ r ∗)D

Combining the budget constraints,

P1C1 +P2C2

1+ r ∗= PH,1YH,1 +

PH,2YH,2

1+ r ∗.

International Finance (Sewon Hur) Lecture 1 17 / 32

Feldstein-Horoika puzzle

Let the domestic real interest rate be de�ned as

1+ r = (1+ r ∗)P1/P2, (8)

Then the consolidated intertemporal budget constraint is

C1 +C2

1+ r=

PH,1

P1

YH,1 +PH,2

P2

YH,2

1+ r.

Given P1 and P2, equation (8) determines the real interest rate faced

by domestic agent.

International Finance (Sewon Hur) Lecture 1 18 / 32

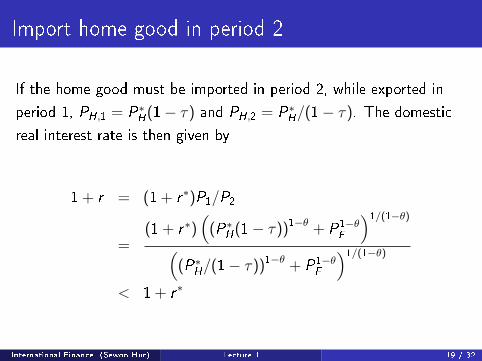

Import home good in period 2

If the home good must be imported in period 2, while exported in

period 1, PH,1 = P∗H(1− τ) and PH,2 = P∗

H/(1− τ). The domestic

real interest rate is then given by

1+ r = (1+ r ∗)P1/P2

=(1+ r ∗)

((P∗

H(1− τ))1−θ + P1−θ

F

)1/(1−θ)

((P∗

H/(1− τ))1−θ + P1−θ

F

)1/(1−θ)

< 1+ r ∗

International Finance (Sewon Hur) Lecture 1 19 / 32

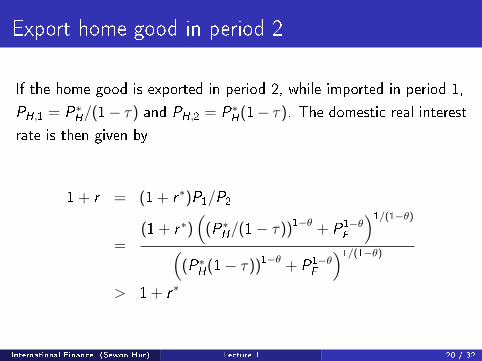

Export home good in period 2

If the home good is exported in period 2, while imported in period 1,

PH,1 = P∗H/(1− τ) and PH,2 = P∗

H(1− τ). The domestic real interest

rate is then given by

1+ r = (1+ r ∗)P1/P2

=(1+ r ∗)

((P∗

H/(1− τ))1−θ + P1−θ

F

)1/(1−θ)

((P∗

H(1− τ))1−θ + P1−θ

F

)1/(1−θ)

> 1+ r ∗

International Finance (Sewon Hur) Lecture 1 20 / 32

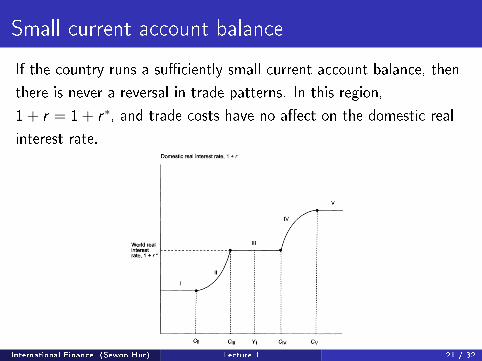

Small current account balance

If the country runs a su�ciently small current account balance, then

there is never a reversal in trade patterns. In this region,

1+ r = 1+ r ∗, and trade costs have no a�ect on the domestic real

interest rate.

354 * OBSTFELD & ROGOFF

Figure 1 DOMESTIC SPENDING AND THE DOMESTIC REAL INTEREST RATE IN A TWO-GOOD MODEL WITH TRADE COSTS

Domestic real interest rate, 1 + r

V

World real l / interest -------- -- rate, 1 + r

First-period total real spending, Cl

CH,2 > YH,2 Since in period 2 the home good must be imported, while in

period 1 it is exported, we have

(1 + r*) (P,-19 + P- 9)11(1-9) 1 +

H F (Pk2 ? P:/9)

(1 + r*) {[PH(1 - 7)11-0 + Pl-}1/(1- ) F= < 1 + r*

{[P/(1 -

T)]1- + p/-F 1/-(0)

in segment I. If the country contemplates being a big lender, it will face an effective real interest rate significantly below the world real interest rate.

Segment II starts when period 1 consumption first reaches the level Cln such that CH,2 = YH,2- In this region, PH,2 is determined by equation (8) and the first relation in equation (9), with CH,2

= YH,2 (so there is no round-

International Finance (Sewon Hur) Lecture 1 21 / 32

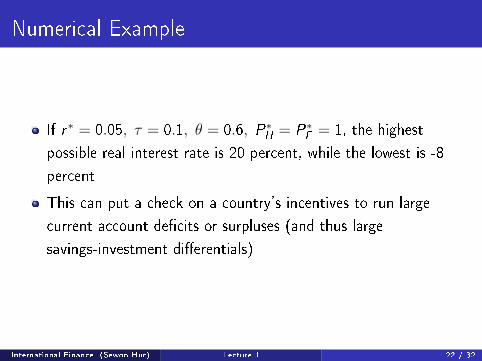

Numerical Example

If r ∗ = 0.05, τ = 0.1, θ = 0.6, P∗H= P∗

F= 1, the highest

possible real interest rate is 20 percent, while the lowest is -8

percent

This can put a check on a country's incentives to run large

current account de�cits or surpluses (and thus large

savings-investment di�erentials)

International Finance (Sewon Hur) Lecture 1 22 / 32

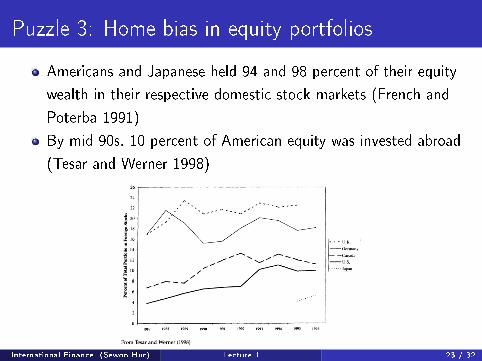

Puzzle 3: Home bias in equity portfolios

Americans and Japanese held 94 and 98 percent of their equity

wealth in their respective domestic stock markets (French and

Poterba 1991)

By mid 90s, 10 percent of American equity was invested abroad

(Tesar and Werner 1998)360 * OBSTFELD & ROGOFF

Figure 2 HOME BIAS IN EQUITY PORTFOLIOS: 1987-1996

26

24

22 , ,

. 16 |;~~~~~~~ 16 -\-----

- l- - - I. K

.S 14 (-Germany

| f10 2^^ y^^"^^"*- - " -Canada

l 12

l f ~----- Japan

X l.

4

1987 1988 1989 990 1991 2 13 1994 15 1996 1987 1988 1989 1990 1991 1992 1993 1994 1995 1996

From Tesar and Werner (1998)

Potential explanations range from nontraded factors such as human

capital (which may worsen or reduce the puzzle; see Baxter and Jermann, 1997) to nontraded consumption goods to asymmetries of information to data inadequacy. Yet it is fair to say that none of the available stories alone has provided a quantitatively satisfactory account of the observed home bias; see Lewis (1999) for an up-to-date and thorough survey.

To set the stage for our discussion of trade costs, it is worthwhile

briefly reviewing what is perhaps the leading explanation, which is based on the classic Salter-Swan traded-nontraded-goods dichotomy we have already mentioned. While these two types of goods lie at polar extremes in terms of their tradability, equity claims on either type of

industry can be frictionlessly traded. Thus, even though cement is

prohibitively costly to transport, there is nothing to stop foreign inves- tors from buying shares in the domestic cement industry. Earnings, of course, must be redeemed in traded goods, since nontradables cannot be shipped to foreign equity holders by assumption. The key result one

gets out of this framework is that, for the baseline case of separable

to 7%. The positive target position in foreign equities, meant to "reduce risk and broaden portfolio diversification while maintaining or improving investment perfor- mance," represents a substantial advance. It still falls far short, however, of the optimal foreign equity share that simple models of international diversification would predict.

International Finance (Sewon Hur) Lecture 1 23 / 32

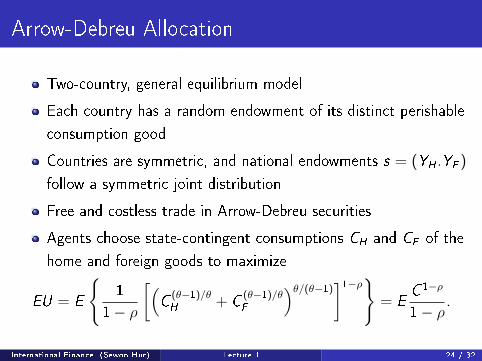

Arrow-Debreu Allocation

Two-country, general equilibrium model

Each country has a random endowment of its distinct perishable

consumption good

Countries are symmetric, and national endowments s = (YH .YF )

follow a symmetric joint distribution

Free and costless trade in Arrow-Debreu securities

Agents choose state-contingent consumptions CH and CF of the

home and foreign goods to maximize

EU = E

{1

1− ρ

[(C

(θ−1)/θH

+ C(θ−1)/θF

)θ/(θ−1)]1−ρ}

= EC 1−ρ

1− ρ.

International Finance (Sewon Hur) Lecture 1 24 / 32

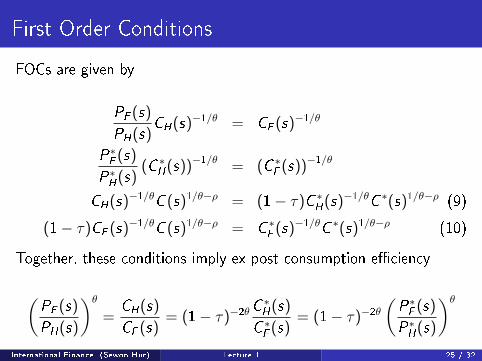

First Order Conditions

FOCs are given by

PF (s)

PH(s)CH(s)

−1/θ = CF (s)−1/θ

P∗F(s)

P∗H(s)

(C ∗H(s))−1/θ = (C ∗

F(s))−1/θ

CH(s)−1/θC (s)1/θ−ρ = (1− τ)C ∗

H(s)−1/θC ∗(s)1/θ−ρ (9)

(1− τ)CF (s)−1/θC (s)1/θ−ρ = C ∗

F(s)−1/θC ∗(s)1/θ−ρ (10)

Together, these conditions imply ex post consumption e�ciency

(PF (s)

PH(s)

)θ=

CH(s)

CF (s)= (1− τ)−2θC

∗H(s)

C ∗F(s)

= (1− τ)−2θ

(P∗F(s)

P∗H(s)

)θInternational Finance (Sewon Hur) Lecture 1 25 / 32

Arrow-Debreu Allocation

The model is closed by the output-market clearing conditions:

C ∗H(s) = (1− τ) (YH(s)− CH(s)) (11)

CF (s) = (1− τ) (YF (s)− C ∗F(s)) (12)

We have four equations, (9)-(12), and four unknowns,

CH ,CF ,C∗H,C ∗

Ffor every state s.

International Finance (Sewon Hur) Lecture 1 26 / 32

Arrow-Debreu Allocation

Assume that ρ = 1/θ. Then

CH(s) =1

1+ (1− τ)θ−1YH(s)

CF (s) =(1− τ)θ

1+ (1− τ)θ−1YF (s)

Equity shares are given by

XH =1

1+ (1− τ)θ−1YH

XF =(1− τ)θ−1

1+ (1− τ)θ−1YF

International Finance (Sewon Hur) Lecture 1 27 / 32

Arrow-Debreu Allocation

In the absence of trade costs, equity shares are 1/2.

For θ = 6 and τ = 0.25, then XH = 0.81

International Finance (Sewon Hur) Lecture 1 28 / 32

Equity Trade Allocation

Now consider the model without Arrow-Debreu securities, but with

trade in equity shares to each country's output.

Example

Assume that ρ = 1/θ. Show that the equity trade allocation is

identical to the Arrow-Debreu allocation.

International Finance (Sewon Hur) Lecture 1 29 / 32

Puzzle 4: Consumption correlations puzzle

Consider a one-good, two-country model with free trade and

complete markets in which all agents have an identical period

utility function:

u(C ) =C 1−ρ

1− ρ

Then home and foreign consumption growth rates are equalized:

Ct+1

Ct

=C ∗t+1

C ∗t

Empirically, consumption growth rates are much less correlated

International Finance (Sewon Hur) Lecture 1 30 / 32

Puzzle 5: Purchasing-power-parity puzzle

Let Q be the real exchange rate between two countries

Q = eP∗

P

where e is the nominal exchange rate

Consider the regression:

logQt = α + ηt + γ logQt−1 + εt

γ ranges from 0.99 (US-Canada; half-life of 69 months) to 0.97

(Germany-Japan; 21 months)

Half-lives of this magnitude are hard to understand if

�nancial-market disturbances with only transitory real e�ects are

very important in explaining short-run volatility.

International Finance (Sewon Hur) Lecture 1 31 / 32

Puzzle 6: Exchange rate disconnect puzzle

Remarkably weak short-term feedback links between exchange

rate and the rest of the economy

PPP puzzle is a special case

Similar to stock-price disconnect puzzle, but links between

exchange rate and real economy are much more direct than for

stock prices

A model with imperfect markets, trade costs, and nominal

rigidities can produce a disconnect in which the exchange rate

responds wildly to shocks

International Finance (Sewon Hur) Lecture 1 32 / 32